Empirical and behavioral effects of stop-loss rules (2020 - 2024)

Introduction: The Paradigm Shift in Risk Management

For decades, the efficacy of dynamic risk management strategies has been a subject of intense academic and practitioner debate. The foundational work of Kaminski and Lo (2014) provided a robust quantitative framework demonstrating that stop-loss policies could theoretically add value by limiting downside exposure during prolonged bear markets, essentially acting as a momentum-based risk overlay. By systematically exiting positions during severe market contractions, investors could ostensibly bypass the most destructive phases of equity drawdowns, thereby improving long-term risk-adjusted returns. However, the structural evolution of global financial markets has necessitated a critical re-evaluation of these models. The proliferation of algorithmic trading, the shift toward zero-commission retail brokerage models, the rise of high-frequency trading (HFT), and the increasing frequency of exogenous macroeconomic shocks have fundamentally altered the market microstructure within which stop-loss orders operate.

The period between 2020 and 2024 served as an unprecedented global laboratory for testing the resilience of traditional risk-mitigation paradigms. Investors were subjected to severe, distinctly contrasting market regimes: the acute deflationary liquidity crisis triggered by the global COVID-19 pandemic lockdowns in early 2020, and the protracted, structurally embedded inflation shock of 2022, which aggressively dismantled the traditional diversification benefits of the classic 60/40 stock-bond portfolio construct 11. During these periods of heightened macroeconomic volatility, empirical observations revealed severe discrepancies between the theoretical expectations of stop-loss performance and their actual real-world execution. The idealized mathematical models of the previous decade repeatedly crashed against the harsh realities of liquidity dry-ups and structural market frictions.

Contemporary research, particularly from top-tier peer-reviewed finance publications such as the Journal of Portfolio Management and the Journal of Finance, alongside authoritative quantitative studies from established asset management firms like AQR and Research Affiliates, indicates that mechanical stop-loss strategies often fail to deliver excess risk-adjusted returns in modern environments 2345. The uncritical deployment of these tools exposes portfolios to a myriad of hidden implementation frictions, including severe whipsaw costs in mean-reverting environments, catastrophic slippage during overnight liquidity gaps, and the substantial, compounding drag of premature tax realization.

Simultaneously, the persistence of stop-loss strategies in both institutional proprietary trading and retail settings cannot be dismissed purely as mathematical ignorance or lack of sophistication. To fully comprehend their pervasive use, one must integrate the rigorous findings of modern market microstructure with the psychological realities of behavioral finance. Stop-loss orders provide a quantifiable "peace-of-mind" utility, addressing deep-seated cognitive biases such as regret aversion and the disposition effect. By outsourcing the critical exit decision to a pre-committed algorithm, investors preserve mental capital, which often proves critical in preventing catastrophic capitulation during extreme market drawdowns 786.

This comprehensive report systematically unpacks the mechanics, empirical performance, and behavioral underpinnings of stop-loss strategies and alternative risk overlays. By expanding the analytical scope to include international emerging markets, alternative asset classes such as cryptocurrencies and commodities, and a rigorous dissection of execution realities, this analysis bridges the gap between theoretical quantitative finance and practical portfolio implementation in the modern era.

