Why Inflation Happens and Why Some Is Healthy

Inflation occurs when the overall demand for goods and services outpaces an economy's ability to supply them, or when the costs of raw materials and labor suddenly spike. While rapid, unpredictable price increases erode consumer purchasing power and destabilize economies, central banks deliberately steer their nations toward a low, steady rate of inflation - most commonly 2 percent. This modest, engineered inflation acts as a vital macroeconomic shock absorber, allowing labor markets to adjust smoothly to crises and providing a crucial buffer against the catastrophic risks of a deflationary downward spiral.

The Core Mechanics of Measuring Inflation

Before diagnosing why prices rise, it is important to understand how economists know they are rising at all. Inflation is not measured by the price of a single commodity, like a gallon of milk or a tank of gas, but by tracking the broad cost of living over time 12.

The Consumer Price Index (CPI) and Its Basket

The most universally recognized metric is the Consumer Price Index (CPI) 34. Statistical agencies construct the CPI by tracking a "basket of goods and services" that represents the spending habits of an average household. This basket is divided into major components such as housing, food, transportation, medical care, apparel, and recreation 25.

Because an average family spends far more on rent or a mortgage than on dairy products, housing is given a much heavier "weight" in the basket. Consequently, a 10 percent increase in rental rates will drive the overall CPI much higher than a 10 percent increase in the price of milk 2. To gather this data, agencies like the Bureau of Labor Statistics (BLS) collect hundreds of thousands of prices each month from retailers, supermarkets, and service providers, adjusting for changes in product quality over time 126.

Headline vs. Core Inflation

When policymakers and economists discuss inflation, they frequently distinguish between two variants of these metrics: * Headline Inflation: This includes every item in the consumer basket. It is the number widely reported in the news and reflects the immediate, total cost of living felt by consumers 5. * Core Inflation: This strips out the prices of food and energy. Because agricultural yields and global oil markets are highly volatile and subject to sudden weather or geopolitical shocks, core inflation provides a smoother, more reliable picture of underlying, persistent economic trends 5.

To further filter out "noise," central banks sometimes look at the trimmed-mean CPI or median CPI. These measures exclude the items with the most extreme price movements in any given month, whether those prices are crashing or surging, to reveal the true baseline inflation rate 12.

Why Central Banks Prefer the PCE

While the CPI is the most famous metric, central banks often prefer slightly different gauges. In the United States, the Federal Reserve's primary metric for its 2 percent target is the Personal Consumption Expenditures (PCE) price index 1.

The primary CPI can overstate inflation because it prices a relatively fixed basket of goods. If the price of apples spikes, shoppers might naturally substitute them with cheaper peaches 1. The traditional CPI calculates inflation as if consumers stubbornly continue buying the exact same number of expensive apples. The PCE is a "chained" index, meaning it constantly adjusts for these behavioral substitutions, making it a more accurate reflection of actual household financial pressure 1. Furthermore, the PCE incorporates different weighting; for instance, medical care holds a 22 percent weight in the PCE compared to just 9 percent in the CPI, reflecting total societal spending rather than just out-of-pocket consumer costs 1.

The Three Root Causes of Inflation

Inflation is a complex macroeconomic phenomenon, but economists generally divide its origins into three primary categories: demand-pull, cost-push, and built-in inflation 377.

Demand-Pull Inflation: Too Much Money, Too Few Goods

Demand-pull inflation occurs when aggregate demand in an economy aggressively outpaces aggregate supply 37. When consumers, businesses, and governments want to buy more goods and services than the economy can sustainably produce, the excess demand acts as a vacuum, bidding prices upward 37.

This typically happens during rapid economic expansions. If interest rates are low, borrowing is cheap, and employment is high, households have more disposable income to spend 7. It can also be triggered by sudden injections of government stimulus. For example, when governments deploy expansionary fiscal policies - such as the widespread distribution of pandemic stimulus checks - consumer spending can surge much faster than supply chains can manufacture and deliver the physical goods 78.

Cost-Push Inflation: The Supply-Side Shock

Unlike demand-pull inflation, which is driven by an abundance of money and consumer optimism, cost-push inflation is driven by supply-side constraints 810. It occurs when the costs of production - such as raw materials, energy, or labor - suddenly increase. To protect their profit margins, manufacturers and service providers are forced to pass these higher input costs down the chain to the end consumer 78.

