Mental accounting and budget categorization in the digital age

1. Introduction: Recontextualizing Mental Accounting in Modernity

The intersection of behavioral economics and digital commerce has fundamentally reshaped the architecture of consumer financial decision-making. Historically, classical economic theory operated on the foundational axiom of fungibility - the assumption that all money is perfectly interchangeable regardless of its origin, storage mechanism, or intended use 13. However, the advent of behavioral economics, pioneered by foundational theorists such as Richard Thaler and Amos Tversky in the late twentieth century, systematically dismantled this assumption. They introduced the concept of mental accounting, defining it as the complex set of cognitive operations used by individuals and households to code, categorize, and evaluate their economic outcomes and financial activities 115. By establishing subjective internal accounts, individuals routinely violate the principle of fungibility, treating equivalent sums of money differently based on arbitrary cognitive labels 2.

While foundational theorists established the psychological architecture of mental accounting, the environment in which consumers exercise these behaviors has undergone a radical transformation. In contemporary consumer environments, the mechanisms of mental accounting have migrated from cognitive abstraction and physical constraints (such as cash in paper envelopes) to highly sophisticated digital ecosystems. Modern financial technology (fintech) - encompassing algorithmic mobile banking vaults, frictionless digital wallets, and pervasive Buy Now, Pay Later (BNPL) platforms - has profoundly altered how consumers compartmentalize their resources 384. The proliferation of these technologies demands a modernized theoretical framework that accounts for real-time data analytics, personalized algorithmic nudging, and dematerialized currency 3.

This exhaustive research report investigates the evolution of mental accounting within highly digitized infrastructures, heavily prioritizing empirical evidence from peer-reviewed publications in behavioral economics, psychology, and marketing from 2023 to 2026 (e.g., the Journal of Consumer Research, Journal of Economic Behavior & Organization). The subsequent analysis explores the "dual mechanisms of decoupling," the shifting dynamics of income source segregation, and the digital amplification of specific behavioral corollaries such as the house money effect, the sunk cost fallacy, and the credit card premium 511613.

Furthermore, this report broadens the scope of traditional behavioral finance by examining profound geographic and cultural divergences. It contrasts the highly financialized, credit-driven mental accounting systems of Western markets with the cash-heavy, mobile-money-centric environments of emerging economies, such as those in Sub-Saharan Africa and Southeast Asia 1415. Ultimately, this analysis explicitly calls out and corrects a pervasive theoretical misconception: it clarifies that cognitive compartmentalization is not merely an irrational economic anomaly, but a highly functional, positive self-control heuristic necessary for navigating a frictionless digital economy 278.

2. Correcting the Misconception: Mental Accounting as a Functional Self-Control Heuristic

A pervasive misconception within both popular finance discourse and orthodox classical economics is the characterization of mental accounting as a purely cognitive error or a detrimental defect in human reasoning. Because mental accounting systematically violates the classical economic principle of fungibility, it is frequently misdiagnosed as an irrational flaw that leads to suboptimal wealth maximization 169. For instance, classical economists often point to the behavior where an individual maintains a high-interest credit card balance while simultaneously holding substantial funds in a low-yield savings account. Mathematically, this is inefficient; the rational action would be to liquidate the savings to eliminate the high-interest debt. Consequently, classical models dismiss this compartmentalization as an irrational cognitive failure 219.

However, contemporary psychological and behavioral economics literature necessitates a fundamental correction of this paradigm. Mental accounting is not a cognitive failure; it is a highly functional, adaptive self-control heuristic designed to mitigate impulsive behavior and enforce financial discipline in environments saturated with consumptive temptation 2710. The human brain faces immense cognitive load when required to continuously calculate the opportunity cost of every single transaction against a holistic, lifetime budget constraint 127. To survive this overwhelming cognitive complexity, individuals rely on heuristics - simplifying cognitive rules-of-thumb that establish rigid, subjective boundaries around specific pools of money 15.

Empirical research from 2024 and 2025 published in behavioral finance journals indicates that mental accounting acts as a vital psychological buffer against present-biased preferences, impulsivity, and hyperbolic discounting 7811. By mentally designating a pool of funds as "sacred" (e.g., a child's education fund, emergency savings, or rent money), consumers erect internal psychological barriers that prevent the depletion of long-term assets for short-term hedonic consumption 188. Studies utilizing structural equation modeling have consistently shown that individuals who actively engage in mental accounting exhibit higher financial self-efficacy, superior budgeting behaviors, and a significantly reduced likelihood of falling into systemic over-indebtedness compared to those who treat all liquidity as a single, fungible pool 81011.

