The disposition effect in trading

The disposition effect constitutes one of the most rigorously documented behavioral anomalies within modern financial markets. Defined as the systematic propensity of investors to realize profitable investments prematurely while holding onto losing investments for extended periods, the phenomenon directly contradicts the foundational axioms of classical expected utility theory and the efficient market hypothesis. The terminology was formalized in the academic literature by Hersh Shefrin and Meir Statman in 1985, who built upon earlier observations by Gary Schlarbaum, Wilbur Lewellen, and Ronald Lease regarding the distinct possibility that individual investor trading patterns were driven by psychological biases rather than strict economic rationalism 12.

Despite decades of investor education, the democratization of financial data, and the proliferation of sophisticated algorithmic trading infrastructure, the disposition effect persists across diverse asset classes, geographical regions, and investor demographics. It creates a structural drag on individual portfolio performance, severely costing the average retail investor in long-term returns, while simultaneously generating broader macroeconomic distortions, including market momentum, delayed price discovery, and post-earnings announcement drift 132.

This comprehensive research article provides an exhaustive analysis of the disposition effect. It explores the psychological frameworks and mathematical utility models that govern the bias, evaluates competing rational counter-explanations, maps the divergence in behavioral execution between human and algorithmic traders, and examines how modern digital interfaces - such as gamified brokerages and social trading environments - are fundamentally altering the architecture of reference-dependent financial decision-making.

The Methodological Framework of Measurement

To transition the disposition effect from a theoretical behavioral concept to an empirically testable metric, the finance literature universally relies on the analytical methodology developed by Terrance Odean in his seminal 1998 study of discount brokerage accounts 1. Prior to this standardization, researchers struggled to measure the effect accurately, as simply counting the absolute number of winning trades sold versus losing trades sold is insufficient; an investor might naturally sell more winners simply during a sustained bull market where the underlying portfolio contains a higher absolute volume of profitable positions 13.

The Calculus of Realization Ratios

Odean established a ratio-based methodology that compares the frequency of asset realization against the base probability or opportunity for realization. The framework relies on tracking the daily status of every asset in a portfolio relative to its initial purchase price. The core metrics are defined as the Proportion of Gains Realized (PGR) and the Proportion of Losses Realized (PLR).

| Metric | Mathematical Definition | Economic Interpretation |

|---|---|---|

| Proportion of Gains Realized (PGR) | $\frac{\text{Realized Gains}}{\text{Realized Gains} + \text{Paper Gains}}$ | The rate at which an investor chooses to liquidate a position when the opportunity to capture a profit exists. |

| Proportion of Losses Realized (PLR) | $\frac{\text{Realized Losses}}{\text{Realized Losses} + \text{Paper Losses}}$ | The rate at which an investor chooses to liquidate a position when facing a deficit relative to the purchase price. |

| Disposition Spread | $\text{PGR} - \text{PLR}$ | The absolute magnitude of the disposition effect. A positive spread indicates the presence of the behavioral bias. |

| Disposition Ratio | $\frac{\text{PGR}}{\text{PLR}}$ | The relative multiplier of realization frequency. A ratio greater than 1.0 confirms the disposition effect. |

