Demographic Analysis of Generational Cohort Differences

The classification of populations into distinct generational cohorts - such as the Silent Generation, Baby Boomers, Generation X, Millennials, and Generation Z - has become a pervasive framework in sociological research, labor economics, and market analysis 123. These delineations attempt to group individuals born within a specific time span who have ostensibly experienced similar formative historical, technological, and cultural events 344. However, empirical scrutiny of behavioral, psychological, and financial data frequently reveals a significant divergence between popular narratives regarding generational traits and the underlying reality 257. Rigorous demographic and economic analyses demonstrate that many presumed generational differences are actually artifacts of life-stage development, macroeconomic period effects, or profound methodological flaws in survey design and cross-sectional comparisons 267.

Methodological Constraints in Cohort Analysis

The foundational challenge in separating empirical fact from sociological fiction regarding generations lies in the mathematical constraints of demographic data. Researchers attempting to isolate the unique characteristics of a birth cohort face structural statistical barriers that routinely lead to the misinterpretation of individual developmental changes as generational phenomena.

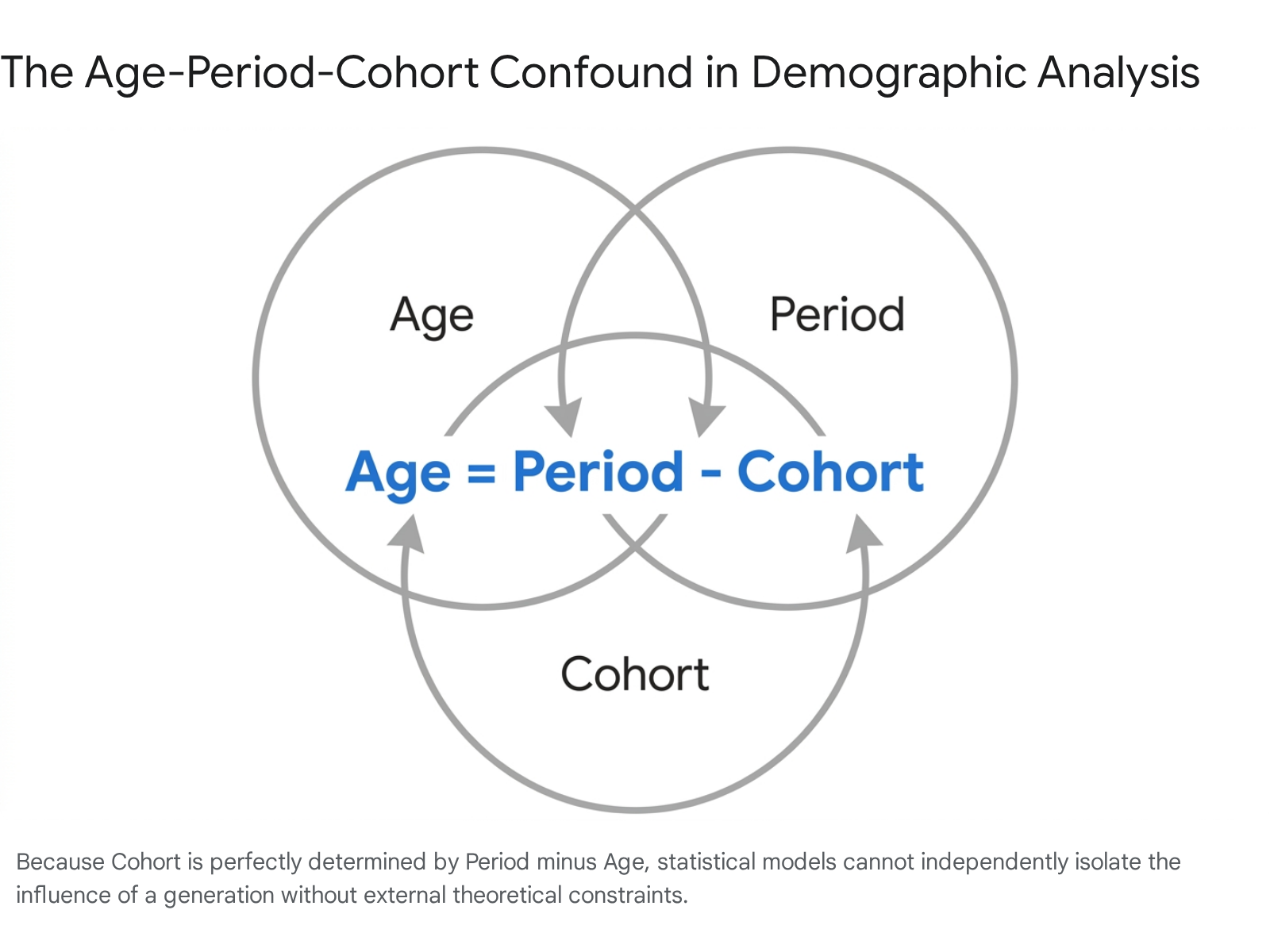

The Age-Period-Cohort Identification Problem

The primary methodological obstacle in generational research is the Age-Period-Cohort (APC) identification problem, an exact linear dependency that prevents the independent estimation of age, period, and cohort effects without applying strict theoretical constraints 67.

The identification problem arises from the deterministic equation: $Age = Period - Cohort$ 6789. If a researcher knows an individual's age and the calendar year (period) in which a survey was conducted, their birth year (cohort) is automatically determined 68910. Because these three variables are perfectly collinear, placing them simultaneously into a standard regression model results in a singular, non-identifiable design matrix 611. Consequently, it is mathematically impossible to isolate linear age, period, and cohort effects from one another using cross-sectional data alone 8.

When analysts observe a specific behavior or outcome in a given year - for example, lower homeownership rates among 30-year-olds in 2024 - they must disentangle three distinct phenomena: 1. Age Effects: Biological, psychological, or developmental changes associated with reaching a specific life stage, such as being 30 years old, regardless of the historical era 67. 2. Period Effects: Broad societal, legislative, or macroeconomic events (e.g., high interest rates, global pandemics, economic recessions) that equally affect all living generations simultaneously at a specific calendar time 67. 3. Cohort Effects: Variations resulting from the unique formative experiences and aggregate exposures of a specific birth cohort that persist throughout their lives as they move across time 67.

