What Is Gap Risk and Why It Matters for Overnight Trading

An overnight gap occurs when a financial asset opens at a significantly different price than its previous closing price, typically driven by major news released while the market is closed. It acts as a hidden cost for investors because standard risk-management tools, such as stop-loss orders, offer zero protection against these instantaneous price jumps, often leaving traders trapped in sudden, outsized losses before they can even react.

The modern global economy is a ceaseless engine of information, but the primary equity markets are strictly bound by time. While the closing bell of the New York Stock Exchange and the Nasdaq rings at 4:00 p.m. Eastern Time, the business world does not clock out 112. Earnings reports are published, regulatory agencies announce sweeping decisions, international conflicts erupt, and macroeconomic data is released while most retail investors are offline, commuting, or asleep.

When the market officially opens again at 9:30 a.m. the following morning, the price of a stock must instantly recalibrate to reflect this entirely new reality. This violent recalibration - the empty space on a chart where no regular trading occurred, but underlying value was fundamentally altered - is known as an "overnight gap" 1.

While day traders who close their positions before the afternoon bell avoid this phenomenon entirely, swing traders, retail investors, and long-term portfolio managers face the persistent, unavoidable threat of gap risk 34. It is often referred to as a "hidden" cost because a vast number of market participants falsely believe that their automated risk controls will protect them from downside exposure. They will not. The reality of market mechanics dictates that an overnight gap bypasses traditional safeguards, forcing investors to either absorb devastating losses or employ far more sophisticated hedging strategies.

The Microstructure of an Overnight Gap

To understand precisely why gaps happen, one must look at the mechanics of liquidity and the structural differences between regular market hours and extended-hours trading sessions.

During regular trading hours, millions of buyers and sellers interact in a highly liquid, heavily regulated environment supported by designated market makers. If a stock begins to face selling pressure, it usually ticks down sequentially - for example, from $50.00 to $49.95, and then to $49.90. This continuous auction allows participants to exit their positions incrementally, and the abundance of counterparties ensures that trades execute smoothly 12.

However, the after-hours and pre-market sessions operate fundamentally differently. Extended-hours trading relies on electronic communication networks (ECNs) that lack the deep liquidity of the primary daytime exchanges 5. During these periods, market makers are not obligated to provide liquidity or maintain tight spreads.

When a major catalyst - such as a surprise earnings miss or an unexpected macroeconomic report - hits the wire after 4:00 p.m., algorithmic traders and institutional players react instantly 16. Because there are comparatively few buyers willing to step in and purchase a plummeting asset in the illiquid after-hours session, sellers are forced to drastically lower their asking prices to find any willing match 12. A seller looking to unload shares might have to drop their ask from $50 directly to $42 just to find a buyer.

By the time the regular market opens the next morning, the "clearing price" based on this overnight supply and demand imbalance will be drastically lower (a gap down) or higher (a gap up) than the previous day's official close 11.

The Primary Catalysts Behind the Price Chasm

Overnight gaps are the market's brute-force reaction to the sudden injection of new information. Because asset prices are essentially the discounted value of all future cash flows, any news that alters the trajectory of a company's future earnings forces an immediate repricing. Common triggers include:

- Corporate Earnings Announcements: Public companies traditionally release their quarterly results either before the morning bell or immediately after the afternoon close. A massive beat or miss regarding revenue, earnings per share, or forward guidance will instantly revalue the equity 156.

- Macroeconomic Data: Inflation data (such as the Consumer Price Index), employment reports, and interest rate decisions by the Federal Reserve are often released at 8:30 a.m. Eastern Time. These reports can move entire sectors or broader market indices before the opening bell 178.

- Mergers and Acquisitions (M&A): A buyout announcement, which usually carries a premium over the current share price, can cause an immediate 20% to 50% gap up in the target company's stock 1.

- Geopolitical Shocks: Events in overseas markets, sudden global conflicts, or supply chain disruptions (such as issues in the Strait of Hormuz) can heavily impact domestic equities while the United States sleeps, as international futures markets process the risk in real-time 789.

