How Much to Save for Emergencies and Where to Keep It

A fully funded emergency cushion should cover three to six months of essential living expenses, but crossing an initial starter threshold of $2,000 provides the most dramatic, immediate boost to a household's financial wellbeing. Savers should keep these funds strictly separated from daily checking accounts, utilizing high-yield savings accounts or a tiered structure of certificates of deposit and Series I Bonds to protect cash against inflation. Because human psychology is naturally wired for immediate gratification, the most successful savings strategies rely on automated transfers and gamified accounts to remove the cognitive friction associated with saving money.

The Fundamental Mechanics of Financial Resilience

An emergency fund is a highly liquid cash reserve specifically earmarked for unexpected financial shocks. Its primary purpose is to act as a financial buffer between a household and the high-cost debt spiral that inevitably follows a crisis. When financial planners and behavioral economists discuss emergencies, they generally divide these events into two distinct categories: spending shocks and income shocks 12.

Spending shocks are unanticipated, immediate costs that require sudden capital outlays. Common examples include a blown car transmission, an emergency medical procedure, or a critical home repair such as a failing HVAC system 123. By contrast, income shocks involve a sudden loss of incoming revenue, typically caused by corporate layoffs, a reduction in working hours, or a severe medical crisis that prevents an individual from performing their job 12.

It is equally critical to establish what an emergency fund is not. An emergency fund is neither an investment vehicle meant to generate long-term wealth, nor is it a secondary checking account for vacations, nor a "sinking fund" for predictable, irregular expenses 34. A twelve-year-old vehicle eventually requiring a new alternator, an annual property tax bill, or an aging pet needing veterinary care are highly predictable events 4. When an individual knows an expense is inevitable - even if the exact month remains unknown - the capital should be planned for in a separate budget category rather than drawn from emergency reserves 4. True emergency funds self-insure against the tail-risk of genuinely unforeseeable events.

The consequences of operating without this buffer are severe and compound over time. According to the Federal Reserve's 2024 Survey of Household Economics and Decisionmaking (SHED), when faced with a modest $400 unexpected expense, 37% of American adults reported they would need to finance the cost by carrying a balance on a credit card, borrowing from family, or selling personal assets . Furthermore, 13% of respondents indicated they would be entirely unable to pay the $400 expense by any means 5. A 2026 Bankrate survey paints a similarly precarious picture, revealing that only 47% of Americans have sufficient liquidity to cover a $1,000 emergency expense 67. Without liquid savings, a minor financial disruption forces households into high-interest consumer debt, effectively increasing the total cost of the emergency through compounding interest and late fees 239.

