What Is the VIX and Why IPO Bankers Watch It

The VIX is a real-time market index that measures the expected 30-day volatility of the S&P 500, universally known on Wall Street as the "fear gauge." Investment bankers and corporate executives watch it obsessively because an elevated VIX - typically any sustained reading above 20 - signals high market uncertainty and widening trading costs, which forces underwriters to delay Initial Public Offerings (IPOs) to avoid massive valuation discounts and disastrous opening-day price collapses.

The Anatomy of Wall Street's Fear Gauge

To comprehend why a single mathematical index holds veto power over the multi-billion-dollar global IPO pipeline, one must first dissect what the Cboe Volatility Index (VIX) actually measures. The financial markets possess two types of volatility metrics: historical (realized) volatility, which measures how wildly an asset has swung in the past, and implied volatility, which measures how wildly the market expects an asset to swing in the future 12. The VIX is purely forward-looking 14.

Originally developed in 1993 by Professor Robert Whaley for the Chicago Board Options Exchange (Cboe), the index was initially based on the S&P 100 26. A decade later, in 2003, the Cboe partnered with Goldman Sachs to update the methodology, shifting the underlying benchmark to the broader S&P 500 Index (SPX) and altering the mathematical formula to better reflect modern hedging practices 2. Today, the VIX operates as the premier benchmark for global equity market stress 17.

The Mathematical Engine Under the Hood

The VIX is not calculated by looking at the prices of standard shares of stock. Instead, it is reverse-engineered entirely from the options market. The methodology relies on aggregating the weighted prices of a wide strip of SPX put and call options across various strike prices and expirations 18.

Options function as financial insurance policies for institutional money managers. When geopolitical tensions escalate, inflation reports disappoint, or credit markets freeze, portfolio managers rush to purchase "put options" to insure their equity holdings against a downward price shock 89. Just as property insurance premiums skyrocket when a hurricane approaches the coast, the premiums for these options surge when investors are fearful. The VIX formula captures these inflating option premiums, interpolates them into a 30-day constant maturity bracket, and distills the variance into a single annualized percentage 18.

If the VIX closes at 20, it means the options market is mathematically pricing in an annualized volatility of 20% over the subsequent 30 days 8. Because this index represents a one-standard-deviation move, a VIX of 20 implies a 68% probability that the S&P 500 will remain within a roughly 5.7% range (up or down) over the next month 3. Because demand for downside protection spikes sharpest during violent market sell-offs, the VIX maintains a strong inverse correlation with the S&P 500. When stocks plummet, the VIX violently spikes; when equity markets grind steadily higher, the VIX compresses and drifts lower 8.

Historical Context and Extreme Regimes

Understanding the absolute level of the VIX requires historical context. Since 1990, the long-term average of the VIX has hovered around 18.5 to 19.5 74. However, the index is prone to extreme, explosive moves during black swan events.

During the Global Financial Crisis of 2008, the VIX reached an intraday high of 89.53, and remained stubbornly above the 20-point threshold for an unprecedented 331 consecutive trading days 34. In March 2020, as the COVID-19 pandemic shuttered the global economy, the index spiked to a record closing high of 82.69, forcing massive hedging flows and margin calls across the financial system 45. More recently, the "Volmageddon" event of February 2018 demonstrated how a sudden, sharp volatility shock could wipe out inverse-volatility exchange-traded products and trigger a self-reinforcing loop of forced deleveraging 6. Even localized panic, such as the sudden tariff announcements and global market sell-offs in early 2025, caused the VIX to briefly eclipse the 50 mark, immediately paralyzing capital markets 7.

The IPO Machine: Valuation and Vulnerability

When a private company decides to go public, it embarks on a highly orchestrated, months-long process designed to transition its ownership from a small pool of venture capitalists and founders to the broader public market. Investment banks, acting as underwriters, guide the company through regulatory filings, marketing roadshows, and the ultimate pricing of the shares 8. This pricing mechanism is arguably the most fragile component of the modern financial system, and it is here that the VIX exerts its tremendous gravitational pull.

Information Asymmetry and the Risk Premium

Pricing an IPO is fundamentally an exercise in navigating information asymmetry. Unlike established public companies like Apple or Microsoft, which feature years of audited, quarter-by-quarter financial data and open-market price discovery, a private company is largely a black box 9. The public must rely heavily on the company's prospectus (the S-1 filing in the United States) and the persuasive power of the underwriting syndicate 89.

