How an IPO Works from Filing to First Trade

An initial public offering transforms a privately held company into a publicly traded entity through a highly regulated, multi-month process of financial audits, institutional marketing, and complex price discovery. While retail investors typically experience an IPO only on the day shares hit the stock exchange, the actual mechanisms - ranging from the filing of the S-1 registration statement to institutional book building and underwriter price stabilization - occur long before the opening bell rings. Ultimately, the process is designed to balance the company's need to raise capital with the underwriting banks' mandate to ensure market stability and reward early institutional backers.

The Long Road to Going Public: Preparation and the S-1 Filing

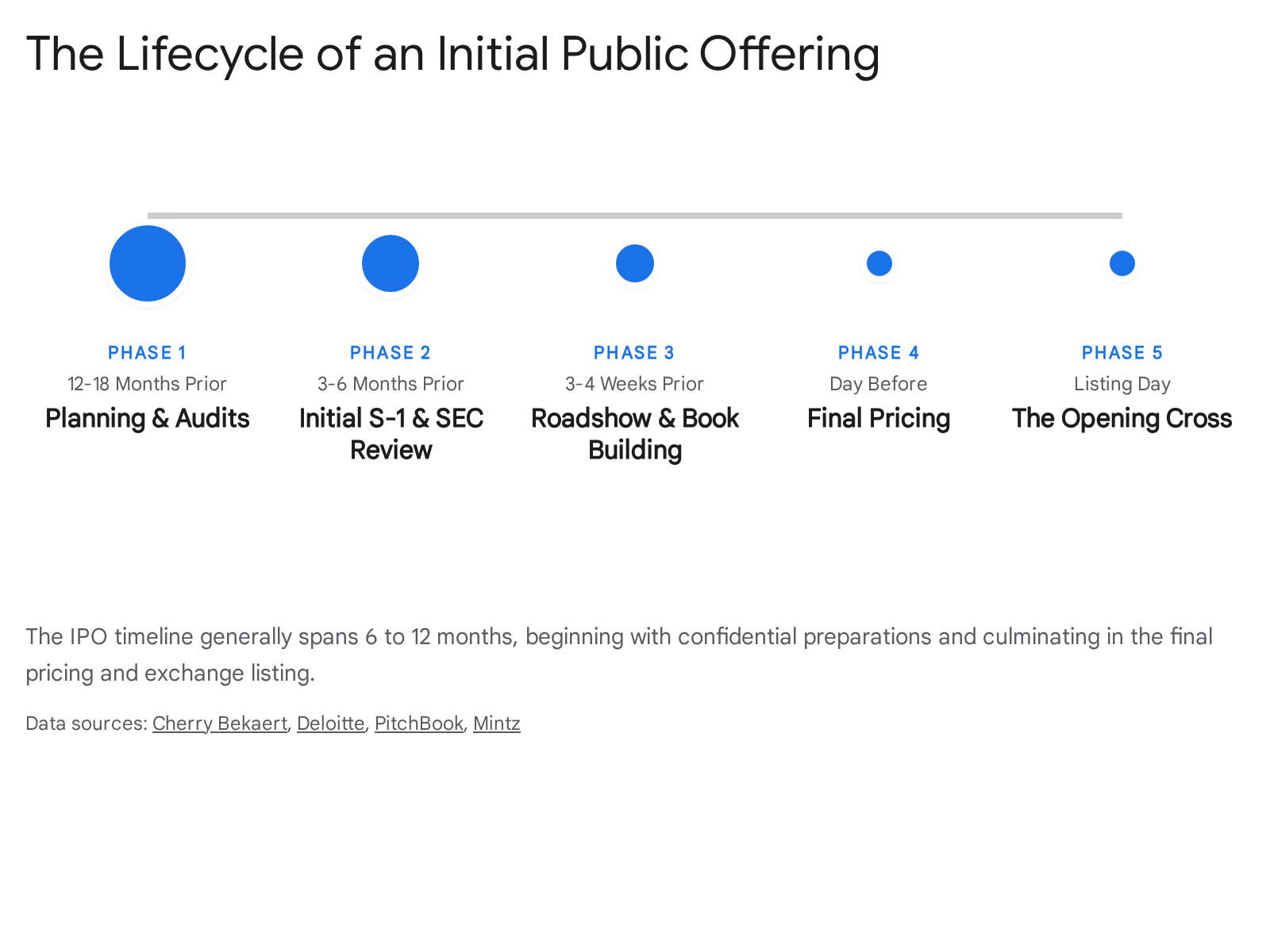

The decision to take a company public is never made overnight. For a traditional initial public offering (IPO), the timeline typically spans twelve to eighteen months from the initial board decision to the day the shares are listed on an exchange 12.

