What Is Prospect Theory and How Does It Work

Prospect theory explains that human beings make decisions based on perceived, relative gains and losses rather than absolute changes to their overall wealth. It demonstrates that the psychological pain of losing something is experienced much more intensely than the pleasure of gaining something of equal value, a phenomenon known as loss aversion. By mapping how our brains systematically distort probabilities and recoil from risk, this behavioral framework reveals why we often make seemingly irrational choices in finance, medicine, and everyday life.

The Origins of Prospect Theory

For the first half of the twentieth century, the study of decision-making under risk was dominated by expected utility theory, developed by John von Neumann and Oskar Morgenstern in 1944 12. This classical economic model assumed that humans operate as perfectly rational agents. According to expected utility theory, individuals carefully calculate the mathematical probabilities of all potential outcomes and make choices that strictly maximize their final asset position 13.

However, real-world observation consistently proved that humans are far from perfect calculating machines. People routinely buy lottery tickets with negative expected values, overpay for insurance on minor items, and make contradictory choices depending on how a question is worded. In response to these behavioral anomalies, psychologists Daniel Kahneman and Amos Tversky published a groundbreaking paper in the journal Econometrica in 1979 titled "Prospect Theory: An Analysis of Decision Under Risk" 14.

Based on a series of controlled experiments involving lotteries and financial gambles, Kahneman and Tversky demonstrated systematic, predictable deviations from expected utility 3. Their descriptive model fundamentally challenged classical economics, effectively establishing the field of behavioral economics and eventually earning Kahneman the 2002 Nobel Memorial Prize in Economic Sciences 14. Tversky had passed away before the prize was awarded 4. The theory was later refined in 1992 into cumulative prospect theory, which accommodated more complex decisions with multiple uncertain outcomes 12.

According to the theory, human decision-making processes unfold in two distinct cognitive stages 15: 1. The Editing Phase: When confronted with a complex choice, individuals organize, simplify, and reformulate the available options. During this phase, people set a cognitive baseline or "reference point" and frame the potential outcomes as either gains or losses relative to that starting position. The editing phase relies heavily on mental shortcuts (heuristics) and frequently leads to the isolation effect, where people ignore components that are shared across all options and focus only on what distinguishes them 36. 2. The Evaluation Phase: Once the options are simplified, individuals compute a subjective value for each alternative. This computation is based on the potential outcomes (gains or losses) and a distorted weighting of their respective probabilities. The individual ultimately chooses the alternative that yields the highest subjective psychological utility 18.

The Core Mechanics of Choice

Prospect theory rests on a foundation of three distinct psychological mechanisms that govern how our brains evaluate outcomes: reference dependence, diminishing sensitivity, and loss aversion.

Reference Dependence

Classical economics assumes that people evaluate a financial choice based on how it impacts their absolute wealth. Prospect theory argues that we evaluate choices relative to a specific reference point, which is usually our current status quo or an expected baseline 14.

Consider a game of Monopoly. If you draw a chance card that forces you to pay $100, the psychological sting is tied entirely to the act of losing the money, regardless of whether you already have $500 or $5,000 in your pile 6. This concept scales to real-world finance. If an investor buys a stock at $100 and it drops to $90, they experience a painful loss. However, an investor who bought the exact same stock at $80 and watches it rise to $90 experiences joy. They both possess an identical asset worth $90, but their emotional reactions are opposites because their reference points differ 4. Furthermore, as researchers Kőszegi and Rabin noted in 2007, reference points are not always fixed to current wealth; they can be heavily influenced by future expectations and environmental context 1.

Diminishing Sensitivity

The second pillar of prospect theory is diminishing sensitivity, meaning that human beings become progressively less sensitive to changes in outcomes the further those outcomes move away from the reference point 49.

