How Could the Future of Nuclear Energy Play Out

The future of nuclear energy will be defined by its ability to power the artificial intelligence revolution and meet global net-zero climate targets while simultaneously overcoming a legacy of massive capital cost overruns. Depending on technological breakthroughs and government policies, the industry could experience a tech-financed renaissance of old plants, transition to mass-produced small modular reactors, or face stagnation driven by increasingly cheap renewable energy. Ultimately, the successful scaling of domestic supply chains and a highly skilled workforce will determine which of these futures materializes.

The Nuclear Crossroads: Re-evaluating the Atom

For decades, nuclear power existed in a state of suspended animation across much of the Western world. High-profile disasters at Chernobyl and Fukushima, coupled with the staggering cost overruns of modern construction projects, led many nations to phase out their nuclear fleets. However, the mid-2020s have brought a dramatic paradigm shift. Driven by the urgent need to decarbonize the global economy and the sudden, ravenous energy appetite of artificial intelligence, governments and private markets are giving nuclear energy a second look.

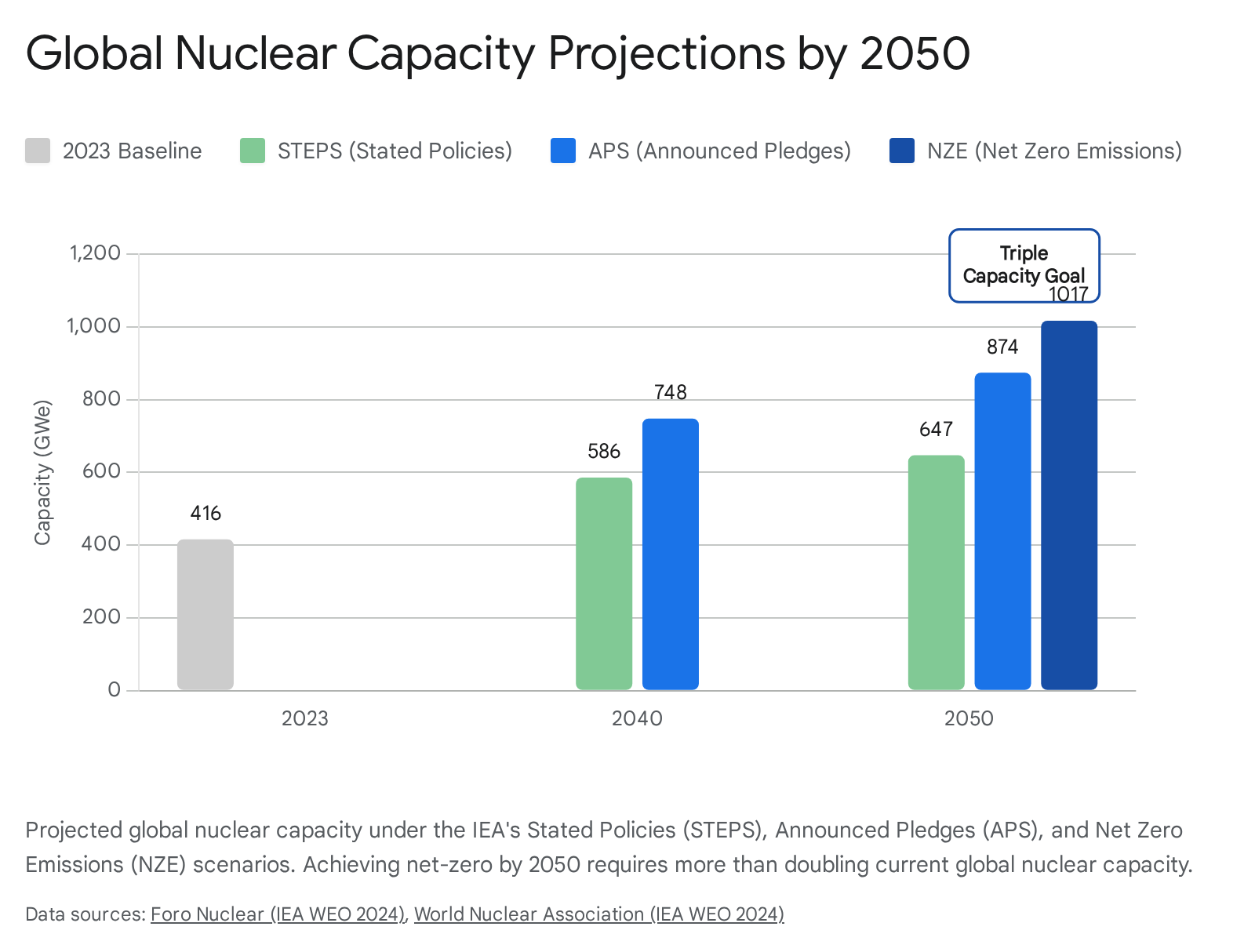

In 2023, global nuclear generating capacity stood at approximately 416 gigawatts electrical (GWe) 1. Yet, the International Energy Agency (IEA) and the global community at the COP28 climate summit recognized that achieving net-zero emissions will likely require tripling that capacity by 2050 112.

The Urgent Need for Baseload Power

Achieving this expansion is an unprecedented infrastructural challenge. Nuclear plants provide unmatched baseload reliability - operating at full capacity over 93% of the time in the United States, compared to around 36% for wind and roughly 24% for solar 34. They also require significantly less land; nuclear plants use approximately 10 hectares per terawatt-hour (TWh) of electricity produced, whereas wind uses about 100 hectares and solar can require over 1,000 hectares 3. Despite these advantages, modern light-water reactors take years to build and routinely exceed their budgets, making commercial lenders hesitant to assume the financial risk 15.

As the world wrestles with the dual challenges of climate change and technological acceleration, the future of nuclear energy is fracturing into several distinct possibilities. To understand where the industry is heading in the coming decades, we must explore five highly debated scenarios.