Therefore, the intentional violation of fungibility represents a strategic behavioral trade-off. Consumers willingly accept minor economic inefficiencies (such as lost interest yield on a savings account while holding debt) in exchange for the immense psychological friction required to enforce behavioral discipline 37. In this light, mental accounting is an essential survival mechanism. It simplifies the overwhelming complexity of continuous financial decision-making by providing clear boundaries and predefined rules, ensuring that predictable costs are met and long-term objectives are not sacrificed to the immediate gratification of the present moment 110.

3. Structural Transformation: Physical Compartmentalization vs. Digital Mental Accounting

For decades, the most tangible and universally recognized manifestation of mental accounting was the "envelope method" - an analog, zero-based budgeting system where physical fiat currency is distributed into categorized paper envelopes representing discrete expenditure limits 22232425. When the physical cash in a specific envelope (e.g., "groceries" or "entertainment") is depleted, spending in that category triggers a "hard stop." This physical compartmentalization relies heavily on the "pain of paying," a well-documented psychological heuristic where the sensory and haptic cues of handing over physical currency - watching one's wallet visibly thin - induce an immediate, visceral emotional resistance to financial depletion 526.

The Dual Mechanisms of Decoupling in the Digital Age

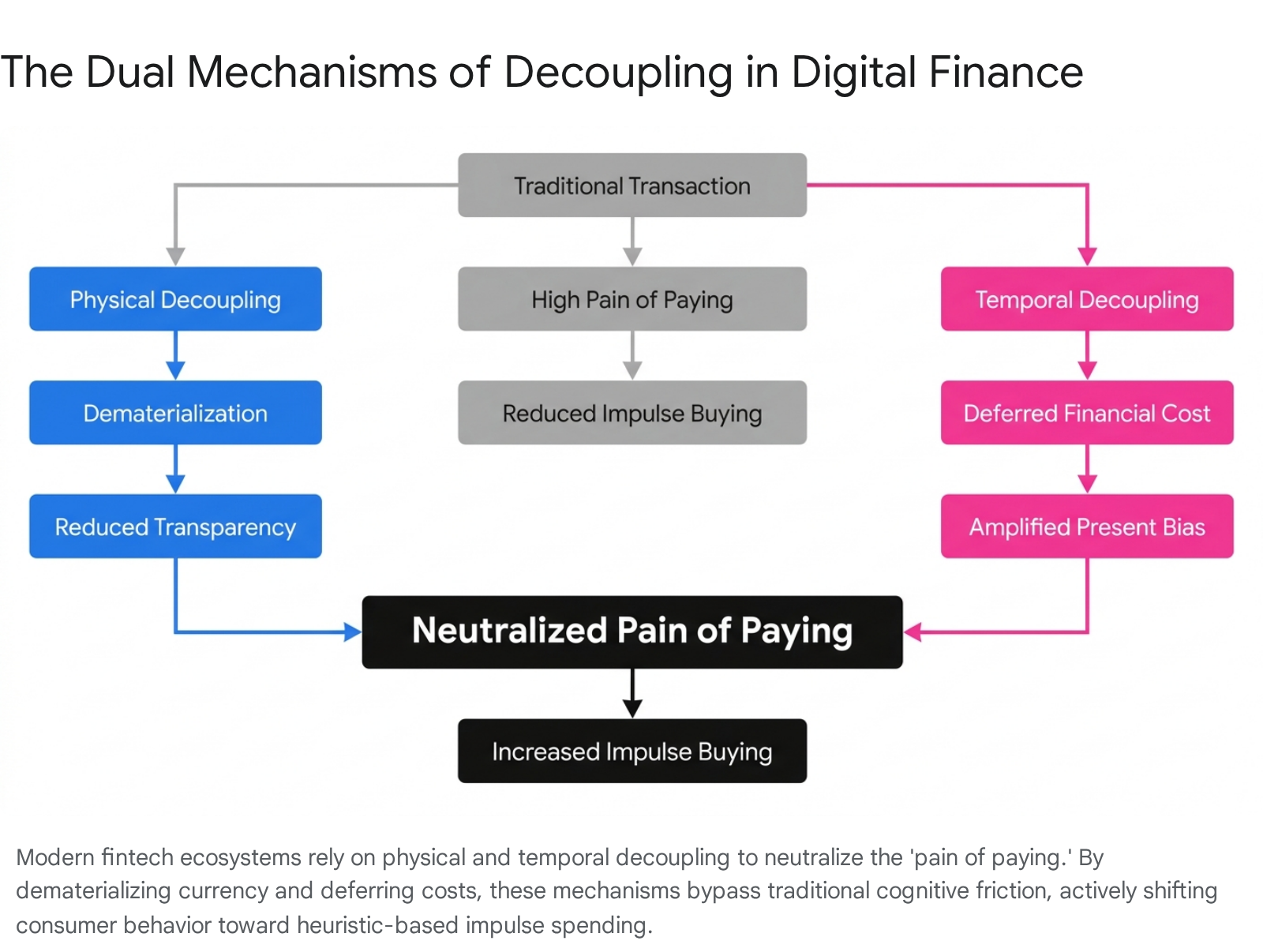

The transition to digital commerce has fundamentally disrupted this analog regulatory mechanism through what contemporary consumer research published in 2026 terms the "dual mechanisms of decoupling": physical decoupling and temporal decoupling 5.

First, physical decoupling refers to the systemic dematerialization of currency. The migration from physical cash to credit cards, and subsequently to invisible, biometric, or zero-touch mobile wallets (such as Apple Pay and Google Wallet), strips away the sensory feedback associated with spending 5. By eliminating the haptic experience of counting and surrendering bills, digital interfaces effectively neutralize payment transparency, heavily muting the pain of paying at the point of sale 5.

Second, temporal decoupling involves the chronological separation of the act of consumption from the actual financial depletion. Facilitated heavily by modern BNPL ecosystems and digital credit, temporal decoupling exploits human time perception 5. The hedonic benefits and utility of a product are experienced immediately in the present, while the financial costs are deferred into an abstract, invisible future, effectively separating the psychological reward from the financial pain 45.

The hyper-acceleration of these decoupling mechanisms has birthed a behavioral phenomenon documented in 2026 literature as "Spendception." Spendception is defined as a psychological construct where diminished visibility, frictionless one-click environments, and invisible background authentication systematically dismantle a consumer's internal cognitive resistance, leading to highly impulsive spending behaviors 5.