If you find $10 in the pocket of an old jacket, you experience a noticeable burst of happiness. However, if you already have $1,000 in cash in your wallet and you add another $10, the emotional impact of that extra $10 is virtually nonexistent 4. The same applies to the domain of losses. The psychological difference between losing $10 and losing $20 feels vast, but the difference between losing $1,110 and losing $1,120 feels negligible, even though the objective financial change is identical in all scenarios 4.

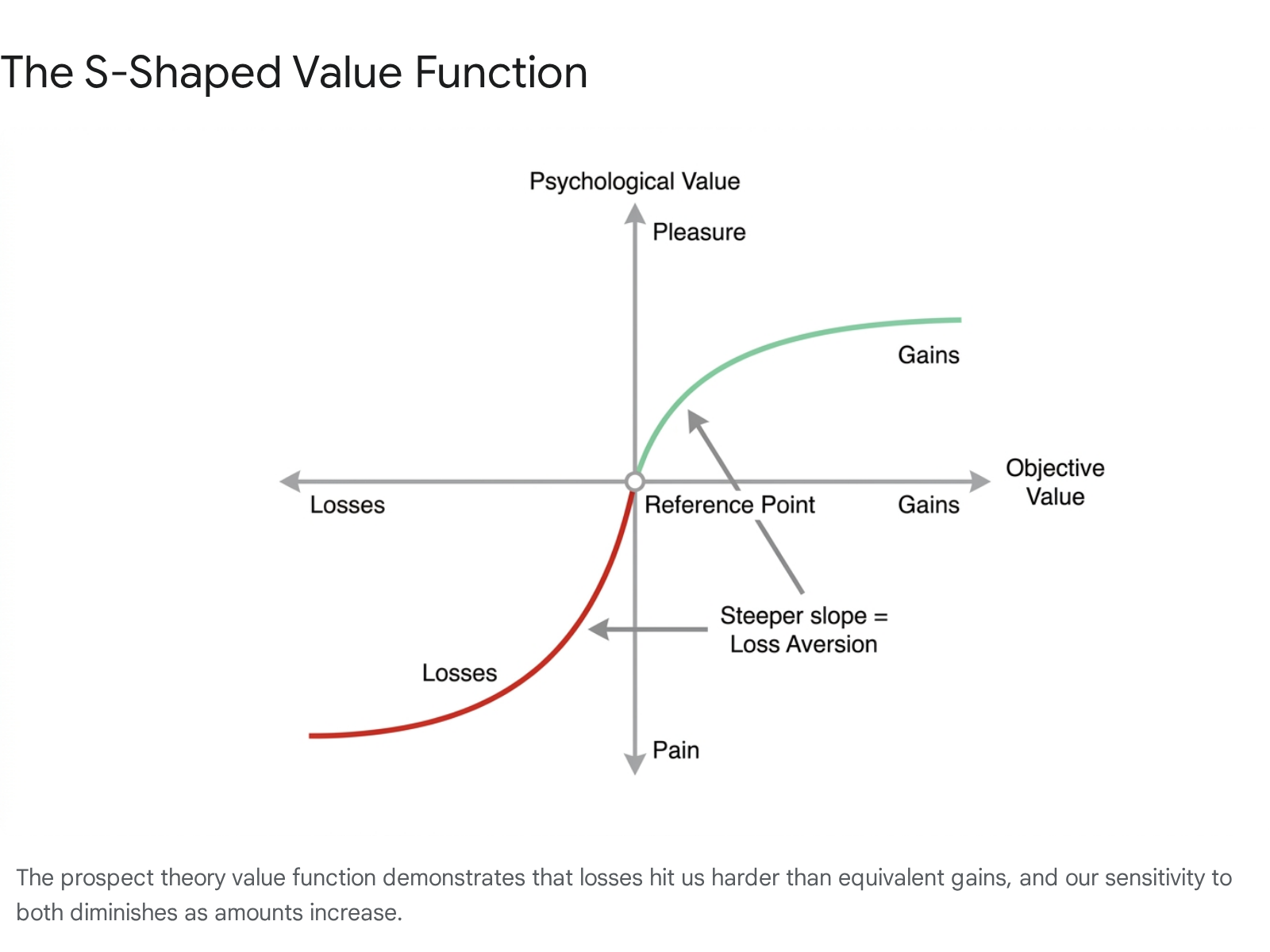

Loss Aversion and the Value Function

The most famous concept to emerge from prospect theory is loss aversion. This principle asserts that the psychological pain associated with a loss is experienced much more intensely than the pleasure derived from an equivalent gain 189. As Kahneman famously summarized, "losses loom larger than gains."

