The 7 Most Common Investing Biases Ranked

Investors consistently underperform the very assets they hold, surrendering roughly 15% of their potential wealth accumulation over a decade due to predictable psychological traps. Extensive behavioral finance research reveals that market outcomes are driven less by rational financial analysis and more by deeply ingrained cognitive biases like loss aversion, overconfidence, and the fear of missing out. Understanding and systematically mitigating these seven mental shortcuts is arguably the single most important factor in long-term investment success.

The Financial Penalty of Being Human

For decades, the foundation of modern portfolio theory and classical economics rested on the Efficient Market Hypothesis (EMH) and the concept of homo economicus - the perfectly rational economic actor who systematically processes all available information to maximize utility and optimize their risk-to-reward ratio 12. In this theoretical framework, markets are perfectly efficient because humans are perfectly logical.

In reality, however, investors are emotional, normal human beings operating with brains optimized for evolutionary survival, not for navigating the abstract complexities of global financial markets 33. When faced with uncertainty, volatility, and an overwhelming deluge of data, the human brain relies on heuristics - mental shortcuts that allow for rapid decision-making. While these shortcuts are useful for escaping predators or making split-second daily choices, they introduce systematic, recurring errors into financial judgments 356.

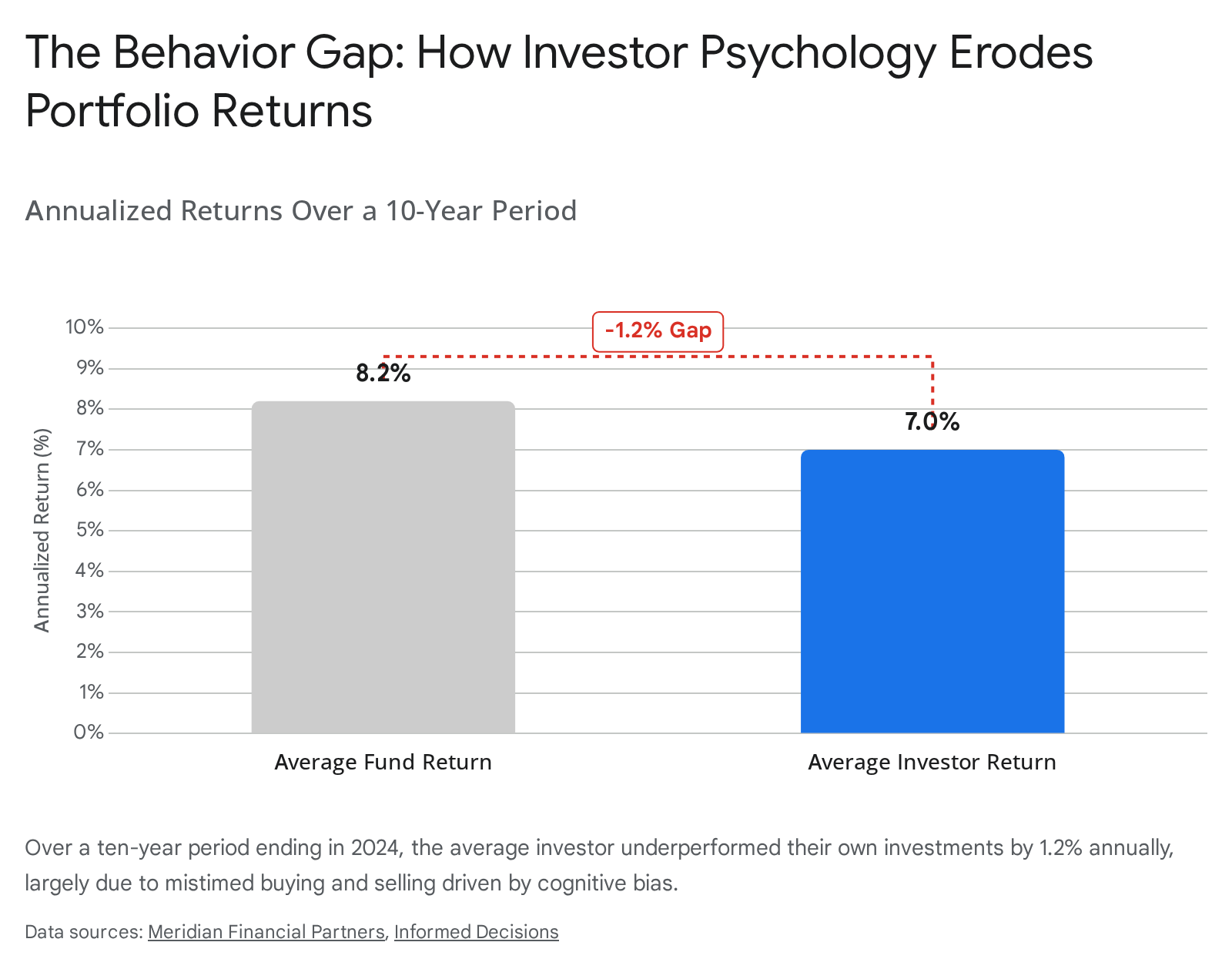

The financial cost of these cognitive errors is immense, measurable, and remarkably consistent across different market cycles. Every year, Morningstar publishes its "Mind the Gap" study, which compares the time-weighted returns of mutual funds and exchange-traded funds (ETFs) against the dollar-weighted returns actually earned by the investors holding those funds 78. The 2025 edition of the study, which analyzed over 25,000 U.S. funds over the ten years ending December 31, 2024, revealed a glaring discrepancy.

While the average fund returned an annualized 8.2% over that decade, the average investor in those exact same funds earned only 7.0% 78. This 1.2-percentage-point annual shortfall is known as the "behavior gap."

