What Is a Stop-Loss Order and Why You Need One

A stop-loss order is an automated instruction placed with a brokerage to execute a trade once a security reaches a specific price, effectively capping the maximum potential loss on an investment. It is the core of staying in the game because it enforces strict mathematical risk management, preventing routine market fluctuations from snowballing into catastrophic drawdowns that mathematically decimate a portfolio. By removing human emotion and hesitation from the exit process, a stop-loss acts as a trader's ultimate safety net in an inherently unpredictable market environment.

In the fast-moving world of financial markets, protecting capital is often more critical than generating outsized returns. Whether you are a retail day trader, a long-term equity investor, or an institutional portfolio manager, understanding how to manage downside risk is the fundamental difference between longevity and ruin. The stop-loss order serves as the foundational tool for this protection, yet its mechanics, behavioral benefits, and hidden vulnerabilities are frequently misunderstood by participants.

The Mechanics of Stop-Loss Orders

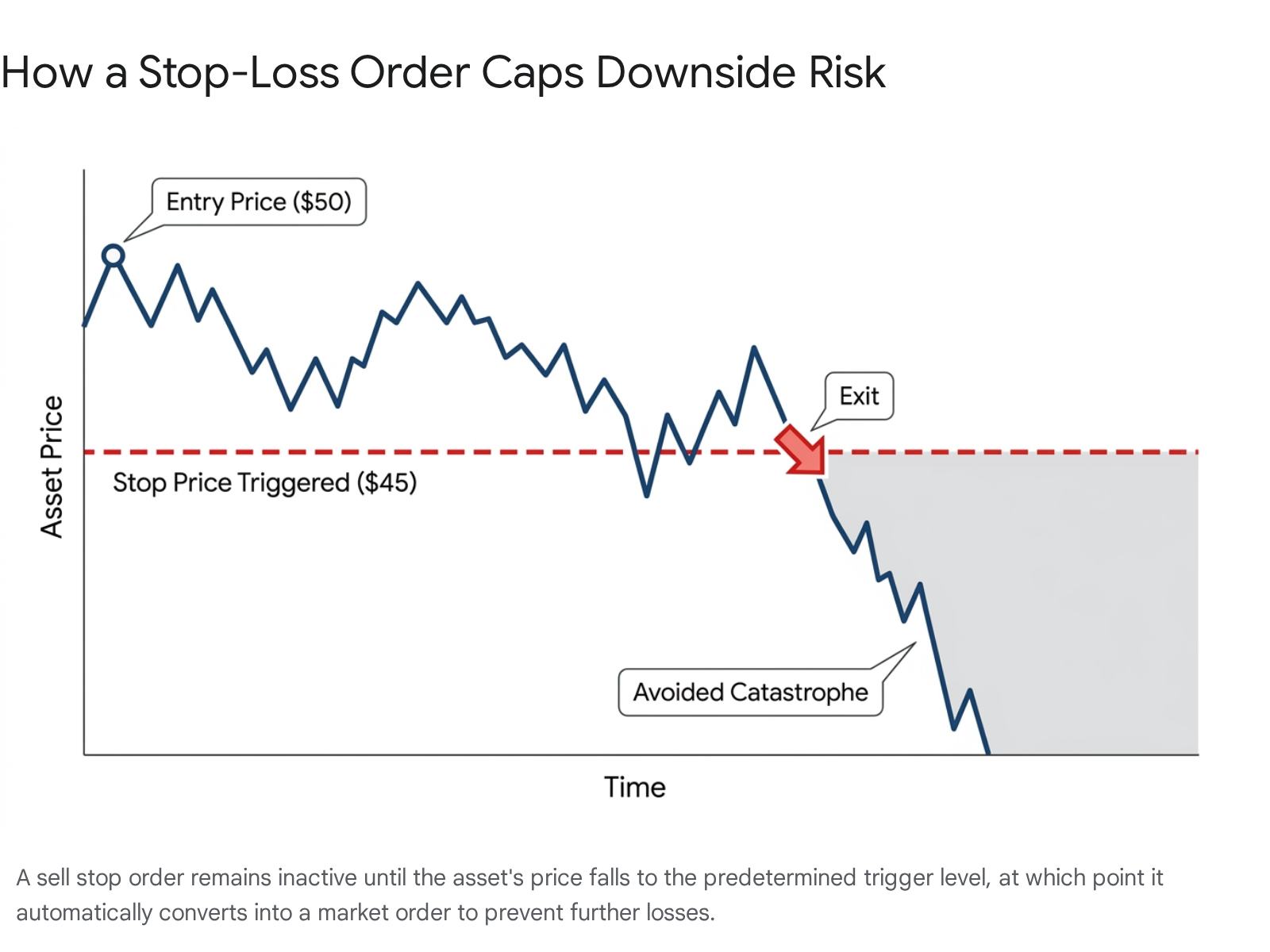

A stop order - often colloquially referred to as a stop-loss - remains dormant on a broker's order book until the market price of an asset hits a designated threshold, known as the "stop price" or "trigger price" 122. When the market trades at or through this price, the condition is met, and the dormant instruction is activated.

If an investor purchases a stock at $50 per share, they might place a sell stop order at $45 to limit their risk. As long as the stock remains above $45, the order does nothing 24. If the market turns and the stock price drops to $45, the stop order is immediately triggered, attempting to liquidate the position to prevent the investor from riding the stock down to $30 or lower 45.

While most commonly utilized as a "sell stop" to protect long positions - assets you own and hope will appreciate - traders routinely use "buy stop" orders to limit losses on short positions 2345. A short seller borrows and sells an asset, hoping its price declines so they can repurchase it cheaper later. If a short seller shorts a stock at $100, they face theoretically infinite risk if the stock rallies. To protect against this, they might place a buy stop at $110 296. If the market rallies against their thesis, the broker automatically repurchases the shares at the $110 threshold to halt the financial bleeding 24.

Comparing Stop Order Variations