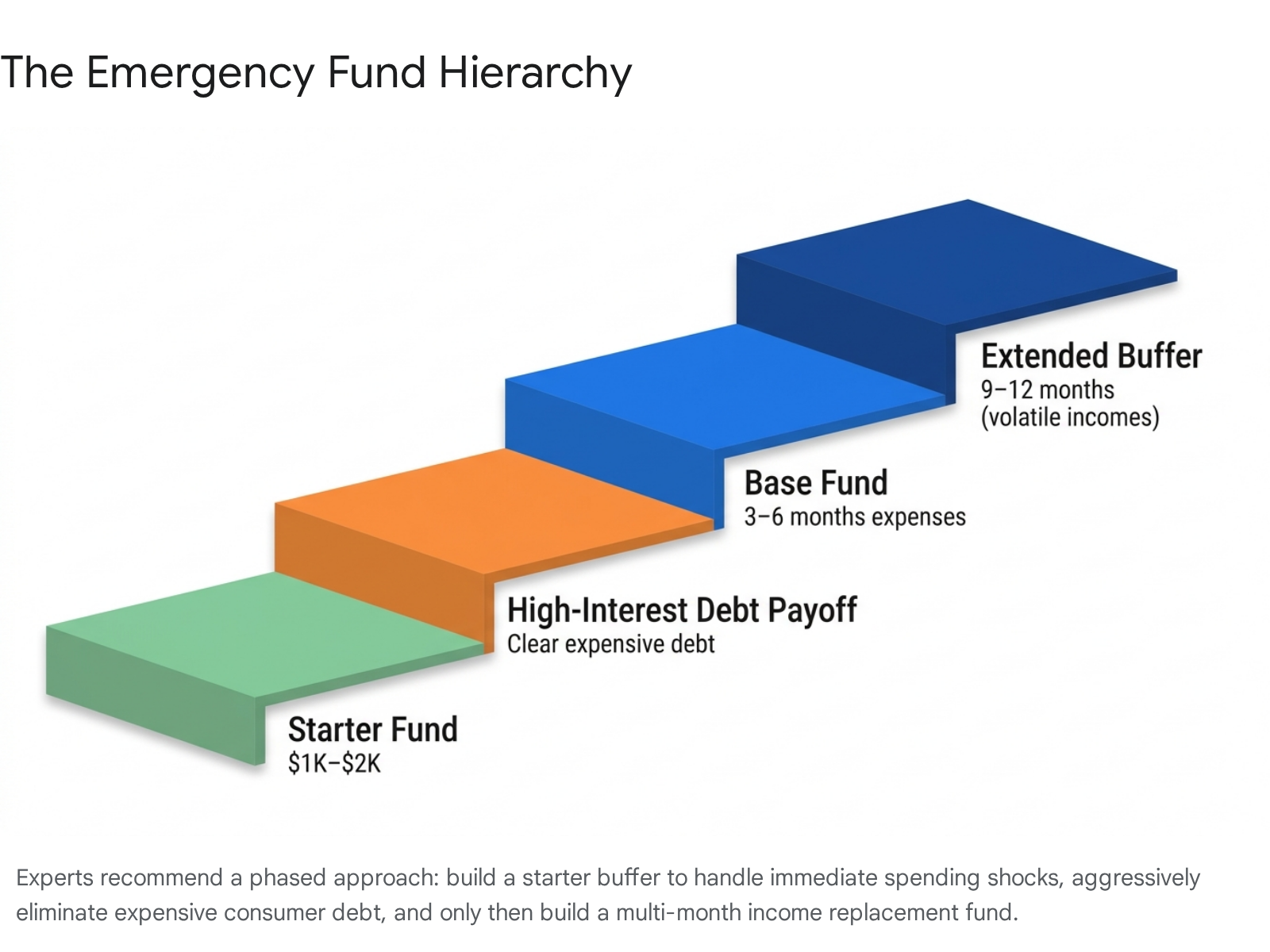

Determining the Appropriate Fund Size

The conventional financial wisdom to "save three to six months of expenses" has permeated personal finance literature for decades. However, behavioral research and modern economic data suggest that this blanket advice lacks the nuance required for varying household risk profiles. The exact size of an emergency fund must be dictated by the stability of the household's income, the rigidity of their expenses, and the broader macroeconomic environment 4.

Rather than aiming for a massive, singular target that can feel mathematically impossible for low-income earners, financial analysts advocate for a tiered, sequential approach to building reserves.

Tier 1: The Starter Buffer

If an individual is currently carrying high-interest consumer debt, such as a revolving credit card balance, the immediate goal should not be a six-month safety net. The first milestone is a starter fund designed solely to prevent minor crises from pushing the household further into debt. While $1,000 was the classic advice popularized in the late 20th century, inflationary pressures and the rising costs of goods mean that a $1,000 limit frequently falls short of covering modern spending shocks 108. For instance, recent automotive industry data indicates that the average cost of a sudden car repair has climbed to $838, consuming nearly the entirety of a traditional $1,000 starter fund in a single event .

Recent comprehensive behavioral research conducted by Vanguard surveyed over 12,400 investors and successfully pinpointed a highly effective "magic number" for this starter phase: $2,000 91011. The Vanguard data reveals that crossing the $2,000 threshold acts as an incredible psychological catalyst. Individuals who secure at least $2,000 in liquid savings report a 21% increase in personal financial well-being 91213. Remarkably, this specific dollar amount moves the needle on psychological wellbeing more than the difference between possessing $1 million in illiquid assets and possessing nothing 1011.

