5 Scenarios for the Electric Grid Under AI Demand

Generative artificial intelligence requires unprecedented amounts of computational power, driving a massive surge in global electricity demand that threatens to strain transmission infrastructure and increase consumer utility bills. Depending on how utilities, technology companies, and regulators respond, the electric grid's future will likely fracture into a complex mix of high-efficiency technological breakthroughs, fossil-fueled bottlenecks, ratepayer price shocks, and off-grid climate havens.

The Physics of AI Compute: The New Energy Math

To understand the profound impact that artificial intelligence is having on global power grids, it is necessary to examine how AI fundamentally alters the physics and economics of the modern data center. For the past two decades, the internet has been powered by data centers designed to support traditional workloads: indexing search engine results, hosting websites, storing cloud data, and streaming video. These tasks are primarily handled by Central Processing Units (CPUs), which execute commands sequentially. Traditional CPU-based server racks typically draw between 5 and 15 kilowatts (kW) of electricity 12.

Generative AI requires an entirely different hardware architecture. Training and operating Large Language Models (LLMs) demands massive parallel processing capabilities, which are provided by Graphics Processing Units (GPUs). Unlike CPUs, GPUs function as thousands of tiny calculators working simultaneously to process billions of parameters 34. When packed into dense server racks, these AI-optimized arrays require extraordinary amounts of electricity. Today, a standard AI server rack demands between 40 kW and 100 kW of continuous power 12. Advanced racks utilizing the latest generation of chips are pushing beyond 130 kW, reaching the physical limits of traditional air cooling and forcing the industry toward energy-intensive liquid and immersion cooling systems 56.

