How Fed Interest Rate Changes Affect Your Wallet

When the Federal Reserve adjusts its benchmark interest rate, it effectively changes the wholesale price of money for the entire banking system. These foundational policy shifts quickly alter the interest you pay on variable-rate debt like credit cards and the yield you earn on savings accounts, as banks immediately pass their increased costs or savings onto consumers. However, long-term borrowing costs, such as 30-year mortgages, are driven indirectly by global bond market expectations, meaning they can - and frequently do - move independently of the central bank's daily decisions.

What the Federal Reserve Actually Controls

The Federal Reserve does not directly dictate the interest rate on your auto loan, your 30-year fixed mortgage, or your high-yield savings account. Instead, the central bank of the United States controls a single, highly influential metric: the federal funds rate 12. Understanding this mechanism requires looking under the hood of the commercial banking system.

By law and operational necessity, depository institutions - such as commercial banks and credit unions - must hold a certain amount of reserve balances at the Federal Reserve 34. Because the daily flow of deposits and withdrawals fluctuates constantly, some banks end the business day with excess reserves, while others fall short of their regulatory or operational requirements 23. To bridge the gap, banks lend money to one another overnight on an uncollateralized basis 34. The interest rate charged on these overnight loans is the federal funds rate 34.

The Federal Open Market Committee (FOMC), the monetary policymaking body of the Federal Reserve, meets eight times a year to set a "target range" for this rate 34. When inflation runs too hot, the Fed raises the target range to make borrowing more expensive between banks, which subsequently cools consumer demand and slows down the broader economy 578. Conversely, when the economy slumps or the job market weakens, the Fed lowers the target range to make borrowing cheaper, stimulating corporate investment and household spending 86.

The Mechanics of Steering the Rate

To ensure the actual market rate - known as the effective federal funds rate (EFFR) - stays within its target range, the Fed utilizes several monetary policy tools rather than relying on mandates. The most prominent tool is adjusting the interest rate it pays banks on reserve balances (IORB), alongside open market operations and the overnight reverse repurchase agreement facility 234. By manipulating the baseline cost of capital in the banking sector, the Fed sets off a chain reaction that ultimately ripples through the entire global financial system.

Historically, this tool has been used to navigate severe economic turbulence. Between 1979 and 1982, Federal Reserve Chair Paul Volcker famously pushed the federal funds rate to nearly 20% to combat extreme stagflation 5. The "Volcker shock" successfully broke the back of inflation, but at the cost of a sharp recession where unemployment reached nearly 11% 5. More recently, the Fed raised rates aggressively from near-zero pandemic lows to a peak range of 5.25% to 5.50% in 2023, before initiating a series of cuts in late 2024 and through 2026 to stabilize a cooling labor market 26107.