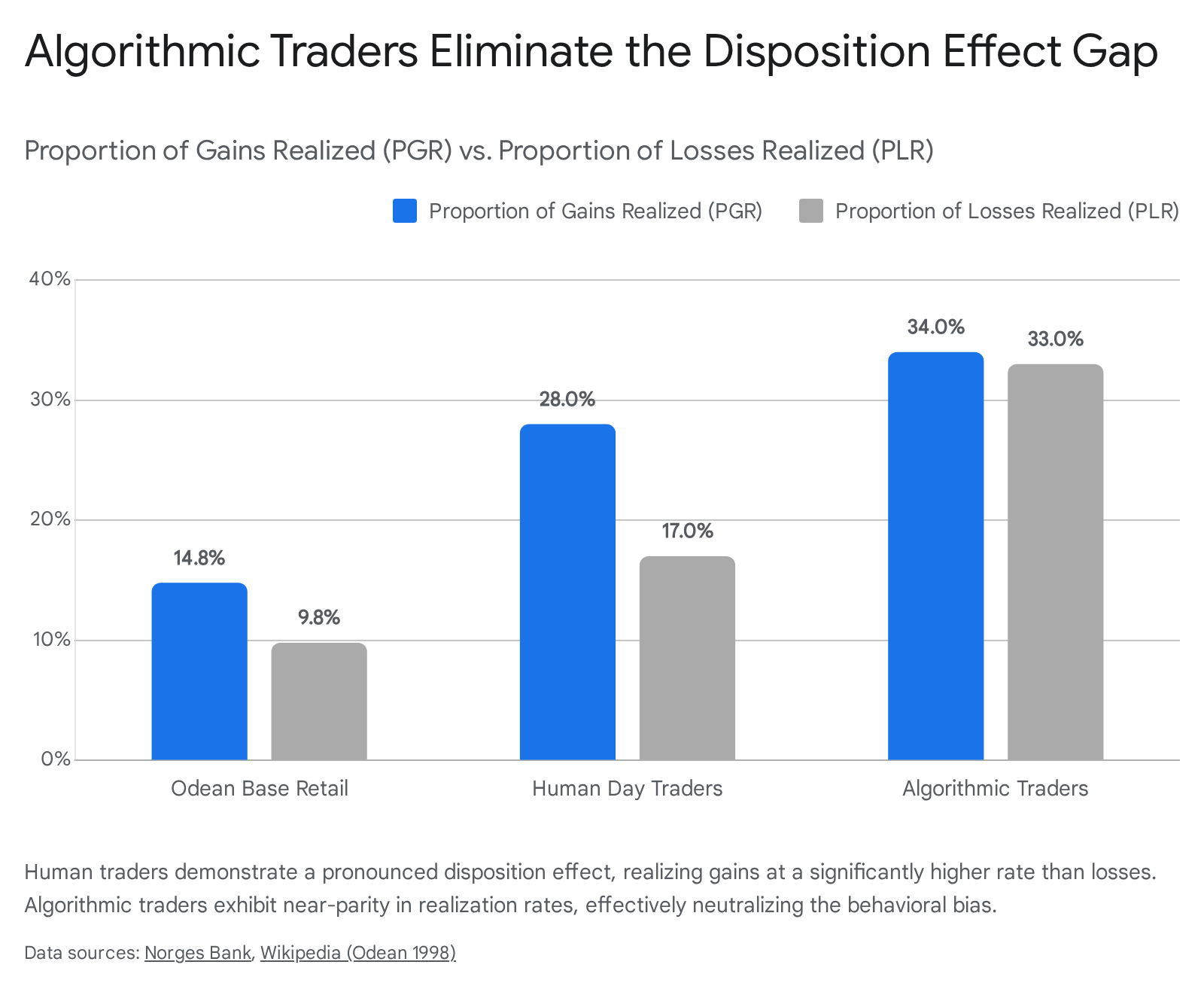

The disposition effect is empirically confirmed when an investor or a market aggregate demonstrates a PGR that is statistically significantly greater than the PLR. In his original dataset, covering 10,000 customer accounts from January 1987 through December 1993, Odean observed an average PGR of 14.8% and an average PLR of 9.8% outside of the month of December 14. This established the baseline empirical fact that retail investors were approximately 50% more likely to close a winning position than a losing one, providing irrefutable statistical evidence of the psychological bias operating at scale 14.

Theoretical and Psychological Foundations

The academic consensus regarding the origins of the disposition effect relies heavily on the integration of cognitive psychology into financial economics. While neoclassical models assume that economic agents make continuous decisions based entirely on the mathematical expectation of future terminal wealth, behavioral models recognize that humans process financial data subjectively. These subjective evaluations are heavily influenced by historical reference points, emotional states, and cognitive dissonance.