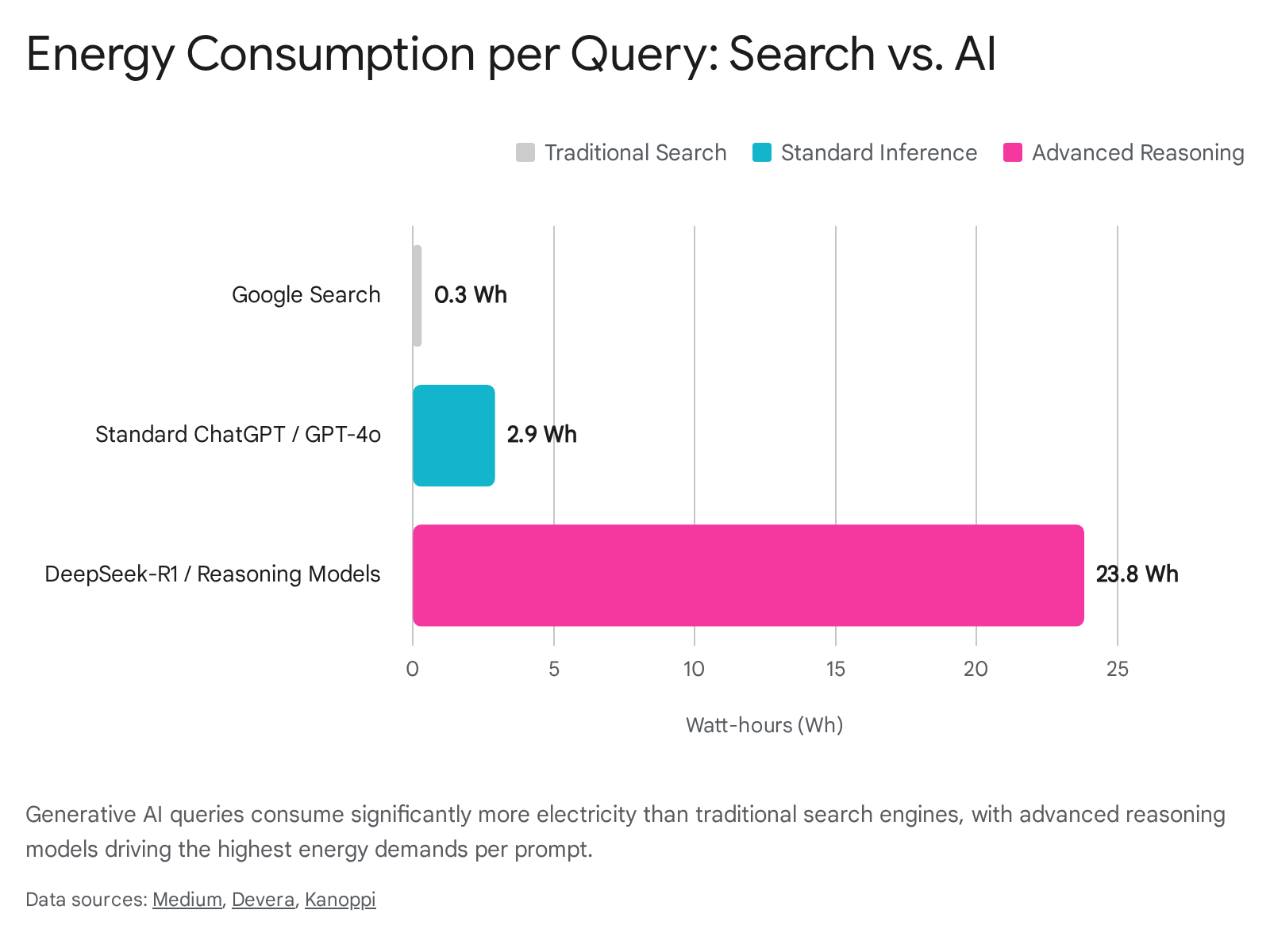

The Energy Cost of a Single Query

This hardware intensity translates directly into heightened energy consumption at the user level. The exact energy cost of interacting with an AI model depends heavily on the size of the model, the efficiency of the underlying hardware, and the complexity of the task (e.g., generating text versus generating high-definition video). However, researchers have established a clear baseline difference between traditional computing and generative AI.

A standard Google search is highly efficient, relying on retrieving pre-indexed information. This process consumes approximately 0.3 watt-hours (Wh) of electricity 78910. By contrast, an AI model does not simply retrieve information; it mathematically generates novel responses token by token. According to estimates from the International Energy Agency (IEA) and independent research organizations, a standard generative AI query (such as a typical interaction with ChatGPT) requires roughly 2.9 to 3.0 Wh - approximately ten times the energy of a conventional search 7910.

The energy demands scale dramatically with the introduction of advanced "reasoning" models. Models designed to process complex logic and mathematical problem-solving over longer inference periods can consume anywhere from 10 to 70 times more electricity than a standard AI prompt, pushing individual query costs upward of 23.8 Wh 9.

To conceptualize this, researchers often use household analogies. Submitting roughly 100 queries to a standard LLM consumes about the same amount of electricity required to boil a liter of water in an electric kettle for a cup of tea 8914. Generating a five-second AI video clip can require over 900 Wh, equivalent to the energy used to ride an electric bicycle for 38 miles .

While an individual user's daily AI queries represent a negligible fraction of their personal carbon footprint, the systemic impact is profound . With billions of users interacting with AI tools daily, the aggregate demand is effectively transforming the architecture of global energy consumption.

Global Projections: Compressing Decades of Growth into Years

The multiplication of these power-intensive queries across a global user base is driving a historic boom in data center construction. Historically, electricity demand in developed nations has remained relatively flat due to advancements in energy-efficient appliances and deindustrialization. Traditional utility planning has long assumed a predictable 1% to 2% annual demand growth over decades 1011. The AI boom has shattered this paradigm.

In 2024, global data centers consumed an estimated 415 terawatt-hours (TWh) of electricity, representing approximately 1.5% of total worldwide electricity generation 12181920. For perspective, if the global data center sector were a country, its energy consumption would rank between Japan and Russia 20.

Looking toward the end of the decade, the trajectory accelerates sharply. The IEA projects that global data center power demand will more than double to roughly 945 TWh by 2030, driven almost exclusively by the proliferation of AI workloads 121819. Within the United States, where the majority of hyperscale infrastructure is concentrated, the projections are even more acute. Research from the Electric Power Research Institute (EPRI) and the Lawrence Berkeley National Laboratory indicates that data centers consumed roughly 4% to 5% of all U.S. electricity in 2023 2131415. By 2030, depending on the speed of infrastructure deployment, data centers could account for anywhere from 9% to 17% of total U.S. electricity consumption 1315.

The Gigawatt Era

The scale of individual facilities is also expanding. Previous generations of cloud data centers typically required 10 to 50 megawatts (MW) of power. Today, developers are pursuing single AI training clusters that require between 100 MW and 1 gigawatt (GW) of continuous power 2013. A 1 GW facility demands the electricity equivalent of a mid-sized to large city, or roughly the output of a single nuclear reactor 71324.