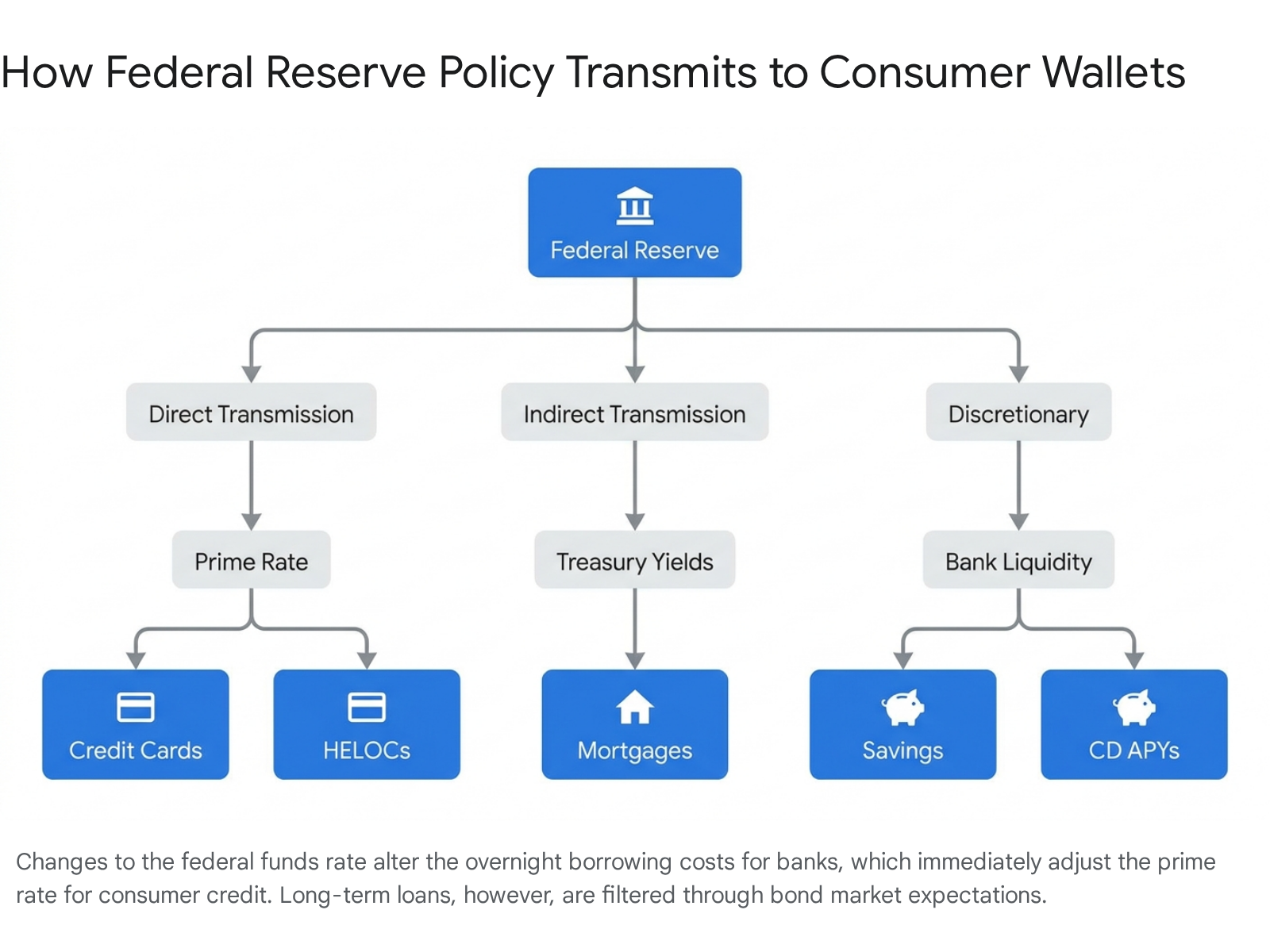

The Speed of Money: Direct vs. Indirect Impacts

The journey from the Federal Reserve's trading desk to your personal wallet varies wildly depending on the type of financial product you hold.

For some accounts, the impact is instantaneous and mathematically mandated. For others, the relationship is loose, delayed, and entirely at the discretion of individual financial institutions or the whims of the bond market.

To understand this dynamic, we must look at the Prime Rate. The prime rate is a benchmark interest rate that commercial banks charge their most creditworthy corporate customers 128. While no single entity "sets" the prime rate by law, it is universally determined by the federal funds rate plus a standard margin - historically about 3 percentage points 789. If the Fed's target range sits at a midpoint of 4.25%, the prime rate will generally hover around 7.25% 1011.

When the financial media reports that the Fed has raised or lowered interest rates, commercial banks almost immediately adjust the prime rate in lockstep 812. The prime rate, in turn, acts as the base index for trillions of dollars in consumer debt.

The speed and severity of a Fed rate change depend entirely on the underlying benchmark of your financial product. The table below summarizes how quickly these policy changes reach different corners of the consumer finance ecosystem.

| Financial Product | Primary Benchmark | Transmission Speed | Linkage Type |

|---|---|---|---|

| Credit Cards | Prime Rate | Immediate (Within 1-2 billing cycles) | Direct: Contractually tied to the Prime Rate via a set margin. |

| HELOCs | Prime Rate | Immediate (Days to weeks) | Direct: Variable rates adjust almost instantly when the Prime Rate moves. |

| Savings Accounts / CDs | Fed Funds Rate | Lagged (Days to Months) | Discretionary: Banks adjust based on their internal liquidity and need for deposits. |

| 30-Year Fixed Mortgages | 10-Year Treasury Yield | Preemptive / Disconnected | Indirect: Driven by bond market expectations, often moving before the Fed acts. |

Credit Cards and HELOCs: The Direct Hit

If you carry a balance on a credit card or hold a Home Equity Line of Credit (HELOC), you are on the frontline of Federal Reserve monetary policy.