Because most generational research relies on point-in-time cross-sectional surveys rather than extensive longitudinal data, differences attributed to a generation are frequently just age-related developmental stages 121012. When a survey compares 25-year-old Millennials to 60-year-old Baby Boomers, the variance in their responses is largely explained by their respective stages in the life cycle, not an inherent generational psychology 210. The failure to account for this confounding variable suggests that a substantial portion of the empirical evidence regarding generations is mathematically compromised 18.

Advanced Analytical Frameworks

To circumvent the identification problem, statisticians and demographers have developed several advanced analytical frameworks, though none offer a perfect solution 78. The most common approach, first suggested by Mason et al. in 1973, is the Constrained Coefficients Generalized Linear Model (CGLIM), which constrains certain parameters in a model to be equal, effectively combining two groups to break the linear dependency 67. However, the results from this analysis depend heavily on the constraints chosen by the investigator, which must be based on external theoretical information rather than the data itself 6.

Other researchers utilize the Hierarchical APC-Cross-Classified Random Effect Model (HAPC-CCREM), developed by Yang and Land 715. This mixed-effects model enters age as a fixed effect, while cohort and period are entered as random contextual effects 15. While some claim this solves the identification problem, critics argue that the collinearity is present in the underlying process that creates the data, meaning no statistical model can completely isolate linear effects without making strong, potentially incorrect assumptions (e.g., assuming true period trends are zero) 78.

Alternatively, the Age-Period-Cohort-Interaction (APC-I) model attempts to represent cohort effects as the differential effects of social change (period effects) depending on an individual's age 13. This model quantifies inter-cohort deviations from age and period main effects, providing a method to test whether the impacts of social events are actually differential for individuals of different ages 13. Furthermore, researchers may decompose time effects into linear and non-linear components, acknowledging that while the linear components remain unidentifiable, the non-linear components are identifiable and can be used for hypothesis testing 11.

The Ecological Fallacy in Demography

Compounding the mathematical challenges of APC analysis is the ecological fallacy, a formal logical error in the interpretation of statistical data that occurs when inferences about the nature of specific individuals are deduced exclusively from inferences about the broader group to which those individuals belong 17141516.

