Will AI Make Universal Basic Income Necessary

Universal Basic Income (UBI) is a proposed macroeconomic safety net in which the government guarantees a regular, unconditional cash payment to every citizen, regardless of their employment status or existing wealth. As rapid advancements in artificial intelligence threaten to displace millions of white-collar workers and automate cognitive labor, economists, tech leaders, and policymakers are aggressively testing UBI and alternative capital distribution models to prevent widespread economic collapse and re-engineer the modern welfare state.

The Automation Catalyst: Why the Labor Market is Forcing the Issue

The debate over unconditional cash transfers has simmered on the fringes of economic and political theory for decades, frequently dismissed as a utopian impossibility. However, the rapid deployment of generative artificial intelligence and large language models has thrust it into the center of mainstream public policy. Unlike previous industrial revolutions that primarily automated physical, blue-collar, and mechanical labor, the current wave of technological disruption is aimed squarely at cognitive, white-collar tasks previously thought immune to machine substitution 123.

The labor market is already exhibiting early signs of this profound structural shift. In 2025 alone, major technology corporations, including industry giants like Oracle and Amazon, shed approximately 400,000 white-collar jobs as artificial intelligence was integrated into core business operations 4. The impact is moving swiftly beyond the tech sector. Positions that rely heavily on data entry, basic financial analysis, human resources administration, legal document review, and routine customer support are experiencing large-scale displacement 2456.

Some industry forecasts, including those modeled by prominent AI executives, suggest that autonomous systems could eliminate up to half of all entry-level white-collar roles within the next few years 57. This dynamic shifts the balance of power between labor and capital, creating an environment where companies achieve higher productivity and profit margins with significantly fewer human staff members 4.

The Threat of "Ghost GDP" and Consumption Collapse

The systemic risk of unmitigated white-collar automation is what economists and analysts refer to as "ghost GDP" 6. In a traditional capitalist economy, corporate growth and consumer spending are inextricably linked; workers earn wages, which they use to purchase goods and services, driving further corporate growth.

If algorithms and autonomous systems absorb a vast percentage of billable hours across the legal, financial, and administrative sectors, the traditional mechanism for wealth distribution - employment - fractures. Without wages, consumer spending, which accounts for roughly 70% of the U.S. economy, would collapse 6. The resulting dynamic would feature soaring corporate productivity and plunging consumer demand. Consequently, an unconditional financial floor like UBI is increasingly viewed by technologists and venture capitalists not merely as a charitable welfare policy, but as an essential macroeconomic stabilizer necessary to preserve market capitalism 59.

The Bureaucratic Burden: UBI vs. Traditional Welfare

To understand the growing bipartisan and institutional appeal of Universal Basic Income, one must examine the severe friction points within the existing social safety net. Traditional welfare programs are inherently targeted, means-tested, and conditional. They require applicants to continuously prove their poverty, demonstrate their physical inability to work, or actively participate in state-mandated job-seeking activities.

While targeted welfare theoretically concentrates scarce government resources on the populations with the deepest need, economists and policy analysts have identified several systemic flaws in its real-world application.

The Scale of the Welfare Bureaucracy

The sheer scale and complexity of the current system create massive inefficiencies. The United States federal government spends anywhere from $1.1 trillion to $1.8 trillion annually across more than 80 to 134 overlapping anti-poverty programs 611. Administering this tangled web of state and federal agencies requires immense overhead. State and federal governments employ vast armies of eligibility screeners, fraud investigators, and compliance officers.

Some estimates suggest that administrative costs consume between 15% to 30% of certain welfare program expenditures - meaning billions of taxpayer dollars never reach the vulnerable populations they were intended to assist 7. A report by the Government Accountability Office (GAO) noted that a significant portion of federal funds for low-income families is diverted simply to cover the administrative execution of these complex benefits rather than direct aid 8.

The Shifting Fiscal Vulnerability of States

Traditional programs are becoming increasingly precarious for local governments. Recent legislative changes to the Supplemental Nutrition Assistance Program (SNAP) illustrate the fragility of conditional welfare. Under the sweeping federal reconciliation legislation known as the One Big Beautiful Bill Act (OBBBA) of 2025, the structure of SNAP funding was drastically altered 915.

