Why Interest Rates Ripple Through the Economy

When a central bank alters its benchmark interest rate, it sets off a cascading chain reaction that permanently alters the cost of capital, the value of collateral, and the psychology of consumers and businesses. This transmission mechanism forces commercial banks to tighten lending, shifts the global value of currencies, and mechanically depresses the valuation of assets like housing and stocks. Because these policy changes must filter through millions of individual financial decisions, it typically takes the broader economy twelve to twenty-four months to fully register the impact on employment and inflation.

The Financial Plumbing: How Transmission Works

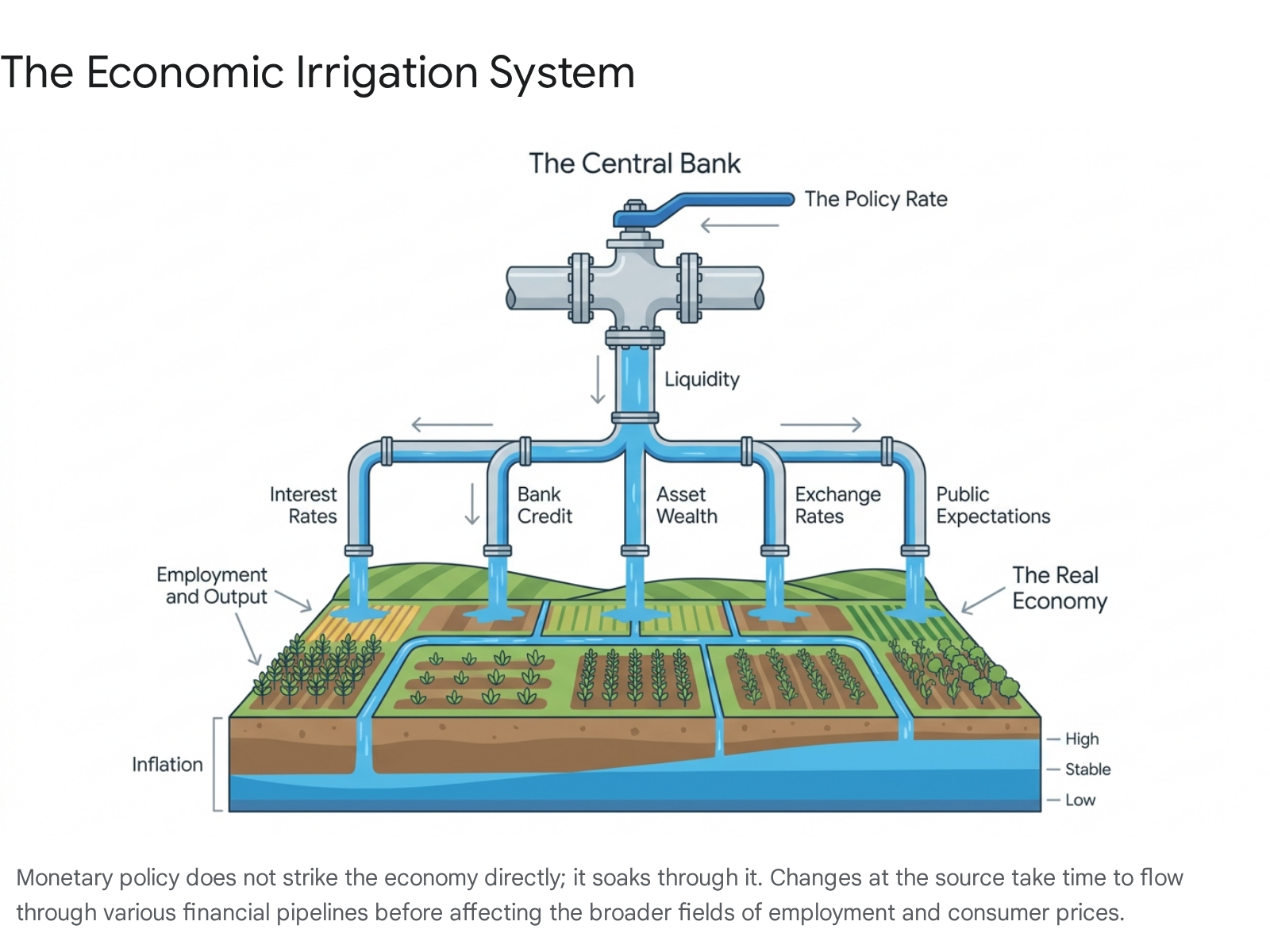

To understand how a single interest rate controlled by a central bank can cool down a soaring global economy or rescue a crashing one, economists often use the analogy of a massive plumbing or irrigation system 12. The central bank does not directly dictate the interest rate you pay on a credit card or a car loan, nor does it hand out money to individual businesses. Instead, it operates the primary pressure valve at the reservoir of the financial system.

