Temporal discounting in impulsive buying and consumer planning

The study of intertemporal choice - the cognitive process by which individuals assign relative values to payoffs at different points in time - has undergone a profound transformation. At the epicenter of this field lies the mechanism of temporal discounting (or delay discounting), defined as the psychological phenomenon wherein the subjective value of a reward diminishes as the delay to its receipt increases 123. Historically relegated to the domain of classical economics, which modeled human actors as perfectly rational agents optimizing long-term utility across their lifespans, temporal discounting is now recognized by behavioral economists and neuroscientists as a highly malleable, context-dependent cognitive mechanism 456.

In the contemporary consumer landscape, this mechanism is systematically targeted, quantified, and exploited by digital market architectures. The rapid expansion of Buy Now, Pay Later (BNPL) platforms, 1-click purchasing ecosystems, and ultra-fast quick commerce (q-commerce) networks has effectively erased the temporal friction that once facilitated rational economic deliberation 789. Concurrently, global macroeconomic volatility - characterized by hyperinflation in specific non-Western markets, socioeconomic instability, and shifting institutional trust - has challenged the traditional assumption that high temporal discounting is strictly an irrational cognitive bias 10111213.

This comprehensive analysis investigates the mechanics of temporal discounting in shaping impulsive buying behavior versus long-term consumer planning. By contrasting theoretical discounting models, differentiating the phenomenon from stable psychological traits and financial illiteracy, examining modern digital ecosystems prioritized in the post-2023 economy, and analyzing geographic diversity, the research synthesizes the current understanding of intertemporal consumer choice and the structural behavioral interventions designed to optimize it.

Theoretical Foundations: Exponential Versus Hyperbolic Models

The fundamental debate in intertemporal choice theory revolves around the mathematical modeling of how humans devalue future events. This debate is not merely academic; it dictates how financial institutions, policymakers, and digital platforms predict and influence consumer behavior, shaping everything from yield curve modeling to retail interface design.

