Impact of generative AI on creative industry labor and income

The rapid diffusion of generative artificial intelligence (GenAI) has fundamentally altered the economic equilibrium of the global creative industries. Unlike prior waves of technological automation, which primarily targeted routine manual labor and deterministic clerical work, current iterations of large language models (LLMs) and multimodal generative systems possess the capability to execute non-routine cognitive and creative tasks. This technological shift has prompted immediate disruption across creative labor markets, challenging the viability of traditional intellectual property frameworks and forcing a renegotiation of how economic gains are distributed between technology developers and human creators.

Synthesizing recent macroeconomic data, global labor indices, freelance market analytics, and collective bargaining outcomes, this report assesses the tangible impacts of GenAI on creative employment and income. Early empirical evidence indicates that while mass, uniform technological unemployment has not yet materialized, significant task displacement, wage compression in specific sub-sectors, and a fundamental reorganization of the creative production process are actively underway.

Macroeconomic Theory and Task Displacement

To understand the labor market effects of GenAI, labor economists distinguish between complete occupational automation and granular task displacement. According to task-based economic models, occupations are not monolithic entities but bundles of discrete, interrelated tasks. When technological innovations expand the set of tasks that algorithmic capital can perform, human labor is displaced from those specific functions 12.

Historically, general-purpose technologies have offset this displacement by simultaneously driving productivity gains that create new, complementary tasks for human workers, thereby increasing overall labor demand. However, current research into generative AI cautions against assuming an automatic equilibrium. Economic frameworks examining "so-so automation" describe technologies that are just productive enough to be adopted by firms - thereby displacing workers and reducing the labor share of income - but not productive enough to significantly raise overall total factor productivity or generate compensatory employment 345. If GenAI systems are deployed primarily to substitute creative labor for marginal cost savings rather than to pioneer entirely new creative mediums, the net economic effect on the creative workforce is likely to be depressive 35.

Advanced methodologies for economic surveillance support this hypothesis of labor substitution. By applying computational linguistics to corporate earnings calls, researchers can track real-time firm-level investments and strategic responses to macroeconomic shocks. Text-as-data approaches reveal that while firms express overwhelming optimism regarding AI's potential (with over 96% of analyzed firms reporting positive sentiment), approximately 48% of corporate discussions around AI explicitly address labor displacement, workforce strategies, and cost reductions. In contrast, only 23% of these discussions mention the creation of new tasks for human employees 567. This dynamic suggests that enterprise adoption of GenAI in the near term is heavily weighted toward substituting human labor to lower the cost of capital rather than augmenting the workforce to expand creative output.

Global Occupational Exposure Assessments

The International Labour Organization (ILO) provides the most comprehensive global framework for assessing occupational exposure to GenAI. In its 2025 update, the ILO refined its methodology by utilizing a 6-digit occupational classification system encompassing nearly 30,000 discrete tasks. This updated model combined expert human inputs with predictive modeling to generate a highly granular assessment of automation vulnerability 89.

The 2025 index categorizes four progressively increasing gradients of GenAI exposure. The findings indicate that globally, one in four workers is currently in an occupation with some degree of GenAI exposure 910. While clerical and administrative roles remain the most highly exposed globally, the 2025 data reveals a marked increase in the exposure scores for media, creative, and web-related occupations 10. This shift is directly attributable to the expanding multimodal capabilities of GenAI models, particularly in image, audio, and video generation, which were less sophisticated during the initial 2023 assessments 910.