Cost-push inflation is often triggered by external shocks. A classic example is a geopolitical crisis that restricts the supply of oil 810. Because energy is required to manufacture and transport virtually every good in the modern economy, a surge in oil prices quickly ripples through the entire supply chain, raising the cost of everything from airline tickets to agricultural fertilizers 10. Currency depreciation can also drive cost-push inflation; if a nation's currency loses value, importing raw materials becomes more expensive, a phenomenon known as "imported inflation" 3810.

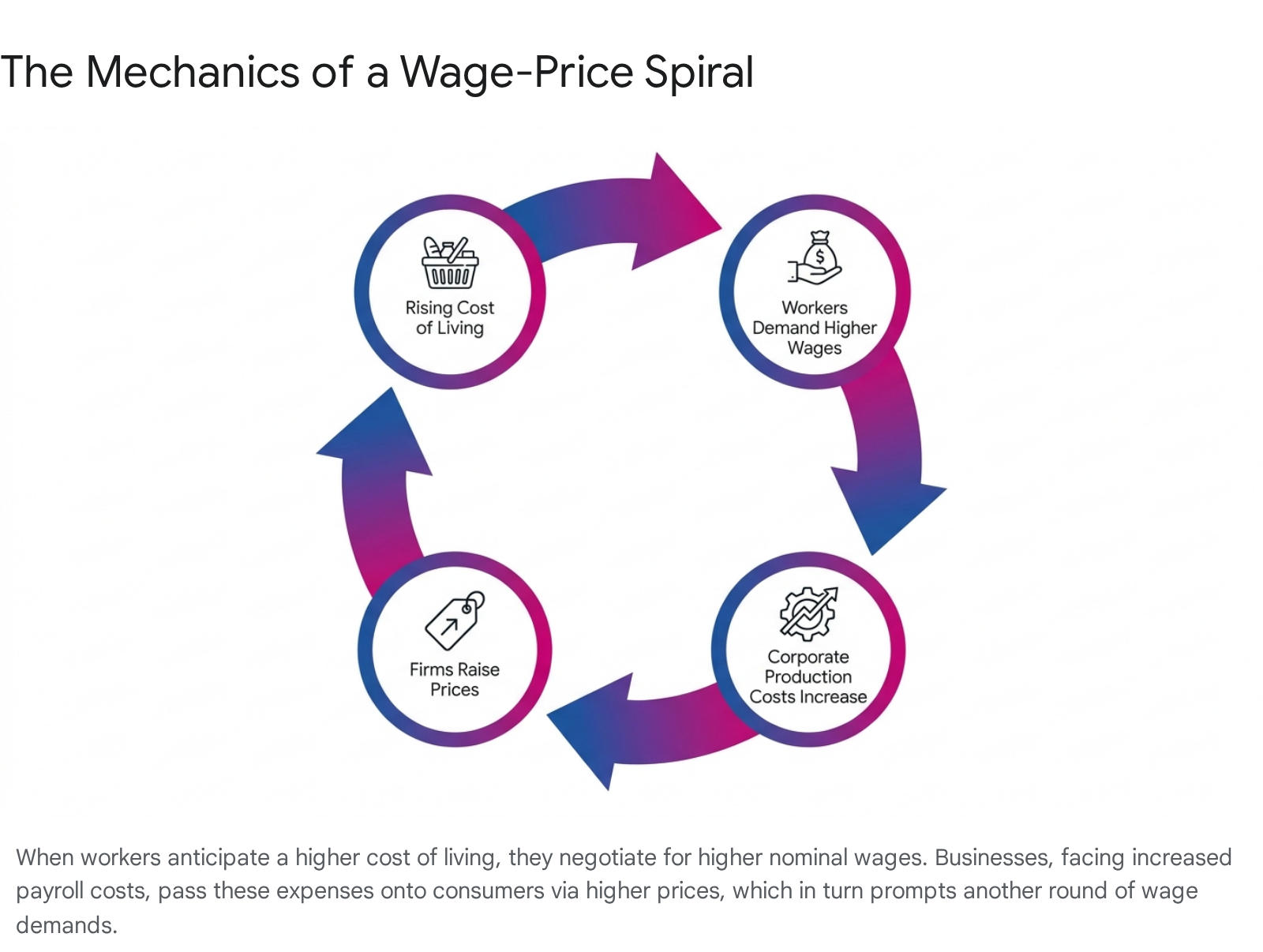

Built-In Inflation and the Wage-Price Spiral

The third driver of inflation is uniquely psychological. "Built-in" inflation is driven by expectations 38. If businesses and households firmly believe that prices will be 5 percent higher next year, they act on that belief today. Consumers will accelerate their purchases to beat future price hikes, thereby increasing current demand 89.

