Framing effects on risk perception and choice in finance and insurance

Theoretical Foundations of the Framing Effect

Classical economic theory, underpinned by the rational maximization model, operates on the assumption that human decision-making is strictly bound by expected utility and description invariance. Under these axioms, an idealized rational agent evaluates choices based on their absolute probabilistic value, meaning that the agent should make identical choices when presented with mathematically equivalent options, regardless of how those options are described 12. However, the evolution of behavioral economics - most notably pioneered by psychologists Daniel Kahneman and Amos Tversky - has demonstrated that human decision-making systematically deviates from these assumptions.

The framing effect refers to the cognitive bias wherein individuals decide on options based on whether they are presented with positive or negative connotations. In financial contexts, this manifests as a strong tendency to avoid risk when a positive frame (a potential gain) is presented, and a tendency to seek risk when a negative frame (a potential loss) is presented 134.

The psychological value of a financial outcome is not linear. Rather, as described by Prospect Theory, it follows an asymmetric, S-shaped value function based around a neutral reference point. Losses exhibit a much steeper psychological impact than mathematically equivalent gains. This creates a state of "loss aversion," driving risk-seeking behavior when choices are framed as losses to avoid the psychological pain, and risk-averse behavior when choices are framed as gains to lock in the psychological pleasure 235.

In modern financial markets, the framing effect is not merely an academic anomaly; it is a fundamental driver of consumer behavior that dictates portfolio allocation, insurance uptake, and retirement planning. Experimental data continuously highlights that human judgments are highly prone to the manner in which options are linguistically and visually structured. For example, in generalized financial experiments, up to 73.1% of participants will select a risk-averse, guaranteed financial gain over a probabilistic option in a positively framed scenario, whereas negative frames consistently elicit probabilistic, risk-seeking choices 1.

Understanding the profound nuances of the framing effect is crucial for grasping how retail investors navigate complex digital choice architectures, how cultural and linguistic variables modulate susceptibility to these cognitive biases, and how regulatory bodies design frameworks to protect consumers from deceptive or exploitative practices.

Framing Dynamics in the Insurance Sector

The insurance sector provides one of the clearest empirical environments for observing the framing effect. Because the core product relies entirely on the pricing and perception of probabilistic risk, and because consumers frequently lack the actuarial expertise to evaluate complex probabilities objectively, purchase intentions are heavily sensitive to narrative framing, temporal orientation, and the structural presentation of premiums 6.

The Annuity Puzzle and Retirement Decumulation

The "annuity puzzle" - the empirical observation that consumers vastly under-utilize annuities despite their theoretical value in hedging longevity risk - can be largely explained by choice framing. A large-scale behavioral experiment conducted by the United Kingdom's Financial Conduct Authority (FCA), involving 907 participants aged 55 to 75, revealed profound shifts in consumer preference based strictly on how decumulation options were described 7.

When retirement income options were presented in a "Consumption Frame," the focus was placed on the income available for spending throughout retirement and the guaranteed protection against outliving one's resources. In this frame, 66% of consumers preferred an annuity over alternative drawdown strategies, such as standard savings accounts 7.

Conversely, when the exact same financial products were presented in an "Investment Frame" - which highlighted the total size of the initial pension pot (e.g., £100,000), the amount "invested," and the lack of a refundable balance upon early death - consumers viewed the annuity as a "gamble" and a risky proposition, fearing they would "lose their money" to the insurance company 78. Under the investment frame, consumer preference for the annuity collapsed to just 17% 7. Furthermore, the mere use of the word "annuity," which carries heavy investment-frame connotations and perceptions of poor value in the public consciousness, was found to independently reduce consumer preference by 16 percentage points compared to when the product's underlying characteristics were described without the specific label 7.

