Behavioral economic mechanisms of buy-now-pay-later and consumer debt

Introduction

The global consumer credit ecosystem has experienced a fundamental structural shift over the past decade, driven by the rapid proliferation of Buy Now, Pay Later (BNPL) platforms. Operating primarily as point-of-sale installment loans, BNPL allows consumers to defer payments for retail purchases by dividing the total cost into short-term, interest-free installments, typically a "pay-in-four" structure executed over six weeks 123. The global BNPL market achieved a gross merchandise volume (GMV) of approximately $560.1 billion in 2025, capturing roughly 5% to 6% of global e-commerce payment methods, and is projected to expand to $911.8 billion by 2030 4556. User adoption has mirrored this trajectory, with global users estimated to reach 900 million by 2027 58.

Unlike traditional consumer credit, which relies on formalized hard credit inquiries and complex revolving interest structures, BNPL providers utilize localized alternative data and "soft" credit checks to issue instantaneous underwriting decisions directly within the merchant checkout flow 34. This frictionless distribution model has heavily democratized access to short-term liquidity. Demographic data indicates that BNPL usage is disproportionately concentrated among Generation Z, Millennials, and consumers with subprime or deep subprime credit scores, who view the service as a transparent alternative to high-interest credit cards 1481078.

Despite the absence of compounding interest, the aggressive expansion of BNPL has triggered intense scrutiny regarding its underlying behavioral economic mechanisms. Research indicates that BNPL interfaces systematically leverage cognitive biases - such as the illusion of control and temporal decoupling - to artificially reduce the psychological friction associated with spending 1391011. Consequently, evidence suggests that BNPL promotes impulse purchasing and contributes to the accumulation of "phantom debt," a form of fragmented liability that is largely invisible to traditional credit bureaus 121314. This report provides an exhaustive analysis of the behavioral economic drivers behind BNPL adoption, the choice architecture embedded in digital checkouts, the cascading effects on consumer debt profiles, and the subsequent evolution of global regulatory frameworks.

Psychological Mechanisms Driving Utilization

The widespread utilization of BNPL cannot be entirely explained by the economic utility of interest-free capital. Instead, the product's market dominance is deeply rooted in its capacity to manipulate standard behavioral economic heuristics. By fundamentally restructuring the payment timeline, BNPL mitigates the psychological resistance that naturally regulates consumer consumption.

Temporal Decoupling and Payment Depreciation

The "pain of paying" is an established behavioral heuristic wherein individuals experience negative affective emotion when parting with financial resources 9201516. This psychological friction serves as an intrinsic regulatory mechanism against overconsumption. Traditional cash transactions enforce a high pain of paying because the financial exchange is immediate, tangible, and tightly coupled to the acquisition of the good 915.

BNPL amplifies the "cashless effect" through a mechanism known as "temporal decoupling" 1516. By fracturing a single transaction into multiple micro-installments and delaying the majority of the financial consequence into the abstract future, BNPL severs the cognitive link between the hedonic joy of acquisition and the utilitarian burden of cost 91517. Research identifies this as "payment depreciation," where the perceived psychological weight of an item drops significantly when only a fractional down payment (e.g., 25%) is required at the point of sale 101011. This lowering of the financial barrier rapidly closes the dopamine reward loop, satisfying the consumer's desire for instant gratification without necessitating prior financial deliberation 82017. As a result, the average BNPL purchase order is 70% higher than the average credit card transaction in online retail, and users spend approximately 6.4% more per digital order compared to non-users 4810.

Mental Accounting and Perceived Liquidity

Mental accounting theory dictates that individuals evaluate and categorize financial resources in distinct mental portfolios rather than treating wealth as perfectly fungible 1024. BNPL systematically distorts these mental accounts by disrupting simple budget cues. When a consumer uses a standard debit card, the full purchase amount is immediately deducted, providing a real-time, accurate reflection of their remaining liquidity 18.

Conversely, BNPL deferred payments postpone the visible depletion of funds from the consumer's primary checking account 18. Because the platform only deducts the initial installment, consumers operate under an "inflated perception of available funds" 18. Empirical research conducted by central banking institutions demonstrates that this systematic bias profoundly distorts subsequent decision-making. Participants utilizing BNPL were found to be 22.2% more likely to purchase additional discretionary products in subsequent shopping rounds compared to those utilizing debit cards 18. Furthermore, the mere expectation of future access to BNPL functions as a form of "liquidity insurance," increasing current spending via non-deferred methods by 3.1% 18.