The Illusion of Safety: Why Standard Risk Controls Fail

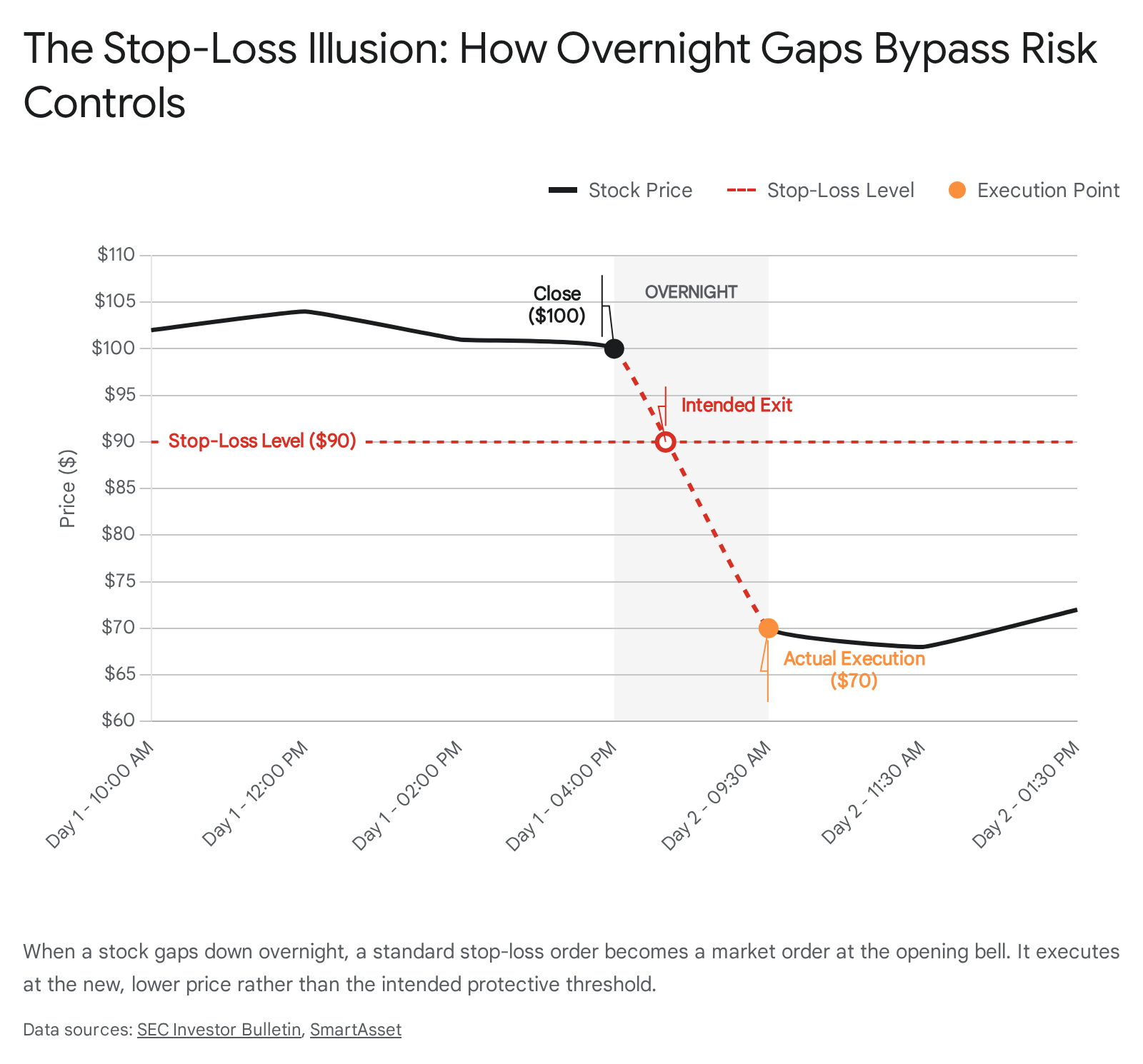

The primary reason gap risk is considered a truly "hidden" cost is due to a widespread, fundamental misunderstanding of how automated risk controls function across trading platforms. Millions of retail investors rely on "stop-loss" orders to protect their capital, assuming these tools offer an ironclad guarantee against catastrophic losses 1011.

A stop-loss order is an instruction provided to a brokerage to automatically sell a security when it reaches a specific price threshold 11. For example, an investor might purchase a stock at $100 and set a stop-loss at $90, operating under the assumption that their maximum risk is strictly capped at a 10% loss. During normal, highly liquid market hours, this assumption is generally correct; as the stock ticks down to $90, the order executes at or very near that price.

