What Are AI Trading Signals and How They Work

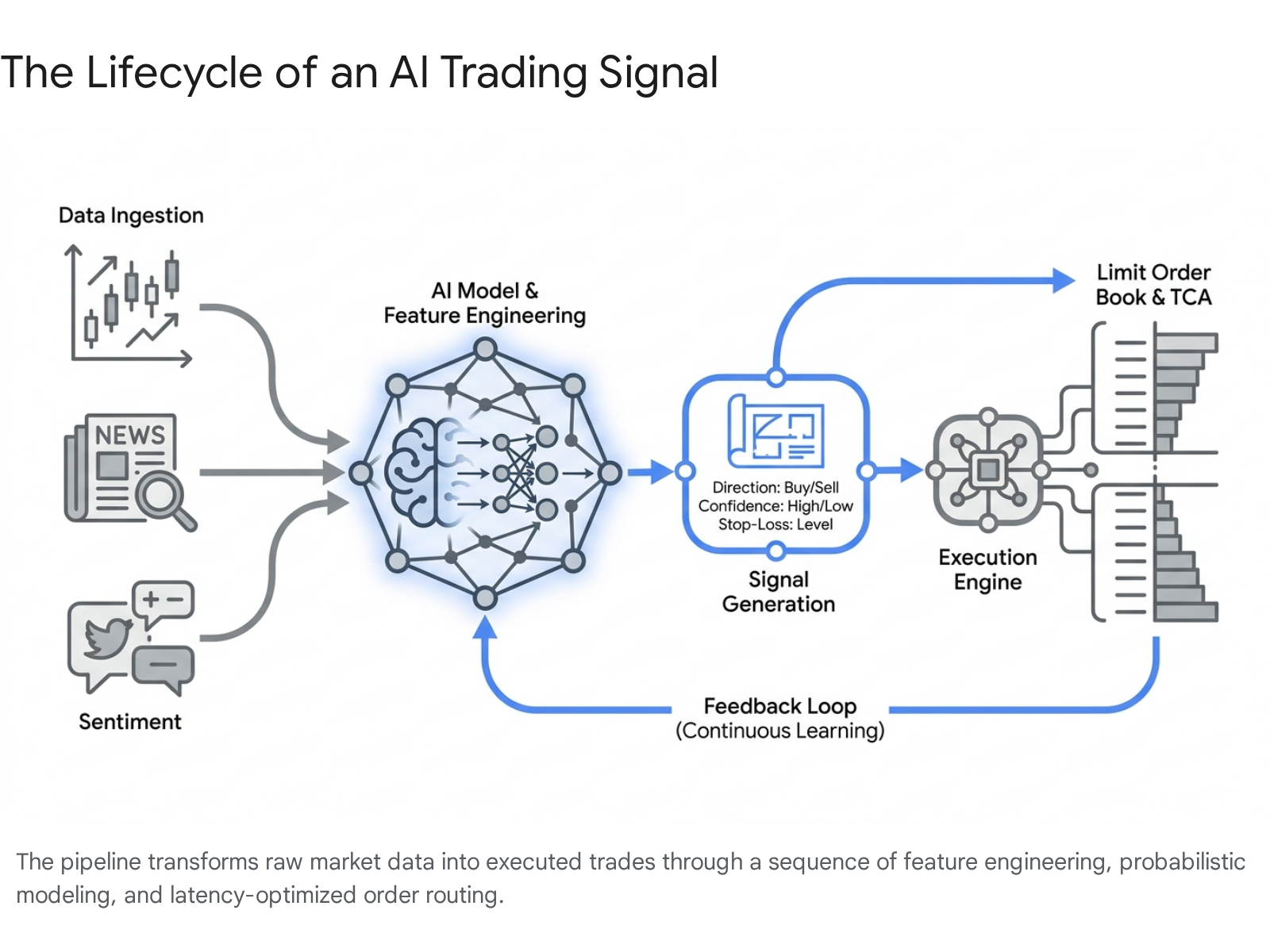

An AI trading signal is an automated, algorithmic recommendation to buy, sell, or hold a financial asset, generated by processing vast datasets through advanced machine learning models. Instead of relying on human intuition or static technical rules, these systems calculate the exact mathematical probability of future price movements to provide a structured execution blueprint that includes entry prices, dynamic stop-loss levels, and optimal position sizing. By transforming raw market noise into calibrated risk profiles, artificial intelligence allows automated systems to execute positions based purely on statistical edge.

