What Is an IPO Lock-Up Period and Why Do Stocks Drop

A stock lock-up period is a predetermined window of time following an initial public offering during which company insiders, founders, and early investors are legally prohibited from selling their shares. When this restriction expires, a massive influx of previously restricted equity becomes available to trade on the open market, which historically triggers a surge in trading volume and a temporary decline in the stock's price. For everyday investors, understanding the timing and mechanics of these expirations is a critical component of navigating the volatility of newly public companies.

The Mechanics of Going Public and the Necessity of Lock-Ups

When a privately held enterprise transitions to the public markets through an Initial Public Offering (IPO), the shares offered to the general public on the first day of trading usually represent only a small fraction of the company's total outstanding equity. Historically, companies float roughly ten to twenty percent of their total shares during the initial offering 12. The remaining vast majority of the company is held by early stakeholders, including founders, executive officers, rank-and-file employees, and venture capital backers.

If all of these insiders were permitted to liquidate their holdings on the very first day of public trading, the sheer volume of sell orders would easily overwhelm retail and institutional buyer demand. This immediate supply shock would trigger a catastrophic collapse in the stock price, entirely undermining the IPO process and destroying the company's public valuation 2243. To prevent this scenario, the investment banks managing the IPO require insiders to sign strict lock-up agreements prior to the listing.

The Core Objectives of the Restriction

Lock-up agreements are structurally designed to achieve several primary market functions that protect both the issuing company and the newly participating public investors.

The most immediate function is price stability. By artificially constraining the supply of freely tradable shares, underwriters can carefully manage the balance of supply and demand in the secondary market. This constrained environment allows the stock price to stabilize and find a natural equilibrium during its highly vulnerable first few months of public trading 43648.

Furthermore, these agreements serve a vital psychological and signaling function for the broader market. Public market investors require assurance that the individuals who know the company's internal workings best actually believe in its long-term financial prospects. If insiders immediately cashed out their equity upon listing, the broader market would interpret the mass exodus as a profound lack of faith in the company's future performance. Such an event would cause prospective retail and institutional buyers to flee the asset entirely 226.

Finally, lock-up periods mitigate the inherent risks of information asymmetry. When a company goes public, insiders possess deep, granular knowledge of the firm's operational health that the public does not yet share. The lock-up period forces insiders to hold their equity through at least one or two quarterly earnings reports. This timeline ensures that the broader public market has access to audited, post-IPO financial data before insiders are permitted to execute large-scale liquidations, effectively leveling the playing field 5.

The Regulatory Landscape of Insider Restrictions

A widespread misconception among retail investors is that IPO lock-up periods are strictly mandated by federal securities law. In the United States, neither the Securities and Exchange Commission (SEC) nor the Financial Industry Regulatory Authority (FINRA) explicitly requires companies to implement a lock-up period 24511.

Instead, lock-up agreements are entirely contractual arrangements negotiated between the issuing company, its existing shareholders, and the lead underwriting banks managing the offering 24511. Because they are contractual instruments rather than statutory requirements, the specific terms, durations, and carve-out exceptions can vary wildly from one IPO to the next.

While the SEC does not mandate the existence of the lock-up, federal regulations heavily dictate the disclosure of these agreements. The precise details of a company's lock-up structure must be transparently outlined to the public and can be found in the "Shares Eligible for Future Sale" section of the company's S-1 registration prospectus 446. Additionally, even after a contractual lock-up period expires, insider sales often remain subject to federal securities regulations, such as SEC Rule 144, which governs the volume and manner in which restricted, unregistered securities can be sold into the public market 11613.

