What Is Walk-Forward Analysis in AI Trading

Walk-forward analysis is a rigorous, sequential backtesting methodology that continuously re-optimizes a trading strategy over rolling historical windows, testing it on unseen future data to simulate real-world market deployment. For artificial intelligence and machine learning trading bots, it acts as a critical defense mechanism against overfitting, ensuring that models adapt to shifting market regimes rather than memorizing historical price noise. Ultimately, it provides quantitative researchers with a realistic estimate of how an algorithmic strategy will perform when exposed to live capital.

The Core Problem: Why AI Trading Bots Fail

The financial markets are littered with the remnants of algorithmic trading strategies that looked flawless on paper but collapsed the moment they interacted with live capital. Many algorithmic trading strategies exhibit stellar performance in historical backtests - boasting high returns, favorable win rates, elevated Sharpe ratios, and minimal drawdowns - yet deteriorate significantly when deployed in the live market 1. This discrepancy is especially pronounced in the modern era of artificial intelligence and machine learning, where the line between genuine predictive edge and statistical illusion is notoriously thin.

The root cause of this widespread failure is almost always overfitting 2. Overfitting occurs when an artificial intelligence model is so finely tuned to past historical data that it mistakes random market fluctuations and noise for meaningful, repeatable patterns 12. While an overfit model will shine brilliantly in a backtest, it becomes structurally brittle. Financial markets are inherently non-stationary systems. Their underlying statistical properties - such as volatility distributions, asset correlations, and liquidity profiles - evolve continuously due to macroeconomic shifts, geopolitical events, and human behavioral psychology 1. When a market regime inevitably changes, historical correlations break down, and an overfit AI bot optimized for yesterday's conditions will suffer heavy losses 14.

Empirical studies underscore the severity of this issue within the quantitative finance industry. An analysis of 888 algorithmic strategies revealed that backtested Sharpe ratios (a standard measure of risk-adjusted return) are remarkably poor predictors of real-world out-of-sample performance, demonstrating a correlation squared (R2) of less than 0.025 2. Furthermore, approximately 44% of published trading strategies fail to replicate their historical success when applied to new, unseen market data 2. This highlights a fundamental disconnect between in-sample optimization and out-of-sample reality.

Retail traders and even some institutional participants frequently fall into the trap of assuming that artificial intelligence can independently generate consistent profits without strict validation 1. This "set-and-forget" mentality is fueled by marketing narratives and backtests showing unrealistic exponential equity curves. Inexperience often leads developers to spend vast amounts of time optimizing every possible parameter across an entire historical dataset, which is a recipe for disaster 5. Machine learning models, particularly deep neural networks and reinforcement learning agents, are exceptionally powerful pattern recognizers. If given a static dataset and enough computing time, they will inevitably find a way to achieve a perfect score, effectively memorizing the past rather than learning generalizable principles for the future 1.

Understanding Walk-Forward Analysis

Walk-forward analysis, frequently referred to as walk-forward optimization or walk-forward testing, is a methodical, step-by-step process designed specifically to minimize the chances of overfitting and to assess the true predictive efficacy of a trading model 6. First introduced to the broader quantitative finance community by Robert E. Pardo in his 1992 book Design, Testing and Optimization of Trading Systems, walk-forward analysis is now widely considered the gold standard for trading strategy validation across the industry 28.