The mechanics of how a computer decides to risk capital matter far beyond the proprietary trading floors of Wall Street quantitative funds. Whether a retail investor is utilizing a smartphone application to allocate their retirement savings, a decentralized cryptocurrency protocol is managing automated liquidity pools, or a massive pension fund is rebalancing the financial futures of millions of workers, artificial intelligence is increasingly dictating the flow of global capital 1. The global algorithmic trading market, valued at $18.73 billion in 2025, is projected to reach $33.45 billion by 2030, with AI systems handling an estimated 89% of global trading volume across equities, derivatives, and digital assets 123. Understanding the lifecycle and logic of these signals is no longer an esoteric exercise for computer scientists; it is a fundamental prerequisite for participating in the modern financial ecosystem.

The Weather Forecasting Analogy: From Point Predictions to Probabilistic Models

To genuinely grasp how an AI model generates a trading signal, it is highly instructive to examine its closest technical relative: modern meteorological forecasting. Both weather prediction and quantitative finance deal with chaotic, non-stationary systems driven by massive arrays of interconnected, rapidly shifting variables.

Historically, both disciplines relied heavily on rigid, deterministic models. In meteorology, traditional Numerical Weather Prediction (NWP) systems ran strict physics-based equations on supercomputers to generate a single "point forecast," predicting an exact output, such as 38 megawatts of wind generation for a specific farm 15. In quantitative finance, traditional technical analysis operated on similarly deterministic rules, generating a binary "buy" signal the moment a 50-day moving average crossed above a 200-day moving average. Both approaches suffer from the identical fatal flaw: they discard the mathematical uncertainty inherent in a dynamic system 5.

Artificial intelligence revolutionizes both fields by shifting the paradigm from definitive point predictions to calibrated probabilistic distributions. In modern AI-native weather modeling - exemplified by systems like Google DeepMind's GenCast, ECMWF's AIFS, and Jua's EPT-2e - neural networks do not simply output a single expected temperature or wind speed 67. Instead, these AI foundation models run massive ensembles, processing slightly different initial conditions to generate a wide spread of probabilities 67. An AI weather model might indicate that while the expected wind farm output is 38 megawatts, the ensemble spread is wide, revealing a 20% statistical probability that output collapses below 12 megawatts due to an approaching atmospheric front 56.

An AI trading signal operates on the exact same probabilistic principles. When an AI model analyzes a stock chart, processes order book depth, and reads global news sentiment, it does not output a guaranteed prediction of the future, because the future is unknowable 8. Instead, it calculates the statistical probability of various price paths. A robust AI trading signal might dictate a buy order, but its true utility lies in the calibrated confidence interval attached to that order 9. Just as an energy trader uses the probability of a wind shortfall to hedge their portfolio, a quantitative trading algorithm uses the AI's probability distribution to dynamically size its position, set precise stop-loss limits, and define the optimal risk-to-reward ratio before capital is ever deployed 610.

In both domains, the mathematical objective is identical: maximize sharpness subject to calibration 5. A model must be confident enough to be useful, but calibrated enough that reality honors its confidence. A model that consistently predicts high probabilities for events that rarely occur is swiftly penalized, whether it is predicting a hurricane using the Continuous Ranked Probability Score (CRPS) or projecting a stock market breakout 511.

How Does AI Tell a Signal from Market Noise?