However, the fatal flaw in this logic is that a stop price is not a guaranteed execution price 1112. A stop-loss is merely a conditional trigger. Once the stock touches or drops below the $90 threshold, the stop-loss order instantly converts into a standard market order, meaning the broker is instructed to sell the shares immediately at the next best available price, regardless of how low that price might be 111315.

If the company in question announces a disastrous earnings report after hours, and the stock opens the next morning at $70, the regular market hours commence with the stock trading $20 below the investor's intended safety net. At 9:30 a.m., the stop-loss is triggered because the price is below $90. The order converts to a market order, and the shares are sold at the prevailing market price of $70 - not the $90 the investor expected 1115. The trader's intended 10% maximum loss has suddenly ballooned into a 30% catastrophic loss, bypassing their safety net entirely.

The Stop-Limit Trap: Why Alternatives Also Fail

Some investors, aware of the dangers of market orders executing at terrible prices, attempt to fix this issue by utilizing a "stop-limit" order 1112. A stop-limit order combines the features of a stop order with those of a limit order. It requires two distinct price inputs: the stop price (the trigger) and the limit price (the absolute minimum the investor will accept) 1214.

While a stop-limit order guarantees a minimum exit price, it fundamentally does not guarantee execution 1514.

Consider the same hypothetical scenario: a trader buys at $100 and sets a stop-limit order with a stop trigger at $90 and a limit price at $89. If the stock gaps down overnight to $70, the trigger fires at 9:30 a.m. However, the order is now an active limit order to sell at $89 or better. Because the stock is currently trading at $70, the order simply sits on the books unfulfilled 1114.

In a severe gap down, the price rarely rebounds immediately. The trader is left holding a plummeting stock, trapped in an active, bleeding position while the broader market continues to sell off 1115. In either scenario, the trader's risk parameters are obliterated. A stop-loss guarantees a terrible price; a stop-limit guarantees no execution at all, leaving the investor fully exposed to further downside 15.

Comparing Standard Equity Order Types

The following table summarizes how different order types behave when subjected to a severe overnight gap down:

| Order Type | Mechanism Upon Trigger | Behavior During an Overnight Gap Down | End Result for the Investor |

|---|---|---|---|

| Market Order | Executes immediately at the current best available price 12. | Sells shares instantly at the new, drastically lower opening price 12. | Guarantees execution, but guarantees a massive loss far below expectations. |

| Stop-Loss Order | Becomes a market order once the stop price is touched or crossed 1113. | Trigger is bypassed overnight; becomes a market order at the lower opening price 1115. | Fails to protect capital; executes at the gap-down price, realizing the severe loss 15. |

| Stop-Limit Order | Becomes a limit order once the stop price is touched, requiring a minimum execution price 1214. | Trigger is bypassed overnight; becomes an unexecutable limit order resting high above the current market price 1114. | Fails to execute; the investor is trapped holding the depreciating asset 15. |

Real-World Case Studies: When Blue Chips Gap Down

To understand how rapidly an overnight gap can alter the financial landscape, it is necessary to examine recent corporate history. Gaps are not theoretical anomalies confined to volatile, low-market-cap biotechnology firms; they frequently strike the largest, most seemingly stable companies in the global economy.

The Collapse of Silicon Valley Bank (March 2023)