Because institutional investors - such as mutual funds, sovereign wealth funds, and pension funds - know they possess less information than the company's insiders, they assume significant risk when purchasing shares in an IPO 9. To compensate for this risk, these buyers demand a "risk premium" 1011. In a calm, bullish market (a low VIX), investors are generally willing to overlook minor flaws and accept smaller risk premiums because their overall portfolio performance is strong and capital is abundant.

However, when macroeconomic uncertainty spikes and the VIX breaches 20, the perceived risk of buying an unproven asset skyrockets 610. The market-wide fear measured by the VIX bleeds directly into the microeconomic valuation of the IPO candidate 12. Institutional buyers become highly defensive, scrutinizing balance sheets for any sign of weakness and demanding much larger risk premiums to absorb the new equity 67.

For the issuing company, a higher required risk premium translates directly into a lower valuation. If a technology startup believed its shares were worth $50 based on internal metrics, a high-VIX environment might mean institutional buyers are only willing to pay $35 13. Faced with this massive valuation haircut, companies and their private equity backers usually balk. They are unwilling to dilute their ownership at deeply discounted prices, leading them to postpone the offering indefinitely 1321.

Book Building and the Psychology of Pricing Ranges

The mechanical process of gathering demand for an IPO is known as "book building." Underwriters publish an initial price range (e.g., $18 to $20 per share) and solicit indications of interest from large clients 14. The goal is to build an order book that is significantly oversubscribed, creating a sense of scarcity 15.

Academic studies reveal deep strategic behavior during this phase. Underwriters often deliberately "lowball" the initial price range to generate artificial momentum and guarantee that the offering is fully subscribed 16. Data indicates that IPOs utilizing this lowballing strategy tend to experience massive opening-day pops, often exceeding 33% 16. Conversely, issuers that "highball" their initial ranges attempt to extract maximum capital but risk weak demand, resulting in anemic first-day returns of less than 1% 16.

The success of the book-building process is highly correlated with the broader market's volatility. Research examining the U.S. markets from 1990 to 2019 demonstrates a fairly strong correlation between low market volatility and the percentage of IPOs that price above their initial filing range 25. During speculative bubbles, such as the late 1990s dot-com era, up to 44% of deals priced above their filing ranges. However, when the VIX is elevated, the leverage entirely shifts from the seller (the company) to the buyer (the institution). In turbulent markets, underwriters struggle to build a robust book, often forcing the company to price the shares at the very bottom of the range, or worse, slash the range entirely just to get the deal done 725.