This psychological dynamic is visually mapped on a graph known as the value function, which takes the shape of an asymmetrical S-curve 19.

The value function curve features three distinct mathematical traits 19: * Reference point at the origin: The curve intersects at zero, highlighting that gains and losses are judged exclusively relative to the status quo. * Concave for gains, convex for losses: This curvature visually represents diminishing sensitivity. The line flattens out as values increase in either direction. * A steeper slope for losses: The angle of the curve drops much more sharply in the lower-left domain of losses than it rises in the upper-right domain of gains. In practical terms, this steeper slope visualizes why losing $100 "hurts" more than winning $100 "feels good" 9.

The Probability Weighting Function

Beyond how we value money or outcomes, prospect theory also revolutionized our understanding of how humans distort math. Under classical expected utility theory, a person evaluates an outcome by multiplying its value by its exact probability. However, prospect theory introduced a probability weighting function, proving that humans subjectively distort odds 67.

Humans generally struggle to comprehend and act upon absolute probabilities, leading to predictable cognitive errors at the extremes of the probability scale: * The Certainty Effect: We severely underweight events with high probabilities. Given the choice, humans strongly prefer a 100% guaranteed gain over a 95% chance of a slightly larger gain, even if the latter has a higher mathematical expected value 34. * The Possibility Effect: We drastically overweight events with tiny, near-zero probabilities 156.

This distortion explains an enormous amount of consumer behavior. It clarifies why people enthusiastically buy lottery tickets, overweighting a minuscule chance of a massive windfall, and why they happily purchase extended warranties on household appliances, overweighting a tiny chance of a total loss 5711. In both scenarios, humans are paying a premium for psychological comfort rather than mathematical utility.

Interestingly, behavioral economists highlight a phenomenon known as the description-experience gap 7. When probabilities are explicitly described to a person (e.g., "you have a 5% chance to win"), they tend to overweight that small probability. However, when people have to learn the probabilities through direct experience - such as pulling a slot machine lever repeatedly without knowing the odds - their perception of risk changes, and they often react differently to those same probabilities 7.

The Four-Fold Pattern of Risk

When the asymmetrical S-shaped value function is combined with the probability weighting function, it results in what Kahneman and Tversky termed the "four-fold pattern" of decision-making 6. This framework reliably predicts when people will act risk-averse and when they will suddenly become risk-seeking.

| Probability Scenario | Domain of Gains | Domain of Losses |

|---|---|---|

| High Probability (Certainty Effect) |

Risk-Averse: People prefer a guaranteed small gain over a gamble for a slightly larger gain. (e.g., Accepting a slightly lower, but guaranteed, settlement in court rather than risking a trial). 6 |

Risk-Seeking: People will take desperate gambles to avoid a guaranteed loss. (e.g., Pouring more money into a failing business or doubling down on a bad bet to "break even"). 612 |

| Low Probability (Possibility Effect) |

Risk-Seeking: People overweight a tiny chance of a massive windfall. (e.g., Buying lottery tickets or highly speculative penny stocks). 67 |

Risk-Averse: People will pay a premium to eliminate a tiny risk of a catastrophic loss. (e.g., Buying comprehensive insurance against rare natural disasters). 612 |

A classic demonstration of this risk reversal is Kahneman and Tversky's famous "Asian disease" experiment 513. Participants were asked to choose between two public health interventions for a disease expected to kill 600 people. When the options were framed positively (e.g., "Program A will save 200 people with certainty"), participants overwhelmingly chose the risk-averse, certain option. When the exact same mathematical outcomes were framed negatively (e.g., "Program C guarantees 400 people will die"), participants suddenly became risk-seeking, preferring a gamble that offered a one-third chance that no one would die, despite the two-thirds chance that all 600 would die 513.