Imagine the economy as a sprawling agricultural field. The central bank is the agency in charge of the water supply. Its mandate is to keep liquidity flowing enough to maximize crop yields, which represent job creation and economic output, but not to pump in so much liquidity that it causes destructive flooding, which represents runaway inflation 12.

When the central bank turns the dial to increase interest rates, it is tightening the water pressure. The central bank achieves this by adjusting the rate at which commercial banks lend reserves to one another overnight 23. Because commercial banks rely on these overnight reserves to meet regulatory requirements and settle daily transactions, increasing the cost of these funds directly squeezes their profit margins. To compensate, commercial banks pass those higher fundamental costs down the pipeline to their customers.

The Hidden Pipes: Repos, Reserves, and Collateral

The exact mechanisms of this plumbing have evolved significantly over the past two decades. Historically, central banks operated in environments where bank reserves were scarce. They would conduct open market operations, buying or selling small amounts of government bonds to slightly adjust the supply of cash, thereby hitting their target interest rate 46.

However, following the 2008 financial crisis, central banks engaged in Quantitative Easing (QE), flooding the system with trillions of dollars in reserves 7. In an environment of abundant reserves, the old method of transmission no longer worked. Instead, modern central banks like the Federal Reserve manage rates using an "interest on reserves" floor system and reverse repurchase agreements (reverse repos) 67.

Through standing repo facilities and reverse repos, the central bank directly interacts not just with massive commercial banks, but with non-bank financial companies like money market funds. By setting the rate they pay on these risk-free deposits, central banks establish an absolute floor for interest rates. Because no rational investor will lend money to a risky private business for less than the central bank is paying for a completely risk-free deposit, the entire structure of global interest rates shifts upward instantly when the central bank adjusts this rate 67.

The Reverse Transmission Mechanism

Furthermore, modern financial plumbing features a "reverse transmission mechanism" driven by the velocity of collateral. Government bonds are used as collateral in trillions of dollars of daily derivative and repo transactions 7.

When central banks shrink their balance sheets during a tightening cycle - a process known as Quantitative Tightening (QT) - they release long-term bonds back into the open market. This sudden increase in available, high-quality collateral can change the effective supply and demand dynamics at the long end of the yield curve. When money market funds buy up this long-term collateral, it pulls cash away from short-term lending, causing short-term borrowing costs to spike even if the central bank has not officially touched its target policy rate 7. This complex interaction highlights that monetary policy is not a simple lever, but a delicate recalibration of the entire financial ecosystem's balance sheet.

The Five Core Channels of Monetary Transmission

While financial media often discusses "the interest rate" as a monolith, central bank policy actually ripples through the real economy via five distinct, overlapping transmission channels. These channels operate simultaneously, though their relative strength varies depending on a nation's financial architecture and the prevailing economic climate 8.

The Traditional Interest Rate Channel

The most direct and widely recognized pathway is the interest rate channel. Because consumer prices and wages are "sticky" - meaning they adjust slowly to new economic realities - a change in the central bank's nominal interest rate directly changes the "real" interest rate, which is the nominal rate minus the expected rate of inflation 89.

The real interest rate is the mathematical foundation for human and corporate spending decisions. When real rates rise, the fundamental cost of capital increases 310. For households, the financing costs for consumer durables like automobiles, appliances, and home renovations become prohibitively expensive, dampening the desire to spend.

For corporations, the impact is governed by the hurdle rate for capital expenditures. A business deciding whether to build a new manufacturing facility or invest in new software will run a discounted cash flow analysis 89. At a 2% cost of borrowing, the future revenues from that factory make the project highly profitable. At a 6% cost of borrowing, the financing expenses devour the projected profit margin, and the expansion is cancelled. By mathematically halting these projects and purchases, the interest rate channel mechanically pulls aggregate demand out of the economy, eventually relieving upward pressure on consumer prices 2811.