The term "stop-loss" is essentially an umbrella phrase. In practice, market participants must define the precise execution behavior of the order. The three primary variations dictate exactly how the brokerage handles the trade once the trigger price is hit, presenting traders with different trade-offs between guaranteed execution and guaranteed pricing.

| Order Type | Execution Mechanism | Execution Guarantee | Price Guarantee | Best Use Case |

|---|---|---|---|---|

| Stop-Market | Converts to a standard market order, executing immediately at the next available bid or ask price 245. | Yes. Unless trading is fully halted by an exchange, the order will fill 14. | No. In fast markets, the fill price can be significantly worse than the trigger due to slippage 255. | Liquid markets where exiting the position immediately is more critical than receiving the exact expected price 21112. |

| Stop-Limit | Converts to a limit order. It will only execute at the specified limit price, or better 2478. | No. If the market drops past the limit price before filling, the trader is left holding a falling asset 2479. | Yes. You will not be filled at a price worse than your defined limit parameter 478. | Exiting positions where price control is paramount, provided the market is not prone to sudden overnight price gaps 21116. |

| Trailing Stop | A dynamic stop that automatically adjusts upward by a fixed percentage or dollar amount as the asset price rises 211710. | Yes. It executes as a market order once the trailing distance is breached by a reversal 27. | No. Subject to normal market slippage upon execution, identical to a stop-market order 24. | Letting winning trades run and locking in profits dynamically without needing to manually adjust the order daily 1181018. |

If you place a basic stop-market order at $45, and the market is moving quickly, the actual executed price might be $44.95 or $44.80. This discrepancy is known as "slippage" - the difference between the expected trigger price and the actual fill price 2411. Slippage is an inherent cost of demanding immediate liquidity in a fast-moving environment.

Conversely, a stop-limit order demands two price parameters: a trigger and a limit. A trader might set a stop price at $45 and a limit price at $44.50 2420. This effectively tells the broker to trigger the sale at $45, but absolutely refuse to sell for a penny less than $44.50 812. The spread between these two numbers is critical; a narrow spread increases the probability that the order will not execute at all during a fast drop, leaving the investor fully exposed as the stock crashes past their limit 24922.