| Framing Strategy | Primary Focus | Emotional Response Elicited | Consumer Behavioral Shift |

|---|---|---|---|

| Consumption Frame | Lifetime spending capacity, hedging against longevity risk. | Security, long-term stability, peace of mind. | High preference for annuities (66%); viewed as safe. |

| Investment Frame | Capital allocation, return on investment, principal loss. | Anxiety regarding capital loss, perceived as a gamble. | Low preference for annuities (17%); preference for lump-sum. |

This behavioral preference for asset preservation over consumption is also evident in broader retirement data. An Employee Benefit Research Institute (EBRI) study analyzing retirees over an 18-year period demonstrated that households with guaranteed pension income only saw a 4% drop in non-housing assets, compared to a 34% drop for those without a pension 9. Retirees actively match their essential spending to their guaranteed income to avoid drawing down the principal balance, demonstrating a powerful psychological preference for asset preservation that can be activated or suppressed depending on how an annuity product is framed 9.

Life Insurance and Long-Term Care (LTC)

Life insurance demand exhibits similar sensitivities to gain and loss framing. Standard economic utility models suggest that loss aversion should decrease the demand for term life insurance, as consumers perceive the premium as a "sure loss" against an unlikely payout if they survive the term without an incident 1011. However, experimental data suggests that targeted framing interventions can significantly alter these baseline aversions.

In the context of Long-Term Care (LTC) insurance, a high-powered survey experiment (N = 1,450) examined the impact of a 2x3 framing intervention on consumer attitudes. Loss-framed messages - such as highlighting the financial devastation a family will face without coverage - triggered higher anxiety-related emotions. In contrast, gain-framed messages - such as highlighting peace of mind and protection - elicited calmness and hope 12. The study found no significant interaction effects between the gain/loss frames and varying narrative frames (such as financial vs. family narratives), but confirmed that framing impacts consumer attitudes through these distinct emotional pathways 12.

Health Insurance and Medical Decision-Making

The efficacy of gain versus loss framing extends deeply into health insurance and protective medical behavior, though the empirical results in this sub-domain are frequently mixed and highly context-dependent 213. For instance, during the COVID-19 pandemic, public health communications utilizing a loss frame (e.g., "if you do not stay at home... people will die") triggered significantly higher negative affect (NA) than gain-framed equivalents 13. Yet, the ultimate persuasiveness of the frame often relies on the audience's perception of threat minimization and trust in authorities 13.

In incentivized health behaviors, such as adolescent Type 1 Diabetes management, the theoretical expectation is that loss aversion should make loss-framed financial incentives more powerful. However, an empirical trial (N=39) testing financial incentives for glucose monitoring found that while both frames improved clinical outcomes over a control group, participants in the gain-frame arm actually earned more financial rewards ($74.97) compared to the loss-frame arm ($71.11), meeting daily insulin administration goals at a higher percentage 14. This highlights that while Prospect Theory provides a baseline, the practical application of framing in health contexts requires calibrated testing.

Deductibles and Narrow Framing

Framing also dictates how consumers select policy deductibles. Experimental studies reveal that when individuals evaluate insurance with "narrow framing" - meaning they assess the risk strictly on the net insurance payoff (indemnity minus premium) - their aversion to risk on that specific, narrow transaction reduces their overall insurance demand 15. When participants are presented with a broad description of a risky situation and asked to decide on deductibles jointly, they make significantly different choices than a control group asked to decide on deductibles separately in a narrow frame 15. Narrow framing causes consumers to isolate the premium payment as a distinct loss, obscuring the broader portfolio protection the insurance provides, which helps explain the broadly observed phenomenon of under-insurance in various markets 1015.

Demographic and Cognitive Moderators of the Framing Effect

The effectiveness of any given frame is not universal; it is heavily moderated by the demographic characteristics, cognitive abilities, and temporal orientation of the target consumer.