The first six to nine months of this period are consumed by intense internal preparation. Private companies must overhaul their corporate governance, transition their accounting practices to meet stringent public market standards, and engage third-party auditors to ensure compliance with the Public Company Accounting Oversight Board (PCAOB) 1.

During this preliminary phase, the issuing company also selects a syndicate of investment banks to act as underwriters. These banks, which will eventually be responsible for marketing and selling the shares, guide the company through the structural considerations of the offering, including evaluating potential market capitalization, determining the size of the share float, and advising on whether to issue a primary offering of new shares, a secondary offering of existing shares, or a combination of both 34.

Once the internal audits are complete and the underwriting syndicate is formed, the formal regulatory process begins with the submission of a Form S-1 registration statement to the U.S. Securities and Exchange Commission (SEC) 56. The S-1 is the foundational disclosure document for any domestic company going public. For foreign private issuers looking to list depositary receipts on American exchanges, the equivalent document is the Form F-1 7.

Initially, companies often file their S-1 confidentially, allowing the SEC to review the documents and issue private comment letters without exposing the company's financial data to competitors 12. The SEC evaluates the S-1 strictly for compliance with disclosure requirements - it does not judge whether the company is a good or bad investment 8. The regulatory body typically takes about thirty days to provide its first round of comments, triggering an iterative process. The company must respond to these comments and file amended versions of the registration statement, commonly referred to as S-1/A filings. It is entirely standard for an issuer to go through two to four rounds of amendments before the SEC is satisfied 29.

Eventually, the S-1 must be filed publicly, opening a window for investors and analysts to scrutinize the company's inner workings. Federal securities laws mandate a "quiet period" following the public filing, during which company executives are heavily restricted from discussing the business or providing forward-looking guidance outside of what is explicitly written in the prospectus, ensuring that all potential investors have access to the exact same information 10.

Decoding the S-1 for the Retail Investor

For the intelligent investor, the S-1 is a treasure trove of data that strips away the marketing veneer of a private startup. Because private companies are not legally obligated to publish financial statements, the S-1 is usually the first time independent, audited financials are made available to the public, covering two to three years of historical revenue, expenses, margins, and cash flow 6.

Navigating an S-1 requires an understanding of its key components. The document always opens with a Prospectus Summary, which serves as the company's executive elevator pitch. It distills the market opportunity, headline financial metrics, and the overarching business model into a highly digestible narrative 611. Following the summary is the Management's Discussion and Analysis (MD&A), a critical section where executives provide a narrative explanation of their financial performance, detailing why revenues grew or why margins contracted during specific quarters 6.

However, the most revealing sections of an S-1 are often buried deeper in the text. The Risk Factors section, mandated by the SEC, requires the company to exhaustively list every conceivable threat to its business operations. While this section is dense with legal boilerplate regarding macroeconomic downturns or generic industry risks, careful reading can uncover company-specific vulnerabilities. For example, a company might disclose that it faces significant regulatory hurdles in a key market, or that a substantial portion of its technology relies on a contested patent 610.

Another vital metric to evaluate is customer concentration, which is typically detailed in the Business section. If a company generates more than thirty percent of its total revenue from a single customer, that client represents a massive single point of failure. If that core customer defects or renegotiates their contract, the entire business model could face collapse. Investors also look closely at contract lengths; a company relying on month-to-month renewals carries significantly more operational risk than one locked into multi-year enterprise agreements 69.

The Use of Proceeds section outlines exactly how the company intends to spend the capital raised in the IPO. Specificity is generally viewed as a strong signal of strategic planning - such as paying down a specific tranche of high-interest debt or funding the construction of a new manufacturing facility. Conversely, if the section relies heavily on vague language about "general corporate purposes," it may indicate a lack of immediate capital deployment strategy 911. Finally, the Related-Party Transactions section, though often only a few pages long, can reveal complex financial entanglements between the company, its founders, and its board members, highlighting potential conflicts of interest before the company transitions into the public sphere 9.