Standard Timelines and Contractual Variations

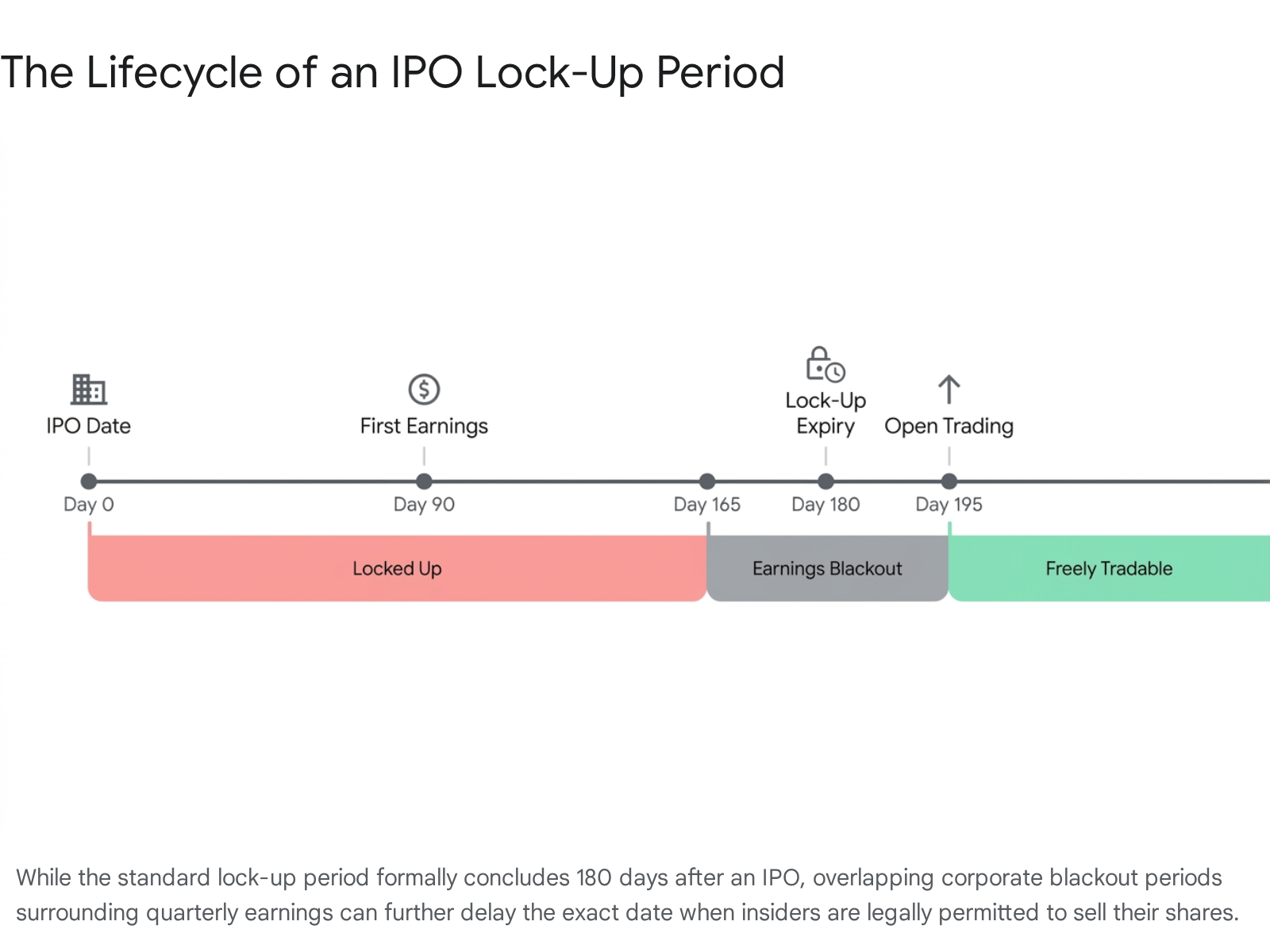

For decades, the standard duration for a traditional IPO lock-up period has been uniformly set at 180 days, or roughly six months, from the date the stock begins trading on a national exchange 23611. However, as capital markets have evolved, underwriters and issuers have developed increasingly complex variations to address specific liquidity goals, tax planning needs, and market conditions.

The Rise of Staggered Expirations

Rather than unlocking the entirety of the restricted insider shares on a single calendar day, many modern technology companies utilize staggered release schedules. This approach releases shares in smaller fractional increments over several months to facilitate a smoother absorption of the new supply into the public float. The intent is to avoid the massive, singular drop in stock price that historically plagues the 180-day mark.