Prospect Theory and the Value Function

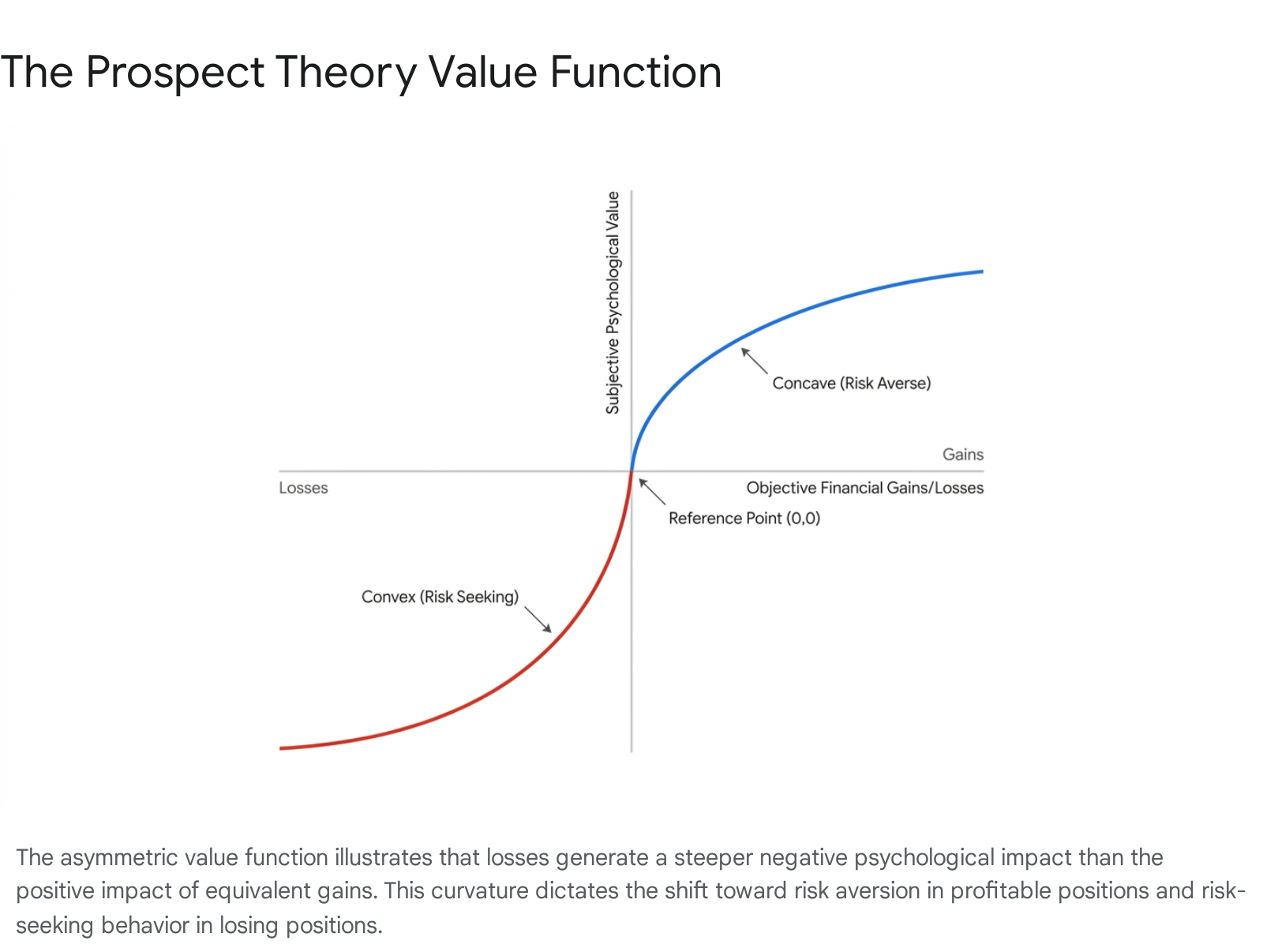

The primary theoretical mechanism utilized to explain the disposition effect is Prospect Theory, developed by psychologists Daniel Kahneman and Amos Tversky in 1979, for which Kahneman later received the Nobel Prize in Economics 58. Expected utility theory acts as a normative framework, describing how entirely rational actors should behave to maximize absolute wealth. In contrast, Prospect Theory operates as a descriptive framework, detailing how human beings actually evaluate risk and reward in real-world environments characterized by uncertainty 89.