Traditional IPOs vs. Alternative Listing Methods

While the traditional IPO process outlined in the S-1 filing is the historical standard, capital markets have evolved to offer companies alternative pathways to public exchanges. The two most prominent alternatives are Direct Listings and Special Purpose Acquisition Companies (SPACs). The decision of which path to pursue depends heavily on a company's financial maturity, its need for immediate capital, and its tolerance for underwriter fees and market volatility 91314.

A traditional IPO is fundamentally a capital-raising event. The company issues new shares, sells them to institutional investors through underwriters, and injects that fresh cash onto its balance sheet to fund growth 1315. However, this process is expensive - underwriter fees alone can consume five to eight percent of the total capital raised - and the timeline is notoriously long and rigid 913.

For highly mature companies that already possess robust balance sheets and strong brand recognition, a Direct Listing offers a streamlined alternative. In a Direct Listing, the company does not issue any new shares, nor does it raise any new capital for the corporate treasury. Instead, the process serves entirely as a liquidity event for existing shareholders - founders, employees, and early venture capital backers - allowing them to sell their previously private shares directly on the public exchange 1315. Because there is no capital raise, there is no need for traditional underwriters to build an order book or guarantee a sale price. The opening share price is determined purely by the organic forces of market supply and demand on the first day of trading. This eliminates the massive underwriting fees, but it also removes the safety net of underwriter price stabilization, often leading to significantly higher initial volatility 1315.

The third pathway is the SPAC, often referred to as a "blank check company." A SPAC is a shell corporation with no commercial operations that goes public through a traditional IPO solely to raise capital 91415. The capital is placed in a trust, and the SPAC's management team - the sponsors - typically has 18 to 24 months to identify and merge with a private operating company. Once a target is found, the two entities undergo a "de-SPAC" merger. Through this transaction, the private company absorbs the SPAC's publicly traded ticker and the cash in its trust, effectively bypassing the arduous traditional IPO timeline 91415.

SPACs offer private companies a faster route to the public markets, usually completing the merger process in three to five months 14. They also provide certainty regarding valuation, as the acquisition price is negotiated privately between the target company and the SPAC sponsors rather than being subject to the whims of institutional bidders during a roadshow 13. However, SPACs carry their own unique risks. The transaction costs can be surprisingly high when accounting for the equity dilution awarded to the SPAC sponsors (the "promote"), and investors in the SPAC hold the right to redeem their shares before the merger closes, which can severely deplete the available cash pool delivered to the target company 91415.

| Feature | Traditional IPO | Direct Listing | SPAC (De-SPAC Merger) |

|---|---|---|---|

| Primary Objective | Raise new capital and create a public market for shares. | Provide liquidity for existing shareholders without raising new corporate capital. | Merge a private company with a publicly traded shell company for a faster listing. |

| Capital Generation | Significant new capital raised through the issuance of new equity. | No new shares are issued; no proceeds flow to the company. | Capital is absorbed from the SPAC's trust and supplementary private financing (PIPE). |

| Underwriter Role | Central. Investment banks manage the sale, price the shares, and stabilize the market. | Minimal. Banks act strictly as financial advisors without guaranteeing share sales. | Replaced by the SPAC sponsors who negotiate the merger valuation directly. |

| Pricing Mechanism | The offering price is set by the underwriter based on institutional book-building demand. | The opening price is determined entirely by market supply and demand on listing day. | The valuation is fixed via a private negotiation between the target and the SPAC. |

| Process Timeline | 12 to 18 months of preparation and regulatory review. | Faster than an IPO, though still requires SEC registration. | 3 to 5 months for the de-SPAC merger execution. |

| Cost Profile | High transaction costs, including underwriter fees of 5% to 8%. | Lowest transaction costs due to the absence of underwriter spread fees. | High overall costs driven by sponsor promotes and complex equity dilution. |

The Roadshow: Pitching to the Titans

Assuming a company chooses the traditional IPO route, the process shifts from regulatory compliance to aggressive marketing approximately three to four weeks before the target listing date. Once the SEC has cleared the preliminary S-1 prospectus, the company embarks on the "roadshow." This is a grueling, multi-city (and increasingly virtual) tour where the company's executive leadership, flanked by their lead underwriters, deliver high-stakes presentations to the world's most powerful institutional investors 161710.