The Global Evidence: Does the Theory Replicate?

Decades after its publication, prospect theory remains one of the most cited frameworks in economics and psychology 815. However, in an era where the behavioral sciences have faced a widespread replication crisis, researchers have rigorously re-tested its core tenets across diverse global populations and modern datasets to see if it holds up 16.

Cross-Cultural Validity

In 2020, an extensive global study led by Kai Ruggeri at Columbia University tested the original Kahneman and Tversky propositions on a massive scale. Across 19 countries, 13 languages, and over 4,000 participants, the researchers successfully replicated 94% of the original items and 12 out of 13 theoretical contrasts 1516. The study confirmed that the bedrock principles of prospect theory - loss aversion, the reflection effect, and framing effects - are highly robust and exist far beyond the original 1970s cohort of Western university students 179.

However, modern research highlights that while the architecture of prospect theory is universal, the magnitude of these biases varies across cultures. Studies mapping prospect theory against cultural dimensions show that societies scoring high in individualism tend to exhibit more severe loss aversion than collectivist cultures 10. In collectivist societies, robust social safety nets, high family cohesion, and communal support structures inherently mitigate the catastrophic perception of individual financial loss, dampening the loss aversion curve 10.

For example, an early cross-cultural study comparing university students found that Ecuadorean participants exhibited significantly lower loss aversion in risky choices compared to Slovakian students, indicating that cultural perception of risk alters decision models 11. Similarly, researchers have found that certain populations in Singapore and China display less risk aversion in loss frames compared to Western counterparts in the Netherlands and New Zealand 6.

The Great Loss Aversion Debate (2024 - 2025)

While the existence of prospect theory is undisputed, the exact mathematical intensity of loss aversion became the subject of intense academic debate between 2024 and 2025. Tversky and Kahneman's 1992 parameterization estimated the loss aversion coefficient (denoted as lambda, or λ) at roughly 2.25, meaning losses hurt 2.25 times as much as equivalent gains 12.

However, recent large-scale meta-analyses have significantly walked back this number, arguing that the original figure was inflated by specific experimental designs:

| Meta-Analysis / Study | Scope of Study | Estimated Loss Aversion (Lambda) |

|---|---|---|

| Tversky & Kahneman (1992) | Original baseline study establishing cumulative prospect theory parameters. 12 | 2.25 |

| Brown et al. (2024) | Examined 607 empirical estimates from 150 articles across economics and psychology. 13 | 1.95 |

| Walasek et al. (2024) | Meta-analysis specifically isolating individual choices between mixed risky gambles. 1214 | 1.31 |

| Yechiam & Zeif (2025) | Re-meta-analysis isolating studies with perfectly symmetrical gains and losses. 2615 | 1.07 (Near Neutral) |

The 2025 re-meta-analysis by Yechiam and Zeif is particularly revealing. They discovered that when researchers present participants with completely symmetrical gains and losses (e.g., flipping a coin to win $50 or lose $50) in randomized orders, the loss aversion coefficient drops to 1.07, meaning participants weigh gains and losses almost equally 2615. The researchers argue that historical findings of strong loss aversion were largely replicated only when studies intentionally used asymmetrical designs where potential gains were much larger than potential losses, or when items were presented in ascending order 2615.

This evolving research does not invalidate prospect theory. Rather, it highlights that human bias is highly contextual. If the stakes are massive, the environment is stressful, or the cognitive load is high, loss aversion spikes 1516. In low-stakes, perfectly symmetric lab environments, humans behave far more rationally than previously thought 15.

