What Gentrification Is and Who Wins and Loses

Gentrification is the complex process by which historically disinvested neighborhoods experience an influx of capital and higher-income residents, fundamentally altering their economic and demographic fabric. While long-term property owners can build immense wealth as neighborhood property values rise, research consistently shows that low-income renters and legacy small businesses are highly vulnerable to physical, economic, and cultural displacement.

Decoding the Definition: More Than Aesthetics

When the general public thinks of gentrification, the imagery is often anecdotal: the sudden arrival of artisanal coffee shops, luxury condominiums, and affluent young professionals in a working-class neighborhood. However, urban sociologists, economists, and geographers define the phenomenon through a much more rigorous, structural lens. The term was originally coined by British sociologist Ruth Glass in 1964 to describe how working-class quarters of London were being invaded and upgraded by the middle and upper classes until the original social character of the districts was entirely transformed 12.

Today, research institutions like the Urban Displacement Project and the Brookings Institution categorize gentrification as a dual process requiring two simultaneous shifts 34. The first is an economic change, defined by the rapid deployment of real estate investment and the in-migration of households possessing significantly higher disposable incomes than the incumbent residents. The second is a demographic change, which involves shifts in educational attainment and, particularly in the context of the United States, a racial transition as higher-income white households replace lower-income minority households 34.

This demographic shift is actively underway in cities globally, driven by a growing demand for central-city living, proximity to urban economic capitals, and access to dynamic social infrastructure 567. Yet, measuring and identifying gentrification remains heavily debated in the academic literature. Different researchers utilize varying thresholds for median income changes, educational attainment increases, and housing price appreciation, meaning a neighborhood identified as gentrifying in one study might be classified as merely "revitalizing" in another 589.

The Displacement Versus Succession Debate

A central controversy in the study of urban change is the exact relationship between gentrification and displacement. In the public imagination, gentrification is synonymous with the forced eviction of the poor. However, quantitative researchers have spent decades testing this assumption, resulting in the "succession versus displacement" debate.

Several major, peer-reviewed national studies have found little to no evidence that absolute residential mobility rates are higher in gentrifying neighborhoods compared to observationally equivalent, non-gentrifying low-income neighborhoods 7812910. A landmark 2023 study analyzing over six million court eviction records across 72 of the largest United States metropolitan areas between 2000 and 2016 revealed that the vast majority of evictions took place in low-income neighborhoods that were not gentrifying 710. In fact, the data demonstrated that eviction rates actually decreased more over time in gentrifying spaces than in non-gentrifying poverty-stricken areas 710.

This data does not suggest that gentrification is harmless; rather, it highlights the severe baseline instability of poverty. Extreme housing churn, high eviction rates, and constant forced mobility are the devastating status quo in deep-poverty neighborhoods 71210. When a neighborhood gentrifies, the nature of the turnover changes. This phenomenon is known as "succession." As lower-income residents move out for routine reasons - such as a changing job, family expansion, or an eviction - they are replaced by higher-income newcomers 611.

Because the neighborhood's baseline housing costs have risen, other low-income residents can no longer afford to move into those vacated units. Researchers refer to this specific dynamic as "exclusionary displacement" 612. The absolute number of people moving out might look identical on a demographic spreadsheet, but exclusionary displacement permanently erodes the affordable housing stock, effectively building a financial wall around the community that prevents the working class from ever returning 61212.

The Three Dimensions of Displacement

When displacement is tied to gentrification, urban scholars generally categorize it into three distinct dimensions, each carrying profound consequences for the incumbent community 361112.

The first is direct, physical displacement. This occurs when long-term residents are forced out of their homes due to skyrocketing rents, non-just-cause evictions, aggressive buyouts, or the physical conversion of rental apartment buildings into luxury condominiums 4612.

The second is the aforementioned exclusionary displacement, where rising costs and discriminatory policies - such as landlords refusing to accept federal housing vouchers - prohibit new low-income households from accessing the neighborhood 612.