Scenario 1: The AI and Tech-Driven Nuclear Renaissance

The most immediate and disruptive force shaping the short-term future of nuclear energy is the explosive growth of artificial intelligence. The expansion of generative AI, large language models (LLMs), and autonomous systems requires a staggering amount of computing power, fundamentally altering global electricity forecasts.

The Staggering Energy Footprint of AI

Data centers are the physical engines of the digital economy. While they have historically grown in efficiency alongside their energy consumption, the advent of AI is breaking that equilibrium. Global electricity generation to supply data centers is projected to grow from roughly 460 TWh in 2024 to 945 TWh by 2030 in the IEA's base case scenario, representing a doubling of demand that will roughly equal the entire current electricity consumption of Japan 678. Under more aggressive "Lift-Off" models, data center electricity demand could surge to nearly 2,000 TWh by 2035, while highly efficient scenarios might curb that growth by 20% 67.

The carbon intensity of this computing boom is severe. A single query to an advanced AI chatbot produces roughly 100 times the carbon emissions of a standard search engine query 9. In 2024, AI-specific servers within the United States used an estimated 53 to 76 TWh, a figure expected to reach 165 to 326 TWh by 2028 10. Currently, fossil fuels provide nearly 60% of the power to data centers globally, with renewables covering 27% and nuclear at 15% . If tech companies rely on local grids powered heavily by coal or natural gas, the emissions generated by the AI sector could eventually rival global aviation. Currently, AI workloads produce an estimated 20 to 40 million tonnes of CO2 equivalent annually compared to aviation's 710 million tonnes, but AI emissions are growing at roughly 15% per year versus aviation's 7% to 8% .

Tech giants - including Microsoft, Google, Amazon, and Meta - have made aggressive corporate pledges to reach net-zero emissions. However, the intermittent nature of renewable energy makes it exceedingly difficult to power a data center that must run without interruption. Nuclear energy has thus emerged as the ideal solution for the tech sector 11.

The Race to Recommission Decommissioned Fleets

This desperation for clean, firm power has led to unprecedented market actions: the recommissioning of closed nuclear plants. In the United States, two major projects currently represent this profound shift.