The most prominent example of this scaling is the rumored "Stargate Project," a joint venture led by Microsoft and OpenAI aiming to build the most advanced AI infrastructure in history. Industry reports suggest the project envisions a $500 billion investment spanning multiple massive data centers, with ultimate power requirements reaching up to 5 to 10 GW 251617. Securing that volume of electricity represents an infrastructural challenge that modern grid operators have never faced.

5 Scenarios for the Electric Grid

How the global electric grid absorbs this historic shock in demand remains an open question. Grid planners, policymakers, and technology executives are navigating a highly volatile landscape constrained by regulatory bottlenecks, supply chain shortages, and ambitious climate commitments. Based on macroeconomic modeling and early market signals, five distinct scenarios are emerging for the future of the grid under AI-driven demand.

Scenario 1: The High-Efficiency Soft Landing

In the most optimistic scenario, rapid advancements in both hardware engineering and software optimization outpace the growth of aggregate energy demand. The IEA models a "High Efficiency Case" in which global energy demand from data centers is successfully curtailed to around 970 TWh by 2035, significantly lower than worst-case projections 1218.

This soft landing relies on a combination of compounding breakthroughs. First, semiconductor manufacturers continue to produce GPUs that yield exponentially more computational power per watt. Second, the AI industry masters techniques like model compression, dynamic batching, and sparse routing, which allow LLMs to deliver accurate results using a fraction of the compute cycles currently required 8.

Furthermore, data centers themselves become marvels of thermodynamics. Facilities successfully transition from traditional air cooling to advanced liquid and immersion cooling systems, slashing cooling energy requirements by 40% to 50% 5. Operators consistently achieve Power Usage Effectiveness (PUE) ratios approaching 1.1, ensuring that almost all electricity entering the building goes directly to computing rather than overhead 5. In this scenario, existing power grids accommodate the AI boom with minimal disruption, avoiding major price spikes for consumers and relying primarily on planned renewable energy additions. Furthermore, AI tools are deployed to optimize the grid itself - predicting maintenance, integrating renewables, and improving transmission capacity - leading to systemic energy savings that offset the data centers' footprint 29.

Scenario 2: The Fossil-Fueled "Lift-Off"

The second scenario envisions a future where AI adoption accelerates rapidly, but clean energy supply chains and transmission line construction fail to keep pace. The IEA terms this the "Lift-Off Case," where global electricity demand from data centers surges past 1,700 TWh by 2035 1218.

In this outcome, technology companies prioritize speed-to-market over sustainability commitments. Because AI data centers require continuous, reliable baseload power to operate 24 hours a day, intermittent renewable energy sources like wind and solar cannot support them without massive, commercially unproven battery storage infrastructure. If battery deployment and nuclear generation lag, utilities will be forced to lean heavily on natural gas and coal to prevent capacity shortfalls.

The IEA projects that in a high-growth environment, fossil fuels could account for nearly 50% of the additional electricity generated for data centers globally between 2024 and 2030 19. This poses a severe threat to global decarbonization targets. Instead of retiring aging coal plants, grid operators may extend their operational lifespans to supply capacity to new tech hubs 1120. To bypass congested public grids entirely, some technology companies may even resort to building their own natural gas reciprocating generators behind the meter to power data centers immediately, locking in years of fossil fuel dependence 1517.

Scenario 3: Infrastructure Gridlock and Cascading Grid Stress

The third scenario outlines a collision between digital ambitions and the physical limitations of electrical engineering. Power grids were historically designed under the assumption that electricity demand is diverse and distributed; thousands of homes and factories draw power in varying amounts at different times, giving operators flexibility to balance loads 21. AI data centers fundamentally break this assumption by concentrating massive, unyielding "block loads" in hyper-specific geographic locations 2133.

When a gigawatt-scale data center cluster drops offline or ramps up suddenly, the local grid experiences violent frequency and voltage deviations. This risk is not theoretical. In July 2024, a minor equipment failure on a transmission line in Northern Virginia caused 60 data centers to disconnect from the grid simultaneously 152122. Roughly 1,500 MW of computational demand vanished in seconds, forcing the regional grid operator (PJM) and local utilities into emergency maneuvers to prevent cascading blackouts across the Mid-Atlantic 31521.

In a Gridlock scenario, these near-misses become the norm. Regions not designed for sustained, highly concentrated loads are forced into a "near-permanently stressed regime," raising the risk of forced load shedding (rolling blackouts) for nearby residential communities 21. The primary bottleneck is transmission. While it takes roughly two to three years to build a massive data center, permitting and constructing the high-voltage transmission lines required to deliver power to that facility can take up to a decade or more 61023. Unable to safely integrate new loads, grid operators institute strict multi-year moratoriums on data center connections, stalling AI expansion and leaving capital investments stranded.