Trailing stops offer an elegant solution for trend-following investors who wish to protect unrealized gains without capping their upside. If a trader buys a stock at $100 and sets a 10% trailing stop, the initial exit level is $90 6117. If the stock climbs to $130, the trailing stop automatically recalculates and moves the exit floor up to $117 11. If the stock subsequently drops 10% from its peak, the broker executes the sale, securing the profit 1112810.

The Mathematics of Drawdowns and Survival

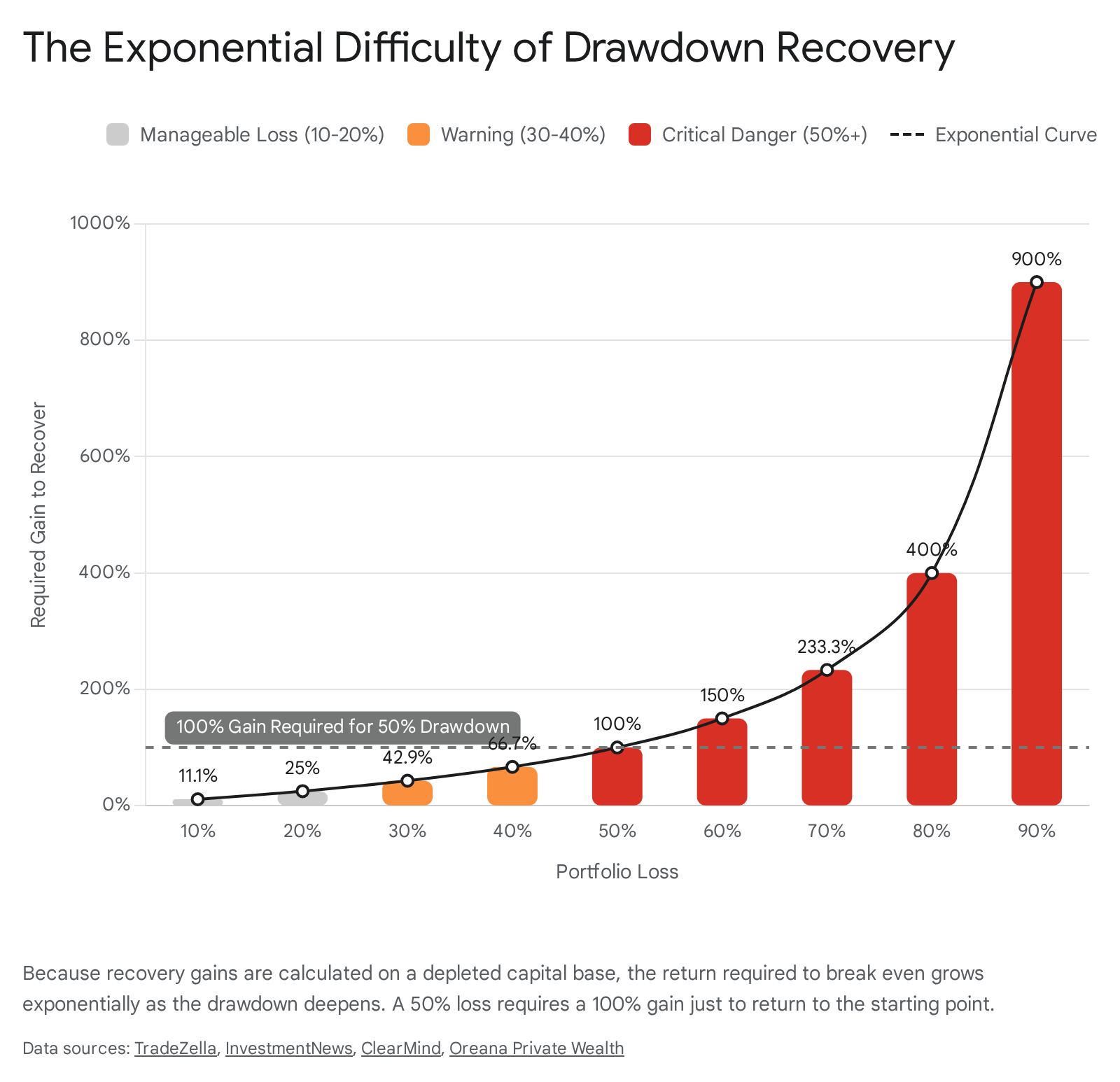

The overarching importance of a stop-loss is rooted in the unforgiving mathematics of investment drawdowns. A drawdown is defined as the peak-to-trough decline of a portfolio, usually expressed as a negative percentage 23131426. The math behind recovering from a loss is deeply asymmetric, meaning that recovering capital is significantly harder than losing it.

Because a portfolio recovers from a newly depleted base, the percentage gain required to break even is always larger than the percentage loss originally incurred 231326. This concept is often referred to as drawdown asymmetry or the Law of Large Losses 2627.

If an investor begins with $50,000 and loses 10% ($5,000), they are left with $45,000 23. To return to the initial $50,000 mark, they must gain $5,000 on their new $45,000 base. This requires an 11.1% gain, which is a painful but manageable recovery 23.

However, the required recovery gap widens exponentially the deeper the drawdown becomes, creating a mathematical point of no return for unhedged portfolios 23132627.

| Portfolio Loss (Drawdown) | Retained Capital (From $50,000 Base) | Required Gain to Recover | Severity & Estimated Trades to Recover |

|---|---|---|---|

| 5% | $47,500 | 5.3% | Normal (~10 trades) 23 |

| 10% | $45,000 | 11.1% | Manageable (~22 trades) 2313 |

| 20% | $40,000 | 25.0% | Warning (~50 trades) 2313 |

| 30% | $35,000 | 42.9% | Severe (~110 trades) 231326 |

| 40% | $30,000 | 66.7% | Critical (~170 trades) 2313 |

| 50% | $25,000 | 100.0% | Near-Impossible (~250+ trades) 231326 |

| 75% | $12,500 | 300.0% | Account Reset / Ruin 2627 |