The Illusion of Control: Execution Realities, Slippage, and Gap Risk

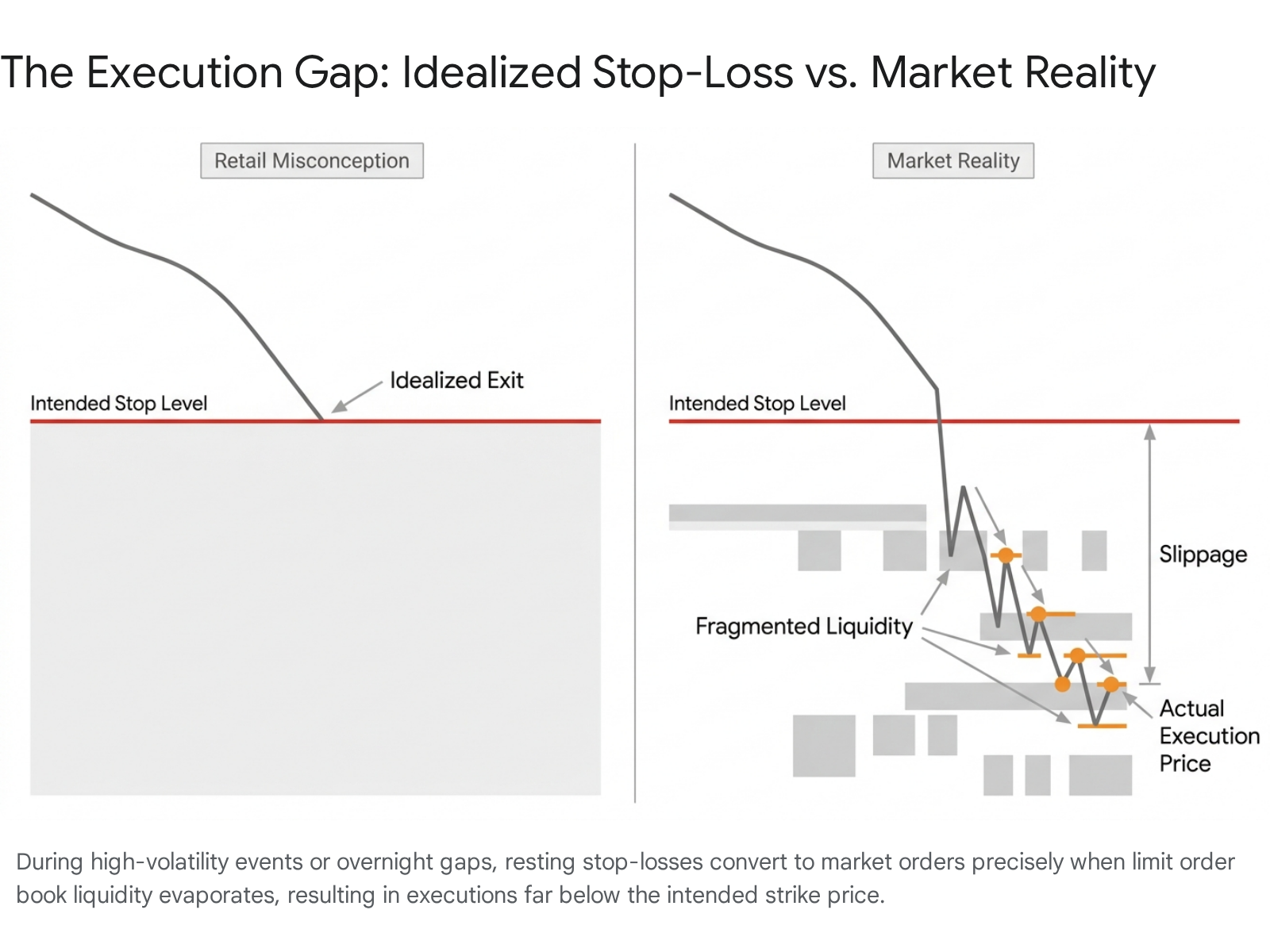

A pervasive and highly damaging misconception among retail and even some institutional market participants is the belief that a stop-loss order guarantees execution at the exact specified strike price. This theoretical assumption is deeply flawed, relying on idealized continuous-time finance models, and fundamentally ignores the mechanics of limit order books and the realities of market microstructure 7. From a strictly operational standpoint, a standard stop-loss is merely a conditional instruction: it rests dormant on a broker's server until the asset's price touches or crosses the predetermined threshold, at which point it immediately converts into an aggressive market order 11. In periods of normal, continuous liquidity and low volatility, the difference between the stop price and the execution price - known as slippage - is typically negligible, averaging one to three pips in major foreign exchange pairs and fractions of a cent in highly liquid large-cap U.S. equities 12.

However, risk management tools are specifically designed for abnormal market conditions, and it is precisely during these high-stress periods that the stop-loss mechanism catastrophically breaks down. When exogenous shocks hit the market - such as sudden geopolitical escalations, unexpected central bank rate adjustments, or black-swan events like the COVID-19 pandemic - liquidity rapidly evaporates. Market makers and high-frequency liquidity providers widen bid-ask spreads dramatically or withdraw their quotes entirely to protect their own books from toxic, one-sided order flow 1213. In these scenarios, the conversion of a stop-loss into a market order forces the execution algorithm to aggressively sweep the depleted order book to find any available buyer. This dynamic can result in executions that are significantly inferior to the intended strike price; for example, algorithmic modeling indicates that during volatility events, a planned 80-pip stop in forex markets can execute 37% to 62% worse than planned 12.