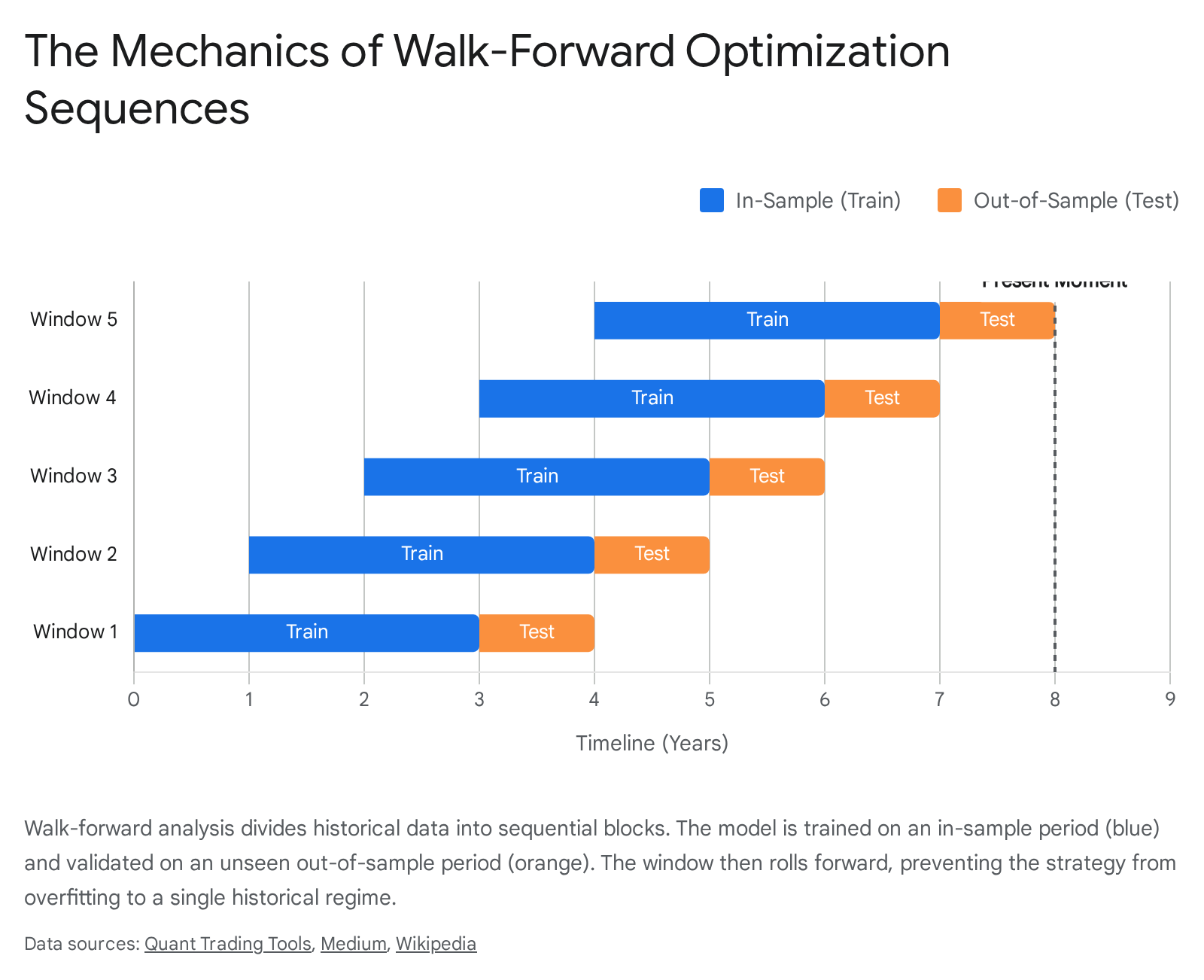

Breaking Down the Mechanics

Unlike traditional static backtesting - which optimizes a strategy's parameters over a single, massive block of historical data and tests it on one small, reserved out-of-sample period - walk-forward analysis embraces the dynamic, chronological nature of markets 910. It operates by splitting the historical time series data into a sequence of rolling windows. For each specific window, the algorithm optimizes the strategy's parameters on the first portion of the data, known as the in-sample or training set. It then strictly evaluates those newly optimized parameters on the immediately following portion of data, known as the out-of-sample or testing set 511.

Once the evaluation for that specific window is complete, the entire time window is shifted forward chronologically by the exact length of the out-of-sample period, and the entire optimization and testing process repeats 212.

This creates a simulation that closely mirrors how a quantitative trader would actually operate a live systematic fund: gathering past data, finding the optimal parameters for the current environment, trading those parameters blindly into the immediate future, and then recalculating everything as new market data arrives.

When all the out-of-sample results from every sequential window are stitched together, the output is a continuous, composite equity curve 1113. This composite curve is the most honest historical performance metric a researcher can generate. It approximates how the trading strategy would have actually performed in real life without the benefit of hindsight bias 1114. In essence, walk-forward analysis is a specific, temporally strict application of cross-validation tailored for time-series data, forcing a strategy to repeatedly prove that its underlying logic can survive tomorrow's noise rather than merely fitting yesterday's anomalies 211.

Methodologies: Rolling vs. Expanding Windows

There are several distinct methodologies for conducting a walk-forward analysis, defined primarily by how the in-sample training window is managed as time progresses. The choice between these methods significantly impacts the types of market regimes the AI model learns from, the stability of its parameters, and its overall computational cost.