Applications in Behavioral Finance

The true power of prospect theory lies in its application outside the laboratory. In retail investing and wealth management, prospect theory manifests prominently through the disposition effect 1718.

The disposition effect is the documented behavioral tendency for investors to sell winning assets far too early while holding onto losing assets far too long 1718. Under classical economics, an investor evaluates a stock based on its future earning potential. Under prospect theory, an investor evaluates a stock based on a mental reference point - usually the initial purchase price 18.

If an investor buys a stock and it rises by 10%, they enter the "domain of gains." According to the four-fold pattern, people facing a high-probability gain become risk-averse. The investor will eagerly sell the stock prematurely to lock in a guaranteed psychological victory and avoid the regret of watching the stock drop 1831. Conversely, if a stock falls by 15%, the investor enters the "domain of losses." Driven by the intense pain of loss aversion, the investor becomes dangerously risk-seeking, refusing to sell the asset and "realize" the loss. They hold the position, hoping desperately that it will bounce back, a detrimental behavior often referred to as "get-even-itis" 617. This behavior routinely damages long-term portfolio returns 31.

Furthermore, research indicates that the disposition effect is actually cyclical. A 2020 study by Bernard, Loos, and Weber found that the disposition effect moves countercyclically to the broader stock market - it is low in boom periods but spikes dramatically in market bust periods. As anxiety and risk aversion rise during downturns, investors are even more likely to impulsively lock in minor gains to secure a win 32.

This behavior is closely related to myopic loss aversion, a concept highlighting the human tendency to hyper-focus on short-term market fluctuations rather than long-term gains 1. Because losses loom larger than gains, checking a stock portfolio daily exposes the investor to frequent psychological pain, often prompting irrational, risk-reducing trades that harm long-term wealth 1.

Applications in Healthcare and Medicine

Prospect theory heavily influences medical decision-making, impacting how physicians establish clinical guidelines and how patients choose treatments 1920. The theory's framing effect demonstrates that the presentation of medical statistics entirely changes patient behavior.

| Framing Strategy | Description | Example in Healthcare |

|---|---|---|

| Attribute Framing | Highlighting a positive or negative characteristic of an object or choice. 3521 | Describing a surgery as having a "90% survival rate" (positive) vs. a "10% mortality rate" (negative). 22 |

| Goal Framing | Emphasizing the positive consequences of an action, or the negative consequences of avoiding it. 3521 | "Taking this medication will help you maintain your mobility" (gain) vs. "If you don't take this medication, you will lose your mobility" (loss). 6 |

For example, when considering a high-risk surgical procedure, patients are overwhelmingly more likely to consent if a doctor uses attribute framing to state the procedure has a "90% survival rate" rather than a "10% mortality rate" 2238. The mathematical probability is identical, but the negative frame of mortality triggers loss aversion, causing the patient to retreat toward risk-averse, non-surgical options.

During the COVID-19 pandemic, public health officials utilized prospect theory to navigate risk perception. Gain-framed messaging (e.g., highlighting the benefits of handwashing and healthy habits) was largely effective for promoting low-risk, preventative behaviors 2324. However, loss-framed messaging (e.g., highlighting the number of lives that will be lost without social distancing) proved highly effective in breaking complacency and urging populations to comply with high-friction, immediate mandates 2324.

Behavioral science is also used in health policy architecture. A seminal 2003 study by Johnson and Goldstein demonstrated that organ donation rates skyrocket when countries make donation the default option, requiring citizens to "opt out" rather than "opt in" 25. This harnesses both the status quo bias and loss aversion, as the effort of changing the default feels like a psychological hurdle. The same logic is increasingly applied to digital health technology adoption; hospital executives are more likely to adopt new software if the pitch emphasizes avoiding a $100 million loss to inefficiency rather than gaining a $100 million profit 26.

Framing Effects in Retail and Negotiation

In business negotiations and everyday shopping, manipulating reference points and framing is a standard, highly effective tactic.