Prospect Theory replaces the concept of absolute wealth evaluation with reference-dependent evaluation. Investors do not evaluate a stock based on its current contribution to their total net worth; instead, they measure it distinctly as a gain or a loss relative to a specific reference point, which in traditional financial contexts is the initial purchase price of the asset 58.

The theory is predicated on a distinct, S-shaped value function characterized by three core properties: 1. Reference Dependence: Financial outcomes are strictly coded as discrete gains or losses relative to the established starting point, completely decoupling the psychological evaluation from overall portfolio wealth. 2. Loss Aversion: The psychological pain experienced from losing capital is significantly more acute than the pleasure derived from gaining an equivalent amount. Empirical estimations from behavioral economics suggest a loss aversion coefficient ($\lambda$) between 2.0 and 2.5, indicating that a $100 loss hurts roughly twice as much as a $100 gain feels good 8. 3. Diminishing Sensitivity: The marginal utility of both financial gains and financial losses decreases as they grow larger in absolute magnitude. This critical property results in a value function that is concave in the domain of gains and convex in the domain of losses 8.

This asymmetric curvature directly drives the disposition effect. When a stock's price appreciates above the purchase price, the investor enters the concave "gains" domain. Diminishing sensitivity implies that further theoretical gains provide progressively less marginal utility, rendering the investor acutely risk-averse; they are psychologically compelled to sell the asset to "lock in" the sure gain. Conversely, when a stock falls below the purchase price, the investor crosses the reference point into the convex "losses" domain. Here, taking a guaranteed, realized loss represents maximum psychological pain due to loss aversion. To avoid crystallizing this pain, the investor becomes risk-seeking, holding onto the declining asset in the irrational hope that it will rebound to the break-even reference point 86.

Nuances of Realization Utility

While Prospect Theory remains the most widely cited foundational explanation, financial economists have identified distinct limits to its explanatory power when applied strictly in pure mathematical models. Barberis and Xiong (2009) challenged the standard application of prospect theory, demonstrating mathematically that if an investor derives utility strictly from annual, unrealized portfolio fluctuations, the model frequently fails to predict the disposition effect reliably 47.

To bridge this theoretical gap, modern behavioral finance utilizes the augmented concept of "realization utility." Proposed by Barberis and Xiong, and later expanded upon by researchers utilizing neurological data (such as Frydman et al.), realization utility posits that prospect theory utility is not derived from passive observation of paper gains or losses 457. Instead, the emotional utility is actively generated at the precise, discrete moment an asset is sold. Selling a winner triggers a tangible burst of positive realization utility (pride), while selling a loser triggers intense negative realization utility (regret) 147. This framing perfectly captures why investors are content to ignore massive paper losses within their portfolios but exhibit extreme reluctance to execute the sell order that finalizes the loss.

Regret Avoidance and Mental Accounting

Operating in tandem with mathematical value functions, Shefrin and Statman identified distinct emotional drivers that catalyze realization utility 18. Chief among these is mental accounting, a cognitive framework pioneered by Richard Thaler. The principle of mental accounting dictates that investors rarely view their portfolio holistically as a single pool of unified risk capital; instead, they compartmentalize individual trades into distinct mental "accounts," tracking the performance of each individual security rigidly against its specific purchase price 114.

This psychological compartmentalization is intrinsically linked to regret avoidance. Closing a mental account at a loss forces the investor to admit a tangible analytical error. This process transfers an abstract, reversible paper loss into an unchangeable, realized failure, generating intense feelings of personal regret and a localized loss of pride 1515. By refusing to close the account, the investor perpetually delays this emotional reckoning. Consequently, the disposition effect must be viewed not just as a cognitive miscalculation of financial probabilities, but as a robust emotional defense mechanism 1515.