In sociological and generational research, ecological fallacies assume that what is true for a population average is true for the individual members of that population 17. The concept dates back to Émile Durkheim's foundational sociological research, which found that predominantly Protestant localities had higher suicide rates than predominantly Catholic localities 15. Concluding that an individual Protestant had a higher suicide risk than an individual Catholic based on group-level geographic data represents an ecological fallacy, as a group-level relationship does not automatically characterize the relationship at the individual level 15. Similarly, if a study notes that countries with higher coffee consumption have lower incidences of heart disease, it is erroneous to conclude that an individual who drinks more coffee inherently has a decreased risk 1621.

Applied to generational cohorts, if data indicates that Millennials, on average, have higher student loan debt than Generation X, it is an ecological fallacy to assume that a randomly selected Millennial is more indebted than a randomly selected Gen Xer 1715. The distribution of characteristics within generations is almost always wider and more heterogeneous than the variance between generations 2. Just because a distribution possesses a positive mean does not preclude it from possessing a negative median, a property linked to the skewness of the data 15. This creates substantial liabilities for organizations that attempt to design human resources policies, management strategies, or marketing campaigns based on generational stereotypes, as they risk making decisions based on aggregate averages that fail to reflect the diverse reality of individual constituents 1.

Shifts in Institutional Reporting Standards

Due to the combination of the APC identification problem, the ecological fallacy, and the risk of perpetuating stereotypes, leading demographic institutions are altering their approach to reporting 121718.

The Pew Research Center, a primary source for much demographic data, announced a shift away from the default use of generational labels 1718. The institution noted that generational categories are not scientifically defined, and the boundaries are often fuzzy, arbitrary, and culture-driven 1719. Pew now prioritizes Age-Period-Cohort analysis to study groups of similarly aged people over time, abandoning default labels like "Millennial" or "Gen Z" unless historically comparable longitudinal data explicitly justifies it 1018. This shift emphasizes that many trends previously attributed to generational shifts speak more accurately to the demographic makeup of a group at a specific life stage; younger adults, regardless of the decade they were born in, tend to react to similar economic and social pressures in similar ways 18.

Generational Work Values and Employee Tenure

The modern workplace is the primary domain where generational theories are deployed, often driving significant investments in human resources consulting, leadership development, and employer branding 2520. However, empirical reviews of the academic literature suggest that generational differences regarding work ethic, values, and organizational loyalty are largely overstated or unsupported by data 125.

Endorsement of Work Ethic and Intrinsic Values

A persistent and heavily publicized narrative suggests that older cohorts, such as Baby Boomers, possess a stronger work ethic and a fundamentally different orientation toward labor than younger generations 52122. Stereotypes suggest younger workers demand rapid advancement, reject traditional job structures, and exhibit a weaker commitment to hard work 52123.

To test these assumptions rigorously, researchers conducted a comprehensive meta-analysis of 105 published studies measuring average work ethic scores across different sample ages 5. The analysis utilized three hierarchical multiple regressions and found absolutely no effect of generational cohort on work ethic endorsement 5. Variance in work ethic was primarily driven by the type of sample - industry workers versus university students - rather than the birth year of the respondents 5. A separate meta-analytic synthesis by Costanza and colleagues found that effect sizes for generational differences in the workplace were uniformly small, with generational membership explaining less than 2% of the variance in any workplace outcome examined 2.

Broader international data confirms this cross-generational consistency. An Organization for Economic Co-operation and Development (OECD) study assessing work needs and values concluded that there is overwhelming evidence that workers of all ages broadly value the exact same things 1224. Across generations, "family" consistently tops the list of personal values 1224. The development of the New Work Values Scale applied to a representative sample of the German population further revealed that work values associated with sustainable organizational development, meaning, and basic needs were highly similar across generations 20.

When discrepancies do appear in survey data, they are predictably tied to life-stage requirements rather than core values. Younger and older generations only differed significantly regarding how much they valued clarity, money, career development, and stimulation - all of which are highly plausible variations from a lifecycle perspective 20. For instance, a report indicating that Gen Z's preferred workplace benefits differed from previous generations was sensationalized; a deeper look at the data showed the top priority for all age groups was identical: medical insurance 1224. The only significant deviation was that younger age groups were more interested in student loan assistance, reflecting their immediate financial realities post-graduation rather than a fundamental psychological shift 1224.