The target audience for the roadshow consists almost exclusively of Qualified Institutional Buyers (QIBs) - pension funds, mutual funds, sovereign wealth funds, and massive hedge funds. These entities control billions of dollars in capital and possess the financial firepower necessary to absorb large blocks of the newly issued stock 1011. The underwriters organize a schedule of one-on-one meetings and large group luncheons, allowing fund managers to interrogate the CEO and CFO about their revenue projections, competitive moats, and path to profitability 3.

The roadshow serves a dual purpose. For the company, it is the primary opportunity to generate hype and secure the capital necessary to guarantee the offering's success 16. For the underwriters, the roadshow is fundamentally an intelligence-gathering operation. The investment banks need to determine exactly how much these institutions are willing to pay for the stock, a process formally known as price discovery 1612.

How Does Book Building Work?

In the early days of capital markets, IPOs were often conducted as fixed-price issues, where the company and its bankers simply guessed a fair price and offered the shares to the public on a take-it-or-leave-it basis 1621. If the price was set too high, the issue would fail; if set too low, the company missed out on massive amounts of capital. To solve this inefficiency, modern capital markets overwhelmingly rely on a dynamic price discovery mechanism known as book building 2122.

Book building functions essentially as a sealed-bid auction. Prior to the roadshow, the underwriters publish an indicative price band - a minimum and maximum estimated price per share 122123. For example, the company might announce its intention to sell 20 million shares at a price band of $28 to $30. During the roadshow meetings, institutional investors evaluate the company and submit confidential bids to the lead underwriter. These bids specify the exact number of shares the institution wants and the maximum price they are willing to pay within (or sometimes above) the price band 161222.

The lead underwriter consolidates all these bids into a master ledger, known as the order book. By analyzing the order book on a daily basis, the underwriter can map the exact demand curve for the stock 122223. If the order book shows that investors have bid for 100 million shares at $30, but the company is only offering 20 million shares, the offering is heavily oversubscribed. In such cases of massive demand, the underwriter and the company may choose to revise the price band upward before the final pricing date 122123.

This exact scenario played out during the highly anticipated IPO of Arm Holdings, the British semiconductor giant backed by SoftBank, in late 2023. Arm initially set an aggressive price band of $47 to $51 per share 13. As the roadshow kicked off in early September, the underwriters rapidly accumulated massive indications of interest from anchor investors, including major tech conglomerates like Apple, Nvidia, and Alphabet 13. Within a week, the order book revealed that institutional demand was six times greater than the supply of shares being offered. Armed with this undeniable proof of market appetite, the underwriters comfortably priced the IPO at the absolute ceiling of the range, setting the final price at $51 per share. This strategic book building successfully secured a $54.5 billion fully diluted valuation for Arm, allowing SoftBank to raise $4.87 billion while parting with less than ten percent of its equity 132514.

Conversely, if the order book is sluggish and bids are clustering at the bottom of the range, the underwriter may have to lower the offering price to ensure all shares are sold, or in extreme cases, postpone the IPO entirely 1612. The book building process ensures that the final offering price is grounded in actual market demand rather than speculative guesswork, drastically reducing the risk of a failed offering 122123.

The Allocation Game: Why Retail Investors Are Last in Line

Once the roadshow concludes and the order book is closed, the underwriters and the company executives meet to finalize the offering price. With the price locked in, the underwriters must decide how to divide the limited pool of shares among the eager bidders. This process, known as allocation, reveals a stark structural divide between institutional wealth and the retail public 1011.

When financial news outlets report that an IPO priced at $30 per share, that is the price paid exclusively by the primary market participants who receive direct allocations from the underwriting syndicate. The vast majority of these coveted allocations - often between 85% and 95% of the total offering - are awarded directly to the institutional funds that participated in the roadshow 1015.

This heavy institutional bias is not born out of malice toward the individual investor, but rather structural necessity and risk management 10. From a logistical standpoint, the underwriting syndicate guarantees the sale of the entire share block. It is vastly more efficient and secure to allocate millions of shares to a handful of massive pension funds and mutual funds than to process hundreds of thousands of micro-transactions for individual retail accounts 11. Furthermore, underwriters prioritize institutional clients because they are perceived as stable, long-term "buy-and-hold" investors. Investment banks actively try to avoid allocating shares to day traders who might "flip" the stock for a quick profit on the first day, as immediate mass selling can crash the share price and ruin the IPO's momentum 1011.