Rational Counter-Explanations and Contextual Applicability

Researchers routinely probe whether the disposition effect could, under specific circumstances, be a rational, mathematically sound response to market environments, rather than an irrational psychological bias. Neoclassical finance attempts to explain the selling of winners and holding of losers through several alternative mechanisms, though empirical evidence largely refutes these as universal primary drivers.

Tax-Loss Harvesting and Portfolio Rebalancing

Tax optimization represents a perfectly rational financial strategy: sophisticated investors should realize losses to offset taxable capital gains and defer realizing gains to delay tax liabilities 19. If investors operated on purely rational lines, tax incentives would dictate a reverse disposition effect throughout the fiscal year. Odean (1998) found that while the disposition effect does indeed reverse in December - when investors engage in urgent end-of-year tax-loss selling - it dominates continuously from January through November 19. This proves that the psychological aversion to loss ultimately overpowers rational tax optimization for the vast majority of the trading year 19.

Similarly, routine portfolio rebalancing - the practice of selling appreciated assets to restore target asset allocation weights - cannot entirely explain the phenomenon. While rebalancing mechanics generate trades that superficially mimic the disposition effect, empirical tracking of individual brokerage accounts demonstrates that the aggregate magnitude of gain realization far exceeds what is mathematically necessary for standard rebalancing mandates 378.

Mean Reversion: When the Disposition Effect is Rational

A more robust rational explanation relies on an investor's belief in mean reversion - the statistical assumption that extreme asset price movements will naturally revert to historical averages. Under this logic, a stock that has risen sharply in value is statistically likely to fall (prompting a rational sale), and a stock that has fallen significantly is statistically likely to rise (prompting a rational hold) 59. In traditional, broad-market equities, this belief is empirically irrational due to the prevalence of post-earnings momentum, resulting in heavy systemic underperformance when retail investors ride their losers 9.

However, the rationality of the disposition effect is highly context-dependent. A comprehensive within-subject experiment involving 193 professional traders conducted by Guenther and Lordan (2023) tested behavioral execution across non-mean reverting and mean-reverting securities 1011. The researchers found that professional traders naturally exhibited the disposition effect when interacting with mean-reverting securities, such as commodities 10. Because commodities generally revert to the physical cost of production or historical supply-demand equilibriums over time, selling winners early and holding losers is a mathematically optimal, profit-maximizing strategy in that specific asset class 1011.

Interestingly, when Guenther and Lordan applied a simple informational intervention designed to force traders to recognize and suppress the disposition effect, it negatively impacted the professional traders' short-term and medium-term returns in mean-reverting markets, highlighting that attempting to cure a perceived "bias" can be destructive if the underlying asset behavior justifies the strategy 1011.

Investor Typology: Demographics, Sophistication, and Algorithms

The susceptibility to behavioral biases is not uniform across market participants. The disposition effect varies drastically depending on the sophistication, scale, gender, and technological nature of the trader.

Retail Investors vs. Institutional Managers

Retail investors consistently exhibit the highest magnitude of the disposition effect. Individual traders generally lack rigorous risk-management frameworks, automated stop-loss discipline, and sophisticated informational advantages, leaving them highly exposed to raw psychological impulses 1220. This exposure translates into a severe structural drag on portfolio performance, with systematic and quantitative strategies routinely outperforming average retail discretionary trading by significant annual margins 3.

Within the retail cohort, specific demographic markers influence bias intensity. Studies analyzing proprietary transaction-level data indicate that older investors and women tend to exhibit a stronger disposition effect. The variance in female investors is often attributed in behavioral literature to statistically higher levels of risk aversion and a greater susceptibility to regret avoidance 132214. Conversely, higher levels of formal education and longer trading experience are correlated with a lower disposition effect, though experience alone rarely eliminates the bias entirely 132214.