The Credit and Risk-Taking Channels

While the interest rate channel focuses on the price of borrowing, the credit channel focuses on the strict availability of loans 5. This channel operates on the reality that financial intermediaries, particularly commercial banks, face their own balance sheet constraints.

When policy rates rise, banks' internal costs to secure funding increase. Concurrently, higher interest rates depress the overall economy, increasing the statistical probability that existing borrowers will default on their obligations. Faced with tighter margins and a riskier macroeconomic environment, banks systematically tighten their lending standards 1167. They demand higher credit scores, require more substantial down payments, and often categorically refuse to lend to riskier small and medium-sized enterprises (SMEs) 8.

This dynamic is closely tied to the "balance sheet channel." Borrowers use their existing assets, such as real estate or corporate inventory, as collateral to secure loans. Because higher interest rates depress asset values, the mathematical value of a borrower's collateral shrinks 58. Even if a business is perfectly willing to pay an exorbitant 9% interest rate to secure vital funding, the bank will deny the loan because the business no longer possesses enough high-quality collateral to back the debt.

Furthermore, central bank policy governs the "risk-taking channel." When rates are kept artificially low for extended periods, it compresses the yields on safe assets like government bonds. Institutional investors and banks, desperate to meet their return targets, are forced to migrate further out on the risk curve, actively seeking higher-yielding, lower-quality corporate debt - a phenomenon known as the "search for yield" 11. When central banks abruptly reverse course and hike rates, this risk-taking behavior violently unwinds. Credit markets freeze as lenders suddenly refuse to finance anything but pristine, AAA-rated entities, starving the broader economy of operating capital.

The Asset Price and Wealth Channel

Interest rates act as the financial gravity for all asset valuations. The fundamental valuation of any financial asset - be it a share of stock, a corporate bond, or a single-family home - is calculated as the present value of its future cash flows 2. When interest rates rise, the discount rate applied to those future cash flows rises in tandem, making the present value of stocks and real estate mechanically less valuable 29.

As housing and equity prices stall or actively decline, the psychological "wealth effect" takes hold. Homeowners and investors track their net worth closely. When they see their retirement portfolios shrink and their home equity evaporate, they feel significantly poorer, even if their day-to-day salary has not changed 26. Feeling financially vulnerable, households tighten their belts, cancel luxury vacations, delay vehicle upgrades, and increase their precautionary savings 9.

This channel also has profound distributional effects across society. High inflation disproportionately devastates lower-income households and retirees on fixed pensions. Conversely, aggressive interest rate hikes disproportionately harm highly leveraged households and young families trying to enter the housing market, while actively benefiting cash-rich entities and retirees who suddenly enjoy substantial, risk-free yields on their bank deposits 101819.

The Exchange Rate Channel

In an era of hyper-globalization, the exchange rate is a vital and rapid transmission mechanism, particularly for open economies deeply integrated into international trade. Global capital is highly mobile and constantly crosses borders in pursuit of the highest risk-adjusted return 8.

If the US Federal Reserve aggressively raises interest rates while the European Central Bank keeps them stagnant, US Treasury bonds suddenly offer a more attractive yield than European sovereign debt 1121. Global macro funds and institutional investors will sell their Euros and purchase US Dollars to acquire those American bonds. This massive, coordinated capital flow rapidly appreciates the value of the US Dollar 38.

A strong domestic currency exerts powerful disinflationary pressure. It makes foreign imports vastly cheaper for domestic consumers, directly lowering the price of goods on store shelves. However, it also makes domestically manufactured exports much more expensive for foreign buyers 89. This dynamic acts as a dual-edged sword: it crushes domestic manufacturing and export-reliant industries, leading to job losses and reduced corporate investment, which further cools the domestic economy 8.

The Expectations Channel

Perhaps the most potent, yet ethereal, of the transmission channels is how central banks shape public psychology. Inflation is largely a self-fulfilling prophecy. If consumers collectively believe that prices will rise by 10% next year, they will logically rush to purchase goods, appliances, and vehicles today before they become more expensive. This panic-induced surge in aggregate demand directly causes the exact price increases they feared 222.

Simultaneously, workers anticipating 10% inflation will demand 10% wage increases to protect their purchasing power. Corporations, facing exploding labor costs, will pass those costs onto consumers via higher prices, cementing a dangerous "wage-price spiral" 23.