The Palisades Nuclear Plant in Covert Township, Michigan, ceased operations in May 2022 after more than 50 years of service, primarily due to an inability to compete economically with cheap natural gas and renewables 121314. Holtec International originally purchased the facility for decommissioning. However, recognizing the shifting market, Holtec reversed course. Supported by a $1.52 billion loan guarantee from the U.S. Department of Energy (DOE) finalized in September 2024, Palisades is currently undergoing the first recommissioning of a retired nuclear plant in U.S. history 121314.

The Palisades Restart Process and Challenges

The restart process is complex, expensive, and heavily regulated. By the spring of 2026, Holtec had successfully completed the "passivation" of the primary system - a chemical process that brings the reactor to normal operating temperature and pressure to improve corrosion resistance and allow for precise control of water chemistry 1516. This followed a first-of-its-kind comprehensive system cleaning that significantly reduced radiation dose rates in sensitive areas of the plant 16.

While originally slated for a late 2025 restart, ongoing equipment testing, regulatory oversight, and the sheer logistical complexity of the refurbishment have pushed the anticipated commercial operation date to early 2026 1419. The 805-MW plant has already received delivery of 68 new nuclear fuel assemblies, preparing for eventual fuel loading once the final inspections of the steam generator tubes and pressure boundary welds are authorized by the Nuclear Regulatory Commission (NRC) 141516.

Three Mile Island's Transformation to the Crane Clean Energy Center

An even more dramatic example of tech-funded revival is the Crane Clean Energy Center in Pennsylvania. In September 2024, Constellation Energy announced a 20-year power purchase agreement with Microsoft to restart Unit 1 of the former Three Mile Island nuclear plant, which had been retired for economic reasons in 2019 2017. Backed by a $1 billion DOE loan finalized in November 2025, the 835-MW project aims to restore carbon-free energy directly to the regional grid to offset Microsoft's AI infrastructure 1819.

However, this restart faces modern infrastructural hurdles. In early 2026, the PJM Interconnection grid operator warned that transmission constraints and backlogs could delay the Crane restart from its planned 2027 date until 2031 20. To bypass this bureaucratic bottleneck, Constellation petitioned the Federal Energy Regulatory Commission (FERC) to transfer existing capacity interconnection rights from its older, fossil-fueled Eddystone plant directly to the Crane site, aiming to use existing grid capacity without triggering lengthy new interconnection studies 202122.

If Scenario 1 holds, the future of nuclear energy will be intrinsically linked to the tech sector. Hyperscalers will finance the modernization of the existing fleet, extend the lifespans of current reactors to 60 or 80 years, and drive the co-location of data centers directly adjacent to nuclear facilities 410.

Scenario 2: The Global Shift to the East and the Global South

Historically, the United States and Europe have dominated the civilian nuclear energy landscape. However, Scenario 2 envisions a future where the center of gravity permanently shifts to Asia and emerging markets. This transition is already well underway, driven by differing geopolitical priorities and state-backed financing models.

China and India's Aggressive Buildouts

China and India are currently executing the largest nuclear expansion programs in history, driven by an urgent need for energy security, air quality improvements, and the rapid industrialization of their economies.

China's policy has been decisively pro-nuclear. Under its 15th Five-Year Plan (2026 - 2030), the Chinese government targeted an ambitious 110 GW of installed nuclear power capacity by 2030 - a staggering 76% jump from its capacity at the end of 2025 22324. While industry analysts at the World Nuclear Association note that domestic construction timelines of five to seven years might push the actual realization of this 110 GW target a few years past the 2030 deadline, the momentum is undeniable 24. China is currently the home to just under half of the world's nuclear reactors under construction 2. By the end of the decade, China is expected to overtake both the United States and France as the world's largest producer of atomic power 24. Furthermore, China is prioritizing advanced domestic reactor deployment, including the planned rollout of 8 GW of fast neutron reactors (such as the CFR-600 and CFR-1000) by 2030 2.