Empirical Data on Employment Tenure

Another widespread assumption is that Millennials and Generation Z are inherently prone to "job-hopping," lacking the institutional loyalty exhibited by previous generations 1223025. Gallup polling data indicating that Millennials are three times more likely to have changed jobs within the past year than non-Millennials is frequently cited as evidence of this generational phenomenon 2230.

While it is statistically accurate that younger workers today change jobs more frequently than older workers today, age-adjusted historical data reveals this is a distinct age effect, not a cohort effect 2526. An extensive analysis of U.S. Bureau of Labor Statistics (BLS) data spanning from 1983 to 2024 reveals that job retention patterns for younger workers closely mirror those of previous generations at the exact same stage of their careers 25.

| Age Group Evaluated | Median Tenure in 1983 (Baby Boomers) | Median Tenure in 2002 (Generation X) | Median Tenure in 2024 (Millennials/Gen Z) |

|---|---|---|---|

| 25 to 34 years | ~3.0 years | ~3.0 years | 2.7 years |

Data aggregated from the U.S. Bureau of Labor Statistics and the National Institute on Retirement Security, tracking median worker tenure across equivalent life stages. 2526

As the historical data demonstrates, Millennials and Gen Z workers between the ages of 25 and 34 had a median job tenure of 2.7 years in 2024, only marginally lower than Baby Boomers when they were the exact same age in 1983 25. Roughly 70% of Millennials aged 22 to 37 in 2018 reported working for their current employer for at least 13 months - virtually identical to the 69% of Gen Xers who reported the same tenure when they were that age in 2002 26. Furthermore, longitudinal data from the National Longitudinal Survey of Youth 1979 indicates that Americans born in the latter years of the Baby Boom held an average of 12.9 jobs between the ages of 18 and 58, with more than 40% of those jobs held between the turbulent early-career ages of 18 and 24 27.

Rather than generational attitudes or a decline in loyalty, employee turnover is driven overwhelmingly by macroeconomic conditions and industry structures 25. Quit rates rise across all generations during strong economies with tight labor markets and fall sharply during recessions, as evidenced during the 2008 Great Recession and the 2020 pandemic 25.

Public Sector and Cross-National Employment Dynamics

The stabilization of tenure is also highly dependent on the availability of robust benefits. Public sector employment, which traditionally offers widespread access to pensions and healthcare, shows significantly lower quit rates across all age demographics compared to retail and professional services 25. In New Zealand, public sector practitioners note that values are similar across generations, with all age groups expressing discomfort with change, where resistance is simply a product of how much an individual has to gain or lose from that change 28. Randstad survey data from New Zealand confirms that across demographics, the top attractors remain fundamental: salary and benefits, work/life balance, and job security 28.

Cross-national empirical studies further erode the concept of generational work attitudes. A study examining key work and organizational attitudes among 1,019 employees in the United States and Turkey found little evidence supporting substantive generational differences 21. In fact, the researchers noted that the U.S.-originated classification of generations could not even be generalized to the Turkish business context, highlighting the fragility of cohort theory when removed from its specific socio-historical origin 21.

Macroeconomic Trajectories and Wealth Accumulation

While psychological traits, work ethic, and intrinsic values show remarkable stability across generations when adjusted for age, economic outcomes present a distinctly different and highly stratified reality 353629. The financial trajectories of cohorts have been heavily influenced by the macroeconomic periods in which they entered the labor market, the cost of higher education, and their ability to purchase appreciating assets like real estate 363031.

Aggregate Wealth Distribution and Inequality

Generational wealth distribution in the contemporary economy is marked by extreme disparities, largely stemming from the compounding effects of asset appreciation over multiple decades. In 2024, older generations held the vast majority of U.S. wealth. Baby Boomers owned 51.7% of the nation's total wealth (approximately $85.41 trillion), while Generation X held 26.1% ($43.70 trillion), and Millennials and Gen Z combined held only 10.7% ($17.97 trillion) 353640. To illustrate the divide in specific asset classes, Baby Boomers hold $25.15 trillion in corporate equities and mutual fund shares, representing 148.5% more than Millennials' $3.72 trillion 40.