Scenario 4: The Ratepayer Price Shock

If utilities embark on a massive infrastructure building spree to accommodate AI data centers - laying thousands of miles of high-voltage transmission lines and constructing new power plants - the financial burden could fall directly on ordinary citizens and small businesses. This is the Ratepayer Price Shock scenario.

Electricity markets use complex mechanisms to ensure enough power plants are available to meet future peak demand, often utilizing "capacity markets." When projected demand spikes (driven by new data centers) and supply shrinks (due to retiring fossil fuel plants), capacity prices skyrocket to incentivize new generation. This exact dynamic recently shocked the PJM Interconnection, the largest U.S. grid operator serving 65 million people across 13 Eastern states 2124.

In PJM's capacity auction for the 2025/2026 delivery year, prices jumped an unprecedented 833%, rising from $28.92 per megawatt-day to $269.92 19372526. In the subsequent 2026/2027 auction, prices hit a record $329.17/MW-day 2437. Grid analysts attribute the majority of this price spike directly to data center load growth 2.

Because the cost of grid upgrades and capacity contracts are typically socialized across all users in a service area, wholesale cost increases eventually trickle down to retail utility bills 242742. Analysts estimate this capacity crunch will increase residential electric bills in affected states by 5% to 20%, translating to an extra $10 to $18 per month for the average household 37252829. Models developed by the Federal Reserve Bank of Dallas suggest that a large-scale data center build-out could even measurably increase national inflation figures. Under plausible scenarios, the Dallas Fed estimates annual Personal Consumption Expenditures (PCE) inflation could rise by 0.04 to 0.13 percentage points by 2030 solely due to electricity price impacts; in an extreme high-capacity scenario, inflation could rise by 1.02 percentage points 30. In this scenario, everyday citizens implicitly subsidize the infrastructure required by trillion-dollar technology conglomerates.

Scenario 5: Islanded Microgrids and Climate Havens

In the final scenario, the regulatory friction, gridlock, and public backlash associated with connecting to traditional public power grids push the AI industry to circumvent legacy infrastructure entirely. Tech companies begin aggressively pursuing "islanded" facilities - data centers operating on self-contained, dedicated power generation grids.

This trend is already materializing through massive private investments in clean firm power. Technology giants are funding startups developing Small Modular Reactors (SMRs) and signing long-term agreements to purchase power directly from existing, dedicated nuclear plants 25192728. By building data centers co-located with dedicated nuclear or massive solar-plus-storage facilities, companies secure their own uninterruptible baseload power without waiting in multi-year utility interconnection queues.

Alternatively, developers seek out geographic "climate havens" - regions with abundant, trapped renewable energy that cannot be easily exported to major population centers. By moving compute-heavy, latency-insensitive AI training workloads to these remote havens, technology companies avoid congested urban grids entirely.

| Scenario | Primary Driver | Grid Impact | Consumer Impact (Retail Rates) | Climate Implication |

|---|---|---|---|---|

| 1. High-Efficiency | Software/Hardware optimization | Manageable integration | Stable utility bills | Neutral to Positive |

| 2. Fossil Lift-Off | Rapid data center build, lagging renewables | Heavy reliance on natural gas and coal | Moderate rate increases | High emissions; fossil lock-in |

| 3. Gridlock | Transmission line bottlenecks | Moratoriums, instability, blackout risks | Stable bills, poor grid reliability | Neutral |

| 4. Ratepayer Shock | Massive utility infrastructure spending | Wholesale capacity market price spikes | Severe utility bill increases | Varies by regional fuel mix |

| 5. Islanded Havens | Off-grid power & geographic relocation | Zero strain on legacy public grids | Stable utility bills | Positive (if nuclear/hydro-powered) |

Regional Case Studies: From Virginia to the Nordics

The impact of AI on the electric grid is not uniformly distributed. Geography dictates destiny, and different regions are experiencing the AI boom through vastly different regulatory, economic, and infrastructural lenses.

Northern Virginia and PJM: The Capacity Crunch

Northern Virginia's "Data Center Alley," primarily located in Loudoun and Fairfax counties, is the densest concentration of digital infrastructure on Earth. Data centers already consume roughly 25% of the total electricity in Virginia, a figure that could rise to nearly 60% by 2030 132846. The sheer concentration of demand is pushing the regional grid operator, PJM, to its physical and economic limits.