The Illusion of Control and Optimism Bias

A core psychological driver facilitating the normalization of BNPL is the "illusion of control" 1392024261928. Traditional credit cards carry the societal stigma of revolving debt, compounding interest, and financial distress. BNPL providers counter this by aggressively framing their products as responsible "budgeting tools" that empower consumers to manage cash flow 102028. This framing preserves the user's illusion of financial caution while facilitating overconsumption 17.

Younger consumers, in particular, often perceive BNPL not as a formal debt instrument, but as an extension of their personal income 2028. This cognitive distortion is reinforced by optimism bias, where individuals systematically overestimate their future income trajectory and budgeting discipline 2026. The fixed, interest-free nature of the installments creates a false sense of predictability. However, the mental burden of managing multiple concurrent repayment schedules across disparate platforms and asynchronous billing dates rapidly induces cognitive overload 2024. What originates as a perceived tool for financial empowerment often transitions into emotional exhaustion, as the consumer underestimates the compounding liquidity risk of fragmented micro-debts 820.

Digital Choice Architecture and Interface Design

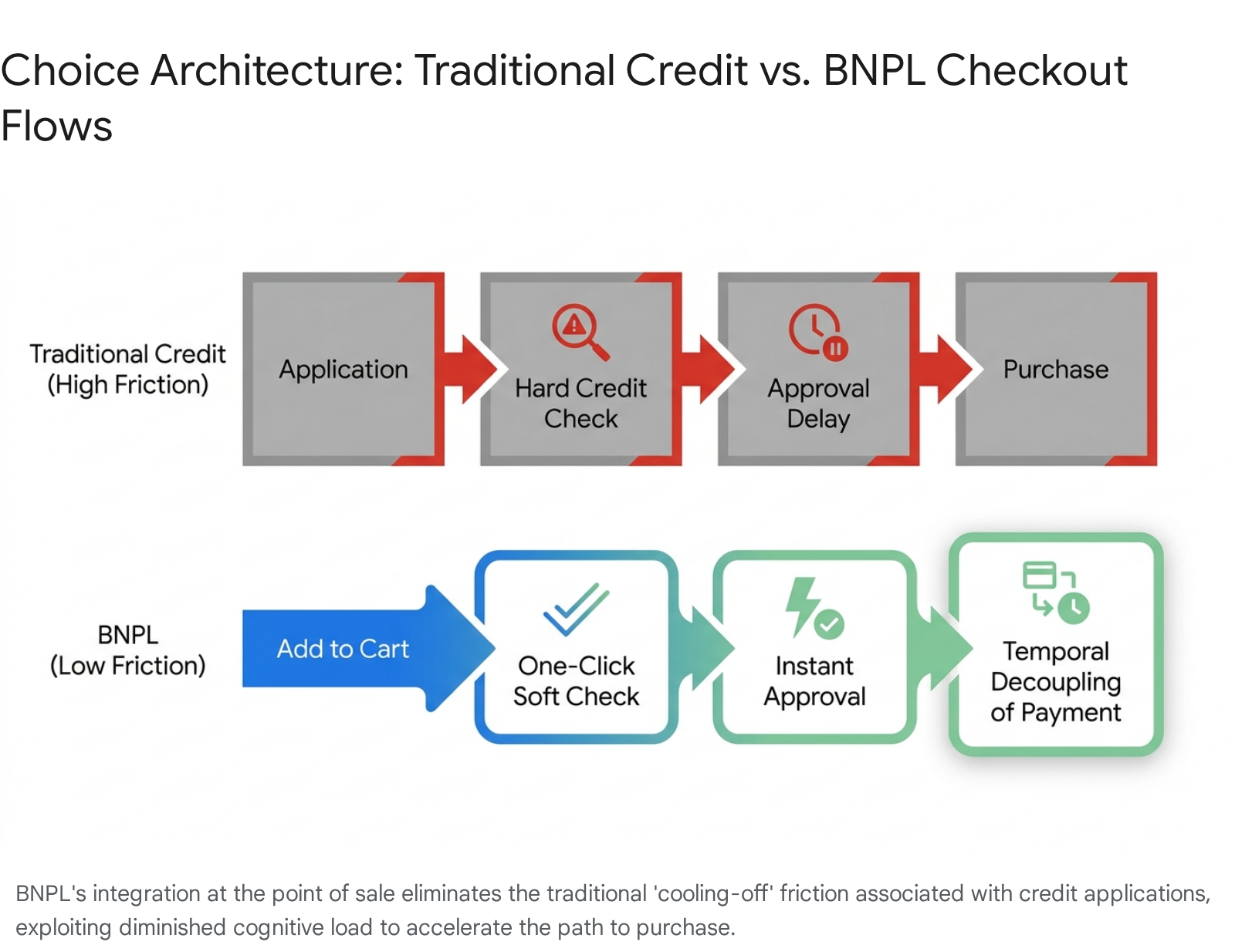

The psychological mechanisms driving BNPL are operationalized through sophisticated digital choice architecture. By integrating the financing option directly into the merchant's checkout flow, BNPL platforms intercept the consumer at the precise moment of highest purchase intent, exploiting periods of diminished cognitive capacity.

Cognitive Load and Frictionless Checkout

Modern e-commerce environments intentionally induce high cognitive load by presenting consumers with continuous micro-decisions regarding product variants, shipping speeds, and promotional add-ons 17. By the time a consumer navigates to the final payment screen, their decision-making energy is severely depleted 17. BNPL providers capitalize on this psychological fatigue by presenting a path of least resistance.

The BNPL application process is engineered to be frictionless, typically requiring only basic contact information to execute a soft credit check and yield instant approval 28203021. This extreme lack of friction acts as a psychological catalyst that strips away the consumer's natural resistance to accumulating debt 28. In traditional consumer lending, the extensive documentation required for approval introduces a deliberate "cooling-off" period, forcing rational deliberation 1521. BNPL's seamlessness actively masks the underlying debt-credit relationship, presenting the loan as merely another payment modality analogous to a debit transaction 2821.

Dark Patterns in Digital Markets

The design strategies utilized within BNPL interfaces frequently cross into the territory of "dark patterns" - interface designs crafted to exploit human psychology and coerce users into target actions 30222324. Academic audits of leading BNPL checkout interfaces have empirically identified multiple dark patterns, including false hierarchies, disguised advertisements, and pre-selected credit options 30212235. Frequently, a BNPL option is visually emphasized with bold colors or pre-selected as the default payment method, nudging consumers toward credit rather than immediate payment 3035.