The Exponential Model: The Normative Baseline

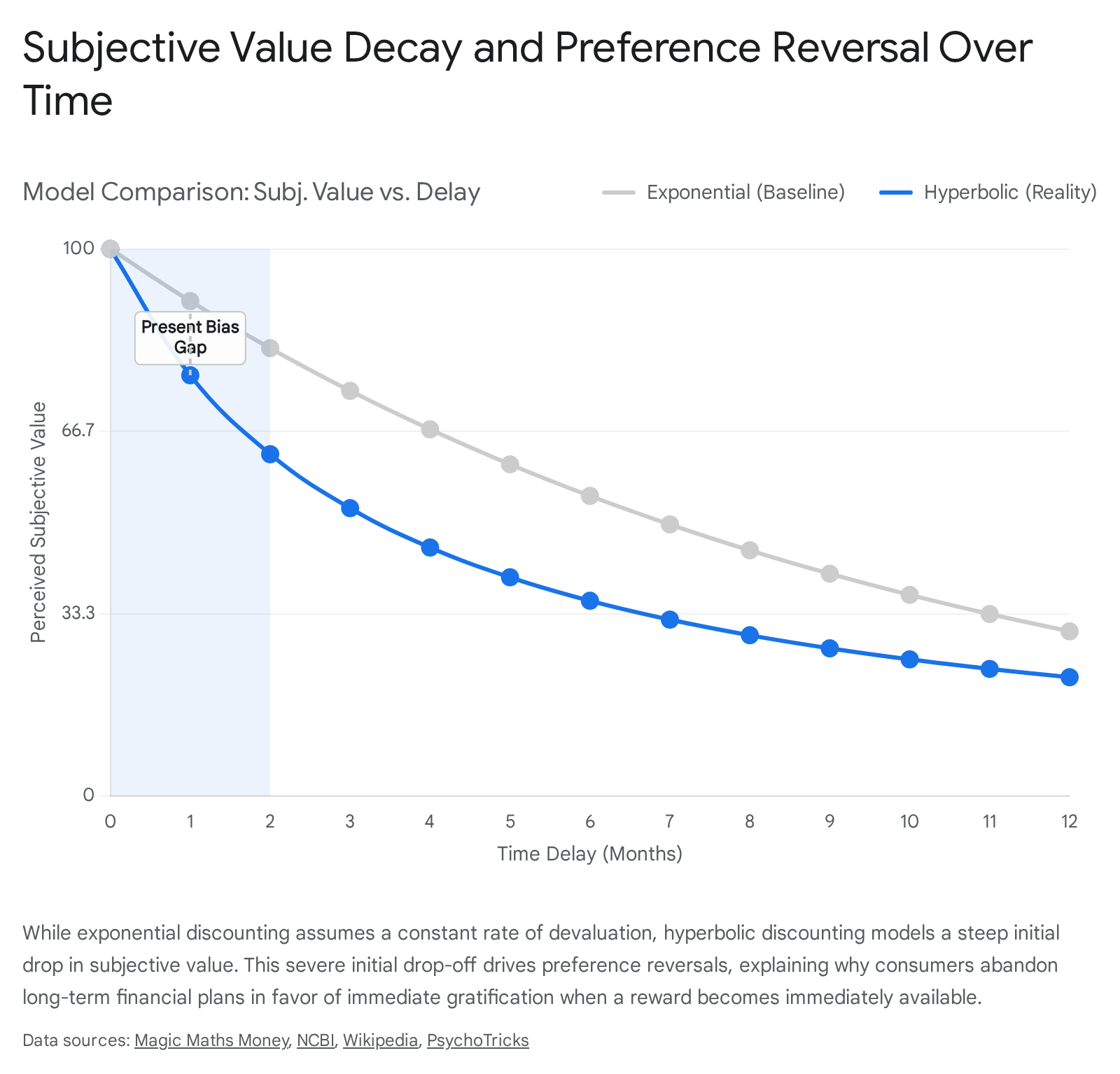

Early economic models, notably Paul Samuelson's Discounted Utility model introduced in 1937, assumed that individuals discount the future at a constant, uniform rate 451415. Modeled mathematically as $V = A e^{-kD}$ (where $V$ is the present subjective value, $A$ is the reward amount, $D$ is the delay, and $k$ is the constant discount rate), exponential discounting posits that human preferences are strictly time-consistent 141615. Under this framework, if a consumer prefers $100 today over $110 next month, they should logically display the exact same preference ratio between $100 in twelve months and $110 in thirteen months.

Exponential discounting assumes that the devaluation of a reward is strictly proportional to the length of the delay, independent of when that delay begins 4. While mathematically elegant and essential for structuring traditional financial instruments like compounding bonds and calculating arbitrage, the exponential model systematically fails to capture the empirical reality of spontaneous human decision-making 41618. The assumption of a constant hazard rate or known interest rate fluctuations rarely applies to the cognitive processes governing everyday consumer choice 18.

The Hyperbolic and Quasi-Hyperbolic Models: The Behavioral Reality

Extensive psychological and neuroeconomic research has demonstrated that spontaneous human preferences adhere to a hyperbolic or quasi-hyperbolic curve rather than an exponential one 414.

The hyperbolic model, commonly expressed as $V = A / (1 + kD)$, illustrates that the subjective value of a reward drops precipitously in the immediate future but levels off substantially as the delay increases 1416.

This steep initial drop is the cognitive engine driving the phenomenon of "preference reversal," a hallmark of time-inconsistent behavior 1416. A consumer may rationally plan to save money for retirement next month (choosing a larger-later reward), but when the moment of choice arrives in the present, the immediate availability of a consumer good triggers a dramatic spike in its subjective value, overpowering the previous long-term intention 16.

In structural econometrics and behavioral modeling, this is frequently conceptualized using a quasi-hyperbolic ($\beta-\delta$) framework. This model introduces a present-bias parameter ($\beta$) that heavily discounts any future period relative to the absolute present, alongside a standard long-run exponential discount factor ($\delta$) applied to all subsequent future periods 41517. The quasi-hyperbolic approximation retains much of the analytical tractability required for dynamic discrete choice models while accurately capturing the severe present bias observed in real-world retail environments 415.

The Debate: Irrational Bias Versus Evolutionary Adaptive Strategy

Traditionally, steep rates of temporal discounting have been classified as an irrational cognitive bias that leads to sub-optimal economic outcomes. From this normative perspective, discounting results in insufficient retirement savings, chronic overspending, and maladaptive health behaviors 5818.