Age and Temporal Orientation

Age is a profound moderating variable. Older individuals generally exhibit lower financial risk tolerance (FRT) than younger cohorts. However, studies parsing the mechanisms behind this decline show that older adults are not inherently more risk-averse in their general attitudes (Risk Attitude, or RAtt); rather, they perceive the exact same financial investment as subjectively riskier (higher Risk Perception, or RP) 16. Consequently, older populations respond robustly to loss-framing in health and accident insurance products, whereas younger demographics show a higher baseline susceptibility to framing effects in general life insurance consumption 17.

For younger adults (aged 25 - 49), life insurance is a product offering long-term benefits that rarely motivates immediate action 17. A field experiment assessing click-through rates and purchase intentions among this demographic found that temporal considerations heavily impact framing efficacy 1217. Gain-framed messages were highly effective for younger consumers, but only when the messaging emphasized benefits situated well into the future, despite the requirement for immediate action 1718. Conversely, when immediate benefits and urgency were required to motivate action, loss-framed messaging outperformed gain-framed messaging, generating 24% higher click-through rates and 18% more form submissions 20.

Financial Literacy and Premium Formatting

Cognitive limitations and varying levels of financial literacy significantly exacerbate consumer susceptibility to framing biases. Research utilizing rating-based conjoint analysis on 299 life insurance policyholders in India demonstrated that financial literacy significantly alters how consumers process premium and maturity benefit framing 1819.

Consumers with low financial literacy are highly susceptible to "premium framing" - for example, viewing a policy as highly affordable and having a higher purchase intention when the cost is framed as a "monthly premium" rather than an "annual aggregate," even if the mathematical, annualized cost is identical 18. Similarly, the framing of benefits as aggregate sums versus incremental payouts deeply biases the perceived value of the product for those lacking numerical fluency 18.

Interventions that elevate financial literacy have been shown to mitigate these heuristic shortcuts. When consumers receive brief educational interventions comparing life insurance benefits with traditional banking instruments, they rely less on the emotional valence of the frame. Improved financial literacy significantly increases purchase intention for policies with monthly premiums and aggregate benefits by allowing the consumer to process the true actuarial value of the policy, leading to more rational purchase intentions that align with actual economic needs 18.

Gender, Language, and Market Participation

Demographic analysis of framing experiments frequently reveals gender-based disparities, with men generally exhibiting higher risk tolerance across all framed scenarios, while women consistently prefer risk-averse options 1. However, the intersection of gender and linguistic framing yields deeper insights into market participation gaps.

Women are historically less likely to participate in complex financial markets, a gap often attributed to lower standard measures of financial literacy 20. Yet, contemporary research demonstrates that financial domains are internally differentiated along gendered lines. Activities like investing and long-term planning are widely stereotyped in marketing language as masculine, whereas saving and budgeting are more weakly gendered or associated with care-oriented responsibilities 20. Studies manipulating the linguistic phrasing and framing of financial tasks demonstrate that gender gaps in observed financial competence can be systematically altered without changing the underlying informational content of the tasks 20.

Digital Choice Architecture and Fintech Interfaces

As retail investment, wealth management, and insurance onboarding increasingly migrate to digital platforms, the concept of "choice architecture" - the deliberate design of the environment in which people make decisions - has become highly formalized 2321. Fintech applications and robo-advisors utilize framing at the user interface (UI) and user experience (UX) levels to nudge investor behavior. This application of behavioral economics can be used to mitigate harmful cognitive biases or, controversially, to accelerate speculative user engagement.

Robo-Advisory Platforms and Goal-Based Framing

Early iterations of robo-advisors, such as Wealthfront and Betterment, emerged with algorithms designed to democratize modern portfolio theory (MPT) through passive, low-cost index allocation 22. A core feature of these platforms is their use of "goal-based framing" to combat the deleterious effects of loss aversion, overconfidence, and recency bias among retail investors 22.