For the everyday retail investor, gaining access to shares at the primary offering price is exceptionally difficult. The SEC does not regulate how underwriters distribute shares, leaving the decision entirely up to the banks' business discretion 11. In highly anticipated, "hot" IPOs where the order book is oversubscribed, underwriters naturally reward their most lucrative, fee-generating institutional clients with the largest allotments 11.

While some major brokerages do receive small tranches of IPO shares to distribute to their retail customers, access is heavily gatekept. Brokerages typically restrict IPO participation to their wealthiest clients. For instance, platforms often require a retail investor to hold between $100,000 and $500,000 in exclusive non-institutional assets, or to be enrolled in premium private client services, just to be eligible to request shares 1528. Even if a retail investor meets these steep financial thresholds, their request is subject to proprietary algorithms that may only allocate a fraction of the shares they applied for 1529.

Consequently, the vast majority of retail investors must wait until the primary allocation is complete and the shares begin trading organically on the secondary market - the stock exchange 16. By the time the stock is available to the general public, the price may have already skyrocketed far above the official IPO offering price, forcing retail investors to buy in at a significant premium 1617.

The Underpricing Phenomenon: Leaving Money on the Table

When a highly anticipated company finally hits the secondary market, it is common to witness a massive surge in its share price. This "first-day pop" is celebrated by financial media as the hallmark of a successful market debut. However, within the realm of academic finance, this phenomenon is known as IPO underpricing, and it represents a massive, hidden transfer of wealth away from the issuing company 181934.

An IPO is considered underpriced when the official offering price - the price the company sold its shares to institutional investors - is significantly lower than the price the market establishes at the end of the first day of public trading 3420. When this happens, the company essentially sold its equity at a steep discount.

Consider the 2023 IPO of the grocery delivery platform Instacart. Following a period of venture capital hype, Instacart and its underwriters priced its IPO at $30 per share, giving the company a fully diluted valuation of approximately $10 billion 212223. The moment the shares debuted on the Nasdaq exchange, intense public demand drove the price to an intraday peak of $42.95, a near 40% premium, before finishing the session at $33.70 for a 12% first-day gain 232425.

While a 12% gain seems modest compared to the dot-com era, the financial implications are profound. If Instacart had set its IPO price at $33.70 instead of $30, it would have captured that extra capital directly on its balance sheet. Instead, that profit was captured by the institutional investors who bought at $30 and instantly held an asset worth $33.70. Financial economists refer to the aggregate foregone capital - calculated by multiplying the first-day price jump by the total number of shares sold - as "money left on the table" 181926.

The sheer scale of money left on the table is staggering. According to comprehensive databases maintained by Professor Jay Ritter at the University of Florida, IPO underpricing is a persistent structural feature of global capital markets 422728. In 2025 alone, the 90 traditional operating companies that went public in the United States experienced an average first-day return of 29.3%. In total, these 90 companies left $13.11 billion on the table 2627. Historically, the money left on the table by issuers routinely dwarfs the explicit fees paid to the underwriting investment banks, sometimes representing years of aggregate corporate profits lost in a single day 1819.

Why Do Companies Accept Underpricing?

If underpricing costs companies billions of dollars in theoretical capital, why do corporate boards and executives continually accept offering prices that seem disconnected from actual market demand? Academic literature categorizes the theoretical explanations into several distinct branches, bridging behavioral psychology, information asymmetry, and strategic marketing 29.

Information Asymmetry and the Winner's Curse: One of the foundational explanations for underpricing is rooted in the "lemons problem." In any IPO, there is an imbalance of information between highly informed institutional investors and uninformed retail investors 2946. Informed investors can accurately value a company; they will only bid on high-quality IPOs and will avoid overpriced, low-quality offerings 29. Uninformed investors, unable to tell the difference, bid on everything. Consequently, uninformed investors face the "winner's curse": they only receive their full allocation of shares when the informed investors have abandoned a bad deal. To keep uninformed investors participating in the IPO market - which is necessary to ensure all deals are fully subscribed - underwriters must systematically underprice all IPOs to guarantee an average positive return that compensates for the risk of buying bad offerings 2946.