However, a robust evolutionary perspective argues that steep temporal discounting is not a flaw, but a highly adaptive biological strategy forged in ancestral environments 161819. From the perspective of natural selection, organisms unfolding complex developmental sequences over time face immense future uncertainty 1820. Using a Newtonian model for time across a fitness landscape, researchers highlight that an organism must account for the high probability that a distant reward may disappear or that the organism may not survive to claim it 1920. Consequently, discounting future returns for guaranteed short-term benefits acts as a phylogenetic constraint imposed by the process of natural selection 1819.

The friction arises because biological hardware, optimized for ancestral scarcity and immediate survival, is profoundly mismatched with modern financial architectures that demand abstract, decades-long planning 816. In this light, high temporal discounting is a rational evolutionary response operating in a novel, engineered environment that exploits its mechanisms.

Differentiating Temporal Discounting from Related Constructs

To accurately analyze consumer behavior and design effective interventions, it is imperative to isolate temporal discounting from related but distinct constructs: trait impulsivity and financial illiteracy. Conflating these mechanisms obscures the specific cognitive pathways involved in consumer decision-making.

Temporal Discounting Versus Trait Impulsivity

Trait impulsivity is a broad, stable personality construct characterized by an inability to inhibit motor responses, a lack of forward planning, and a general tendency toward rash action, particularly under emotional distress 2122. While high trait impulsivity is correlated with steep temporal discounting, the two are not synonymous and operate through overlapping but distinct neurobiological pathways 2123.

Temporal discounting is specifically a valuation metric - a quantifiable measure of how an individual subjectively trades off time and reward magnitude, represented by the $k$-value or Area Under the Curve (AUC) 13. Unlike trait impulsivity, which remains relatively rigid across contexts, temporal discounting exhibits strong "state" characteristics 24. It fluctuates dramatically based on the framing of the choice, the individual's current physiological state, and the specific modality of the reward 2425. Empirical reviews demonstrate that non-monetary outcomes (such as health benefits, food, or tangible consumer goods) are typically discounted far more steeply than highly liquid cash 24. Therefore, a consumer may exhibit steep temporal discounting for a specific luxury good (exhibiting severe present bias) while displaying low trait impulsivity in standardized psychometric assessments.

Temporal Discounting Versus Financial Illiteracy

Financial illiteracy refers to a deficit in basic numeracy and a lack of declarative knowledge regarding financial mechanics, such as compounding interest, inflation dynamics, and risk diversification 2627. While empirical evidence demonstrates a correlation between high numeracy and economically rational decision-making 2627, financial literacy alone is insufficient to prevent impulsive consumption driven by present bias.

Seminal field studies linking experimentally measured discount factors to real-life financial decisions provide clarity on this distinction. In a major study offering free credit counseling to over 870 individuals, researchers elicited the time preferences of both participants and non-participants using incentivized choice experiments 282930. The results revealed a stark behavioral divide: individuals who chose to acquire personal financial information exhibited substantially higher discount factors (i.e., they were more patient) than those who declined 2829. Impatient individuals actively self-selected out of financial education, viewing the cognitive effort required to become financially literate as an immediate cost with an overly delayed payoff 2829.

Furthermore, dual-process theories of cognition elucidate this divide 826. Numeracy and financial literacy rely heavily on the "cool," deliberative executive functions of the prefrontal cortex, whereas temporal discounting is heavily modulated by the "hot," reward-seeking limbic system 1631. A consumer can fully comprehend the punitive interest rates of revolving credit (possessing high financial literacy) but still execute a purchase due to overwhelming present bias 826. In some experimental approximations involving stock sales, excessive reliance on financial literacy without accompanying numeracy actually amplified cognitive biases like loss aversion, proving that literacy does not automatically neutralize discounting behaviors 26.

The Digital Exploitation of Present Bias (2023+ Contexts)

The contemporary digital marketplace is explicitly engineered to minimize the friction between desire and acquisition. By structurally eliminating temporal delays and physically abstracting the payment process, digital platforms shift consumer focus entirely to immediate gratification, successfully overriding long-term financial parameters.