Despite this high exposure, the ILO concludes that the overwhelming global effect of GenAI will be to augment occupations rather than automate them entirely, largely due to the persistent need for human oversight and strategic direction 8. However, regional data underscores significant variability based on the density of knowledge work. In highly developed, service-oriented economies, occupational exposure is substantially higher.

| Region / Assessment Entity | Key Findings on GenAI Workforce Exposure | Primary Vulnerable Demographics |

|---|---|---|

| Global (ILO 2025 Update) | 1 in 4 workers globally are in occupations with some degree of GenAI exposure. Mean automation score is 0.29. | Clerical workers, highly digitized professional/technical roles; highly gendered impact affecting female employment. |

| London (GLA Economics 2025) | 46% of the workforce (approx. 2.4 million people) resides in roles where GenAI could automate a share of tasks. | Knowledge-intensive and creative professionals clustered in urban centers. |

| United Kingdom (National Avg.) | 38% of the national workforce faces significant task exposure to GenAI. | Media, web-related, and administrative occupations. |

| United States (CVL Economics) | 204,000 entertainment industry jobs projected to be disrupted by 2026. | 3D modelers, sound editors, broadcast technicians, concept artists. |

The concentration of creative, media, and knowledge industries in urban centers makes them ground zero for near-term labor market disruptions. The disparity between the global average and specific creative hubs highlights that the disruption will not be felt equally; rather, it will be acutely concentrated in sectors reliant on digital asset creation and knowledge synthesis 811.

Sector-Specific Income Contractions

While macroeconomic indicators suggest gradual augmentation over time, granular data from specific creative sectors reveals immediate friction. Empirical analyses indicate that occupations with higher exposure to GenAI are already experiencing localized wage erosion and contracting employment opportunities as production pipelines reorganize.