Historically, the federal government covered 100% of the monthly food benefits and split the administrative costs 50/50 with the states 910. Under OBBBA, states are mandated to assume a much larger share of the burden. Beginning in late 2026, states will see their share of administrative expenses leap from 50% to 75% 91510. Furthermore, starting in 2027, states will be required to cover between 5% and 15% of the actual SNAP food benefit costs, depending on their administrative error rates 1517.

This massive cost shift is projected to increase the share of state budgets allocated to SNAP by a median of 202%, with some states facing an increase of up to 768% 9. For large states like California and Florida, this translates to billions in new liabilities 9. Faced with impossibly high costs, states are expected to cut other essential programs, raise taxes, or impose draconian work requirements that strip millions from the food safety net entirely 91517.

The Welfare Cliff and Work Disincentives

Beyond administrative bloat, traditional conditional welfare creates a well-documented economic trap known as the "welfare cliff" or "benefits cliff" 711. Traditional benefits act as a ceiling rather than a foundation. If a recipient earns an income that surpasses a strict, often arbitrary, eligibility threshold, their benefits are abruptly terminated.

This dynamic actively penalizes upward mobility. A modest wage increase or a transition from part-time to full-time work can result in a devastating net financial loss for a family due to the sudden withdrawal of food (SNAP), housing assistance, and medical care (Medicaid) 711. In contrast, because a Universal Basic Income is unconditional, it is never withdrawn when a recipient finds employment. It simply acts as an economic floor that rises alongside earned income, theoretically preserving the incentive to seek better-paying work without the threat of catastrophic benefit loss 7.

Comparing Systemic Approaches to Poverty Alleviation

| System Feature | Traditional Means-Tested Welfare (e.g., SNAP, TANF) | Universal Basic Income (UBI) |

|---|---|---|

| Eligibility Verification | Highly restrictive; requires continuous proof of deep poverty, disability, or work status. | Universal; granted automatically to all defined residents or citizens regardless of status. |

| Work Incentives | High risk of penalizing work due to sudden benefit cut-offs (the "welfare cliff"). | Preserves incentives; unconditional income stacks on top of newly earned wages. |

| Administrative Overhead | Massive overhead (15-30%) due to caseworkers, strict audits, and complex compliance systems. | Extremely low overhead; distributed via automated direct deposits or digital wallets without behavioral tracking. |

| Usage Restrictions | Heavily restricted and paternalistic (e.g., SNAP funds can only purchase specific grocery items). | Completely unrestricted; empowers recipients to allocate funds based on their immediate and unique personal needs. |

| Social Stigma | High; often carries social and political stigma associated with dependency. | Low; widely viewed as a fundamental right, an economic dividend, or shared societal inheritance. |

Ground Truth: Evaluating the OpenResearch Initiative

While theoretical debates dominate political discourse, the mid-2020s have yielded an unprecedented volume of empirical data from massive, well-funded pilot programs. By observing how humans actually behave when provided with unconditional cash, researchers are beginning to separate economic reality from ideological rhetoric.

In the United States, the most closely watched experiment was the OpenResearch Unconditional Cash Study, heavily backed by OpenAI CEO Sam Altman. Launched in 2019 and concluding its primary data release in the summer of 2024, the $60 million study was one of the largest and most comprehensive basic income experiments in U.S. history 191213. The study provided 1,000 low-income residents in Texas and Illinois (earning below $28,000 annually) with $1,000 per month for three years, comparing their outcomes against a control group of 2,000 people who received $50 a month 1913.