The lack of this starter buffer carries measurable costs in human capital and workplace productivity. The Vanguard study demonstrated that individuals without emergency savings spend an average of 7.3 hours per week worrying about or actively managing financial stress, compared to just 3.7 hours for those who maintain the $2,000 buffer 9. In the workplace, employees lacking a cash buffer spend approximately 6.1 hours a week visibly distracted by financial anxiety, which represents roughly 15% of their total working hours 1213. Furthermore, households without this buffer are three times more likely to report a year-over-year increase in financial stress 1013.

Tier 2: The Savings Versus Debt Dilemma

Securing the starter buffer immediately forces households to confront one of the most paralyzing decisions in personal finance: choosing whether to route subsequent extra cash toward paying down debt or toward expanding the emergency fund to a full three months.

A cash cushion protects against unexpected expenses, but carrying a balance on a consumer credit card at an average 21% Annual Percentage Rate (APR) acts as a mathematically guaranteed drain on net worth 414. The Consumer Financial Protection Bureau (CFPB) advocates for a calculated middle path. Their research indicates that households should build the $1,000 to $2,000 starter emergency fund first, and then temporarily pause aggressive savings while they redirect all surplus capital toward high-interest debt 14.

If an individual allocates absolutely every spare dollar to credit card debt while keeping zero cash in the bank, the next time an appliance breaks or a medical bill arrives, they will be forced to place that expense right back onto the credit card 914. The CFPB's experimental models and qualitative research show that people naturally desire to preserve a savings cushion, and households that maintain a small liquid buffer while simultaneously paying down debt are far more resilient against falling back into a debt spiral 14.

Tier 3: The Standard Baseline

Once high-interest consumer debts are completely cleared, individuals should resume expanding the emergency fund to cover three to six months of living expenses. This tier serves as an income replacement mechanism, providing the financial runway necessary to secure new employment after a layoff without facing eviction, foreclosure, or severe lifestyle degradation 115.

A critical distinction must be maintained when calculating this figure: the target is three to six months of essential expenses, not three to six months of total gross income 316. Essential expenses are strictly defined as housing costs (rent or mortgage), utility bills, basic groceries, required transportation, insurance premiums, and minimum debt payments on low-interest loans like student debt or auto loans 31516. Discretionary spending, dining out, and entertainment are excluded from this calculation.

To quantify this using recent macroeconomic data, the U.S. Bureau of Labor Statistics (BLS) Consumer Expenditure Survey for 2024 reports that the average American consumer unit spends roughly $78,535 annually 5. Therefore, a baseline three-month emergency fund consisting of average expenses equates to approximately $19,634, while a full six-month buffer would require nearly $39,268 5. When analyzing current household preparedness against these figures, the data highlights a massive shortfall. The Federal Reserve reports that only 55% of U.S. adults have three months of expenses saved, and 30% of adults indicate they could not cover three months of expenses by any means, even if they resorted to borrowing or selling assets 5.

Tier 4: The Extended Buffer for Income Volatility

The traditional six-month rule fundamentally assumes a standard W-2 employment model where finding a replacement job follows a predictable timeline. However, for households characterized by high income volatility, financial analysts recommend a significantly deeper well of liquidity, extending the target to 9 to 12 months 820.

This extended buffer is highly recommended for freelancers, independent contractors, and gig economy workers. As of recent data, 68% of Gen Z freelancers report experiencing severe income volatility, and 41% entirely lack a basic three-month emergency fund 17. Gig workers operate without severance packages, corporate health insurance, or guaranteed weekly hours, placing the entire burden of financial smoothing onto their personal savings 2018.

An extended 9-to-12-month buffer is equally vital for individuals working in highly specialized fields, or industries actively undergoing severe disruption due to artificial intelligence or macroeconomic shifts, where securing a comparable role could legitimately take the better part of a year 423. Finally, households heavily reliant on a single earner - especially those with multiple dependents or chronic medical conditions - require larger reserves to offset the concentrated risk of a single point of failure 231920.