By decisively raising interest rates and communicating an unyielding commitment to price stability, a central bank can "anchor" these expectations 211. If the public implicitly trusts that the central bank will induce a painful recession rather than tolerate inflation, workers will accept smaller wage increases, and consumers will revert to normal saving and spending patterns. During the 2022 tightening cycle, economists noted a massive shift in market-perceived policy rules; survey data indicated that the public's expectation of how aggressively the Fed would respond to inflation jumped from a near-zero correlation to a one-for-one response 23. This psychological anchoring often achieves the central bank's goals before the physical interest rate hikes have even fully penetrated the credit markets.

Evaluating the Efficacy of Transmission Channels

| Transmission Channel | Primary Mechanism of Action | Main Sector Affected | Speed of Transmission | Fails or Weakens When... |

|---|---|---|---|---|

| Interest Rate | Alters the pure cost of capital, shifting the incentive to save versus the incentive to spend. | Broad consumer durables, housing, and large-scale business capital investment. | Fast to Medium (Weeks to Months). | The economy hits the "effective lower bound" (rates approach zero) and conventional cuts lose impact. |

| Credit / Lending | Shrinks banks' willingness to supply loans and destroys the market value of borrower collateral. | Small-to-medium enterprises (SMEs) and highly leveraged households without capital market access. | Slow (Months to Years). | Banks suffer capital crises, or when shadow banking entities easily bypass traditional banking regulations. |

| Asset Price / Wealth | Alters the perceived net worth of asset holders, mechanically shifting consumer confidence and spending habits. | Existing homeowners, equity investors, and luxury goods markets. | Medium (Months). | Asset markets are insulated by massive external structural shortages (e.g., severe multi-decade housing supply deficits). |

| Exchange Rate | Appreciates currency value, cheapening imports while devastating the competitiveness of domestic exports. | Manufacturing, export-heavy industrial bases, and import-reliant consumers. | Fast (Days to Weeks). | The country operates on a strictly pegged or highly managed fixed exchange rate regime. |

| Expectations | Alters inflation psychology, resetting future wage contract negotiations and corporate pricing models. | Broader labor markets, union negotiations, and long-term corporate strategic planning. | Very Fast (Immediate upon credible central bank announcement). | The central bank loses public credibility after a history of policy flip-flops or persistent target failures. |

Data synthesized from the Bank for International Settlements, the Federal Reserve, and the European Central Bank 23811.

The Waiting Game: Why Does Transmission Take So Long?

A persistent source of frustration among consumers, corporate executives, and politicians is the agonizingly delayed reaction of the real economy to central bank action. When a central bank announces a dramatic 75-basis-point rate hike, inflation does not miraculously drop the next morning. Economists refer to this temporal disconnect as the "impact lag" - the time required for an adjustment in the overnight bank rate to filter through the complex web of financial markets and tangibly alter human behavior 811.

Milton Friedman famously theorized that monetary policy operates with "long and variable lags." Because the impact lag is both protracted and unpredictable, discretionary monetary policy risks inadvertently destabilizing the economy; policymakers might tighten conditions just as a natural recession begins, or ease conditions just as organic inflation accelerates 8.

