Equity volatility and the timing of initial public offerings

Introduction to Equity Volatility and Capital Formation

The relationship between equity market volatility and primary capital issuance represents a fundamental dynamic in corporate finance. The initial public offering (IPO) process requires a delicate equilibrium between issuer valuation expectations, underwriter risk management, and institutional investor demand. This equilibrium is highly sensitive to broader market uncertainty, which dictates the willingness of capital allocators to absorb unseasoned risk. The standard proxy for this uncertainty is the Cboe Volatility Index (VIX), a metric that functions as a primary gating mechanism, dictating whether the equity underwriting window is open, restricted, or closed to new entrants.

The VIX, often colloquially referred to as the "fear gauge," traces its origins to the financial economics research of Menachem Brenner and Dan Galai in 1989, who proposed a series of volatility indices updated frequently to serve as underlying assets for futures and options 1. Officially introduced in 1993 and subsequently updated in 2003 in collaboration with Goldman Sachs, the modern VIX measures the 30-day forward-looking implied volatility of the S&P 500 index 12. It is calculated by aggregating the weighted prices of a broad spectrum of put and call options on the S&P 500, effectively distilling the market's expectation of near-term price variance into a single, observable index value 123.

In the context of equity capital markets (ECM), the predictability of future asset prices is the bedrock of transaction execution. When equity volatility is low, pricing certainty is high, facilitating smooth bookbuilding and the efficient allocation of shares. Conversely, when the VIX spikes, the pricing of risk becomes highly erratic, widening bid-ask spreads in the secondary market and increasing the probability that an IPO will fail to price within its indicative range or will break its issue price in aftermarket trading 45. To quantify the acceleration of this fear, institutions also monitor the VVIX, an index measuring the volatility of the VIX itself, providing insights into the velocity of market panic 1.

Historically, investment banks and ECM syndicates have utilized specific thresholds of the VIX - most notably the 20 and 25 levels - as heuristic boundaries for market accessibility 67. However, recent shifts in the macroeconomic landscape, particularly the transition from the Zero Interest-Rate Policy (ZIRP) era to a high-rate environment, have altered the absolute applicability of these thresholds 89. Furthermore, the evolution of alternative liquidity structures, such as private credit and robust secondary markets, has diminished the urgency for companies to endure volatile public markets 71112. Simultaneously, highly capitalized megatrends, such as artificial intelligence (AI), have demonstrated an unprecedented immunity to traditional volatility gating, supported by massive institutional demand that overrides broader market hesitations 131415.

The Underwriting Risk Model and Information Asymmetry

To fully comprehend why implied volatility acts as a strict gatekeeper, it is necessary to examine the fundamental mechanics of the IPO underwriting process. Taking a private company public involves substantial information asymmetry between the corporate issuer (who possesses intrinsic knowledge of operations), the underwriting syndicate (acting as an intermediary and underwriter of risk), and institutional buyers (who must evaluate the asset based on disclosed prospectus data and roadshow presentations) 589.

Pre-Deal Investor Education and Price Discovery

The IPO bookbuilding process is essentially an elaborate price discovery mechanism designed to mitigate this structural asymmetry. Prior to the formal roadshow, underwriters engage in Pre-Deal Investor Education (PDIE) to gauge preliminary demand 5. During these phases, institutional investors signal their appetite and price sensitivity, allowing underwriters to narrow the indicative price range 5.

In environments characterized by low volatility, macroeconomic conditions, future cash flows, and terminal discount rates are relatively stable. This stability makes it easier for buy-side analysts to agree on a valuation multiple and for mutual funds to confidently allocate capital 8. When the VIX rises, it signifies a sudden spike in the expected variance of the broader market. This exogenous uncertainty dramatically increases the cost of pricing errors for all parties involved. Underwriters face the immediate threat of holding unsold inventory on their balance sheets if they price an offering too high in a volatile market - a scenario that severely penalizes syndicate capital. Conversely, pricing the offering too low merely to guarantee a clearing price leaves excessive "money on the table," heavily diluting the issuing company's founders and early venture backers 510.