To counter the loss of physical friction and the rise of Spendception, modern fintech applications have attempted to digitize the envelope method via mobile banking vaults, digital "buckets," and automated zero-based budgeting applications (e.g., YNAB, PocketGuard) 826271229. While these tools provide robust analytics, real-time tracking, and automated categorization, they fundamentally alter the psychological stakes of compartmentalization 826. The digitization of mental accounting presents a profound paradox for consumer welfare: while fintech apps that visualize spending patterns can mitigate behavioral biases by promoting awareness and externalizing memory, the seamlessness of the underlying payment infrastructure continuously threatens to exacerbate those same biases 3. As the cognitive friction of parting with money evaporates, consumers are forced to rely heavily on artificial, software-imposed constraints, offloading the labor of self-control to algorithms that may be easily overridden with a single swipe 826.

Comparative Analysis: Traditional vs. Digital Compartmentalization

The structural divergence between analog and digital mental accounting dictates how effectively a consumer can enforce self-control. The following table systematically contrasts the two paradigms across core psychological and functional dimensions.

| Feature / Dimension | Physical Compartmentalization (Traditional Envelope Method) | Digital Mental Accounting (Fintech Vaults & Apps) |

|---|---|---|

| Medium & Tangibility | Physical fiat currency allocated into designated, labeled paper envelopes 222324. | Virtual balances partitioned via software algorithms, sub-accounts, and digital buckets 82526. |

| The "Pain of Paying" | Extremely high. The visceral, haptic experience of surrendering cash triggers acute loss aversion 2627. | Abstract and attenuated. Frictionless swiping, tapping, or biometric authentication neutralizes emotional resistance 526. |

| Boundary Enforcement | Hard Stop: Depletion of physical funds creates an absolute, undeniable physical barrier to further consumption in that category 222627. | Soft Stop: Push notifications and visual alerts warn of overspending, but algorithmic overdrafts or linked credit lines easily bypass limits 82526. |

| Cognitive Load & Administration | High manual effort. Requires physical trips to the bank, manual withdrawal, counting, and tracking of currency 2326. | Low cognitive load. Automated transaction parsing, API bank integration, and real-time dashboard categorization 82629. |

| Vulnerability to External Manipulation | Minimal external manipulation. The user maintains complete sovereign control over the physical architecture 2224. | High vulnerability. Algorithmic nudges, dark patterns, gamification, and platform-driven choice architecture can actively encourage spending 3430. |