Institutional investors and mutual fund managers operate within structured environments designed specifically to mitigate emotional biases. However, they are not entirely immune. Research by Frazzini (2006) utilizing comprehensive mutual fund holdings data confirmed the presence of the disposition effect among professional fund managers, though it operates at a notably weaker magnitude than in the retail cohort 24. Institutional disposition effects contribute heavily to widespread market inefficiencies, as large mutual funds reluctant to realize losses delay necessary price corrections across major index components 29.

The algorithmic control group: Human vs. AI Trading

The rapid integration of Artificial Intelligence (AI) and High-Frequency Trading (HFT) provides behavioral economists with a unique control group for analyzing the disposition effect. Because algorithms execute predefined logical parameters devoid of emotional resonance, they theoretically eliminate psychological noise 312.

A critical study by Liaudinskas published through Norges Bank utilized comprehensive, granular trade data from the Copenhagen Stock Exchange to map human day traders against similarly trading algorithms 24. The findings provided unparalleled causal evidence of the psychological root of the disposition effect 24.

The research revealed that human day traders demonstrated a substantial disposition effect that fluctuated directly based on external mood proxies, specifically local weather. On colder mornings, human traders exhibited significantly higher disposition metrics, tightening their aversion to loss and clinging tighter to depreciating assets. At 10 a.m., the human disposition effect averaged 9.6 percentage points on cold mornings versus 7.5 percentage points on warmer mornings 24. In stark contrast, algorithmic traders exhibited a statistically insignificant aggregate disposition effect and remained entirely insensitive to weather, environmental mood shocks, or market sentiment 24.

While AI systems generally avoid the bias, Liaudinskas found that certain High-Frequency Trading algorithms engaged heavily in short-term mean-reversion strategies mechanically mimic disposition-like trading patterns, selling minor winners and holding minor losers 24. However, unlike human traders - who deploy these strategies irrationally and suffer measurable financial losses as a result - algorithms executing these quantitative trades do not suffer identical performance degradation, highlighting the vast operational difference between a calculated statistical strategy and an emotional bias 24.

Macroeconomic Cycles and Cultural Variances

Investor behavior is highly fluid, deeply contextual, and responsive to broader environmental forces. The macroeconomic regime and the cultural framework of the traded asset heavily modulate the intensity of the disposition effect.

Bull Markets, Bear Markets, and Volatility

Extensive empirical studies indicate that the disposition effect operates countercyclically relative to broader equity markets. Research by Bernard et al. (2020), alongside analyses of the Estonian and Taiwanese stock exchanges, confirms that the bias intensifies significantly during bear markets and economic busts 915.

During severe market downturns, investors witness widespread portfolio degradation. Out of a psychological fear of enduring total, all-encompassing losses, they rush to liquidate their few remaining profitable positions to secure fragmented, tangible gains 915. Furthermore, general systemic risk aversion spikes during market crashes, which mathematically heightens the convexity of the loss domain within the prospect theory value function. Conversely, during sustained, multi-year bull markets, the disposition effect weakens. As overall market returns persistently rise, investors become increasingly overly optimistic, and the sheer abundance of rising assets across the portfolio dulls the psychological urgency to immediately lock in profits 1525.

Cultural Paradigms and Home Bias

Market structure and cultural paradigms significantly influence the execution of behavioral distortions. Studies examining the "A-share" market in China and emerging markets in Taiwan report disposition effect intensities that are significantly higher than those recorded in mature Western markets 132627. This variance is frequently attributed to a combination of heavy retail-dominated trading volumes, lower overall market pricing efficiency, and indigenous sociopsychological characteristics embedded within the regional investment culture 2627.

Additionally, the disposition effect interacts heavily with "home bias" - the preference for familiar, domestic assets. Research encompassing over one million retail forex trades across 126 countries demonstrates that investors are significantly more prone to realize gains quickly and hold losses for extended periods when trading familiar, home currencies compared to foreign currency pairs 28. This implies that familiarity breeds a deeper emotional attachment to the asset, ultimately intensifying regret aversion when the asset declines in value 28.