The third, and perhaps most insidious, is cultural or social displacement. This occurs when long-time residents manage to remain in their physical homes but experience a profound loss of community identity and meaningful social life 3111314. As the neighborhood transforms, the cultural institutions, local political representation, corner stores, and informal social networks that residents relied upon are supplanted by establishments catering to affluent newcomers 31115. Incumbent residents report feeling alienated, marginalized, and treated as outsiders in the very spaces they inhabited for decades 31113.

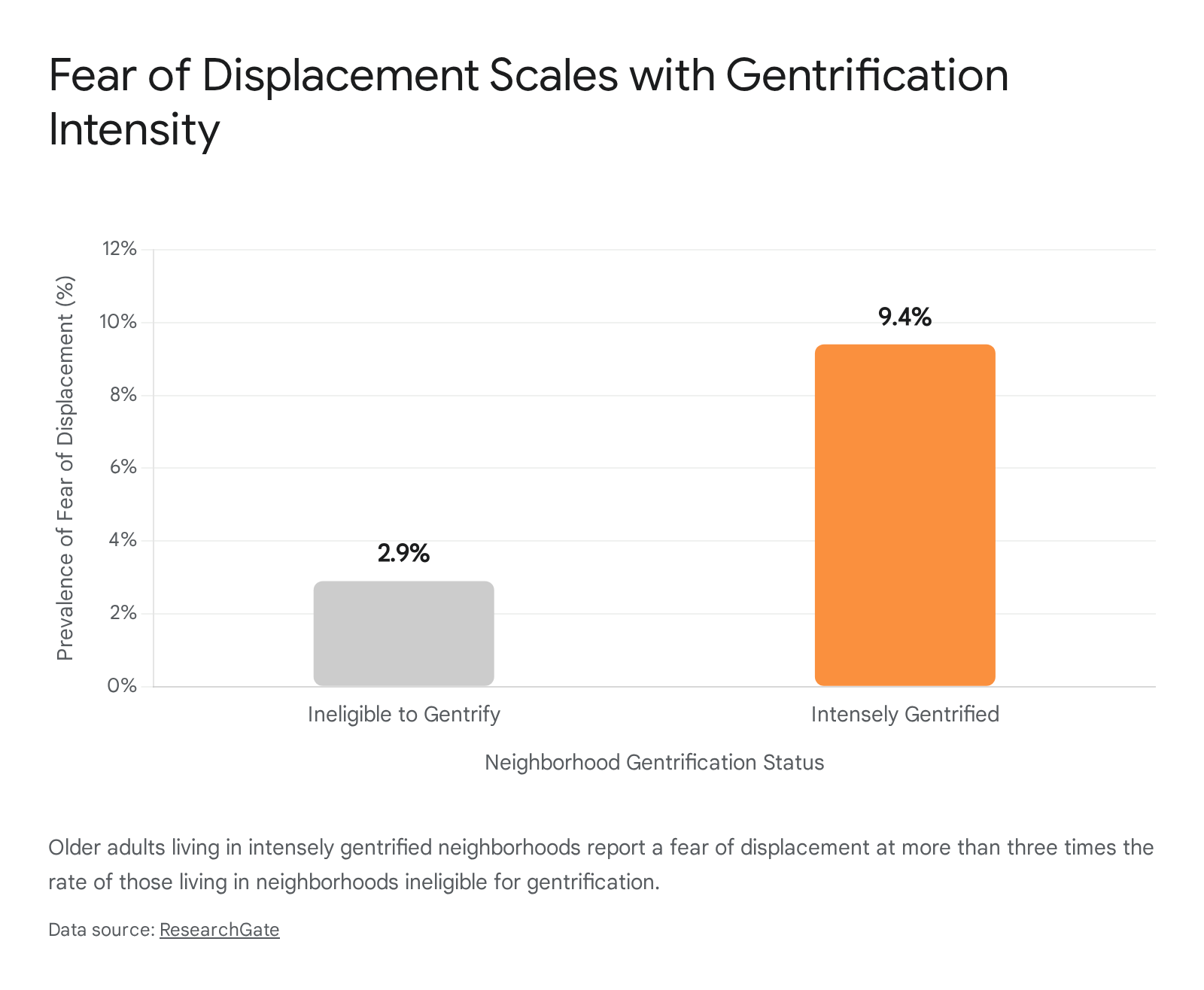

Quantitative evidence supports the reality of this psychological burden. A recent study leveraging data from the REasons for Geographic and Racial Differences in Stroke (REGARDS) project surveyed over 4,000 older Black and white United States adults. The research revealed that the prevalence of the fear of displacement was 9.4 percent among those living in intensely gentrified areas, compared to just 2.9 percent among those in areas ineligible to gentrify 1320.

This fear was particularly acute among Black participants, highlighting how gentrification systematically disrupts the social attachments and place-based identity of marginalized groups 1314.

The Economic Engines: Why Does Gentrification Happen?

To understand who ultimately benefits from gentrification, it is necessary to examine the macroeconomic engines that make neighborhood transformation possible. Neighborhoods do not gentrify by accident; they are actively shaped by capital flows, historical policy decisions, and real estate speculation.