4. Income Source Segregation: Evaluating the Marginal Propensity to Consume (MPC)

A critical pillar of mental accounting is the Behavioral Life Cycle Hypothesis (BLCH), developed collaboratively by Hersh Shefrin and Richard Thaler 1813. The BLCH dictates that individuals do not treat their total wealth as a unified, fungible reservoir. Instead, they mentally segregate their assets into distinct tiers of psychological protection - typically categorizing them as current income, current assets, and future wealth 713. Consequently, the source, labeling, and framing of incoming funds heavily dictate a consumer's Marginal Propensity to Consume (MPC) - the economic metric defining the proportion of additional income that an individual will spend rather than save 11415.

Scheduled vs. Unscheduled Income

The origin of liquidity fundamentally alters its psychological ownership and perceived fungibility within the consumer's mind. Scheduled, highly predictable inflows, such as a regular salary or monthly pension, are heavily protected. Consumers routinely assign regular wages to rigid mental accounts designated for essential expenditures, housing, structural debt servicing, and basic survival needs 1435.

Conversely, unscheduled or unpredictable inflows - such as lottery winnings, unexpected bonuses, inheritance, or macroeconomic stimulus checks - are mentally coded as "windfalls" 3637. Because these funds reside outside the foundational budget architecture and were never factored into baseline survival calculations, they lack psychological protection. Empirical studies analyzing transaction-level banking data from 2024 and 2025 demonstrate that the MPC for windfalls is significantly higher than that for regular salary 141537. In these instances, consumers feel a psychological "license to splurge," deploying windfall money on hedonic or discretionary items without triggering the guilt typically associated with depleting baseline income 1415. Furthermore, banking data reveals a phenomenon of "depositor inattention," where unscheduled income that is not immediately spent is often left to languish in low-yield checking accounts much longer than scheduled income, demonstrating a failure to mentally integrate the windfall into optimal wealth-building strategies 1416.

The Tax Refund Anomaly and Strategic Reallocation

Tax refunds occupy a unique and complex space within the literature of mental accounting. From a purely rational economic perspective, a tax refund is merely the restitution of a taxpayer's own overwithheld earnings; it is delayed scheduled income, and therefore should be treated with the same protective MPC as a bi-weekly paycheck . However, behavioral economics reveals that consumers routinely categorize tax refunds as "bonus money" or found windfalls 17. Because it arrives as a large lump sum independent of the regular payroll cycle, the refund historically triggers the same elevated MPC associated with lottery winnings, driving surges in retail consumption and durable goods purchases 1417.

Interestingly, severe macroeconomic pressures have recently begun to force a systemic recalibration of this specific mental account. Extensive survey data and behavioral studies from the 2025 and 2026 tax seasons highlight a profound shift in how younger demographics (particularly Millennials and Gen Z) handle tax refunds amid persistent inflation and rising costs of living 404118. A growing proportion of consumers - nearly 40% in recent surveys - are now utilizing this predictable windfall not for immediate hedonic consumption, but for defensive deleveraging. Specifically, they are redirecting refunds toward paying down high-interest credit card debt or funding emergency survival accounts 404118. This reflects a highly adaptive utilization of mental accounting: when baseline income is insufficient to manage inflationary pressures, consumers consciously reclassify their windfall accounts to preserve financial solvency, indicating that mental accounting boundaries are responsive to severe environmental stress.

Comparative Analysis of Spending Behaviors by Income Source

To systematize these psychological variances, the following table compares consumer spending behaviors and MPC across distinct income classifications.

| Income Source / Liquidity Type | Mental Categorization | Marginal Propensity to Consume (MPC) | Primary Utility and Consumer Behavior |

|---|---|---|---|

| Regular Salary / Wages | Current Income (Highly Protected) 713 | Low to Moderate | Strictly allocated to fixed expenses, housing, utilities, and essential living costs. High cognitive friction against frivolous use 35. |

| Unpredictable Windfalls (Lottery, Gifts, Bonuses) | Found Money / Hedonic Account (Unprotected) 36 | Very High | Rapidly deployed toward discretionary spending, luxury items, or high-risk investments. Triggers a "license to spend" 83537. |

| Tax Refunds | Historically: Windfall. Presently (2025+): Strategic Liquidity Event 4041 |