Buy Now, Pay Later (BNPL) Architectures

The exponential growth of Buy Now, Pay Later (BNPL) services represents the most direct, algorithmic exploitation of quasi-hyperbolic discounting in the modern credit landscape 589. Traditional credit cards impose a temporal delay in the pain of payment by shifting the balance to the end of a billing cycle. BNPL platforms amplify this dynamic by dividing the cost into interest-free micro-installments presented directly at the digital point of sale 89.

This mechanism relies heavily on "cognitive partitioning" and the "left-digit bias" 8. When a consumer contemplates a $600 purchase, the immediate psychological cost acts as a barrier. BNPL partitions this into four installments of $150. The consumer's brain, governed by steep hyperbolic discounting, heavily devalues the future installments, focusing almost exclusively on the immediate $150 required to obtain the item instantly 58. This decoupling of consumption from the holistic pain of payment severely reduces the psychological salience of accumulated debt 32.

Recent demographic and financial behavior data highlights the pervasive impact of this architecture.

| BNPL Market Dynamics (2024-2026 Projections) | Empirical Findings & Consumer Impact |

|---|---|

| Global Market Scale | The global BNPL market is estimated to reach approximately $560.1 billion in Gross Merchandise Volume (GMV) by 2025, capturing an estimated 5-6% of all global e-commerce payments 33. |

| User Base Growth | Global users reached approximately 380 million in 2024, with projections scaling to nearly 670 million by 2028. Adoption is heavily skewed toward Millennials (13%) and Generation Z (10%) 3337. |

| Merchant Revenue Impact | BNPL integration consistently increases Average Order Value (AOV) by 15% to 40% and boosts checkout conversion rates by up to 30%, demonstrating the power of mitigating immediate cost 33. |

| Long-Term Financial Harm | BNPL usage is negatively associated with short-term financial resilience. Users are significantly less likely to hold emergency savings and more likely to experience bank overdraft fees. Crucially, a growing subset of consumers finance their BNPL installments using high-interest revolving credit cards, compounding their debt burden 3234. |

Through the lens of habit formation theory, the recurrent reliance on BNPL not only amplifies present-biased decision making in isolated instances but creates state-dependent behavioral loops, normalizing persistent, fragmented debt obligations 32.

1-Click Purchasing and Biometric Friction Removal

"1-Click" purchasing technologies, historically pioneered and patented by platforms like Amazon, function by removing the temporal and physical friction of the checkout process 73536. The mechanical necessity of entering shipping addresses and credit card numbers traditionally acts as an enforced "cooling-off" period. This brief delay provides the rational prefrontal cortex an opportunity to override impulsive limbic system responses.

By integrating 1-click modalities alongside seamless biometric authentications (e.g., FaceID, fingerprint recognition), the digital space hooks directly into the dopaminergic seeking system 8. The purchase is transformed from a calculated decision into an instant reflex. Studies analyzing interaction modalities suggest that seamless, low-effort purchasing channels - particularly those integrating voice assistants or single-tap confirmations - generate significantly higher rates of indulgent and impulsive choices compared to manual, high-friction processes 37. The reduction of physical delay to absolute zero ensures that the subjective value of the immediate reward remains at its theoretical maximum on the hyperbolic curve 8.

Quick Commerce (Q-Commerce) and Instant Delivery

The emergence of "Quick Commerce" (q-commerce) - platforms promising the delivery of groceries, electronics, and personal care items within 10 to 30 minutes - has fundamentally altered the temporal parameters of retail 3839. Platforms operating extensively in high-density urban markets, such as Blinkit, Zepto, and Swiggy Instamart, rely heavily on impulse purchases, utilizing decentralized networks of micro-warehouses (dark stores) to fulfill orders almost instantaneously 3940.

In a traditional e-commerce environment where delivery takes several days, consumers must plan, consolidate purchases, and engage in forward-thinking behavior 38. Q-commerce collapses this temporal distance. The psychological triggers embedded in instant commerce create a feedback loop where extreme speed breeds reliance on immediate fulfillment 3945. Research indicates that the proliferation of 15-minute delivery windows has successfully pushed consumers to increase their Average Order Value (AOV). For instance, platforms have expanded catalogs beyond essential groceries into higher-margin impulse items like cosmetics and electronics, driving AOVs to over Rs. 600 in certain markets 3845. This demonstrates that when the delay parameter ($D$) in the discounting equation is forcefully minimized by logistics, consumer spending thresholds and impulsivity increase dramatically 38.