Music and Audiovisual Production

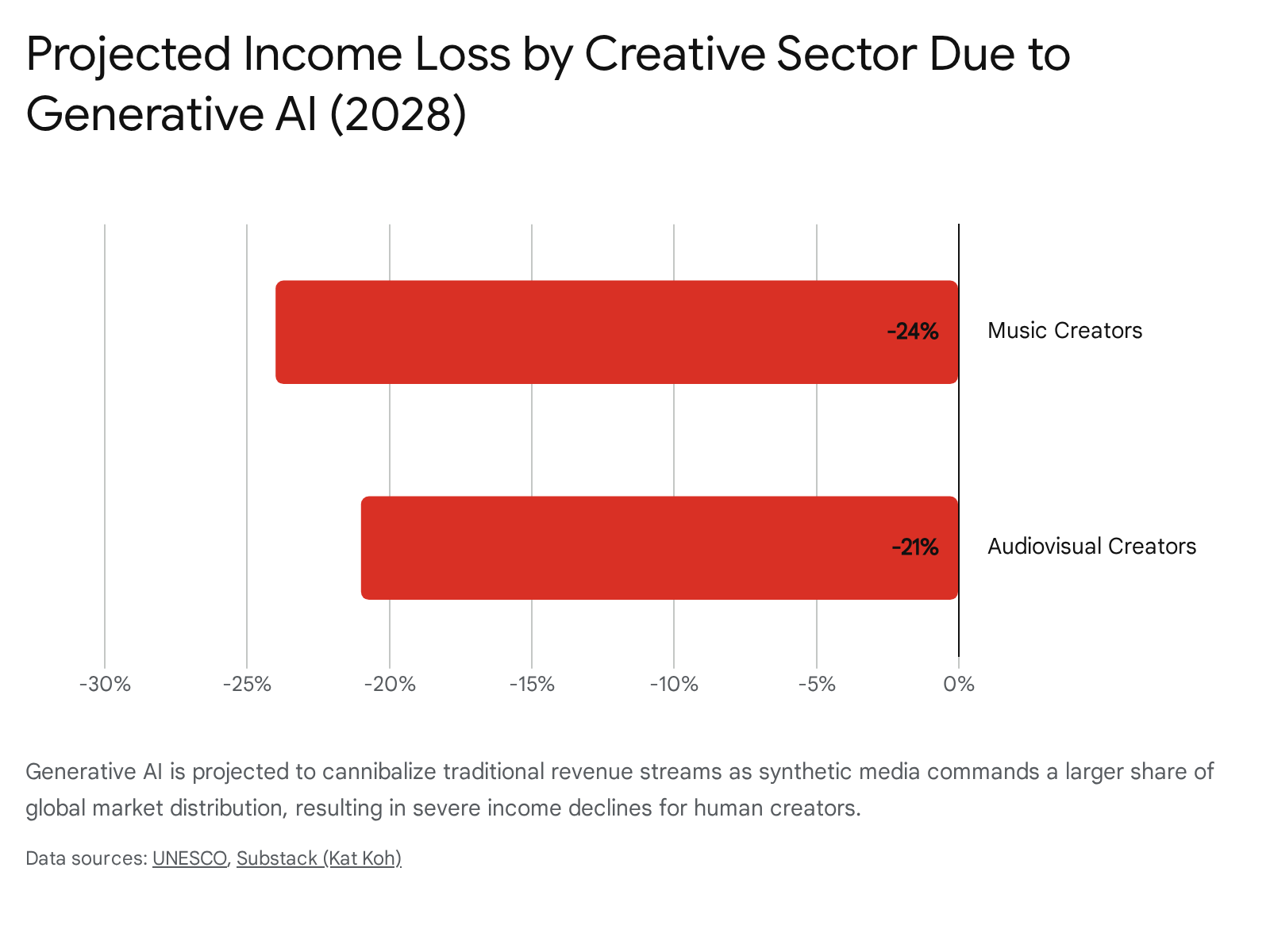

The financial pressures on global creators have been systematically quantified in the 2026 UNESCO report, Re|Shaping Policies for Creativity. Drawing on data from over 120 countries, the report projects significant, near-term income losses for artists driven by the proliferation of AI-generated content entering global markets 1213.

By 2028, music creators are projected to experience a 24% decline in revenue, while workers in the audiovisual sector face a 21% income reduction 12.

These proportional declines translate to massive capital transfers. A global economic study commissioned by the International Confederation of Societies of Authors and Composers (CISAC) calculated a cumulative loss of €22 billion over five years - €10 billion extracted from the music industry and €12 billion from the audiovisual sector 1416. This shift represents a direct transfer of economic value from human creators to the technology firms operating generative AI models.

The mechanisms driving these losses are structural. AI-generated music is projected to capture approximately 20% of traditional streaming platform revenues by 2028, and a staggering 60% of music library revenues, directly cannibalizing the synchronization and licensing income that sustains human composers 16. A survey by PRS for Music found that 74% of its members were deeply concerned about AI-generated music directly competing with human-made compositions 16.

Writing, Translation, and Screenwriting

In the writing domain, translation and localization present the most severe displacement risks. The CISAC study projects that translators and adaptors for dubbing and subtitling will see 56% of their revenue at risk as AI systems rapidly achieve parity in localization tasks 16. Real-world impacts are already measurable: a 2024 survey of nearly 800 respondents by the UK Society of Authors found that 36% of translators had already lost work directly due to generative AI, and 43% reported a measurable decrease in their overall income 16. Among general authors and illustrators, 86% reported that GenAI had reduced their earnings, and 32% of illustrators reported lost commissions or canceled projects 16.

The screenwriting sector in Hollywood is experiencing a similar contraction, driven by a combination of AI integration and broader post-strike industry realignment. The Writers Guild of America (WGA) West's annual financial report for 2024 revealed that total member earnings, while rebounding slightly from the strike-depressed figures of 2023, remained 21% below 2022 levels 16. Most critically, employment in television and digital platforms fell 28.5% from 2022, and TV writing jobs specifically dropped by 42% in the 2023 - 2024 season 16. Industry insiders note that this labor contraction in writers' rooms is partly facilitated by showrunners utilizing AI assistants for drafting and outlining, effectively replacing junior staff positions 15.

Animation, Visual Effects, and Gaming

The visual arts, particularly commercial animation, visual effects (VFX), and video game development, are experiencing aggressive task consolidation. A 2024 study by CVL Economics, commissioned by industry guilds including the Animation Guild, estimated that 204,000 entertainment jobs across the United States would be disrupted by AI by 2026, with 62,000 of those jobs located in California 1617.

