Why IPO Stocks Pop and How Prices Are Set

Initial public offering (IPO) prices are deliberately set below their estimated secondary market value by investment banks to ensure the stock sells out and to reward early investors for taking on the risk of an unproven public company. The famous first-day "pop" is the result of this intentional underpricing colliding with massive public demand and a tightly restricted supply of shares on the open exchange. Before long-term fundamentals take over, the opening days of trading are governed entirely by these engineered supply-and-demand imbalances.

The Mechanics of Going Public

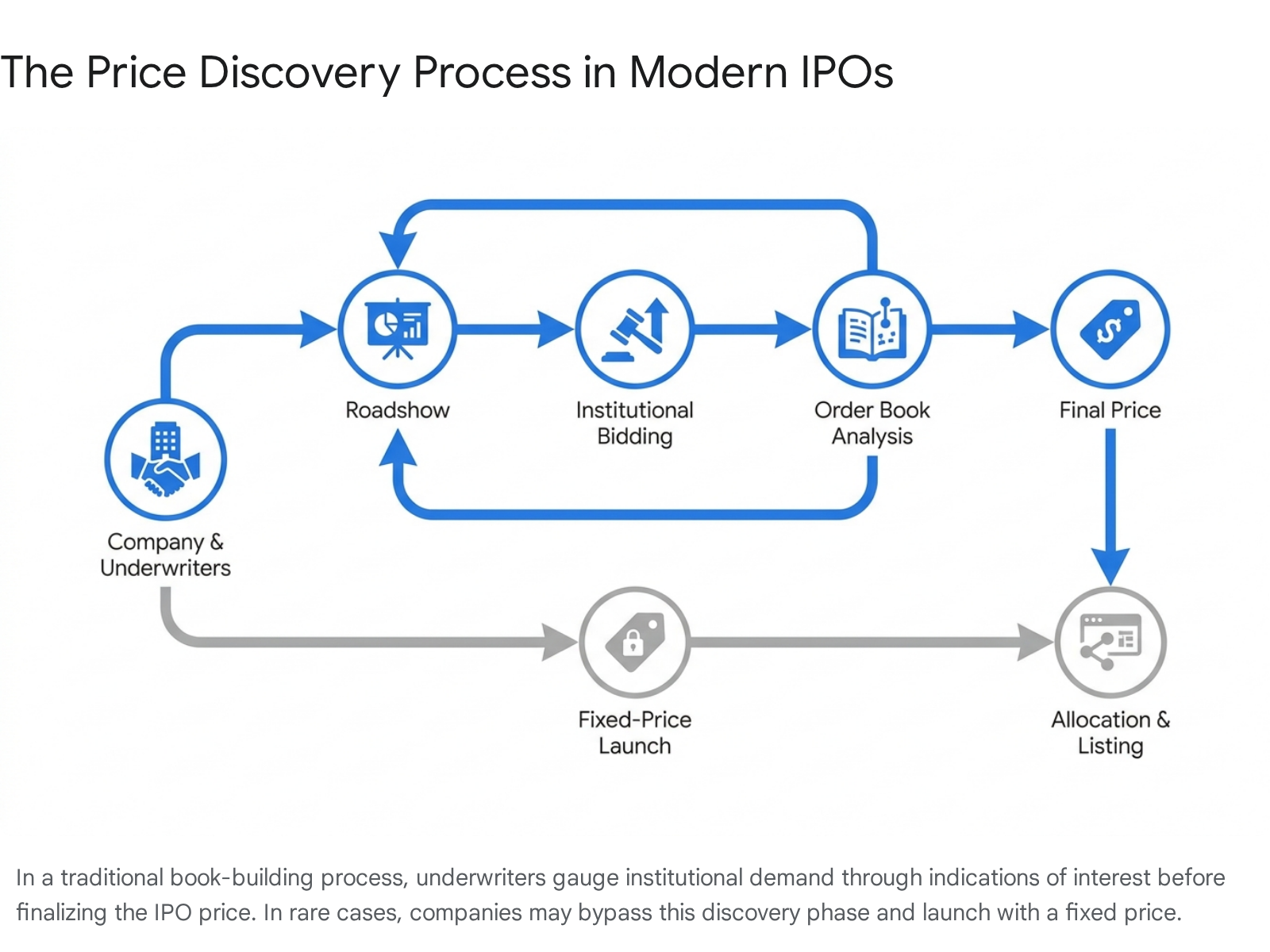

When a private corporation decides to transition into a publicly traded entity, it rarely establishes its own share price in isolation. Instead, the company hires underwriters - typically a syndicate of large investment banks like Goldman Sachs, Morgan Stanley, or J.P. Morgan - to manage the complex regulatory and financial transition 1234. The underwriters serve as the critical bridge between the issuing company and the investing public, and their primary mechanism for discovering the stock's market value is a highly structured process known as "book building" 123.

The Book-Building Process

To understand book building, it is helpful to contrast it with a fixed-price offering.

In a fixed-price model, a company simply dictates the price of its shares and hopes the broader market will purchase them at that exact valuation. Book building, which has become the preferred and standard method on almost all major global stock exchanges, is much more dynamic and relies on active price discovery 345.

The process begins with an IPO roadshow. Company executives and their lead underwriting bankers travel - both physically and virtually - to pitch the business to institutional investors, such as mutual funds, pension funds, hedge funds, and high-net-worth individuals 24. During these presentations, the underwriters present a preliminary price range based on the valuation of comparable public companies, the company's financial metrics, and broader macroeconomic conditions 245.

Following the pitch, institutional investors are invited to submit "indications of interest" (IOIs) or bids, detailing exactly how many shares they would be willing to purchase and at what specific price 123. These bids are strictly non-binding, but because of the reputational nature of the investment banking industry, institutions rarely renege on their stated interest 7.