For example, the cloud data company Snowflake released twenty-five percent of its restricted shares after just 91 days, while the food delivery platform DoorDash released forty percent of its shares after the same duration. Other firms, such as the restaurant software company Toast, released fifteen percent of shares immediately following their first public earnings report 2. While staggered releases grant a company more control over the supply of its shares, market analysts note that in some instances, they simply result in multiple, smaller price dips at each respective release date rather than preventing volatility altogether 2.

Conditional Performance-Based Releases

In recent years, underwriters have increasingly utilized price-based or performance-based early release provisions to reward early investors if the public offering is highly successful 22. These complex clauses stipulate that if a newly public stock performs exceptionally well and meets sustained valuation metrics, a designated portion of the lock-up will expire early.

A standard performance condition typically dictates that if the stock closes at a specified percentage above its original IPO price for a sustained period, an early release is triggered. For instance, the agreements for companies like Instacart, Klaviyo, and Reddit dictated that if the stock traded at least thirty-three percent above the initial offering price for ten out of fifteen consecutive trading days following a specific date, a portion of the shares would unlock 21415. In the highly anticipated framework surrounding SpaceX's future public offering, the company outlined a rolling schedule where insiders could sell twenty percent of their shares after the first earnings release, and an additional ten percent if the stock maintained a thirty percent premium over the IPO price 7.

Overlaps with Corporate Blackout Periods

Even when a contractual 180-day lock-up period reaches its mathematical expiration date, insiders may still be legally barred from executing any trades. Public companies maintain strict internal insider trading policies that prohibit employees and executives from buying or selling stock during corporate blackout periods. These blackout windows generally occur in the weeks immediately preceding and following a quarterly earnings announcement, designed to prevent individuals from trading on material, non-public financial results 451417.

If a lock-up expiration date happens to fall squarely inside a quarterly blackout window, insiders must wait until the company officially reports its earnings and the trading window reopens before they can liquidate their equity 5178.

The Economics of the Supply Shock

The expiration of a lock-up period is a highly anticipated and scrutinized event in the financial markets because it fundamentally alters the underlying supply-and-demand mechanics of the specific equity.

When a lock-up expires, the public float of the company can expand exponentially. To illustrate the mathematical severity of this event, if a company initially floated ten million shares during its IPO, and forty million insider shares are suddenly unlocked on day 181, the available supply of the stock quintuples literally overnight 85. Because the market demand from buyers for the stock rarely increases by hundreds of percent at that exact same moment, the basic macroeconomic laws of supply and demand dictate that the asset price must fall to absorb the massive influx of new supply 1459.

