Will AI Data Centers Raise Your Summer Power Bill in 2026

The Short Answer

Yes, artificial intelligence data centers are structurally poised to raise summer electricity bills in 2026, though the severity of the impact will be fiercely mediated by geographic location and local utility regulation. The proliferation of hyperscale computing has triggered a historic surge in wholesale electricity capacity prices, most starkly illustrated by an 833% price shock in the PJM Interconnection mid-Atlantic grid for the 2025/2026 delivery year, followed by another auction that hit the absolute regulatory price ceiling for 2026/2027 1214. While wholesale capacity costs represent only a fraction of a residential utility bill, the massive infrastructure upgrades required to support AI are inevitably exerting upward pressure on retail base rates. Consumers in high-density regions like Virginia, Ohio, and Texas are currently facing utility requests for substantial base rate increases to fund new power plants and transmission lines 523. However, public utility commissions are increasingly stepping in to mandate strict, multi-year "take-or-pay" tariffs designed to force tech conglomerates to shoulder their own infrastructure costs, aiming to shield everyday residential ratepayers from subsidizing the artificial intelligence boom 456.

The Everyday Hook: From Pixel Generation to Peak Load

To conceptualize the computational weight of modern convenience, consider the energy required for routine digital tasks. A standard internet search utilizes a mere fraction of a watt-hour of electricity, operating virtually unnoticed by the broader electrical grid. Conversely, generating a single high-definition image using a generative artificial intelligence model or querying a large language model can consume ten times the energy of a traditional search 411. When this energy intensity is scaled globally to process billions of requests per minute, the power requirements cease to be abstract. A single hyperscale AI data center requires a constant, unyielding power draw ranging from 100 to 300 megawatts, with some planned campuses projecting needs in the gigawatt range 21213.

To place that demand into an everyday perspective, powering a single modern AI data campus is the equivalent of turning on the central air conditioning units in up to 300,000 homes simultaneously on a sweltering afternoon in late July, and leaving them running twenty-four hours a day, three hundred and sixty-five days a year 7. Unlike residential cooling, which typically peaks around 5:00 PM as residents return from work and subsides by midnight, an AI data center exhibits a completely flat baseload profile. It demands its maximum power allocation regardless of the hour, the seasonal weather patterns, or the real-time strain on the broader electrical grid. This insatiable, round-the-clock consumption is currently colliding with an aging electrical grid, setting the stage for one of the most profound and contentious energy pricing shifts of the modern era.

FAQ 1: Are AI Data Centers Actually Consuming That Much Power?

To accurately gauge the impending impact on retail electricity bills, one must first quantify the sheer scale of the macroeconomic demand shock currently unfolding across the United States. For nearly two decades, the American electrical grid operated in a paradigm of relatively flat demand growth. Despite population increases and economic expansion, advancements in energy-efficient technologies - such as the widespread adoption of LED lighting - and the steady off-shoring of heavy industrial manufacturing kept domestic electricity consumption remarkably stable 8169. That era of stability has definitively ended.

According to the United States Energy Information Administration's (EIA) May 2026 Short-Term Energy Outlook, total national electricity consumption is surging to unprecedented record highs. The agency projects that domestic power demand will rise to 4,193 billion kilowatt-hours in 2025 and reach 4,283 billion kilowatt-hours by 2026, marking a fundamental structural shift in how the nation consumes energy 810. Within this broader acceleration, the internal dynamics of energy consumption are shifting dramatically. For the first time in recorded history, the EIA projects that commercial electricity demand - the sector that physically houses data centers - will outpace residential electricity demand by 2027 1911. The commercial sector is expected to see electricity sales grow by 2.2% to approximately 1,530 billion kilowatt-hours in 2026, followed by a staggering 5.3% growth the subsequent year, largely driven by the infrastructure demands of cloud computing and artificial intelligence 11. Data centers, which historically consumed roughly 4% to 5% of total U.S. electricity, are currently on a trajectory to consume up to 8.6% by 2035, with some projections estimating they could account for as much as 12% of total national electricity consumption by the end of the decade 47812.

The primary catalyst for this unprecedented growth is the fundamentally distinct architecture required for artificial intelligence computing compared to traditional cloud storage. Training complex large language models requires tens of thousands of specialized accelerators operating in massive parallel clusters at maximum thermal capacity for months at a time 1312. The training phase alone for a model like GPT-4 required an estimated 30 megawatts of continuous power 12. Furthermore, once a model is trained, the "inference" phase - where the model actively answers user queries and generates content - proves to be equally power-hungry. As these models transition from development to ubiquitous deployment across enterprise software, search engines, and consumer applications, inference workloads are expected to consume two-thirds of all AI computing power in 2026, transforming episodic training demands into continuous, escalating baseload requirements 11.