Compensating for Information Production: A related theory posits that underpricing is a necessary bribe paid to institutional investors. During the roadshow, underwriters rely on the feedback from fund managers to gauge market demand and discover the true value of the company 30. Producing this deep fundamental analysis costs time and money. If an underwriter prices an IPO perfectly at its maximum market value, the institutional investor extracts zero profit for their analytical labor 3048. Therefore, underwriters deliberately underprice the shares to compensate these institutions for revealing their true valuations, ensuring their continued participation in the book-building ecosystem 3048.

Marketing and Legitimacy: From a corporate strategy perspective, many companies view the money left on the table not as a loss, but as a highly effective marketing expense 3132. A massive first-day pop generates relentless positive coverage on financial news networks. For consumer-facing companies, this media frenzy translates directly into increased web traffic, brand recognition, and product sales 32. Furthermore, a surging stock price enhances the company's prestige, making it vastly easier to recruit top-tier talent and negotiate favorable terms with suppliers 2031.

Prospect Theory and Wealth Effects: Perhaps the most compelling explanation for why founders and executives do not rage against their investment bankers is rooted in behavioral economics. The "Prospect Theory" model highlights that human beings evaluate outcomes based on changes in wealth rather than absolute wealth levels 181951. When a company goes public, the founders usually sell only a small fraction of their total equity, retaining the vast majority of their shares. While the company leaves millions on the table via the shares it did sell, the surging secondary market price simultaneously multiplies the paper value of the executives' retained shares 1820. The psychological euphoria of becoming newly minted billionaires completely overshadows the abstract frustration of foregone corporate capital 1851.

Agency Conflicts and "Spinning": A darker explanation involves conflicts of interest between the underwriter and the issuer. Because underwriters are compensated based on the success of the deal, they have an inherent incentive to underprice the offering to ensure it sells out quickly with minimal marketing effort 4648. Furthermore, during the late 1990s dot-com boom, it was revealed that underwriters routinely engaged in "spinning" - allocating highly underpriced, guaranteed-profit IPO shares directly into the personal brokerage accounts of executives at other companies 52. In exchange for this personal windfall, those executives would hire that specific investment bank to underwrite their own company's future stock offerings. In this scenario, underpricing was essentially used as currency for corporate bribery 52.

| Historical IPO Data Highlights (U.S. Market) | 1980 - 2019 Average | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Number of Operating Company IPOs | 158 | 54 | 72 | 90 |

| Average First-Day Return (Underpricing) | 19.0% | 15.3% | 15.3% | 29.3% |

| Aggregate Money Left on the Table | N/A | $1.92 Billion | $3.72 Billion | $13.11 Billion |

| Average Age of Company at IPO | 9.5 Years | 10 Years | 14 Years | N/A |

Data sourced from Professor Jay Ritter's IPO Database, University of Florida. Excludes SPACs, penny stocks, and ADRs 264227.

Listing Day: The Anatomy of the First Public Trade

For the general public, the culmination of the entire IPO process occurs on the morning the stock officially lists on a major exchange. However, a common source of confusion for retail investors is the timing of the first trade. While the U.S. stock market officially opens at 9:30 AM Eastern Time, a newly minted IPO almost never begins trading at the opening bell. It is entirely normal for a highly anticipated stock to remain locked for an hour or more while the exchange processes a massive backlog of buy and sell orders 3354.

This delay is a necessary feature of the market. Prior to the open, there is no established secondary market price for the stock. If the exchange simply unlocked trading at 9:30 AM, the sheer volume of uncoordinated market orders would result in chaotic, highly destructive price swings. To prevent this, exchanges utilize sophisticated price discovery mechanisms to calculate an opening equilibrium price. How this is achieved depends entirely on the specific exchange where the company chose to list.

The New York Stock Exchange: Human-Led Auctions

The New York Stock Exchange (NYSE) relies on a hybrid trading model that blends modern electronic order matching with traditional human oversight 3435. The linchpin of the NYSE IPO process is the Designated Market Maker (DMM), a specialized floor trader responsible for maintaining a fair and orderly market for the newly listed stock 3436.