Academic Evidence of the Expiration Overhang

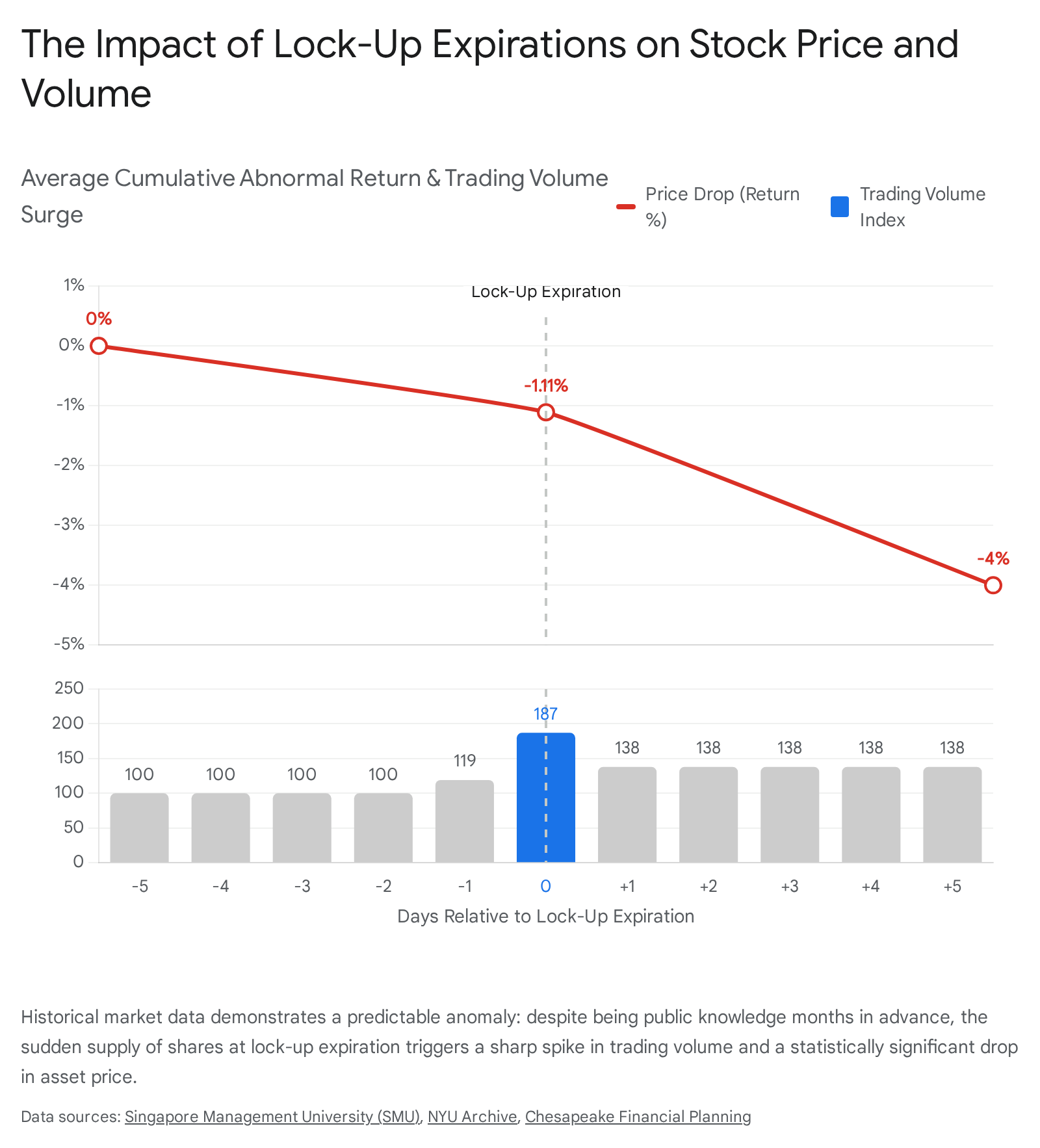

Extensive academic research, analyzing thousands of initial public offerings across several decades, confirms that lock-up expirations consistently result in a permanent downward adjustment in the stock price accompanied by a massive surge in trading activity.

Researchers have documented that stock prices experience a statistically significant average drop directly at the time of lock-up expiration. Studies analyzing U.S. markets indicate abnormal negative returns ranging from just over one percent to nearly three and a half percent 1610. Meanwhile, trading volume skyrockets to absorb the new shares. Research indicates a permanent upward shift in trading volume of approximately thirty-eight to forty percent in the days immediately following the expiration, reflecting the permanent expansion of the tradable float 110.

Furthermore, wealth management data suggests that the downward pressure is rarely confined to a single trading session. Stocks routinely decline an average of three to five percent in the full week following the expiration, and five to ten percent in the subsequent month. This prolonged period of depressed pricing is commonly referred to by institutional traders as the lock-up expiration overhang 11.

| Metric Evaluated | Academic Research Findings at Lock-Up Expiration |

|---|---|

| Average Price Drop (Day of Expiry) | Decreases between 1.15% and 3.29% depending on the specific study and timeframe 1610. |

| Average Trading Volume Surge | Permanent upward shift of 38% to 40% compared to pre-expiration baseline 110. |

| Short Selling Volume | Increases dramatically, occasionally doubling from the pre-expiration average 6. |

| Extended Price Weakness | Declines average 3% to 5% in the first week, and up to 10% in the following month 11. |

The Efficient Market Hypothesis Anomaly

To academic economists and financial theorists, the measurable price drop associated with lock-up expirations presents a fascinating structural anomaly. According to the foundational Efficient Market Hypothesis, sophisticated financial markets instantly reflect all known public information in the price of an asset. Because lock-up expiration dates are explicitly written into public SEC filings months in advance, the market knows exactly when the supply of shares will increase 1610.