The Broad Scope: Compounding Factors and the Megawatt Footprint

While artificial intelligence has captured the bulk of public imagination and regulatory scrutiny, it is crucial to recognize that the physics of the power grid do not distinguish between different sources of electron demand 22. The surge in AI data center construction is occurring simultaneously with a suite of other massive electrification trends, creating a compounding, multiplier effect on both generation and transmission infrastructure. Electric vehicle adoption, the reshoring of semiconductor and battery manufacturing, and the stubborn persistence of cryptocurrency mining are all vying for capacity on the exact same constrained grid 910.

Cryptocurrency mining, particularly the Bitcoin network, remains a formidable consumer of electricity. As of mid-2026, the global Bitcoin network's annual electricity consumption is estimated to range between 145 and 171 terawatt-hours, representing roughly 0.5% of total global electricity production - a figure comparable to the annual consumption of entire industrialized nations like Poland or Argentina 111324. Simultaneously, the electrification of the mobility sector is adding significant load. The United States electric vehicle fleet consumed approximately 24 terawatt-hours of electricity for charging in 2025, a figure that is doubling annually as adoption curves steepen and fleet operators electrify their logistics networks 22.

However, when analyzing the impact on grid stability and wholesale pricing, the critical distinction between these competing technologies lies in their load flexibility. An electric vehicle represents a highly flexible load; it can be programmatically instructed to charge at 2:00 AM when regional wind energy is abundant and overall grid demand is at its absolute lowest 22. Similarly, a Bitcoin mining operation represents an economically elastic load. Miners can be contractually incentivized by grid operators to power down their specialized ASIC rigs within seconds during a severe summer heatwave, providing vital demand response to ease grid strain in exchange for financial compensation 13.

An artificial intelligence data center, by contrast, is an entirely different asset class. These facilities represent multi-billion-dollar capital investments filled with highly sensitive, incredibly expensive GPU clusters that require continuous, maximum utilization to justify their staggering upfront costs and remain economically viable 1113. They are structurally inflexible, requiring "firm" baseload power that the regional grid must supply without interruption, regardless of localized grid emergencies, heatwaves, or the intermittency of renewable energy generation 25. This inflexibility forces utility planners to build dedicated, dispatchable generation - often natural gas peaker plants - specifically to back up these facilities, driving up system-wide costs.

| Sector / Technology | Estimated Global Electricity Footprint (TWh) | Typical Load Flexibility | Key Drivers of Future Growth |

|---|---|---|---|

| All Global Data Centers (Including AI) | 620 - 1,050 TWh (2026 Base Case) 1126 | Low to Moderate | Hyperscale cloud expansion, 5G network rollouts, enterprise digitalization. |

| Dedicated AI Workloads (Training & Inference) | 80 - 400+ TWh (2026 Estimate) 1113 | Very Low | Advanced LLMs, continuous generative inference, corporate AI integration. |

| Cryptocurrency Mining (Bitcoin) | 138 - 171 TWh (2025/2026 Estimate) 1124 | Very High | Network hashrate difficulty, underlying asset price, specialized ASIC efficiency. |

| Electric Vehicle (EV) Charging (U.S. Only) | ~24 TWh (2025 Estimate) 22 | Very High | Consumer adoption incentives, commercial fleet electrification, charging infrastructure buildout. |

| Total U.S. Commercial Sector (2026 Forecast) | ~1,530 TWh (Total Sector Sales) 1113 | Moderate | Data center integration, commercial space cooling, office building electrification. |

FAQ 2: What is the Difference Between Capacity Markets and Energy Markets?

To fully grasp the mechanics of how a hyperscale data center opening in a neighboring county can aggressively inflate a residential electricity bill, it is essential to demystify the underlying structure of wholesale electricity pricing. The United States power grid does not operate as a single unified entity; rather, it functions through a patchwork of regional independent system operators and regional transmission organizations. These highly complex organizations generally manage two distinct but deeply symbiotic financial ecosystems: the Energy Market and the Capacity Market 1415.

The fundamental distinction between these two markets can be effectively understood through the real-world analogy of modern telecommunications and cellular phone plans.