Consumption Patterns and Necessities

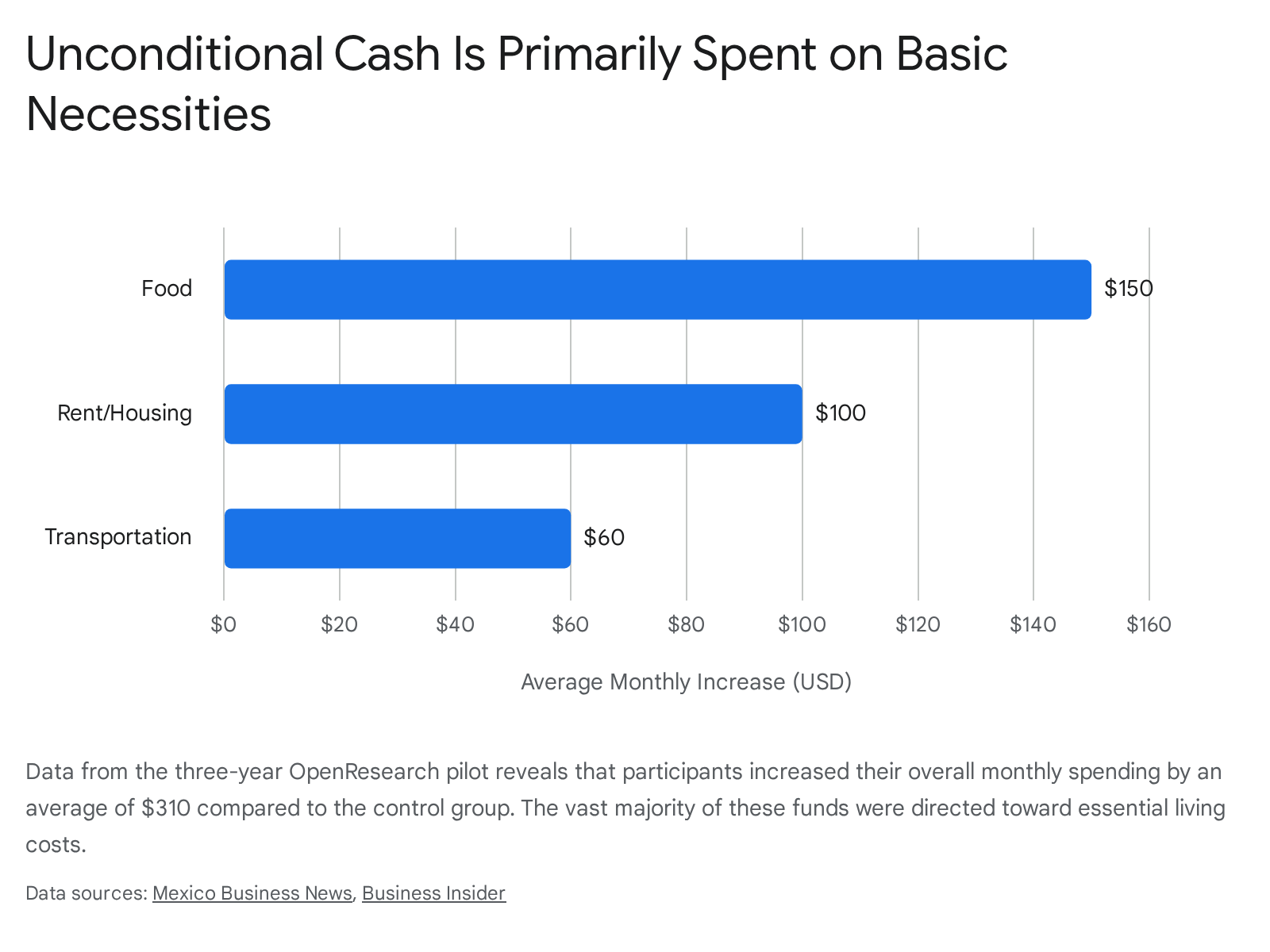

The findings challenged assumptions across the political spectrum. A primary criticism of unconditional cash transfers is that recipients will squander the funds on frivolous or harmful consumption. The OpenResearch data definitively refuted this. Beneficiaries increased their total spending by an average of $310 per month compared to the control group, and the vast majority of this capital was funneled directly into basic survival necessities 1913.