This dynamic is severely exacerbated by the phenomenon of gap risk, which constitutes the most severe execution failure for mechanical stops. Financial assets do not trade in continuous, unbroken price functions; they are subject to discrete, discontinuous jumps. Overnight sessions, weekend news events, and pre-market earnings announcements frequently cause assets to gap down at the open. If a security closes at a price of $\$100$ and a trader holds a stop-loss at $\$95$, adverse overnight news may cause the stock to open the following morning at $\$85$. The stop-loss is immediately triggered at the open, and the position is liquidated at $\$85$, resulting in a realized loss that far exceeds the investor's carefully calculated risk parameter 148. This reality directly mirrors the systemic failures observed during the 1987 Black Monday crash, where synthetic portfolio insurance - which operated mechanically as a giant, institutional stop-loss order - triggered cascading sell programs into an illiquid market, exacerbating the collapse rather than mitigating it 7.

From the perspective of quantitative finance and derivatives pricing, placing a stop-loss is economically equivalent to writing a short put option and surrendering its premium to the market makers without compensation 1216. When an investor places a stop order below the current market price, they are implicitly providing liquidity providers with a valuable embedded option - the right to execute against the investor's position during a downward volatility spike. In highly volatile regimes, the theoretical value of this embedded option is substantial. By utilizing traditional stop-losses instead of purchasing formal protective put options on a derivatives exchange, investors implicitly surrender this volatility premium while bearing the full brunt of execution risk, essentially paying the cost of insurance without receiving the contractual guarantee of a strike payout 129.

Implementation Frictions: Whipsaw Costs and the Tax Drag Imperative

Beyond acute execution failures during crises, the systematic implementation of stop-loss strategies introduces chronic, compounding frictions that steadily erode gross portfolio returns during normal market conditions. Chief among these structural inefficiencies are whipsaw costs and tax drag, two critical factors frequently omitted from idealized academic backtests but devastating in real-world application.

Whipsaw occurs when an asset's price briefly breaches a stop-loss threshold, triggering the liquidation of the position, only to immediately reverse course and resume its upward trajectory. The investor is thus forced to absorb the realized loss and is left entirely uninvested during the subsequent recovery, or must re-enter the position at a higher price point, incurring additional bid-ask spread costs and trading commissions 181920. This phenomenon is particularly acute in modern equity markets dominated by mean-reverting algorithms and high-frequency trading, where standard intraday volatility routinely triggers tight stop-loss orders.

A seminal empirical study by Baur and Dimpfl (2023), published in the Journal of Portfolio Management, rigorously tested the conventional wisdom of "cut your losses" strategies applied to large-cap U.S. equities 4. Utilizing an initial equal ($1/N$) weighting methodology across different portfolio sizes, the researchers found that virtually any iteration of a cut-your-losses strategy underperformed a simple buy-and-hold benchmark, reducing absolute returns while simultaneously increasing portfolio volatility 4. Their empirical analysis spanning periods including the 2008 financial crisis and the 2020 COVID-19 outbreak confirmed that because equity markets exhibit strong long-term upward drift, selling assets merely because they cross an arbitrary short-term loss threshold frequently results in locking in transient volatility rather than preventing permanent capital impairment 4. The study ultimately found no empirical evidence that holding onto losing stocks was detrimental over the long term, directly challenging the mathematical foundation of mechanical stops in structurally upward-trending markets 4.