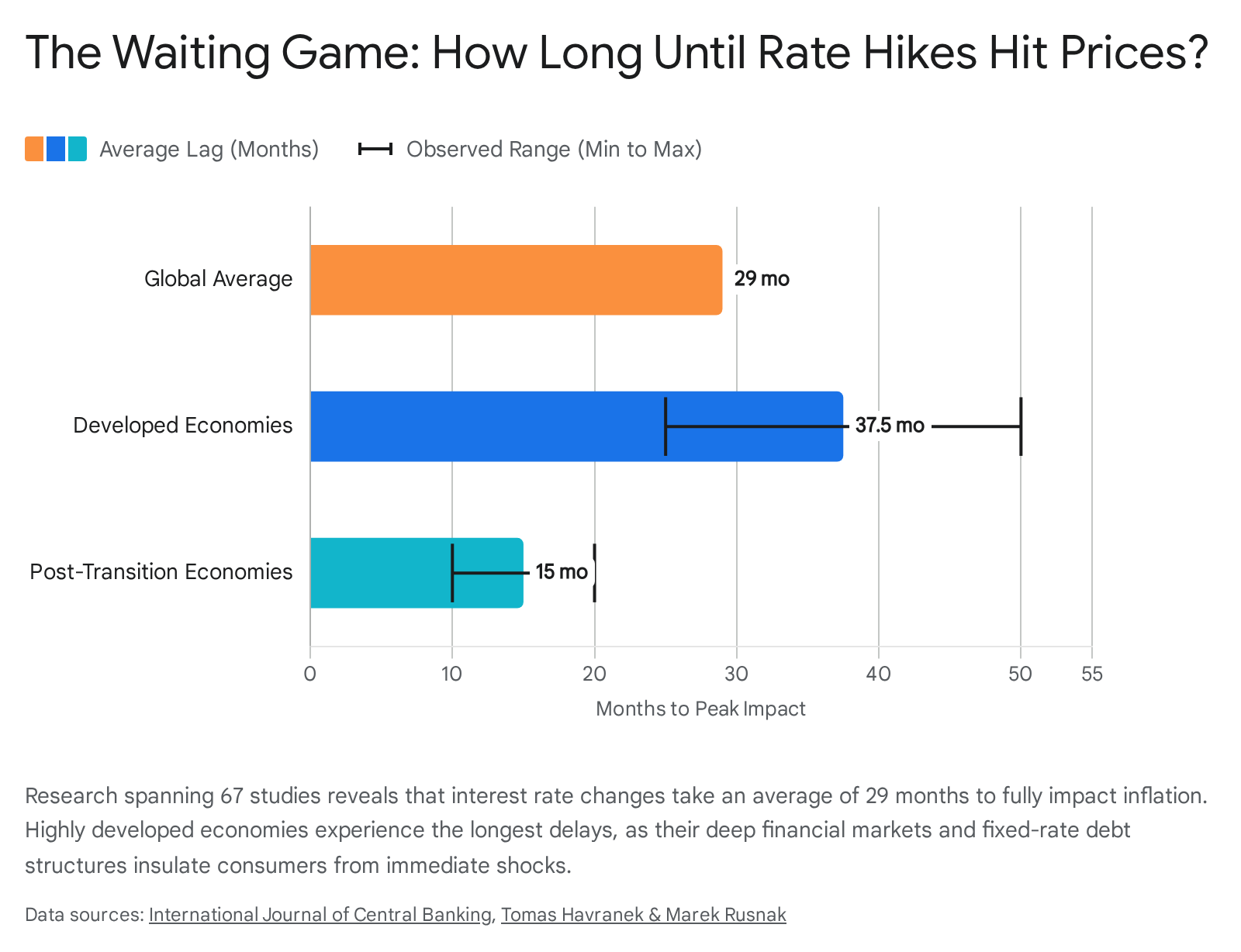

Historical data and extensive meta-analyses suggest that the average time required for a monetary contraction to achieve its maximum downward pressure on consumer prices is roughly 29 months 2425. However, this is merely a statistical average. The actual transmission speed varies wildly based on a specific country's financial architecture, the depth of its capital markets, and the structure of its household debt.

The Paradox of Financial Development

Counterintuitively, the more advanced, mature, and developed a country's financial system is, the slower the transmission of monetary policy 2426. In highly developed economies, transmission lags span a vast window of 25 to 50 months, compared to a highly condensed 10 to 20 months in post-transition or emerging economies 2512.

Deep, sophisticated capital markets in developed nations provide massive corporations with numerous avenues to bypass traditional bank lending. If commercial banks tighten credit in response to central bank rate hikes, large multinational firms can simply issue long-term corporate bonds, tap into private equity reserves, or rely on their own massive internal cash hoards. This financial insulation forces the central bank to keep rates painfully high for an extended period to finally exhaust these alternative funding sources and force a genuine change in corporate hiring and expansion behavior.

Structural Insulation: Fixed vs. Floating Rate Debt

The structural composition of household debt serves as the ultimate governor of transmission speed, with mortgage markets playing the most critical role.

In the United States and France, the vast majority of homeowners hold long-term, fixed-rate mortgages (often 30 years in the US) 1329. If the central bank aggressively raises rates from 0% to 5%, a homeowner who astutely locked in a 3% mortgage the prior year feels absolutely zero change in their monthly housing payment. Their disposable income remains completely untouched, allowing them to continue spending on goods and services as if the rate hikes never occurred. In these economies, transmission only occurs at the margins - affecting new home buyers or those forced to move, while the bulk of the population remains shielded.