In addition to food, rent, and transit, recipients actively improved their financial resilience. The study found that beneficiaries' individual savings in their bank accounts increased by nearly 25% during the study, growing from an average of $1,000 to $1,250 1913. Furthermore, recipients spent about 26% more on supporting other people in need compared to the control group, demonstrating an unexpected communal multiplier effect from the cash injection 13.

Labor Reductions and the Pursuit of Agency

The impacts on labor participation were intensely scrutinized. Program beneficiaries did reduce their working hours compared to the control group, though the precise magnitude is viewed by economists as a moderate effect. Recipients worked roughly 1.3 to 1.4 hours less per week on average, with some specific demographics seeing reductions of up to four hours 1914. Employment rates among the beneficiaries decreased by roughly 7% during the second and third years of the experiment 19.

However, interpreting this reduction as a total withdrawal from the workforce is inaccurate. Rather than exiting the labor market entirely, recipients redirected their time toward leisure, caregiving, and deliberate career advancement. Beneficiaries showed a 15% increase in participation in job training programs 19. The data suggests that a guaranteed income provides workers with the agency to reject precarious, exploitative labor and take the time necessary to search for better long-term opportunities 191215.

This agency translated directly into business creation. While entrepreneurship did not surge universally across the entire cohort, it spiked significantly among marginalized groups. In the third year of the program, Black recipients were 26% more likely to report starting or helping to start a business than Black participants in the control group. Similarly, female recipients saw a 15% increase in entrepreneurial activity 12.

The Limits of Cash on Long-Term Health

Health outcomes from the OpenResearch study were unexpectedly muted, revealing the limitations of basic income in a vacuum. While recipients utilized their funds to increase spending on medical and dental care by 12% - and experienced a 10% increase in emergency room visits - researchers observed no significant, lasting improvements in physical or mental health 191314.

During the first year of the program, beneficiaries reported notable drops in financial stress and food insecurity 1913. However, these positive psychological effects were not sustained over time. By the second and third years, stress levels had returned to a baseline similar to those of the control group 1913. This suggests that while $1,000 a month provides a vital, immediate buffer against acute poverty, a flat cash stipend cannot entirely insulate individuals from the systemic pressures, structural healthcare costs, and broader economic anxieties of modern society.

Sovereign and Municipal UBI Successes Worldwide

While the OpenResearch study analyzed short-term behavioral changes in the United States, global experiments are yielding data on the long-term, macroeconomic effects of permanent basic income systems.

The Maricá Experiment (Brazil)

In stark contrast to temporary North American pilots, the city of Maricá in Brazil has successfully operated the largest permanent basic income program in Latin America. Funded through municipal oil royalty revenues, the Renda Básica de Cidadania (RBC) program launched in 2015 and has steadily expanded to cover approximately 93,000 beneficiaries - roughly half of the city's population 16251718.

The RBC pays a fixed monthly amount, but crucially, it does so using a localized digital currency called the mumbuca 162518. The mumbuca is pegged one-to-one with the Brazilian real, but it can only be spent within the geographic boundaries of Maricá 1618. This closed-loop monetary design is highly intentional; it prevents capital flight and ensures that the unconditional cash directly stimulates the local commercial economy 1828.

A rigorous quantitative evaluation released in late 2024 by the Jain Family Institute (JFI) and the Universidade Federal Fluminense analyzed the impacts of this permanent policy. The results demonstrated profound socioeconomic shifts 1619. Recipient households saw a 9% net increase in household income and a 5% rise in overall household consumption compared to non-recipients 162820.

Notably, the study uncovered a fascinating labor paradox: while total household income increased, labor income specifically dropped by 17% 2820. Researchers attribute this decline not to indolence, but to structural labor market improvements. The RBC provided a financial floor that allowed workers to abandon highly undesirable jobs or stay home to care for vulnerable family members, particularly during pandemic shocks 1620. At the macro level, the localized injection of mumbucas drove formal employment growth in Maricá at a significantly faster rate than in comparable neighboring municipalities, proving that cash transfers can simultaneously reduce individual labor desperation while boosting total regional employment 1820.