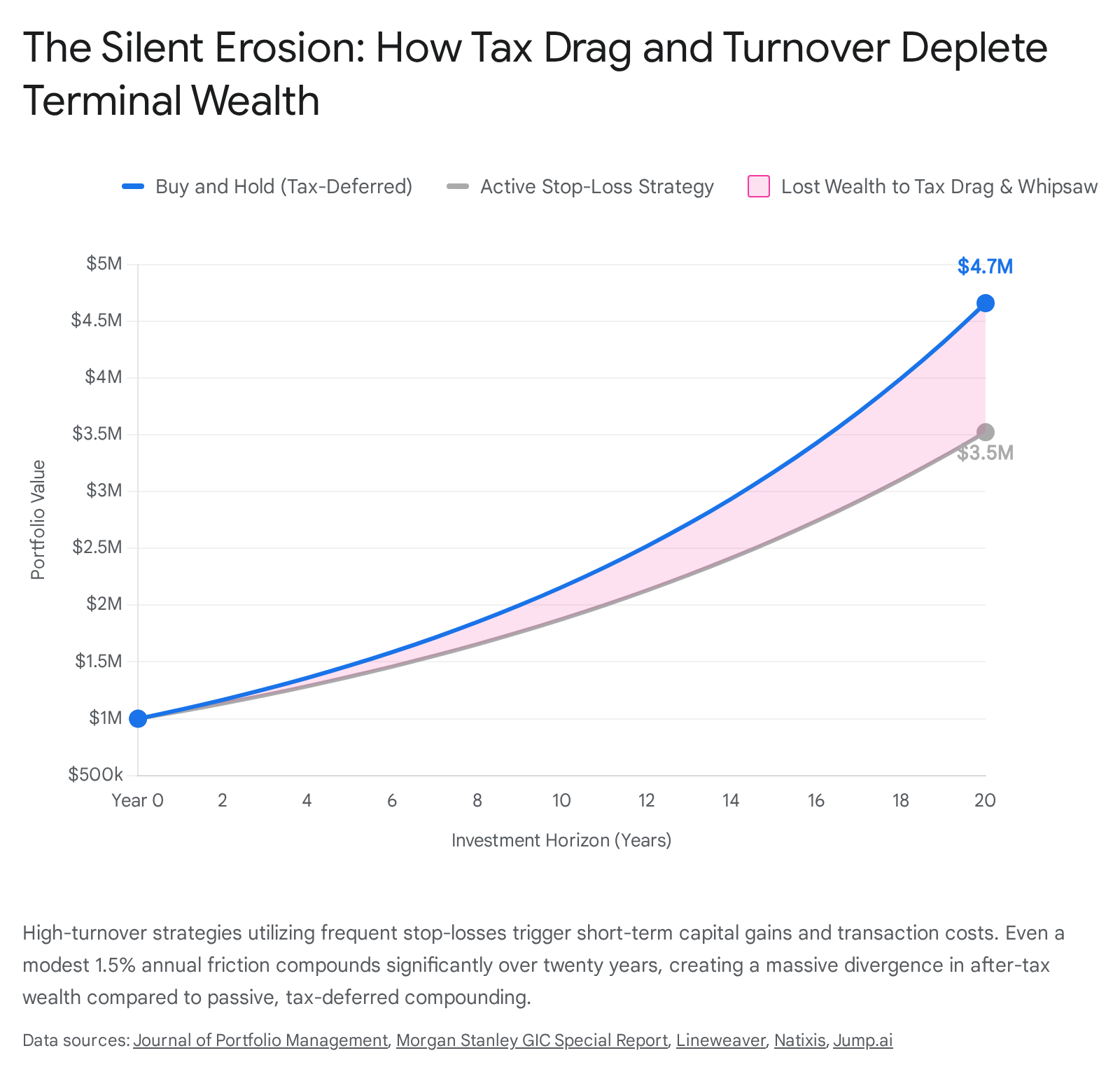

However, the most insidious implementation friction associated with stop-loss and momentum-based risk overlays is tax drag. For taxable investors, the cadence of capital gains realization is the primary determinant of long-term wealth compounding. Stop-loss strategies inherently increase portfolio turnover, transforming unrealized, tax-deferred growth into realized, taxable events 1011. When a trailing stop-loss is triggered on a position that remains in a net profitable state relative to its original cost basis, it forces the premature realization of capital gains 2312.

If the asset has been held for less than a year, these gains are subjected to punitive short-term capital gains tax rates, which align with ordinary income brackets and can exceed $37\%$ in the United States 25. Even for assets held longer than a year, the forced realization of long-term capital gains interrupts the exponential compounding process. Extensive quantitative research from institutions like J.P. Morgan and Morgan Stanley demonstrates that the tax drag associated with high-turnover active strategies and mechanical stop-loss implementations can reduce annualized net returns by $1.0\%$ to $2.5\%$ relative to tax-efficient, low-turnover indices 101314. Over a multi-decade investment horizon, a continuous annual tax drag of $1.5\%$ effectively eradicates the vast majority of excess gross returns generated by any alpha-seeking mechanism, potentially resulting in a terminal wealth difference of up to $50\%$ after 30 years 112930.

Consequently, modern tax-aware portfolio management increasingly favors direct indexing, systematic tax-loss harvesting, and strategic asset location over arbitrary stop-loss liquidation 301516. A sophisticated loss-harvesting framework deliberately offsets necessary gains with strategic loss realization, maintaining strict beta exposure while generating "tax alpha" 111417. In stark contrast, mechanical stop-loss orders operate with complete disregard for the investor's cumulative tax lot architecture, frequently generating disastrous tax outcomes by indiscriminately selling positions based on isolated price action rather than holistic portfolio optimization 1034.