Variability of Initial Returns and Aftermarket Liquidity

High market volatility increases the dispersion of analyst estimates and inevitably widens the bid-ask spreads in secondary trading. Research examining IPOs between 1965 and 2005 demonstrates that initial return variability is considerably higher when the fraction of difficult-to-value companies going public increases, a dynamic that is exacerbated during periods of elevated aggregate uncertainty 11. In these environments, the risk premium demanded by investors to absorb newly issued, unseasoned equity rises sharply 812.

If the required risk premium exceeds the issuer's willingness to discount their equity, the transaction fails to clear, effectively closing the IPO window. Volatility, therefore, is not merely a psychological barrier; it mathematically impairs the risk-reward ratio of the syndication process 622. The 1998 Russian debt default serves as a prime historical example; as global volatility skyrocketed, a severe mutual fund "flight to liquidity" occurred, disproportionately crushing the issuance and aftermarket performance of small-cap IPOs while investors retreated to safe-haven assets 13.

Empirical Volatility Thresholds and Bracketing Mechanics

While equity capital markets are inherently dynamic, distinct behavioral thresholds related to the VIX have been empirically documented and are actively utilized by leading underwriters, including Morgan Stanley, Goldman Sachs, and JPMorgan 61425. Extensive historical data demonstrates that aggregate initial public offering volume contracts sharply during quarters where the implied volatility index sustains levels above 20. Furthermore, the market approaches a complete standstill when volatility crosses the 25 threshold, indicating severe institutional risk aversion 62226.

The prevailing industry consensus categorizes market receptivity into specific volatility brackets, which dictate syndicate behavior, pricing leverage, and overall issuance volume.

| VIX Level Bracket | Market Window Status | ECM Syndicate Behavior and Issuer Dynamics |

|---|---|---|

| < 15 | Optimal / Wide Open | Benign volatility encourages high issuance volumes. Pricing is highly predictable, and issuers frequently price at or above the midpoint of the indicative range. Growth-stage companies and smaller capitalizations face minimal friction in accessing capital 1516. |

| 15 - 20 | Normal / Selective | The historical mean of the VIX generally resides in this range (e.g., a long-term average around 19 to 20) 1417. The window is open, but institutional investors exercise standard diligence. Solid business models with clear paths to profitability are required 1418. |

| 20 - 25 | Restricted / Gated | Crossing the 20 threshold is historically viewed as the demarcation line for average transactions. It generally delays IPO launches by two to four weeks. The syndicate requires steeper IPO discounts to compensate for aftermarket trading risk 62531. |

| > 25 | Closed / Hard Stop | Severe market stress. Broad-based fear overrides individual company fundamentals. Institutional capital rotates into defensive assets. Nearly all planned IPOs are postponed, withdrawn, or shifted toward alternative private funding mechanisms 62226. |

The threshold of 20 serves as the critical pivot point. When the VIX sustains levels above 20, portfolio managers pivot toward hedging their existing portfolio exposures rather than absorbing the unique, unseasoned risks associated with an IPO 619. In periods of extreme distress - such as when the VIX remained above 30 for 75 non-consecutive days during the 2011 European sovereign debt crisis - issuance approaches absolute zero, leading to significant backlogs of mature companies trapped in the private markets 20.

Data compiled by Jay Ritter on IPO statistics from 1980 through 2025 highlights these cyclical droughts and floods. During benign volatility periods, such as 1996, the market saw 689 operating company IPOs 10. Conversely, during the volatility spikes of the 2008 global financial crisis, only 21 operating companies successfully went public 10. Even the Special Purpose Acquisition Company (SPAC) boom, which offered an alternative route to public markets and generated annualized SPAC period returns of 23.9% between 2010 and 2020, eventually succumbed to broader market volatility and regulatory scrutiny as the macro environment shifted 21.