The most profound challenge in financial machine learning is the notoriously low signal-to-noise ratio (SNR) of global capital markets 12. If an AI model is trained to recognize images of domestic cats, the "signal" (the feline shape, ears, and eyes) is highly consistent, while the "noise" (background blur or lighting variations) is easily ignored 12. This constitutes a high SNR environment where deep learning networks achieve near-perfect accuracy 12. Financial markets, conversely, are aggressively low SNR environments. The genuine "signal" - a fundamental economic catalyst or a true structural imbalance driving a price move - is almost entirely buried beneath a chaotic avalanche of high-frequency algorithmic trading noise, random human panic, macroeconomic shocks, and unpredictable geopolitical events 12.

To separate genuine signals from this overwhelming noise, sophisticated AI architectures do not rely on a single technical algorithm; they utilize complex ensemble methods and strict regime-adjusted thresholds 9. An isolated technical indicator, such as a Relative Strength Index (RSI) showing a stock is "oversold," is merely mathematical noise when viewed in isolation 9. An AI system upgrades this isolated data point into a viable signal by layering contextual intelligence 9. It utilizes computer vision to analyze the micro-structure of the candlestick chart, natural language processing (NLP) to read the sentiment of the morning's earnings call, and anomaly detection models to measure if the current volatility is a statistical outlier compared to historical baselines 10112.

Furthermore, institutional-grade AI systems constantly classify the current "market regime" - determining whether the broader market is trending, consolidating, or experiencing a high-volatility liquidity shock 14. Because a trading setup that works perfectly in a low-volatility bull market will fail catastrophically in a high-volatility bear market, the AI dynamically adjusts its internal decision thresholds 15. If the market regime is highly erratic, the AI will require a much higher consensus across its internal sub-models before it classifies a data pattern as a valid signal, effectively filtering out the weak or false breakouts that routinely trap human day traders 92.

The Core Architectural Frameworks of Signal Generation

To structure the chaos of the market, quantitative researchers deploy different mathematical frameworks depending on the specific objective of the trading strategy. The architecture of the AI directly dictates the nature of the signal it produces.

| Model Category | Core Mechanisms & Architecture | Signal Outputs | Primary Financial Use Cases |

|---|---|---|---|

| Classification Models | Utilizes algorithms such as Random Forests, Support Vector Machines (SVM), and Logistic Regression to categorize non-linear market data into discrete, predefined classes based on learned historical patterns 1416. | Categorical variables (e.g., generating a binary "Buy," "Sell," or "Hold" directive, or identifying discrete market regimes like "High Volatility" versus "Low Volatility") 1417. | Short-horizon directional trading, regime detection, filtering false breakouts, and binary event prediction (e.g., forecasting whether a company will beat or miss earnings) 914. |

| Regression Models | Employs Linear Regression, Gradient Boosting, or deep neural networks to mathematically model the relationship between independent variables (features) and a continuous dependent variable 16. | Continuous numerical values (e.g., predicting the exact future price of an asset, estimating transaction slippage in basis points, or forecasting continuous portfolio returns) 16. | Transaction Cost Analysis (TCA), estimating optimal execution prices, predicting continuous sovereign yield curves, and dynamic position sizing 16. |

| Probability-Based & Generative Models | Leverages Bayesian Networks, Long Short-Term Memory (LSTM) networks, Diffusion models, and Transformer foundation models to capture sequential dependencies and complex spatial-temporal correlations 181920. | Calibrated probability distributions over future outcomes (e.g., outputting an 82% probability of a trend reversal, accompanied by a dynamic confidence interval and expected value metric) 920. | Advanced risk management, derivatives and options pricing, sophisticated multi-factor portfolio rebalancing, and navigating highly uncertain, low signal-to-noise environments 1921. |

How Do Predictions Become Actual Trades?

Possessing a high-conviction mathematical prediction is entirely different from realizing a profitable trade in a live market. The process of translating a theoretical signal into a capitalized position is known as trade execution, and it is here that the physical constraints of the market - liquidity, latency, and transaction costs - ruthlessly attack a model's theoretical edge 163.