However, comparing the total aggregate wealth of a 65-year-old to a 35-year-old is a classic failure to control for the life cycle 710. Younger households typically hold less wealth as they grow into their careers, accumulate savings over their working life, and eventually draw down those assets in retirement 36. When adjusted for age and historical inflation, the narrative regarding the financial impoverishment of younger generations becomes highly nuanced and complex.

According to data derived from the Federal Reserve Survey of Consumer Finances, Millennials have actually accumulated more average wealth at age 35 than Generation X did at the same age 40.

| Cohort | Calendar Year Evaluated | Median Age | Average Wealth per Person (Inflation-Adjusted to 2025) |

|---|---|---|---|

| Baby Boomers | 1990 | 35 | $134,961 |

| Generation X | 2008 | 35 | $105,334 |

| Millennials | 2024 | 35 | $219,742 |

Data reflects historical average wealth per person, adjusted for inflation, comparing generations at the identical life stage of 35 years old. 40

By 2022, the median wealth of older Millennials (born 1980 - 1989) reached over $130,000, tracking 37% above historical expectations . This represents a dramatic economic swing from 2016, when their wealth was tracking roughly 35% below expectations . This sudden surge in median wealth for individuals born in the 1980s and 1990s was primarily driven by rapid housing asset appreciation and vehicle-related asset growth between 2019 and 2022 .

Despite this higher average wealth, wealth inequality within the Millennial generation is significantly more pronounced than in previous cohorts, resulting in an uneven distribution of economic security 3532. While Millennials in the 90th percentile hold 20% more wealth than similarly ranking Baby Boomers did at age 35, the median Millennial - the point at which half have more and half have less - holds 30% less wealth than the median Baby Boomer at the same age 32. This indicates that a highly affluent subset of Millennials is skewing the generational average upward, while the typical individual in the middle of the economic distribution is worse off than their historical predecessors 3233.

Discretionary Consumption and Structural Inflation

A persistent popular narrative attributes the delayed financial milestones and lower median wealth of Millennials and Gen Z to frivolous discretionary spending - colloquially summarized by media commentators as the "avocado toast" or "latte" theory 73134. This narrative suggests that younger cohorts are forgoing homeownership and wealth accumulation in favor of daily luxuries, frequent travel, and expensive technology 3445.

Analysis of macroeconomic consumption data entirely refutes this premise 3145. A Federal Reserve study assessing millennial income, savings, and consumption patterns found that, when adjusted for demographic and socioeconomic factors, Millennial spending preferences do not differ significantly from those of previous generations 731. The economic pressure on younger cohorts does not stem from minor daily luxuries, but from the massive inflation of structural, non-discretionary necessities.

While items traditionally considered luxuries in the 1980s (such as televisions, electronics, and appliances) have become exponentially cheaper relative to income, the core pillars of middle-class stability - specifically housing, healthcare, and higher education - have vastly outpaced wage growth 45. For example, in the 1980s and 1990s, the median home price relative to income was significantly lower, allowing families to buy property early in adulthood 36. Between 1990 and 2024, median home prices increased by more than 400%, while median household income rose by less than 200% 36. The "latte factor" is a mathematical distraction; saving small amounts on daily coffee consumption cannot bridge the hundreds of thousands of dollars required for modern down payments or tuition costs 3445.

Real Estate Appreciation and Homeownership Rates

The structural divergence in generational wealth is primarily tied to real estate acquisition timing 3629. Older generations benefited from entering the housing market during periods of lower cost-to-income ratios and subsequently experiencing a long period of strong market returns and asset appreciation 36. Consequently, homeownership rates for younger cohorts have consistently lagged behind historical baselines.

At age 27, 32.6% of Gen Zers owned their home in 2024, compared to 38.4% of Gen Xers when they were 27, and 40.5% of Baby Boomers at that same age 35. At age 30, only 35% of older Millennials were homeowners, representing a steep 13-percentage-point drop compared to Baby Boomers, who reached a 48% homeownership rate by age 30 36. For Millennials at age 35, 56% owned a home in 2024, compared to 59.4% of Gen Xers and 61.5% of Baby Boomers at age 35 35.