The underwriters compile these bids into an order book. By analyzing the volume and price sensitivity of the incoming demand, the underwriters construct a real-time demand curve 12. If the order book is massively oversubscribed - meaning institutional investors want to buy substantially more shares than the company is offering - the underwriters will likely price the IPO at the top of the initial range or even revise the range upward 24. Conversely, weak demand may force the price to the bottom of the range. The final offer price, sometimes referred to as the "cut-off price," is ultimately a weighted average that balances the company's desire to raise maximum capital against the market's collective willingness to pay 23.

Allocating the Shares

Once the price is set, the underwriters must decide who actually receives the shares. Unlike a pure auction where the highest bidder automatically wins, book building allows underwriters massive discretion in allocating shares 956. They prioritize high-quality institutional investors who are perceived as long-term holders, rather than short-term speculators looking to "flip" the stock for a quick profit 612.

Typically, up to 90% of a major IPO is allocated to these institutional players, leaving a fraction - often just 10% - for the general public 131415. This intentional scarcity in the retail market sets the stage for the chaotic trading that typically unfolds on debut day.

The Economics of the First-Day Pop

One of the most persistent and globally documented phenomena in modern finance is that IPOs routinely "pop" on their first day of trading. This occurs when the stock opens on the secondary market (like the Nasdaq or the New York Stock Exchange) at a price significantly higher than the official IPO offer price paid by the initial institutional investors 912.

Historically, this has resulted in massive amounts of capital being "left on the table." Between 1990 and 1998 alone, public companies left an estimated $27 billion in potential capital uncollected because their shares were priced far below what the open market was willing to pay on day one 91617. During the dot-com bubble and the more recent post-pandemic bull market of 2020 and 2021, the average first-day pop routinely exceeded 30% to 40% 1718.

This raises a logical question: if the open market is willing to pay $50 a share, why would a company and its sophisticated investment bankers deliberately price the stock at $40? The answer lies in a complex mix of risk management, academic economic theory, and institutional psychology.