Grocery Shopping and Consumer Framing

Marketers consistently use reference dependence to trigger purchases. A retail price tag that simply reads "$450" is far less appealing than a tag that reads "Original Price: $500, You Save $50" 38. The $500 sets an artificial reference point, turning the purchase from an absolute loss of $450 into a relative psychological "gain" of $50.

Supermarkets use attribute framing constantly on packaging. A consumer is much more likely to purchase a yogurt labeled "80% fat-free" than one labeled "contains 20% fat," despite the nutritional content being identical 2122. Similarly, a buyer will favor a disinfectant wipe that "kills 95% of germs" over one where "5% of germs survive," simply because the brain recoils from the negative survival frame 21. Scarcity tactics, such as hotel booking sites flashing "Only 2 rooms left at this price!", weaponize loss aversion, making the consumer fear the loss of an opportunity more than they scrutinize the actual cost of the purchase 643.

Strategic Negotiations

When negotiating a car purchase or a corporate contract, anchoring bias and loss framing are powerful levers. For example, rather than a software vendor saying, "Our product will increase your efficiency by 15%," a skilled negotiator will frame it as, "Without this tool, your current downtime is costing you $100,000 a quarter" 27. By shifting the baseline, the counterpart is placed into the domain of losses, instigating a sense of urgency to close the deal 2728.

In car buying, salespeople frequently use payment framing, drawing the buyer's attention to an affordable monthly payment rather than the absolute out-the-door cost of the vehicle 4346. They may also employ the contrast effect by showing a buyer a heavily overpriced, less desirable car before showing them the target car, making the second car appear as a massive bargain by comparison 4329. To counter this, experts advise rigorously defining absolute out-the-door costs before entering a dealership, refusing to allow the seller to dictate the initial reference point 4346.

Overcoming Our Biases: The Interpersonal Shift

Recognizing these cognitive traps is the first step toward better decision-making. While it is difficult to completely rewire our emotional responses to loss and probability, behavioral science offers a robust mitigation strategy: the interpersonal shift.

One of the most fascinating recent discoveries in behavioral economics is that prospect theory's biases are largely confined to personal decision-making. When individuals make decisions on behalf of others, the famous four-fold pattern flattens, and loss aversion is severely diminished 64830.

In a comprehensive suite of studies by researchers Evan Polman, Qingzhou Sun, and Huanren Zhang, data revealed that people process risk far more rationally when managing someone else's money or medical choices 63031. The researchers attributed this transformation to a unique signature in interpersonal emotions. Because the visceral emotional sting of a loss is removed when the stakes belong to a friend, child, or client, the interpersonal decision-maker evaluates probabilities more linearly, free from the distortions of fear and hope that plague self-directed choices 48.

For individuals looking to protect their finances and well-being, experts recommend several tactics to sidestep prospect theory traps: * The "Friend" Test: Before making a major financial or medical decision, ask yourself what advice you would give to a close friend facing the exact same scenario. This simple psychological distance neutralizes loss aversion and brings you closer to rational, expected-utility thinking 6. * Change the Frame: Force yourself to restate any proposition in the opposite terms. If an investment emphasizes an 80% chance of a payout, actively write down that it carries a 1-in-5 chance of total failure 2251. * Focus on Absolute Utility: Discard artificial reference points like "original retail price" or "the price I bought this stock at." Ask yourself: "Given my total current wealth, does this transaction make objective sense?" 6.

Bottom line

Prospect theory fundamentally reshaped economics by proving that humans do not evaluate decisions based on rational wealth maximization, but rather through a psychological lens of relative gains and losses. We predictably overweight tiny probabilities, cling to artificial reference points, and suffer the pain of losses far more intensely than we enjoy equivalent gains. While recent research suggests the extreme magnitude of our loss aversion can be mitigated by careful framing, symmetrical environments, and social context, understanding these cognitive distortions remains the most reliable way to navigate investments, medical choices, and daily consumer traps.