The Energy Market is the direct equivalent of a strict pay-as-you-go minutes plan. In this market, power generators - whether they operate natural gas combined-cycle plants, sprawling wind farms, or nuclear facilities - are compensated strictly for the actual, tangible electricity they successfully generate and inject into the grid on a minute-by-minute, day-by-day basis to meet immediate consumer demand 153031. The metric of commerce here is the megawatt-hour. If a power plant sits idle because the sun is shining brightly and cheaper solar power is flooding the grid, that idle plant receives absolutely no revenue from the energy market for that specific hour 30.

The Capacity Market, conversely, functions much like a fixed monthly data subscription or a professional retainer fee. It is a forward-looking financial mechanism designed exclusively to guarantee long-term grid reliability 1633. In a capacity market, generators are paid a substantial fixed fee simply for the ironclad promise that they will be available to produce power three years in the future, particularly during critical peak hours or unforeseen grid emergencies 143016. Returning to the telecommunications analogy, a capacity market ensures that the cellular network operator has constructed enough physical towers to handle the absolute maximum volume of phone calls that might occur on New Year's Eve, providing a financial return on those towers even if they sit largely unused for the remaining three hundred and sixty-four days of the year 30.

Capacity markets were engineered to solve the persistent "missing money" problem inherent in energy-only deregulated markets. The revenues generated purely from selling day-to-day electricity in the energy market are frequently insufficient to convince private investors to risk billions of dollars constructing a new power plant, especially "peaker" plants that might only be economically dispatched for a few dozen hours during the hottest days of summer 3031. By participating in competitive capacity auctions, a power plant owner secures a guaranteed, steady income stream that covers their fixed capital costs, debt servicing requirements, and ongoing maintenance overhead 3016.

When retail utility companies - the entities that send the monthly bill to residential homes - purchase power on behalf of their localized customers, they do not just pay for the physical electrons consumed. They are legally required by the grid operator to purchase a proportional share of the entire region's capacity costs 14. These aggregated, socialized capacity charges are then blended with the energy costs, transmission fees, and distribution charges, ultimately passing down to the retail consumer. Therefore, when the cost of securing future reliability skyrockets due to constrained supply and unprecedented data center demand, every single ratepayer in that grid territory absorbs a fraction of that financial shock.

FAQ 3: Why Are Wholesale Capacity Prices Spiking Unprecedentedly Right Now?

The prevailing public narrative that "artificial intelligence is breaking the grid" is a vast oversimplification of a deeply complex infrastructural reality. Artificial intelligence is merely the ultimate accelerator; the physical grid was already speeding toward a structural bottleneck years before the current generative AI boom. The unprecedented price spikes recently observed in wholesale capacity markets - most notably the historic 833% increase in the PJM Interconnection, which manages the grid for thirteen states stretching from Illinois to New Jersey - are the result of a "perfect storm" of compounding, systemic failures 121718.