The Marshall Islands 'Enra' Program

In November 2025, the Republic of the Marshall Islands executed one of the boldest policy moves in modern economics, becoming the first sovereign nation to implement a permanent, nationwide, unconditional basic income for all resident citizens, including children 213222.

The program, named "Enra," pays roughly $800 annually per person, distributed in $200 quarterly installments 32222324. While this nominal figure may appear modest to Western observers, it represents a massive financial injection relative to the local economy. The initiative commits approximately 8% of the nation's GDP to universal cash transfers, with a companion program allocating an additional 6% for high-need communities 213222. For comparison, an equivalent transfer in the United States would equal roughly $750 a month per citizen 32.

The Marshall Islands program solves a key constraint of UBI: taxation. Rather than imposing heavy domestic taxes on its citizens, the government funds Enra entirely through external rents - specifically a U.S.-capitalized sovereign wealth fund created under the Compact of Free Association 21322224. The goal is to act as a financial safety net against high levels of outward migration and severe climate vulnerability 2224.

To overcome the immense logistical hurdles of distributing funds across 24 remote Pacific atolls with limited traditional banking infrastructure, the government deployed a dedicated citizen digital wallet named Lomalo 2225. The system is integrated with the RMI's Digital Sovereign Bond (USDM1), a U.S. dollar-denominated stablecoin fully collateralized by short-dated U.S. Treasuries 2225. By issuing the basic income digitally on a blockchain, the government bypasses predatory intermediaries, ensuring instant, low-cost, and secure settlement directly to citizens 2225.

Diverse Global Implementation Strategies

Beyond massive municipal and sovereign programs, various nations are testing highly targeted Guaranteed Basic Income (GBI) frameworks aimed at specific vulnerable populations:

- Wales (United Kingdom): The Welsh government is running a multi-year pilot providing £1,600 (roughly $2,166) per month to young adults aging out of the foster care system, attempting to provide financial stability during a highly precarious life transition 26.

- South Korea: Gyeonggi Province has launched a targeted initiative directed at farmers and fishermen - sectors vulnerable to climate and trade shocks - providing annual or monthly stipends reaching up to 210,000 recipients 26.

- India: Several states, including Tamil Nadu and Delhi, are executing massive unconditional cash transfer programs specifically for women. These stipends, ranging from 1,000 to 2,500 rupees monthly, are designed to circumvent patriarchal financial controls and foster direct female economic independence 26.

The Macroeconomic Equation: Cost, Taxation, and the Inflation Threat

Despite the undeniable micro-level successes of pilot programs, scaling Universal Basic Income to the size of a massive, industrialized economy like the United States presents staggering macroeconomic hurdles that divide economists.

The Staggering Cost of Universality

The raw arithmetic of a true universal basic income is the primary barrier to its implementation. Providing just $1,000 a month ($12,000 annually) to every American adult would require a gross federal expenditure of approximately $3 trillion every single year 2739. To contextualize this figure, the entire U.S. federal revenue in 2019 was roughly $3.4 trillion, and total federal spending was $4.5 trillion 28.

Funding a full-scale UBI without exploding the national deficit would demand radical and unprecedented tax overhauls. Economists calculate that funding such a program could require increasing federal taxes by over 70% 28. Proposals to finance UBI vary widely but generally include enacting national consumption taxes (e.g., a nearly 20% national sales tax), implementing progressive value-added taxes (VAT) on luxury goods, creating a heavy land value tax, or vastly increasing corporate rates 284142.

Sophisticated econometric modeling by the Penn Wharton Budget Model demonstrates the trade-offs: funding a more modest $6,000 annual UBI would require implementing an 11.25% dedicated payroll tax 42. While this would successfully increase federal revenues by over 56%, it would dramatically alter the take-home pay of the middle and working classes, effectively negating the benefit of the UBI for large swaths of the population 4229.

The "Robot Tax" Debate

To avoid heavily taxing human workers, policymakers and tech luminaries like Bill Gates have proposed the "Robot Tax" or automation tax 4430. The core premise is that the tax system currently relies heavily on labor taxation (payroll and income taxes). When capital investment (software, robotics, AI) permanently replaces human labor, the government loses the associated revenue stream 4430. An automation tax would penalize corporations based on the labor they replace, funneling that specific revenue directly into a UBI pool 4430.