Rationally, the anticipated price drop caused by the upcoming supply shock should be fully priced into the stock by investors long before the 180th day actually arrives. Yet, despite being a scheduled and heavily publicized event, the asset price consistently drops anyway on the exact day of the expiration 110.

Market analysts attribute this persistent anomaly to downward-sloping demand curves and severe mechanical constraints on short selling. Short selling is the practice of borrowing shares to bet against a stock, profiting when the price declines. During the 180-day lock-up window, the total supply of available shares in the public float is so constrained that short-sellers literally cannot find enough shares to borrow. Because pessimistic investors are structurally prevented from betting against the stock, the asset price is artificially propped up by optimistic retail buyers during the initial months of trading. When the lock-up ends, the sudden availability of millions of shares finally allows short-sellers to aggressively enter the market, driving the price down to its true mathematical equilibrium 6.

The Real Reasons Insiders Choose to Sell

When everyday retail investors witness a massive wave of insider selling immediately following a lock-up expiration, they frequently panic, assuming that the company's executive team is abandoning a sinking ship 57. While poor internal company performance can certainly motivate an early exit, massive post-lockup sell-offs are almost entirely driven by practical financial mechanics rather than a fundamental lack of faith in the business model.

For early employees and founders who have spent years building a startup, company equity often represents between forty and sixty percent - or significantly more - of their total personal net worth 11. Fiduciary financial advisors strictly mandate selling portions of this concentrated equity simply to diversify risk. Holding millions of dollars of net worth in a single, highly volatile technology stock is considered dangerous speculative positioning, regardless of how strong the underlying company appears to be 11.

Furthermore, the mechanics of venture capital force systemic selling. Institutional investors, such as venture capital and private equity firms, have their own investors, known as Limited Partners, to answer to. Venture capital funds operate on strict life cycles and are contractually obligated to return liquid capital and realize profits within specific timeframes. When a lock-up expires, these funds routinely liquidate or distribute shares to their Limited Partners regardless of their long-term belief in the company's trajectory 56.

Finally, employees holding Restricted Stock Units (RSUs) or non-qualified stock options often face massive income tax liabilities upon the stock vesting and the company going public 11. Selling a portion of the unlocked shares is frequently the only viable way an employee can generate the sheer cash required to satisfy their obligations to the Internal Revenue Service.

To mitigate the negative optics and the disastrous market impact of these massive sales, sophisticated insiders rarely execute standard market orders to dump everything at once. Instead, they utilize algorithmic trading tools. Mechanisms such as Volume-Weighted Average Price (VWAP) or Time-Weighted Average Price (TWAP) algorithms quietly sell small, calculated batches of shares over days or weeks. These tools are designed to blend the insider sales into the normal daily trading volume, ensuring the liquidity event does not violently crash the stock 12.

High-Profile Lock-Up Expiration Case Studies

The expiration of a lock-up period can trigger drastically different market reactions depending on the broader macroeconomic environment, the current profitability of the firm, and the specific capitalization table of the company. Recent market history provides clear examples of both the classic supply-shock disaster and the highly unpredictable short squeeze.

The Classic Glut of Supply

Historically, some of the most hyped public offerings of the modern era have suffered brutal, sustained sell-offs directly linked to their lock-up expirations.

When the social media conglomerate Facebook saw its lock-up expire in August 2012, approximately 270 million insider shares flooded the secondary market. Early investors rushed to exit, and the stock plunged seven percent in a single day to under $20 per share - leaving it trading nearly fifty percent below its highly publicized $38 IPO price 13. Similarly, following months of disappointing post-IPO performance, the ride-sharing giant Uber saw its 180-day lock-up expire in November 2019. The stock plunged 8.7 percent to a record low on the expiration day, erasing nearly $40 billion in market value from its initial IPO valuation 14.

The electric vehicle manufacturer Rivian experienced an even more dramatic collapse in 2022. The company saw its shares sink twenty-one percent in a single trading session when selling restrictions lifted, allowing massive early corporate stakeholders like Ford and Amazon to finally liquidate their positions in a rapidly cooling electric vehicle market 2515.