The Behavioral Economics of Stop-Losses: The "Peace-of-Mind" Utility

If empirical evidence overwhelmingly suggests that stop-loss orders degrade long-term mathematical returns through whipsaw, slippage, and tax friction, their enduring popularity across all echelons of trading requires an explanation rooted outside classical financial models. Behavioral finance provides this necessary framework. Human beings are not perfectly rational, utility-maximizing automatons; their financial decision-making is deeply constrained by cognitive biases, emotional heuristics, and biological stress responses. Within this paradigm, the stop-loss order transcends its role as a mathematical tool and functions as a critical psychological defense mechanism.

The psychological foundation of the stop-loss is firmly anchored in Kahneman and Tversky's Prospect Theory, which established that human beings exhibit profound loss aversion 63536. Empirically, the emotional pain derived from a financial loss is approximately twice as intense as the psychological satisfaction gained from an equivalent financial gain 8. This severe asymmetry directly leads to the disposition effect - the widely documented and irrational tendency of investors to sell winning positions prematurely to lock in guaranteed psychological rewards, while holding onto losing positions to avoid finalizing the regret of a poor decision 8351838. As paper losses compound, investors often succumb to paralysis, holding deteriorating assets deep into a drawdown out of a desperate hope for mean reversion 836.

By establishing a mechanical stop-loss at the exact moment of trade entry, an investor effectively pre-commits to a disciplinary framework, neutralizing the toxic influence of the disposition effect 1839. The decision to exit the position is removed from the "heat of the moment" and delegated to a rigid algorithm 39. This pre-commitment effectively mitigates regret aversion, as the investor views the execution of the stop as a function of the systemic rule rather than a personal intellectual failure 8640.

Furthermore, contemporary behavioral literature has begun to quantify the "peace-of-mind" utility embedded within these risk controls 8641. While a purist mathematical approach argues that investors should simply endure high volatility to capture long-term equity risk premiums, this ignores the finite nature of human psychological endurance. Drawdowns consume what practitioners term "mental capital" 7. If severe portfolio volatility causes an investor to suffer from chronic anxiety, disrupting their sleep and professional efficacy, the mathematical optimization of the portfolio is entirely irrelevant 36. More dangerously, exhausted mental capital typically leads to capitulation at the exact point of maximum pessimism, locking in permanent, catastrophic losses right before a market recovery 739.

In this context, the fractional performance drag introduced by a stop-loss is not an inefficiency; it is an insurance premium paid in exchange for psychological stability. The "just feel safer" angle is entirely rational when viewed through a holistic subjective value inventory (SVI) that evaluates emotional well-being, disciplinary adherence, and the preservation of mental capital alongside terminal financial wealth 19.

Empirical Efficacy During Modern High-Volatility Events (2020 - 2024)

The theoretical debates surrounding stop-loss efficacy were subjected to extreme empirical stress tests during the exogenous macroeconomic shocks of the current decade. The 2020 COVID-19 crash and the 2022 global inflation shock provided distinctly different market environments, both of which exposed the vulnerabilities of traditional mechanical risk mitigation.

The market collapse in February and March of 2020 was characterized by an unprecedented velocity of decline, driven by an acute deflationary and liquidity shock as global economies locked down. During this period, correlations across almost all asset classes converged toward one, and secondary market liquidity rapidly evaporated. Empirical studies tracking investor behavior during this crash - including Vanguard survey data analyzed by Maggiori et al., correlated with actual retail and institutional trading portfolios - revealed that while investor expectations of economic disaster skyrocketed, institutional and retail stop-loss execution was highly problematic 20. Because the market gapped down aggressively over weekends and overnight sessions as pandemic news worsened, mechanical stop-losses were frequently executed at severe discounts to their strike prices, suffering massive slippage 48.

Moreover, the subsequent, unprecedented intervention by the Federal Reserve and global central banks catalyzed a historic, V-shaped recovery. Investors whose portfolios were liquidated into cash at the market trough by rigid stop-loss parameters found themselves entirely uninvested during the most aggressive rally in modern history. This exact scenario validates the findings of Baur and Dimpfl (2023), who demonstrated that during the COVID-19 outbreak, strategies explicitly designed to cut losses systematically failed to capture the subsequent upside momentum, resulting in severe long-term underperformance compared to those who simply held their positions through the volatility 4.

The market environment of 2022 presented an entirely different mechanism of failure for stop-losses. Unlike the rapid deflationary crash of 2020, 2022 was defined by a protracted, grinding bear market induced by sticky global inflation, supply-chain disruptions from the war in Ukraine, and aggressive monetary tightening by central banks 21222347. This supply-side inflation shock broke the fundamental premise of the modern 60/40 portfolio: the assumption that sovereign bonds would act as a non-correlated safe haven when equities declined 1. As interest rates surged to combat inflation, both fixed income and equity markets collapsed simultaneously 1.