The Rent Gap Theory

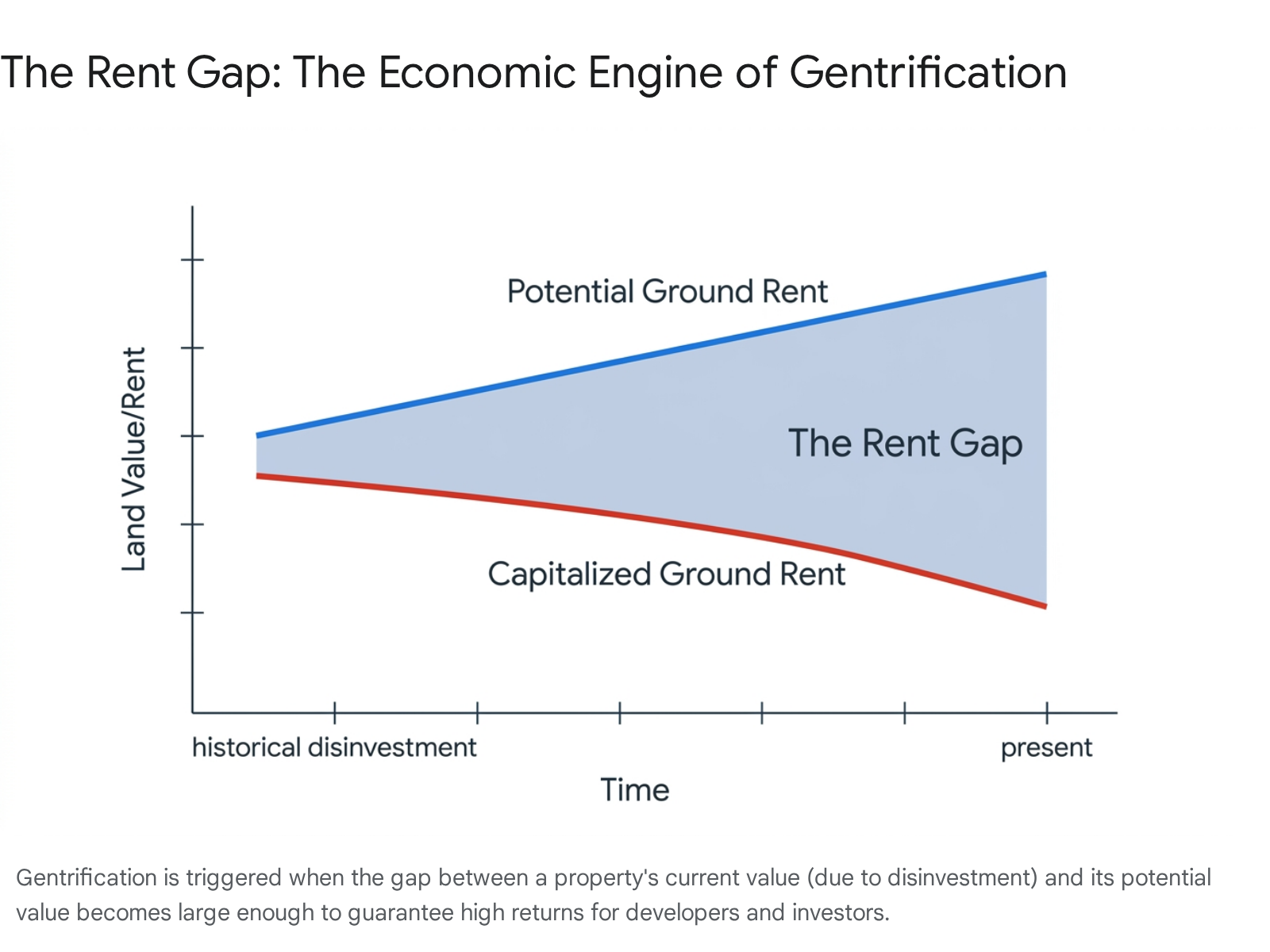

In the field of urban geography, the most prominent theoretical framework explaining the supply-side mechanics of gentrification is the "Rent Gap Theory," originally proposed by geographer Neil Smith in the late 1970s 22116. The rent gap theory conceptualizes gentrification not merely as a shift in consumer preferences, but as a structural outcome of capitalist urban development.

The "rent gap" is defined as the disparity between a property's capitalized ground rent (the actual income or value it currently generates in its dilapidated, disinvested state) and its potential ground rent (the maximum value it could command if it were rehabilitated to its "highest and best use") 2116.

When a city expands and capital looks for new avenues of accumulation, investors turn their attention to the urban core. If a neighborhood has been severely neglected by both the state and private markets for decades, property values plunge to rock bottom, opening a massive, lucrative gap between what the land is currently worth and what it could be worth 2116.

Real estate developers, speculators, and institutional investors purchase these undervalued properties cheaply, invest capital into rapid renovations, and capture the immense profit margins when the neighborhood is rebranded for middle- and upper-class consumers 2116. Under this framework, individual gentrifiers - such as artists or young professionals seeking affordable housing - are merely the initial demand-side pioneers. The true driver of widespread displacement is the systemic, supply-side flow of capital seeking maximum returns on suppressed land values 2117.

Redlining and Historical Disinvestment