This delay in market entry severely impacts long-term compounding wealth. Demographic analysis indicates that individuals who purchase a home at age 30 possess a 22.5% greater net worth by age 50 than those who delay purchase until their mid-to-late 40s, even after controlling for income and education 30. Earlier entry provides more years for housing wealth to grow through appreciation and mortgage amortization, while stabilizing monthly housing costs 30. In 2024, Baby Boomers owned 40.9% of all real estate in the U.S., Gen X owned 29.4%, Millennials 20.4%, and Gen Z a marginal fraction 40.

Debt Profiles and Financial Vulnerability

The composition of household debt also highlights stark generational differences . The delay in Millennial homeownership is largely driven by the burden of student loan debt, which restricts the capacity to save for down payments and alters their debt-to-asset ratios 36303136.

Millennials hold an average of $34,504 in student loan debt, while Gen Z already holds an average of $12,523 before fully completing their higher education cycles 49. This is significantly higher than Generation X, who held roughly half the educational debt of Millennials 49. Consequently, while Millennial families are more likely to have defined contribution retirement plans (like 401(k)s) than previous cohorts at the same age, their higher median debt levels offset these asset gains 29.

Contrary to narratives of reckless borrowing, Millennials actually have slightly lower overall real average debt balances than Gen X did at the same age ($44,000 for Millennials in 2017 vs. $49,000 for Gen X in 2004) 31. Furthermore, Millennials hold significantly less credit card debt and fewer mortgages than older cohorts did at the same age; their debt is heavily concentrated in non-dischargeable student loans and auto loans 31.

Generation X, currently navigating their peak earning and pre-retirement years, faces a unique set of financial pressures. Often termed the "sandwich generation" or the "forgotten generation," Gen Xers are simultaneously supporting children and providing care for aging parents 193738. A FINRA Foundation study revealed that 51% of Gen Xers report feeling stressed often by finances 37. They are the cohort most likely to hold a mortgage, and 15% of Gen Xers with mortgages reported making late payments in the past 12 months 39. Alarmingly, 31% of Gen Xers reported using high-cost alternative financial services (such as payday loans or auto title loans) in the past five years, indicating severe liquidity constraints for a segment of this population 39.

The Period Effect of the COVID-19 Pandemic

While core psychological values and behavioral traits remain stable across generations, major macroeconomic and social shocks - known statistically as period effects - can disproportionately impact specific cohorts depending on their vulnerable life stages 613. The COVID-19 pandemic serves as a profound, localized period effect that interrupted the critical educational, developmental, and early-career phases of Generation Z and younger Millennials 4054414243.

Labor Market Disruptions and Career Trajectories

Survey data collected over the years following the pandemic indicates a lasting impact on the social and professional integration of younger adults 4043. Nearly half of Gen Z (45%) and Millennials (43%) view the pandemic as a highly impactful event in their lives, compared to 31% of Gen X and just 26% of Baby Boomers 40.

For Generation Z, the pandemic struck during their initial entry into higher education or the labor market. A survey of Gen Z workers found that 66% felt their planned career paths were less stable than previously expected due to the outbreak 54. During the crisis, 34% of Gen Zers experienced canceled job interviews, 30% suffered a reduction in work hours, and 12% were furloughed 54. Furthermore, 46% of Gen Z respondents aged 13-24 reported that the pandemic made pursuing their educational or career goals actively more difficult, a concern shared by fewer Millennials (36%) and Gen Xers (31%) 42.

Institutional Trust and Social Development

The period effect of the pandemic extended deeply into social development and mental health. For younger cohorts, the lockdowns disrupted formative social milestones such as proms, first dates, and university integration 40. Consequently, 65% of Gen Z reported having to actively "relearn" social skills after pandemic restrictions were lifted, a psychological challenge reported by only 22% of Boomers 40. Additionally, about a third of Gen Z and Millennials report that their work-life balance contributes significantly to their stress levels, and over half report experiencing loneliness or depression tied to the pandemic's aftershocks 4143.