Digital Architecture: Gamification and User Interface Design

The architecture of retail financial interaction has been revolutionized over the past decade by the advent of zero-fee mobile brokerages, social trading networks, and behavioral gamification. These User Interface (UI) and User Experience (UX) innovations are not neutral conduits for trade execution; they actively alter how investors process financial information, inadvertently creating new psychological reference points that exacerbate the disposition effect.

| Interface Feature | Psychological Mechanism | Impact on Disposition Effect |

|---|---|---|

| Gamification (Badges, Confetti) | Converts analytical processes into hedonic, dopamine-driven experiences. | Amplifies. Encourages rapid realization of gains to trigger reward pathways, while masking stagnant losses 2915. |

| Social Transparency | Introduces peer observation and reputational stakes. | Mitigates. Public visibility forces disciplined adherence to strategies, reducing the disposition effect by up to 35% 2231. |

| Mobile App Logins | Frequent checking creates dynamic, temporal anchoring. | Complicates. Generates the "Last Login" effect, establishing competing reference points that stall decision-making 7. |

Zero-Fee Brokerages and Digital Engagement Practices

Platforms like Robinhood have successfully democratized market access but introduced highly scrutinized Digital Engagement Practices (DEPs), such as push notifications, interactive leaderboards, and celebratory trade animations 291532. These gamified elements fundamentally transform the act of investing from a stoic analytical process into a hedonic, engaging experience 33.

The regulatory scrutiny surrounding these features - highlighted by the 2024 Massachusetts Securities Division enforcement action against Robinhood - centers on the premise that gamification subtly nudges retail investors toward excessive, high-risk trading patterns that benefit the broker's order-flow revenue 153216. By actively lowering the psychological barrier to execution, gamification amplifies investor overconfidence and dramatically exacerbates the disposition effect. Investors, triggered by constant dopamine stimuli, trade more frequently, realizing marginal gains hastily to trigger reward animations, while holding silent, uncelebrated losses in the background of the app interface 291532.

The "Last Login" Effect and Dynamic Attention

The mechanics of modern digital brokerages create profound micro-behavioral shifts regarding how reference points are established. Groundbreaking research by Quispe-Torreblanca et al. (2023) identified the novel "last login" effect. By analyzing granular platform telemetry data, they discovered that an investor's attention is so heavily anchored by the digital interface that every time an investor logs in and actively views their portfolio, the current asset price is cemented as a new psychological reference point, operating in parallel to the original purchase price 7.

This creates a highly complex, interacting disposition matrix. Investors dynamically assess gains and losses not just against their original cost basis, but against what the portfolio was theoretically worth the last time they looked at their phone. The psychological interaction between these reference points is violently asymmetrical: even a minor, temporary loss since the previous login is sufficient to psychologically nullify the positive feelings of a massive, long-term gain since the original purchase, severely suppressing the investor's willingness to sell a long-term winner 7.

Social Trading and Reputational Discipline

The advent of social trading platforms (STPs), where retail investors can observe, comment on, and directly copy the portfolios of their peers, introduces a complex duality to behavioral dynamics.

On one hand, the "herding" effect promoted by social feeds can lead to excessive risk-taking and the chasing of momentum anomalies 1718. However, regarding the disposition effect specifically, public visibility can act as a powerful disciplining mechanism. Research by Danbolt et al. (2022) utilizing proprietary fintech data found that when individual portfolios and trades are made entirely public to the platform, the disposition effect actually diminishes by approximately 35% 2231. The transparency of the social environment triggers heightened reputational awareness, encouraging investors to adhere to more rational, rigorous trading strategies to avoid the public embarrassment associated with mismanaging capital and holding obvious "loser" assets 2231.

The Cryptocurrency Ecosystem: A Microcosm of Behavioral Extremes

The digital asset sector presents a highly accelerated ecosystem for observing behavioral finance anomalies. Cryptocurrency markets are characterized by unprecedented historical volatility, extreme retail participation, 24/7 continuous trading availability, and a general absence of traditional corporate valuation fundamentals (such as earnings reports or discounted cash flows). This renders the crypto ecosystem an unparalleled incubator for sentiment-driven cognitive biases 193839.