Static Walk-Forward Analysis

Static walk-forward analysis implements a single, fixed split of the dataset. A common configuration involves a warm-up period to initialize indicators, followed by a single training period, a validation period, and a final test period 15. While this approach is marginally better than optimizing on an entire dataset, it only provides a single point of optimization. Consequently, it remains highly vulnerable to regime-specific overfitting 15. If the chosen out-of-sample test period happens to share the same macroeconomic characteristics as the training period, the strategy will appear robust, only to fail when deployed in a new regime. Institutional quant desks generally view static walk-forward analysis not as a validation framework, but merely as an initial screening tool to quickly eliminate obviously broken strategies and reduce computational burdens before applying more rigorous tests 15.

Rolling Walk-Forward Analysis

In a rolling walk-forward analysis, the in-sample training window maintains a constant duration (for example, exactly three years of data) that physically slides forward at each step 1114. As the window advances to capture new market data, the oldest historical data is intentionally dropped from the training set. This ensures the model is always trained exclusively on the most recent, and theoretically most relevant, market behavior 1114.

Rolling walk-forward analysis is the preferred methodology when a researcher suspects a regime change in the market, meaning the predictive relevance of older data has decayed 14. By dropping stale data, the algorithm is forced to adapt its parameters to current conditions. For highly reactive intraday trading models, short-term momentum algorithms, and adaptive artificial intelligence agents that need to pivot quickly, the rolling method often provides the most accurate assessment of parameter stability 1516.

Expanding (Anchored) Walk-Forward Analysis

Expanding walk-forward analysis, sometimes referred to as anchored walk-forward analysis, takes a different approach by keeping the starting point of the in-sample window fixed at the absolute beginning of the historical dataset 1116. As the simulation rolls forward, the training window progressively grows larger and larger, incorporating an ever-increasing amount of market history 1116.

The institutional quantitative finance community generally considers expanding walk-forward analysis to be the optimal standard for production-ready deployment 15. By constantly expanding the training set, the AI model eventually learns from multiple distinct market regimes, including bull markets, bear markets, high-volatility shocks, and sideways drift 15. This maximizes the available information and generally leads to highly stable parameters as history accumulates, severely reducing the risk of erratic parameter instability when the model is transitioned to live trading 15.

| Validation Methodology | In-Sample Data Treatment | Primary Use Case | Institutional Verdict |

|---|---|---|---|

| Traditional Backtest | Single massive block covering almost all available history. | Conceptual exploration and basic hypothesis testing. | Highly prone to overfitting; fundamentally insufficient for live capital deployment 10. |

| Static Walk-Forward | Single fixed split (Train -> Validate -> Test). | Rapid initial strategy screening. | Inadequate for production; heavily vulnerable to single-regime bias 15. |

| Rolling Walk-Forward | Fixed-length window that slides forward, actively dropping old data. | Adaptive strategies, high-frequency models, and detecting decaying alpha. | Excellent for identifying regime-dependent shifts and assessing parameter responsiveness 1415. |

| Expanding (Anchored) | Fixed start date; the training window grows continuously as time advances. | Deep learning models requiring massive datasets; long-term robust systems. | The "Gold Standard" for production deployment; maximizes data utilization and parameter stability 15. |

Walk-Forward Efficiency (WFE) and Performance Metrics

Merely running a walk-forward optimization is not sufficient; the resulting data must be rigorously interpreted using specialized metrics. The primary benchmark used to evaluate a strategy under this framework is Walk-Forward Efficiency (WFE).

Calculating and Interpreting Walk-Forward Efficiency

Walk-Forward Efficiency provides a quantitative measure of how well a strategy's optimization translates to genuinely unseen out-of-sample performance 13. It is mathematically calculated as the ratio of the annualized out-of-sample net profit (or sometimes the out-of-sample Sharpe ratio) divided by the annualized in-sample net profit 13151617. This metric answers the fundamental question: does optimization actually improve real-world performance, or does it merely curve-fit historical data?

A Walk-Forward Efficiency score above 1.0 (or 100%) indicates that the strategy actually performed better out-of-sample than it did during training. This is an exceptional result and strongly suggests that the optimization process identified genuine, persistent market inefficiencies rather than fitting to noise 15. When the Walk-Forward Efficiency falls between 0.5 and 1.0 (50% to 100%), the strategy successfully retained a significant portion of its optimized performance on unseen data. Professional quantitative developers generally consider a WFE above 50% to 60% as the minimum threshold required for a system to be considered genuinely robust and suitable for live deployment 13163.

Conversely, a Walk-Forward Efficiency below 0.5 (under 50%) is a severe warning sign. It indicates that the strategy suffered massive performance degradation when exposed to unseen data, strongly suggesting that the in-sample optimization was merely curve-fitting to historical noise 1317. A strategy with a sub-50% WFE is considered highly brittle and has a high probability of failure in live markets 17.