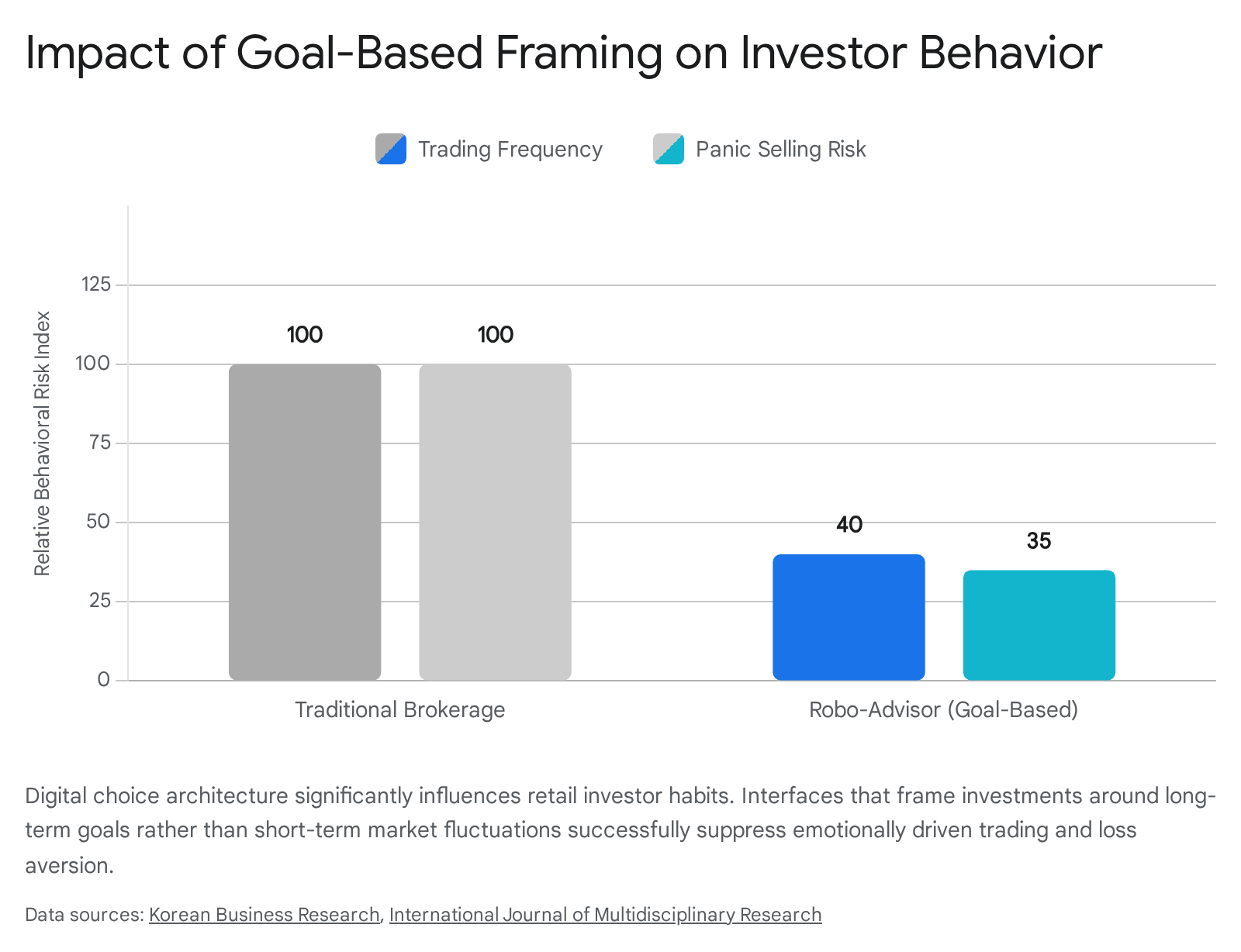

Traditional brokerage interfaces frame portfolios around daily percentage changes, red and green ticker colors, and short-term market performance. This architecture inadvertently triggers loss aversion and encourages panic selling during market downturns, as investors are disproportionately sensitive to immediate portfolio drops 22. In contrast, robo-advisors frame the investment journey around long-term, personalized objectives (e.g., "Retirement in 30 Years," "Home Ownership") 22.