Cryptocurrency retail investors represent a highly active, hyper-financialized cohort, logging into brokerage accounts exponentially more often than traditional equity investors - averaging roughly 90 logins per month 40. Studies utilizing raw blockchain data and exchange order books universally confirm the presence of robust disposition effects in Bitcoin and broader altcoin markets 204243.

However, the extreme cyclicality of the digital asset class generates a distinct behavioral pattern across market phases. Empirical data demonstrates that cryptocurrency investors exhibit a reverse disposition effect during euphoric crypto bull markets. Driven by extreme Fear Of Missing Out (FOMO) and narrative momentum, they will hold winning tokens endlessly and sell minor losers quickly to reallocate capital into rapidly surging assets 193839. Yet, when the market cycle breaks, this reverses into a devastating return to the traditional disposition effect during bear markets. Retail participants routinely hold heavily depreciated assets - colloquially referred to as holding "bags" - in a desperate, often mathematically impossible hope to return to their initial cost basis 193839.

This behavior is further complicated by "post-liquidation tilt," a phenomenon where retail traders who have just suffered complete losses on leveraged positions rapidly re-enter the market with even higher leverage in an irrational attempt to break even, mirroring the extreme risk-seeking behavior predicted by the deepest convex trenches of the prospect theory value function 39.

Macroeconomic Implications and Market Inefficiencies

The disposition effect does not operate in an isolated vacuum; the aggregate sum of millions of biased, individual retail and institutional decisions heavily distorts macroeconomic price discovery mechanisms.

The primary systemic consequence of the disposition effect is the generation of short-term market momentum and the subsequent underreaction to public news. When highly positive news about a publicly traded company is released (such as an earnings beat), the intrinsic fundamental value of the stock immediately rises. However, because a large cohort of disposition-prone investors currently hold the stock at a paper gain, they rush to liquidate their positions to secure the new profit. This massive wave of artificial, psychologically driven selling pressure dampens the upward price adjustment, causing the asset's price to underreact to the good news 129. Over subsequent months, as this initial selling pressure slowly subsides and the market absorbs the floating shares, the price drifts upward to its true fundamental value, creating observable momentum anomalies 129.

Conversely, when negative news breaks, investors experiencing the pain of loss universally refuse to sell, shielding the asset from the necessary, rational downward selling pressure. This collective refusal prevents the market from clearing efficiently, delaying vital price corrections and artificially sustaining overvalued assets for extended periods 129.

Furthermore, extensive unrealized loss exposure creates a secondary chilling effect on market liquidity. Research indicates that when a portfolio consists largely of unrealized losses, the investor not only refuses to sell the existing assets but becomes highly reluctant to initiate entirely new positions, effectively suppressing capital reallocation and starving emerging market opportunities of fresh liquidity 21.

Conclusion

The disposition effect represents a fundamental and enduring clash between standard economic rationality and the complex realities of human psychology. Driven primarily by prospect theory's asymmetric value function, loss aversion, and the emotional mechanics of regret avoidance and mental accounting, investors systematically cannibalize their own long-term financial returns by selling winning assets prematurely and clinging obstinately to depreciating investments.

While certain unique market environments - such as mean-reverting commodity sectors - render this specific trading behavior mathematically optimal, in the momentum-driven realities of global equities and the extreme volatility of digital assets, it functions as a severe structural liability. As global financial markets grow increasingly digitized and accessible, the velocity of these behavioral errors is noticeably accelerating. The proliferation of zero-fee gamification, mobile application telemetry, and social trading interfaces constantly bombard retail investors with new psychological reference points, heavily amplifying emotional triggers and stalling rational decision-making. Ultimately, mitigating the disposition effect on a systemic scale requires a transition from discretionary, emotion-driven portfolio management toward highly disciplined, systematic, algorithmic frameworks, acknowledging the prevailing reality that in modern capital markets, an investor's greatest adversary is invariably their own psychology.