Moderate to High | Traditionally spent on major discretionary purchases. Increasingly diverted to debt reduction and essential backlog spending due to inflation 40411819. |

| Credit Lines & BNPL | Future Wealth / Borrowed Capital (Temporally Deferred) 4544 | High (due to Temporal Decoupling) | Utilized for immediate gratification. The cost is mentally decoupled from the present, leading to systemic underestimation of total liabilities 45. |

5. The Digital Amplification of Mental Accounting Corollaries

The architecture of digital finance does not merely change how money is moved from one ledger to another; it fundamentally alters how money is perceived by the human brain. By systematically manipulating the boundaries of mental accounts, digital platforms amplify several key behavioral economic corollaries, frequently optimizing them to maximize transaction volume, platform retention, and corporate revenue.

Buy Now, Pay Later (BNPL) and the Liquidity Flypaper Effect

Buy Now, Pay Later (BNPL) platforms represent the zenith of temporal decoupling. Traditional classical economic models, such as exponential discounting, fail to capture the severity of present bias exhibited by BNPL users 4. Instead, consumer behavior on these platforms aligns with quasi-hyperbolic discounting models, wherein the allure of immediate gratification heavily outweighs the abstract reality of future repayment 45. A 2025 study in the Journal of Economic and Applied Electronic Commerce Research demonstrated that BNPL effectively eliminates the distorting friction of present bias during the purchase phase because both the consumption and the payment are shifted to the future, allowing merchants to command higher prices without a corresponding drop in demand 4.

Mental accounting literature identifies a related phenomenon known as the "liquidity flypaper effect" or the psychological ownership of borrowed money 444. When consumers are granted a BNPL credit limit, they frequently integrate that limit into their mental account of "total available funds," rather than accurately coding it as an active liability 4. Consequently, consumers do not substitute a cash purchase with a BNPL purchase; rather, the presence of BNPL expands their perceived purchasing power, directly increasing overall expenditure 444. Furthermore, by splitting a $200 purchase into four interest-free payments of $50, BNPL exploits the human cognitive tendency toward "narrow bracketing" 58. The consumer evaluates the affordability of the transaction based purely on the $50 immediate outflow, completely ignoring the cumulative debt burden forming in their future wealth account 245. Additionally, the "endowment effect" is triggered immediately upon receipt of the item; because the initial installment is low, consumers feel less constrained by the financial commitment and rapidly view the item as their own, further reducing the likelihood of returns and cementing the debt 49.

The Credit Card Premium and Mobile Wallets

The "credit card premium" is a robust behavioral phenomenon describing the increased willingness to pay (WTP) and higher total basket values when consumers transact with credit rather than cash 1345. Recent meta-analyses from 2024 and 2025 confirm that decades of classical credit card premiums have successfully migrated to mobile payments and digital wallets (e.g., Apple Pay, Google Pay) 1320. While some studies suggest the pure "cashless effect" may be slightly weakening as consumers become overwhelmingly familiar with digital payments, the premium remains highly economically significant 1336.

Digital wallets facilitate a heightened state of physical decoupling. The transaction becomes entirely invisible, often requiring only a biometric facial scan or a quick tap of a smartwatch 513. Furthermore, the integration of premiumization strategies within digital banking - such as tiered lifestyle benefits, gamified reward points, and dynamic cashback offers - encourages users to view spending not as a depletion of resources, but as an active, gamified strategy to maximize return on investment 4721. This sophisticated framing manipulates mental accounting by categorizing consumption as a rewarding utility and an assertion of status, rather than an economic loss 2947.

The House Money Effect in Gamified Fintech and Crypto

The "house money effect" postulates that individuals exhibit significantly higher risk tolerance following a prior financial gain. They treat the newly acquired profits as conceptually separate from their initial capital - much like a gambler playing with the casino's chips rather than their own savings 1164922.