Target Fund Sizes by Household Profile

| Household Profile | Income Stability | Target Size | Primary Purpose |

|---|---|---|---|

| In Debt / Starting Out | Variable | $1,000 - $2,000 | Prevent new high-interest debt from minor spending shocks. |

| Dual-Income W-2 | High (Two salaries) | 3 Months of Expenses | Cover a single job loss; the secondary income provides a floor. |

| Single-Income W-2 | Moderate (One salary) | 6 Months of Expenses | Full income replacement during a prolonged job search. |

| Freelancer / Gig Worker | Low / Highly Volatile | 9 - 12 Months of Expenses | Survive lean months, delayed client payments, and industry downturns. |

Strategic Account Selection for Liquidity and Yield

When determining where to park an emergency fund, individuals must constantly balance three competing priorities: safety from market loss, immediate liquidity for access, and sufficient yield to protect purchasing power against inflation 26.

Financial guidance universally dictates that an emergency fund should never be placed into equities or long-term investment accounts like mutual funds or ETFs 32627. The stock market carries significant price fluctuations. In the event of a macroeconomic recession, a worker is highly likely to experience a job loss at the exact moment their equity portfolio crashes in value. Being forced to liquidate stocks at a loss to pay for groceries defeats the entire purpose of a cash buffer 2627. Instead, savers should leverage specialized cash-equivalent vehicles.

High-Yield Savings Accounts (HYSAs)

For the vast majority of emergency savings, a High-Yield Savings Account serves as the optimal primary home. While traditional brick-and-mortar bank accounts frequently pay a practically nonexistent 0.01% Annual Percentage Yield (APY), online HYSAs operate without the overhead costs of physical branches, passing those margins back to the consumer in the form of elevated interest rates 212223.

As of May 2026, the Federal Deposit Insurance Corporation (FDIC) reports the national average savings rate sits at a meager 0.38% 522. In stark contrast, top-tier HYSAs are yielding between 3.80% and 4.21%, delivering more than ten times the national average 222425. Maintaining $10,000 in a traditional account yielding 0.01% generates roughly $1 a year, whereas the same capital in a 4.21% HYSA yields over $420 22.

These accounts provide federal insurance protection up to $250,000 per depositor and maintain high liquidity, generally allowing capital to be transferred to a primary checking account within one to three business days 32626.

Money Market Accounts (MMAs)

Money Market Accounts function quite similarly to HYSAs but frequently offer check-writing privileges and debit card access, making the funds slightly more liquid and accessible in a true emergency 202721. To offset this convenience, banks typically require higher minimum balances - often $2,500 or more - to avoid monthly maintenance fees 202721. Furthermore, while bank-issued MMAs are FDIC-insured, money market mutual funds held in brokerage accounts are not, though they are generally protected by the Securities Investor Protection Corporation (SIPC) and maintain stable net asset values 2026.

Certificates of Deposit (CDs)

A Certificate of Deposit requires an individual to lock their capital away for a rigidly specified term ranging from a few months to several years. In exchange for surrendering liquidity, the bank provides a guaranteed, fixed interest rate that is often higher than a variable savings account 272126. If funds are withdrawn prior to the maturity date, the saver incurs a penalty, typically forfeiting several months of earned interest 202726.

Because true emergencies demand immediate access to cash, financial planners caution against placing an entire emergency fund into a CD 2026. However, sophisticated savers frequently utilize a strategy known as a "CD Ladder" for the back-half of their fund - specifically months four through six of their reserves 2134. By staggering the maturity dates of multiple CDs, a portion of the cash becomes liquid at regular intervals, capturing higher yields without locking up the entire safety net 2134.

Series I Savings Bonds (I-Bonds)

Issued directly by the U.S. Treasury, Series I Savings Bonds are unique, non-marketable assets engineered specifically to protect cash from the erosive effects of inflation 2728. The total interest rate on an I-Bond is composite, calculated from two distinct components: a fixed rate that remains constant for the 30-year life of the bond, and an inflation rate that resets every six months based on changes in the Consumer Price Index for all Urban Consumers (CPI-U) 2729.

For bonds issued during the May 1, 2026, to October 31, 2026 period, the composite rate sits at a highly competitive 4.26%, which combines a 0.90% fixed rate with a 3.36% annualized inflation rate 2930. Interest accrues monthly and compounds semiannually, meaning the interest rate is applied to a growing principal value 2728. Crucially, the Treasury guarantees that even in periods of severe deflation, the combined rate will never fall below zero 27.