Situational Modifiers: Cognitive Load, Stress, and Socioeconomic Status

Temporal discounting is not an isolated, static cognitive function; it is highly sensitive to the consumer's immediate environmental and psychological state. Variations in cognitive load, acute stress, and broader socioeconomic status actively warp the shape of the discounting curve.

The Cognitive Tax of Poverty and Resource Scarcity

Economic inequality and systemic poverty profoundly impact economic decision-making through what behavioral scientists term the "bandwidth tax" hypothesis 41. Individuals living in resource-scarce environments must constantly juggle immediate, pressing financial emergencies - such as securing food, paying imminent rent, and avoiding utility shut-offs.

This persistent state of triage imposes a severe cognitive load, heavily taxing executive functions including sustained attention, working memory, and self-control 41. Consequently, cognitive depletion leads to an over-reliance on intuitive, immediate-focused heuristics rather than deliberative planning 41. Low socioeconomic status is consistently correlated with steeper temporal discounting because immediate survival necessitates prioritizing present resources 2141. This dynamic creates a vicious, self-perpetuating cycle: poverty induces high temporal discounting as an adaptive survival mechanism, which in turn leads to decisions - such as accepting predatory high-interest payday loans or foregoing long-term educational investments - that structurally perpetuate poverty 122141.

Stress, Emotional Valence, and Income Volatility

Acute stress and negative emotional states similarly contract a consumer's temporal horizon. High-stress environments trigger a "present-oriented" cognitive focus, prioritizing immediate affective relief over future stability 42. Individuals struggling with Substance Use Disorders (SUDs), pathological gambling, or chronic stress exhibit negative tendencies toward future time perspectives, seeking the instant dopamine release of a purchase or substance to escape unpleasant current realities 224243. Neurobiological evidence links impulsive behavior and steep temporal discounting to overactivation in the ventral striatum and structural pathways governing reward processing 43.

Furthermore, modern gig-economy structures frequently subject workers to "feast-or-famine" income volatility. This unpredictability systematically shapes temporal discounting patterns 41. When the arrival of future income is highly uncertain, the most mathematically rational response is to heavily discount the future and consume resources immediately upon their availability 41. Predictability and stability are prerequisites for a low discount rate; without them, long-term planning frameworks collapse 414450.

Geographic Diversity: Stable Versus Volatile Non-Western Markets

The macroeconomic environment of a specific nation acts as a macro-level modifier of temporal discounting. While massive 61-country cross-cultural studies (capturing over 13,000 participants) have established that the fundamental psychological patterns of temporal discounting are globally generalizable 124546, the utility and rationality of steep discounting vary drastically between stable Western economies and volatile non-Western markets.

Stable Economies: The Foundation of Exponential Planning

In stable economic environments - characterized by low inflation, robust social safety nets, and high institutional trust (predominantly observed in Northern and Western Europe, the United States, and East Asia) - low rates of temporal discounting are systematically rewarded 11. The value of the local currency remains relatively constant, making it economically rational for citizens to defer consumption, save diligently, and invest in long-term assets like equities or real estate 11. In these societies, temporal discounting aligns closer to the normative exponential model, where long-term capital accumulation is both biologically and economically advantageous 11.

Volatile Markets: "Front-Loading" as an Adaptive Strategy

In sharp contrast, consumers residing in highly volatile economies experiencing severe structural inflation, rapid currency devaluation, and political instability exhibit consumption behaviors that mirror steep temporal discounting but actually function as highly rational economic defenses 1013.

In emerging markets like Argentina and Turkey, where inflation rates have historically eroded purchasing power on a monthly or even weekly basis, holding liquid cash is a guaranteed, rapid loss of wealth 104748. Consequently, middle-class consumers in these regions engage in "precautionary front-loading" 13. Upon receiving their monthly income, consumers immediately accelerate the purchase of durable goods, household appliances, and non-perishables, effectively converting depreciating fiat currency into tangible, usable assets before prices inevitably rise 1355.