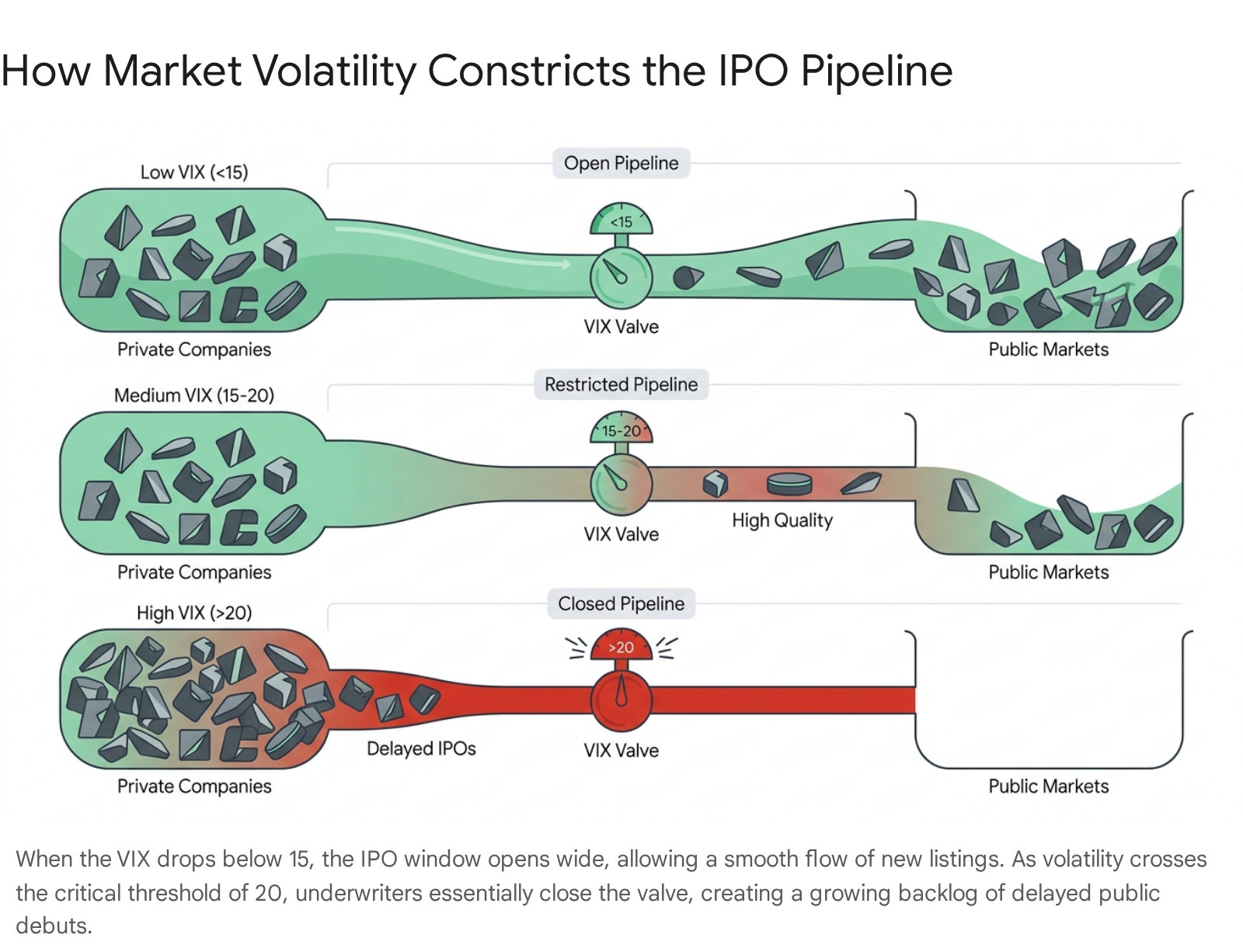

Why a VIX Above 20 Freezes the IPO Pipeline

While 20 is not a rigid law of physics, it operates as a psychological and structural boundary across global trading desks 6. When the VIX sustains levels above 20, the IPO pipeline rapidly constricts.

Empirical research clearly quantifies this dampening effect. A comprehensive study modeling the impact of macroeconomic variables on new listings found that every single-point increase in the VIX reduces expected IPO volume by 3.7% 17. The study further noted that during the post-2008 financial crisis recovery, a sustained elevated VIX led to a 75.1% reduction in IPOs compared to baseline periods 17. Investment bankers understand that launching a company into a volatile market is financially hazardous, as volatile markets inherently expose the primary market makers, the institutional investors, and the founders to unacceptable levels of risk 18.

Comparing IPO Volume Across Market Regimes

To illustrate how drastically market sentiment impacts the ability of companies to raise public capital, it is useful to examine the fluctuating volume of IPOs alongside the predominant market narrative of recent years. The U.S. IPO market has experienced wild cyclical swings dictated largely by central bank policy and the corresponding levels of market volatility.

| Year | Total U.S. IPOs | Aggregate Proceeds ($B) | Prevailing VIX Environment & Market Context |

|---|---|---|---|

| 2019 | 232 | $46.3 | Moderate. Normal cyclical volatility; steady volume of tech unicorns going public. |

| 2020 | 480 | $78.2 | Bifurcated. Massive VIX spike in March halted all deals, followed by heavy central bank intervention that suppressed the VIX and triggered a late-year SPAC boom. |

| 2021 | 1,035 | $142.4 | Historically Low VIX. Unprecedented liquidity, low rates, and suppressed fear led to an all-time record year for new public equities. |

| 2022 | 181 | $8.6 | High VIX / Bear Market. Surging inflation, aggressive rate hikes, and the outbreak of war in Ukraine kept the VIX elevated; the market suffered a 91% drop in proceeds. |

| 2023 | 154 | $19.5 | Elevated / Cautious. Stubborn inflation and regional banking crises kept the IPO window mostly closed, with only selective, high-quality deals surviving. |

| 2024 | 225 | $33.0 | Stabilizing. Gradual easing of inflation and normalization of the VIX allowed a modest recovery, though investors remained highly selective. |

| 2025 | 347 | $47.4 | Constructive. VIX moderated into the 15-20 range; strong rebound led by AI, digital assets, and large healthcare carve-outs. |