PJM projects a peak load growth of 32 gigawatts between 2024 and 2030, explicitly noting that data centers are responsible for 94% of that anticipated increase 21. Because building high-voltage transmission lines generally takes a decade - compared to just two to three years to construct a hyperscale data center - PJM is facing a severe transmission bottleneck 61023. This mismatch between digital ambition and physical wires is the primary catalyst behind the historic 833% price spike in the region's capacity markets 21026. To protect residential ratepayers, Virginia regulators are beginning to mandate that large tech loads pay for a larger share of transmission upgrades, signaling a shift away from traditionally "socialized" grid costs 10.

Texas (ERCOT): The Wild West of Load Growth

Texas is experiencing a similar rush of data center development but operates under a fundamentally different market design. The Electric Reliability Council of Texas (ERCOT) operates an energy-only market decoupled from federal regulation, relying entirely on price signals rather than capacity mandates to ensure grid stability.

Projections show ERCOT could face nearly 51 GW of new, grid-wide demand by 2030, effectively compressing a half-century of historical load growth into a single planning cycle 10. Texas data centers demanded just under 8 GW of power at their peak in early 2025 10. To manage this explosion in demand, ERCOT has identified roughly $14.9 billion in planned transmission projects through 2030 10.

However, power prices in Texas currently sit below the level needed to incentivize major new natural gas generation projects 22. While the state's loose regulatory environment and abundant wind and solar resources attract developers, the sheer scale of the incoming baseload threatens to destabilize a grid that is heavily scrutinized for its vulnerability to extreme weather events 221. Recognizing the risk, the Texas legislature has begun introducing bills aimed at addressing local reliability and affordability concerns 15.

Ireland (EirGrid): Drawing the Regulatory Line

If Virginia and Texas represent largely unconstrained growth, the Republic of Ireland represents aggressive regulatory intervention. Data centers currently consume roughly 21% to 22% of Ireland's total electricity, a figure projected to jump to 31% by 2034 13132. Because the island's grid is physically isolated from the broader European continent, this load growth presents an acute threat to national energy security.

In late 2025, Ireland's Commission for Regulation of Utilities (CRU) finalized a strict new connection policy that fundamentally rewrites the rules for data center expansion. Under the new framework, any new data center seeking to connect to the Irish grid must fulfill two stringent requirements. First, it must provide onsite or proximate dispatchable generation (such as grid-scale batteries or gas plants) that matches its own maximum import capacity, and that capacity must participate in the wholesale electricity market 3233.

Second, within a six-year glide path from energization, the facility must source at least 80% of its annual electricity demand from newly built, additional renewable energy projects located within the Republic of Ireland 315051. Existing renewable generation cannot be used to satisfy this mandate 51. This policy effectively forces data center operators to physically fund and build the grid's green transition rather than simply drawing off existing power, shifting the burden of capacity away from the state and onto the technology sector.

Asia-Pacific: Tight Grids and Efficiency Mandates

In the Asia-Pacific region, dense urban geographies make traditional data center sprawl impossible. The collision between AI compute growth and infrastructure is particularly severe, with APAC electricity consumption for data centers projected to climb from 320 TWh in 2024 to 780 TWh by 2030 33.

In Singapore, severe land and power constraints forced the government to implement a multi-year moratorium on data center approvals. While the moratorium was recently lifted, it was replaced with strict sustainability and efficiency mandates 3352.

Japan and South Korea are similarly constrained by geography and grid limitations. Japan's Ministry of Economy, Trade and Industry (METI) has introduced strict efficiency targets under the Act on Rationalizing Energy Use. The legislation sets a national average PUE limit of 1.4 by 2030 and requires all new data centers built from 2029 onward to achieve a highly efficient PUE of 1.3 5354. Furthermore, the Japanese government is actively pushing a "Watt-Bit Collaboration" strategy, which aims to optimize grid infrastructure by placing data centers near renewable energy hubs rather than in congested urban centers like Tokyo 3435.

In South Korea, data centers use roughly 8 TWh of power, but the grid faces massive structural bottlenecks 58. The country relies heavily on nuclear and coal generation concentrated on the East Coast, while the overwhelming majority of new data center connection requests (up to 70%) are located in the densely populated Seoul metropolitan area 636. Because building a new 345-kilovolt transmission line in South Korea can take up to 13 years due to local opposition and permitting, the state-run utility KEPCO is suffering from severe transmission congestion 637. In response, KEPCO has deployed an AI-driven grid management system to optimize existing transmission lines and is exploring mandates that link new AI data center load growth strictly to verifiable green energy supply 5436.