When an AI model generates a signal to buy 100,000 shares of a specific equity, it cannot simply dump a massive market order onto the exchange. Doing so would immediately exhaust the available sellers at the current price, forcing the algorithm to buy shares at progressively higher prices as it rapidly eats through the limit order book 323. This discrepancy between the expected entry price of the signal and the actual executed price is known as "slippage," and it is the silent killer of algorithmic trading strategies 16324. Slippage, combined with direct broker commissions, bid-ask spreads, and regulatory fees, constitutes the total transaction cost 3. For high-frequency, short-term AI signals that target micro-anomalies, these hidden execution costs can rapidly erode 100% of the strategy's theoretical profit if not properly managed 3.

To solve this execution puzzle, the raw signal is passed to a specialized AI-driven execution engine. Using advanced techniques like Reinforcement Learning (specifically Q-Learning frameworks), the execution engine treats the exchange's limit order book as a complex, adversarial environment 1618. The AI agent learns the optimal way to slice the large "parent" order into hundreds of smaller "child" orders, dynamically placing them across multiple dark pools and public exchanges to obscure the trader's true intent 16. These Smart Order Routing (SOR) systems constantly adapt to the microstructure of the market, reading milliseconds of tick data to anticipate short-term price fluctuations and execute the children orders at the most advantageous micro-prices 23.

Furthermore, leading institutions utilize Supervised Learning for Transaction Cost Analysis (TCA) 16. Before a trade is even approved for execution, the TCA model predicts the expected market impact and slippage of the transaction based on historical liquidity patterns 16. If the AI determines that the transaction costs will outweigh the expected alpha (profit) of the generated signal, the execution engine will veto the trade entirely, enforcing a strict mathematical discipline that human traders routinely ignore due to emotional bias and the fear of missing out 2526.

The Democratization of Alpha: Retail AI vs. Institutional Quant Models

For decades, quantitative trading was the exclusive, impenetrable domain of elite institutional hedge funds, massive pension portfolios, and proprietary high-frequency trading (HFT) desks 3. These entities commanded billions of dollars in capital, hired legions of PhD researchers, paid exorbitant fees for private microwave networks to reduce latency to the microsecond, and utilized massive supercomputer clusters to uncover statistical anomalies 3. The retail trader, armed with delayed data feeds and rudimentary charting software, was structurally relegated to providing liquidity for the institutions, consistently underperforming the broader market 3.

Between 2023 and 2026, the proliferation of scalable cloud computing, open-source machine learning frameworks, and robust application programming interfaces (APIs) triggered a profound democratization of financial technology 327. Everyday retail investors are now deploying autonomous AI agents capable of parsing order book depth, conducting natural language sentiment analysis on global news, and executing trades with a level of sophistication previously reserved for multi-billion-dollar funds 825. Platforms integrating Financial Learning Models (FLMs) allow retail traders to operate on rapid 5- to 15-minute time horizons, capturing intraday volatility with automated risk management that enforces discipline 2829.

The results of this technological shift are actively altering market dynamics. A comprehensive 2026 quantitative study conducted by JPMorgan Chase strategists Arun Jain and Nikolaos Panigirtzoglou revealed that retail investors utilizing concentrated AI-assisted stock-picking strategies consistently outperformed traditional Wall Street benchmarks, including dollar-cost averaging strategies tied to the tech-heavy Nasdaq 100 45. By leaning heavily into the AI infrastructure super-cycle - identifying micro-anomalies in high-momentum assets like Nvidia (NVDA), Advanced Micro Devices (AMD), and Micron Technology (MU) - retail portfolios demonstrated unusual conviction and achieved exceptional returns 284532. In optimal market windows, some automated retail agent portfolios reported annualized returns approaching 124%, while specialized AI trading agents operating on 15-minute intervals maintained win rates above 61% by ruthlessly cutting losing positions 28.

Despite these remarkable advancements, it is vital to acknowledge the persistent structural gulf that remains between retail AI tools and institutional quantitative infrastructure 3. The institutional advantage is no longer just about the algorithm; it is about infrastructure and data 33. Institutional quant models do not rely on third-party web platforms or retail brokerage APIs. They operate directly inside exchange colocation centers, giving them a speed advantage measured in nanoseconds 3. While retail AI excels at interpreting directional trends and parsing daily sentiment, institutional AI dominates the market microstructure - capturing fleeting, sub-second arbitrage opportunities that retail algorithms cannot even detect before they vanish 334.