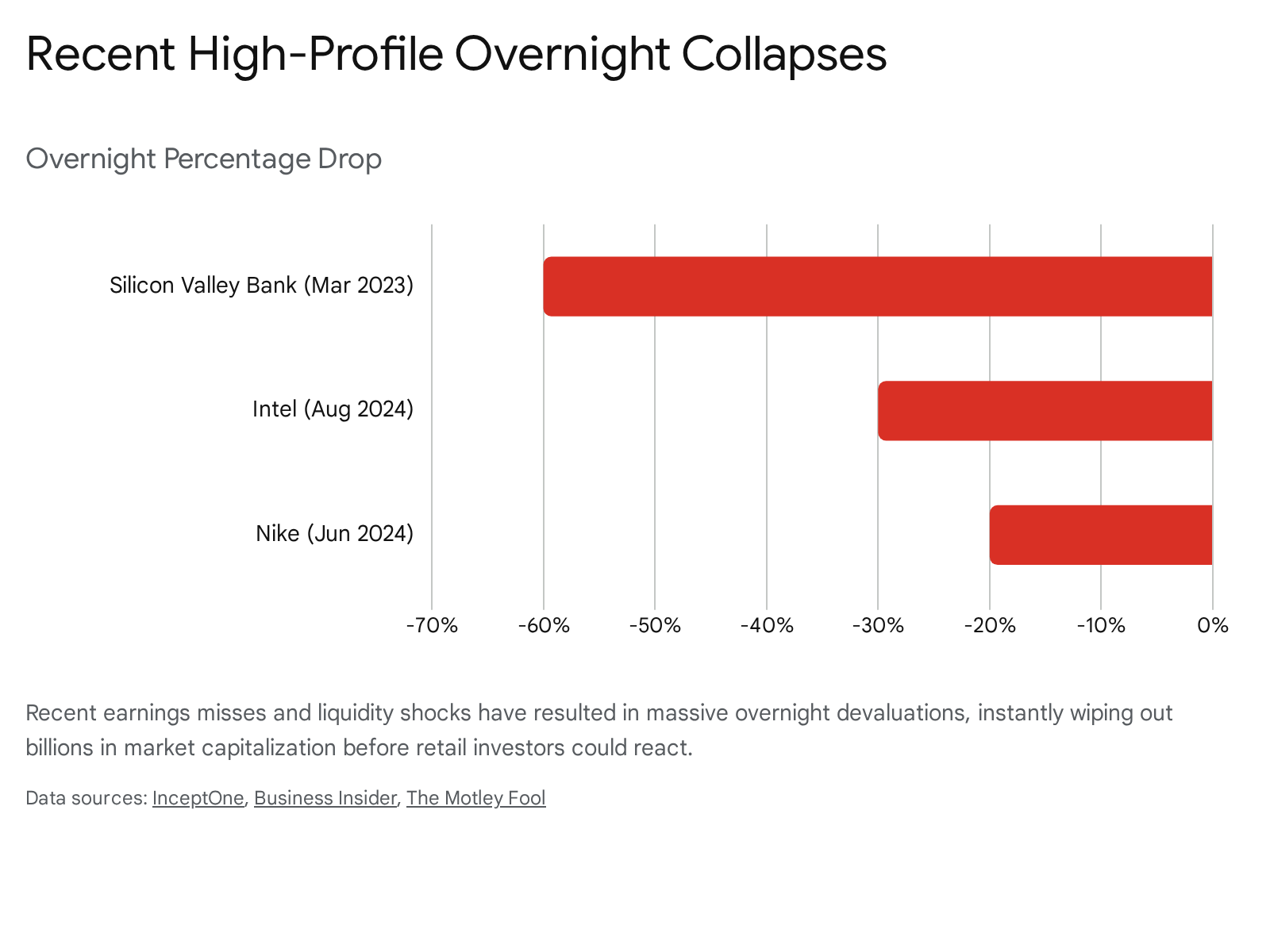

Perhaps the most dramatic recent example of overnight gap risk was the implosion of Silicon Valley Bank (SVB), which served as a powerhouse for the technology and venture capital sectors 1518. During the pandemic, SVB saw its deposits explode, which it subsequently invested heavily in long-term U.S. Treasury bonds 161718. When the Federal Reserve rapidly raised interest rates throughout 2022 and early 2023, the value of those long-term bonds tanked, as bond prices fall when yields rise 1617.

On March 8, 2023, SVB announced a massive balance sheet restructuring. It reported a $1.8 billion loss on a $21 billion bond firesale and revealed plans to dilute shares to raise capital 1618. By the morning of March 9, a classic bank run was underway, with customers withdrawing $42 billion in a single day 1818.

The stock market's reaction was merciless. On March 9, shares tumbled 60% 1816. The following morning, in pre-market trading on Friday, March 10, the stock plunged another 60% before it was halted entirely at a final traded price of $106.04 - a devastating collapse from its heights in the $700 range 1518. Regulators seized the bank shortly after. This catastrophic gap down left retail shareholders effectively wiped out before regular trading even commenced, forcing the stock onto the Over-the-Counter (OTC) markets as a bankrupt entity (SIVBQ) 1518.

Intel's Historic 30% Plunge (August 2024)

Intel Corporation (INTC), historically a foundational blue-chip stock in the semiconductor industry, shocked Wall Street on August 1, 2024. After the closing bell, the company reported a disastrous second quarter, missing adjusted earnings per share estimates (reporting just $0.02 versus the expected $0.10) 1920. More alarmingly, Intel suspended its dividend, provided dismal future guidance, and announced a $10 billion cost-reduction plan that included laying off 15,000 employees 192021.