While a traditional behavioral economist observing this from a stable Western context might view the immediate consumption of a year's worth of supplies as impulsive or representative of a massive $k$-value in a delay discounting task, in a hyperinflationary environment, this steep discounting of future monetary value is an economically optimal, adaptive strategy 1349. The delay discounting of the fiat currency accurately reflects its objective mathematical decay.

Institutional Trust and the Geopolitics of Time Preference

Beyond pure inflation, institutional trust dictates a population's fundamental willingness to plan for the future. Research comparing populations under long-term economic sanctions (such as Russia and Iran) reveals that institutional trust correlates directly with economic coping strategies 50. In societies where citizens distrust the central banking system, fear the sudden erosion of property rights, or doubt the basic stability of the state (trends often observed across the Balkans, parts of Africa, and heavily sanctioned economies), citizens display highly hyperbolic temporal preferences 115051.

If the state apparatus cannot guarantee the long-term security of a pension or a savings account, investing in the future represents an unacceptable, unquantifiable risk. Therefore, high rates of temporal discounting in these regions are heavily influenced by historical trauma and geopolitical factors, rendering extreme short-termism a completely rational response to systemic institutional insecurity 1150.

Temporal Framing in Consumer Research

Recent research published in top-tier marketing journals, including the Journal of Consumer Research (2023), highlights how the specific granular framing of time profoundly impacts duration perceptions and subsequent discounting behavior 52.

The "days-of-the-week effect" demonstrates that consumers perceive temporal intervals as objectively longer when they are described using specific days (e.g., "Monday, February 1 to Saturday, February 6") compared to equivalent intervals described solely by standard calendar dates (e.g., "February 1 to February 6") 52. The days-of-the-week framing activates "narrow-span implicit scales" within consumer memory, which have significantly lower cognitive thresholds for categorizing a duration as "long" or "very long" 52.

When temporal distance feels subjectively longer, the future reward is discounted much more heavily. Consequently, in time-versus-money tradeoffs, framing future dates with high granularity (days of the week) significantly decreases a consumer's willingness to wait for a larger financial reward, exacerbating present bias 52. For instance, in controlled studies, participants were notably less likely to choose a longer task for a higher payment when the duration was framed using days of the week, indicating that the perceived "cost" of the additional time outweighed the monetary incentive 52. Conversely, framing delays in broader, more abstract terms can reduce perceived psychological distance, thereby flattening the discounting curve 52.

Behavioral Interventions: Mitigating Present Bias and Restructuring Choice

Given the profound societal costs of steep temporal discounting in domains ranging from individual debt accumulation to addiction and public health, extensive research has focused on behavioral interventions designed to systematically alter the subjective valuation of the future. The most efficacious of these interventions seek to bypass the reliance on sheer willpower, instead leveraging "behavioral architecture" to align immediate actions with long-term goals.

Interventions primarily fall into two categories: cognitive restructuring (altering how the brain perceives the future) and environmental restructuring (altering the physical or digital choice architecture). The table below synthesizes the mechanisms and documented empirical efficacy of the leading behavioral interventions.

| Intervention Type | Mechanism of Action | Empirical Efficacy & Characteristics |

|---|---|---|

| Pre-Commitment Devices (Financial) | Operates by utilizing the rational, "cool" past self to establish external, automated constraints that bind the impulsive, "hot" present self. Removes the decision entirely from the immediate environment (e.g., automated 401k deductions, inaccessible savings accounts) 16. | High Efficacy. Highly successful when mechanisms are largely irrevocable. Relies on removing friction from saving and injecting massive friction into spending. Prevents preference reversal by eliminating the point of choice altogether 163153. |

| Pre-Commitment Devices (Behavioral) | Voluntary imposition of social or psychological constraints (e.g., "self-binding" contracts, freezing a credit card in ice) to introduce a forced temporal delay, allowing the prefrontal cortex time to engage 1631. | Moderate to High Efficacy. EEG/ERP studies show that even revocable pre-commitments (where consumers can opt out) lower impulsivity and alter N1 and P300 amplitudes, though they are less robust than strict financial binding 5354. |