India is matching this ambition, viewing nuclear power as a strategic hedge for energy security 23. The Indian government aims to hit the 100 GW mark by 2047, coinciding with its 100th year of independence 23. With 24 operable reactors and eight more under construction in recent years, India's nuclear fleet is projected to more than double its baseline capacity to 20 GW by the early 2030s 23.

Exporting Technology and the Belt and Road Initiative

In this scenario, Western nations may lose their competitive edge in nuclear technology exports. As China successfully mass-produces reactors domestically, keeping costs relatively controlled compared to Western budget overruns, it is positioning itself to export this technology globally. Through initiatives like the Belt and Road Initiative, China is securing long-term technological and diplomatic influence 224. For instance, China National Nuclear Corporation has already signed agreements with the Algerian Atomic Energy Commission to cooperate on nuclear energy and research reactors, setting the stage for deeper integration 25.

Emerging Markets Exploring Nuclear Power

Beyond the established giants, a wave of emerging economies in Southeast Asia, the Middle East, and Africa are actively pursuing nuclear programs to power their urbanization and mitigate their reliance on imported fossil fuels.

In Southeast Asia, the ASEAN region is closely evaluating the technology. Vietnam has advanced plans for its first nuclear plant following bilateral agreements with Russia, while Singapore has participated in International Atomic Energy Agency (IAEA) reviews to gauge its ability to safely adopt nuclear power 23. In Sub-Saharan Africa, Kenya signed agreements with the Korea Electric Power Corporation (KEPCO) for feasibility studies, targeting an eventual 1,000 MWe of nuclear capacity to reduce electricity prices and enable cross-border exports in the Eastern Africa Power Pool 25.

Scenario 3: The SMR and Advanced Reactor Breakthrough

Perhaps the most discussed future scenario is the commercial triumph of Small Modular Reactors (SMRs) and advanced microreactors. If traditional nuclear plants are custom-built "Eiffel Towers," SMRs are designed to be "Broadcast Towers" - standardized, factory-built, and modular 5.

Overcoming the "Eiffel Tower" Problem with Modularity

The primary deterrent to traditional large-scale light-water reactors is their colossal upfront capital requirement and the extreme financial risk of construction delays. The overnight construction cost (OCC) of a conventional nuclear plant in the West averages around $6,600 per kW 5. Projects like the UK's Hinkley Point C have ballooned to an estimated £34 billion (roughly $20,000 per kW), and similar overruns have plagued the Vogtle plant in the U.S. and Flamanville in France 526.

SMRs aim to solve this by shifting construction from the field to the factory. Because they are smaller (typically producing 300 MW or less), they can be assembled on a manufacturing line, transported by truck or rail, and installed in series. This unlocks the "economics of mass production."

The Complexities of the Levelized Cost of Electricity

The economic viability of SMRs is heavily debated. According to energy analytics, while a "first-of-a-kind" (FOAK) SMR might carry a high levelized cost of electricity (LCOE) of around $180/MWh, scaling up production to "nth-of-a-kind" (NOAK) units could reduce that LCOE by 40% to $100/MWh by 2030 27. Some open-source blueprints suggest an SMR could be built in 1.5 years at a capital cost of $2,901/kW, yielding a highly competitive LCOE of $36/MWh 28.

Crucially, shorter build times dramatically reduce the accumulated interest on financing. For example, assuming a 5% interest rate, a conventional plant taking 15 years to build will accrue significantly more debt than an SMR built in 5 years. Consequently, even if an SMR has a higher initial sticker price of $10,000 per kW, the total capitalized cost comes out lower than a conventional plant due to the reduced accumulation of interest 5.

Executive Orders and the Push for Domestic Supply Chains

The leap from theory to commercial reality is accelerating. The U.S. government has subsidized this transition through a series of Executive Orders in 2025, including EO 14301 and EO 14299, which established a pilot program aiming to have at least three advanced reactors achieve criticality by mid-2026 2934. The government has also utilized the Defense Production Act to secure the nuclear fuel supply chain, focusing on the processing and enrichment of High Assay Low Enriched Uranium (HALEU), which is required for many next-generation designs 2930.