Most credit cards and HELOCs feature variable interest rates 1212. Your cardholder agreement stipulates that your Annual Percentage Rate (APR) is calculated as the prime rate plus a predetermined "margin" based on your individual creditworthiness 121219. For example, if the prime rate is 7.25% and your bank's individualized margin is 15%, your credit card APR is exactly 22.25%.

When the Fed adjusts the federal funds rate, the prime rate moves in accordance 1219. Consequently, your credit card APR typically adjusts within a single billing cycle 12. The Federal Reserve Bank of Boston found that this transmission channel is highly effective at cooling consumer demand; when credit card interest rates increase by 1 percentage point, consumers actively reduce their credit card spending by an average of 8.7% in the following month 12. For the average account, this translates to a reduction of roughly $74 in monthly spending 12.

For HELOCs, the mechanism is virtually identical. A HELOC acts essentially as an adjustable-rate mortgage tied directly to the prime rate 1219. Lenders calculate HELOC rates by adding a margin on top of the prime rate based on the borrower's credit score and Combined Loan-to-Value ratio (CLTV) 1219. When the Fed hikes rates, the monthly dollar amounts homeowners must pay to service their HELOCs jump, pulling disposable income out of their wallets and slowing the broader economy 9.

Why Credit Card Rates Remain Stubbornly High

A persistent point of frustration and confusion for consumers is why credit card interest rates remain astronomically high, even when the Federal Reserve cuts the federal funds rate. By mid-2026, despite multiple rate cuts totaling well over a full percentage point since late 2024, the average credit card APR on accounts carrying a balance remained elevated near 23.79% - only slightly down from their all-time peak of 24.92% in 2024 611.

| Credit Card Category | Average APR (2026) | Typical Range |

|---|---|---|

| General Purpose (Rewards) | 21% - 24% | 17% - 28% |

| Store / Retail Cards | 30.14% | 22% - 36% |

| Secured Cards | 20% - 27% | 10% - 28% |

| Student Cards | 17% - 23% | 13% - 27% |

| Business Cards | 14% - 22% | 11% - 26% |

Research indicates that the base cost of funds (the prime rate) is only one piece of the puzzle. Credit card companies price their products based on several unique, structural factors that keep rates elevated regardless of central bank policy:

First, there is the issue of un-diversifiable default risk. Credit card debt is unsecured. If you default, there is no house or car for the bank to quickly repossess to make themselves whole 20. Economic research from the Federal Reserve Bank of New York reveals that credit card charge-offs - the rate of debt formally written off by banks as uncollectable - tend to spike uniformly across all credit score brackets during economic downturns 13. Because this risk is heavily correlated with the broader macroeconomy, it cannot be easily diversified away by the bank. To compensate for this un-diversifiable risk, banks are forced to price in a massive "default risk premium" upfront, which keeps the baseline margin extraordinarily high 1314.

Second, credit card operations carry exceptionally high operating and marketing costs. The modern credit card market is fiercely competitive regarding travel rewards, cash back, and lucrative sign-up bonuses. A Wharton study found that credit card operations consume 4% to 5% of dollar balances annually in operating expenses 13. Marketing budgets alone account for 1% to 2% of assets annually - roughly ten times the proportion spent by other banking divisions 13. Banks pass these massive customer acquisition costs directly onto the consumer through higher APR margins.

Finally, consumer behavior plays a massive role. Cardholders tend to respond far more energetically to the promise of rewards features (like airline miles or lounge access) than they do to the underlying interest rates they are charged 14. Many consumers fail to realize that the lucrative rewards enjoyed by transactors - those who pay their balance in full every month - are effectively subsidized by the high interest rates paid by revolvers, those who carry a balance from month to month 1415. Because consumers remain largely insensitive to the interest rate when choosing a rewards card, banks have little competitive incentive to lower margins even when the federal funds rate drops.

Mortgages: The Bond Market Disconnect

One of the most common misconceptions in personal finance is the belief that when the Federal Reserve cuts interest rates, 30-year fixed mortgage rates will automatically and proportionately drop. In reality, the Federal Reserve does not control mortgage rates, and the two metrics can - and frequently do - move in completely opposite directions 241617.

While the Fed controls overnight lending costs (the shortest possible term), mortgages are long-term loans. Therefore, the 30-year fixed-rate mortgage is primarily benchmarked to the 10-year U.S. Treasury note 241618.