The behavior gap is not caused by high management fees, poor asset selection, or unpredictable black swan events. It is caused entirely by investor timing 79. The data shows that investors consistently add money to the market after prolonged rallies out of greed, and withdraw capital during sharp declines out of fear, missing out on the subsequent recoveries 411. While a 1.2% annual penalty may sound trivial, when compounded over a decade, it means that the average retail investor forfeits roughly 15% of the total wealth their portfolio generated 8411. Market research firm DALBAR's annual Quantitative Analysis of Investor Behavior Report corroborates this phenomenon, demonstrating that constant portfolio churn is uniquely deleterious to wealth building 411.

While psychologists have identified hundreds of distinct cognitive biases, the field of behavioral finance has isolated a specific subset that repeatedly sabotages portfolio growth. Based on meta-analyses, trading data, and global surveys, these are the seven cognitive biases ranked by how frequently they distort real-world investment decisions.

1. Loss Aversion and the Disposition Effect

Loss aversion is arguably the most powerful and heavily researched behavioral bias in finance. Introduced by Nobel laureate Daniel Kahneman and Amos Tversky as the foundation of "prospect theory," loss aversion describes the psychological asymmetry in how humans experience financial outcomes 125. Extensive behavioral experiments prove that the psychological pain associated with losing a specific amount of money is experienced roughly twice as intensely as the joy of gaining that exact same amount 1467.

If an individual is offered a gamble with a 50% chance of winning $100 and a 50% chance of losing $100, the vast majority of people will decline the bet, even though the mathematical expected value is zero 17. The sting of the potential loss heavily outweighs the allure of the gain.

The Sunk Cost Fallacy

Loss aversion gives rise to several dangerous secondary biases, most notably the sunk cost fallacy. This is the tendency for individuals to continue pouring resources - whether time, effort, or capital - into a failing endeavor simply because they have already invested heavily in it 617.

In a study by JoNell Strough on age demographics and sunk costs, researchers presented college students and older adults with a scenario where they paid over $10 for a movie ticket, only to realize within the first five minutes that the film was terrible 6. A purely rational economic actor would leave the theater, recognizing that the $10 is gone regardless of whether they stay, and that staying only costs them their valuable time. However, a massive percentage of participants chose to sit through the terrible movie to "get their money's worth." In financial markets, this exact mindset prevents investors from abandoning a flawed thesis, pushing them into deeper holes as they spend more time and capital defending a bad trade 618.