Statistical Modeling of IPO Volume and Overdispersion

Recent academic and quantitative studies have sought to rigorously define the relationship between the VIX and IPO counts using advanced econometric techniques. Because IPO volume represents count data characterized by periods of extreme euphoria followed by extended droughts, it violates the basic assumptions of standard Ordinary Least Squares (OLS) regression 18. Instead, researchers employ Negative Binomial Regression to account for the inherent overdispersion in the data 18.

Bai-Perron Structural Break Detection

A critical feature of modern IPO market analysis involves the application of Bai-Perron structural break detection. This methodology partitions historical IPO activity into distinct regimes based on endogenous market shifts rather than arbitrary calendar dates 18. Empirical testing using monthly data from 1995 to 2024 reveals that IPO markets do not follow a single stable data-generating process. The Bai-Perron analysis identifies multiple structural breaks that partition IPO activity into six distinct regimes, each exhibiting fundamentally different variance characteristics 18.

The negative binomial models confirm a statistically significant inverse relationship: elevated VIX levels explicitly reduce IPO activity 18. The models also incorporate the 10-year Treasury yield (DGS10) as a proxy for financing costs. The stability of the negative coefficients across various specifications (e.g., VIX at -0.038 and DGS10 at -0.187) confirms that both market uncertainty and the risk-free rate exert a persistent, dampening effect on capital issuance 18. Regime-specific likelihood ratio tests reveal that extreme overdispersion (with variance-to-mean ratios ranging from 2.77 to 33.74) typically emerges during financial crises, subsides during stable post-recession periods, and returns with unprecedented intensity following black swan events, such as the pandemic-induced volatility in early 2020 18.

Stock Fragility and Precautionary Cash Holdings

These econometric models also highlight the phenomenon of "stock fragility." Firms observe higher aggregate uncertainty (proxied by high VIX periods) and high product market fluidity, recognizing that their equity is susceptible to non-fundamental demand shocks 35. When equity fragility increases, corporate management teams build precautionary cash holdings, reduce capital expenditures, and actively avoid issuing equity in the public markets. This creates a self-reinforcing feedback loop that further depresses IPO volume during volatile regimes 35.

Regional Volatility Indices: VSTOXX and VHSI

While the VIX is the premier global gauge due to the dominance of the US equity market, regional volatility indices dictate the underwriting windows in Europe and Asia. The gating mechanics are conceptually similar, but the liquidity profiles, threshold sensitivities, and underlying derivative structures vary significantly by geography.

The European Market and VSTOXX

In Europe, the EURO STOXX 50 Volatility Index (VSTOXX) serves as the primary gauge of investor sentiment and implied volatility 3637. The VSTOXX is calculated based on the rolling 30-day implied volatility of options on the EURO STOXX 50 Index 3738. European IPO markets tend to be more fragile and sensitive to geopolitical and macroeconomic shocks compared to the deep liquidity pools of the US 3639. Consequently, the VSTOXX gating threshold is often more rigid, and sudden market corrections expose less-liquid European exchanges to disorderly sell-off episodes 36.

During periods of high economic policy uncertainty, European investors rapidly demand higher liquidity premiums 436. The European Securities and Markets Authority (ESMA) frequently notes that when VSTOXX spikes, European IPO issuance plummets, as evidenced by the heavy delays in listings during the onset of the COVID-19 pandemic before rebounding in late 2020 36.

To better capture this regional nuance, researchers developed the EURsent index, a composite sentiment measure constructed using Principal Component Analysis (PCA). The first principal component of EURsent accounts for over 51% of the total variance in European market sentiment, integrating the VSTOXX alongside German bond yield spreads and gold prices 40. Because European capital markets rely heavily on bank financing, local issuers are more likely to seek alternative financing - such as private debt or European Central Bank (ECB) subsidized corporate bond purchases - when VSTOXX is elevated. ECB interventions, such as the Corporate Sector Purchase Programme (CSPP), have historically lowered primary issuance spreads by up to 41 basis points during normal conditions, offering a vital bypass when equity markets are volatile 41.