By the time the market officially opened the following morning on August 2, Intel's stock had gapped down severely, eventually plunging 30% to close around $21 - its worst single-day drop since at least 1982, erasing billions in market value and pulling the entire global semiconductor sector down with it 202122. Any investor holding Intel with a tight 5% or 10% stop-loss saw their protection bypassed entirely as the stock opened significantly lower.

Nike's Unprecedented Sizing Issue (June 2024)

On June 27, 2024, athletic wear titan Nike (NKE) closed at $89.72 26. Following the close, the company reported a 2% decline in quarterly sales and warned of a surprisingly steep 10% decline in the upcoming year due to a struggling direct-to-consumer strategy and losing vital market share to newer, agile brands like Hoka and On 232824.

The market reaction was instantaneous and brutal. The stock gapped down violently the next morning, opening at $73.47, and finished the day at $71.79 - down 20% 26. This single overnight gap erased $28.4 billion in market capitalization, marking the absolute worst trading day in the company's 44-year public history 232824.

The Upside of Gaps: Sudden Windfalls

It is important to note that gap risk cuts both ways. For traders holding the correct asset during a positive catalyst, an overnight gap can yield instantaneous, unearned windfalls that are impossible to achieve during the slow grind of regular market hours.

- Nvidia (NVDA): On February 21, 2024, Nvidia closed at $67.35 (split-adjusted) 30. That evening, CEO Jensen Huang reported $12.3 billion in quarterly profits, crushing analyst expectations, and announced that data centers would need to invest roughly $2 trillion to meet surging artificial intelligence demands 25. The stock gapped up the next morning, opening at $74.89, instantly enriching overnight holders and sparking a massive multi-month rally 3025.

- Meta Platforms (META): Similarly, in early February 2024, Meta reported robust earnings, beating analyst expectations by a wide margin. More significantly, Meta announced it would begin paying a quarterly dividend for the first time in its history 26. The stock gapped up 16% in pre-market trading, a massive dislocation that instantly benefited long-term holders 26.

In the realm of active gap trading strategies, specialized traders attempt to capitalize on these specific dislocations. A Gap and Go strategy bets that the momentum of an overnight earnings gap will continue in the same direction after the opening bell, driven by institutional buying 1. Conversely, a Gap Fade strategy bets that the initial overnight move was an emotional overreaction by retail traders and algorithms. The trader shorts the stock at the open, expecting the price to retrace back toward its previous close to "fill the gap" 1. Both strategies require intense discipline and an understanding that the pre-market gap is the primary driver of the day's action.

Day Trading vs. Swing Trading: The Overnight Dilemma

The handling of gap risk represents the central philosophical dividing line between two of the most popular active trading styles: day trading and swing trading 3427. The choice between the two is ultimately a choice of which specific risks an investor is willing to tolerate.

Day traders operate strictly within the bounds of regular market hours, aiming to capture small, intraday price movements 427. Their defining characteristic is that they close all positions before the final bell at 4:00 p.m., ensuring they have exactly zero exposure to overnight gaps 3427. Swing traders, conversely, hold positions for days, weeks, or even months to capitalize on broader, structural market trends 427. By choosing to hold, swing traders inherently accept gap risk as the unavoidable cost of doing business 328.

Comparing the Strategic Trade-offs

| Strategic Factor | Day Trading | Swing Trading |

|---|---|---|

| Overnight Gap Risk | Zero. All positions are meticulously closed before the market closes 427. | High. Fully exposed to earnings, global news, and macroeconomic data released overnight 327. |

| Capital Requirements | Higher. Often requires a $25,000+ minimum for Pattern Day Trader (PDT) compliance in US equities 3. | Lower starting capital allowed, though overnight margin requirements can be stricter and tie up capital 3. |

| Time Commitment | Intense. Requires constant monitoring of screens, Level II data, and news feeds during market hours 34. | Flexible. Analysis can be done periodically outside of market hours, accommodating traditional employment 3427. |

| Primary Risk Profile | Intraday volatility, execution errors (slippage), and the psychological toll of rapid decision fatigue 327. | Gaps bypassing stop-losses; external geopolitical events; and "thesis drift" (holding a loser hoping for a rebound) 3. |

While swing trading offers the luxury of flexibility and avoids the intense screen-staring fatigue of day trading, overnight gap risk remains its definitive Achilles' heel 327. Swing traders must constantly balance the desire for larger, multi-day profits against the knowledge that a single after-hours headline could devastate their position.