Furthermore, urgency cues - such as low inventory warnings, limited-time checkout timers, or tailored promotional emails - are frequently deployed alongside BNPL offerings 172526. These tactics amplify the fear of missing out (FOMO) and leverage loss aversion, pushing consumers to utilize BNPL to secure an item before it becomes unavailable, effectively overriding rational affordability assessments 172526. Peer-reviewed studies note that such urgency cues combined with perceived affordability directly correlate with post-purchase regret, a factor often measured indirectly through user reports of subsequent financial distress 2526.

The deployment of these techniques has drawn severe regulatory scrutiny. The United States Federal Trade Commission (FTC) has explicitly warned BNPL providers and partner retailers that optimizing strictly for conversion at the expense of consumer comprehension constitutes a deceptive practice 2739. The FTC's enforcement posture establishes that companies cannot utilize multi-party ecosystems to disclaim liability when consumers are manipulated by interface design 27. Similarly, the UK Advertising Standards Authority (ASA) has published guidance indicating that choice structure manipulation that exploits cognitive biases violates general provisions on misleading advertising 23.

Comparative Architecture: BNPL Versus Traditional Credit

To accurately assess the behavioral and systemic impact of BNPL, it is necessary to contrast its architectural and reporting mechanics directly with traditional credit cards. The divergent approaches to underwriting, friction, and revenue generation dictate distinct behavioral responses from consumers.

| Architectural Feature | Buy Now, Pay Later ("Pay-in-Four") | Traditional Credit Card |

|---|---|---|

| Approval Friction | Extremely low; instant soft credit checks utilizing alternative data 3420. | High; formal applications requiring hard inquiries and documented income 320. |

| Credit Bureau Visibility | Historically invisible ("Phantom Debt"); sporadic and delayed reporting 3121328. | Full visibility; highly standardized monthly reporting to all major bureaus 328. |

| Interest Structure | Zero-interest if paid on time; flat late fees (up to $35) that do not compound 4820. | Compounding revolving interest (APRs often exceeding 22-24%) 81020. |

| Repayment Cadence | Rigid, bi-weekly auto-debits (four installments over six weeks) 13429. | Flexible monthly minimums; allows perpetual balance carrying 820. |

| Psychological Impact | Induces "Temporal Decoupling" and "Illusion of Control" 139201524. | Imposes moderate "Pain of Paying" and high debt salience 9111517. |

| User Demographics | Skews younger (Gen Z/Millennial); high concentration of subprime borrowers 410729. | Broader distribution; dominates among older and prime credit consumers 41029. |

| Merchant Cost | High interchange and platform fees (merchant subsidizes the credit) 31030. | Standard interchange fees (lower than BNPL merchant fees) 330. |