The rent gap does not emerge in a vacuum; in many contexts, it was historically manufactured by discriminatory public policy. In the United States, current patterns of gentrification are heavily tied to the twentieth-century legacy of "redlining" 3.

During the 1930s, the federal government and lending institutions utilized color-coded maps to assess mortgage lending risk. Neighborhoods populated predominantly by people of color and immigrants were explicitly outlined in red and labeled as "hazardous" 3. This institutional denial of capital meant residents could not secure mortgages to buy homes or secure loans to maintain their properties.

This federally sponsored disinvestment was compounded by "white flight" to the suburbs, fueled by discriminatory mortgage programs like the GI Bill, and destructive urban renewal projects that routed massive highway systems directly through thriving minority communities 3424. These policies systematically and artificially depressed property values in the urban core. Today, these artificially cheapened neighborhoods - which boast ideal central locations near downtown jobs and transit - are ripe for real estate speculation. Research shows a direct correlation; for instance, 87 percent of San Francisco's historically redlined neighborhoods are currently classified as low-income areas undergoing gentrification 3.

The Rise of Corporate Landlords

A modern driver accelerating neighborhood transition and exacerbating the rent gap is the rise of the institutional investor. Following the 2008 global financial crisis and the resulting wave of foreclosures, private equity firms and corporate landlords began purchasing distressed single-family homes in bulk, converting them into permanent rental properties 1826.