Table 1: U.S. IPO deal volume and gross proceeds (2019 - 2025) mapped against prevailing volatility environments. Data reflects traditional IPOs and SPACs exceeding $50mm market cap. 19203021

As the data clearly demonstrates, capital flows freely when volatility is suppressed. In 2021, when the Federal Reserve pushed interest rates to zero and the VIX remained highly subdued, an astonishing 1,035 companies went public in the United States 30. But as inflation roared back in 2022 and the VIX spiked in response to rapid monetary tightening, the IPO market was effectively obliterated, seeing total proceeds collapse from $142.4 billion to a mere $8.6 billion 1920.

Widening Bid-Ask Spreads and Liquidity Death

Beyond the psychological fear of a market crash, a high VIX physically degrades the trading infrastructure necessary for a successful stock debut. This degradation happens through the widening of the "bid-ask spread."

The bid-ask spread is the price gap between what a buyer is willing to pay and what a seller is demanding 22. Market makers - the massive financial institutions that facilitate trading by constantly quoting both buy and sell prices - earn their profit by capturing this spread 23. However, market makers are not in the business of directional speculation; they seek to remain "delta-neutral," meaning they hedge their inventory so they do not lose money if the broader market crashes 23.

When the VIX is elevated, the statistical probability of a stock making a violent, sudden move increases 34. This volatility increases the "inventory risk" for the market maker. To compensate for the increased likelihood of severe slippage while executing their hedges, market makers widen their bid-ask spreads significantly 2324.

For an IPO, a wide bid-ask spread is toxic. A newly listed company relies on deep, tight liquidity to ensure that early trading is smooth and that large institutional orders can be absorbed without wildly distorting the share price 15. When spreads are exceptionally wide due to a high VIX, the stock becomes illiquid 34. A minor wave of retail selling, or a single institution deciding to exit its position early, can cause the stock price to gap down violently, instantly destroying shareholder value.

The Threat of the Broken IPO

The ultimate nightmare scenario for both the issuing company and the underwriting bank is the "broken IPO." A broken IPO occurs when a newly listed stock begins trading below its initial offering price on the open market, or falls below that price shortly after its debut 1525.

A broken IPO is a highly visible, public failure. It signals to the broader financial ecosystem that the underwriters misread the room, priced the valuation far too aggressively, or failed to adequately support the stock in the aftermarket 15. It profoundly damages the reputation of the lead investment bank, angers the institutional clients who were allocated shares of a depreciating asset, and severely demoralizes the company's founders and employees 1315.

When the VIX is trading above 20, the macroeconomic headwinds make broken IPOs highly probable 15. Even mega-cap companies with flawless balance sheets are not immune. For example, during turbulent market cycles, heavily anticipated listings frequently face severe valuation overhangs. A massive offering naturally acts as a liquidity vacuum, and if the broader market is simultaneously experiencing a risk-off liquidation event, the demand will simply not be deep enough to support the newly created supply of shares 1525.

Underwriter Stabilization and the Greenshoe Option

To prevent an IPO from breaking, investment banks utilize a mechanism known as price stabilization. When an underwriter takes a company public, they typically negotiate an "overallotment" or "Greenshoe" option 37. This allows the underwriters to legally oversell the offering to clients by up to 15% 37.

By overselling the IPO, the underwriters effectively create a short position for themselves. If the stock begins to crash on its first day of trading, the underwriters step into the open market and buy back those excess shares 3726. This massive buying pressure serves to artificially prop up the stock price, creating a price floor that prevents the IPO from breaking. Academic research confirms that the distribution of first-day returns is heavily skewed toward exactly 0%, providing concrete evidence that underwriters aggressively intervene to stop prices from falling below the offer mark 122627.

However, price stabilization is an expensive, high-wire act. If the overall market is collapsing due to an exogenous shock (reflected by a surging VIX), the underwriter cannot fight the entire market forever. Eventually, they must withdraw their support, at which point the stock price will inevitably capitulate 26. Because underwriters loathe being forced into extensive stabilization efforts in a crashing market, they will strongly advise their corporate clients to delay the IPO until the VIX drops to a more manageable level 18.