Even when companies exhibit strong fundamental growth, the lock-up overhang can cap stock momentum. The grocery delivery platform Instacart priced its 2023 offering at $30 per share, briefly popping to $40 before settling into the mid-$30s. Despite the company achieving profitability, the broader macroeconomic environment of high interest rates had forced the company to drastically cut its internal valuation from $39 billion during the pandemic down to roughly $10 billion at the time of the IPO, creating heavy selling pressure from early investors eager to salvage returns when the lock-up cleared 161718.

In the healthcare sector, Medline Industries executed the largest IPO of 2025, raising $6.26 billion at $29 per share in December 2025 1931. The vertically integrated medical supplier had previously been acquired by a consortium of private equity titans including Blackstone, Carlyle, and Hellman & Friedman 3132. As the company approached its June 2026 lock-up expiration, the stock drifted back down to its initial offering price. The tape was heavily dominated by the private equity owners launching massive secondary offerings, steadily increasing the freely tradeable float and capping upward price movement through an abundance of supply 31.

The Relief Rally and the Short Squeeze

Conversely, if the market widely anticipates a massive insider sell-off that never actually materializes, the stock can experience violent upward momentum. Short sellers who heavily bet against the stock in anticipation of the expiration are forced to rapidly buy shares to cover their losing bets, triggering a short squeeze.

The Mediterranean fast-casual restaurant chain CAVA Group saw its lock-up expire in December 2023. Retail traders and institutional short sellers had aggressively bought put options, heavily betting that insiders would dump their shares into the market. Instead, executives and early investors held their positions tight. The complete lack of anticipated selling pressure resulted in what Wall Street analysts termed a relief rally, and the stock unexpectedly popped nearly ten percent 1333.

The British semiconductor designer ARM Holdings provided an even more extreme example in 2024. The company went public in September 2023, but the Japanese conglomerate SoftBank retained a staggering ninety percent ownership stake, floating only 9.5 percent of the company to the public 34352037. When the lock-up on SoftBank's $127 billion stake expired on March 12, 2024, Wall Street braced for a historic crash 343537. However, SoftBank signaled its intent to hold the vast majority of the shares to capitalize on the artificial intelligence boom, using the highly valued equity as collateral for massive corporate loans. Because the market float remained artificially thin, the stock actually gained 2.1 percent on the day of expiration, entirely defying historical trends 342037.

The social media platform Reddit also navigated a highly scrutinized lock-up expiration in August 2024. While Series F late-stage investors were actually sitting on slight losses compared to the 2021 private funding rounds, early Series A investors were sitting on massive twenty-times return multiples 21. Despite fears of a crash, the stock held remarkably stable through the August 9 expiration date, as algorithmic trading managed the employee sell-off and enthusiastic retail buyers absorbed the new supply 152139.

Alternatives to the Traditional IPO Lock-Up

As modern capital markets have evolved, the traditional IPO is no longer the sole pathway for a mature private company to enter the public markets. Two prominent alternatives - Special Purpose Acquisition Companies and Direct Listings - feature radically different lock-up architectures.

The Direct Listing Exemption

Pioneered by technology giants like Spotify in 2018 and Slack in 2019, a Direct Listing allows a company to skip the traditional underwriter process entirely. Because no new capital is raised for the corporate treasury, and no investment bank is hired to guarantee the sale of the equity, there is absolutely no lock-up period imposed on the insiders 2241232425.

In a direct listing, existing employees, executives, and venture capital investors can sell their shares directly on the open exchange on the very first minute of the first day of trading. While this structure provides immediate, democratic liquidity to insiders and entirely prevents the delayed supply shock of a traditional 180-day lock-up, it leaves the stock highly vulnerable to extreme, unfettered price volatility during its first weeks of trading 222627.

To bridge this gap, the SEC recently approved rules for Primary Direct Floor Listings. This hybrid mechanism allows companies to raise fresh capital by selling new shares directly into the opening auction alongside insider shares, without utilizing traditional underwriters. However, widespread adoption of this specific pathway remains rare 252829.

The SPAC Sponsor Lock-Up

In a Special Purpose Acquisition Company (SPAC) transaction, a publicly traded shell company merges with a private target company to take it public. While the rank-and-file employees of the private target company generally face a standard 180-day lock-up similar to an IPO, the financial sponsors who created the SPAC face much stricter timelines.