South Korea took an early step toward this model by reducing tax incentives for corporate investments in labor-replacing equipment 3. However, economists note severe practical headwinds. Defining what constitutes a "robot" versus standard productivity-enhancing software is an administrative nightmare 344. Furthermore, aggressively taxing technological efficiency could cripple a nation's global economic competitiveness, driving AI development offshore to more favorable tax jurisdictions 4430.

Does UBI Cause Runaway Inflation?

The most persistent mainstream criticism of UBI is that flooding the consumer market with liquid cash will trigger runaway inflation, ultimately neutralizing the purchasing power of the stipend 464748. Opponents argue that if every citizen receives $1,000 a month, landlords will simply raise rent by $1,000, and grocery stores will uniformly hike prices, leading to an inflationary spiral that devalues labor and damages the broader economy 464849.

Economic theory, however, suggests the inflationary impact of a UBI is not a simple binary, but rather depends on numerous structural variables - most notably economic capacity and the funding mechanism 47.

Inflation occurs when the aggregate demand for goods outstrips the aggregate ability to supply them. If an economy is operating with significant "slack" (excess production capacity), a UBI will simply stimulate production. Factories will produce more goods, and builders will construct more housing to capture the new consumer cash, absorbing the demand without drastically raising prices 47. This phenomenon was observed in a macro-level experiment in Kenya, where the local economy absorbed massive cash transfers through increased supply generation, resulting in virtually zero inflation 47.

Conversely, if an economy is already operating at maximum capacity, or if the UBI triggers a massive reduction in the labor force that diminishes the supply of goods, the newly introduced money will simply bid up the prices of existing scarce resources 4748.

Furthermore, the funding mechanism dictates the outcome. A UBI financed entirely by deficit spending (printing new money) poses a severe inflationary threat because it introduces vast amounts of new liquidity into the money supply 394647. A UBI funded strictly through redistributive taxation - taking money from high-income earners and transferring it to low-income earners - is theoretically deficit-neutral. It does not create new money, but rather shifts the velocity of existing money, posing a much lower risk of hyperinflation 4731.

The Silicon Valley Pivot: Universal Basic Compute (UBC)

As the staggering political and economic realities of implementing a multitrillion-dollar fiat cash transfer system become apparent, the very Silicon Valley visionaries who originally championed UBI are shifting their paradigms.

By early 2026, Sam Altman, CEO of OpenAI and previously one of the world's most vocal UBI advocates, publicly walked back his support for traditional cash transfers. In a widely covered interview, Altman stated, "I no longer believe in universal basic income as much as I once did" 3233. He argued that while fixed fiat cash payments might temporarily alleviate poverty, they fail to address the core structural issue of the impending AI revolution: the total shifting of economic leverage from human labor to corporate capital 33.