In tandem with recommissioning older plants, companies are using existing sites for SMR deployment. Holtec, for instance, plans to deploy two SMR-300 units (Pioneer-1 and -2) at the Palisades site by the early 2030s, backed by a $400 million DOE matching grant 15. If this scenario prevails, nuclear power becomes decentralized. SMRs will be co-located with industrial hubs, directly powering energy-intensive data centers, desalination plants, and heavy manufacturing 2731.

Scenario 4: High-Cost Stagnation and the Renewables Squeeze

A rigorous analysis of the future must account for the possibility of stagnation. In this scenario, despite ambitious policy targets and public enthusiasm, the nuclear renaissance is suffocated by its own economics and outpaced by the relentless cost declines of wind, solar, and advanced battery storage.

The Brutal Reality of LCOE and Renewable Competition

When analyzing energy markets, the LCOE is the ultimate baseline metric. According to global energy reports, the LCOE for utility-scale solar PV and onshore wind has plummeted over the last decade. In 2023, solar PV was estimated to cost around $55/MWh and is expected to decline to $25/MWh by 2050 32. Wind energy costs similarly hover between $35 and $40/MWh 32.

By contrast, the LCOE for advanced nuclear power remains stubbornly high. Various analyses place nuclear LCOE anywhere from $110/MWh to as high as $252/MWh for large-scale implementations 42632. Research bodies like the CSIRO in Australia have frequently cited these figures to argue that nuclear power is simply too expensive compared to firmed renewables 4. This makes nuclear power, in raw generation terms, significantly more expensive than modern solar and wind installations.

Intermittency vs. System Cost Debate

Proponents of nuclear energy correctly point out that traditional LCOE models fail to account for the "system costs" of managing intermittent renewables. Because the sun does not always shine and the wind does not always blow, a grid heavily reliant on renewables requires massive overbuilding of generation capacity, extensive transmission network expansions, and highly expensive utility-scale battery storage to balance the load 3238.

For example, to equal the sheer electrical output of a standard 900-MW nuclear reactor operating at a 93% capacity factor, a utility would need to build nearly 800 average-sized land-based wind turbines or roughly 8.5 million solar panels 3. Furthermore, building renewables requires significantly more geographic footprint. Solar requires about 1,000 hectares per TWh of electricity produced per year, and wind uses about 100 hectares, compared to nuclear's minimal footprint of just 10 hectares per TWh 3.

When Innovation Fails to Scale

However, in the "High-Cost Stagnation" scenario, energy storage technology advances faster than nuclear construction. If long-duration energy storage - such as iron-air batteries or second-life EV microgrids - becomes commercially viable and cheap, the "dispatchability" premium of nuclear power vanishes 33. If SMRs fail to achieve cost parity, suffer from the same regulatory delays as traditional megaprojects, and remain stuck in the FOAK (first-of-a-kind) cost phase, private investors will inevitably flee to the safer, faster returns offered by solar, wind, and storage. In this future, nuclear remains a vital but stagnant niche, utilized only where geography strictly prohibits renewables.

Scenario 5: The Net-Zero Coordinated Global Buildout

The final scenario represents the realization of the international community's most ambitious climate goals. In this future, the target set by the Net Zero Nuclear initiative at COP28 - to triple global nuclear capacity by 2050 - is actually achieved, pushing global capacity beyond 1,000 GWe 112.

The Policy Engine and Regulatory Overhaul

Tripling global capacity from roughly 416 GW to 1,200 GW in 25 years requires a wartime level of industrial mobilization. Free markets alone will not achieve this due to the immense risk profiles of nuclear financing; long timelines for permitting and construction can push the breakeven point for commercial lenders to 20 or 30 years after project initiation 1. Instead, this scenario relies on massive, sustained government intervention, regulatory reform, and international supply chain coordination.