As the market recovered, these entities evolved their strategies to include "build-to-rent" communities, commissioning entire neighborhoods specifically designed for rental income rather than homeownership 1826. While corporate landlords currently own less than 4 percent of all single-family homes nationwide, their purchasing power is highly concentrated in specific regional markets and neighborhoods 1819. Armed with vast pools of capital and the ability to make all-cash offers, these entities easily outbid prospective local homebuyers, locking working-class families out of the wealth-building mechanism of homeownership 20.

Once a substantial portfolio is acquired, corporate landlords utilize centralized management systems and algorithmic pricing models to maximize yields. Research out of the Atlanta metropolitan area indicates that a higher concentration of corporate landlords directly leads to a decrease in homeownership rates for Black residents and is correlated with disproportionate eviction filings against minority and lower-income tenants 1019. However, some market analysts argue that institutional investors are merely a symptom of a larger problem, noting that restrictive exclusionary zoning laws - which severely limit the construction of new housing supply - are the true root cause of soaring real estate prices 1819.

Winners and Losers: A Stakeholder Breakdown

Gentrification is frequently described by urban planners as a "double-edged sword" 429. The revitalization of a neighborhood brings undeniable benefits: improved municipal services, enhanced public transit infrastructure, reduced crime rates, cleaner streetscapes, and the arrival of grocery stores in former food deserts 421.

However, these benefits do not accrue evenly across the population. Because gentrification inherently shifts the class and economic demographics of a physical space, its impact depends entirely on a stakeholder's relationship to property ownership.

| Stakeholder Group | Primary Status | Key Benefits (The "Wins") | Key Risks (The "Losses") |

|---|---|---|---|

| Homeowners | Mixed / Winners | Significant property value appreciation; the ability to borrow against new home equity for renovations; enjoyment of improved local amenities 422. | Increased property tax burdens (a risk for the elderly on fixed incomes); community division; cultural alienation as long-time neighbors leave 422. |

| Renters | Losers | Access to better neighborhood services, greater income mixing, and reduced crime - but only if they manage to avoid being priced out 4. | High risk of involuntary displacement via severe rent hikes, eviction, and condo conversions; loss of community support networks; downward economic mobility 4622. |

| Small Business Owners | Mixed | Increased neighborhood foot traffic; access to a new customer base with substantially higher disposable income; potential for higher overall sales 41532. | Sharp commercial rent increases; displacement in favor of well-capitalized national chains; cultural mismatch with the changing neighborhood demographic 4153223. |

Renters: The Most Vulnerable

Renters are universally recognized in the research literature as the most vulnerable group in a gentrifying market. Because they do not own the land beneath them, they absorb all the financial shocks of neighborhood appreciation with none of the associated wealth-building benefits. Statistical analyses merging tract-level census data with longitudinal mobility records show that a renter in a gentrifying neighborhood is significantly more likely to report an involuntary move - such as an eviction or a lease non-renewal - than a renter in a non-gentrifying area 2224.

When low-income renters are physically displaced, they are rarely able to relocate to "better" or equally resourced neighborhoods. Instead, they are frequently pushed to under-resourced, declining suburbs or peripheral areas with lower-quality schools, fewer transit options, and higher crime rates 389.

The trauma of this forced mobility is profound, particularly for families. Moving to worse-off neighborhoods intensifies poverty conditions and inhibits intergenerational economic mobility. Research from Philadelphia demonstrates that these involuntary moves lead to long-term financial strain, evidenced by sharply declining credit scores for the displaced families 3. Furthermore, the health impacts are severe; mothers who face eviction are 20 percent more likely to report clinical depression a year later, while children affected by frequent, unstable moves experience higher rates of behavioral problems, illicit drug use, and reduced continuity of healthcare 3.