Conversely, in countries like Australia, Spain, Portugal, and the United Kingdom, variable-rate (floating) mortgages are the standard financial product 21329. In these highly sensitive economies, when the central bank hikes rates, millions of households see their mandatory monthly mortgage payments surge within a matter of weeks. Their discretionary disposable income evaporates instantly, forcing a severe, immediate contraction in consumer spending at restaurants, retail stores, and service providers. Consequently, monetary policy transmits through the Australian and Spanish economies at breakneck speed compared to the heavily insulated American economy 29.

Lag Heterogeneity Across Economic Sectors

Further complicating matters is the reality that monetary policy does not impact all sectors of the economy at the same velocity. Recent analysis by the ECB and regional central banks confirms that lags are highly heterogeneous 14.

Empirical evidence utilizing structural vector autoregression (SVAR) models suggests that it takes approximately 12 to 18 months for a conventional monetary policy shock to reach its peak impact on broad economic output and "headline" inflation (which includes volatile items like energy and food) 14. However, the transmission lags to more persistent economic indicators, specifically "core" inflation and the services sector, are substantially longer. Because service prices are heavily dependent on sticky wage contracts and long-term commercial leases, it requires more than 24 months for policy hikes to fully pass through to these sectors 1415. Concluding that a tightening cycle has failed simply because inflation has not normalized after twelve months conflates an intentional, structural delay with an absence of effect 29.

The 2022 - 2024 Cycle: A Case Study in Muted Transmission

Between early 2022 and mid-2023, the global economy endured the fastest and most aggressively synchronized monetary tightening cycle since the early 1980s. Facing inflation rates not seen in a generation, the US Federal Reserve hiked its benchmark federal funds rate from near zero to over 5.25% in a condensed 19-month window 3216. The European Central Bank executed a similarly historic climb, dragging rates out of negative territory by hiking 450 basis points in just 14 months 1317.

Standard macroeconomic models, calibrated on decades of historical data, predicted that such a violent tightening of financial conditions would rapidly induce a severe global recession, spark mass layoffs, and crush consumer demand. Yet, throughout 2023 and into 2024, the global economy - and particularly the US labor market - remained bafflingly resilient 1819. Did the vaunted transmission mechanism finally break?

A 25 Percent Weaker Transmission?

Economic researchers at the International Monetary Fund (IMF) conducted a forensic econometric analysis of the 2022 data to answer this exact question. Utilizing pre-pandemic data to establish a baseline, they estimated a model to filter out the sequence of monetary shocks consistent with the new reality. They found that between February and July 2022, the transmission of monetary policy in the United States was, in fact, approximately 25 percent weaker than historical norms would dictate 3220.

This statistical divergence meant that for every three interest rate hikes the Fed executed during that critical window, they essentially had to add a fourth hike just to achieve the equivalent economic braking power they would have expected prior to the COVID-19 pandemic 32.

Why was transmission so heavily muted? The global economy was experiencing a bizarre, unprecedented collision of macroeconomic forces. While central banks were aggressively slamming on the monetary brakes, the lingering effects of massive pandemic-era fiscal stimulus (government direct transfers and corporate bailout loans) were still acting as a heavy foot on the accelerator 3221. Consumers had accumulated trillions of dollars in "excess savings" during global lockdowns, providing a thick financial buffer against rising credit card and auto loan rates. Additionally, post-pandemic supply chain blockages were gradually resolving on their own, naturally bringing down the prices of goods entirely independent of the central bank's interest rate hikes. The transmission mechanism was fighting uphill against a mountain of residual cash.

The Labor Hoarding Phenomenon

The most stubborn puzzle of the 2022-2024 cycle was the labor market. Typically, when corporate borrowing costs soar, businesses protect their profit margins by aggressively laying off workers. By late 2024, the average borrowing cost for small and medium-sized enterprises (SMEs) in the US had climbed to a painful 9.4% 39. Yet, unemployment remained anchored near historic lows 18.

This baffling resilience was driven by a behavioral phenomenon known as "labor hoarding." During the chaotic post-COVID reopening of 2021, businesses faced a traumatic, unprecedented labor shortage, struggling for months to fill vital roles 3239. When the economy eventually began to slow down due to punitive interest rates in 2023, corporate executives were terrified of letting their hard-won workers go, fearing it would be impossible to rehire them when economic growth inevitably resumed.