The United States has attempted to provide a blueprint for this mobilization. Executive Orders aimed to facilitate 5 gigawatts of power uprates to existing nuclear reactors and begin construction on ten new large reactors by 2030 2934. These directives force agencies to reform nuclear reactor testing, expedite the licensing process, and treat AI data centers paired with DOE nuclear facilities as critical defense infrastructure 29.

Empowering the Local Community and Workforce

Scaling up to this degree will fundamentally reshape the energy labor market. Unlike many renewable energy installations, which require a large upfront labor force but minimal long-term operational staff, nuclear plants require thousands of highly skilled, permanent workers.

In the U.S., the nuclear sector employed approximately 67,900 workers in 2024, with high median salaries across the board - nuclear engineers ($127,520) and reactor operators ($122,610) rank among the highest in the electric power generation sector 35. Globally, a massive expansion would create millions of jobs. France's current nuclear sector alone supports 220,000 workers, offering stable careers for technicians and engineers 36. When integrated into local economies, these facilities serve as cornerstones of community growth; for example, Canada's Bruce Nuclear Generating Station provides over 4,000 direct jobs and revitalizes the local economy 36.

Managing the Global Nuclear Fuel Cycle

However, achieving the Net-Zero scenario requires solving a severe talent and supply chain bottleneck. In 2024, 63% of U.S. manufacturing employers in nuclear power generation reported that hiring was "very difficult" 35. A global tripling of capacity will require an unprecedented push in STEM education, vocational training for welders and electricians, and cross-industry talent placement (such as transitioning workers from aerospace or oil and gas into the nuclear sector) 3135.

Furthermore, nations must navigate the complexities of the nuclear fuel cycle. Expanding uranium processing, managing spent nuclear fuel, and developing advanced fuel recycling capabilities are prerequisites for a sustainable, century-long buildout 2930. If governments can solve these financing and labor roadblocks, nuclear energy will serve as the indispensable backbone of a fully decarbonized global economy.

Summary of Nuclear Future Scenarios

| Scenario | Primary Drivers | Key Geographical Focus | Technological Focus | Anticipated 2050 Outcome |

|---|---|---|---|---|

| 1. AI & Tech Renaissance | Hyperscaler data center demand, tech capital, PPA agreements. | United States, Europe (Tech Hubs). | Plant restarts, lifetime extensions, co-located microreactors. | Nuclear becomes a privatized baseload utility for the digital and AI economy. |

| 2. Global East & South Shift | Energy security, industrialization, state-backed financing. | China, India, MENA, ASEAN. | Domestic fast-neutron reactors, Belt & Road nuclear exports. | China and India dominate global capacity; Western influence diminishes. |

| 3. SMR Breakthrough | Economies of mass production, factory assembly, modularity. | Global (flexible deployment). | Small Modular Reactors (SMRs), advanced fuels (HALEU). | Cost parity achieved; decentralized reactors deployed directly at industrial sites. |

| 4. High-Cost Stagnation | Capital cost overruns, cheap solar/wind/batteries, regulatory lag. | Western Economies (stagnating). | Legacy Light-Water Reactors (managing decline). | Nuclear fails to scale; capacity barely maintained as renewables dominate the grid. |

| 5. Net-Zero Coordination | Climate change mandates, massive state subsidies, global treaties. | Global (Coordinated). | Fleet-wide expansion, Next-Gen reactors, supply chain integration. | Global capacity triples to >1,000 GWe; nuclear serves as the backbone of a decarbonized world. |

Bottom line

The future of nuclear energy is no longer a tale of inevitable decline, but rather a complex race against surging energy demands and competing technologies. Buoyed by the immense power needs of AI data centers and global climate targets, nuclear power has an unprecedented opportunity to scale through tech-funded plant restarts and the commercialization of Small Modular Reactors. However, if the industry cannot overcome its historic legacy of exorbitant capital costs, supply chain bottlenecks, and sluggish construction timelines, it risks being sidelined by the relentless economic efficiency of wind, solar, and advanced battery storage.