Homeowners: Wealth and Tax Tensions

The narrative surrounding long-term, incumbent homeowners in gentrifying areas has historically been heavily debated. For decades, a prevailing theory suggested that rising property taxes caused by gentrifying property values would force elderly, low-income homeowners to sell their homes and flee their communities 422.

However, rigorous quantitative studies leveraging property tax data and mobility records paint a starkly different picture. Recent research demonstrates that gentrification has virtually no effect on the absolute mobility rates of homeowners 2224. In fact, several studies indicate that homeowners in gentrifying neighborhoods may actually be less likely to move than homeowners in comparable, non-gentrifying areas 825.

Rather than being forced out by taxes, homeowners often act rationally as economic actors: they realize their home is a rapidly appreciating asset and choose to stay put, letting the equity climb 2224. In Cleveland's revitalizing Hough area, longstanding homeowners saw average equity increases of approximately $20,000 during periods of intense gentrification 4. Homeowners tend to be older, have deeper roots in the community, and view their property as a long-term financial vehicle 2224. While rising property taxes certainly cause financial strain, the massive gain in generational wealth generally offsets the burden, making incumbent homeowners the primary economic "winners" among the original community.

Small Businesses: Adaptation or Eviction

The impact of gentrification on mom-and-pop storefronts is notoriously complex and under-researched compared to residential displacement. Small businesses face a dual threat during neighborhood transition: their commercial leases (which lack the minimal legal protections afforded to residential leases) spike dramatically, and their traditional customer base is simultaneously displaced 4815.

Commercial gentrification frequently threatens businesses owned by immigrants and people of color. These entrepreneurs historically face greater lending discrimination, operate with thinner profit margins in the consumer service and retail industries, and have significantly less bargaining power against commercial landlords 15. In San Francisco's Mission District during the late 1990s technology boom, commercial rents jumped by 41 percent in just two years, devastating local merchants 4.

When these long-standing local businesses are forced out, they are rarely replaced by other small, independent businesses. Instead, research using microdata from New York City shows that displaced storefronts often sit vacant for longer periods, or the spaces are swallowed by well-capitalized national chains and multiple-establishment franchises that can absorb the exorbitant new rents 4823.

However, commercial displacement is not an absolute certainty. Businesses capable of pivoting their offerings or aesthetic to cater to the incoming, higher-income demographic can thrive. The influx of new residents brings increased purchasing power to the neighborhood, translating to higher overall retail sales 432. For adaptable business owners - such as a longtime dry cleaner in Harlem that saw business improve - the changing market can yield record profits 426.

The New Frontiers: Climate Haunts and Digital Nomads

As the global economy and planetary environment shift in the twenty-first century, the mechanisms of gentrification are evolving rapidly. The phenomenon is no longer limited to the traditional "urban pioneer" moving into an inner-city industrial loft. Two new variations are actively rewriting the geography of displacement in 2024.

Climate and Blue Gentrification

As extreme weather events, catastrophic wildfires, and sea-level rise become undeniable existential threats, wealthy populations are beginning to retreat to safer, more resilient geographies, inadvertently triggering "climate gentrification" 27.

In the coastal United States, properties situated on higher elevation ridges - which were historically redlined or relegated to minority communities because they lacked prime waterfront access - are suddenly highly coveted by developers and affluent buyers fleeing flood zones 27. Conversely, researchers are documenting the rise of "blue gentrification," particularly in Southeast Asia and regions like Sardinia, Italy. In these areas, exclusive, elite-driven waterfront redevelopment displaces local coastal livelihoods and traditional fishing communities in favor of high-end tourism, massive land reclamation projects, and foreign real estate investment 38394041.

In the American West and South, mountain cities are experiencing severe housing crises driven by an influx of climate refugees. Flagstaff, Arizona, sitting at an elevation of 7,000 feet, offers an essential escape from the unbearable, life-threatening summer heat of Phoenix 27. Consequently, roughly 25 percent of Flagstaff's housing stock is now tied up in second homes for wealthy seasonal residents, driving local property values out of reach for the working class 2742.