The disruption is not evenly distributed across the production pipeline. C-suite executives and managers indicated that roles heavily reliant on digital rendering, environmental design, and asset generation are highly vulnerable.

| Most Vulnerable Roles (Expected Displacement by 2026) | Moderately Vulnerable Roles | Least Vulnerable Roles |

|---|---|---|

| 3D Modelers (approx. 33% anticipate displacement) | Compositors (25% anticipate impact) | Storyboard Artists (15% anticipate impact) |

| Sound Editors / Designers (over 50% anticipate impact) | Graphic Designers (25% anticipate impact) | Look, Surface, and Material Artists |

| Re-recording Mixers / Audio Technicians | Software Analysts and Testers | Physical Dancers / Live Performers |

| Concept Artists / Visual Developers (Gaming Sector) | Tools Programmers | Choreographers |

Data sourced from the 2024 CVL Economics Entertainment Industry Report 1617.

This exposure has fundamentally altered traditional hiring patterns. While new roles - such as "AI creative director" or prompt orchestrator - are emerging, these positions generally focus on curating AI outputs rather than producing individual assets 16. The consensus among industry analysts is that displaced entry-level and mid-tier digital artists do not automatically transition into these new oversight roles, as the required strategic skill sets are not a one-to-one conversion 17. Consequently, studios are achieving production goals with fundamentally smaller human crews, limiting entry points for emerging professionals.

Regional Friction in High-Digitization Markets

The integration of GenAI is acutely visible in highly digitized, rapid-production mediums, offering a preview of global trends. South Korea, possessing the world's largest webtoon market and serving as a primary cultural exporter, provides a critical case study 18.

Within the webtoon industry, solo creators face intense scheduling demands, often producing high volumes of serialized art weekly without institutional support. Industry forums reveal a complex dynamic: many independent creators argue that utilizing GenAI is an essential productivity mechanism that democratizes creation, allowing them to raise their output to compete with larger, well-capitalized studios 19.

However, the adoption of AI in webtoons has generated severe sociotechnical friction. Qualitative research into the sector identifies a "Tripartite Mediation Model" governing AI adoption, characterized by ongoing tension between production efficiency, reader reception, and market distribution 20. Readers place a high premium on the parasocial authenticity of human creators and frequently reject AI-assisted artwork as "soulless," viewing it as a breach of the creator-consumer contract 20. This consumer backlash compels creators to adopt "strategic silence" regarding their workflow. They leverage the technology invisibly to reconcile the grueling industrial demands of digital comics with the audience's demand for the illusion of a purely human touch 20.

In the South Korean voice acting sector, displacement is more transparent and immediate. Voice actors report that entry-level commercial work - such as automated television shopping disclaimers, educational narrations, and corporate videos - has been almost entirely absorbed by synthetic voice technologies 1823. Production companies increasingly utilize digital voice libraries to bypass professional casting entirely. The Korea Voice Performance Association has highlighted instances where AI models were trained on the historical recordings of human actors without ongoing consent or compensation. In response, labor organizations are actively lobbying for a legally recognized "voice publicity right" to treat vocal characteristics as protected commercial attributes and to ban model training without explicit contractual consent 18.

Freelance Market Restructuring and Valuation

Because a significant portion of creative labor is executed through independent contracting, gig economy platforms offer real-time data on the shifting valuation of creative tasks. In 2026, the United States freelance workforce reached approximately 76.4 million individuals, representing roughly 40% of the workforce and contributing an estimated $1.27 trillion to the economy 2425. By 2027, projections suggest this number will climb to 86.5 million 24. An analysis of the two dominant freelance marketplaces, Upwork and Fiverr, reveals a bifurcated market reacting violently to the introduction of GenAI.

Contract Volume and Earnings Compression

A comprehensive 2025 study published by the Brookings Institution examined the direct impact of GenAI on freelance employment outcomes. Analyzing platform data in the months following the public release of advanced LLMs, researchers identified a 2% decline in the total number of contracts and a 5% drop in total earnings for freelancers operating in highly exposed occupations 21. Crucially, these negative trends did not dissipate as a short-term shock but persisted and grew over the subsequent eight months, suggesting a structural shift in how specific services are valued and delivered 21.