If an investor refuses to cut a losing trade and suffers a 50% drawdown, the required gain to simply break even is 100% 23132627. If the portfolio bleeds to a 70% loss, it requires a staggering 233.3% gain to recover, an achievement bordering on the impossible for the vast majority of retail participants 2326.

A hard stop-loss prevents an investor from ever crossing this mathematical point of no return 2313. Historical market research demonstrates that avoiding deep drawdowns is vastly more important to long-term compounding growth than any specific strategy for picking winning stocks 2313.

Position Sizing and the One Percent Rule

Professional traders operationalize stop-losses using rigorous risk management frameworks, the most common being the fixed fractional method, heavily associated with the "1% risk rule." This rule dictates that a trader should limit their total exposure so they never risk losing more than 1% to 2% of their total account capital on a single trade 282930.

Position sizing is mathematically impossible without first determining a stop-loss level. The stop-loss is the anchor variable in the equation 2829. If a trader holds a $50,000 account, a 1% risk threshold limits their maximum allowable loss on the next trade to exactly $500 2829.

The trader identifies a promising stock trading at $150 per share. Technical analysis suggests that if the stock falls below recent support at $145, the trade thesis is invalidated 281516. By placing a stop-loss at $145, the trader isolates a risk of exactly $5 per share. To discover the correct position size, the trader divides the total risk budget ($500) by the risk per share ($5), arriving at exactly 100 shares 2830.

This systematic approach entirely removes guesswork. It ensures that the market structure, rather than the trader's emotional conviction, dictates the appropriate size of the investment 293016. Limiting each loss to 1% provides immense operational longevity. A trader would have to endure 100 consecutive losing trades to wipe out their capital, an event statistically unlikely for anyone employing a sound methodology 293017.