Simultaneously, the economic turbulence following the pandemic - specifically rapid global inflation - exacerbated institutional distrust among young adults 4143. In cross-national surveys spanning Brazil, India, the UK, and the U.S., a majority of adults aged 18-34 expressed the belief that businesses actively used the pandemic as an excuse to raise prices unnecessarily, fueling resentment toward corporate power 43. Over 40% of young adults across these markets report feeling "left behind" and angry at the wealthy due to pandemic-era economic shifts 43. This specific erosion of trust in business, government, and scientific institutions is a distinct period effect shaping the civic engagement of Gen Z 43.

Limitations of Western Generational Taxonomy

A critical, often unaddressed limitation in generational research is the overwhelming reliance on North American historical and cultural markers to define global populations 121. The sociological labels "Baby Boomer," "Generation X," and "Millennial" are fundamentally tied to mid-20th-century Western events, such as the post-WWII fertility spike in the United States, the advent of the personal computer, and the cultural impact of the September 11 attacks 1332.

Cultural Discrepancies in Formative Events

Applying these Western-centric labels to non-Western populations lacks methodological validity and creates conceptual inconsistencies 1. Generational cohort theory posits that a generation shares the same political, economic, and social events during the early stages of life (typically ages 17 to 23), developing a similar set of beliefs based on those shared events 4444. Because historical events are localized, cohorts cannot be globally uniform.

In regions utilizing different calendar systems (such as Islamic, Buddhist, or Chinese calendars), the term "Millennial" is chronologically irrelevant 1. In nations with distinct geopolitical histories, generations are defined by entirely different epochs and regime changes. For example, demographic research in China pragmatically labels cohorts by decade (e.g., the "Post-80s" and "Post-90s" generations), reflecting the massive internal shifts following economic liberalization and the One-Child Policy 159. In Japan, the equivalent to Gen Z is often termed the "Satori Generation" (representing roughly 14.5% of the population), a Buddhist term translating to the "enlightened generation," characterized by being free from material desires and focused on self-awareness following decades of economic stagnation 59.

In Latin America, generational boundaries are shaped by local economic crises rather than global technological shifts. Researchers in Mexico and Brazil emphasize that external events defining personal values require unique generational classifications for urban consumers 4444. Studies indicate that Mexico and Colombia form distinct cultural clusters regarding values like the Power Distance index (tolerance for authoritarianism), differing significantly from neighboring Argentina or the United States 4.