Parameter Stability and Deflated Sharpe Ratios

While Walk-Forward Efficiency is the headline metric, it cannot be interpreted in isolation. A robust assessment examines several other advanced performance characteristics, starting with parameter stability. If the optimal parameters selected by the walk-forward algorithm - such as the specific length of a moving average, the breakout threshold, or the learning rate in a neural network - swing wildly from one sequential window to the next, the strategy does not possess a stable edge 1119. For instance, if an algorithm dictates a 10-period lookback in one window, jumps to a 50-period lookback in the next, and drops to 15 in the third, the model is merely chasing transient noise rather than capturing an underlying market truth 1119.

Institutional evaluations also rely heavily on the Deflated Sharpe Ratio (DSR). Traditional backtesting often involves testing hundreds or even thousands of parameter combinations. This massive computational search inherently increases the probability of finding a spuriously high Sharpe ratio purely by statistical chance 20. The Deflated Sharpe Ratio corrects for this "researcher degrees of freedom" problem by adjusting the observed Sharpe ratio downward to mathematically account for the number of testing trials conducted and the non-normality of the asset's returns 20. This provides a much more stringent and realistic benchmark for institutional deployment.

Profit Consistency and Maximum Drawdown Realities

A strategy might exhibit a high aggregate Walk-Forward Efficiency simply because a single out-of-sample window generated massive, outlier profits, masking the fact that the majority of the other validation windows lost money. To prevent this deception, rigorous walk-forward frameworks require that the distribution of profits is consistent. A common institutional standard requires that at least 50% - and ideally over 70% or 80% - of the individual walk-forward test periods are independently profitable, and that no single time period contributes more than 50% of the strategy's total net profit 319.

Furthermore, drawdown analysis within the walk-forward context is critical. A robust walk-forward analysis examines maximum drawdown consistency across all validation windows 13. A strategy that maintains a high average profit but exhibits wildly fluctuating, severe drawdowns across different out-of-sample periods indicates underlying fragility despite a deceptively acceptable average performance 13.

Why WFA Matters Specifically for Modern AI Systems

The rapid integration of artificial intelligence - ranging from deep neural networks to reinforcement learning agents and large language models - has drastically increased the complexity of algorithmic trading. Because these models contain millions or even billions of parameters, they carry an infinitely higher risk of overfitting compared to traditional, parameter-light systems 11. For modern AI, walk-forward analysis is not just a best practice; it is an absolute necessity.

Taming Reinforcement Learning and Dynamic Adaptation

In recent years, reinforcement learning (RL) has emerged as a powerful tool for portfolio optimization and high-frequency trading. By modeling the financial market as a dynamic environment that yields rewards based on correct trading decisions, RL agents utilizing algorithms like Proximal Policy Optimization (PPO), Advantage Actor-Critic (A2C), and Deep Deterministic Policy Gradient (DDPG) can theoretically learn complex, non-linear market dynamics 21423.

However, standard reinforcement learning methods trained exclusively on a static block of historical data often fail catastrophically when market regimes change unexpectedly 15. While AI is highly capable of recognizing patterns, it lacks true contextual intelligence and beneficial human instincts - such as caution, strategic hesitation, and the ability to dynamically reduce exposure when market conditions become visibly abnormal 1.

Walk-forward analysis is critical in this context because it enforces a continuous re-training and re-evaluation loop. By embedding the reinforcement learning training process inside an expanding or rolling walk-forward framework, quantitative developers ensure the agent is constantly updating its policy networks with the latest market state 152125. This forces the RL agent to prove its ability to generalize across different sequential regimes, ensuring it learns underlying market mechanics rather than simply memorizing a specific sequence of historical price movements.

The Challenge of LLMs and Sentiment-Based Trading

The latest frontier in quantitative finance involves utilizing Large Language Models (LLMs) to extract sentiment from financial news, SEC regulatory filings, earnings call transcripts, and social media, directly integrating these text-based signals into trading algorithms 56277. Empirical studies demonstrate that hybrid AI models incorporating natural language sentiment data can achieve exceptionally high theoretical risk-adjusted returns. For example, research utilizing the GPT-3-based OPT model to analyze nearly a million financial news articles demonstrated an accuracy of 74.4% in predicting stock market returns, yielding a massive theoretical Sharpe ratio of 3.05 in a self-financing long-short strategy 272930. This drastically outperformed traditional lexicon-based approaches like the Loughran-McDonald dictionary model, which yielded a mere 1.23 Sharpe ratio 2729.