Adjusting for Volatility with Average True Range

Setting the stop-loss level is a delicate art governed by market volatility. Placing a stop too close to the entry price - a "tight stop" - often results in the trade being prematurely closed by normal, random market noise before the intended trend can develop 535181920.

To combat being "whipsawed" out of good trades, technical analysts frequently utilize the Average True Range (ATR). The ATR is an indicator that measures a security's historical volatility by calculating the average range of its price movement over a set period 1828152140.

By incorporating the ATR, a trader ensures their stop-loss sits safely outside the asset's normal daily fluctuations 282140. If a stock is trading at $100 and its ATR is $2, the trader knows the stock routinely swings by two dollars a day 40. Instead of setting an arbitrary stop at $99, which is highly likely to be triggered by standard market noise, the trader might set their stop at 1.5 or 2 times the ATR, placing the safety net at $97 or $96 2140. This dynamic risk management technique allows the market to breathe while strictly enforcing capital protection 182140.

The Behavioral Finance of the Stop-Loss

Beyond the strict mathematics of capital preservation, a stop-loss functions as a psychological defense mechanism. Behavioral finance, an academic discipline merging psychology and economics, demonstrates that human beings are fundamentally irrational when processing financial gains and losses 22424344.

According to Prospect Theory - pioneered by behavioral economists Daniel Kahneman and Amos Tversky - investors suffer from "loss aversion." The psychological pain experienced from losing a sum of money is perceived as roughly twice as intense as the joy derived from gaining an equivalent amount 22434445.

This deep-seated cognitive bias leads directly to a phenomenon known as the "disposition effect." The disposition effect describes the widespread tendency for investors to quickly sell winning assets to lock in the emotional satisfaction of a profit, while stubbornly holding onto losing assets in the desperate hope that the market will reverse 434423. Without a predefined exit strategy, a trader watching a position bleed capital will experience denial, fear, and ego, whispering justifications like "it's just a market dip" or "I'll sell the moment it gets back to breakeven" 4748495024.

A hard, automated stop-loss removes this emotional burden entirely 5184524252627. By determining the exit point prior to entering the trade, the investor creates necessary psychological distance from the outcome, transforming an emotionally charged moment of panic into a predetermined business expense 45495556. Research analyzing stock market participants indicates that implementing ordinary stop losses significantly counteracts the reluctance to realize losses, effectively shutting down the behavioral biases that lead to portfolio ruin 2356.

Mental Stops Versus Hard Physical Stops

In trading circles, a persistent debate exists between the use of automated broker-held stop-losses and "mental stops." A mental stop is an unofficial price level a trader monitors manually, intending to execute the sale themselves if the price drops to their threshold 5485027.

The primary advantage of a mental stop is flexibility 18482757. It allows the trader to assess the broader context of a price drop. If the dip appears to be a temporary algorithmic blip rather than a fundamental shift in the asset's valuation, they retain the option to hold the position and wait for a recovery 502757. Some financial literature argues that extremely tight, hard stop-losses can inadvertently harm long-term performance by truncating market exposure and causing the portfolio to miss out on eventual massive gains due to being constantly stopped out 1928.

However, mental stops harbor severe drawbacks for the average investor. They demand unwavering discipline and constant, exhausting screen monitoring 485057. When a market begins to plummet violently, traders relying on mental stops often experience decision paralysis. Caught like a deer in headlights, they fail to pull the trigger out of shock, allowing what should have been a minor, manageable loss to spiral into a catastrophic account drawdown 484957. Hard physical stops resting on the broker's servers execute automatically, offering fixed risk and entirely removing the possibility of emotional self-sabotage 18484957.

The Stop-Loss Analogy: Corporate Insurance Risk

To fully conceptualize the role of a stop-loss, it is helpful to examine how major institutions utilize the exact same mathematical concept outside of the stock market.