Why do 30-year loans track a 10-year bond? The answer lies in consumer behavior. Most home buyers sell their homes or refinance their mortgages long before the 30-year term expires. Due to this prepayment behavior, the average lifespan (or duration) of a typical 30-year mortgage is actually somewhere between five and nine years 171819. Thus, institutional investors seeking to buy Mortgage-Backed Securities (MBS) demand a yield that is competitive with the safest comparable investment available: the 10-year U.S. Treasury note 2420.

Historical tracking shows that the 30-year fixed mortgage rate moves almost in lockstep with the 10-year U.S. Treasury yield. The two lines consistently track upward and downward together over decades, separated by a distinct gap known as the "mortgage spread," which typically ranges between 1.5 and 2.0 percentage points to compensate lenders for various risks 171820.

Deconstructing the Mortgage Spread

The mortgage rate offered to a prospective homebuyer is determined by adding a "spread" to the benchmark 10-year Treasury note rate. This spread is composed of two primary layers:

- The Primary-Secondary Mortgage Spread: This is the difference between the retail rate offered to the borrower and the wholesale yield on a mortgage-backed security in the secondary market. This portion of the spread covers the industry's tangible costs of originating the mortgage, lender profit margins, servicing fees, and government-sponsored enterprise guaranty fees 18.

- The Secondary Mortgage Spread: This is the difference between the yield on a mortgage-backed security and the rate of the 10-year Treasury note. This margin exists to compensate institutional investors for the additional risks inherent in mortgages compared to virtually risk-free government bonds. The primary fear is prepayment risk - the possibility that borrowers will refinance their loan early if interest rates drop, forcing the investor to reinvest their returned principal into a lower-yielding market 1821. It also covers minor credit risk, which is the possibility of default 18.

During times of severe economic stress, this spread can widen dramatically and behave unpredictably. When the Federal Reserve raises short-term rates aggressively to fight inflation, it often causes an inverted yield curve - an abnormal scenario where short-term borrowing costs become higher than long-term bond yields 31922. An inverted yield curve signals that the market widely expects an imminent economic slowing and subsequent rate cuts by the central bank.

When the yield curve inverts, the expected duration of newly originated mortgages drops sharply. Lenders assume that borrowers will immediately refinance as soon as the expected future rate cuts materialize 19. Because short-duration assets require higher yields in an inverted curve environment, mortgage prices are forced upward, causing the mortgage spread to "blow out" to unusually high levels, as witnessed during the volatile rate environments of late 2022 through 2024 181923.

Why Mortgage Rates Move Before the Fed

The bond market is incredibly efficient and forward-looking. Treasury yields fluctuate daily, minute by minute, based on investor expectations for future inflation, employment data releases, and anticipated central bank policy 241820.

By the time the Federal Reserve officially convenes to announce a rate cut, the bond market has often already "priced in" the move weeks or even months in advance 1720. Consequently, it is not uncommon for mortgage rates to stay entirely flat - or even rise - on the actual day the Fed cuts rates. For example, when the Fed aggressively cut the federal funds rate by 0.50 percentage points in September 2024, many consumers expected instant relief. Instead, the average 30-year mortgage rate rose from 6.09% on the day after the cut to as high as 6.84% by late November 18. This happened because the rate cut had already been priced in, and subsequent strong economic data caused investors to fear future inflation, triggering a massive sell-off in Treasury bonds that pushed yields and mortgage rates higher 241820.

Savings Accounts and CDs: The Bank's Discretion

While borrowers acutely feel the pain of Federal Reserve rate hikes, savers generally celebrate them. However, the transmission of the federal funds rate to your savings account is neither legally mandated nor instantaneous. It is a highly discretionary business decision made by your bank's treasury department.

When the Fed raises the federal funds rate, borrowing money overnight from other institutions becomes much more expensive. To fund their lucrative lending operations, banks must turn to the next best source of capital: consumer deposits 1024. To attract more deposits and ensure adequate liquidity, banks raise the Annual Percentage Yield (APY) on their savings accounts and Certificates of Deposit (CDs) to stay competitive 24.

The Lag in Savings Rates

Historically, banks are remarkably quick to lower savings rates when the Fed cuts, but lethargic to raise them when the Fed hikes. This asymmetrical behavior is driven by simple corporate profit maximization.