On the morning of the IPO, the DMM acts as an auctioneer. Sitting at the center of the trading floor, the DMM aggregates all the incoming electronic buy and sell orders into an electronic book 3436. Rather than letting an algorithm blindly execute the trades, the DMM manually publishes a "pricing indication" - a public dollar range estimating where the stock is likely to open based on the current order flow 36.

This human element provides critical flexibility. The DMM remains in constant communication with the lead underwriter and the floor brokers. If there is a massive imbalance of buy orders, the DMM can widen the pricing indication to attract more sellers, or inject various price points into the system to manually gauge market elasticity 3436. The pricing indication is updated iteratively, gradually narrowing the range until a perfect equilibrium point is found where supply meets demand. Only when the DMM and the underwriter are satisfied that the order book is stabilized does the DMM lock in the single price, print the first bulk execution to the tape, and officially open the stock for continuous trading 3436. The NYSE argues that this human-curated process results in significantly lower volatility on listing day 3435.

The Nasdaq: Algorithmic Price Discovery

In stark contrast to the NYSE's traditional floor auction, the Nasdaq operates a fully electronic, algorithmic trading environment 35. Nasdaq's IPO price discovery is handled entirely by an automated facility known as the Opening Cross 3738.

The Nasdaq process is defined by strict phases of data dissemination. Starting at 9:25 AM, Nasdaq begins accepting pre-open limit and market orders 5437. Simultaneously, it begins broadcasting the Net Order Imbalance Indicator (NOII). The NOII is a vital data feed that acts as the market's radar; it publicly displays the current indicative clearing price and reveals whether there is an overwhelming surplus of buy orders or sell orders at that specific price 543760.

Following a mandatory ten-minute "Display Only" period, the IPO enters the "Pre-Launch Period" 37. During this window, there is no fixed maximum time limit. The lead underwriter sits at a terminal, monitoring the NOII data in real-time 5437. If the algorithm shows a chaotic imbalance - for instance, heavy retail buying pressure unmatched by institutional selling - the underwriter will delay the launch, allowing the system to absorb more orders until the imbalance neutralizes 3760.

Once the order flow stabilizes, the algorithm calculates the exact crossing price. This price is determined mathematically: it is the single price point within the bid-ask spread that maximizes the number of shares that can be paired off, while simultaneously minimizing the number of unexecuted orders 3860. When the algorithm finds this optimal node, the lead underwriter gives the green light. The Nasdaq system executes the Opening Cross in a fraction of a second, broadcasting the Nasdaq Official Opening Price (NOOP) to the global tape, and regular trading commences 373860.

| Exchange Feature | New York Stock Exchange (NYSE) | Nasdaq Stock Market |

|---|---|---|

| Trading Model | Hybrid: Blends human floor trading with electronic systems. | Fully Electronic: Relies entirely on automated algorithms. |

| Central Authority | Designated Market Maker (DMM) manually manages the open. | The Opening Cross algorithm mathematically matches orders. |

| Price Transparency | DMM publishes iterative "pricing indications" (a dollar range). | System broadcasts the Net Order Imbalance Indicator (NOII). |

| Underwriter Interaction | Verbal/floor communication with the DMM to judge order flow. | Digital monitoring of the NOII feed to determine launch timing. |

| Corporate Identity | Historically favored by blue-chip, industrial, and financial giants. | Historically favored by high-growth technology and biotech firms. |

Sources: NYSE and Nasdaq exchange documentation 5434353638.

Global Markets: Listing in London vs. Hong Kong

While the NYSE and Nasdaq dominate the global capital landscape, the battle for international listings highlights distinct structural and geopolitical differences in IPO processes. Historically, the London Stock Exchange (LSE) was the premier destination for cross-border listings. However, in recent years, London has suffered a severe hemorrhage of listings. In 2023, 88 companies delisted or transferred their primary listings away from London, replaced by only 18 new entrants, pushing LSE fundraising to its lowest levels since 1995 39.

Conversely, the Hong Kong Stock Exchange (HKEX) has experienced periodic revivals, frequently surpassing both New York and London in global IPO rankings by serving as the primary conduit between Chinese enterprises and international capital 39. The HKEX listing process mirrors the UK and US in its reliance on institutional roadshows and book building, but it operates under unique regulatory frameworks designed to manage cross-border complexities 740.