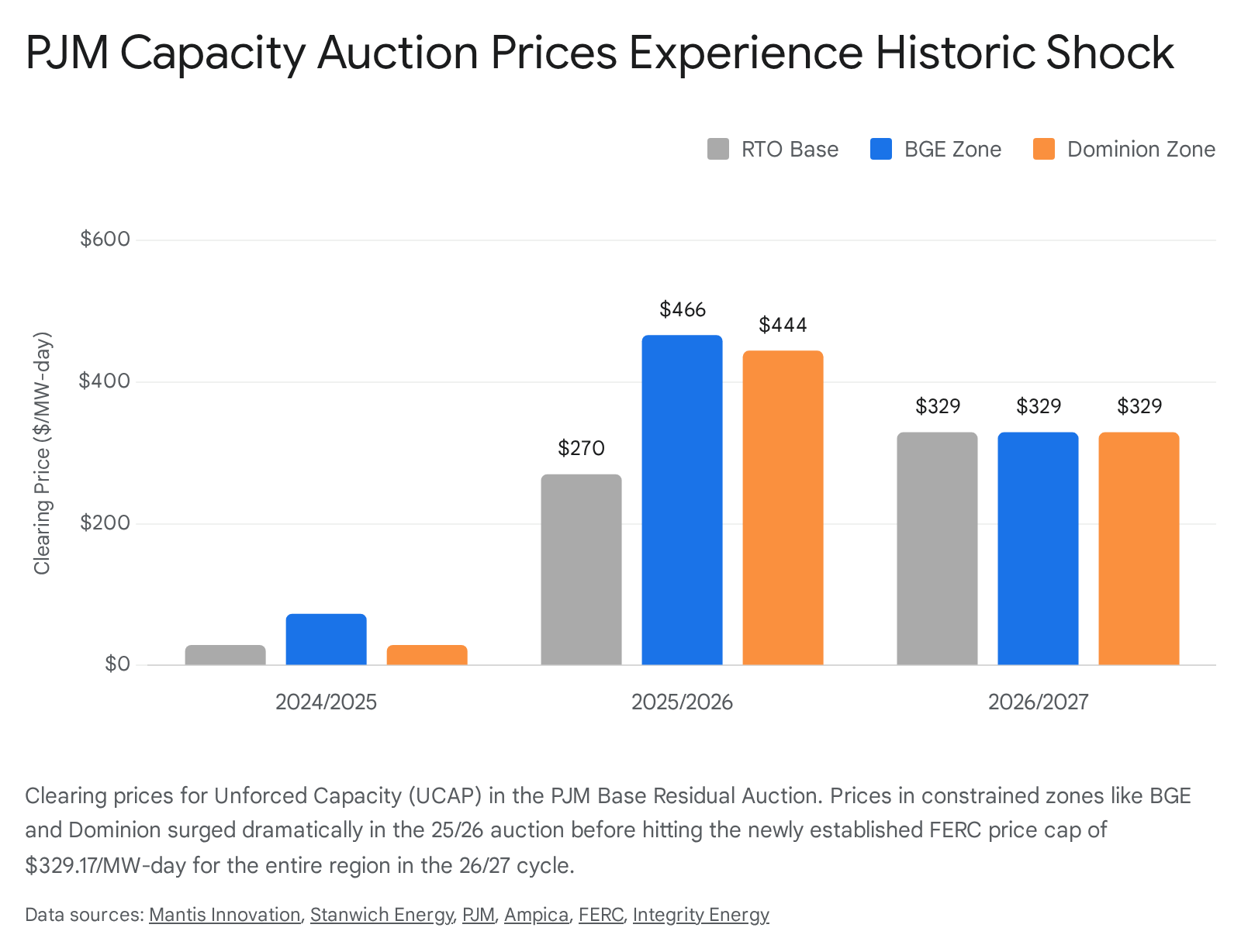

The PJM Base Residual Auction is the primary mechanism through which the region secures power supplies three years in advance of the delivery date. For the 2024/2025 delivery year, the baseline capacity clearing price across the vast majority of the regional footprint was a mere $28.92 per megawatt-day 117. This low price reflected a historical period of abundant legacy supply and stagnant load growth. However, when the auction results for the 2025/2026 delivery year were released, the baseline price had exploded to $269.92 per megawatt-day across the broader region 11736. Even more alarming were the results in deeply constrained geographic zones facing massive, concentrated data center build-outs. These specific zones exhausted all cheap supply and hit their absolute maximum zonal price caps. The Baltimore Gas and Electric zone cleared at an astonishing $466.35 per megawatt-day, while the Dominion zone - which serves the hyperscale epicenter of "Data Center Alley" in Northern Virginia - hit $444.26 per megawatt-day 1361920.

The situation deteriorated further in the subsequent auction. For the 2026/2027 delivery year, after federal regulators intervened to establish a pricing collar to prevent total market failure, prices hit the newly established hard cap of $329.17 per megawatt-day across the entire PJM footprint, representing yet another 22% rate hike over the already elevated regional baseline 2139.

This multi-billion-dollar upward shift in wholesale capacity costs is driven by four intersecting, systemic crises operating simultaneously.

First, the grid is experiencing an unprecedented wave of generator retirements. Driven by increasingly stringent environmental regulations, aggressive state-level decarbonization mandates, and the unfavorable operating economics of legacy facilities in previous low-price environments, older fossil-fuel plants - primarily coal and less efficient natural gas units - are being systematically deactivated at a pace that vastly exceeds new construction. In the PJM 2025/2026 auction alone, approximately 6,600 megawatts of generation resources either formally retired or utilized must-offer exceptions signaling their immediate intent to retire, completely removing their capacity from the available pool 117. The grid is hemorrhaging reliable, dispatchable baseload power precisely when it needs it most. While the massive price spikes have convinced a small fraction of these plants to withdraw their deactivation notices - specifically 17 generating units totaling approximately 1,100 megawatts following the 2025/2026 auction - the overall trend of legacy asset retirement remains severe 1.

Second, grid operators are grappling with exploding, highly concentrated demand forecasts. Driven by the clustering of AI data centers, the aggressive reshoring of industrial manufacturing, and policy rules forcing the rapid electrification of building heating and transportation fleets, regional peak load forecasts are being revised upward at historic rates. PJM, for instance, increased its projected peak load requirement from 150,640 megawatts for the 2024/2025 delivery year to 153,883 megawatts for the 2025/2026 delivery year, a massive single-year jump 117. When massive tranches of supply are forcibly removed from the market at the exact moment that structural demand spikes vertically, the ruthless mechanics of competitive auctions dictate that clearing prices must skyrocket to incentivize the rapid construction of new generation 417.