Counterintuitively, the study revealed that high-skill, experienced freelancers suffered the most pronounced negative effects 21. Prior economic theory held that high-skill labor would be insulated from automation due to the complexity of the tasks. However, generative AI serves to reduce the variance in output quality; by enabling lower-skill individuals or the clients themselves to produce acceptable baseline content, the technology diminishes the premium previously commanded by top-tier professionals executing standardized tasks 21.

The Rise of the AI-Augmented Specialist

Despite the localized drop in contract volume for highly exposed, routine tasks, overall average freelance rates have experienced upward momentum. In 2026, the average U.S. freelancer earns an estimated $47.71 to $54.00 per hour, representing an 11% year-over-year growth 24252722.

This apparent paradox - aggregate wage growth amidst task displacement - is driven by a compositional shift in the market known as the "Specialization Premium." GenAI has effectively established a zero-dollar price floor for generic, low-complexity deliverables (e.g., basic SEO blog posts, simple logo generation, routine data entry) 2723. Consequently, these low-wage gigs are disappearing from the platforms, mathematically pushing the average rate upward as only complex work remains.

Simultaneously, freelancers who have integrated AI into complex, strategic workflows are commanding substantial premiums. Upwork data from 2026 indicates that freelancers who explicitly mention AI proficiency in their profiles charge an average of 25% more than their peers 27.

| Freelance Category | 2026 Average Hourly Rate (USD) | YoY Trend / AI Impact Note |

|---|---|---|

| AI & Automation Consulting | $80 - $200+ | Up 23%. Highest demand premium; low talent supply. |

| UX/UI & Strategic Design | $45 - $100+ | Up 15%. Focus on systems design rather than basic asset creation. |

| Complex Software / Web Dev | $50 - $150+ | Up 12%. Integration of AI APIs and custom deployment. |

| Copywriting & Content Strategy | $27 - $60 | Up 9%. Pure SEO writing declining; strategic brand voice commanding premiums. |

| Basic Data Entry / Admin | $5 - $15 | Stagnant/Declining. Heavy displacement by automated agents. |

Data aggregated from 2026 Upwork, Clockify, and Jobbers industry reports 272230.