Similarly, in Asheville, North Carolina, a combination of climate migration and intense tourism has caused median home prices to skyrocket. This influx has fueled the construction of "slim-talls" - narrow, expensive, multi-story homes built on small lots - that are physically and economically reshaping the city 2844. These pressures, combined with a brutal legacy of urban renewal, have contributed to a drastic decline in Asheville's Black population, which fell from 20 percent in 1980 to under 11 percent today 2444.

The Post-Pandemic "Zoom Town" and Geoarbitrage

The COVID-19 pandemic permanently severed the link between high-paying corporate jobs and physical office locations, giving rise to mass remote-work migration 452930. Armed with Silicon Valley, London, or New York salaries, "digital nomads" are leveraging geographic arbitrage (geoarbitrage) to live in cheaper, highly desirable international locales 4831.

Cities across the Iberian Peninsula, such as Lisbon, Madeira, and Las Palmas, are facing acute socio-spatial friction due to this influx. In Funchal and Ponta do Sol in Madeira, rental prices surged by over 30 percent between 2020 and 2023, completely decoupling the local housing market from the regional wage economy 29. While heavily promoted by national governments as a tool for post-pandemic economic revitalization, digital nomadism frequently accelerates gentrification by driving up demand for short-term rentals and co-living spaces 293048. This process transforms authentic residential neighborhoods into transient hubs that cater to foreign expatriates, placing immense pressure on local infrastructure and displacing the domestic workforce 3048.

The Global South: Gentrification as a Planetary Phenomenon

For decades, academic research on gentrification was heavily biased toward Western, Anglo-Saxon cities like London and New York. However, modern urban geography recognizes gentrification as a truly planetary phenomenon 23233. Yet, gentrification in the Global South often operates through entirely different mechanisms, driven less by individual consumer preferences and more by aggressive, state-led urban mega-projects and the violent clearing of informal settlements 23252.

In Latin America, gentrification relies heavily on direct government intervention. The state actively brands cities for global capital, prioritizing large-scale high-rise constructions, new transport infrastructure, and land valorization policies over the rehabilitation of historic, central neighborhoods 252. The traditional format of Western gentrification is less appealing; instead, the market responds to international-national cooperation that clears space for elite residential towers 252.

In Africa and parts of Asia, gentrification is frequently tied to brutal slum clearance. The most notorious historical example is the 1990 destruction of Maroko, a vast informal settlement on Lagos Island in Nigeria. The military government of Lagos state deployed bulldozers to forcefully evacuate an estimated 300,000 residents with virtually no notice 3334. The area was completely leveled and subsequently redeveloped into high-end, exclusive estates for the ultra-wealthy 34.

These Global South examples highlight the stark violence of displacement when municipal governments prioritize speculative, entrepreneurial urbanism and foreign capital investment over the housing rights and basic safety of their most vulnerable citizens 24032.

Evaluating Policy Solutions: What Actually Works?

As cities globally recognize the destructive nature of unchecked displacement, a myriad of policy interventions have been proposed to balance the need for urban investment with the necessity of social equity. Research demonstrates that relying entirely on the free market guarantees the displacement of the poor. However, well-intentioned policy interventions can also backfire if improperly designed.

| Policy Tool | Mechanism | Research Findings on Effectiveness | Key Drawbacks |

|---|---|---|---|

| Inclusionary Zoning (IZ) | Requires or incentivizes developers to set aside a specific percentage of units in new housing developments as below-market affordable housing 353637. | Moderate/Mixed: Mandatory IZ is highly effective at integrating neighborhoods. New York's mandatory program generated vastly more affordable units than its previous voluntary model 355758. | If the required set-aside percentage is too high (e.g., above 15%), it acts as a punitive tax on development, halting new construction entirely and exacerbating the regional housing shortage 365859. |