For example, mainland Chinese enterprises listing in Hong Kong often structure their offerings as "H-shares" or "Red chips" 41. H-shares refer to companies incorporated in mainland China that gain approval to list on the HKEX, creating a bifurcated equity structure where "foreign shares" trade freely in Hong Kong while "domestic shares" remain restricted on the mainland 41. Furthermore, Hong Kong IPOs enforce a strict retail clawback mechanism. If the public retail tranche is heavily oversubscribed during the book-building phase, the HKEX mandates that shares initially allocated to global institutional investors be legally clawed back and redistributed to the Hong Kong retail public, ensuring domestic market participation - a regulatory safeguard entirely absent in the institutional-heavy US market 40.

Aftermarket Stabilization: The Greenshoe Option

The opening cross marks the beginning of secondary market trading, but the underwriter's job is far from finished. The first few days of trading following an IPO are notoriously erratic. Massive blocks of shares are changing hands as institutional investors lock in day-one profits, and retail investors flood the market driven by media hype 4.

To prevent the stock from entering a catastrophic free-fall due to this chaotic volume, underwriters utilize a powerful, SEC-sanctioned price stabilization mechanism known as the Over-Allotment Option, universally referred to on Wall Street as the Greenshoe Option 426566.

Named after the Green Shoe Manufacturing Company, which first pioneered the clause in 1919, the Greenshoe operates through the mechanics of legal, naked short selling 4265. The mechanism is embedded in the underwriting agreement long before the roadshow begins. It grants the underwriting syndicate the right to legally oversell the IPO by up to 15% of the total base offering 4243.

The stabilization strategy unfolds in three distinct steps:

1. Creating the Short Position: Imagine a company wants to raise capital by issuing 10 million shares at $20 per share. To establish pricing control, the underwriter deliberately accepts orders from institutional clients for 11.5 million shares. The underwriter fulfills these orders, meaning they have sold 1.5 million shares that do not actually exist yet. The underwriter is now in a naked short position of 1.5 million shares 4243.

2. The Market Reaction: Once the stock begins trading on the exchange, the market dictates the underwriter's next move. * Scenario A: The Price Surges. If the IPO is a massive success and the stock price rockets to $25, the underwriter is mathematically exposed to a devastating loss on their 1.5 million share short position. To protect themselves, the underwriter officially exercises the Greenshoe Option. This contractual clause forces the issuing company to instantly create the extra 1.5 million shares at the original $20 IPO price. The underwriter buys these newly minted shares directly from the company to cover their short position. The underwriter neutralizes their risk, and the issuing company receives a massive bonus - an extra 15% in capital raised beyond their initial goal 426543. * Scenario B: The Price Collapses. If the IPO is poorly received - a "break issue" - and the stock immediately plummets to $18, the underwriter shifts from defense to offense. Because they are short 1.5 million shares, they must eventually buy shares to close out their position. Instead of exercising the Greenshoe to buy new shares from the company at $20, the underwriter steps directly into the open market and begins buying the plummeting stock at $18 4243.

3. Achieving Stabilization: Scenario B is the true magic of the Greenshoe. As panicked retail and institutional investors try to sell their falling shares, the underwriter acts as a massive, artificial buyer of last resort. The underwriter's relentless purchase of 1.5 million shares absorbs the excess supply on the market, creating a floor beneath the crashing stock and providing vital liquidity 4243. Furthermore, because the underwriter originally sold those shares at $20 and is now buying them back at $18, the bank pockets the $2 spread as profit, turning a market failure into a lucrative stabilization exercise 43.

Ultimately, the Greenshoe is the only method the SEC permits underwriters to use to legally manipulate a newly issued stock's price, serving as a critical shock absorber that protects both the issuer's reputation and the investors' capital during the turbulent transition to public life 6566.

Bottom line

The journey of an IPO is fundamentally an exercise in risk management and price discovery. From the rigorous disclosures of the S-1 filing to the high-stakes negotiations of the institutional roadshow, every step is designed to secure capital for the issuer while protecting the underwriting banks from market failure. While retail investors are structurally disadvantaged during the initial allocation phase, understanding the hidden mechanics of book building, intentional underpricing, and Greenshoe stabilization reveals exactly why newly public stocks behave with such volatility the moment they hit the open exchange.