Third, federal regulators have implemented sweeping market reforms designed to enforce strict extreme weather modeling. Following catastrophic, systemic grid failures during severe weather events such as Winter Storm Uri and Winter Storm Elliott, the Federal Energy Regulatory Commission approved comprehensive market overhauls requiring grid operators to implement deeply conservative reliability risk models 11736. All capacity resources - including wind, solar, batteries, and even traditional natural gas plants - are now subject to rigorous accreditation standards. This means their theoretical "nameplate" megawatt capacity is deeply discounted based on their statistically proven ability to actually perform and deliver power during extreme weather events when fuel lines might freeze or wind might cease. This administrative "tightening" of the supply balance, while necessary for grid resilience, functionally removed thousands of megawatts of paper capacity from the market, further driving up scarcity prices 1736.

Finally, the grid is paralyzed by catastrophic interconnection queue delays. Even with record-high capacity price signals theoretically screaming for new investment and offering massive financial returns, developers cannot simply plug a newly constructed solar farm, battery array, or gas peaker plant into the physical transmission network. Regional interconnection queues are hopelessly backlogged, burdened by global supply chain bottlenecks for critical components like high-voltage transformers, localized permitting disputes, and the necessity of highly complex, years-long engineering studies to ensure that new additions do not destabilize the existing network 181920. If new capacity cannot physically connect to the grid, the underlying supply scarcity persists unchecked, ensuring that prices remain artificially elevated for the foreseeable future.

FAQ 4: How Do Data Centers Specifically Affect My Local Regional Grid?

The impact of hyperscale AI data center load is decidedly not distributed evenly across the United States. It is a highly localized phenomenon, governed by a complex matrix of state tax incentives, fiber optic corridor access, available land, and the radically divergent market designs implemented by various regional grid operators 16. Consequently, the financial risk to the residential ratepayer manifests completely differently depending on the state.

PJM Interconnection (The Mid-Atlantic & Rust Belt)

The PJM Interconnection remains the undisputed epicenter of the global data center capacity crisis. As previously discussed, this specific region utilizes a highly structured, centralized forward capacity market to ensure long-term reliability 1516. Because the PJM footprint includes the state of Virginia - home to the infamous "Data Center Alley" in Loudoun County, which alone houses an estimated 35% of all known hyperscale AI data centers worldwide - the grid operator is absorbing the absolute brunt of the industry's physical expansion 21.

Monitoring Analytics, acting as the independent market watchdog for the PJM grid, issued a stark report calculating that roughly 70% of the recent multi-billion-dollar capacity price increases could be directly mathematically attributed to the relentless load growth from data centers locking in future demand forecasts 422. The watchdog estimated that data center demand resulted in $9.3 billion of increased electricity costs across the region in a single year 22. The unique danger within the PJM structure is that because overall capacity costs are often socialized across massive geographic delivery zones, a sprawling new AI campus built in one county can mathematically raise the capacity obligations - and thus the monthly retail bills - of residential ratepayers living hundreds of miles away within that same delivery zone 4.

ERCOT (The Electric Reliability Council of Texas)

Texas operates under a fundamentally different economic philosophy: an "energy-only" market structure 312343. Unlike PJM, ERCOT explicitly does not run a forward capacity market, and therefore does not pay generators a massive financial retainer just to be available 31. Instead, Texas relies entirely on the concept of "scarcity pricing." During periods of extreme grid stress, ERCOT allows wholesale energy prices to spike violently to thousands of dollars per megawatt-hour, theoretically providing enough sudden, massive revenue to incentivize generators to come online and encourage developers to build new plants to capture future windfalls 31.

The Dallas-Fort Worth metropolitan area is rapidly expanding as a primary secondary hub for artificial intelligence, currently hosting nearly half of the state's more than 400 operating data centers 45. The growth projections are staggering. ERCOT officially anticipates that peak summer demand could soar to nearly 145 gigawatts by 2031, up from roughly 85 gigawatts in 2024 24. Data centers and cryptocurrency mining operations are projected to account for a massive 32 gigawatts of that new demand 24. Oncor, the primary transmission and distribution utility for the Dallas-Fort Worth region, testified before the Texas House State Affairs Committee that its localized peak demand could literally double within five years if adequate transmission infrastructure can be built fast enough to support the incoming interconnection requests 45. For Texas residential ratepayers, the financial risk from AI load does not manifest in a discrete, highly visible "capacity charge" on their bill. Instead, it appears through wildly elevated wholesale energy prices during summer scarcity events, and critically, through steady, significant increases in Transmission and Distribution Utility (TDU) pass-through delivery fees required to physically build out the miles of heavy power lines and substations serving these massive corporate campuses 1247.