Intentional Risk Compensation

At a practical level, investment banks intentionally price IPOs roughly 10% to 20% below their estimated intrinsic value to create a built-in safety margin 1218. Going public is an inherently precarious event for a business. Without an active secondary market prior to the IPO, there is no absolute, undeniable benchmark for true investor demand 12.

Underpricing serves as a risk premium to compensate institutional investors for backing an unproven public entity. Furthermore, underwriters are highly incentivized to ensure the deal is a complete success. A "busted" or "broken" IPO - one that drops below its offering price on the first day - severely damages the underwriter's reputation and makes it exceedingly difficult for the bank to secure future corporate clients 1819. Banks would rather leave a little money on the table to guarantee full subscription and a positive media narrative than risk a disastrous, highly public failure 18.

The Winner's Curse and Information Asymmetry

Academic finance offers a more rigorous theoretical explanation for underpricing, famously articulated by economist Kevin Rock in 1986. Rock's model relies on the concepts of information asymmetry and the "Winner's Curse" 1619207823.

The theory divides the market into two distinct groups: informed institutional investors who have the resources to accurately assess the true value of a company, and uninformed retail investors who bid blindly based on hype 161923. Informed investors will only submit bids on IPOs that they know are attractively priced. If an IPO is overpriced, informed investors will withdraw their bids entirely.

Therefore, if an uninformed investor actually succeeds in receiving a large allocation of shares in an IPO, it is mathematically probable that they "won" the shares only because the informed investors stayed away. In this scenario, winning the allocation is actually a curse, because it means the stock is almost certainly overpriced 161923. To prevent uninformed investors from realizing they are being played and dropping out of the IPO market entirely, underwriters must systematically underprice all IPOs. This structural discount ensures that even when uninformed investors bid blindly, their expected returns remain positive on average, keeping them in the market to provide necessary liquidity 161923.

The Signaling Hypothesis

Another prominent academic theory, proposed by Allen and Faulhaber in 1989, is the signaling hypothesis. This framework suggests that underpricing is a deliberate strategic maneuver by high-quality firms 1624.

By leaving money on the table during the IPO, a company signals to the market that it has highly favorable future prospects. The logic dictates that only a truly strong, cash-generative company can afford to sacrifice immediate capital. The company knows it will easily recover the cost of this initial "signal" when it issues more shares in subsequent seasoned equity offerings (SEOs) at a much higher price 162425. Underpricing leaves a good taste in investors' mouths, fostering goodwill and paving the way for future, more lucrative fundraising rounds 16.

Underwriter Agency Conflicts

A more cynical explanation for underpricing revolves around underwriter agency conflicts. Investment banks are hired by the issuing company, but their primary, long-term clients are the institutional investors who buy the shares and pay lucrative trading commissions 192025.

By severely underpricing an IPO, underwriters can allocate guaranteed profits to their favored institutional clients. These mutual funds and hedge funds immediately benefit from the first-day pop. In return for these highly lucrative allocations, the institutions direct their ongoing, high-fee trading business to the underwriting bank 192025. While lawmakers and regulators have attempted to curtail these quid-pro-quo practices, the fundamental conflict of interest inherent in the book-building process continues to exert downward pressure on IPO pricing 25.

Market Mechanics: Supply Constraints and FOMO

Beyond academic theory, the raw mechanics of supply and demand on the trading floor heavily dictate the magnitude of the first-day pop. On the day a company goes public, the actual supply of shares available for public trading - known as the free float - is severely artificially constrained 1218.

Typically, companies only offer a tiny fraction of their total equity to the public during the IPO. Furthermore, the company's founders, executives, employees, and early venture capital backers are subjected to a lock-up period 121326. This regulatory restriction, usually lasting between 90 and 180 days, legally prohibits insiders from selling their shares on the open market 13269. This lock-up is designed to prevent the market from being suddenly flooded with supply, which would crash the stock price 2628.