By anchoring the user's focus on the probability of reaching a defined future goal rather than the daily volatility of the underlying assets, the interface dampens emotional impulses. Wealthfront utilizes machine learning to adjust investment strategies based on dynamic risk profiling, pairing academic risk assessment frameworks with automated liquidity controls to prevent suboptimal, emotionally driven trades 23. Empirical evidence indicates that users engaged with goal-based robo-advisory frameworks exhibit significantly reduced trading frequency, maintain consistent risk exposure, and are less likely to liquidate assets during severe market turbulence compared to self-directed retail investors using traditional brokerage interfaces 22.

Emotional Design and Gamification in Retail Trading

Conversely, other financial technology platforms have historically utilized interface framing to maximize engagement rather than strict, passive discipline. The evolution of trading applications like Robinhood highlights how visual branding and interface framing dictate the perceived seriousness of financial risk 23.

In its earlier iterations, Robinhood employed a "youthful disruptor" archetype, utilizing gamification, achievement milestones, leaderboards, and bold colors that framed options trading and equity purchasing as accessible, frictionless, and game-like 23. While successful in driving user acquisition, this framing drew regulatory and academic scrutiny for encouraging speculative behavior and obscuring the severity of complex financial instruments.

As the platform matured, it executed an identity reframe. By shifting its positioning to a "holistic financial platform," the application traded its disruptive energy for an aura of "expert calm" 23. This reframing was executed through deliberate emotional design choices: shifting to a restrained neutral color palette, adopting technical illustration systems inspired by institutional financial charts, and updating typography to balance authority with approachability 23. These subtle visual and linguistic framing adjustments are designed to alter the user's mental accounting, prompting them to view the platform as a secure environment for long-term wealth building rather than a venue for short-term, dopamine-driven speculation.

Linguistic and Cross-Cultural Dimensions of Framing

Financial decision-making and framing susceptibility do not exist in a psychological vacuum; they are heavily mediated by grammatical structures, linguistic properties, and broad cultural backgrounds. The language in which financial information is processed, as well as the cultural baseline for risk tolerance, dictates how effectively a frame will alter behavior 24.

The Foreign Language Effect (FLE)

One of the most profound discoveries at the intersection of psycholinguistics and behavioral finance is the "Foreign Language Effect" (FLE). Experimental data consistently demonstrates that when individuals make financial decisions in a non-native (foreign) language, they are significantly less susceptible to emotional biases, loss aversion, and the framing effect 42125.

The primary mechanism behind the FLE is the "emotional distance hypothesis," combined with dual-process theory. Native languages are acquired in emotionally rich, foundational contexts, embedding deep affective resonance in words like "loss," "risk," or "death" 421. A foreign language, typically learned in a structured academic environment later in life, lacks this deep emotional tethering. Consequently, processing financial gambles in a second language forces slower, more analytical, and deliberative cognitive processing (System 2 thinking), which dampens the intuitive, heuristic-driven reactions (System 1 thinking) that power the framing effect 26.

In classical equivalency framing experiments, participants operating in their native language showed a steep drop in selecting a "safe" option when the problem was shifted from a gain frame (71% safe choice) to a loss frame (44% safe choice) 25. However, when the exact same problem was presented to bilingual participants in their foreign language, the cognitive disparity collapsed, with choices remaining highly consistent across both gain (69%) and loss (58%) frames 25.

This attenuation of bias extends directly to localized financial markets. The well-documented "home bias" - the irrational tendency of investors to overweight domestic assets despite the diversification benefits of foreign equities - is significantly mitigated when investment decisions are framed in a foreign language. A 2025 study involving 12 rounds of incentivized investment decisions showed that participants deciding in their native language exhibited strong home bias (investing roughly 10.74% more in local stocks relative to foreign), whereas those deciding in a foreign language exhibited no home bias, allocating capital almost evenly (59.81% local vs. 58.74% foreign) based on rational risk-reward metrics 27.