More importantly, workers who expect the cost of living to rise will demand higher wages to protect their real income 712. When powerful trade unions or tight labor markets allow workers to successfully negotiate significant wage hikes, corporate payroll costs soar. To cover these higher wages, firms raise the prices of their goods and services. Workers then see those higher prices and demand yet another round of wage increases.

This self-fulfilling positive feedback loop is known as the wage-price spiral 1210.

Theoretical Perspectives on the Spiral

Modern Keynesian economic models view this spiral as a fundamental distributional conflict between workers and firms 111213. When an external shock reduces the overall wealth of an economy, firms try to maintain their profit margins by raising prices, while workers try to maintain their living standards by demanding higher wages. The gap between the real wage firms are willing to pay and the real wage workers aspire to earn produces a persistent nominal escalation 1113.

However, the severity of the wage-price spiral is debated. Economist Milton Friedman famously criticized the concept, arguing that a spiral is merely an external manifestation of inflation, not its root source 10. In Friedman's view, an inflation spiral will naturally break if the central bank refuses to increase the money supply to accommodate it. Supporting this, recent studies by the International Monetary Fund (IMF) suggest that while short-term spirals are common during supply shocks, they rarely lead to a sustained, perpetual increase in price levels unless accompanied by fundamentally loose monetary policy 10.

Case Study: The 2021 - 2022 Global Inflation Spike

The theoretical causes of inflation rarely happen in isolation. The global inflation surge of 2021 and 2022 serves as a perfect modern case study of how demand-pull dynamics, cost-push constraints, and psychological expectations can violently collide.

The Perfect Storm of Demand and Supply

Following the economic lockdowns of the COVID-19 pandemic, global inflation spiked to levels not seen since the 1970s 1415. Research from the Bank for International Settlements (BIS) and the National Bureau of Economic Research (NBER) indicates this was a "perfect storm" of overlapping shocks 1416.

First, there was a massive demand-pull effect. Unprecedented fiscal stimulus packages and near-zero interest rates left households flush with cash just as pandemic restrictions were lifted 81417. Because people were still wary of traveling or dining out, there was a massive shift in consumer demand away from services and directly toward physical goods 14.

Simultaneously, severe cost-push shocks crippled the global supply side. Supply chains were tangled by factory closures, labor shortages, and port backlogs, creating acute shortages of microchips, vehicles, and raw materials 815. In 2022, Russia's invasion of Ukraine further shocked the system, sending global energy and agricultural commodity prices soaring 141518.

Why Central Banks Misdiagnosed the Threat

Why did inflation get so bad before authorities intervened? According to macroeconomic analyses, central banks globally misdiagnosed the initial threat 1618.

In the first half of 2021, many policymakers dismissed the rising prices as a temporary, normal "catch-up" following the pandemic's deflationary start 1618. A comprehensive review by the BIS outlined several reasons for this policy failure: 1. Misdiagnosing the Shocks: Central banks believed the supply chain issues were purely transitory 1618. 2. Neglecting Expectations Data: Policymakers firmly believed that long-term inflation expectations were securely anchored after two decades of low inflation 16. 3. Over-reliance on Past Credibility: Central banks assumed their hard-won reputations would keep inflation in check, giving them the illusion that they had room to keep interest rates low to support employment recovery 1618.

By the time it became clear that aggregate demand was structurally outpacing supply, central banks had to aggressively reverse course. They engaged in belated but highly aggressive interest rate hikes to destroy excess demand and prevent a devastating wage-price spiral from taking permanent hold 1419.

Why Do Central Banks Target 2 Percent Inflation?