Watering the Weeds: The Disposition Effect

In active trading and portfolio management, loss aversion primarily manifests as the "disposition effect." This is the overwhelming psychological urge to sell winning investments far too early to "lock in" profits, while holding onto losing investments indefinitely to avoid the psychological pain of admitting defeat 1419.

When a purchased stock goes up, the brain is flooded with dopamine. Selling the stock at a profit feels like an immediate validation of the investor's intellect: I made a good call 14. However, when a stock drops, the psychology flips. Selling a stock at a loss means officially admitting a mistake. To the human ego, holding onto an underperforming asset feels less painful because the loss remains a theoretical "paper loss" until the position is closed. The investor holds on, hoping the price will recover just enough to allow them to break even and escape without ego damage 1420.

A landmark 2009 study from the Yale School of Management analyzed millions of retail trades and found that this behavior is almost universal. Roughly 80% of retail investors consistently sell their winning stocks at minor gains of 5% to 10%, while holding onto losing stocks for months or years 14. Legendary portfolio manager Peter Lynch famously likened this behavior to "watering the weeds and pulling the flowers" in a garden 8.

By systematically cutting winners and letting losers breathe, investors completely destroy the mathematical advantage of compounding returns and their portfolio's risk-reward ratio 1419. They turn what could have been a 50% or 100% long-term gain into a 7% blip, while allowing a manageable 20% drawdown to cascade into a catastrophic 50% loss 148. Professional traders operate on the exact opposite principle - cutting losses aggressively and letting winners run - not because they are inherently smarter, but because they have built mechanical systems to override their brain's natural loss aversion 14923.

2. Overconfidence and the Illusion of Control

If loss aversion explains why investors hold onto losers, overconfidence bias explains why they enter bad trades in the first place. Overconfidence occurs when an individual overestimates their own knowledge, analytical skills, and ability to predict market outcomes 32024.

According to a recent report by the Financial Industry Regulatory Authority (FINRA), almost two in three U.S. investors (64%) rate their own investment knowledge highly 10. This illusion of superiority creates a severe disconnect between perceived ability and the chaotic reality of financial markets.

Behavioral finance divides overconfidence into three distinct, measurable sub-categories 1112: 1. Overestimation: The tendency for an individual to overrate their actual achievements and capabilities, believing they are smarter or more resilient than objective data suggests. 2. Overplacement: The predisposition to rank one's own accomplishments higher than those of others. In investing, this means believing one has a distinct edge over the millions of other highly educated market participants. 3. Overprecision: Having excessive, unwarranted certainty in the accuracy of one's own forecasts, leading to a failure to properly weigh downside risks.

The Cost of Churn

A highly cited behavioral finance study by researchers Brad Barber and Terrance Odean tracked the performance of thousands of individual investors to measure the cost of this bias. They discovered that overconfidence is the primary driver of excessive trading 328.

Because overconfident investors genuinely believe they can consistently time market tops and bottoms, or discover hidden value that Wall Street analysts have missed, they trade frequently 2813. This rapid portfolio churn racks up massive transaction costs, bid-ask spread losses, and capital gains taxes. More importantly, it results in mistimed market entries and exits. Barber and Odean found that this overconfidence-driven trading led to net returns that significantly lagged behind passive benchmark strategies, often dragging performance down by 3 to 5 percentage points annually 28.

The Illusion of Control

Overconfidence is often tightly paired with the "illusion of control" - the false belief that an investor can influence, navigate, or mitigate external events that are entirely dictated by macroeconomic forces 181314.

This bias frequently leads to dangerous under-diversification. For example, corporate employees often heavily over-allocate their retirement portfolios to their own employer's stock 18. Because they walk the halls of the company and understand its products, they suffer from an illusion of control, falsely believing their proximity to the firm mitigates their financial risk. If the company faces a sudden bankruptcy or sector-wide downturn, the employee tragically loses both their current income and their life savings simultaneously.