Instead of executing outright layoffs, companies absorbed the higher financial costs, temporarily sacrificed their profit margins, and quietly reduced working hours or shifted staff to part-time status 3940. Household employment data corroborated this shift: between June 2023 and September 2024, part-time employment in the US rose by 1.91 million, while full-time employment quietly declined by 1.13 million 39.

A comprehensive study led by the ECB confirmed this asymmetry in corporate behavior: while low interest rates encourage firms to hoard labor during mild downturns, it requires a significantly higher pain threshold of sustained, punitive interest rates to force executives to finally abandon hope and execute mass layoffs 40. The transmission mechanism hadn't fundamentally broken; it was simply temporarily jammed by the psychological scars of the pandemic labor shortage.

The Global Spillover: How the US Dollar Dictates World Markets

Because the US Dollar serves as the undisputed bedrock of the international monetary system, the Federal Reserve's transmission mechanism does not stop at the American border. When the Fed adjusts rates, it dictates the financial weather for the entire globe, particularly for vulnerable Emerging Market Economies (EMEs) 21.

Research indicates a strict "hierarchy" of global spillovers. While ECB monetary policy shocks are largely confined to trade dynamics and commodity prices, Federal Reserve monetary policy shocks trigger massive, immediate spillovers into the global financial markets, drastically altering real activity in emerging economies 22.

Historically, aggressive Fed rate hikes trigger immediate, catastrophic financial crises in the developing world. When US rates rise, a phenomenon known as the "dollar comes home" effect occurs 42. Global investors abandon riskier emerging market assets and repatriate their capital to the absolute safety of high-yielding US Treasury bonds. This causes a "sudden stop" in capital flows, crashing emerging market currencies 4243. Because these developing nations historically borrowed heavily in US dollars to fund their infrastructure, a weaker local currency meant their dollar-denominated debt instantly became mathematically impossible to repay, sparking brutal sovereign defaults (as seen in Latin America in 1982, Mexico in 1994, and the notorious "taper tantrum" of 2013) 164244.

Why Emerging Markets Survived the 2022 Shock

As the Federal Reserve embarked on its historic tightening campaign in 2022, veteran economists braced for a devastating wave of emerging market defaults and currency collapses. Remarkably, the anticipated global crisis never materialized 4245. Emerging markets exhibited unprecedented resilience due to deep, painful structural reforms undertaken over the preceding two decades:

- Proactive, Preemptive Monetary Policy: Rather than waiting for the Fed to act and reacting defensively, emerging market central banks acted preemptively. Recognizing the inflationary threat early, central banks in Brazil, Chile, and Mexico began aggressively hiking their own domestic interest rates in early 2021, a full year before the Fed moved in March 2022 1646. This early, decisive action maintained a wide interest rate differential with the US, keeping their sovereign bonds highly attractive to global investors and effectively defending their currencies from collapse 1646.

- The De-Dollarization of Sovereign Debt: Over the last twenty years, major emerging markets successfully deepened their own domestic capital markets. Consequently, the share of their public debt denominated in foreign currencies dropped from a fatal 100% in the 1990s to roughly 60% today 1645. By issuing debt in their local currency, these governments transferred the currency risk to the investors. When the US dollar surged in 2022, the debt burden for these countries did not automatically explode into insolvency.

- Robust Foreign Exchange Reserves: Emerging markets spent the 2010s aggressively hoarding foreign exchange reserves. This ensured they had ample stockpiles of US dollars on hand to seamlessly cover short-term debts and intervene to smooth out wild currency fluctuations without resorting to panicked, economy-crushing capital controls 1645.

The Evolution of Emerging Market Crisis Resilience

| Economic Era | Catalyst (US Fed Action) | Emerging Market Debt Structure | Central Bank Reaction Speed | Typical Macroeconomic Outcome |

|---|---|---|---|---|

| Early 1980s | "Volcker Shock" (Extreme, unprecedented rate hikes to kill inflation). | Highly reliant on short-term, US Dollar-denominated loans. | Reactive and severely constrained by rigid currency pegs. | Devastating debt crises; the infamous "Lost Decade" in Latin America. |

| Mid 1990s | Sudden, unexpected 3% tightening cycle in 1994. | High dollar debt; highly vulnerable to rapid capital flight. | Reactive; struggled and failed to defend currency pegs. | "Tequila Crisis" in Mexico; severe currency devaluations across Asia. |

| 2022 - 2024 | Fastest tightening cycle in 40 years (5.25% increase). | Shifted heavily toward local-currency domestic debt. | Highly Proactive (hiked rates months before the US Fed). | Mild currency depreciation; resilient growth; successfully avoided systemic defaults. |

Data sourced from the Dallas Fed, Brookings Institution, and the Bank for International Settlements 16424445.