Given the financial pain caused by the post-pandemic inflation surge, a logical question arises: Why do central banks target inflation at all? Why not aim for exactly 0 percent, where the cost of living remains perfectly flat?

The near-universal consensus among modern economists is that a low, predictable rate of positive inflation - usually 2 percent - is optimal for a healthy, growing economy 2024. This is because a slight inflationary headwind solves several severe macroeconomic problems.

The Accidental Origins in New Zealand

While the rationale for a low, positive inflation rate is grounded in solid economic theory, the specific choice of exactly "2 percent" is not derived from a complex mathematical formula. It originated as a pragmatic, somewhat accidental policy choice in New Zealand 92122.

In the late 1980s, New Zealand was battling chronic, high inflation 21. As part of a legislative overhaul to grant the nation's central bank operational independence, the government required the bank to commit to a specific, measurable target to ensure accountability 921. During a television interview, New Zealand's Finance Minister offhandedly remarked that he would ideally like to see inflation around 0 to 1 percent 922.

The Reserve Bank of New Zealand, realizing they needed to formalize a target following this public remark, accounted for some upward biases in inflation calculations and established a target band of 0 to 2 percent 922. It was an arbitrary figure plucked out of the air to anchor public expectations 9. However, the policy was a resounding success; inflation in New Zealand plummeted 921. Throughout the 1990s and 2000s, central banks in Canada, the UK, the European Central Bank (ECB), and eventually the US Federal Reserve (which officially adopted the target in 2012 under Chairman Ben Bernanke) copied the 2 percent figure 2021. Over time, it simply became the institutionalized global standard for central bank credibility 21.

The Danger of a Deflationary Spiral

The primary theoretical reason central banks cling to the 2 percent target is to establish a safety buffer against deflation - a sustained drop in general price levels 242227. While falling prices sound great to consumers at the grocery store, widespread deflation is widely considered an economic disaster 2329.

When prices are broadly expected to fall, rational consumers delay major purchases. Why buy a car or a house today if it will be 5 percent cheaper next year? 232924. This mass deferral of spending causes aggregate demand to collapse. Businesses lose revenue, forcing them to halt investments and lay off workers. As unemployment rises, consumer demand falls even further, forcing businesses to slash prices more aggressively just to survive. This vicious, self-reinforcing cycle is known as a deflationary spiral, and it was the defining mechanism that exacerbated the Great Depression 272924.

Greasing the Wheels of the Labor Market

Mild inflation also acts as an essential lubricant for the labor market 2325. In a dynamic economy, specific industries inevitably face downturns and need to restructure. To survive, a struggling company might need to reduce its real labor costs by 2 percent.

Human psychology dictates that workers fiercely resist nominal wage cuts; handing an employee a paycheck that is 2 percent smaller than last month destroys morale, damages productivity, and invites union strikes 1029. Economists refer to this as "sticky wages." However, if the overall economy has an inflation rate of 2 percent, that same company can simply freeze wages 929. The employee's nominal paycheck stays the same, but inflation quietly does the work of reducing their real wage by 2 percent. This phenomenon allows labor markets to adjust smoothly to economic shocks without triggering mass layoffs 232925. Additionally, nominal wage increases of 2 percent - even if they merely keep pace with inflation - provide a psychological boost and a sense of career progress for workers 20.

The Impact on Debt and Mortgages

Deflation mathematically increases the real burden of debt 272432. Because loans and mortgages are denominated in fixed nominal figures, falling prices and wages mean borrowers must use money that is more valuable to pay off their old debts, leading to widespread defaults, bankruptcies, and banking crises 2726.

Conversely, mild inflation actively benefits borrowers. If a consumer takes out a 30-year fixed-rate mortgage, the nominal balance remains exactly the same, but mild inflation steadily erodes the real purchasing power of the money owed 32272829. Over time, the borrower is repaying the lender with "depreciated dollars," effectively transferring wealth from the lender to the borrower 3229. While lenders are aware of this dynamic and price an "inflation premium" into interest rates at the time of origination, unexpected bursts of inflation still disproportionately benefit those holding long-term, fixed-rate debt 32.

Global Divergence: Do All Economies Target 2 Percent?