Interestingly, professional expertise does not automatically cure overconfidence. Studies indicate that while financial literacy helps investors recognize basic market mechanics, "experts" such as corporate managers and investment bankers often suffer from overconfidence more than novices when dealing with tasks in their specific domain 1231. A string of successful trades during a bull market can easily convince a manager that they possess unique genius, blinding them to the fact that a rising tide lifts all boats 2013.

3. Herding Mentality and Fear Of Missing Out (FOMO)

In a 2015 global survey of financial practitioners administered by the CFA Institute, respondents were asked to select the behavioral bias that affects investment decision-making the most. Herding garnered 34% of the vote, standing out as the undisputed top bias, far outpacing confirmation bias (20%) and overconfidence (17%) 15.

Herding mentality is the psychological tendency to follow the actions of the crowd, abandoning independent fundamental analysis because conforming provides intense psychological comfort 3716. From an evolutionary standpoint, staying with the herd ensured physical survival. To step away from the crowd was to risk isolation and death. In modern capital markets, however, following the herd is financially lethal. By the time the "herd" is rushing into an asset and making front-page news, the risk premium is entirely priced in. Buying at this stage simply provides exit liquidity for the early adopters, leading to the inflation and inevitable collapse of asset bubbles 241634.

The Global FOMO Index

In the digital age, herding behavior has been supercharged by technology, evolving into the Fear of Missing Out (FOMO). Retail frenzies around meme stocks like GameStop, the meteoric rises of cryptocurrencies, and highly anticipated initial public offerings (IPOs) are deeply intertwined with social media amplification 343517. An investor watching their peers post screenshots of massive overnight returns on platforms like Reddit or Twitter feels an intense psychological pressure to participate. This emotional anxiety often causes them to abandon a disciplined, long-term strategy to chase short-term, highly speculative gains 3518.

Recent academic attempts have sought to quantify the exact market impact of this anxiety. In 2025, researcher Yosef Bonaparte developed the "Global FOMO Index," which tracks online search behaviors for terms like "FOMO," "Buy Stock," "Get Rich Quick," and "Bitcoin Price" over a twenty-year period 17. The research yielded a fascinating, counterintuitive insight: in the immediate short term, elevated FOMO actually decreases market volatility by roughly 2%. Because the crowd is moving uniformly in one direction, responding to the exact same social cues, markets achieve a temporary, artificial stability 17.

However, this stability is a trap. The same research shows that peak FOMO consistently correlates with significantly lower risk-adjusted returns in the subsequent months and years 17. When retail investors abandon fundamental analysis to follow the crowd, they almost invariably buy assets at their absolute peak and sell them in a panic during the inevitable correction 18. The anxiety about missing out is often a reliable signal that the investor should be doing the exact opposite.

4. Confirmation Bias and the Echo Chamber

Confirmation bias is the human tendency to seek out, interpret, favor, and recall information in a way that confirms one's pre-existing beliefs, while actively ignoring, rationalizing, or dismissing data that contradicts those beliefs 281638.

First formally studied by English psychologist Peter Wason in 1960 through his famous "2-4-6 task" experiment, confirmation bias is now recognized as one of the most destructive forces in behavioral finance 628.

The Cost of Being "Right"

In trading, confirmation bias creates an impenetrable echo chamber. If an investor takes a heavy position in a specific technology stock or a cryptocurrency, their brain naturally begins to filter the world to support that decision. They will gravitate toward bullish news articles, optimistic earnings forecasts, and social media forums that validate their thesis 173839. Conversely, if a bearish analyst releases a report highlighting major regulatory risks or deteriorating margins, the investor will dismiss the report as "flawed," "biased," or "short-sighted" 1720.

The danger of confirmation bias is that it generates an illusion of infallibility. The investor feels increasingly certain of their thesis because their highly curated information diet only reflects their own views 24.

When confirmation bias goes unchecked, it leads to irrational, emotionally-driven decisions at the worst possible times. For example, if a major cryptocurrency exchange collapses or a company misses earnings targets by a wide margin, the rational response is to reassess the thesis. An investor blinded by confirmation bias, however, will view the price drop not as a warning sign, but as an opportunity to "buy the dip" and double down on a failing asset 39.