In this prolonged regime, AQR researchers noted that while pure trend-following strategies and managed futures (CTAs) exhibited significant outperformance by successfully shorting the global fixed-income complex and riding the downward momentum, standard trailing stop-loss strategies applied to long-only equity portfolios suffered immensely 2320. Because the 2022 bear market was characterized by violent, short-lived bear-market rallies (whipsaws) amidst a broader downward channel, trailing stops were repeatedly triggered near local bottoms, only for the portfolio to re-enter during false rallies and be immediately stopped out again 48. The structural regime of 2022 highlighted that inflation-driven sell-offs create uniquely hostile environments for passive stop-loss triggers, demanding active, dynamic macro overlays rather than static percentage thresholds 2.

Market Regimes: A Matrix of Strategic Viability

The ultimate success or failure of any risk mitigation strategy is entirely contingent upon the prevailing market regime. Advanced quantitative trading systems do not deploy static rules; they dynamically adjust parameters based on underlying measurements of trend persistence, volatility expansion, and correlation structure 492451.

Markets generally oscillate between two primary states: trending (momentum-driven) and ranging (mean-reverting). In a strongly trending market, asset prices exhibit positive serial correlation, meaning past positive returns predict future positive returns, and vice versa. In this environment, trend-following and volatility-adjusted trailing stop-losses excel. They allow the investor to capture the asymmetric upside of the trend while guaranteeing an exit when the macroeconomic narrative fundamentally shifts 4851.

Conversely, in ranging or mean-reverting regimes, price action behaves like a rubber band, constantly oscillating around a moving average without establishing clear long-term directionality. In such environments, the deployment of tight stop-losses guarantees mathematical failure 748. The natural volatility of the asset will constantly trigger the stop-loss order at the lower bound of the range, effectively forcing the investor to sell at the localized bottom just before the price reverts upward 485253. Thus, utilizing a strict stop-loss in a mean-reverting environment explicitly ensures that the investor will buy high and sell low in perpetuity.

To manage this stability-reactivity tradeoff, sophisticated practitioners rely on regime filters such as the Average Directional Index (ADX) and the VIX to deploy risk controls selectively 485154. The impact of these regimes on expected net returns can be clearly mapped to guide strategic deployment.

Expected Net-Return Impact of Stop-Loss Rules Across Market Regimes

| Market Regime Dynamics | Identifying Characteristics (Quantitative Indicators) | Expected Stop-Loss Net Return Impact | Execution Mechanics & Frictions Encountered | Optimal Risk Overlay Approach |

|---|---|---|---|---|

| High-Trend / Low-Volatility | ADX > 25, clear moving average slopes, low VIX (typically < 15) 4851. | Highly Positive | Captures the bulk of the directional move. Infrequent triggering minimizes tax drag and transaction costs. | Trailing Stops / Trend-Following. Allows profits to run while locking in mathematical floors 4851. |

| High-Trend / High-Volatility | ADX > 30, VIX > 25, wide and expansive price channels. | Neutral to Positive | Prevents catastrophic loss during violent paradigm shifts, but vulnerable to intraday shakeouts if stops are placed too tight. | Volatility-Adjusted Stops (ATR). Stops must be placed multiple standard deviations away from the mean to survive normal market noise 3953. |

| Mean-Reverting / Low-Volatility | ADX < 20, price oscillating tightly between defined support and resistance 4851. | Negative | Stops are repeatedly triggered at range boundaries. High transaction costs and opportunity cost from missing the reversion. | Time-based exits or Options Overlays. Yield harvesting (e.g., covered calls, iron condors) is preferred over directional stops 5254. |

| Mean-Reverting / High-Volatility | VIX > 30, erratic macro headlines, violent and sudden bear-market rallies. | Severely Negative | Catastrophic whipsaw. Generates maximum tax drag (short-term losses) while systematically buying tops and selling bottoms. | Broad Diversification & Position Sizing. Reduce exposure dynamically across uncorrelated assets rather than relying on price-based stops 2053. |

Geographic and Asset Scope: Evaluating EMs, Crypto, and Commodities

The contemporary debate surrounding stop-loss efficacy is heavily skewed by its predominant focus on U.S. large-cap equities. The U.S. market has benefited from an extraordinary 15-year period of exceptionalism, buoyed by the hegemony of the U.S. dollar, massive liquidity injections, and the outsized performance of mega-cap technology firms 252627. In a market that structurally drifts upward with minimal permanent impairment to its major indices, stop-losses inevitably underperform buy-and-hold strategies 4. However, expanding the analysis to other geographic regions and asset classes reveals vastly different structural realities.