When mid-to-large companies decide to self-fund their employee health insurance - meaning the company pays medical claims directly out of their operating budget rather than paying fixed premiums to a traditional carrier - they face a terrifying vulnerability 29606162. What happens to the company's financial stability if a single employee requires a highly complex, $1,000,000 life-saving surgery? 29606162

To stay in the game and avoid bankruptcy, these self-funded companies purchase "Medical Stop-Loss Insurance" 2960616263. The company agrees to pay all medical claims up to a specific deductible, such as $50,000 per employee. If an employee's medical bills hit $51,000, the specific stop-loss coverage triggers, and the insurance carrier reimburses the company for every single dollar above the initial threshold 29606130. Furthermore, companies can purchase aggregate stop-loss insurance, which caps the maximum liability for the entire health plan over the course of the year, regardless of individual claims 6061633031.

This insurance structure is identical in purpose to a trading stop-loss. It does not prevent the entity from taking expected routine losses; it enforces a hard mathematical ceiling on financial liability, guaranteeing that standard operational costs do not escalate into catastrophic ruin 29606232.

The Vulnerabilities: Slippage and Market Gaps

While stop-loss orders are the indispensable cornerstone of financial risk management, they are not foolproof guarantees. Modern financial markets, dominated by algorithmic trading and split-second volatility, can easily exploit or bypass the mechanical nature of these orders.

The greatest inherent weakness of a standard stop-loss order is "gap risk." Financial charts often appear as smooth, continuous lines, but prices regularly jump abruptly from one level to another without any trading occurring in between 9116768.

When the traditional stock market closes at 4:00 PM EST, information continues to flow through the real world. If a company announces disastrous earnings results after hours, or if a major geopolitical conflict erupts over the weekend, the stock will invariably "gap down" when the market reopens the following morning 13911356768.

If a stock closes on Friday at $100, and an investor has a stop-loss resting at $95, a devastating weekend news cycle might cause the stock to open on Monday at $80. Because the stop-loss order is only eligible to trigger when the market is open and actively trading, the broker's system realizes the price is well below $95 the moment the opening bell rings. The stop instantly converts into a market order, selling the shares at the next available price - $80 59116768. The investor suffers immense slippage, absorbing a loss far more severe than their risk management plan dictated 9116869.

The Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) have repeatedly issued warnings regarding these dynamics. FINRA Regulatory Notice 16-19 and 21-12 specifically instruct brokerage firms to prominently disclose to retail investors that stop prices are not guaranteed execution prices, and that rapid intraday market moves or weekend gaps can result in executions significantly worse than the stated stop level 451270.

Flash Crashes and Structural Market Failures

Stop-loss orders can also fail spectacularly during "flash crashes" - rare but devastating events where asset prices plummet wildly in a matter of minutes due to sudden liquidity vacuums and cascading algorithmic sell-offs 3334357475.

The 2010 U.S. Equity Flash Crash

On May 6, 2010, the Dow Jones Industrial Average plunged nearly 1,000 points in minutes, wiping out roughly one trillion dollars in market value before rapidly recovering 34353677. As high-frequency trading algorithms aggressively withdrew liquidity from the order books, thousands of retail stop-loss orders were simultaneously triggered 3437.

Because these stop-losses converted to market orders during a period of near-zero liquidity, they executed against "stub quotes" - placeholder bids left by market makers. As a result, shares in major corporations and Exchange-Traded Funds (ETFs) briefly executed at $0.01 per share 333637. Investors utilizing stop-losses were devastated, automatically sold out of their positions at the absolute bottom of the flash crash just moments before prices snapped back to normal 3637.

The 2015 Swiss National Bank Shock

In the foreign exchange markets, an even more dramatic failure of stop-loss mechanics occurred on January 15, 2015. For three years, the Swiss National Bank (SNB) had maintained a strict minimum exchange rate peg, guaranteeing that one euro would buy no less than 1.20 Swiss francs 79808182. Treating this peg as a guaranteed floor, traders and institutions piled into highly leveraged long positions on the EUR/CHF pair, placing their stop-losses just below the 1.20 threshold 7981.