The financial cost of this blindness is severe. As noted in the Barber and Odean studies, confirmation-driven trading leads investors to hold onto losing positions far too long, blinding them to fundamental deterioration. This failure to cut positions when objective signals demand it reduces long-term annual returns by several percentage points 28.

Furthermore, education alone does not cure the issue. Highly experienced professionals, who have been explicitly trained to avoid bias in their research, often fall victim to confirmation bias if they have strongly ingrained preconceptions 6. Their deep industry knowledge actually works against them, giving them sophisticated, highly technical vocabulary to rationalize away contradictory evidence 2013.

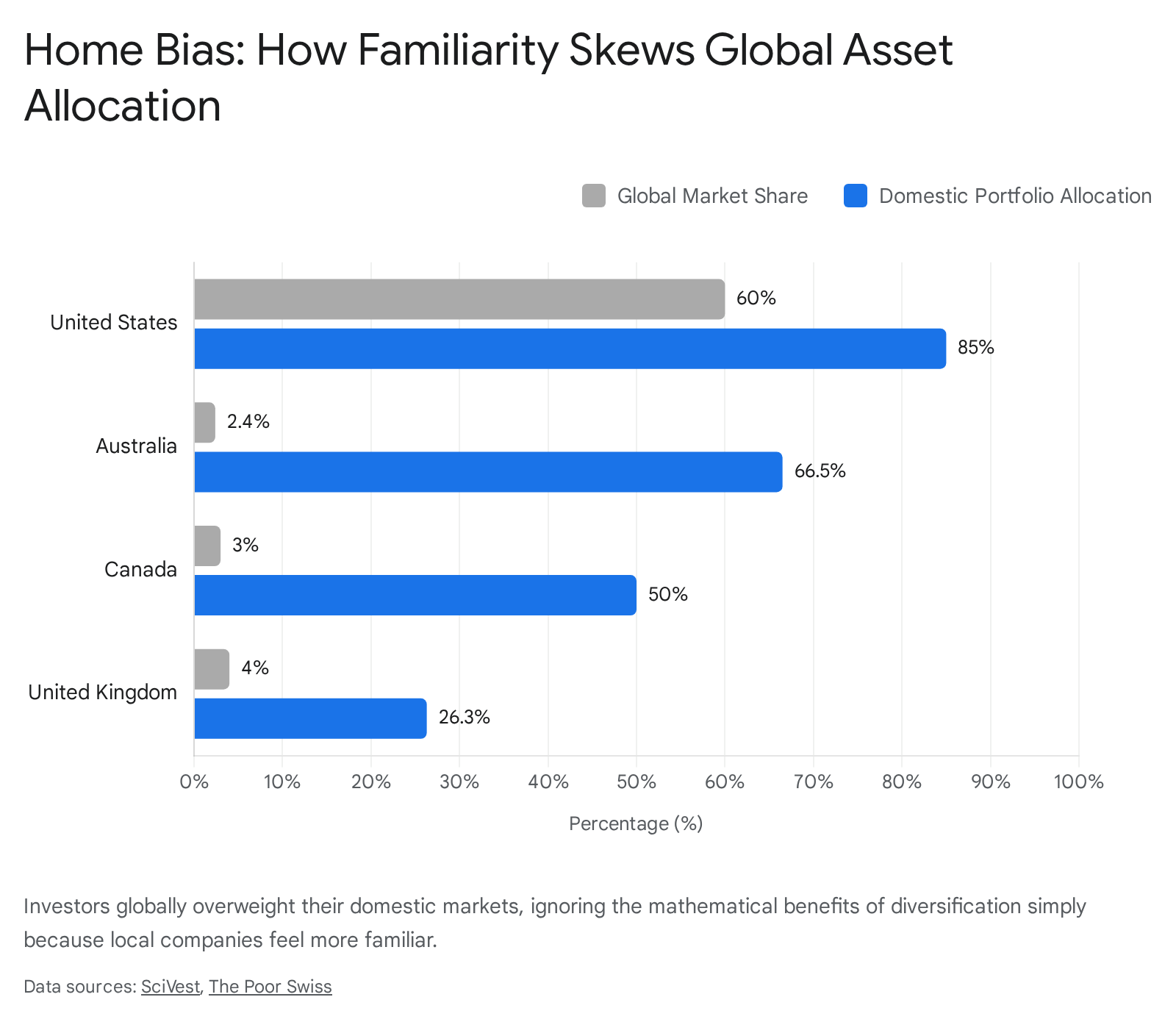

5. Home Country Bias: The Illusion of Familiarity

Home bias is the widespread tendency for investors to disproportionately allocate their capital to domestic equities, sacrificing the mathematical and structural benefits of global diversification simply because local assets feel safer and more familiar 74019.

Modern portfolio theory strongly suggests that a globally diversified portfolio minimizes single-country regulatory risk and broadens exposure to emerging growth sectors. An optimal, frictionless portfolio should roughly mirror global market capitalization. Yet, investor behavior deviates wildly from this baseline, making home bias one of the single largest and most persistent active tilts in global equity portfolios 20.

A 2024 analysis by Vanguard and other market researchers analyzing trillions of dollars in ETF holdings revealed the staggering magnitude of this familiarity bias across different developed markets 4020.

| Country | Approximate Share of Global Stock Market | Actual Average Portfolio Allocation to Domestic Stocks | Degree of Over-Allocation |

|---|---|---|---|

| United States | ~60.0% | ~85.0% | 1.4x |

| Canada | ~3.0% | ~50.0% | 16.6x |

| Australia | ~2.4% | ~66.5% | 27.7x |

| United Kingdom | ~4.0% | ~26.3% | 6.5x |

Data sources: Vanguard (2024), Fidelity International, and academic studies of global ETF holdings 4043. Market share approximations reflect conditions as of the mid-2020s.