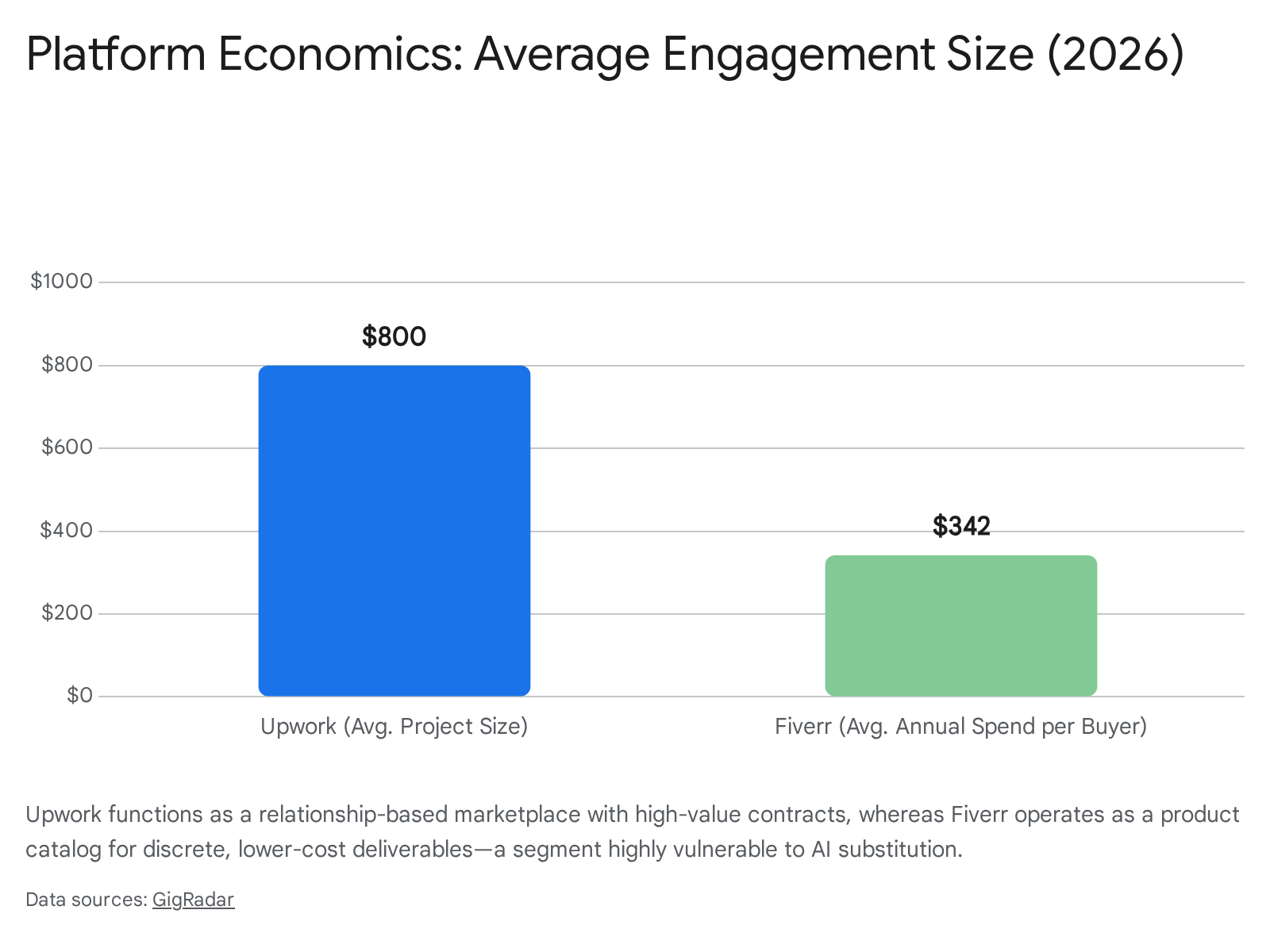

Platform Economics and the Shift to Value-Based Pricing

The pricing structures of the platforms reinforce this bifurcation between commoditized tasks and strategic relationships. Fiverr, traditionally structured as an e-commerce catalog for discrete gigs, takes a flat 20% commission from freelancers alongside a 5.5% buyer fee 2431. Upwork, tailored toward larger agency relationships and ongoing contracts, transitioned in 2025/2026 to a flat 10% freelancer fee, supplemented by variable client-side initiation fees 243132.

As AI commoditizes the quick, under-$100 deliverables that form Fiverr's core historical business, professional creatives are increasingly forced to migrate toward Upwork's relationship-based, $800+ average project model to sustain a living wage 32.

Furthermore, the integration of AI is altering optimal freelance pricing models globally. Hourly billing inherently caps a freelancer's income to their time worked. As AI drastically reduces the time required to complete drafting, coding, or rendering tasks, hourly workers face an effective pay cut for becoming more efficient 24. Consequently, there is an industry-wide push toward value-based and project-based pricing. Data from the Jobbers Freelance Benchmark Report indicates that freelancers utilizing value-based pricing report a median income of $96,000, compared to just $58,000 for those billing hourly - a massive 66% income gap 24. By unlinking compensation from time spent, augmented freelancers can capture the financial upside of their AI-enabled efficiency.

Collective Bargaining and Guild Responses

In the face of technological disruption, organized labor within the entertainment industry has mounted unprecedented resistance. The 2023 strikes by the Writers Guild of America (WGA) and the Screen Actors Guild - American Federation of Television and Radio Artists (SAG-AFTRA) marked a historic inflection point. Prior to these strikes, the Directors Guild of America (DGA) established the first AI provisions in any guild contract in June 2023, but it was the protracted dual strikes of writers and actors that established the primary contractual guardrails regarding GenAI in the creative sector 16252636.