Despite the attractive yields, I-Bonds carry severe liquidity constraints. By federal law, they cannot be cashed out for the first 12 months under any circumstances 2831. Furthermore, if the bonds are redeemed before five years, the owner forfeits the previous three months of interest 2831. Due to the strict one-year lockup, I-Bonds must only be used for the deepest, "extended" portion of an emergency fund. A common and safe accumulation strategy involves purchasing I-Bonds incrementally while maintaining a large, liquid cash buffer in an HYSA. As the 12-month lockup periods expire on the older bonds, the saver gradually shifts their long-term safety net over to Treasury assets 31.

Comparing Emergency Fund Vehicles

| Account Type | Liquidity Constraints | Typical Yield Profile (2026) | Optimal Role in Strategy |

|---|---|---|---|

| Traditional Checking | Instant access. | Near 0.00% | Daily operating expenses only; inappropriate for savings. |

| High-Yield Savings (HYSA) | 1-3 Business Days. | ~3.80% - 4.21% | The core foundational layer (Months 1-3) of the emergency fund. |

| Money Market Account (MMA) | Instant (via Check/Debit). | ~3.90% - 4.10% | Alternative to HYSA for larger balances where check access is desired. |

| CD Ladder | Poor (Early withdrawal penalties). | Variable (Fixed terms). | Illiquid upper tiers (Months 4-6) capturing guaranteed fixed rates. |

| Series I-Bonds | Locked for first 12 months. | 4.26% (Inflation-adjusted). | Deep, long-term reserves specifically shielding against heavy inflation. |

The Behavioral Finance of Saving: Outsmarting Cognitive Friction

Understanding the basic arithmetic behind an emergency fund is simple; executing the required behavior is notoriously difficult. Traditional economic models assume humans act rationally to maximize utility, but the subfield of behavioral finance - which blends psychology and economics - demonstrates that human financial decision-making is heavily distorted by cognitive biases, emotional impulses, and heuristics 323334.

The primary psychological hurdle preventing successful saving is known as present bias, or hyperbolic discounting. This is the cognitive tendency for the human brain to place a disproportionately high value on small, immediate rewards at the expense of much larger, long-term security 35363738. To the human nervous system, spending $100 today on a tangible luxury triggers an immediate dopamine response. Conversely, transferring $100 into a savings account to protect against a hypothetical future crisis feels abstract, offering no immediate gratification and instead triggering feelings of loss and pain 3638.

Because the gap between intention and behavior is so vast, financial educators emphasize that relying on sheer willpower to save money is a failing strategy. Instead, individuals must design a structural architecture that outsmarts their own biases 36.

Utilizing Automation and Defaults

Every time an individual is required to manually transfer money from a checking account into savings, present bias is given an opportunity to hijack the decision 36. The most robust defense against this is automation. By setting up an automatic, recurring transfer to execute on the exact day a paycheck clears, the capital is moved before the brain registers it as "available to spend" 2373948.

This leverages the "status quo bias" or inertia 3648. Behavioral studies on retirement planning, such as the famous SMarT program experiments by Benartzi and Thaler, proved that changing the default structure from opt-in to opt-out drastically increases participation rates 36. When automation handles the heavy lifting, inertia works in favor of the saver rather than against them.

Mental Accounting and Cognitive Compartmentalization

Economically speaking, money is entirely fungible - a dollar in a checking account has the exact same purchasing power as a dollar in a savings account. However, human psychology relies heavily on "mental accounting," a phenomenon where individuals assign different subjective values to money based on where it is located and how it is labeled 3548.

If an emergency cushion is commingled within a primary checking account, it is highly likely to be absorbed by lifestyle inflation and discretionary spending 316. Financial advisors highly recommend opening a separate HYSA at an entirely different banking institution to introduce deliberate cognitive and physical friction 162640. Removing the convenience of instant, same-screen transfers forces a pause. Furthermore, simply labeling the account specifically as "Emergency Fund" alters its psychological profile. Because the money is explicitly earmarked, attempting to withdraw it for a non-emergency triggers "loss aversion" - the phenomenon where the pain of losing something feels twice as intense as the pleasure of gaining it - effectively causing the saver to protect the funds from their own impulses 33354841.