In the contemporary digital landscape, this effect has been weaponized by zero-commission trading apps, cryptocurrency exchanges, and gamified financial platforms (such as Robinhood or eToro) 11225152. These platforms utilize user interface (UI) features explicitly mirroring those of digital gambling - such as real-time leaderboards, push notifications, and variable reward structures - to induce persistent dopamine loops 31153. A 2025 empirical study on cryptocurrency and retail trading published in experimental economics journals demonstrated the power of the "realization effect." When investors realize gains, they rapidly segregate those earnings into a "house money" mental account, vastly increasing their propensity to engage in subsequent, highly speculative, positive-skewed lotteries (e.g., volatile alt-coins, meme stocks, or out-of-the-money options) 11302252. Conversely, paper losses often increase risk-taking as investors attempt to break even, while realized losses tend to decrease it 2252. By framing the investment environment as a frictionless game, fintech platforms actively dissolve the psychological friction that typically restrains reckless capital allocation 1151.

The Sunk Cost Fallacy in the Subscription Economy

Mental accounting is intrinsically linked to the sunk cost fallacy - the irrational cognitive bias that drives individuals to persist in an endeavor or continue consuming a service simply because an initial, unrecoverable investment of time, effort, or money has already been made 6305455.

The modern digital subscription economy relies on the systemic, algorithmic exploitation of this cognitive bias 30535657. Consumers heavily compartmentalize small, recurring charges (e.g., $5 to $15 monthly) into trivial, isolated mental accounts, systematically underestimating their cumulative annual impact - a phenomenon termed "subscription creep" 5657. Industry data from 2025 indicates that unused memberships collectively cost consumers roughly $10.57 per month, draining household budgets without providing utility 56.

When users contemplate canceling unused services (e.g., streaming platforms, SaaS tools, fitness apps), choice architects leverage loss aversion and the sunk cost fallacy to maximize retention 305355. Platforms employ "trigger-action-reward loops" and remind users of the data, curated playlists, or streaks they will lose upon cancellation. This triggers an emotional response that overrides the rational recognition that the service is no longer providing marginal utility 30535657. The status quo bias, reinforced by auto-renewals, ensures that retention is often driven not by product value, but by the friction of change 3055. Recognizing these predatory retention tactics, regulatory bodies like the U.S. Federal Trade Commission (FTC) introduced "click to cancel" rules in 2024 to force companies to align cancellation friction with subscription ease 56.

Furthermore, the prevalence of virtual, in-app currencies (e.g., "gems," "tokens," or "coins") within mobile applications adds an additional layer of behavioral obfuscation. By forcing consumers to convert fiat currency into an arbitrary digital token, platforms create a profound mental separation from real money. Consumers who would rationally hesitate to spend $5 on a digital upgrade routinely spend 500 "gems" without friction, as the mental account for virtual tokens is entirely detached from the emotional weight of real-world fiat currency 6.

6. Geographic and Cultural Diversity: Cash-Heavy vs. Financialized Markets

Mental accounting is not a universal psychological monolith; it is highly malleable and deeply influenced by cultural norms, religious beliefs, institutional design, and macroeconomic conditions. A comparative analysis of global markets reveals striking divergences in how cognitive compartmentalization manifests across different economic realities 3142324.

Cash-Heavy Emerging Economies: Mobile Money and Survival Accounts

In emerging economies - particularly across Sub-Saharan Africa and Southeast Asia - the digital revolution has bypassed traditional retail banking entirely, leapfrogging legacy systems. The explosive adoption of mobile money, most notably M-Pesa in Kenya and UPI in India, illustrates a unique evolution of mental accounting 15606125. In Africa, 12 out of 15 countries now have more citizens utilizing mobile money than traditional bank accounts, with M-Pesa alone processing over $300 billion annually 15.

In these historically cash-heavy environments, systemic poverty and a lack of access to formal credit fundamentally alter the behavioral life cycle 356026. Low-income households predominantly construct "survival accounts" - mental budgets strictly dedicated to immediate subsistence and risk mitigation against catastrophic shocks like illness or crop failure 35. Mobile money platforms have effectively digitized the traditional, community-based reliance on "wealth-in-people" and informal savings groups (ROSCAs) 6061.

Crucially, mobile money in these regions frequently carries strict mental earmarks that dictate behavior. Experimental evidence from Bangladesh and Kenya (2024 - 2026) demonstrates that digital remittances received via mobile money are often psychologically coded with specific expectations from the sender (e.g., "this money is for school fees" or "this is for preventative health") 2060. Unlike the West, where digital payments definitively increase the propensity to spend frivolously via the credit card premium, the earmarking effect in emerging markets can actually reduce the willingness to spend on discretionary items. The digital wallet acts as a highly disciplined, ring-fenced mental account prioritizing familial obligation and survival over hedonic consumption 152060. Furthermore, religious constraints, such as adherence to Islamic Shariah law which prohibits the payment of interest, force structural adaptations in how credit and deferred payments are mentally accounted for and institutionally provided in many of these regions 24.