Yet, applying static backtesting to LLM-driven sentiment strategies is highly problematic and often misleading. Financial language and market narratives are extremely dynamic, meaning the predictive value of specific words, phrases, or news sources decays rapidly over time 431. A language model trained on sentiment data from a high-liquidity bull market might severely misinterpret the macroeconomic context of a sudden bear market.

Walk-forward analysis ensures that the supervised learning models mapping these LLM sentiment scores to actual trade execution are continuously re-calibrated. It forces the system to repeatedly prove that its interpretation of current sentiment translates into persistent out-of-sample profitability, preventing the model from relying on stale data or outdated linguistic correlations 68.

Infrastructure and the Computational Cost of Dynamic Reasoning

The primary drawback of applying rigorous walk-forward analysis to modern artificial intelligence systems is the immense computational infrastructure required 1013. Walk-forward testing multiplies processing time exponentially. If a historical dataset is divided into 15 rolling windows, the AI model must be trained, hyperparameter-tuned, and validated 15 separate times from scratch.

For deep learning models or agentic LLM workflows that already consume massive amounts of GPU compute, repeated walk-forward re-training can become prohibitively expensive and time-consuming. Recent systems-level analyses on the cost of dynamic reasoning in AI agents reveal that agent-based test-time scaling can result in a 62-fold to 136-fold increase in GPU energy per query compared to standard single-turn LLM inference 93410. When this computational intensity is multiplied across dozens of walk-forward validation windows, it creates a looming sustainability and cost crisis for quantitative firms 9.

To mitigate these latency and infrastructure bottlenecks, quantitative researchers are exploring novel architectures. Concepts like Historical State Reconstruction (HSTR) aim to decouple the heavy computational cost of context acquisition from the latency-sensitive critical path of decision-making 11. By pre-computing complex state facets offline and utilizing bitemporal databases, systems can allow trading agents to essentially "time travel" to reconstructed historical states with near-zero latency 1137. This drastically speeds up the walk-forward testing cycle, reducing context retrieval latency by over 97% while maintaining strict temporal integrity to prevent data leakage 11.

Common Pitfalls and the Illusion of Rigor

While walk-forward analysis is an incredibly powerful safeguard, it is not an invincible shield against market realities. A poorly implemented walk-forward framework can provide a false sense of security, leading to disastrous live performance. Quantitative traders must carefully navigate several critical failure modes.

Fitness Function Shopping and Meta-Overfitting

Walk-forward analysis requires the researcher to make numerous structural choices, such as determining the exact length of the in-sample training window, the length of the out-of-sample testing window, and selecting the primary optimization metric (e.g., maximizing absolute profit versus minimizing maximum drawdown). A pervasive and dangerous mistake is "fitness function shopping." This occurs when a developer tests dozens of different window size configurations and objective functions until they find a combination that produces a highly favorable Walk-Forward Efficiency 13.

This practice does not eliminate overfitting; it simply shifts the overfitting from the trading strategy's core parameters to the walk-forward testing parameters themselves. If a strategy only works when optimized on exactly three-month windows and validated on one-month windows, but collapses under any other configuration, the strategy is fragile 13. To prevent this meta-overfitting, window sizes and testing criteria must be predetermined logically - typically 2 to 4 years for optimization and 3 to 6 months for validation - and left strictly alone during the analysis 13.

Transaction Costs, Slippage, and Latency

Artificial intelligence models, particularly those operating at high frequencies or reacting rapidly to sentiment shifts, often generate a high turnover of trades. An algorithmic strategy might show exceptional out-of-sample gross returns in a walk-forward analysis but result in deeply negative net returns once real-world trading frictions are accurately modeled 1512.

Failing to properly account for broker commissions, bid-ask spreads, slippage (the difference between the expected price of a trade and the executed price), and market impact (how a large order moves the market against the trader) is a fatal error 212. Rigorous institutional validation requires that these costs be hardcoded into every step of the walk-forward process to ensure the strategy is genuinely viable in a live execution environment 15.

Data Snooping and the Importance of the Hold-Out Sample

Walk-forward analysis relies entirely on strict temporal integrity. If any data point from the future inadvertently leaks into the training process, the entire test is invalidated. This look-ahead bias can occur in subtle ways, such as using an indicator that requires future data points to calculate its present value, or backtesting on a dataset that suffers from survivorship bias (e.g., an index list that has already removed bankrupt or delisted companies, guaranteeing the AI only trains on historical winners) 11539.