Consumer Debt Accumulation and Financial Stability

While BNPL default rates have historically remained lower than those of traditional credit cards, this surface-level metric masks deeper underlying financial fragility 572931. Because BNPL repayments are typically automated via direct debit to primary checking accounts, defaults are artificially suppressed, but upstream financial stress increases 57. The uncoordinated accumulation of BNPL debt fundamentally alters consumer balance sheets, introducing risks that traditional underwriting models struggle to quantify.

Phantom Debt and Loan Stacking

One of the most profound systemic risks associated with the proliferation of BNPL is the creation of "phantom debt" 5121314283246. Historically, BNPL providers have opted not to report standard "pay-in-four" obligations to the major national credit reporting agencies 35122932. Because these micro-liabilities remain invisible to traditional lenders, consumers can accumulate substantial debt volumes that fail to register in standard debt-to-income (DTI) ratio calculations 12131433.

This opacity facilitates "loan stacking," a practice wherein consumers initiate multiple concurrent installment loans across disparate, competing BNPL platforms 5143133343550. A comprehensive analysis by the Consumer Financial Protection Bureau (CFPB) revealed that 63% of BNPL borrowers held simultaneous loans, with 33% holding obligations across entirely different firms 1013. Lenders, operating blind to a borrower's activities on rival platforms, inadvertently extend credit to heavily over-leveraged individuals. The ease of access, combined with the illusion of control, frequently traps economically vulnerable consumers in a debt treadmill, where new BNPL loans are utilized merely to manage baseline cash flow 315136.

Demographic Vulnerability and Default Metrics

The demographic distribution of BNPL users exacerbates the risks of phantom debt. BNPL adoption is heavily concentrated among financially fragile cohorts. Data from 2021 to 2022 indicates that borrowers with "deep subprime" credit scores (FICO scores between 300 and 579) accounted for 45% of total BNPL originations, while those with "subprime" scores (580 to 619) comprised an additional 16% 10729. Consequently, over 60% of the market volume during this period was extended to high-risk consumers.

A stark divergence exists between official charge-off rates and consumer-reported distress. Industry data frequently cites BNPL charge-off rates hovering between 1.83% and 2.63%, notably lower than the roughly 4.19% charge-off rate observed in commercial bank credit cards during late 2023 5572951. However, consumer surveys indicate a much higher prevalence of financial friction. Estimates suggest that between 34% and 41% of BNPL users report making at least one late payment annually 55102931. This gap illustrates that while auto-debit mechanisms ensure ultimate collection, the process frequently triggers non-sufficient funds (NSF) penalties at the consumer's primary bank, transferring the financial distress away from the BNPL provider and onto the consumer's broader liquidity profile 5832.

Spillovers to Unsecured and Mortgage Debt

The hypothesis that BNPL operates as an isolated financial tool is empirically inaccurate; its usage demonstrates heavy interaction with other debt obligations. While BNPL loans may not natively accrue compounding interest, the financial strain they induce frequently spills over into traditional, interest-bearing credit products 29.

Statistical models demonstrate a strong correlation between heavy BNPL usage (defined as originating more than 12 loans per year) and elevated balances across personal loans, retail loans, alternative financial services, and student loans 729. Notably, BNPL users are significantly more likely to carry revolving balances on traditional credit cards. In 2023, 71% of BNPL users revolved on their credit cards, compared to just 40% of non-users 1. The average credit card utilization rate for BNPL borrowers consistently hovers between 60% and 66%, nearly double the 34% utilization rate observed among non-users 107. This data suggests that consumers frequently deploy BNPL as a "liquidity valve" after exhausting traditional credit limits, pushing their overall debt profile into riskier, highly leveraged territory 11028. Although the Richmond Fed notes there is no definitive proof of a direct causal link between BNPL usage and aggregate unsecured indebtedness, the correlative indicators of financial stress are robust 29.