As the data clearly shows, investors in nations with tiny global footprints heavily over-index to their own borders. A Canadian investor allocating 50% of their equity to domestic stocks is carrying 16 times more exposure to the Canadian economy than is justified by its 3% weight in global indexes 40.

This bias is not confined to retail investors. Emerging market institutions exhibit massive home biases as well. In Brazil, Mexico, and South Africa, domestic banks, mutual funds, and pension funds hold massive concentrations of local currency government bonds 2122. While regulatory limits on foreign exchange positions play a role, the profound concentration of local assets vastly increases systemic risk if the domestic economy falters 21.

While there are some structural justifications for a mild home bias - such as minimizing currency exchange risk, benefiting from local tax incentives on dividends, or avoiding opaque foreign accounting standards - the sheer magnitude of the bias cannot be explained by pure economics 23. It is primarily driven by the psychological comfort of investing in familiar brands seen daily on supermarket shelves or local news broadcasts 1019. When global markets shift rapidly - such as the massive 10% outperformance of non-U.S. stocks over U.S. stocks observed in early 2025 due to tariff concerns and shifting growth expectations - investors paralyzed by home bias find themselves entirely on the wrong side of the trend 20.

6. Anchoring Bias: Obsessing Over the First Number

Anchoring bias is a cognitive error that occurs when individuals rely too heavily on the first piece of information they receive (the "anchor") when making subsequent judgments, pricing, or valuation decisions, even if that initial information is arbitrary or completely irrelevant 474824.

In consumer psychology, anchoring is used to drive sales. If a customer sees a television originally priced at $1,000, and returns a week later to see it marked down to $800, their brain anchors to the $1,000 figure, making the new price feel like an incredible bargain 24. They may purchase it impulsively, ignoring the fact that competing stores sell the exact same model for $700.