Grammatical Structure: Future-Time Reference

Beyond bilingualism, the inherent grammatical structure of a consumer's native language implicitly frames their perception of financial risk and time. Linguists categorize languages by their Future-Time Reference (FTR). "Strong-FTR" languages (like English or Vietnamese) require speakers to grammatically separate the present from the future using distinct markers (e.g., "I will save money"). "Weak-FTR" languages (like Mandarin or German) blur this morphological distinction, allowing speakers to use present-tense phrasing to describe future events 1625.

Empirical research indicates that speakers of weak-FTR languages view the future as psychologically closer and less distant than speakers of strong-FTR languages. This subtle, continuous linguistic framing results in profound macroeconomic behavioral shifts. Controlling for income, education, cultural values, and institutional factors, speakers of weak-FTR languages are 31% more likely to save money in any given year, 24% less likely to smoke, and exhibit higher overall financial risk tolerance across their lifespans 1625.

Cultural Baselines and the Cushion Hypothesis

Cultural milieu establishes the psychological baseline against which financial frames are evaluated. Cross-cultural studies consistently highlight disparities in baseline risk perception between Eastern and Western populations. Chinese and other highly collectivistic individuals frequently perceive themselves as more risk-tolerant than their individualistic (e.g., American) counterparts 1628.

This divergence is frequently attributed to the "cushion hypothesis," which suggests that individuals in collectivistic societies perceive lower individual financial risk because they rely on robust familial and social networks to act as a safety net in the event of financial failure 29. However, while cultural framing heavily dictates perceived risk tolerance, empirical analysis of actual portfolio creation reveals a disparity. Analyses of Chinese and American mock portfolios, alongside actual household finance surveys, indicate that despite higher stated risk tolerance, actual equity allocation and portfolio volatility often remain similar across these cultures 2829. This suggests that other variables, such as differing levels of financial literacy or institutional trust, offset the cultural propensity for higher risk 29.

Regulatory Frameworks and Consumer Protection Policies

Because framing fundamentally alters consumer choices, financial institutions are heavily incentivized to engineer choice architectures that maximize profitability. When these frames exploit behavioral biases to obscure costs, steer consumers toward suboptimal products, or create immense friction in exiting agreements, they transition from benign marketing strategies to deceptive or exploitative practices. Consequently, global regulatory bodies have increasingly shifted from simple disclosure requirements to outcome-based behavioral oversight to combat harmful framing.

The FCA Consumer Duty and Sludge Practices (UK)

In the United Kingdom, the Financial Conduct Authority (FCA) implemented the Consumer Duty in 2023, marking a paradigm shift in financial regulation. Moving away from the archaic notion that a rational consumer will successfully navigate any market if provided with accurate textual disclosures, the FCA explicitly integrated behavioral science into its regulatory framework 30. The Duty acknowledges that because consumer reactions to choice architecture are predictable, harm resulting from deceptive framing is inherently "foreseeable" 3031.