Furthermore, BNPL intensity serves as a leading indicator for broader macroeconomic distress, notably mortgage delinquency 2832. Research from the JPMorgan Chase Institute highlights that frequent BNPL users possess an 8.1% higher likelihood of missing a mortgage payment within their first year of homeownership 28. This association is most acute among subprime borrowers, who experience a 4.7% increase in delinquency odds 28. Following macroeconomic shocks, such as an involuntary job loss, affected households often keep bureau-reported credit card balances stable to protect their formal credit scores, while covertly shifting incremental spending to BNPL to preserve liquid cash. For lower-income Federal Housing Administration (FHA) homeowners, BNPL obligations can exceed 20% of total spending following a job loss, masking true financial deterioration from mortgage servicers 28.

Credit Reporting Integration and Scoring Evolution

In response to the escalating systemic risk of phantom debt and mounting pressure from federal policymakers, the global credit reporting ecosystem is undergoing structural evolution to ingest point-of-sale installment data.

The Implementation of FICO Score 10 BNPL

A critical inflection point in consumer credit risk assessment is the introduction of updated credit scoring models explicitly designed to capture BNPL transaction history. In 2025, Fair Isaac Corporation (FICO) announced the deployment of FICO Score 10 BNPL and FICO Score 10 T BNPL, representing the first major standardized scoring models to systematically incorporate BNPL repayment data 101253373839. Scheduled for broader implementation throughout 2026, these models seek to equip lenders with a holistic view of a consumer's true liabilities, effectively illuminating the phantom debt blind spot 515337.

The algorithmic logic underpinning these new scores is tailored to the unique cadence of digital installments. The models dynamically aggregate multiple concurrent BNPL loans, preventing the flurry of small, fragmented retail transactions from being penalized identically to standard new-account openings under legacy models 1237. For "credit-thin" consumers or recent immigrants lacking traditional credit histories, consistent, on-time BNPL payments can serve as an accelerated conduit to prime credit access 1251533839.

However, this newfound transparency carries inherent risks for overextended borrowers. Delinquencies and missed payments - which affect roughly 41% of users - will now negatively impact core creditworthiness with the same severity as traditional credit card defaults 5101253. Early FICO simulation data suggests that the aggregate impact of simulated BNPL inclusion is relatively modest for the majority: 85% of BNPL customers experienced score changes of fewer than 10 points, and 97% of highly active BNPL users (5+ accounts) experienced score changes of fewer than 20 points 1237.

Bureau Reporting Resistance and Standardization

Despite these technological advancements, the efficacy of the FICO 10 BNPL models relies entirely on the voluntary participation of BNPL providers to furnish the data, and the willingness of mainstream lenders to adopt the updated, potentially costlier, scoring models 5337. While major platforms like Affirm and Klarna have initiated data reporting to bureaus like Experian and TransUnion, others continue to resist full integration 1253. Providers opposing integration argue that legacy scoring paradigms inherently misinterpret the rapid churn of micro-installments as elevated credit risk, potentially penalizing responsible borrowers 329.

Consequently, lawmakers in the U.S. Senate have exerted heavy pressure on the major credit bureaus to standardize BNPL data intake via the Metro 2 format 36. The lack of a uniform reporting standard across agencies allows consumers to appear artificially creditworthy to traditional lenders, while simultaneously preventing responsible BNPL users from fully realizing the credit-building benefits of their timely payments 36.

Evolving Regulatory Frameworks

As the behavioral impacts and systemic risks of BNPL have crystallized, global regulatory bodies have transitioned from observation to active legislative intervention. The regulatory landscape entering 2026 is characterized by a complex, fragmented patchwork of regional approaches, focusing predominantly on mandatory affordability checks, the eradication of dark patterns, and the formal classification of BNPL as traditional credit.

United States: Federal Volatility and State Action

The trajectory of BNPL regulation in the United States has been marked by significant volatility and legal contention. In May 2024, under the Biden administration, the Consumer Financial Protection Bureau (CFPB) issued an interpretive rule explicitly bringing BNPL providers under the purview of the Truth in Lending Act (TILA) and Regulation Z 155740. This mandate sought to formally classify BNPL platforms as credit card providers, requiring them to issue periodic billing statements, provide standardized cost-of-credit disclosures, and grant consumers the right to dispute charges and secure refunds for returned merchandise 155740.

However, the industry, spearheaded by the Financial Technology Association (FTA), aggressively litigated the mandate. The FTA argued that the interpretive rule bypassed the Administrative Procedure Act and that the structural mechanics of "pay-in-four" loans did not map to legacy credit card statutes 65740. Following a shift in the federal administration, the CFPB formally withdrew the interpretive rule in May 2025 565740. The agency declared the original rule procedurally defective and signaled a stark deprioritization of federal BNPL enforcement 565740.