If the Fed lowers rates, banks' wholesale borrowing costs drop instantly. Finding themselves under far less pressure to attract retail deposits, they swiftly cut CD and savings yields to preserve their profit margins 1024. CD rates often drop the fastest and earliest. Because a CD locks the bank into paying a fixed rate to a consumer for months or years, if a bank anticipates that the Fed will cut rates in the near future, it will proactively slash its CD yields today to avoid overpaying for capital tomorrow 1025.

Conversely, traditional brick-and-mortar mega-banks rely heavily on "sticky" customers. These are consumers who prioritize the convenience of physical branches, ATMs, and bundled financial services, and who rarely endure the friction of moving their money 102425. These massive institutions often pay near-zero interest on savings (e.g., 0.01% APY) regardless of how high the federal funds rate climbs, simply because they already possess massive deposit bases and do not need to compete aggressively for capital 102425.

Online-only banks, unburdened by the massive real estate and personnel overhead of physical branches, operate on an entirely different business model. They actively compete for deposits by offering High-Yield Savings Accounts (HYSAs). During peak rate environments in recent years, while the national average savings APY sat around a dismal 0.38% to 0.40%, online HYSAs offered lucrative yields upwards of 5.00% APY 72526.

| Account Type | Liquidity & Access | Typical APY Behavior |

|---|---|---|

| Traditional Savings | High (Branch & ATM access) | Extremely low, rarely adjusts to Fed hikes. |

| High-Yield Savings (HYSA) | High (Online transfers) | Highly competitive, tracks Fed movements closely. |

| Money Market Accounts | High (Often includes check-writing) | Competitive, similar to HYSAs but may require higher minimums. |

| Certificates of Deposit (CD) | Low (Locked for a fixed term) | Fixed at origination, highly sensitive to future Fed expectations. |

The Impact of Inflation and Taxes on Real Yields

When evaluating savings rates, consumers must look beyond the advertised APY and consider their "real return" - the actual increase in purchasing power after accounting for inflation and taxes.

Inflation quietly reduces the value of money over time. If a HYSA pays 5.00% APY, but inflation runs at 2.7%, the real return is only about 2.3% 10. Furthermore, the IRS considers interest earned on savings accounts and CDs as ordinary income 10. Depending on your federal and state tax brackets, this can further erode the take-home yield. Therefore, while a high-yield account is vastly superior to a traditional checking account, relying solely on cash deposits during periods of high inflation can result in a net loss of real purchasing power, even if nominal rates seem historically high 610.

The Global Ripple Effect of US Monetary Policy

The Federal Reserve's dual mandate requires it to focus purely on domestic price stability and maximum employment, but its decisions create seismic macroeconomic waves across the global economy. The U.S. dollar is the world's primary reserve currency, and its value is inextricably linked to U.S. interest rates 36.

When the Fed aggressively hikes rates, dollar-denominated assets (such as U.S. Treasury bonds) begin to offer higher, safer returns than those available in other countries 527. Global capital efficiently flows out of foreign investments and emerging markets, flooding into the United States to capture these higher, risk-free yields 3627. This massive influx of capital fundamentally strengthens the value of the U.S. dollar against foreign currencies 3627.

While a strong dollar is a boon for American consumers - making imported goods and international travel significantly cheaper - it creates severe financial friction abroad, a phenomenon economists refer to as the "global financial cycle" 2728.

The Burden on the Global South

Many emerging market nations and foreign corporations hold substantial amounts of debt denominated in U.S. dollars. When the Fed raises rates and the dollar strengthens, the local-currency cost of servicing that dollar-denominated debt skyrockets 2728.

This dynamic is not merely theoretical; it has caused catastrophic financial crises. In the 1970s, Latin American countries received vast amounts of investment from international creditors, fueling an economic boom 5. However, following the Volcker shock in 1979, rising interest rates in the U.S. expanded Mexico's debt burden far beyond its repayment capacity 5. The result was the Latin American debt crisis of 1982 - a sudden curtailment of international credit across the region that prompted mass defaults and forced developing nations to redirect vital capital from poverty relief and social programs merely to service their foreign debt 5. Studies show that interest rate increases in northern, industrialized economies remain strongly correlated with the onset of banking crises in southern, developing economies 5.

Trade Channels and Imported Inflation

The global spillover effects also travel through trade channels. As foreign currencies weaken against the almighty dollar, other nations face the immediate threat of imported inflation. This is because globally traded commodities, most notably crude oil and agricultural staples, are almost universally priced in U.S. dollars 2729. When the dollar strengthens, it requires more of a foreign nation's currency to buy the exact same barrel of oil, directly driving up domestic inflation in that country.