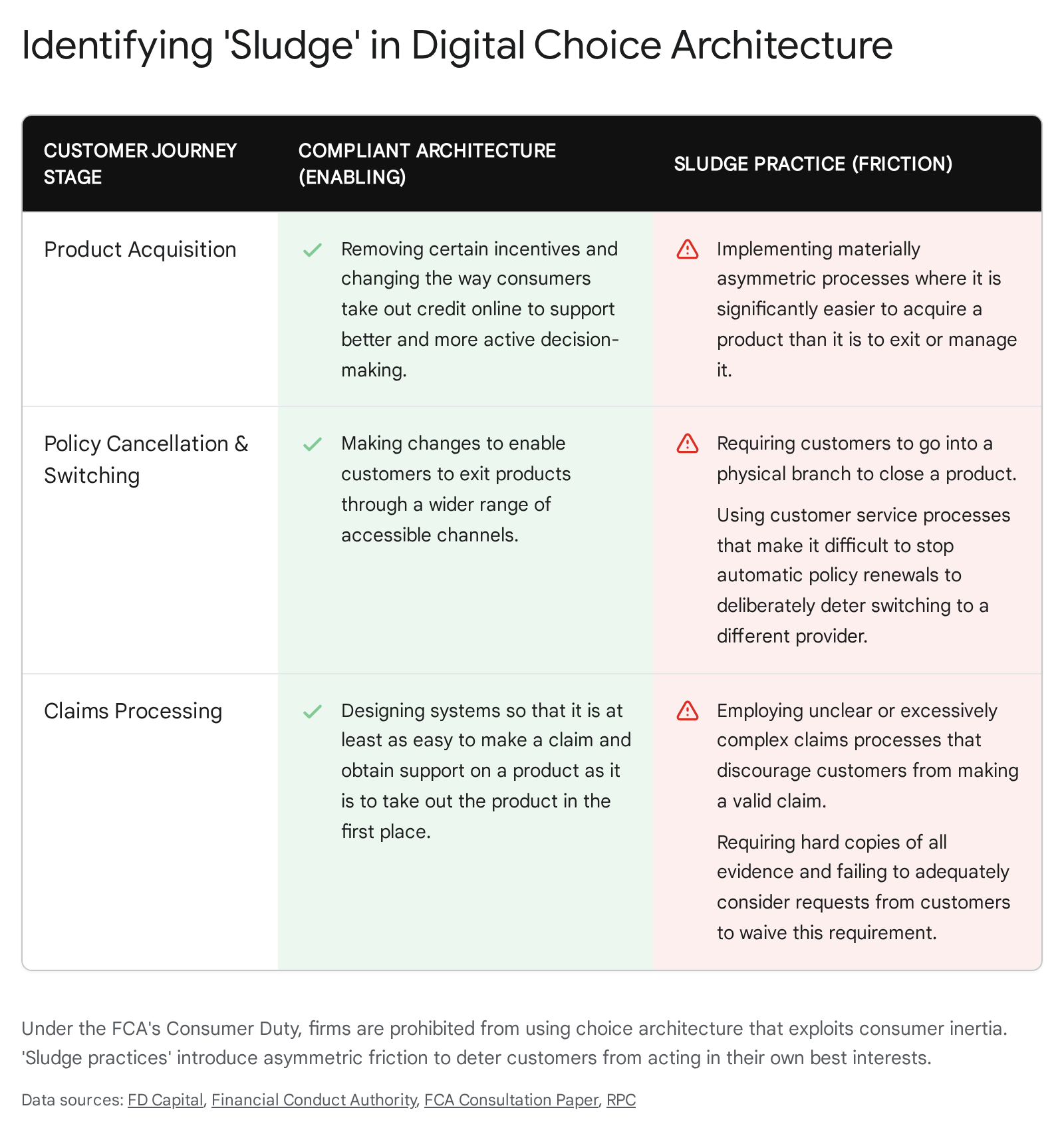

The Consumer Duty mandates that firms must act to deliver good outcomes for retail customers, underpinned by three cross-cutting rules: acting in good faith, avoiding foreseeable harm, and enabling consumers to pursue their financial objectives 3233. Central to this framework is the regulatory attack on "sludge practices."

Sludge refers to intentional, friction-heavy framing designed to exploit consumer inertia, loss aversion, or cognitive fatigue 313435. Prevalent examples identified by the FCA include: * Asymmetric user journeys where a product requires a single click to purchase but demands a phone call, physical letter, or branch visit to cancel 313436. * Overly complex insurance claims processes framed to discourage consumers from pursuing valid payouts, such as requiring hard copies of all evidence without waiver options 3536. * Auto-renewal frames that exploit customer inertia to maintain policies at below-market savings rates or above-market insurance premiums 3136.