The Asian Market and VHSI

In the Asia-Pacific region, the HSI Volatility Index (VHSI) operates as the regional equivalent of the VIX, measuring the 30-day expected volatility of the Hang Seng Index in Hong Kong 382243. The Hong Kong market possesses unique structural characteristics, including heavy retail participation and the prevalence of highly leveraged derivative instruments like Callable Bull/Bear Contracts (CBBCs) 43.

CBBCs function as knock-out barrier options; if the underlying index hits a specific call level, the contract is immediately terminated, potentially resulting in total loss of the investment 43. The high volume of these instruments exacerbates intraday volatility. Gating thresholds in Hong Kong are heavily influenced by both domestic Chinese economic policy and global US dollar liquidity. When VHSI spikes, the underwriting window for mid-cap technology and consumer firms in Asia frequently shuts. However, the Hong Kong market occasionally exhibits higher tolerance for volatility in state-backed or heavily subsidized sectors, resulting in a dual-track IPO environment where premium offerings can sometimes push through an elevated VHSI environment, while standard corporate offerings remain gated 2223.

Regime Fluidity: Interest Rates and Macroeconomic Policy

A critical nuance in contemporary financial analysis is the recognition that the "VIX 20" threshold is not an absolute law of physics, but a fluid boundary that shifts alongside the prevailing macroeconomic interest rate regime 745. The transition from a historically loose monetary environment to a restrictive one fundamentally alters how volatility interacts with capital formation.

The ZIRP Era vs. High-Rate Environments

During the Zero Interest-Rate Policy (ZIRP) era that dominated the aftermath of the 2008 financial crisis through the early 2020s, global central banks provided unprecedented liquidity 8946. In this environment, the cost of capital was artificially suppressed. Because fixed-income yields were near zero, institutional investors were forced further out on the risk curve in search of yield, creating an insatiable appetite for equities - specifically high-growth, unprofitable technology IPOs 84748. Under ZIRP, the market could tolerate higher localized volatility because the overarching macro environment guaranteed liquidity; the "central bank put" effectively subsidized risk-taking 8.

The transition to a high-rate regime (post-2022) fundamentally altered the mathematics of equity underwriting 2450. With risk-free rates climbing significantly, the discount rate applied to future corporate cash flows in discounted cash flow (DCF) models increased dramatically 5051. In a high-rate environment, the combination of a high VIX and high borrowing costs creates a compounding restrictive effect. Investors demand immediate cash flow and profitability, severely punishing speculative assets that rely on terminal value projections a decade into the future 5152.

Therefore, in the contemporary landscape, a VIX of 18 in a high-rate environment may act as a stronger deterrent to an IPO than a VIX of 22 did during the ZIRP era. The interaction between the VIX and interest rate differentials is also evident in foreign exchange markets. Studies on Uncovered Interest Rate Parity (UIRP) deviations demonstrate that funding liquidity (often measured by the TED spread) and market stress (VIX) are inextricably linked 1225. Sudden unwinding of currency carry trades tends to occur when global risk appetite drops and funding liquidity tightens, transmitting volatility across borders and simultaneously shutting equity issuance windows globally 1225.

Shifting Valuation Paradigms: The Rule of 40

As the macroeconomic regime shifted and the cost of capital normalized, the underwriting criteria utilized by investment banks to evaluate IPO candidates underwent a brutal recalibration. The era of "growth at all costs" - where venture-backed consumer and technology companies were rewarded with massive revenue multiples regardless of their cash burn - was decisively superseded by a mandate for "precision and profitability" 145254.