To defend their currencies from freefall and stem catastrophic capital flight, foreign central banks are often forced to raise their own interest rates to match the Fed 2729. For instance, when the U.S. dollar surged, nations like Brazil were forced to hike rates in response to currency weakness, despite their own domestic economic concerns 27. This global tightening can stunt international economic growth, reduce global investment, and ultimately lead to lower demand for U.S. exports 272829.

Strategies for Navigating Rate Cycles

Interest rates move in vast, multi-year cycles, responding to the push and pull of macroeconomic forces. Whether you are facing an aggressive tightening cycle aimed at crushing inflation or a loosening cycle meant to stave off a recession, tactical financial adjustments can insulate your wallet and optimize your wealth. Financial anxiety during uncertain economic periods is common, but it is highly manageable if you focus on proactive, long-term goals rather than obsessing over daily rate fluctuations 30.

Moves for a Rising Rate Environment (Tightening)

When the Federal Reserve is aggressively raising rates to cool the economy, borrowing becomes punitive, but cash becomes king.

- Tackle Variable Debt Immediately: Your absolute highest priority should be paying off credit cards and adjustable-rate loans. Because the prime rate will adjust upward within weeks of a Fed announcement, carrying a balance on a 25% APR credit card becomes exponentially more expensive and can rapidly trap you in a debt spiral .

- Delay Discretionary Borrowing: If possible, delay taking out a Home Equity Line of Credit (HELOC) or financing a new vehicle. As rates climb, the monthly carrying cost of these large purchases will strain your cash flow .

- Wait on CD Locks: As rates climb, avoid locking your money into long-term Certificates of Deposit prematurely. Because yields are on an upward trajectory, a CD that looks attractive today may look anemic in six months. Stick to highly liquid High-Yield Savings Accounts until rates appear to peak 24.

Moves for a Falling Rate Environment (Easing)

When the Fed pivots to cutting rates to stimulate a sluggish economy, the playbook flips entirely. Borrowing becomes accessible again, but the yields on safe cash deposits begin to evaporate.

- Lock in Yields Quickly: As rate cuts approach, banks will rapidly and preemptively reduce APYs on HYSAs and CDs. Securing a long-term CD ladder - spreading investments across 1-year, 2-year, and 5-year terms - before the cuts fully materialize allows you to enjoy premium yields even as the broader market cools 1030. If you prefer a stable, liquid option, money market accounts can sometimes offer slightly higher rates than standard savings to keep funds accessible 30.

- Reevaluate Mortgages and Refinance: If long-term Treasury yields fall and mortgage rates drop significantly (typically by 1% or more below your current rate), aggressively investigate refinancing to lower your monthly payment 31. However, remember that mortgage rates may remain stubborn even if the Fed cuts, so maintaining a high credit score is essential to secure the best possible terms 31.

- Shift to Equities Strategically: Lower borrowing costs tend to boost corporate profits and fuel stock market growth 32. Decreasing yields on fixed-income investments generally make equities a more attractive asset class. However, this must be balanced against recessionary risks; if the Fed is cutting aggressively out of economic panic because consumer spending has cracked, corporate earnings may still falter, leading to stock market volatility 313233.

- Focus on Habits, Not Just Rates: The macroeconomic interest rate environment will always be out of your control. Even if savings yields drop from a peak of 5% down to 3%, a high-yield account remains vastly superior to a traditional checking account. Implementing smart strategies - like consistent monthly saving, aggressive debt avoidance, and diversified investing - will ensure your financial goals remain on track regardless of where the federal funds rate sits 82430.

Bottom line

The Federal Reserve's interest rate decisions act as the baseline heartbeat of the global financial system, setting the wholesale cost of money that dictates global capital flows. While changes to the federal funds rate immediately dictate the cost of carrying a credit card balance or a HELOC through direct adjustments to the prime rate, long-term products like 30-year mortgages are subject to the forward-looking, often disconnected whims of the bond market. For consumers, successfully navigating a changing rate environment requires understanding these varying transmission speeds: aggressively paying down variable-rate debt during hikes, locking in fixed yields before cuts occur, and accepting that the bond market will always attempt to price in the future long before the Fed officially acts.