Demographic Disparities in Emerging Markets

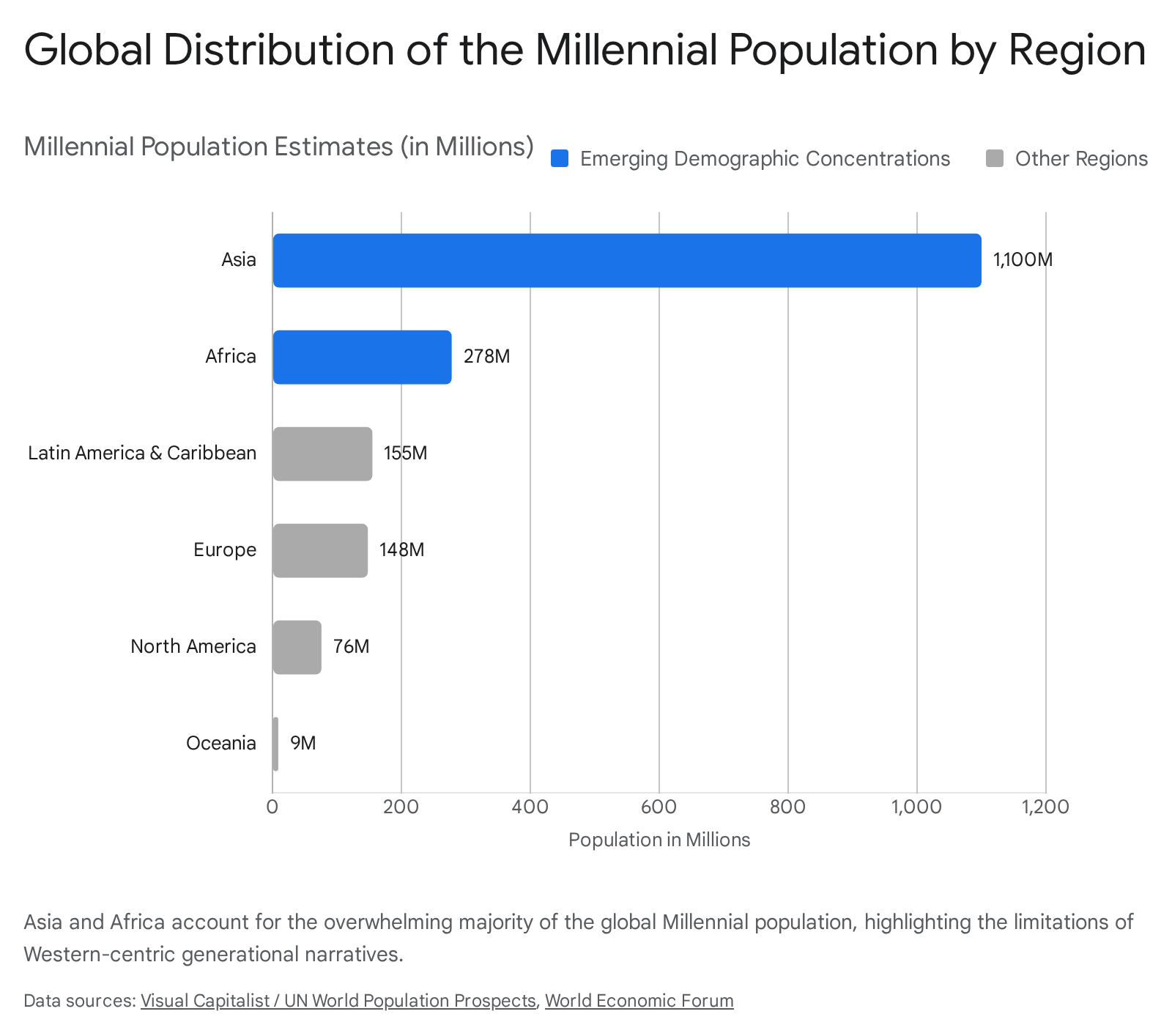

Despite the incompatibility of the specific cultural labels, tracking equivalent age brackets globally reveals massive demographic and economic shifts centered in emerging markets. Worldwide, there are an estimated 1.8 billion Millennials, making up approximately 23% of the global population 6045.

Asia is unmatched in demographic volume, serving as home to 1.1 billion Millennials, or 24% of the region's total population 6045. Africa contains the second-largest equivalent cohort, with 278 million young adults who currently control 65% of the continent's purchasing power, spending over $845 billion annually on household needs 6045.

By 2030, analysts project that Gen Z and Millennials will contribute the largest share of consumer spending across Sub-Saharan Africa, India, Indonesia, the Philippines, and much of Latin America, entirely reshaping global consumer markets 46. In the Association of Southeast Asian Nations (ASEAN) alone, Millennials and Gen Z are projected to make up 75% of all consumers by 2030 6045. Because advanced economies are facing diminished subsequent cohorts due to population decline, Gen Z is projected to be the largest and highest-spending generation ever in developing nations that have maintained population growth 46.

Synthesis

When subjected to rigorous statistical analysis and empirical review, the strict demarcation of society into distinct generational cohorts with unique, immutable psychological profiles falters. Extensive differences in work ethic, institutional loyalty, and intrinsic values are largely ecological fallacies, routinely debunked by meta-analyses that demonstrate individuals across diverse age groups broadly desire the same baseline outcomes out of life and labor 5121720. Apparent shifts in attitudes, such as job-hopping or demands for specific benefits, are demonstrably artifacts of an individual's current stage in the life cycle, rather than a permanent cohort attribute 1225.

Where generations truly differ is in their macroeconomic reality. Older cohorts benefited from historical periods characterized by accessible real estate and lower educational costs, resulting in a structural advantage in wealth accumulation that has compounded over decades 3630. Conversely, younger cohorts face compounding structural debt, hyper-inflated housing markets, and delayed asset ownership - realities frequently obscured by media narratives focusing erroneously on discretionary spending 363145. To accurately assess demographic shifts and project future economic behavior, institutions must move beyond the constraints of generic generational labels and focus directly on the intersection of individual life stages and the specific, localized economic periods in which they unfold 61017.