The New Fundamental Gatekeeper

The defining metric of this new regime is the "Rule of 40." Primarily applied to Software-as-a-Service (SaaS), fintech, and technology-enabled companies, the Rule of 40 dictates that a company's revenue growth rate plus its EBITDA margin should equal or exceed 40 percent 472454.

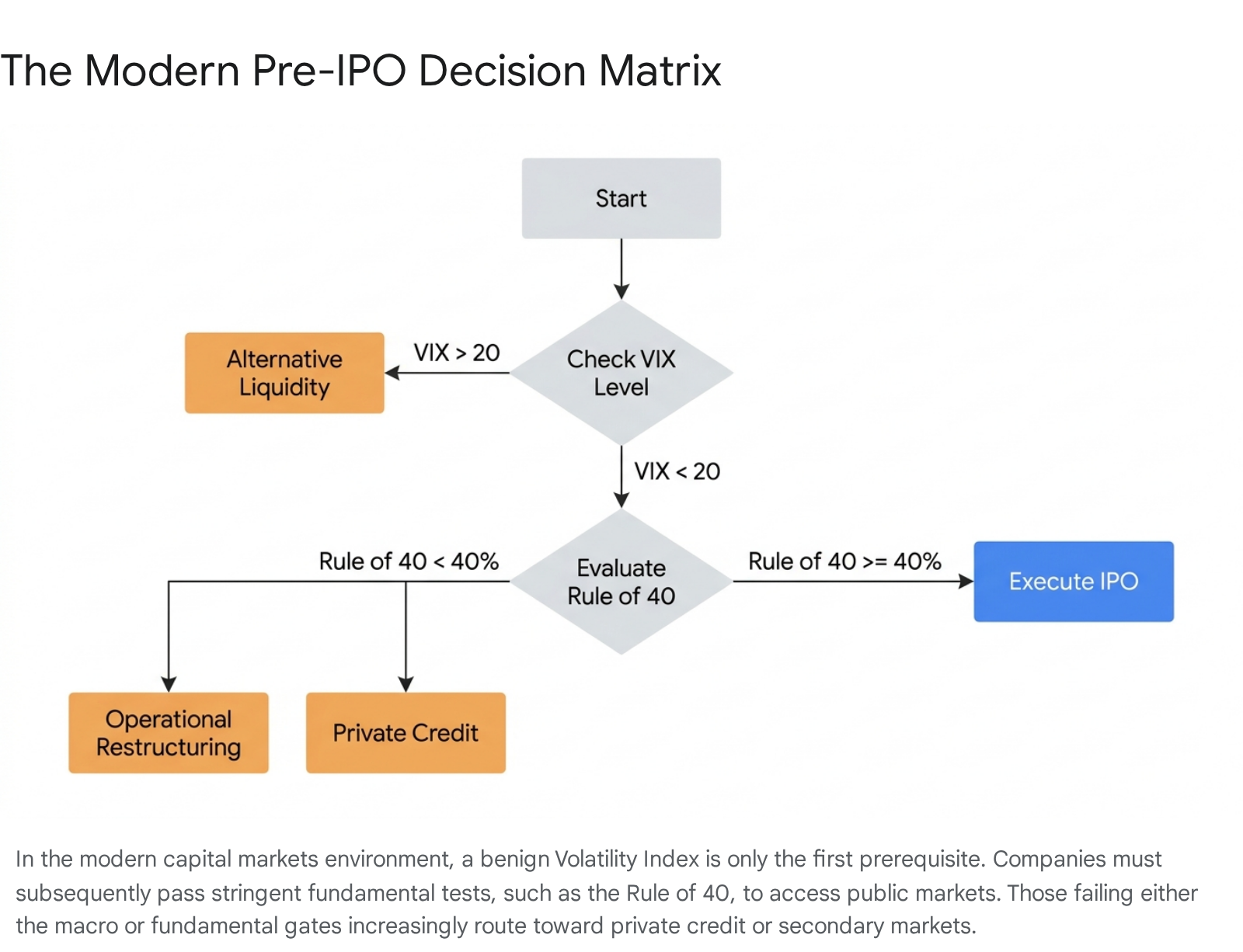

In the current market, the Rule of 40 serves as a secondary, fundamental gating mechanism that operates in tandem with the macro VIX threshold.