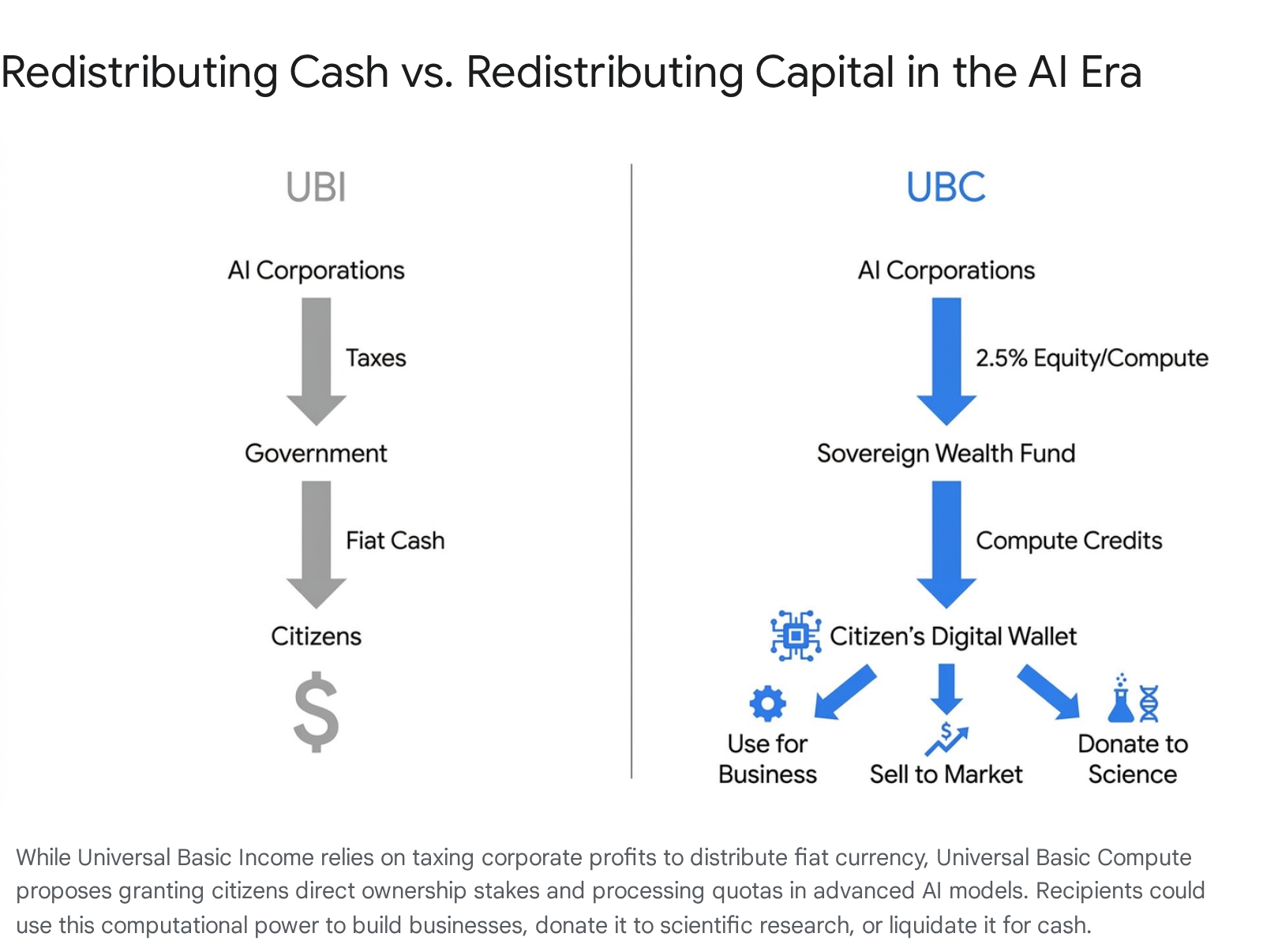

In its place, Altman and a growing cohort of AI accelerationists have proposed a radical alternative: Universal Basic Compute (UBC) or Universal Basic Capital 31343555.

Instead of the government attempting to capture and tax AI companies' profits to distribute fiat currency - a process fraught with bureaucratic friction and tax evasion - society would distribute the underlying means of production directly to citizens. Under this model, every citizen would be granted a fractional ownership share of the raw compute power generated by the world's most advanced large language models (e.g., a recurring "slice" of GPT-7's compute capacity) 34355536.

How Universal Basic Compute Would Function

The theoretical mechanics of UBC operate similarly to a decentralized digital dividend. A sovereign wealth fund would collect a mandatory equity and compute tax - frequently modeled around 2.5% of total corporate value and processing output - directly from frontier AI labs 5557. Citizens would then receive regular allocations deposited into a digital wallet in the form of "compute credits."

A recipient would have total sovereignty over their slice of the AI economy, with three primary options: 1. Liquidation: If a citizen merely needs cash to pay rent or buy groceries, they can click a button to "sell" their AI processing power back to the open market or enterprise clients, converting the compute into regular fiat currency transferred to their bank account 555. 2. Utilization: If a citizen has an entrepreneurial idea, they can utilize their allocated compute to launch automated ventures, train personalized AI agents, or perform high-level digital labor at zero baseline cost 57. 3. Donation: Citizens who do not need the capital can aggregate and donate their massive compute cycles to specific humanitarian or scientific causes, effectively crowd-sourcing supercomputing power for cancer research or climate modeling 34355536.