Simultaneously, the institutional buyers who secured allocations during the initial book-building phase often acquire these shares for long-term holding, not immediate flipping 12. When the opening bell rings, this artificially limited supply collides with an overwhelming wave of demand from retail traders and unallocated hedge funds suffering from a fear of missing out (FOMO). Because the supply of available shares is so tight, buyers are forced to aggressively bid the price up to coax the few un-locked holders into selling 1218.

Recent Evidence: Blockbuster Tech Debuts

To illustrate how pricing strategies and market mechanics translate into real-world performance, we can examine the data from highly anticipated recent market debuts.

While the pop is a persistent feature of the market, its size varies wildly based on macroeconomic conditions, sector-specific hype, and the aggressiveness of the underwriters.

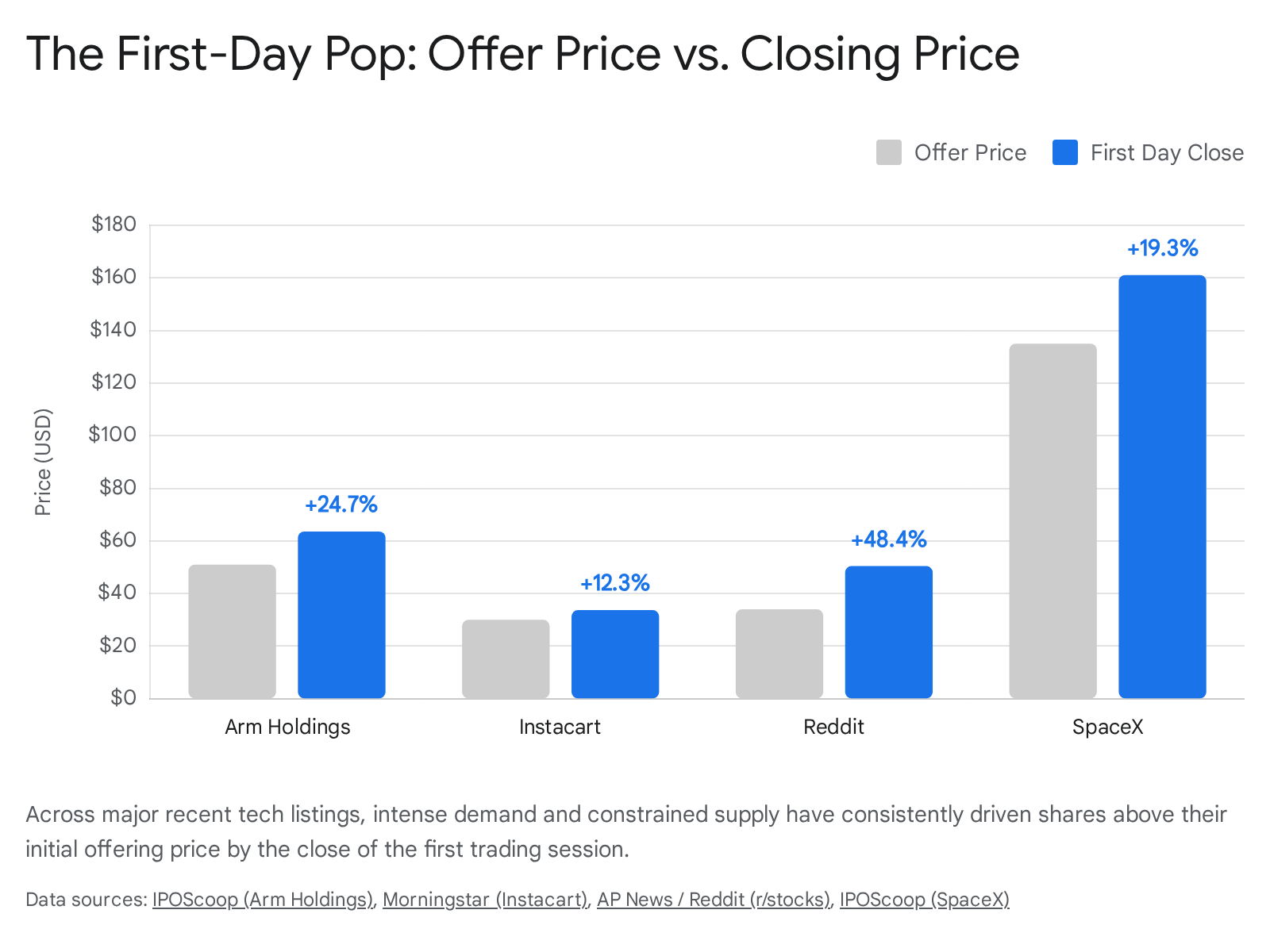

| Company | IPO Date | Offer Price | First Day Opening Trade | First Day Close | First Day Gain (Close) |

|---|---|---|---|---|---|

| Arm Holdings | Sept. 14, 2023 | $51.00 | $56.10 | $63.59 | +24.7% |

| Instacart | Sept. 19, 2023 | $30.00 | $42.00 | $33.70 | +12.3% |

| March 21, 2024 | $34.00 | $47.00 | $50.44 | +48.3% | |

| SpaceX | June 12, 2026 | $135.00 | $150.00 | $161.11 | +19.3% |

The September 2023 IPO of British chip designer Arm Holdings serves as a textbook example of a highly successful, heavily managed pop. Priced at $51 at the absolute high end of its expected filing range, the stock opened at $56.10 and surged nearly 25% to close at $63.59, valuing the SoftBank-backed company at over $65 billion on day one 2910311112. The pop successfully signaled strength in the semiconductor sector without leaving an egregious amount of money on the table 1012.

Conversely, grocery delivery application Instacart priced its shares at $30 just a few days later, achieving a valuation of roughly $10 billion 343536. This represented a massive haircut from its $39 billion private market valuation achieved during the pandemic 3536. While the stock initially opened strong at $42, it faced heavy selling pressure from investors recognizing the intense competition in the delivery sector, ultimately giving up most of those intraday gains to close its inaugural session up a much more modest 12.3% at $33.70 3436.