| Episodic Future Thinking (EFT) | A cognitive intervention requiring the individual to vividly imagine and mentally simulate specific, highly detailed future personal events. This reduces the abstract nature of the future, effectively lowering psychological distance 1655. | Moderate Efficacy. Comprehensive meta-analyses covering dozens of studies indicate EFT significantly reduces temporal discounting (Hedges' g = 0.52). Efficacy is highest when future imagery is distinctly positive (g = 0.64) 5657. |

| Temptation Bundling | Strategically pairs an action providing immediate gratification (a reward) with an action promoting a long-term goal (a cost). Creates an immediate neurochemical bridge to sustain engagement with a delayed benefit 16. | Moderate Efficacy. Highly effective for repeated, ongoing behaviors (e.g., exercising while listening to an exclusive podcast), but generally less effective for major, isolated financial decisions 16. |

| Explicit-Zero Reframing | Modifies choice architecture by explicitly stating null outcomes (e.g., framing a choice as "Receive $50 today and $0 in a year" vs. "$0 today and $100 in a year"). Increases baseline attention to the future loss 2. | Low to Moderate Efficacy. Reduces discount rates by shifting present bias and altering temporal attention allocation, but effect sizes are generally small and primarily suited for hypothetical scenarios 2. |

The Mechanics and Efficacy of Episodic Future Thinking (EFT)

Among cognitive interventions, Episodic Future Thinking (EFT) has garnered substantial empirical and clinical support, particularly in the treatment of Substance Use Disorders (SUDs) and behavioral addictions 225558. Temporal discounting occurs largely because the present moment is vivid, sensory-rich, and immediately rewarding, while the future is abstract and computationally difficult to simulate. The prefrontal cortex struggles to assign emotional weight to a nebulous concept like "retirement" or "future health" 1622.

EFT forces the brain to engage in "mental time travel." By actively constructing a vivid scenario based on autobiographical memory (e.g., visualizing a specific beach vacation destination, rather than just the abstract concept of "saving money"), the individual activates prospective memory circuits and prefrontal-mediotemporal interactions 16225355. This vividness transfers emotional weight from the limbic system to the prefrontal cortex, artificially increasing the perceived present value of the future self 162259.

Extensive meta-analyses confirm that EFT reliably shifts preferences away from smaller-sooner rewards toward larger-later rewards, mitigating the impulsivity driving destructive consumer debt and substance abuse 555657. Interestingly, research indicates that the modality of the EFT cue matters; utilizing drawn visual cues can be just as effective, if not more so, than written cues in reducing delay discounting, particularly for individuals who heavily index toward an immediate time perspective 55.

Conclusion

Temporal discounting is not a fixed, irrational flaw in human cognition; rather, it is an evolutionarily conserved valuation mechanism that continuously weighs the certainty of the present against the probabilistic risk of the future. In the context of modern consumer behavior, this mechanism has become a primary structural battleground.

Digital market architectures - through the seamless integration of BNPL micro-installments, 1-click biometric authentications, and 10-minute q-commerce delivery guarantees - are continuously evolving to compress temporal delays to near zero. By doing so, they target the steepest, most vulnerable segment of the quasi-hyperbolic discounting curve, maximizing present bias and driving impulsive, debt-fueled consumption. Conversely, systemic global factors such as resource scarcity, hyperinflation, and institutional distrust validate steep temporal discounting, transforming what appears from a Western normative perspective to be short-sighted impulsivity into a highly rational, adaptive strategy for economic and physical survival.

Addressing the negative externalities of temporal discounting in stable economies requires a paradigm shift: from relying on passive financial literacy and brute-force willpower to implementing active, structural behavioral architecture. Future interventions must move beyond mere education to actively reshape choice environments - utilizing irrevocable pre-commitment devices to shield consumers from future temptations, and deploying Episodic Future Thinking mechanisms to make long-term financial security as psychologically vivid and rewarding as immediate digital gratification. As digital consumption continues to accelerate in speed and scale, the defining regulatory and commercial challenge of the coming decade will be designing digital ecosystems that respect, rather than exploit, the deeply ingrained architecture of human intertemporal choice.