Under the Duty, firms are required to actively test their digital interfaces and communications. If management information data reveals that consumers are lingering on certain screens, abandoning claims at high rates, or failing to understand pricing frames, the firm is liable for the resulting foreseeable harm, regardless of whether the terms and conditions were technically accurate 30.

The CFPB and Standardized Disclosures (US)

In the United States, the Consumer Financial Protection Bureau (CFPB) approaches framing primarily through the lens of Unfair, Deceptive, or Abusive Acts or Practices (UDAAP) regulations, focusing heavily on the standardization of disclosures. The underlying regulatory philosophy is that standardizing the presentation frame across the industry allows consumers to compare products objectively, mitigating the cognitive overload that lenders often use to obscure predatory terms.

A primary example is the TILA-RESPA Integrated Disclosure (TRID) rule, implemented to combine previously overlapping and complex mortgage disclosures into a single, comprehensible Loan Estimate and Closing Disclosure 37. By legally mandating the layout, typography, and specific vocabulary of these documents, the CFPB restricts the ability of lenders to use visual or linguistic framing to hide high finance charges or adjustable-rate risks 38. Empirical studies on TRID's implementation indicate that standardizing the frame effectively decreased consumer information processing costs, allowing for better comprehension, though it concurrently increased secondary market frictions for banks, resulting in a slight tightening of overall mortgage credit availability 37.

Furthermore, the CFPB actively monitors how framing is used discriminatorily. In 2024, the Bureau released a matched-pair testing study on small business lending. The study revealed that lenders utilized verbal framing to steer Black entrepreneurs toward alternative, often more expensive financing products (such as business credit cards or real estate-secured loans) at a significantly higher rate (59%) than white participants with similar or weaker credit profiles (39%) 39. Lenders also used discouraging linguistic framing to suppress application rates among minority groups, expressing explicit interest in obtaining loan applications from 40% of white participants, but only 23% of Black participants 39. This illustrates that framing is not only a tool for consumer manipulation but can also be deployed as a covert mechanism for unlawful financial discrimination 3940.

| Regulatory Body | Key Policy Framework | Primary Mechanism to Combat Deceptive Framing |

|---|---|---|

| FCA (UK) | Consumer Duty | Outcome-based enforcement targeting "sludge practices" and asymmetric digital friction; demands active testing of consumer comprehension 3034. |

| CFPB (US) | TRID & UDAAP | Strict standardization of visual layout and terminology in disclosures (e.g., Loan Estimates) to prevent cognitive overload and obscurement of terms 37. |

Conclusion

The framing effect fundamentally disrupts the classical economic assumption that financial consumers process information rationally and invariantly. In reality, consumer perception of risk and reward is highly malleable, dictated by whether options are presented as gains or losses, investments or consumption, and mediated by the cognitive friction introduced by digital interfaces.

In the insurance sector, framing determines whether a product is viewed as a vital safety net or an unnecessary gamble, with demographic factors like age, financial literacy, and temporal orientation dictating which linguistic approach is most persuasive. Fintech and robo-advisory platforms have demonstrated that while framing can be weaponized to encourage excessive trading, it can also be harnessed positively - through goal-based UI design - to override loss aversion and enforce disciplined, long-term financial behavior.

Furthermore, framing is not a culturally or linguistically universal constant. The Foreign Language Effect and variations in Future-Time Reference demonstrate that the emotional resonance of words and grammatical structures inherently bias risk evaluation, proving that the medium of communication is inseparable from the economic decision itself.

As the understanding of these behavioral mechanisms matures, regulatory frameworks are evolving in tandem. Paradigms like the FCA's Consumer Duty and the CFPB's standardized disclosure rules reflect a modern consensus: the architecture of a choice is just as critical as the choice itself. Protecting consumers in modern financial markets requires regulators to scrutinize not only the mathematical fairness of a product but the psychological frame in which it is sold.