The Danger of Arbitrary Benchmarks

In investing, anchoring routinely distorts valuation assessments. For example, an investor might purchase a stock at $100 per share. Over the next year, the company's fundamentals drastically deteriorate, losing market share and issuing weak forward guidance. The stock price drops to $60. The rational move would be to assess the stock's future potential from the $60 baseline based purely on current data. However, the investor remains psychologically anchored to their $100 entry price. They refuse to sell, making the irrational decision to wait until the stock "gets back to what it is worth," failing to recognize that the company's actual worth has fundamentally changed 1650.

Similarly, the psychological magnet of the 52-week high or 52-week low serves as a powerful, but dangerous, anchor for market participants. Investors may avoid buying a rapidly growing, highly profitable company simply because it is trading near its 52-week high, anchoring to the belief that it is now "too expensive" to touch. Conversely, they may try to catch a "falling knife" by buying a failing company just because it looks "cheap" compared to its historical high, ignoring the structural reasons for the decline 5051.

Anchoring is also prevalent in institutional finance and private placements. In private equity negotiations or M&A talks, the party that issues the first offer gains a massive psychological advantage. That initial number, even if it is an extreme lowball or highball figure, becomes the benchmark for all subsequent negotiations, dictating the tone of the conversation and shifting the final settlement closer to the anchor 5051.

7. Availability and Attention Bias (The AI Era Trap)

Availability bias is the human tendency to overestimate the importance, likelihood, or frequency of events based on how easily examples come to mind 1316. When assessing the stock market, investors naturally gravitate toward companies that have been in the news recently, or asset classes that have recently experienced dramatic price swings. This leads to recency bias - extrapolating the events of the past few weeks into permanent future trends, while completely ignoring decades of historical market data 710.

Because the human brain can only process a finite amount of information, investors filter the universe of thousands of publicly traded companies down to the handful they see mentioned on financial television or social media feeds. This causes massive capital inflows into a small handful of highly visible stocks, while fundamentally sound but "boring" companies are starved of capital 1625.

AI and the Automation of Bias

Fascinating new research from the CFA Institute (2026) highlights that availability bias is evolving into a dangerous new form in the era of artificial intelligence. Large Language Models (LLMs) used by portfolio managers, analysts, and retail investors for financial summarization and trade generation are trained on the internet's vast financial data ecosystem 2553.

However, this data ecosystem is not neutral. Megacap tech stocks, highly visible consumer brands, and volatile crypto assets generate exponentially more media coverage, analyst reports, and forum chatter than mid-cap industrial or regional banking stocks 25. Because these popular assets dominate the training data, AI models exhibit a systematic "attention bias" 2554.

When prompted for investment ideas or portfolio summaries, AI models will persistently favor these highly visible, large-cap firms simply because of the sheer volume of their training data, rather than any objective assessment of underlying economic fundamentals 2553. Furthermore, LLMs suffer from a "lost in the middle" phenomenon, where they heavily favor information at the start and end of sequence prompts while neglecting the nuanced context in the middle, further degrading complex financial analysis 54.

If left unchecked, algorithms designed to increase market efficiency may inadvertently automate and amplify human herding behavior. By repeatedly clustering their outputs around highly visible names, AI tools risk pushing portfolios into overcrowded momentum trades and increasing systemic concentration risk, all under the guise of objective technological analysis 2553.

Does Culture Impact Cognitive Bias?

While cognitive biases like loss aversion and herding are deeply wired into human neurology, cross-cultural research indicates that geographic, economic, and societal factors significantly influence how severely these biases manifest. Culture acts as a lens that either magnifies or dampens human psychology 1255.

Hofstede's Dimensions and the Social Safety Net

Studies assessing behavioral finance through the framework of Geert Hofstede's cultural dimensions have found compelling correlations. Research analyzing investors across 53 countries demonstrates that highly individualistic and highly masculine societies (such as the United States and Australia) often exhibit significantly greater susceptibility to both overconfidence and loss aversion 125556.

In highly individualistic cultures, financial success is viewed as a direct reflection of personal merit, making financial loss a severe blow to the ego. Furthermore, the lack of broad social safety nets means that a financial loss carries existential risk 55. In contrast, in more collectivist societies, the presence of strong communal safety nets - whether from state welfare programs or deeply integrated extended family networks - removes some of the sting of financial loss. If an individual loses capital, the society or family structure acts as a buffer. This communal support structure modestly dampens the panic associated with loss aversion, allowing investors to act slightly more rationally during downturns 555.