Social media platform Reddit tested the market in March 2024 following an extended dry spell for legacy tech listings. Despite the company's history of net losses, underwriters priced the offering at $34, the absolute top of the expected range 37383913. The stock opened at $47 and climbed as high as $57.80 in midday trading before closing at $50.44. This massive 48% premium signaled a strong return of risk appetite for growth companies and generated a substantial windfall for Reddit's early investors, including Condé Nast's parent company 373913.

The SpaceX Mega-IPO: Rewriting the Rulebook

The June 2026 initial public offering of Elon Musk's SpaceX - the largest IPO in global history - shattered many of the traditional conventions regarding how stock prices are set and who is permitted to buy them.

Raising $75 billion by selling roughly 555.6 million shares, the transaction assigned SpaceX an implied valuation of approximately $1.77 trillion, making it the seventh-largest U.S. company by market capitalization on its very first day of trading 4114434445. To achieve this unprecedented scale, SpaceX deliberately abandoned standard Wall Street practices 144615.

A Fixed Price and a Staggering Valuation

Historically, underwriters publish an indicative price range to gauge institutional demand during the pre-IPO roadshow. SpaceX bypassed this entirely, filing its paperwork with a fixed, take-it-or-leave-it price of $135 per share 14454648. This unusual structure completely removed the primary mechanism by which a company negotiates price discovery with institutions. By dictating a fixed price, SpaceX signaled immense confidence that market demand would violently outstrip supply regardless of conventional guardrails 44615.

The demand was indeed historic. Order books were reportedly four times oversubscribed, with total investor demand exceeding $250 billion by the time the books closed a day early on June 11 441454950. However, analysts cautioned that massive oversubscription at a fixed price does not guarantee infinite upside; institutions often artificially inflate their orders knowing their final allocations will be drastically cut back 4. Despite posting a $4.28 billion net loss in the first quarter of 2026 alone - largely driven by massive artificial intelligence infrastructure expenditures for its xAI integration - the stock opened at $150 and closed at $161.11, yielding a 19.34% first-day gain 41454951.