CAISO (California Independent System Operator)

California presents an entirely unique operating environment, constrained by some of the most aggressive legislative decarbonization goals in the world, exceptionally high base utility rates, and severe localized permitting challenges. Rather than a centralized PJM-style capacity auction, CAISO utilizes a localized "Resource Adequacy" framework, where individual Load Serving Entities and utilities must bilaterally contract for their own sufficient reserves to meet state mandates 232526.

The scale of the incoming demand is immense. Pacific Gas & Electric, the state's largest utility, reported to regulators that data center projects actively seeking interconnection in their planning pipeline could add approximately 10 gigawatts of pure electricity demand over the next decade - a figure roughly equivalent to four times the total generating capacity of the massive Diablo Canyon nuclear plant 27. However, California's primary operational challenge remains the infamous "duck curve" - a massive oversupply of cheap solar energy during the midday hours, followed by a steep, dangerous drop-off in generation at sunset, occurring at the exact moment residential cooling demand peaks 2328.

Because artificial intelligence data centers require 24/7 firm, unyielding power, their massive nighttime load cannot be met by solar arrays. It must be met by expensive, newly constructed utility-scale battery storage or legacy natural gas peaker plants, heavily exacerbating evening wholesale procurement costs 52. Furthermore, California utility base rates are already among the absolute highest in the nation - with Southern California Edison's average residential rate hitting 34.5 cents per kilowatt-hour in early 2026 - due to decades of aggressive, mandated infrastructure spending on wildfire mitigation and grid hardening 525329. Layering the multi-billion-dollar costs of data center infrastructure upgrades on top of these already historic rates has prompted severe warnings from independent watchdogs like the Little Hoover Commission regarding the imminent threat to consumer affordability 27.

FAQ 5: Will These Multi-Billion Dollar Wholesale Costs Actually Reach My Residential Bill?

The central, overriding anxiety for the American consumer is whether these abstract, multi-billion-dollar wholesale capacity spikes and localized transmission upgrades will actually appear on their physical monthly utility statement. The answer is an unequivocal yes, but the translation is not a simple 1:1 ratio, and the final impact is currently the subject of intense, state-by-state regulatory warfare.

It is important to understand the mechanics of cost pass-through. Wholesale capacity costs typically account for roughly 10% to 20% of a final retail electricity bill, depending heavily on the specific region and the retail provider's hedging strategy 11639. Therefore, an 833% increase in wholesale capacity prices does not mathematically equate to an 800% increase on a residential bill. Following the record-breaking 2026/2027 auction, PJM officials estimated that the newly capped capacity rate of $329 per megawatt-day would translate to a year-over-year retail bill increase of roughly 1.5% to 5% for most residential consumers within their footprint, though heavy users could see higher fluctuations 21.

However, capacity procurement is only one half of the equation. The physical grid infrastructure itself - the massive new high-voltage transmission lines, the heavy-duty substations, and the massive transformers required to physically connect a 300-megawatt data center to the regional grid - must be constructed, and the utility must be legally permitted to recover those capital costs 12722. Historically, state public utility commissions operate under the bedrock principle of socializing infrastructure costs across all classes of ratepayers. The traditional theory held that encouraging massive industrial load growth broadens the utility's total revenue base, ultimately lowering the per-unit cost of electricity for everyone 2852.

The sheer, violent scale and unprecedented speed of AI load growth have utterly shattered this historical paradigm. If a hyperscale tech conglomerate requests a $500 million specialized grid upgrade but subsequently abandons the project halfway through due to macroeconomic shifts, or utilizes only a fraction of their requested power due to sudden breakthroughs in chip efficiency, the utility will still demand full repayment for the constructed assets. Under traditional rules, residential ratepayers would be left legally shouldering massive "stranded costs" for infrastructure they never needed and from which they derive absolutely no benefit 24272855.

The Regulatory Pushback: Ring-Fencing the Residential Ratepayer

Recognizing the existential political and economic threat to consumer affordability, state Public Utility Commissions and lawmakers across the country have mobilized aggressively throughout 2025 and 2026 to overhaul outdated rate classes and mandate stringent, unprecedented financial protections. The unified regulatory strategy is to structurally shift the financial risk of grid expansion away from the public and entirely onto the balance sheets of the tech companies themselves.