The core strategy of these guilds is not to completely outlaw the technology - which labor attorneys acknowledge is impossible given studio ownership of underlying intellectual property - but to ensure consent, secure compensation, and prevent the uncredited ingestion of union-covered work into proprietary training models 2637. The WGA secured provisions ensuring that AI is not classified as a "writer," meaning AI-generated output cannot be considered source material that would reduce a human writer's credit, compensation, or residuals 252638. SAG-AFTRA secured requirements for informed consent and compensation before a studio can create or utilize a digital replica of an actor 2728.

However, as technology rapidly evolves, these initial protections are already viewed as fragile. During the 2026 contract negotiations, which extended past their initial February deadlines, SAG-AFTRA signaled a highly aggressive posture regarding synthetic performers 253829. Spurred by the introduction of fully synthetic AI actors (such as "Tilly Norwood"), the guild proposed the "Tilly Tax" - a mandatory financial fee studios must pay to the union's health and pension funds whenever an AI actor is utilized in lieu of a human performer 382942. This proposal operates fundamentally as an economic friction mechanism, artificially raising the cost of synthetic labor to ensure that human actors remain the financially logical choice for studios seeking to cut costs 3829. Alongside AI, SAG-AFTRA continued to press for expanded streaming residuals, proposing a $40 million success bonus pool 42.

The Animation Guild (TAG) 2024 Contract Disputes

The Animation Guild (IATSE Local 839), representing over 5,000 artists, writers, and technicians, entered its 2024 negotiations with AI as an existential priority 3630. Following months of bargaining, targeted rallies ("March on the Boss"), and complex negotiations, TAG reached a tentative agreement with the Alliance of Motion Picture and Television Producers (AMPTP) in late 2024, which was subsequently ratified in December by 76.1% of voting members 363031.

The resulting Memorandum of Agreement secured significant traditional labor victories, including a tiered minimum wage increase of 7% in the first year, 4% in 2025, and 3.5% in 2026, alongside vital remote work protections and the recognition of Juneteenth as a paid holiday 30313233. However, the AI provisions were met with intense internal controversy. The contract does not forbid studios from utilizing GenAI 31. Instead, it establishes a framework requiring producers to provide advance written notice if an employee will be required to use a GenAI system, and allows employees the opportunity to "consult" on alternative, non-AI tools if time permits 30. Furthermore, the contract guarantees that employees using GenAI will not lose credit or entitlements, and indemnifies workers against legal liabilities (such as copyright infringement) stemming from studio-mandated AI use 30.

Critics within the guild - including members of the negotiating committee like director Mike Rianda, who publicly urged a "no" vote - argued that these notification requirements lack the teeth necessary to prevent job displacement, noting that "consultation" does not equate to "consent" and that entry-level positions remain highly susceptible to elimination 3435. Leadership acknowledged these limitations, stating that no single union contract can halt the macroeconomic force of AI on its own. Consequently, TAG pledged to pivot toward a multi-faceted approach involving legislative lobbying and advocating for state and federal tax incentives that exclusively support and subsidize human-made art 313435.

| Labor Organization | Contract Cycle | Core GenAI Protections Secured / Proposed | Mechanism of Enforcement |

|---|---|---|---|

| WGA (Writers) | 2023 - 2026 | AI cannot be credited as a writer; AI output cannot reduce human residuals; companies cannot mandate AI use. | Strict definitional boundaries protecting "literary material" status. |

| SAG-AFTRA (Actors) | 2023 - 2026 / 2026+ | Informed consent required for digital replicas. 2026 proposal: The "Tilly Tax" on synthetic performers. | Consent waivers per project; proposed financial penalties for synthetic substitutions. |

| DGA (Directors) | 2023 - 2026 | First guild to establish AI boundaries; protects directorial creative rights from automated generation. | Creative rights provisions limiting unguided AI generation. |

| TAG (Animation) | 2024 - 2027 | Advance notification of mandatory AI use; right to consult on alternatives; legal indemnification for workers. | Procedural compliance and liability shielding; no outright ban on studio AI utilization. |