Even if the VIX is benign (e.g., below 15), companies that fail the Rule of 40 struggle to price an IPO without suffering massive valuation haircuts 5152. By late 2025, median public SaaS revenue growth had fallen to 12.2%, yet roughly half of leading public SaaS firms had achieved EBITDA profitability, as management teams pivoted sharply from growth to margin discipline 4724.

| Valuation Paradigm | ZIRP Era (Pre-2022) | High-Rate Era (2024-2026) |

|---|---|---|

| Primary Valuation Metric | Top-line Revenue Growth; Total Addressable Market (TAM). | Rule of 40 (Growth + EBITDA Margin); Unit Economics (LTV:CAC > 3:1). |

| Profitability Stance | Acceptable to burn cash heavily to capture market share 54. | EBITDA profitability (or a rapid, credible path to it) is mandatory 1451. |

| SaaS Revenue Multiples | Hyper-inflated: 15x - 30x forward revenue 4754. | Compressed: 3.4x - 8x forward revenue 5154. |

| VIX Tolerance | High tolerance; IPOs priced even during moderate volatility spikes due to FOMO. | Low tolerance; elevated VIX combined with high rates immediately halts unprofitable offerings 6. |

The market enforces this rule aggressively. SaaS companies scoring above 40% command median valuations of approximately 9.4x revenue, whereas those falling below the threshold languish in the 2x to 3x range 52. This bifurcation signifies that public market investors are no longer willing to subsidize unprofitable operations. For example, a business growing at 20% with a 25% margin (Score: 45) will receive a stronger reception from an IPO syndicate than a business growing at 40% with a negative 10% margin (Score: 30) 52. European healthtech unicorns, such as Doctolib, experienced 40% secondary market devaluations primarily due to this multiple compression, forcing them to aggressively cut losses to prepare for future public offerings 51.

Sectoral Divergence: The Artificial Intelligence Exemption

While the broader consumer, fintech, and traditional SaaS sectors remain heavily constrained by the VIX and the Rule of 40, the 2025-2026 market has revealed a striking exception: the Artificial Intelligence (AI) and deep-tech infrastructure sectors 131455. The sheer magnitude of the AI megatrend has created a distinct micro-climate within the equity markets, demonstrating a remarkable degree of immunity to standard volatility gating.

The Compute Capital Siphon

Public equity markets have found themselves structurally underweight in pure-play, scaled AI businesses 13. Because the fastest-growing AI companies have remained private longer than technological pioneers in previous cycles, a massive gap formed between private market innovation and public market access 13. Consequently, there is overwhelming, pent-up institutional demand for exposure to AI compute, infrastructure, and semiconductor manufacturing 1355.

This dynamic is perfectly exemplified by the anticipated mega-IPOs of entities like SpaceX - whose Starlink constellation is increasingly positioned as an orbital AI compute asset - and foundational model developers like Anthropic, OpenAI, and hardware manufacturers like Cerebras 155657. Investment banks projecting exponential revenue growth have engineered massive retail and institutional FOMO (Fear Of Missing Out). For instance, Goldman Sachs projections suggesting SpaceX's AI-related revenue could surge to $322 billion by 2030 illustrate the scale of the narrative being sold to the market 1558.

For these apex assets, the traditional VIX threshold is effectively overridden. The scarcity of tier-one AI assets means that passive investment flows, early index eligibility expectations, and thematic allocations will absorb the offering regardless of ambient market volatility 1357. Furthermore, as AI scales, it introduces concepts from the token economy, where metrics such as token velocity and network burn rates are evaluated alongside traditional earnings per share, challenging Wall Street to adapt its valuation frameworks in real-time 55. However, it is vital to note that this immunity is strictly localized to infrastructure, compute, and highly defensible data platforms; consumer-facing AI applications lacking a clear technological moat remain subject to the standard volatility and profitability gates 146061.