To definitively protect against inadvertent data snooping or procedural overfitting, institutional quants rely on a final "hold-out" sample. This involves reserving the absolute most recent 10% to 20% of the available historical data, keeping it completely untouched and hidden during the entire development, backtesting, and walk-forward analysis phases 13. Once the strategy is finalized, it is run exactly once on this hold-out sample. If the strategy fails this ultimate out-of-sample test, it is discarded, providing a final, uncorrupted check against the optimization of the testing process itself 13.

Retail Traders vs. Institutional Execution

The democratization of cloud computing power, open-source Python libraries, and advanced data APIs has significantly narrowed the technological gap between institutional quantitative desks and retail investors 134041. Today, retail traders have unprecedented access to sophisticated algorithmic platforms that offer built-in walk-forward optimization capabilities, enabling them to test complex strategies that were once the exclusive domain of hedge funds 13342.

The Democratization of AI Trading Tools

Retail trading applications are increasingly integrating artificial intelligence features, ranging from predictive machine learning analytics to chatbot-assisted order management and sentiment tracking 4344. While these tools allow individual investors to process vast amounts of market data in milliseconds, they also introduce severe risks 43.

The primary danger for retail participants is an over-reliance on black-box AI platforms. Many retail traders use AI screeners or trading bots without understanding the underlying logic, validation methodology, or the specific historical data the model was trained on 4445. If a retail trader blindly trusts an AI system that has not been subjected to rigorous walk-forward analysis, they are highly vulnerable to unanticipated losses when the market experiences a volatility shock or an unprecedented macroeconomic event not represented in the bot's training data 4346.

The Institutional Edge: Process Over Prediction

The true differentiator in modern algorithmic trading is no longer mere access to technology, but a strict adherence to scientific process. Retail traders frequently pursue the illusion of a "magic signal" or focus entirely on direction prediction - trying to build an AI that perfectly guesses whether a stock will go up or down 447. Institutional quants understand that markets actively punish pure prediction because patterns decay and market regimes constantly shift 4.

Instead, institutions build resilient systems focused on execution, risk management, and exploiting temporary market inefficiencies (such as statistical arbitrage) rather than predicting directional trends 447. For the institutional developer, walk-forward analysis is just one layer of a comprehensive risk framework. They bake multi-layered validation into their research, combining expanding walk-forward analysis with Monte Carlo simulations to stress-test equity curves, multi-market testing to ensure the logic works across different asset classes, and strict parameter stability checks 474849.

| Paradigm | Retail AI Trading Approach | Institutional Quant Approach |

|---|---|---|

| Primary Goal | Finding a "magic signal" for directional price prediction 447. | Exploiting structural inefficiencies and managing risk 447. |

| Validation Method | Basic static backtesting; heavy reliance on in-sample metrics 25. | Multi-layered: Expanding WFA, Monte Carlo, hold-out samples 1347. |

| AI Utilization | Black-box commercial bots; basic sentiment screeners 4445. | Custom multi-agent LLM frameworks; dynamic RL retraining 2150. |

| Failure Mode | Blind trust in overfit models during sudden regime changes 245. | Infrastructure/compute costs and latent look-ahead bias 911. |

Managing Risk in Autonomous Agentic Workflows

As the industry moves toward autonomous, agentic AI frameworks - where multiple specialized LLMs act as researchers, analysts, and traders collaborating in simulated firms - the need for robust validation grows exponentially 505152. While these multi-agent systems show incredible promise in improving cumulative returns and Sharpe ratios, they also introduce unique operational risks 50. Autonomous agents operating without strict human oversight can be manipulated into executing unauthorized actions, exposing confidential data, or reacting irrationally to false information injected into the market 5354. Walk-forward analysis, combined with real-time runtime security controls and continuous paper-trading, is essential to ensure these autonomous systems behave predictably and safely before they are granted access to live capital 4954.

Bottom line

Walk-forward analysis is an indispensable validation framework that forces algorithmic trading strategies to prove their worth on unseen data through continuous, rolling re-optimization. For modern artificial intelligence and machine learning models - which are dangerously prone to memorizing historical noise - walk-forward analysis provides the most realistic simulation of how an adaptive system will perform in live, non-stationary markets. While the process is computationally demanding and requires strict vigilance against secondary overfitting and data leakage, executing a disciplined walk-forward sequence remains the most reliable method for separating genuine predictive edge from statistical illusion.