Digital Currencies and the Future of Transmission

Looking forward, the architecture of monetary transmission faces a novel existential threat: the rise of digital currencies and stablecoins. Central bankers are increasingly concerned that the wide-scale adoption of privately issued stablecoins could critically weaken domestic monetary policy transmission 7.

If citizens and corporations begin holding their wealth in US-dollar-backed stablecoins rather than domestic bank deposits, the traditional credit channel breaks down. Domestic banks would lose their deposit base, crippling their ability to lend, while the central bank's interest rate adjustments would fall on deaf ears, as the population transacts in a parallel digital currency governed by a foreign entity. This fungibility between deposits and digital currency could dramatically increase capital flow volatility and force emerging markets to rethink their entire regulatory framework to maintain economic sovereignty 7.

Common Misconceptions About Central Banks and Inflation

Because monetary transmission is largely invisible, deeply complex, and operates on a massive temporal delay, it breeds significant public misunderstanding.

Misconception: Central Banks Directly Set Mortgage Rates

A pervasive and deeply entrenched myth is that when the central bank announces a rate hike, they are directly setting consumer mortgage rates. In reality, central banks only directly control the overnight borrowing rates for commercial banks 474849.

Long-term consumer mortgage rates are dictated by the open market - specifically, the yield on 10-year government bonds. While the central bank's overnight rate obviously influences these long-term bonds, market expectations matter significantly more. If the bond market believes inflation will rage out of control for the next decade, 10-year bond yields (and thus mortgage rates) will skyrocket, even if the central bank hasn't touched its overnight rate yet 1147. Conversely, and counterintuitively, mortgage rates can actually fall immediately after a central bank hikes rates, provided the market believes the aggressive hike will successfully destroy long-term inflation, making long-term bonds safer.

Misconception: Beating Inflation Means Prices Go Back Down

When central banks successfully transmit high interest rates through the economy and declare that they have "beaten" inflation, consumers often expect the prices of groceries, rent, and vehicles to fall back to their pre-crisis levels. This stems from a fundamental misunderstanding of the mathematics of inflation 185023.

Inflation measures the rate of change of prices, not the absolute price level. If inflation drops from a punishing 8% down to the central bank's target rate of 2%, it does not mean prices are dropping. It means prices are still rising, they are just rising at a slower, healthier pace 23. An actual broad-based decline in prices is called deflation. Central banks actively utilize monetary policy to prevent deflation at all costs. In a deflationary environment, consumers realize their money will be worth more tomorrow than it is today, causing them to infinitely delay purchases. This collapse in consumer spending can trigger catastrophic, self-feeding economic depressions 18.

Misconception: High Wages Cause Inflation

During inflationary spikes, financial headlines frequently warn of a looming "wage-price spiral," suggesting that greedy workers demanding higher pay are the root cause of inflation. While it is true that exploding labor costs force businesses to raise prices to survive, economists largely view rapid wage growth as a symptom of inflation, not the root cause 5052.

The primary, foundational cause of inflation is a macroeconomic imbalance where too much money (often expanded by central bank stimulus or deficit government spending) chases too few goods (often constrained by supply chain failures or wars) 19. As the fundamental cost of living rises due to this imbalance, workers demand higher wages simply to survive and maintain their purchasing power. Hiking interest rates reduces the total aggregate demand in the economy, which eventually cools the labor market, removing the leverage workers have to demand those large wage increases, thereby breaking the cycle 18.

Bottom line

Monetary policy does not strike the global economy like a lightning bolt; it soaks through it like water, navigating a complex, ever-shifting plumbing system of credit availability, asset valuations, and foreign exchange rates. While the historically aggressive 2022 - 2024 tightening cycle proved that modern economies - particularly structurally reformed emerging markets - are far more resilient to interest rate shocks than in decades past, the fundamental mechanics of transmission remain intact. The full, compounding impact of recent interest rate maneuvers will continue to shape global employment, corporate investment, and consumer pricing well into the late 2020s, serving as a stark reminder that central banking requires steering the global economy while looking through a windshield that is always delayed by two years.