The Ohio Precedent: AEP's 85% "Take-or-Pay" Tariff

In July 2025, the Public Utilities Commission of Ohio issued a landmark, highly contentious ruling approving a specialized tariff requested by the utility AEP Ohio 430. Under these new rules, any large new data center customer (defined as exceeding 25 megawatts of demand) is legally mandated to pay for a minimum of 85% of the total energy and capacity they contractually subscribe to use - even if their facility ultimately utilizes significantly less power 43057. This rigorous "take-or-pay" mechanism effectively forces data center operators to shoulder the massive upfront financial risk of localized grid expansions. Furthermore, the tariff demands that data centers provide hard proof of long-term financial viability and imposes severe exit fees - equal to three full years of minimum guaranteed charges - if they cancel a project prematurely 457. The requirements are locked in for a 12-year term, establishing a foundational national shift in cost allocation that directly insulates Ohio residential bills from speculative technological developments 575859.

Wisconsin's Uncompromising "Very Large Customer" Order

Following the precedent set in Ohio, the Public Service Commission of Wisconsin approved an even stricter, highly publicized framework in early 2026 concerning a proposal from the utility We Energies. Regulators formally created a specific, punitive rate class for hyperscale operations, significantly widening the net by lowering the eligibility threshold from the proposed 500 megawatts down to any facility requiring 100 megawatts or more 531. The Wisconsin order demands that data center operators sign unprecedented 15-year minimum contract terms to absolutely guarantee long-term asset recovery 5. Most crucially, regulators explicitly rejected a softer proposal that would have allowed data centers to pay only 75% of the generation costs. Instead, the commission mandated that these massive tech companies must cover exactly 100% of the capital costs to build, maintain, and fuel any new power plants that are constructed specifically to serve their localized demand, ensuring zero subsidization from the residential base 65532.

Virginia's GS-5 Class and Dominion's Capital Demands

In Virginia, the epicenter of the crisis, the battle over cost allocation reached a fever pitch. Dominion Energy formally proposed a base rate increase in 2025 that will add roughly $16 to an average monthly residential bill over a two-year period - comprising a 6.1% base rate hike alongside subsequent fuel charge increases 5233. Dominion cited the massive, billion-dollar capital expenditures required to build dedicated generation - such as the deeply controversial $1.47 billion Chesterfield Energy Reliability Center - necessary to support the explosive growth of Data Center Alley 23363. However, acknowledging the intense public backlash, the State Corporation Commission simultaneously mandated the creation of a stringent new "GS-5" rate class specifically targeting large data centers 264. Effective in 2027, these hyperscale facilities will be subjected to strict 14-year contracts that legally require them to pay for minimum thresholds of their requested infrastructure: specifically, a floor covering 85% of their localized transmission and distribution costs, and 60% of their generation costs 264. This officially begins the state's transition away from historical cost-sharing methodologies that unfairly burdened residential households for industrial growth 64.

Texas Senate Bill 6 and Oncor's Base Rate Review

Similarly, in Texas, state lawmakers recognized the vulnerability of their energy-only market to concentrated industrial load. The Texas legislature successfully passed Senate Bill 6, a targeted legislative effort aiming to require large electrical loads exceeding 75 megawatts to definitively bear a larger, proportional portion of the complex interconnection and operational costs associated with ERCOT grid integration, focusing heavily on transparency and fairness in capital cost allocation 12. Meanwhile, Oncor, managing the physical infrastructure for the data-center-heavy Dallas region, requested a comprehensive base rate review that is expected to result in an approximate 3% to 4.7% overall increase on residential bills (roughly $4.64 to $7.00 per month for a standard 1,000 kWh user) to strengthen the resiliency of a system strained by rapid industrial and technological growth 3.

Across all major jurisdictions, from the Rust Belt to the Sun Belt, the regulatory consensus is hardening: the historical era of blindly socializing the multi-billion-dollar infrastructure costs of hyperscale technology companies onto the backs of residential families is definitively ending.

FAQ 6: What Practical Steps Can Consumers Take to Manage Rising Costs?