Retail Democratization and the Danger of Flipping

Perhaps the most disruptive element of the SpaceX IPO was its structural democratization. In a standard mega-cap US listing, retail investors are lucky to receive 5% to 10% of the allocated shares 154150. SpaceX actively subverted this norm by carving out an unprecedented 30% of its massive float - equating to roughly $22.5 billion - specifically for retail buyers through brokerages like Robinhood, SoFi, and Fidelity 154145461552.

While this allowed ordinary investors direct exposure to the commercial space economy, it carried severe risks for aftermarket volatility 15445354. Retail investors are statistically more prone to momentum trading, often chasing intraday highs and panic-selling on dips 15. To prevent mass retail selling from collapsing the stock on day one, brokerages enforcing the allocations implemented strict anti-flipping penalties. Firms like Fidelity warned customers that selling SpaceX shares within 15 days of the debut would result in a six-month suspension from participating in any future IPO allocations, while other brokers threatened permanent bans for repeat offenders 52. These aggressive measures highlight how heavily underwriters rely on a stable, locked-in shareholder base to support prices in the immediate aftermath of a listing.

Alternative Pathways to the Public Market

For companies that find the traditional book-building process too expensive, or who deeply resent leaving 20% of their valuation on the table for the sole benefit of Wall Street banks and institutional clients, alternative pathways to the public equity markets have emerged.

Direct Listings

A direct listing bypasses the underwriting, roadshow, and book-building process entirely. Existing shareholders - such as founders, early employees, and venture capitalists - simply list their current shares directly on a public exchange 52692855.

| Feature | Traditional IPO | Direct Listing |

|---|---|---|

| Capital Raised | Issues new shares to raise fresh capital for the company. | Does not traditionally raise new capital; only existing shares are sold. |

| Price Discovery | Set by underwriters based on institutional bids. | Determined solely by market supply and demand on the first trading day. |

| Underwriting Fees | High (typically 4% to 7% of gross proceeds). | Low (typically 0.5% to 1% in advisory fees). |

| Lock-Up Period | Strict 90-to-180 day lock-up for insiders. | No lock-up period; insiders can sell immediately. |

Note: Comparisons derived from standard market mechanisms 26928555616.

Because no new shares are issued, the company does not raise any fresh capital during a traditional direct listing 2695516. The opening price is completely dictated by raw supply and demand at the opening bell, functioning much like an unrestricted market auction 26916. This route eliminates hefty underwriting fees, avoids the dilutive effects of issuing new equity, and crucially, removes the standard lock-up period, allowing early employees to achieve immediate liquidity 2692855. Tech companies with massive existing brand awareness and strong balance sheets, such as Spotify, Slack, and Coinbase, successfully pioneered this route 2655.

However, direct listings carry immense risk. Without an underwriter to artificially support the price through stabilization mechanisms, or a book-building process to precisely gauge demand, the opening days of trading can be violently volatile 2628555616. In the 2024 - 2026 market cycle, direct listings have largely been relegated to smaller micro-cap companies, many of which displayed extreme first-day price instability due to the lack of institutional sponsorship 17. Consequently, many large-cap companies continue to choose traditional IPOs simply for the structured price stability and the guaranteed capital infusion they provide 165960.

Open Auctions

Another theoretical alternative is the open auction model, specifically uniform price "dirty" auctions. Instead of investment banks selecting favored clients to receive shares, an open auction allows all investors - retail and institutional alike - to submit sealed bids indicating the price and quantity they desire. The shares are then allocated to the highest bidders until the offering is filled.

Academics have long argued that open auctions result in more accurate pricing, significantly less underpricing, and consequently, more capital raised for the issuing company 562518. Despite this mathematical superiority, auctions have struggled to supplant traditional book building globally. Underwriters argue that the implicit rules and relationships of book building give them the necessary control to manage risk, ensure the stock lands in the hands of stable long-term holders, and curate a smooth, predictable transition to the public market 5618.