Global Evidence and Notorious Listings

The destructive combination of high volatility and fragile pricing is a global phenomenon. During the height of the COVID-19 pandemic, researchers examining the Turkish stock market found that while IPO volume paradoxically increased, the underpricing and subsequent aftermarket volatility of those companies were extreme, highlighting the difficulty of accurate valuation during a crisis 28. Similarly, studies of Chinese A-shares demonstrate that macroeconomic sentiment and inflation fears heavily dictate first-day returns and the frequency of broken IPOs 2930.

Historical mega-IPOs underscore how critical timing and market conditions are to long-term success. Alibaba Group's $25 billion listing in 2014 executed flawlessly in a stable environment, yielding a 38% first-day gain . Conversely, Facebook's $16 billion IPO in 2012 was marred by technical glitches and market jitters, barely closing above its issue price before suffering a prolonged, months-long decline . General Motors' massive $23.1 billion return to the public markets in 2010 also faced intense volatility, with the stock struggling heavily in the aftermarket amidst industry downturns . The lesson across all these events remains consistent: size alone cannot protect a company from the gravitational pull of market-wide volatility.

Alternative Exits: Direct Listings and SPACs

Frustrated by the traditional IPO process - with its expensive underwriting fees, restrictive lock-up periods, and vulnerability to VIX-induced delays - many companies have sought alternative pathways to the public markets. The two most prominent alternatives in recent years have been Direct Listings and Special Purpose Acquisition Companies (SPACs). However, both mechanisms possess structural flaws that make them highly sensitive to volatility.

Direct Listings: Flying Without a Net

In a direct listing, a private company bypasses the traditional underwriting process entirely. Instead of issuing new shares to raise fresh capital, the company simply allows its existing insiders, employees, and early investors to sell their shares directly to the public on an exchange 144546.

The primary allure of a direct listing is cost savings. By removing the investment bank's underwriting fees and skipping the exhaustive roadshow process, companies save tens of millions of dollars 46. It also prevents the dilution of existing ownership, as no new shares are created 46.

However, the major drawback of a direct listing is the absolute absence of a safety net 46. Because there is no underwriter, there is no book-building process to gauge precise institutional demand, and more importantly, there is no Greenshoe option to stabilize the price 3746. The opening price is determined via an unvarnished, raw auction matching supply and demand 45.

If a direct listing occurs when the VIX is high, the stock is exposed to the full, brutal force of market sentiment. Early trading can be violently volatile, making direct listings highly unsuitable for any company lacking massive, preexisting global brand recognition 4647. Regulatory efforts by the SEC to allow primary capital raises within direct listings have included strict pricing limits to mitigate this exact volatility risk 31. Consequently, direct listings practically vanish during periods of elevated market fear 32.

The SPAC Phenomenon and Regulatory Arbitrage

A Special Purpose Acquisition Company (SPAC) is a publicly traded shell company formed strictly to raise capital through an IPO for the purpose of acquiring an existing private company 3334. When the SPAC successfully merges with a target, the private company inherits the SPAC's listing, effectively going public through the back door (the "de-SPAC" transaction) 34.

During the historically low-VIX environment of late 2020 and 2021, SPAC issuance exploded, driven by retail enthusiasm and a flood of institutional capital 3334. SPACs were heavily marketed as a faster, cheaper alternative to traditional IPOs, offering the perceived benefit of "price certainty" since the valuation was negotiated privately between the SPAC sponsor and the target company 33.

However, deep academic scrutiny has revealed that the SPAC ecosystem is highly fragile and extraordinarily expensive. The costs embedded in the SPAC structure - driven by the "sponsor promote" (essentially free shares given to the SPAC's creators) and massive dilution from warrants - far exceed the underwriting fees of a traditional IPO 3536. Furthermore, research demonstrates that the issuance of new SPACs actually exhibits a negative correlation with the VIX 37. When macroeconomic uncertainty rises, risk-averse investors refuse to park their capital in opaque shell vehicles 3437.

The aftermarket performance of companies that went public via a SPAC merger has been overwhelmingly dismal. Empirical analysis reveals that over a one-year horizon post-merger, de-SPAC companies drastically underperform the broader market, generating an average market-adjusted return of negative 24.6% 36. These devastating losses ultimately led to severe regulatory crackdowns by the SEC to close the disclosure loopholes - often termed "regulatory arbitrage" - that allowed SPAC targets to make wildly optimistic financial projections that a traditional IPO candidate could never legally publish 34.