Emerging Markets (EMs)

Emerging market equities and sovereign debt operate under fundamentally different macroeconomic constraints than U.S. assets. They are highly sensitive to U.S. monetary policy, dollar strength, external debt burdens, and localized political instability 25262829. Historically, EMs have suffered severe, multi-year drawdowns during crises (e.g., the Asian Financial Crisis, local currency devaluations) from which they do not quickly V-shape recover 25. During the 2022 global inflation shock, emerging markets with weak monetary institutions and high currency devaluation proved highly vulnerable, leading to massive capital outflows 60. Consequently, the volatility inherent in EM equities is significantly higher, and the risk of permanent capital impairment is very real.

In these environments, risk mitigation is not just a psychological comfort; it is a mathematical necessity. Quantitative research indicates that applying a volatility-reduction overlay - such as a trend-following stop or long/short dynamic allocation - to EM equities can drastically improve the Sharpe ratio by avoiding multi-year structural declines 30. Because EMs frequently experience prolonged bear markets due to capital flight, cutting losses early and shifting to cash or U.S. dollar proxies preserves capital effectively. Interestingly, post-2024, as U.S. policy exhibits increased volatility, debt burdens mount, and EM valuations sit at near 40% discounts to the U.S., institutional analysts observe a potential convergence in risk profiles, suggesting that the relative necessity of stops in EMs versus the U.S. may begin to equalize 25262729.

Cryptocurrencies and Decentralized Finance

The cryptocurrency ecosystem provides the ultimate stress test for risk management tools. Operating 24/7 with extreme inherent volatility, minimal regulatory oversight, and highly leveraged participants, digital assets routinely experience breathtaking crashes. During the 2022 macroeconomic tightening, crypto assets definitively failed to act as a hedge against inflation, behaving instead as hyper-sensitive risk assets heavily correlated with U.S. tech stocks 116062. The collapses of the Terra/Luna algorithmic stablecoin ecosystem and the FTX exchange wiped out over $1.8 trillion in value, wiping out millions of retail investors and demonstrating the existential threat of "holding the bag" during systemic failures 131.

However, the efficacy of stop-loss orders in crypto is highly compromised by the structural prevalence of "stop-hunting" and liquidation cascades. Because crypto derivative platforms offer massive leverage, well-capitalized market makers and institutional participants frequently drive prices down through highly visible technical support levels specifically to trigger resting retail stop-loss orders 112. This forced selling creates a cascading effect, liquidating billions of dollars in open interest in a matter of minutes - such as the $917 million wiped out in a single 24-hour episode in mid-2024 1. An investor using a standard stop-loss in crypto is virtually guaranteed to be executed at the absolute bottom of a flash crash, right before the asset instantly rebounds. In crypto, strict position sizing and cold-storage custody act as vastly superior risk mitigants compared to mechanical price stops.

Commodities

Unlike equities, which have a theoretical baseline of zero and infinite upside, commodities are physically constrained assets subject to the immutable laws of supply and demand, storage costs, and geopolitical embargoes 20. Commodity markets are uniquely suited for trend-following and momentum overlays rather than static stop-losses 64. Because shocks to supply (such as the 2022 energy crisis) create persistent, structural trends, systematic trend followers (CTAs) routinely capture massive returns by utilizing wide, volatility-adjusted trailing stops (ATR stops) 2064. However, investors must be acutely aware of the futures curve structure. A static stop-loss on a commodity ETF often fails to account for the severe negative roll yield (friction) generated when futures are in contango, which decays the asset price independently of spot market movements 20.

Comparative Analysis of Risk-Mitigation Strategies

Given the myriad implementation frictions associated with basic stop-loss orders, institutional portfolios rely on a spectrum of alternative risk overlays. Each carries distinct mechanical advantages and associated costs. To build a robust portfolio, investors must graduate from the binary "hold vs. sell" mentality of a fixed stop and evaluate strategies based on their Greek exposures - specifically, their sensitivity to time decay (theta), volatility (vega), and the velocity of price movement (gamma) 12169.