Global Perspectives on IPO Pricing

The mechanics of IPO pricing and aftermarket trading are not uniform globally; intense regulatory interventions play a massive role in shaping how stocks behave on their first day across different sovereign jurisdictions.

In the United States and Europe, the open market determines the ultimate ceiling of a first-day pop. In China, however, regulators impose strict mathematical boundaries to tame speculative fervor and artificially maintain market order. For A-share IPOs listed on the Shanghai and Shenzhen stock exchanges, the government introduced measures in 2015 that strictly cap first-day gains at exactly 44% above the initial offer price 62.

This artificial ceiling fundamentally alters market psychology. Because organic demand typically vastly exceeds this 44% cap, Chinese A-share IPOs are often viewed by domestic investors as guaranteed "sure win" lottery tickets 62. Bloomberg data from 2017 showed that all 432 initial public offerings that year hit the exact 44% maximum limit on their first day of trading 62. Following the debut, secondary market daily price swings are further restricted to 10% in either direction. This regulatory friction often results in newly listed stocks riding a continuous, uninterrupted upward trend for weeks as the pent-up demand slowly unwinds within the government's guardrails 62. Japan utilizes a similar mechanism, setting daily price limits in absolute yen amounts to curb extreme single-day fluctuations 63.

Exchanges also differ radically in their approach to retail participation. While the US market is heavily skewed toward institutions, markets in India and Hong Kong mandate retail inclusion. In Hong Kong, an IPO typically requires a clawback mechanism: while 10% of shares are initially allocated to the public, if retail demand is more than 100 times oversubscribed, shares are automatically clawed back from institutional investors until the retail allocation reaches 50% 13. Similarly, the Securities and Exchange Board of India (SEBI) mandates that specific portions of an IPO be strictly reserved for different investor classes, requiring that at least 35% of the net offer be set aside exclusively for retail investors 14.

In Brazil, the B3 exchange has seen a massive structural shift. Historically, exceptionally high local interest rates (often averaging over 10%) meant Brazilian retail investors safely parked their cash in fixed-income assets, resulting in less than 1% of the population investing in equities 19. However, as the central bank has aggressively cut rates to stimulate the economy, a massive pool of retail savings has flooded into the Brazilian equity market, entirely changing the demand dynamics for local stock offerings 19.

The Long-Term Reality: Do Pops Last?

While the first-day pop dominates headlines and enriches early insiders, long-term post-IPO performance tells a much more sobering story. Extensive academic research spearheaded by economists like Tim Loughran and Jay Ritter has consistently demonstrated a glaring anomaly: while IPOs wildly out-perform the market in the short run, they routinely underperform broader market benchmarks over a three-to-five-year horizon 17202122.

The reasons for this mean reversion are multifaceted. Initial market euphoria eventually fades, forcing the company to trade on fundamental earnings rather than future promises. Furthermore, as the 180-day lock-up periods inevitably expire, a massive wave of insider shares hits the open market, drastically increasing supply and depressing the stock price 26. Finally, the "Winner's Curse" asserts itself: the retail investors who eagerly bought at the top of the day-one pop often find themselves holding the bag as institutional money quietly rotates out of the stock to chase the next lucrative IPO allocation 19236869.

Bottom line

IPO prices are intentionally engineered by investment banks to be lower than their true market value. This deliberate underpricing ensures a successful offering, compensates early investors for taking on risk, and triggers a wave of positive media publicity. The resulting first-day "pop" is a structural feature of modern finance, born from the collision of heavily discounted pricing, artificially locked-up shares, and intense public FOMO. While new mechanisms like direct listings and fixed-price mega-offerings challenge this status quo, the fundamental tension between a company desiring maximum capital and a market demanding a built-in discount remains the driving force behind every public debut.