Behavioral Economics: The Psychology of the Gap

When a trader falls victim to a massive gap down, the financial damage is often severely compounded by psychological errors. Because a gap occurs instantaneously, it bypasses the trader's rational decision-making process, frequently triggering the sunk cost fallacy 29.

The sunk cost fallacy in trading is the destructive tendency to hold onto losing positions because of the time, money, or emotional effort already invested, rather than making a rational decision based on the current risk-reward outlook 29. When an investor wakes up to find their carefully planned position has gapped down 15%, their technical thesis for entering the trade is usually broken. Rationally, they should exit the trade immediately to preserve capital.

However, cognitive biases take over. Because they have already suffered the loss on paper, they anchor to their original entry price 29. Instead of cutting the loss, they hold the position, thinking, "I have already lost too much to sell now; I will just wait for it to bounce back to breakeven" 29.

This "breakeven obsession" replaces objective analysis. Research into retail brokerage accounts shows that traders hold losing positions 1.5 to 2 times longer than winning positions, primarily because they refuse to accept the permanence of an overnight gap 29. The hold duration itself becomes the justification for continuing to hold. In the worst-case scenarios, traders will even "average down" by buying more shares of the plummeting stock to lower their cost basis, attempting to fight the market trend and turning a single gap-down disaster into a portfolio-destroying event 29.

Overcoming this requires strict journaling and post-trade analysis, forcing the trader to ask: "If I did not already own this stock, would I buy it at today's price?" If the answer is no, the sunk cost fallacy is likely dictating their behavior 29.

Regulatory Scrutiny: The Push for Extended Hours

As technology improves and retail participation in the markets grows, brokerage firms have increasingly pushed to stretch trading hours far beyond the traditional 9:30 a.m. to 4:00 p.m. window. Major brokerages like Charles Schwab and Robinhood have expanded their offerings, in some cases piloting 24-hour trading for retail clients, five days a week 3031.

While increased access is marketed as a convenience, regulatory bodies and behavioral economists have grown increasingly concerned about retail investors stumbling blindly into the risks of illiquid, extended-hours markets. The Financial Industry Regulatory Authority (FINRA) explicitly mandates through Rule 2265 (Extended Hours Trading Risk Disclosure) that broker-dealers must proactively highlight the specific dangers of trading outside regular hours to their clients 3032.

If a broker permits extended-hours trading, they must provide disclosures warning customers about several distinct, structural dangers: 1. Risk of Lower Liquidity: With fewer market participants actively trading, orders may be only partially executed, or ignored completely 13933. 2. Risk of Higher Volatility: Thinly traded stocks are prone to wild, exaggerated price swings, meaning the price can whip back and forth drastically on very low volume 323933. 3. Risk of Wider Spreads: The spread (the difference between what buyers are willing to pay and what sellers demand) expands significantly because market makers are not providing liquidity. This forces investors to pay a premium to enter or exit trades 3933. 4. Risk of Unlinked Markets: Prices displayed on one extended-hours ECN may not match prices on another concurrently operating system, leading to inferior pricing 323933. 5. Risk of News Announcements: Material news is typically released in extended hours, which, when combined with low liquidity, causes unsustainable and exaggerated price effects 33. 6. Risk of Changing Prices: The price of a security in extended hours may not reflect the price at the end of regular market hours, nor predict the price at the opening bell the next morning 3933.

Beyond the structural risks, behavioral finance experts warn against the psychological toll of 24-hour access. Removing the mandatory "cooling off" period provided by the overnight market closure invites impulsive, fatigue-driven decision-making 31. When an investor can react to an 8:00 p.m. news headline immediately from their smartphone, they are heavily reliant on emotional, "System 1" (fast) thinking, rather than the objective, "System 2" fundamental analysis required for sound long-term investing 31. The inability to "sleep on a trade" amplifies behavioral biases like herd behavior and return-chasing 31.

Defensive Tactics: How to Actually Mitigate Gap Risk

If standard stop-loss orders fail in the face of gap risk, and extended-hours trading is fraught with illiquidity, how can swing traders and long-term investors effectively protect their capital? Institutional professionals and seasoned retail traders rely on three primary, mathematically sound methods.

1. Position Sizing, Avoidance, and Diversification

The simplest and most effective way to mitigate gap risk is to avoid holding concentrated positions through known catalysts. Professional traders obsessively check economic calendars, earnings schedules, and FDA approval dates. If a company is slated to report earnings after the bell, many traders will reduce their position size or entirely liquidate the trade to avoid the 50/50 gamble of an earnings gap 341.