Islamic Finance and Shariah Literacy

Belief systems and religious frameworks also act as powerful modifiers of financial behavior. Extensive studies of retail investors in the Middle East and Gen Z investors in Indonesia reveal that high levels of Islamic financial literacy (Shariah literacy) can actively suppress speculative herding behavior and FOMO 1114.

Islamic finance operates on strict ethical principles, strictly prohibiting riba (usury/interest), gharar (excessive uncertainty or deception), and maysir (speculation or gambling) 11. Investors who deeply understand and adhere to these ethical investing guidelines demonstrate significantly less vulnerability to the wild, emotion-driven swings of market bubbles. Because their theological framework inherently filters out overly speculative, highly leveraged, or opaque financial assets, they are less likely to chase trends blindly 11. While they are not immune to biases like the illusion of control or hindsight bias, their adherence to a principles-based system acts as a natural behavioral guardrail against the most destructive forms of herd mentality 14.

Can We Train Our Brains Out of Bias?

The persistence of the behavior gap raises a vital question for both individual investors and institutional managers: can these deeply ingrained cognitive biases actually be trained away?

The psychological evidence is promising. A 2025 controlled experiment involving the majority of national risk analysts in a European country demonstrated that bias is not immutable. The study evaluated the effectiveness of a "one-shot debiasing training intervention" on both expert national security analysts and novice university students. The results showed that a single, targeted training session significantly reduced confirmation bias and the "bias blind spot" across both groups 5859. By actively teaching individuals to "consider the opposite" and systematically invert their hypotheses, researchers proved that cost-effective interventions can durably improve expert judgment under uncertainty 5860.

Structural Guardrails and Automated Wealth

However, while psychological training is helpful, the most reliable way to mitigate cognitive bias in financial markets is to implement structural, systemic guardrails that remove emotional decision-making from the process entirely 61.

- Statistical Investment Checklists: A recent 2024 study utilizing machine learning algorithms analyzed a five-year dataset of institutional investment decisions. The data revealed that confirmation, anchoring, and recency biases negatively affected 38% of all trade decisions. However, when the firm implemented a strict statistical framework - incorporating mandatory pre-trade checklists and automated risk alerts - biased decision-making was reduced by a staggering 77%, leading to a direct positive correlation with overall investment performance 6162.

- Automated Asset Allocation: On the retail side, automation is the ultimate cure for the behavior gap. According to Morningstar's "Mind the Gap" analysis, investors who utilized fully or partially automated allocation funds (such as target-date retirement funds) experienced the narrowest behavior gap of any cohort, losing only 0.4% to poor timing compared to the 1.2% average 4. Because these funds automatically rebalance and enforce a "set it and forget it" structure, they physically prevent the investor from panic-selling at the bottom or FOMO-buying at the top 94.

- Pre-planned Structural Exits: To fight the disposition effect (the urge to sell winners early), experienced traders implement structural, rather than emotional, exit strategies. Instead of closing a highly profitable position entirely to lock in a gain, they use automated trailing stop-loss orders. As a stock climbs, the stop-loss climbs with it. They may also incrementally scale out of a position (e.g., selling 30% of the asset while letting the remaining 70% run) 923. This satisfies the psychological need to secure profits while mechanically allowing the bulk of the asset to continue compounding without human interference.

Bottom line

Cognitive biases like loss aversion, overconfidence, and herding cause investors to act as their own worst enemies, leading to well-documented behavioral penalties that severely erode long-term wealth. While these mental shortcuts are deeply ingrained in human evolutionary psychology and influenced by cultural environments, they are not insurmountable. By acknowledging our inherent irrationality, learning to recognize our mental blind spots, and shifting from emotional stock-picking to rules-based, automated investment frameworks, investors can successfully close the behavior gap and capture the returns the market actually offers.