| Rent Control / Stabilization | Legally limits the percentage by which landlords can increase rent annually on existing tenants 3839. | Strong for Incumbents: Excellent at keeping long-term, low-income, and minority residents in their homes. A Stanford study in San Francisco proved it vastly reduced immediate displacement 3839. | Negative for Future Renters: Landlords frequently react by converting rental units to condos or avoiding maintenance, which ultimately shrinks the total supply of affordable rentals over time 3839. |

| Community Land Trusts (CLTs) | A non-profit organization owns the land permanently in a trust, while residents buy or rent the physical homes upon the land at deeply subsidized rates 40636441. | Highly Effective: CLTs disrupt the speculative real estate market entirely. During the 2008 financial crash, CLT homeowners were over 8 times less likely to face foreclosure than conventional buyers 6466. | Extremely difficult to scale rapidly. Requires massive initial philanthropic or public funding to acquire land, along with intensive ongoing technical management 6364. |

The Inclusionary Zoning Balancing Act

Inclusionary Zoning (IZ) is an increasingly popular policy because it attempts to leverage private market momentum to pay for affordable housing without direct public subsidies. However, housing economists warn that IZ mandates must be carefully calibrated to local market realities 353659.

A 2024 analysis by UCLA estimated that arbitrarily increasing mandatory affordability requirements heavily suppresses overall market-rate housing production. Their models suggested that for each additional percentage point of IZ mandated between 1 percent and 16 percent, market-rate housing production decreases by 4,600 to 11,900 units over a ten-year period 3658. When developers face strict mandates without adequate incentives - such as density bonuses that allow them to build taller buildings to recoup their losses - they simply halt development 3559. Alternatively, they opt to pay an "in-lieu" fee to the municipality, which often results in affordable housing being built in cheaper, segregated neighborhoods rather than integrating the gentrifying core 3559.

The Community Land Trust Solution

For ensuring long-term, permanent neighborhood affordability, researchers increasingly point to the efficacy of Community Land Trusts (CLTs). By legally separating the ownership of the physical building from the ownership of the land beneath it, CLTs completely strip real estate of its speculative market value 6441.

When a CLT homeowner decides to sell their property, the trust's resale formula strictly limits their total profit, ensuring the home remains affordable for the next low-income buyer in perpetuity 6441. Studies evaluating CLTs in California have shown that the physical presence of a CLT actively reduces the probability of displacement for renters residing in the immediate surrounding blocks, acting as a vital anchor of stability in an otherwise turbulent, gentrifying real estate market 66.

Protecting Small Businesses

To protect local commerce from the ravages of gentrification, researchers advocate for the implementation of robust "commercial tenant protections," which are currently virtually nonexistent compared to residential tenancy laws 4243.

Effective anti-displacement strategies for small businesses include implementing zoning laws and form-based codes that strictly limit the physical size of retail spaces, thereby discouraging massive national chains from entering the neighborhood 42. Furthermore, municipalities can deploy public-private grant programs - such as San Francisco's Legacy Business program, which provides direct subsidies to historic establishments that have operated for over 30 years - and help organize local merchant associations to build collective political and bargaining power against predatory commercial landlords 2943.

Bottom line

Gentrification is a powerful economic engine capable of revitalizing deeply disinvested neighborhoods, but its financial spoils are captured almost entirely by property owners, real estate developers, and affluent newcomers. The academic research is unequivocal: while original homeowners can build immense generational wealth, low-income renters and legacy small businesses face severe risks of eviction, exclusionary zoning, and profound cultural erasure. While quantitative data suggests that deep, persistent poverty causes just as much physical displacement as gentrification, it is undeniable that unchecked speculative development permanently destroys a neighborhood's baseline affordability. Ultimately, managing gentrification requires aggressive, highly targeted policy interventions - such as carefully calibrated inclusionary zoning and the expansion of community land trusts - to ensure that the residents who survived a neighborhood's hardest decades are actually able to stay and enjoy its renaissance.