The Nordics: Europe's AI Climate Haven

As legacy grids in major hubs like Frankfurt, London, Amsterdam, and Dublin face strict constraints, operators are flocking to Northern Europe. Norway, Sweden, and Finland have quietly emerged as the premier "climate havens" for AI infrastructure 6138.

The Nordics offer a highly attractive triad for developers: nearly 100% renewable electricity (anchored by deep, stable hydropower reserves in Norway and Sweden), naturally cool climates that drastically reduce the need for energy-intensive cooling systems, and fast-track permitting processes 396465. A facility in Sweden, for example, can leverage wind power at a fraction of the cost of Western European markets 64. OpenAI selected a remote town in northern Norway to deploy 100,000 GPUs, citing the ability to run the facility entirely on renewable hydroelectricity 3964.

However, the influx of technology giants has sparked domestic debates, and the regulatory environment is tightening. Norway recently implemented comprehensive Data Centre Regulations to monitor the industry, strengthen security, and manage power consumption 40. Furthermore, citing the need for greater efficiency and fairness, Sweden and Norway revoked historical tax subsidies in 2023 that previously gave data centers ultra-low electricity rates, bringing their tax burdens in line with general industrial tariffs 414269. Finland is currently debating a similar move to transition data centers out of lower tax brackets by 2026 4142. Despite these policy shifts, the fundamental advantages of abundant green baseload power keep the Nordics at the forefront of sustainable AI expansion.

The Sustainability Paradox: Greenwashing or Grid Catalyst?

As public scrutiny over AI's immense energy footprint intensifies, major technology companies are eager to assure consumers and regulators that their data centers are sustainable. Claims that facilities are "100% powered by renewable energy" or "carbon matched" are ubiquitous 570. However, the physical reality of how electricity flows through a grid makes these claims highly nuanced, leading to complex debates over corporate "greenwashing."

When a data center operator claims it is powered by renewables, it generally relies on one of three distinct procurement methods:

- Renewable Energy Certificates (RECs): The company buys standard, blended electricity from the local utility grid - which is likely a mix of coal, natural gas, nuclear, and renewables. To offset the carbon emissions on paper, the company purchases RECs, which represent the environmental attribute of renewable energy generated somewhere else 707172.

- Power Purchase Agreements (PPAs): The company funds the construction of a new wind or solar farm that feeds clean power into the general grid. While the data center itself still pulls "dirty" blended power from its local utility, it has added an equivalent amount of clean energy to the broader system over the course of a year 70.

- Behind-the-Meter Sourcing: The company builds a renewable power plant and connects it directly to the data center facility, physically ensuring the electrons consumed onsite are carbon-free 7073.

The vast majority of technology companies rely on RECs and PPAs rather than direct physical sourcing 70. Critics argue that RECs are essentially accounting tools that do not always provide "additionality" - meaning the financial purchase did not necessarily result in a new solar panel being built; it simply subsidized an existing one 717243.

Furthermore, because wind and solar generation are intermittent (dependent on weather and daylight), a data center running 24/7 on a PPA is physically relying on fossil fuel peaker plants at night when renewable generation drops 7073. Even if a company buys enough solar PPAs to cover its total annual volume, its facility is still burning natural gas after sunset.

To solve this discrepancy, leaders in the technology and energy sectors are shifting toward "24/7 carbon-free energy" (CFE) matching. This rigorous standard requires hourly tracking to ensure that every megawatt consumed is matched by a megawatt of clean energy generated on the same regional grid, at the exact same hour 4375. Achieving 24/7 CFE is immensely difficult with only wind and solar, which is why the AI boom is driving the technology industry's massive capital investments into "firm" clean power - notably next-generation geothermal and advanced nuclear reactors, which can provide the constant baseload power AI demands without the carbon footprint of natural gas 251928.

Bottom line

The explosive energy requirements of generative artificial intelligence have fundamentally altered the trajectory of global electricity demand, transforming grid capacity from a background utility into the primary bottleneck for technological supremacy. While AI models hold the potential to eventually optimize grid management and drive profound economic efficiencies, their immediate, concentrated power density threatens to outpace the slow reality of transmission line construction. Navigating this transition will require radical leaps in hardware efficiency, expedited infrastructure permitting, and stringent regulatory frameworks to ensure that the trillion-dollar pursuit of artificial intelligence does not shift the financial burden onto residential ratepayers or derail global decarbonization efforts.