Moreover, institutions possess the capital to purchase highly exclusive "alternative data" streams 3. While retail AI analyzes public charts and free news feeds, an institutional model might be ingesting satellite imagery of retail parking lots to predict quarterly sales, parsing raw credit card transaction data, and analyzing bespoke supply chain logistics feeds 10. According to 2023 industry benchmarking data, a large institutional investor with $150 billion in assets under management maintains an annual technology and AI budget of approximately $20 million to $40 million, ensuring their models maintain an informational edge that consumer-grade applications simply cannot replicate .

The Illusion of Permanence: Overfitting, Model Decay, and Market Reflexivity

The rapid proliferation of AI trading applications has birthed a dangerous misconception among the general public: the belief that a machine learning model is an infallible crystal ball capable of printing guaranteed wealth 836. In reality, the deployment of artificial intelligence in financial markets is fraught with severe mathematical pitfalls, structural paradoxes, and hidden risks.

The most common engineering failure in AI signal generation is "overfitting" 1637. When researchers train a deep learning model on historical market data, the algorithm is designed to ruthlessly optimize itself to find every possible pattern that led to a profit in the past 1637. However, because financial data is intensely noisy, a poorly constrained AI will inevitably memorize random statistical noise - such as a meaningless correlation between a specific stock's price and the weather in Tokyo on a particular Tuesday - and present it as a flawless, highly profitable trading strategy in backtesting 12. When this overfitted model is deployed into live, out-of-sample market conditions, its performance immediately collapses because the noise it memorized does not repeat 1637.

Even a perfectly engineered, highly predictive AI model faces an inescapable financial reality: alpha decay 3839. "Alpha" represents the excess return earned by exploiting a market inefficiency. However, financial markets are highly adaptive ecosystems. When an AI algorithm discovers a profitable signal and begins trading it, the sheer act of buying and selling physically alters the price of the asset, slowly closing the arbitrage window 39.

This phenomenon is best understood through the lens of George Soros' Theory of Reflexivity, a concept that highlights the mutual, iterative influence between market participants' beliefs and actual market outcomes 394041. Soros posited that markets are not passively observed entities; they are shaped by a continuous two-way feedback loop between the participants' perceptions (the cognitive function) and the actual market fundamentals (the participative function) 4243.

In the context of AI trading, reflexivity manifests as a phenomenon known as "performative prediction" 39. As thousands of sophisticated AI models - both retail and institutional - analyze the exact same datasets and arrive at the exact same conclusions, their coordinated trading activity instantly corrects the very inefficiency they were trying to exploit 39. The alpha is rapidly arbitraged away, leading to an accelerated homogenization of the market 39. This creates "Red Queen dynamics," where the competitive response to alpha decay is increased investment in AI infrastructure, which paradoxically accelerates the decay even further 39. Consequently, an AI model that generates phenomenal returns today is virtually guaranteed to degrade in effectiveness over the coming months. Quantitative researchers combat this relentless model decay through continuous retraining, constantly seeking new alternative data sources to stay one step ahead of the collective algorithmic intelligence 3839.

Global Developments: Generative AI, Alternative Data, and Systemic Risk (2023 - 2026)

The landscape of quantitative finance underwent a violent evolutionary leap between 2023 and 2026, driven primarily by the integration of Large Language Models (LLMs) and Generative AI into live market operations 1844. Previously, AI excelled almost exclusively at quantitative analysis - processing vast numerical grids of price and volume data. The advent of sophisticated LLMs has unlocked the qualitative universe, allowing machines to reason through massive oceans of unstructured alternative data 1844.