To prove to retail investors that they are genuinely committed to the long-term viability of the newly merged entity - and are not simply looking to execute a rapid pump-and-dump scheme - SPAC sponsors typically agree to be locked up for a full twelve months 2. However, these sponsor lock-ups frequently include performance-based early release triggers if the stock price surges post-merger 22.

Comparing Public Market Pathways

| Feature | Traditional IPO | SPAC (De-SPAC Merger) | Direct Listing |

|---|---|---|---|

| Primary Goal | Raise new capital and establish a public valuation. | Faster path to public markets via corporate merger. | Immediate liquidity for existing shareholders without raising new capital. |

| Underwriting Fees | High (typically up to 7% of capital raised) 30. | Moderate to High (deferred underwriter fees and PIPE financing) 3050. | Low (fees paid to financial advisors, but no traditional underwriting spread) 2224. |

| Lock-Up Period for Company Insiders | Standard 180 days 22. | Standard 180 days for target company 2. | None. Immediate liquidity on day one 224123. |

| Lock-Up Period for Sponsors | N/A | Often 12 months for the SPAC Sponsors 2. | N/A |

| Price Discovery Mechanism | Determined by underwriters via private institutional "book-building". | Negotiated privately between the target firm and the SPAC sponsor 50. | Determined purely by public market supply and demand in the opening auction 2229. |

Recent Regulatory Proposals Affecting Post-IPO Liquidity

The regulatory landscape governing how quickly newly public companies can facilitate subsequent stock sales continues to shift. In May 2026, the SEC proposed sweeping amendments under a broader "Make IPOs Great Again" agenda. These proposals aim to significantly streamline the registered offering framework 313233.

A major component of this proposal seeks to dramatically expand eligibility for Form S-3, the short-form registration statement that allows companies to conduct highly efficient shelf offerings. Previously, newly public companies were forced to wait twelve months post-IPO before utilizing Form S-3, and smaller companies with a public float below $75 million faced strict caps on how much equity they could sell. By proposing to eliminate the twelve-month waiting period and the $75 million threshold, the SEC aims to allow recently listed companies to tap the capital markets much faster 313233. If enacted, these reforms would drastically alter the post-lockup environment, granting newly public firms unprecedented agility to execute secondary offerings and at-the-market programs immediately following the expiration of their initial lock-up agreements.

Strategies for the Retail Investor

For everyday retail investors looking to purchase shares of a newly public company, understanding the mechanics of the lock-up period is an essential component of portfolio risk management.

Because the expiration overhang is a statistically verified phenomenon across thousands of equities, many wealth managers advise retail clients to simply avoid buying IPO stocks until the 180-day lock-up period has fully cleared 454. Waiting out this restricted period allows the market to fully digest the massive influx of insider shares, ensures that the company has published at least two quarters of audited public earnings for scrutiny, and allows the stock to settle into a true, unconstrained equilibrium price 554.

While some aggressive traders attempt to actively time the market by short-selling the stock in the days immediately preceding the expiration, this is a highly volatile and dangerous strategy. As evidenced by the trading activity surrounding CAVA and ARM Holdings, if insiders decide not to sell their unlocked shares, the resulting short-squeeze can inflict catastrophic financial losses on those betting against the stock 4345556. Ultimately, tracking expiration dates in SEC filings allows retail investors to avoid unnecessary volatility and make purchasing decisions based on complete market data.

Bottom line

A lock-up period is a highly specific contractual mechanism designed to stabilize a newly public company by preventing insiders from flooding the market with shares immediately after an IPO. When this standard 180-day window expires, the sudden expansion of tradable shares routinely triggers a massive surge in trading volume and a temporary decline in the stock's price, creating an anomaly known as the expiration overhang. While retail investors frequently misinterpret post-lockup selling as a lack of executive confidence in the business, these sales are overwhelmingly driven by routine portfolio diversification, venture capital fund mechanics, and the need to cover heavy tax obligations. Investors should carefully track these expiration dates in public filings, as they represent moments of extreme volatility and permanently shifting supply-and-demand dynamics.