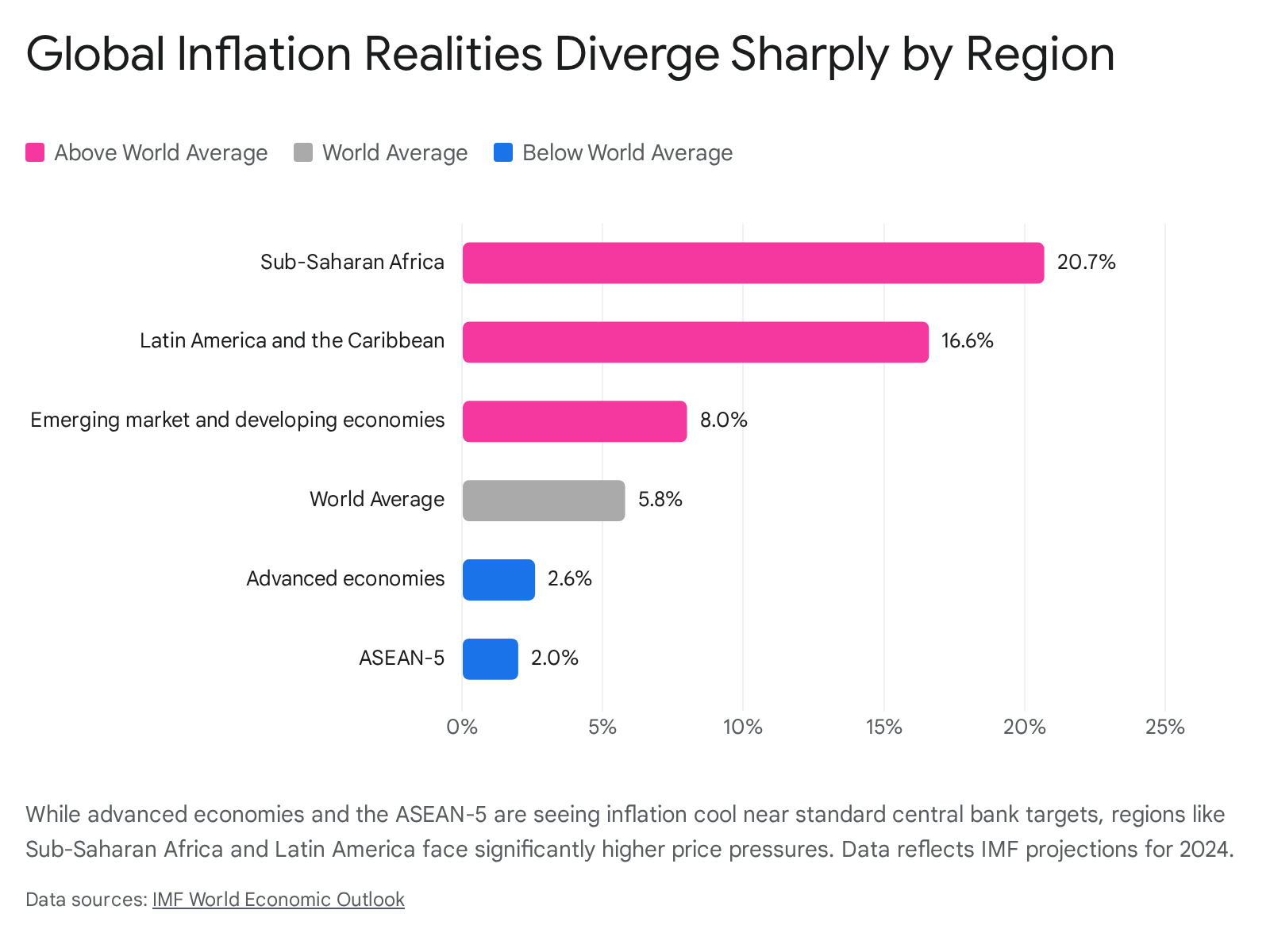

While 2 percent is the gospel for advanced, high-income economies, the picture looks very different in the developing world. Emerging Market Economies (EMEs) typically set their inflation targets noticeably higher, usually ranging between 2.5 and 6 percent 2530.