Comparison of Public Listing Methods

To clearly delineate the varying degrees of volatility exposure across the different listing mechanisms, the table below highlights their structural mechanics and risk profiles.

| Feature | Traditional IPO | Direct Listing | SPAC Merger |

|---|---|---|---|

| New Capital Raised? | Yes | Generally No (Secondary sales only) | Yes (via Trust Account & PIPEs) |

| Underwriter Stabilization? | Yes (Greenshoe Option) | No | No |

| Pricing Mechanism | Book-building process | Free-market opening auction | Private negotiation with Sponsor |

| Sensitivity to VIX | Extremely High (Deals delayed if VIX > 20) | High (Requires calm markets due to lack of stabilization) | High (Issuance drops in volatile markets; high redemption risk) |

| Primary Drawback | Underpricing leaves "money on the table" | Unpredictable opening day volatility | Massive dilution and poor long-term returns |

Table 2: Structural comparison of the three primary pathways to the public equity markets and their respective vulnerabilities to volatility. 1445463436

The Economic Ripple Effects of Delayed IPOs

When the VIX remains stubbornly above 20 and the primary market window closes, the financial pain radiates far beyond the trading floors of Wall Street. A frozen IPO market creates a severe bottleneck that chokes the broader innovation economy, impacting everyone from elite venture capitalists to entry-level software engineers 2155.

The Venture Capital Trap

The venture capital (VC) business model is predicated on liquidity. VC funds raise money from institutional limited partners, invest it in risky, early-stage private companies, and rely on an IPO (or an acquisition) five to ten years later to cash out and return those profits 2137.

When heightened volatility delays IPOs indefinitely, venture capital firms become trapped in their existing portfolios. This extended illiquidity prevents them from returning capital to their investors, which in turn severely complicates their ability to raise their next fund 21. As capital gets tied up in late-stage, mature startups that cannot go public, funding for new, early-stage innovation inevitably dries up across the ecosystem.

Forced "Down Rounds" and Toxic Debt

Private startups generally burn cash at a high rate, building their business models around the assumption that public equity will eventually be available 21. When a VIX spike destroys their IPO timeline, these late-stage companies face sudden and acute funding shortfalls 21.

To survive the delay, they must return to the private markets for emergency capital. However, because the macroeconomic environment is fearful, private investors will demand punitive terms. Startups are frequently forced into accepting a "down round" - a new financing round that values the company at a significantly lower price than its previous valuation 21. Down rounds are catastrophic for a startup's reputation; they severely damage investor confidence, trigger complex anti-dilution provisions that penalize founders, and signal deep distress to the market 21. Alternatively, startups may resort to heavy debt financing, saddling a cash-burning company with massive interest obligations that destroy its long-term financial flexibility 21.

The Plight of the Startup Employee

The most acutely distressed stakeholders in a frozen IPO market are the employees. Tech and biotech startups routinely offset lower base salaries by offering generous stock options, operating under the promise that an eventual IPO will generate life-changing wealth 5556.

When the IPO is delayed, employees find their net worth trapped on paper. The situation becomes dire if an employee wishes to leave the company or is subjected to layoffs, which often follow periods of economic uncertainty 56. Departing employees generally face a draconian 90-day window to exercise their vested options before they expire 5556. Exercising these options requires significant upfront cash, and worse, triggers immediate tax liabilities (such as the Alternative Minimum Tax) on the "paper" gains, despite the employee having no way to sell the stock to cover the tax bill 55.

While a burgeoning secondary market exists for private shares, it is an imperfect solution. Selling shares on secondary platforms requires the company's explicit approval (Right of First Refusal), is restricted to a very limited pool of accredited buyers, and typically forces the employee to accept a steep 20% to 40% discount relative to the stock's fair value 55. For thousands of workers in the innovation economy, a high VIX effectively locks their life savings in a vault to which they hold the combination, but cannot turn the dial.

Bottom line

The VIX serves as the ultimate arbiter of risk in the global capital markets. When the index crosses the critical threshold of 20, the mathematical reality of widening bid-ask spreads and surging risk premiums forces investment bankers to shutter the IPO pipeline to avoid the reputational damage of broken listings. Until macroeconomic fears subside and volatility compresses, a growing shadow backlog of mature private companies, trapped venture capital, and illiquid employee wealth remains paralyzed, waiting for the window to reopen.