The Philosophical Divide over UBC

Proponents argue that Universal Basic Compute represents a fundamentally fairer economic paradigm. Because AI models are trained on the digital footprints, copyrighted material, and aggregate data of all humanity, the public inherently deserves an equity stake in the resulting infrastructure 57. UBC theoretically prevents a dystopian oligopoly where a few massive corporations own all cognitive capital, instead integrating humanity directly into the production side of the AI ecosystem 957.

However, the concept faces intense skepticism from economists and labor advocates. Critics view UBC as a highly sophisticated evasion tactic by the tech industry to avoid paying the massive, traditional corporate taxes required to fund a true cash-based social safety net 9. By distributing highly volatile "compute credits" instead of stable fiat currency, AI companies effectively offload market risk onto ordinary citizens. A displaced paralegal struggling to pay a medical bill does not need a slice of GPT-7's processing architecture; they need immediate, stable cash 655. Critics argue that inserting a digital commodities market between citizens and their basic survival needs is an unnecessary complication of the welfare state 955.

Legislative Battlegrounds and the Future Outlook

As the timeline for widespread AI automation accelerates, the ideological divide over basic income is moving from academic whitepapers into fierce legislative battles across the United States.

At the federal level, progressive lawmakers are actively attempting to push the concept into the mainstream statutory framework. In late 2025, Representative Bonnie Watson Coleman reintroduced the Guaranteed Income Pilot Program Act 73738. The ambitious bill proposes a three-year, nationwide experiment involving 20,000 Americans. Under the legislation, 10,000 participants would receive a monthly, no-strings-attached cash payment exactly equal to the fair market rent of a two-bedroom apartment in their respective zip codes 73738. The bill's sponsors explicitly frame the legislation as a necessary evolutionary step for the safety net, designed to preempt the devastating loss of livelihoods driven by the concentration of AI technologies among a few corporate entities 3738.

Conversely, the concept has met highly coordinated resistance at the state level. Viewing guaranteed basic income as a dangerous expansion of socialism that inherently discourages labor participation, conservative lawmakers across multiple states - including Arizona, Iowa, South Dakota, Texas, and Wisconsin - have drafted or successfully passed legislation explicitly prohibiting local municipal governments from establishing their own basic income pilot programs 739. These lawmakers argue that unconditional cash fosters long-term government dependency and undermines the fundamental American ethos of work 711.

Simultaneously, broader partisan economic frameworks are threatening to further destabilize the financial security of the middle class, making the UBI conversation even more urgent. The widely debated Project 2025 proposals, for example, outline a radical restructuring of the federal tax code. By advocating for flattened income tax brackets (such as a flat 15% rate for earners up to $168,000) while simultaneously eliminating various vital deductions and slashing the corporate tax rate to 18%, economists argue the plan would functionally raise net taxes on working-class families by thousands of dollars 4041.

In a volatile macroeconomic environment where traditional social support mechanisms are being systematically defunded, cost-shifted to struggling states, or legally banned by partisan legislatures, the pressure to adopt a streamlined, universal safety net will only intensify as automation continues to erode traditional employment.

Bottom line

Universal Basic Income has evolved from a fringe academic theory into an actively tested macroeconomic stabilizer designed to counteract the rapid onset of AI-driven white-collar unemployment. Recent mega-pilots prove that while unconditional cash effectively addresses immediate survival needs, prevents administrative bloat, and provides a buffer against acute financial stress, it cannot entirely shield recipients from broader systemic economic flaws or structural healthcare costs. Moving forward, the multi-trillion-dollar cost of implementing a fiat-based UBI has fractured consensus, igniting a fierce policy debate over whether governments should redistribute cash through massive taxation, or instead redistribute raw technological capital through emerging concepts like "Universal Basic Compute."