Institutional platforms like the Bloomberg Terminal completely overhauled their legacy architectures to embed Generative AI natively into the workflow 44. Models now ingest millions of daily corporate filings, real-time earnings call transcripts, central bank policy statements, and global news wires, synthesizing them into actionable, context-aware summaries in a fraction of a second 446. During the initial AI rollout in 2025, Bloomberg introduced AI document insights and automated company summaries that effectively triaged the 1.5 million external items the terminal ingests daily 44. This allows the AI to instantly quantify the tone, regulatory risk, and forward guidance of a CEO's speech, transforming human language directly into a mathematical trading signal long before a human analyst finishes reading the first paragraph 1044.

Globally, the adoption of AI in financial markets has accelerated dramatically. Data from the Microsoft AI Economy Institute in 2026 revealed that global adoption of generative AI tools reached 16.3% of the world's population, though a stark divide remains, with adoption in the Global North (24.7%) vastly outpacing the Global South (14.1%) 7. However, open-source models like DeepSeek have rapidly gained traction in markets historically underserved by traditional tech providers, democratizing access to advanced reasoning capabilities 7.

In the Asia-Pacific region, AI trading adoption is surging, driven by a combination of deep liquid markets and supportive government policies 247. Financial institutions in Japan, Singapore, and Hong Kong are aggressively deploying machine learning algorithms, while the region's massive retail investor base is increasingly utilizing robo-advisors and AI-powered trading bots 47. Regulators, such as Japan's Financial Services Agency (FSA) and Singapore's Monetary Authority of Singapore (MAS), have actively updated guidelines and launched sandbox programs to manage this rapid technological integration 47.

Simultaneously, the industry is witnessing a critical transition from passive analytical AI to autonomous "Agentic AI" 4849. Rather than waiting for a human programmer to explicitly define a strategy, autonomous AI agents are now designed to act as independent quantitative researchers 4849. These agents are given a high-level directive - such as "maximize risk-adjusted returns in the semiconductor sector while strictly controlling for turnover and transaction costs" - and left to independently mine data, formulate novel mathematical expressions using symbolic regression, backtest their strategies across historical limits, and deploy capital into live markets 48. In simulated U.S. equity market testing, agentic AI frameworks have successfully generated robust alpha factors, delivering annualized Sharpe ratios exceeding 3.0 48.

However, the sheer scale of this autonomous infrastructure has triggered profound regulatory and systemic anxieties 288. Global financial authorities recognize that the interconnected nature of LLMs poses unique, unprecedented systemic risks 289. If multiple hedge funds, proprietary trading firms, and retail agents are relying on the exact same foundational AI models, an unexpected model hallucination or a synchronized misinterpretation of a geopolitical event could trigger massive, correlated sell-offs 2589. Academic research from the Wharton School has even identified the risk of "algorithmic collusion," where AI trading systems inadvertently learn to collude and manipulate prices without any explicit programming or communication, severely compromising market liquidity and efficiency 9.

The International Monetary Fund (IMF) and central banks are actively monitoring the potential for AI-driven flash crashes. Their recent Global Financial Stability Reports note that while machine learning significantly enhances day-to-day market efficiency and price discovery, it exponentially increases the potential for rapid destabilization, opacity, and extreme volatility during periods of severe financial stress 478.

Bottom line

Artificial intelligence has fundamentally redefined the underlying architecture of global financial markets, decisively replacing the era of human intuition with the uncompromising regime of mathematical probability. An AI trading signal is not a magical oracle predicting a guaranteed future; it is a highly calibrated mathematical instrument that ingests vast amounts of structured and unstructured data, applies probabilistic reasoning to separate actionable patterns from chaotic noise, and navigates the treacherous physics of market liquidity to execute trades.

While the rapid democratization of these tools has allowed retail investors to challenge the historical dominance of institutional Wall Street, the fundamental laws of finance remain unbroken. Hidden transaction costs will continually erode theoretical margins, overfitted models will inevitably fail in live conditions, and the reflexive nature of markets guarantees that yesterday's informational edge is tomorrow's baseline. Ultimately, the integration of artificial intelligence in trading is not about removing human judgment, but about elevating it - allowing disciplined market participants to manage risk, parse complexity, and allocate capital with unprecedented speed, scale, and statistical clarity.