The International Monetary Fund (IMF) notes that this divergence is entirely logical 25. Emerging economies are fundamentally different from advanced ones: they grow much faster, experience higher baseline volatility, feature weaker institutional frameworks, and undergo rapid structural transformations 2531. A slightly higher inflation target gives central banks in developing nations more flexibility to absorb global commodity shocks and manage intense pressures on their exchange rates 253233. Pushing inflation down to 2 percent in a rapidly developing nation can require punitively high interest rates that actively stifle economic growth and infrastructure investment 25.

The table below outlines the current structural inflation targets (or target bands) for a selection of major global central banks, illustrating the divide between advanced and emerging markets.

| Economy / Country | Central Bank | Current Inflation Target | Context & Flexibility |

|---|---|---|---|

| United States | Federal Reserve | 2.0% | Adopted a "flexible average" targeting approach in 2020, allowing temporary overshoots to balance periods of low inflation 2241. |

| Euro Area | European Central Bank | 2.0% | Revised from "below but close to 2%" to a symmetric 2% target to prevent deflationary risks 34. |

| Mexico | Bank of Mexico (Banxico) | 3.0% | Expected by the IMF to converge to target by late 2025/2026 amidst moderately contractionary interest rates 354445. |

| Brazil | Central Bank of Brazil | 3.0% (± 1.5%) | Shifted to a continuous rolling measurement in 2025 rather than an end-of-calendar-year target assessment 363738. |

| South Africa | South African Reserve Bank | 3.0% - 6.0% | Exploring debates to lower the target point, as current inflation has persistently remained near the top of the band, straining the exchange rate 32. |

| Indonesia | Bank Indonesia | 2.5% | Steadily revised downward from 6% in 2005 to 2.5% in 2024 as the economy stabilized and structural reforms took hold 32. |

This disparity in targets results in distinctly different inflation realities globally. As global supply chains untangle and central bank interest rate hikes take effect, inflation is retreating, but at vastly different paces depending on the region's structural makeup and baseline targets.

The Modern Debate: Should the Target Be Higher?

In the wake of the painful 2021 - 2022 inflation shock and the aggressive interest rate hikes required to tame it, a quiet but serious debate has emerged among prominent economists regarding the sanctity of the 2 percent target 394041.

The Argument for 3 Percent

Economists such as Olivier Blanchard and Jason Furman have discussed whether advanced economies should raise their inflation targets to 3 percent 4041. The macroeconomic logic is tied to interest rates. A central bank's primary weapon during a recession is cutting interest rates to spur borrowing and investment. However, rates generally cannot be cut much below zero - a barrier known as the "zero lower bound."

If an economy targets 2 percent inflation, its baseline interest rates during normal times will be relatively low. If it targets 3 or 4 percent inflation, its baseline nominal interest rates will naturally sit higher. Therefore, when the next major recession hits, a central bank with a 3 percent inflation target would have significantly more mathematical room to slash interest rates and stimulate the economy before hitting zero 22. Furthermore, some economists argue that tolerating slightly higher inflation could prevent unnecessary job losses during the final, difficult phases of cooling an overheated economy 39.

The Credibility Risk

Despite these theoretical benefits, practicing central bankers remain deeply hesitant to officially change the target. The power of a central bank rests almost entirely on its credibility and its ability to anchor public expectations 942.

If a central bank moves the goalposts simply because inflation is proving difficult to tame, markets and consumers may permanently lose faith in the institution. As Federal Reserve policymakers have warned, if the public believes the central bank will tolerate higher inflation today, expectations will become unanchored 4243. This loss of trust could ironically ignite the very wage-price spirals central banks are trying to avoid, making inflation even harder to control in the long run 942. Consequently, while the 2 percent target may have originated as an arbitrary accident, abandoning it now carries immense psychological and economic risks.

Bottom line

Inflation is driven by a complex, interconnected web of excessive consumer demand, constricted supply chains, and the self-fulfilling psychology of wage-price spirals. While the post-pandemic era starkly proved how damaging rapid inflation can be to household purchasing power, a healthy macroeconomy actually relies on a low, steady rate of price growth - typically 2 percent in advanced economies - to prevent the crippling effects of deflation and to allow labor markets to adapt flexibly to shocks. Ultimately, whether central banks can maintain strict adherence to this 2 percent historical benchmark in an era of geopolitical fragmentation and structural supply shifts remains a defining uncertainty for the global economy.