While state regulators and utility commissions are rapidly erecting legislative firewalls to protect base distribution rates from the absolute worst of the data center expansion, the systemic, nationwide elevation of wholesale energy and capacity prices means the era of reliably "cheap electricity" is largely over 1665. United States average electricity prices rose approximately 40% between 2020 and 2026, and the compounding, relentless effects of mandated grid modernization, extreme weather hardening, and the inflexible baseload demands of artificial intelligence guarantee that upward pressure on retail rates will persist through the end of the decade 734. However, consumers are not powerless and can employ several aggressive, practical strategies to mitigate the financial impact on their summer utility bills:

Firstly, consumers must learn to leverage Time-of-Use (TOU) Arbitrage. As regional grids struggle intensely to balance the unyielding, flat baseloads of AI data centers against the sharp, massive peaks of residential evening cooling demand, utilities are aggressively transitioning customers to mandatory Time-of-Use rate plans 2967. These complex tariff structures charge exorbitant, premium rates during peak afternoon and evening hours (typically 4:00 PM to 9:00 PM) when the grid is most dangerously stressed, while offering heavily discounted, highly affordable rates during the overnight hours. By actively shifting heavy appliance use, programming electric vehicle charging, and aggressively pre-cooling homes to off-peak periods, consumers can completely bypass the most punitive pricing tiers and drastically reduce their monthly expenditures 2967.

Secondly, the mathematical logic for investing in Behind-the-Meter Solar and Battery Storage has never been stronger. The absolute most effective long-term hedge against escalating utility monopolies and volatile wholesale markets is localized energy independence 5368. Installing residential rooftop solar paired with advanced lithium-ion battery storage systems allows homeowners to generate their own power during the peak sunlight hours, store the excess, and critically, discharge their batteries to power their homes during the astronomically expensive peak evening hours 5367. By executing this localized energy arbitrage, homeowners avoid peak grid tariffs entirely. As utilities in deeply constrained regions like Southern California push standard residential rates upward of 34.5 cents per kilowatt-hour in 2026, the financial return on investment for residential solar and storage systems has accelerated dramatically, transforming from a luxury environmental choice into a harsh financial necessity 53.

Finally, homeowners must aggressively eliminate wasted consumption by conducting Professional Energy Audits. Particularly in extreme summer climate zones like Texas and Southern California, aging HVAC systems, degraded ductwork, and poor attic insulation force central cooling units to work exponentially harder during prolonged summer heatwaves 29. Professional energy audits utilize thermal imaging and blower door tests to identify specific, hidden inefficiencies. By executing targeted, relatively inexpensive upgrades based on these audits, homeowners can structurally lower their property's baseload demand 29. This is critical because it permanently shields the homeowner from volumetric rate hikes; if the underlying price per kilowatt-hour rises due to data center capacity constraints, the easiest defense is simply requiring fewer kilowatt-hours to maintain a comfortable home.

The Bottom Line

Will artificial intelligence data centers raise your summer electricity bill in 2026? Indirectly, yes, the structural pressures are undeniable. The explosive, unyielding, and highly inflexible power demands of hyperscale artificial intelligence have fractured the delicate, decades-long equilibrium of the United States electrical grid. This massive, unprecedented demand shock - combining lethally with the rapid, necessary retirement of legacy fossil-fuel plants, catastrophic delays in the renewable interconnection queues, and the implementation of deeply conservative extreme weather modeling - has triggered historic, multi-billion-dollar price spikes in regional wholesale capacity markets 11617.

However, it is absolutely vital to apply calibrated uncertainty when projecting the final retail bill impacts. A multi-billion-dollar, 833% surge in wholesale capacity costs does not mathematically equate to a doubling of a residential monthly bill. Wholesale capacity remains only a fraction of the total delivered cost of power. The true, systemic financial risk to the American consumer lies in the massive capital expenditures required to physically construct the new high-voltage transmission lines and dedicated generation facilities necessary to power these sprawling technological campuses 72224.

Fortunately for residential ratepayers, the years 2025 and 2026 have marked a profound, historic turning point in American utility regulation. Public utility commissions in key battleground states like Ohio, Virginia, Wisconsin, and Texas have clearly recognized the imminent threat of "Utility Overload" and have enacted aggressive, highly protective, precedent-setting tariffs 2451225. By legally forcing multi-trillion-dollar tech conglomerates into strict, uncompromising 12-to-15-year "take-or-pay" contracts, and demanding that they fund up to 100% of their localized infrastructure capital costs, regulators are ensuring that the entities actively driving the unprecedented need for new energy infrastructure are the exact ones footing the bill 5657.

As the digital economy further intertwines with the physical realities of copper wire and spinning turbines, the baseline cost of electricity will undoubtedly rise 65. But through vigilant, aggressive regulatory oversight, sophisticated rate design, and proactive consumer adaptation through solar and storage, the immense financial burden of powering the artificial intelligence revolution will increasingly fall directly on the hyperscalers themselves, rather than quietly draining the wallets of the American household.