If they must hold a position overnight, they meticulously adjust their position size relative to the stock's historical volatility. A technical metric called the Average True Range (ATR) can be used as a proxy for potential overnight risk 9. For example, if a stock typically swings $10 a day (its ATR), a trader might model a worst-case overnight scenario as a 2x ATR move. If they hold 200 shares, they must be financially prepared to absorb a $4,000 hit ($10 x 2 x 200) if a severe gap occurs 9. By sizing the position so that a $4,000 loss represents only a tiny fraction of their total portfolio, the gap risk is neutralized 19.

For passive, long-term investors, the definitive solution is broad asset allocation and diversification. Holding a diverse mix of equities across varying market caps, sectors, and international borders, alongside fixed-income products like high-quality Treasury bonds, ensures that a catastrophic gap down in a single stock - or even a single sector - does not devastate the broader portfolio 3435. Diversification diffuses individual gap risk into manageable systemic exposure 35.

2. Options Hedging: The Protective Put

For active traders who wish to hold a specific stock overnight but demand absolute, contractual downside protection, the options market provides the ultimate solution. While standard stock options only trade during regular market hours, they act as binding legal contracts that are entirely immune to price gaps 9.

The most straightforward hedge is the Protective Put 363738. An investor who owns 100 shares of a stock trading at $100 can purchase a "put option" with a strike price of $90. A put option gives the buyer the right, but not the obligation, to sell their 100 shares at the strike price before a specific expiration date 373839.

Even if the stock announces bankruptcy after hours and gaps down to $20 overnight, the trader possesses the contractual right to exercise their put and sell their shares at $90. The protective put acts exactly like a true financial insurance policy for the portfolio 363839.

However, this insurance comes with significant drawbacks. Options cost money, known as the "premium." Buying insurance constantly can create a slow bleed on a portfolio's returns, known as "time decay," as the option loses value approaching expiration 37. Furthermore, if the stock goes up as desired, the put expires worthless, and the trader permanently loses the premium paid 37. Options are also subject to implied volatility; buying a put right before a major, highly anticipated earnings report will be exceptionally expensive because the market is already pricing in the gap risk 37.

3. Advanced Hedging: The Options Collar

To offset the high premium cost of buying a protective put, a trader can execute an advanced options strategy known as a Collar 3640.

In a collar strategy, the trader holds their 100 shares of stock and buys an out-of-the-money protective put to establish a hard floor against gap risk. Simultaneously, the trader sells an out-of-the-money call option (a covered call) 3640. The cash premium collected from selling the call option is used to partially or fully finance the purchase of the protective put 363940.

This strategy effectively rings the stock in a protective "collar." The downside is strictly capped by the put, but the trade-off is that the upside is also strictly capped by the short call. If the stock rockets upward on good news, the trader's shares will be called away at the short call's strike price, limiting their maximum profit 3840.

Summary of Gap Risk Mitigation Strategies

| Mitigation Strategy | Mechanism of Protection | Drawbacks and Limitations |

|---|---|---|

| Avoidance / Liquidation | Closing positions before the 4:00 p.m. bell or prior to known earnings catalysts 341. | Eliminates the possibility of profiting from positive gaps or overnight momentum 41. |

| Position Sizing (ATR) | Reducing share size so a worst-case gap (e.g., 2x ATR) does not breach total portfolio risk limits 19. | Limits total profit potential; requires constant mathematical adjustments as volatility shifts 19. |

| Protective Put | Buying a put option to establish a contractual floor price to sell shares, immune to gaps 363738. | The premium costs act as a drag on portfolio returns; subject to time decay and high volatility pricing 37. |

| Options Collar | Buying a protective put while simultaneously selling a covered call to offset the premium cost 3640. | Strictly caps the upside profit potential if the stock surges 3840. |

Bottom line

Overnight gap risk is the structural reality of a financial system that processes global news 24 hours a day but restricts peak liquidity to a 6.5-hour daily window. It renders traditional stop-loss orders useless, converting intended safety nets into disastrous market-order executions that lock in severe losses. While diligent position sizing, broad asset diversification, and contractual options hedging can effectively mitigate the damage, any investor who chooses to hold assets after the 4:00 p.m. bell must accept that their portfolio's value is entirely subject to instantaneous, uncontrollable revaluation by the time the sun rises.