Mechanics, Pros, and Cons of Alternative Risk-Mitigation Overlays

| Risk Mitigation Strategy | Mechanical Operation | Key Advantages | Primary Frictions / Disadvantages |

|---|---|---|---|

| Fixed Stop-Loss | Sells automatically at a predetermined absolute price level upon execution of a market order 1139. | Simple to implement, enforces discipline, prevents catastrophic, total loss of capital in single-stock events. | Extreme vulnerability to gap risk, slippage, and whipsaw. Creates massive tax drag via premature realization 1234. |

| Trailing Stop (Volatility-Adjusted) | Stop level moves upward dynamically as the asset price rises, usually calculated via Average True Range (ATR) multiples 113964. | Allows winners to run; adapts to the asset's inherent volatility signature, preventing noise-based exits 5364. | In severe bear markets characterized by sharp false rallies, it will constantly trigger at local bottoms. Still suffers from gap execution risk 3448. |

| Options Hedging (Protective Puts) | Purchasing a put option below the current spot price, establishing a guaranteed mathematical floor 14965. | Absolute gap protection. The investor holds a contractual guarantee of the strike price regardless of liquidity dry-ups or overnight crashes 9. | High ongoing cost (insurance premium). Investor constantly bleeds time decay (theta) and pays a premium for implied volatility 16. |

| Trend-Following / Momentum Overlay | Utilizing moving average crossovers or time-series momentum signals to dynamically scale exposure up or down 166667. | Shifts capital to defensive assets (cash, bonds, commodities) systematically. Re-enters markets when conditions stabilize 1967. | Exhibits negative vega (suffers heavily when markets chop sideways). Difficult to execute effectively in non-tax-advantaged accounts due to high turnover 1666. |

| Mean-Variance-Leverage / Position Sizing | Limiting initial capital exposure to 1-2% of total equity per position, relying on portfolio-level diversification 73968. | Mathematically bounds risk at the portfolio level without relying on unpredictable secondary market liquidity for exits 68. | Requires a massive capital base to effectively diversify. Caps upside exposure by demanding severe fragmentation of bets 739. |

As detailed above, there is no risk mitigation strategy that does not extract a toll. Options hedging provides a perfect, contractual barrier against the liquidity failures of a flash crash, but requires the investor to continuously bleed capital to options writers via theta decay 169. Trend-following is mechanically cheaper to implement than purchasing continuous options, but it leaves the investor directly exposed to short-term volatility and the severe whipsaw costs associated with ranging markets 16. The ultimate decision rests on matching the specific tool to the investor's tax environment, liquidity needs, and psychological tolerance for drawdowns.

Conclusion

The post-2020 financial landscape unequivocally demonstrates that the uncritical reliance on mechanical stop-loss orders is a hazardous practice, particularly for long-term investors operating in taxable accounts. While theoretical models may project downside protection, the reality of fragmented limit order books, high-frequency mean reversion, and sudden liquidity gaps frequently converts the idealized stop-loss into a mechanism that locks in slippage and crystallizes massive tax liabilities. The empirical record - highlighted by the failure of mechanical stops to navigate the V-shaped recovery of the 2020 COVID crash and the grinding whipsaw of the 2022 inflation shock - proves that attempting to cure market volatility with rigid price triggers often degrades gross portfolio returns. In systematically upward-drifting markets like U.S. equities, cutting losses arbitrarily leads to verifiable, long-term mathematical underperformance.

However, to dismiss the stop-loss entirely is to ignore the profound insights of behavioral finance. Financial models assume a mathematically infinite threshold for pain, whereas human investors possess finite mental capital. The profound asymmetry of loss aversion and the paralysis of regret dictate that without pre-committed disciplinary frameworks, investors will inevitably succumb to emotional decision-making at the most inopportune moments, leading to catastrophic capitulation. The stop-loss, therefore, functions not as an alpha-generating financial derivative, but as a psychological prophylactic - a tax paid in the form of whipsaw and slippage in exchange for the "peace-of-mind" utility required to remain engaged in the markets over a lifetime.

Ultimately, sophisticated portfolio management demands a graduation from static stops to dynamic, regime-aware risk overlays. In highly efficient markets, risk is better managed through stringent initial position sizing, broad asset class diversification, and strategic tax-loss harvesting. Conversely, in structurally volatile arenas such as emerging markets, cryptocurrencies, and commodities, dynamic trend-following methodologies calibrated to asset-specific volatility metrics provide a vastly superior framework for preserving capital. By acknowledging the explicit trade-offs between execution reality, tax friction, and behavioral endurance, practitioners can construct resilient portfolios capable of withstanding the inevitable exogenous shocks of the modern financial era.