Alternative Liquidity Bypasses: Private Credit and Secondary Markets

Historically, a closed IPO window meant that venture-backed companies were stranded, forced into highly dilutive down-rounds, or required to drastically slash operational expenditures. However, the maturation of alternative private markets over the last decade has fundamentally decoupled liquidity from public listings 711. Today, when the VIX spikes and shuts the underwriting window, late-stage issuers possess robust alternative bypasses: the private secondary market and the private credit market 71262.

The Expansion of Late-Stage Secondaries

The private secondary market has exploded in volume, surpassing $240 billion globally by 2025, a 48% year-over-year increase 711. As companies delay their IPOs to mature their governance and financials in order to meet the Rule of 40, founders, early employees, and venture funds from older vintages require liquidity 12. Through structured private liquidity programs, company-sponsored tender offers, and proprietary platforms like the FNEX Institutional Dark Pool, institutional capital can purchase equity from existing shareholders without the company undergoing a public offering 71162.

For ultra-high-net-worth (UHNW) family offices and institutional allocators, purchasing pre-IPO shares of mature unicorns offers asymmetric growth exposure without the daily mark-to-market volatility of the public exchanges 12. Secondaries provide visibility into established company performance with exit pathways usually within a 3 to 5 year horizon, effectively acting as a pressure release valve that allows companies to satisfy early stakeholders while waiting for the VIX to recede 12.

Private Credit as Equity Replacement

Simultaneously, the private credit market has stepped in to replace traditional equity growth rounds 711. When public equity markets are volatile, issuing new shares is highly dilutive and structurally dangerous. Instead, late-stage venture-backed companies are increasingly utilizing senior-secured growth loans. These instruments extend corporate runway ahead of a potential liquidity event without resetting valuations or diluting existing cap tables 7.

These private credit structures offer immense flexibility. They typically feature customized terms, delayed funding takedowns, interest rates hovering around 10% to 11%, and conservative loan-to-value ratios under 25%, often paired with minimal warrants representing less than 1% of fully diluted ownership 7. By leveraging private debt, management teams can maintain their growth trajectories, execute M&A, and achieve Rule of 40 compliance in a controlled, private environment. The IPO is no longer a desperate necessity for corporate survival; it has been relegated to a position of strategic optionality, executed solely when volatility conditions are optimal and valuations can be maximized 7.

Conclusion

The VIX remains the indispensable barometer of market sentiment, acting as the primary gating mechanism for initial public offerings. The historical paradigm - where a VIX below 15 signals an open window and a VIX above 20 triggers a hard stop - remains fundamentally valid for the vast majority of corporate issuers. High equity volatility mathematically destroys the pricing certainty required by underwriting syndicates to clear massive blocks of unseasoned stock, exacerbating information asymmetry and driving institutional capital toward safe havens.

However, the architecture of the global capital markets has evolved significantly. The VIX threshold is no longer a static figure but a fluid boundary that interacts heavily with prevailing interest rates and the macroeconomic cost of capital. In the post-ZIRP environment, the hurdle to go public has been raised considerably. Fundamental operational metrics, specifically the Rule of 40, have replaced the speculative fervor of "growth at all costs," acting as a secondary gate that issuers must pass regardless of the ambient volatility level.

While certain generational megatrends, specifically AI compute and infrastructure, possess the gravity and institutional demand to force open the IPO window irrespective of market fear, the broader corporate landscape must rigorously respect the volatility gauge. Fortunately, the exponential growth of private secondary markets and bespoke private credit facilities has provided a vital structural buffer. Companies are now equipped to navigate periods of high volatility by accessing vast pools of private capital, allowing them to patiently optimize their unit economics until the VIX recedes and the public underwriting window reopens.