Highly Financialized Western Markets: Credit-Driven Compartmentalization

In stark contrast, Western markets (e.g., the United States and the United Kingdom) are characterized by hyper-financialization, abundant access to unsecured credit, and highly individualistic cultural values 141535.

In these economies, the structure of mental accounting is multifaceted and heavily market-oriented. Rather than focusing solely on "survival accounts," middle- and high-income consumers operate complex architectures of "wealth appreciation," "education reserves," and "lifestyle" accounts 1435. The cultural acceptance of debt fundamentally alters financial behavior; taking on leverage is not viewed as a failure of survival, but as an optimized, rational strategy for consumption smoothing and asset acquisition 21824.

Western investors exhibit significantly higher risk tolerance, driven by an individualistic pursuit of outsized returns via diversified equities, mutual funds, and complex financial instruments 14. However, this credit-driven paradigm makes Western consumers acutely vulnerable to the predatory aspects of digital decoupling. The saturation of credit cards, the seamless integration of BNPL at online checkouts, and frictionless digital wallets have largely dismantled the natural friction of physical cash. This leads to record levels of consumer debt and widespread subscription fatigue 5361856. While emerging market consumers use digital wallets to enforce survival-based mental accounting and facilitate vital remittances, Western consumers frequently fall victim to algorithmic choice architectures that intentionally blur the boundaries of their discretionary mental accounts, encouraging systemic over-consumption 51536.

7. Macroeconomic and Policy Implications

The microeconomic reality of mental accounting has profound macroeconomic implications, particularly concerning how governments design and implement fiscal policy. The effectiveness of economic stimulus, tax relief, and monetary transmission is heavily dependent on how the public mentally categorizes those interventions 192728.

When governments issue stimulus checks or adjust tax withholding to inject liquidity into the economy, classical models predict a uniform response based on the permanent income hypothesis. However, behavioral economics proves that the delivery method dictates the spending proportion 143727. Smaller, standalone government transfers are often coded as windfalls and spent immediately, effectively boosting short-term consumption, whereas larger or blended payments may be saved or used for deleveraging 1527. Furthermore, as banks increasingly rely on digital deposits, the "inattention" of depositors - who fail to reallocate unscheduled funds out of low-yield accounts due to mental accounting inertia - allows financial institutions to delay passing through interest rate hikes, directly impacting monetary policy transmission and bank franchise value 1416.

Recognizing that human behavior systematically violates fungibility, policymakers must utilize choice architecture and digital nudging to foster equitable financial environments. This includes designing targeted interventions that guide households to allocate assets rationally, utilizing fintech tools to optimize psychological account management, and regulating the aggressive use of temporal decoupling by BNPL providers 33035.

8. Conclusion

The evolution of mental accounting in the digital age represents one of the most critical transformations in contemporary consumer behavior. Far from being a defunct cognitive error, mental accounting remains an essential psychological scaffolding that allows individuals to exert self-control and navigate the overwhelming complexities of personal finance 178.

However, the migration from analog cash envelopes to the frictionless, algorithmically driven interfaces of modern fintech has fundamentally destabilized this heuristic mechanism. Through the dual forces of physical decoupling (digital wallets) and temporal decoupling (BNPL), digital environments actively neutralize the "pain of paying" that historically enforced budgetary discipline 5. Furthermore, the strategic application of the house money effect, the sunk cost fallacy, and the credit card premium by platforms seeking to maximize user engagement highlights a profound conflict of interest between corporate revenue models and consumer financial well-being 11132256.

As globalization continues, it is evident that the impact of digital finance is not uniform. The divergent realities of M-Pesa users in Kenya utilizing digital wallets for survival earmarking versus Western consumers accumulating debt through gamified trading apps underscore the need for culturally adaptive, context-specific regulations 1415. The challenge for the future of the digital economy is not to eradicate mental accounting, but to design ethical choice architectures that support it. Cultivating robust digital financial literacy and mandating transparency in subscription models and BNPL terms are vital first steps 3530. Fintech innovation must pivot toward mechanisms that intentionally reintroduce positive friction - empowering consumers to leverage their natural cognitive boundaries to achieve resilient, long-term financial stability in an increasingly frictionless world.