Technological Innovations: Gamification and Prize-Linked Savings

To fundamentally counteract the lack of immediate gratification inherent in saving, financial technology companies and traditional banks are increasingly turning to behavioral gamification 4243.

By integrating game-like elements into financial applications, institutions seek to transform the abstract chore of saving into a highly engaging, rewarding experience 444546. Applications utilize digital badges, consecutive daily streaks, progress visualization dashboards, and micro-bonuses to trigger short-term reward cycles 43444647. These features heavily leverage the "goal gradient principle" - a behavioral mechanism demonstrating that individuals naturally accelerate their efforts as they visually approach a clearly defined target 46. Empirical research on digital nudges indicates that gamified goal-setting can increase savings deposits by upwards of 18% over a six-month period compared to non-gamified control groups 42.

Perhaps the most fascinating and impactful behavioral innovation in personal finance is the advent of the Prize-Linked Savings Account (PLSA). Across the United States, households spend an average of $600 annually on lottery tickets, largely because low-income individuals fall victim to the availability heuristic and view the highly skewed lottery payoff as their only viable mechanism for a large financial windfall 484950.

PLSAs harness this exact psychological drive, redirecting the human desire to gamble into positive financial behavior 484951. Rather than paying a standard, guaranteed interest rate to every depositor, the financial institution pools a portion of the generated interest and raffles it off as massive cash prizes to account holders 4851. Depositors receive the exact same neurological thrill and anticipation of a lottery drawing, but with absolute principal security 484951. Even if an individual never wins a raffle, they keep 100% of the capital they deposited.

Research indicates that PLSAs are incredibly effective at converting non-savers into consistent depositors. Programs like "Save to Win" in the United States and Nationwide's "Start to Save" in the United Kingdom have successfully demonstrated that substituting the psychological pain of delayed gratification with the immediate thrill of a game dramatically increases both the frequency and volume of savings among financially fragile populations 48505152.

Macroeconomic Context: Why U.S. Households Require Larger Buffers

When international economists analyze standard American financial advice, the recommendation to hoard six full months of living expenses often stands out as uniquely massive. This requirement is not arbitrary; it is a direct reflection of structural differences in global social safety nets 5354.

In the United States, employment is intrinsically tied to health insurance access. If an American worker loses their job, they not only lose their salary but must also fund incredibly expensive COBRA health insurance premiums entirely out of pocket during a period of zero income 185354. Furthermore, state unemployment benefits in the U.S. are generally less comprehensive and harder to access than in peer nations, and the U.S. ranks below the OECD average in measures of social support, exhibiting a relative poverty rate of 17.8% 5355. Consequently, in the event of an economic downturn, the U.S. heavily relies on Congress to pass emergency stimulus packages rather than relying on automated welfare triggers 5355.

By stark contrast, European workers operate within systems that provide robust institutional emergency funds, reducing the burden on personal liquidity 5354. In Germany, the standard jobless benefit replaces 60% of a worker's previous salary for an entire year 5355. In France, unemployed workers can receive up to 75% of their previous daily wage for up to two years, while retaining universal access to high-quality medical care without fear of medical bankruptcy 535455. OECD unemployment data from early 2026 shows the U.S. at a 4.2% unemployment rate, Germany at 3.5%, and nations like Spain battling rates as high as 10.9% 565758. However, because the macroeconomic safety net in the U.S. is structurally thinner, the mathematical burden of surviving those periods of unemployment falls squarely on the cash reserves of the individual household, necessitating significantly larger personal emergency funds 535459.

Bottom line

Building a resilient emergency fund is less about achieving mathematical perfection and far more about constructing psychological defenses against financial shocks. While the ultimate objective is to accumulate three to six months of essential living expenses - or up to twelve months for those with volatile gig economy incomes - securing a highly liquid $2,000 starter buffer provides the most significant and immediate reduction in personal financial stress. To protect against the erosive effects of inflation and outsmart inherent present bias, this capital should be automated into separate high-yield savings accounts or structured Treasury assets, ensuring the funds remain out of sight for daily discretionary spending but immediately accessible when life inevitably disrupts financial plans.