Without warning, the SNB suddenly issued a statement removing the peg 79808283. The EUR/CHF pair instantly plunged 30% 79808283. Global liquidity vanished entirely; major broker circuit breakers triggered, and retail stop-losses were entirely bypassed due to an absolute lack of buyers 7980. When the dust settled and execution eventually took place, prices were so severely slipped that thousands of traders ended up owing their brokers vastly more money than they had deposited in their accounts, resulting in negative equity and the bankruptcy of major brokerages like Alpari UK 798283.

Cryptocurrency and 24/7 Market Liquidity

The rise of cryptocurrency trading introduced the 24/7 market, which fundamentally alters stop-loss dynamics. Because digital asset exchanges never close, true "overnight gap risk" is virtually eliminated; there is no Monday morning opening bell for a price to magically jump past 848586.

However, continuous trading creates severe liquidity fragmentation. Liquidity during weekends or late-night hours is notoriously thin 848687. When massive news breaks - or large, leveraged algorithmic liquidations occur - during these illiquid hours, it causes violent, momentary price spikes known as "wicks" 167438.

A cryptocurrency trader might set a sensible 5% stop-loss, only to have a low-liquidity flash crash trigger their stop, sell their asset, and immediately bounce back to normal levels thirty minutes later - a frustrating phenomenon known as a "whipsaw" 121677.

The leverage inherent in cryptocurrency derivatives exacerbates this. On October 10, 2025, over $19 billion in leveraged positions were wiped out in hours following a shock geopolitical announcement 38. As margin calls cascaded, centralized exchanges struggled under the load. Traders reported that stop-loss orders failed, and Auto-Deleveraging (ADL) systems were activated, forcibly closing profitable positions to cover exchange-level bad debt 38. In an even more localized example, in May 2026, a pricing API glitch at the neobank Revolut briefly displayed Bitcoin at near-zero prices, triggering panic and highlighting the dangers of relying on automated stop orders in systems with shallow internal liquidity books 39.

Stop Hunting: How Smart Money Exploits Predictability

In modern electronic markets, stop-loss orders are not well-kept secrets; they are highly predictable clusters of liquidity. Retail traders notoriously place their stop-loss orders in the exact same, visually obvious locations: just below major support levels, under recent swing lows, or exactly at round numbers (like $100.00 or 1.1000) 169091409394.

Because a triggered sell-stop immediately results in an automated market sell order, a cluster of stops acts as a massive pool of forced selling liquidity 9394. Institutional traders, market makers, and advanced high-frequency algorithms actively scan for these liquidity pools to fill their own massive block orders without causing unfavorable price slippage against themselves 90919394.

This leads to the highly controversial market mechanic known as "stop hunting" or "running the stops" 919394. Large players will intentionally push the price of an asset slightly below a major support level or round number, specifically to trigger the retail stop-losses waiting just underneath 919394. Algorithms will routinely send small "pinging" orders into suspected stop zones to detect hidden liquidity 90.

Once the retail traders are automatically flushed out of their positions by their own risk management tools, the institutional smart money absorbs the sudden influx of liquidity at a discount. The asset price then abruptly reverses and rallies in the original intended direction 909193.

To combat this systematic harvesting of retail orders, sophisticated traders deliberately avoid anchoring stops at obvious round numbers or exact swing lows 15909394. Instead, they utilize volatility indicators like the ATR to place their stops far enough outside the predictable clustering zones, denying institutional algorithms easy access to their liquidity 28159093.

Bottom line

A stop-loss order is an indispensable mechanism for preserving capital and maintaining mathematical control over your longevity as an investor. By automating risk management, it acts as a behavioral safeguard, protecting traders from their own psychological biases and preventing the hopeful, disastrous holding of deeply losing assets. However, market participants must remain highly vigilant of market mechanics; fast markets, overnight liquidity gaps, and institutional stop-hunting algorithms can frequently bypass or exploit these automated orders. While stop-losses are critical for managing downside risk, they do not guarantee perfect protection against extreme structural market failures.