Geographic Disparities: AI and the Global South

The global discourse surrounding AI in the creative and knowledge sectors has predominantly focused on the economic realities of the Global North, where formal labor unions and robust social safety nets exist. However, the macroeconomic implications for the Global South are uniquely perilous. Across regions like Sub-Saharan Africa, South Asia, and Latin America, informal work remains the dominant form of employment. According to the ILO and WIEGO, approximately 61% of the world's workers - representing roughly 2 billion people - are informally employed 36.

In advanced economies, workers transitioning due to AI disruption may rely on formalized retraining programs and unemployment benefits. In developing nations, a severe digital divide limits adaptation. While 67% of individuals in developed countries possess essential digital skills, the figure drops precipitously to just 28% in developing regions 12.

Furthermore, the Global South has spent the last two decades building vast economies around outsourced business process outsourcing (BPO), call centers, and entry-level IT services 3751. Generative AI directly threatens these sectors. Countries like India and the Philippines, which house an estimated 1.7 million call center workers, are experiencing immediate contraction in customer support and back-office roles, with companies replacing human agents with advanced conversational AI 37. In India alone, reports suggest up to 20 to 25 million jobs could be displaced by 2030 as routine information-processing tasks are automated 37.

Simultaneously, a new, highly precarious class of AI labor has emerged. In Kenya, a burgeoning industry of data labelers - workers earning as little as $1.50 to $2.00 per hour to filter graphic content and train LLMs for major platforms - faces a bleak paradox: they are providing the foundational labor to train the very algorithms designed to render their roles obsolete in the near future 37. The World Economic Forum projects that between 2025 and 2030, 22% of total global jobs will undergo transformation, with 170 million new jobs created but 92 million displaced 38.

For the Global South, this transition risks initiating a form of "AI colonialism." The low-wage, invisible labor of data annotation is extracted by the Global North, while the subsequent economic rewards, massive productivity gains, and high-value algorithmic orchestration roles remain deeply concentrated in Silicon Valley and other developed technology hubs 37. Reversing this trajectory requires urgent transnational policy interventions focused on building equitable digital infrastructure, fostering sovereign algorithmic development, and creating portable digital identities to legitimize and protect the informal workforce 3651.

Conclusion

The integration of generative artificial intelligence into the creative industries represents a profound structural shock, reshaping labor dynamics on a global scale. Analysis of current income and employment data reveals that GenAI is not a uniform job destroyer, but rather a polarizing economic agent. It aggressively commoditizes routine, lower-complexity creative tasks - such as basic drafting, commercial illustration, routine translation, and localized commercial voice performance - leading to distinct wage compression and diminished contract volumes for workers entrenched in those specific sectors.

Conversely, the technology heavily rewards deep specialization. Creative professionals capable of moving up the value chain to act as strategic orchestrators of AI outputs are capturing a significant "specialization premium." By adopting value-based pricing models, these augmented professionals are pushing average freelance wages higher, even as the total available volume of discrete, low-level tasks shrinks.

Labor organizations find themselves operating at the very boundaries of traditional collective bargaining. While guilds have successfully negotiated frameworks for consent, compensation, and notification, they increasingly recognize that standard labor contracts cannot entirely halt macroeconomic technological substitution. Ensuring a sustainable creative economy moving forward will require a multifaceted approach: modernized intellectual property regulations to protect training data, fiscal policies that disincentivize unchecked automation (such as the proposed Tilly Tax), and equitable international development strategies to prevent the deepening of the global digital divide. Absent proactive, coordinated intervention, the economic architecture of the creative industries will inevitably concentrate wealth among platform owners and elite technological curators, while rapidly hollowing out the middle class of working artisans worldwide.