This resulting federal vacuum has catalyzed aggressive state-level intervention. Democratic-led states have moved rapidly to assert direct supervisory authority over fintech lending. Most notably, the New York Department of Financial Services (NYDFS) enacted robust legislation classifying BNPL as "closed-end credit" 39574142. The New York framework requires BNPL providers to secure explicit state licenses, adhere to strict 16% usury caps, comply with heightened disclosure requirements regarding dark patterns, and formally verify consumer affordability 39574142. Furthermore, multi-state coalitions - led by attorneys general in states such as Connecticut, North Carolina, and California - are increasingly leveraging unfair, deceptive, or abusive acts and practices (UDAAP) statutes to investigate BNPL data harvesting and interface manipulation 34574142.

Europe and the United Kingdom: Mandatory Affordability

Internationally, regulatory regimes are moving with greater cohesion to directly address the behavioral economics of digital lending.

In the European Union, member states are finalizing the implementation of the updated Consumer Credit Directive (CCD II), which comes into full enforcement in 2026 63561. CCD II intentionally eliminates previous regulatory loopholes that exempted short-term, interest-free credit from oversight 661. It mandates real-time creditworthiness checks that must accurately assess repayment ability without introducing unnecessary checkout friction, a difficult technological balance 3561. Crucially, the directive explicitly bans the marketing of credit through misleading dark patterns, definitively forbidding the pre-selection of BNPL by default at online checkouts 35.

The United Kingdom is undertaking a similar structural overhaul. By mid-2026, third-party BNPL providers (e.g., Klarna, Clearpay) will fall under the comprehensive supervision of the Financial Conduct Authority (FCA) 6143. The FCA's framework introduces mandatory affordability and creditworthiness assessments prior to extending credit 43. This requirement deliberately disrupts the rapid, frictionless model upon which BNPL growth historically relies, forcing providers to invest heavily in compliance infrastructure 43. Interestingly, the UK framework currently retains an exemption for BNPL offered directly by merchants (under Article 60F(2)), creating a two-tier regulatory system that industry observers warn may lead to significant competitive imbalances 6143.

Africa and Emerging Markets: Mobile Money and B2B BNPL

Emerging markets are experiencing explosive BNPL adoption as digital credit proliferates via mobile money ecosystems. In Africa, the BNPL market is projected to grow from $5.2 billion in 2025 to $16.8 billion by 2031, anchored by super-apps and platforms in Nigeria, Kenya, South Africa, and Egypt 6444. A unique driver in this region is the dominance of B2B (Business-to-Business) BNPL, embedded within FMCG (Fast-Moving Consumer Goods) platforms, enabling small retailers to secure inventory via algorithmic underwriting 6444.

To prevent debt spirals among economically vulnerable populations, regulatory bodies are instituting strict digital lending frameworks. The Federal Competition and Consumer Protection Commission (FCCPC) in Nigeria and the Central Bank of Kenya (CBK) have enacted regulations requiring explicit licensing for non-deposit-taking credit providers 45. These frameworks emphasize mandatory reporting to credit bureaus, curb aggressive debt collection practices, and enforce transparent disclosures 4445. As compliance and capital costs rise, the African BNPL landscape is expected to consolidate, favoring well-capitalized, bank-backed models over smaller, highly leveraged fintechs 4467.

Conclusion

Buy Now, Pay Later services represent a foundational paradigm shift in consumer finance, successfully leveraging principles of behavioral economics to restructure the retail environment. By employing temporal decoupling, BNPL significantly reduces the psychological pain of paying. Simultaneously, its frictionless choice architecture - frequently augmented by interface dark patterns - exploits cognitive load to encourage impulsive, instant gratification. The framing of these services as benign budgeting tools cultivates an illusion of control, effectively masking the realities of debt accumulation from the consumer.

While the absence of compounding interest provides genuine economic utility for highly disciplined users, the macro-level impact reveals a concerning accumulation of phantom debt. The prevalence of loan stacking, coupled with pronounced spillover effects into unsecured and mortgage debt, highlights the financial fragility of consumers relying on invisible credit to sustain baseline consumption. As the industry matures into 2026, the integration of BNPL data into sophisticated scoring models like FICO Score 10 BNPL, alongside aggressive state and international regulatory interventions, signals the end of the unregulated digital credit frontier. Ultimately, while BNPL provides unprecedented transactional fluidity, the convergence of strict affordability checks and transparent credit reporting will be vital in ensuring that the mitigation of checkout friction does not result in systemic financial instability.