Retail Disruption Theory and E-commerce Platforms

The architecture of global retail is undergoing a structural realignment driven by digital platform ecosystems, advanced algorithmic supply chains, and shifting consumer expectations. Historically, the evolution of retail markets has been interpreted through a sequence of theoretical frameworks, most notably Malcolm P. McNair's Wheel of Retailing and Clayton M. Christensen's theory of Disruptive Innovation. As incumbent digital retailers transition into mature market leaders pursuing sustaining innovations, a new cohort of consumer-to-manufacturer (C2M) platforms and social commerce applications has emerged. These platforms leverage unprecedented supply chain integration, data-driven production, and hyper-aggressive pricing strategies to capture market share.

Theoretical Frameworks of Retail Evolution

Before the advent of digital commerce, the evolution of retail structures was largely understood through cyclical, environmental, and conflict models that mapped the predictable life cycles of physical retail formats. Understanding these foundational theories provides essential context for analyzing modern e-commerce dynamics.

The Wheel of Retailing Hypothesis

Introduced by Malcolm P. McNair in 1958, the Wheel of Retailing theory suggests that retail businesses evolve through a predictable, cyclical process 113. The hypothesis posits that new types of retailers invariably enter the market as low-status, low-margin, and low-price operators 12. In this entry phase, these retailers attract cost-conscious consumers by offering limited services, basic facilities, and minimum operational overhead 125.

As these firms achieve market traction and secure a customer base, they enter a "trading-up" phase. During this period, retailers reinvest capital to enhance their store facilities, expand product assortments, and introduce supplementary customer services 12. This strategic maturation inevitably increases the retailer's cost structure, forcing an upward adjustment in pricing and profit margins to support the new operational baseline 12. Ultimately, the retailer reaches a mature phase characterized by high levels of service, extensive product assortments, and premium pricing 15. This high-cost position renders the firm vulnerable to a new generation of low-cost entrants, who enter at the bottom of the market and restart the cycle 112.

The Wheel of Retailing successfully explained the rise and subsequent vulnerability of department stores, discount houses, and mid-market supermarkets throughout the 20th century 2. Department-store merchants, who originally appeared as vigorous, low-cost competitors to smaller specialty retailers, eventually became vulnerable to discount houses and supermarkets following this exact pattern 2. However, the hypothesis exhibits limitations in the modern era. It oversimplifies retail evolution by focusing primarily on sequential cost and status progressions, often neglecting the nonlinear impacts of technological advancements, abrupt shifts in consumer behavior, and the complexities of globalized supply chains 15.

Retail Life Cycle and Environmental Models

Building upon the cyclical nature of the Wheel, the Retail Life Cycle theory applies the classic product life cycle framework to retail formats 11. This concept was developed in response to the weaknesses of the Wheel of Retailing, specifically its narrow focus on cost margins 2. The Retail Life Cycle theory categorizes format evolution into four distinct stages: introduction, growth, maturity, and decline 112.

The introduction phase is marked by high innovation and experimentation, where a novel retail format emerges 11. This is followed by a growth phase, characterized by rapid store expansion and broad market acceptance 12. Maturity brings market saturation and intensified competition, eventually leading to a decline phase if the retailer fails to adapt to shifting consumer preferences, technological disruptions, or the emergence of newer retail formats 1. At this point, the retailer faces store closures or the necessity of format reinvention 12.

Parallel to these cyclical models is the Environmental Theory of retail development, which emphasizes external macro-forces as the primary drivers of retail evolution 12. Under this framework, retail formats mutate in constant adaptation to external pressures, such as economic conditions, regulatory frameworks, demographic shifts, and technological breakthroughs 12. The current macroeconomic environment - characterized by persistent inflation, elevated interest rates, and a cost-of-living squeeze - creates an environmental catalyst that uniquely favors the emergence of ultra-low-cost e-commerce models 678. Furthermore, Conflict Theory emphasizes the competitive nature of retailing, illustrating how strategic maneuvers between competing retail formats generate innovation that ultimately benefits the consumer through lower prices and better services 12.

| Theoretical Framework | Core Mechanism | Evolutionary Trajectory | Modern Applicability and Limitations |

|---|---|---|---|

| Wheel of Retailing | Cyclical margin expansion | Low-cost entry $\rightarrow$ Service upgrades $\rightarrow$ High-cost vulnerability | Fails to fully account for digital platforms that scale services without proportionally increasing physical overhead costs 5. |

| Retail Life Cycle | Format maturation | Introduction $\rightarrow$ Rapid Growth $\rightarrow$ Saturation $\rightarrow$ Decline | Highly relevant for tracking the stagnation of traditional mall-based and big-box physical formats 1. |

| Environmental Theory | External adaptation | Formats mutate based on macroeconomic, technological, and social pressures | Accurately explains the post-2022 surge in value-driven cross-border e-commerce due to global inflation 17. |

| Conflict Theory | Competitive friction | Dialectic synthesis of opposing retail formats | Explains the convergence of social media and commerce as platforms integrate competing functionalities 12. |

Clayton Christensen and Disruptive Innovation Theory

While early retail theories described format evolution, Clayton M. Christensen's theory of Disruptive Innovation provided a rigorous economic rationale for why successful, well-managed companies consistently fail to defend against new entrants. Introduced in his 1997 book The Innovator's Dilemma, the theory reshaped how businesses understand technological and market change 345.

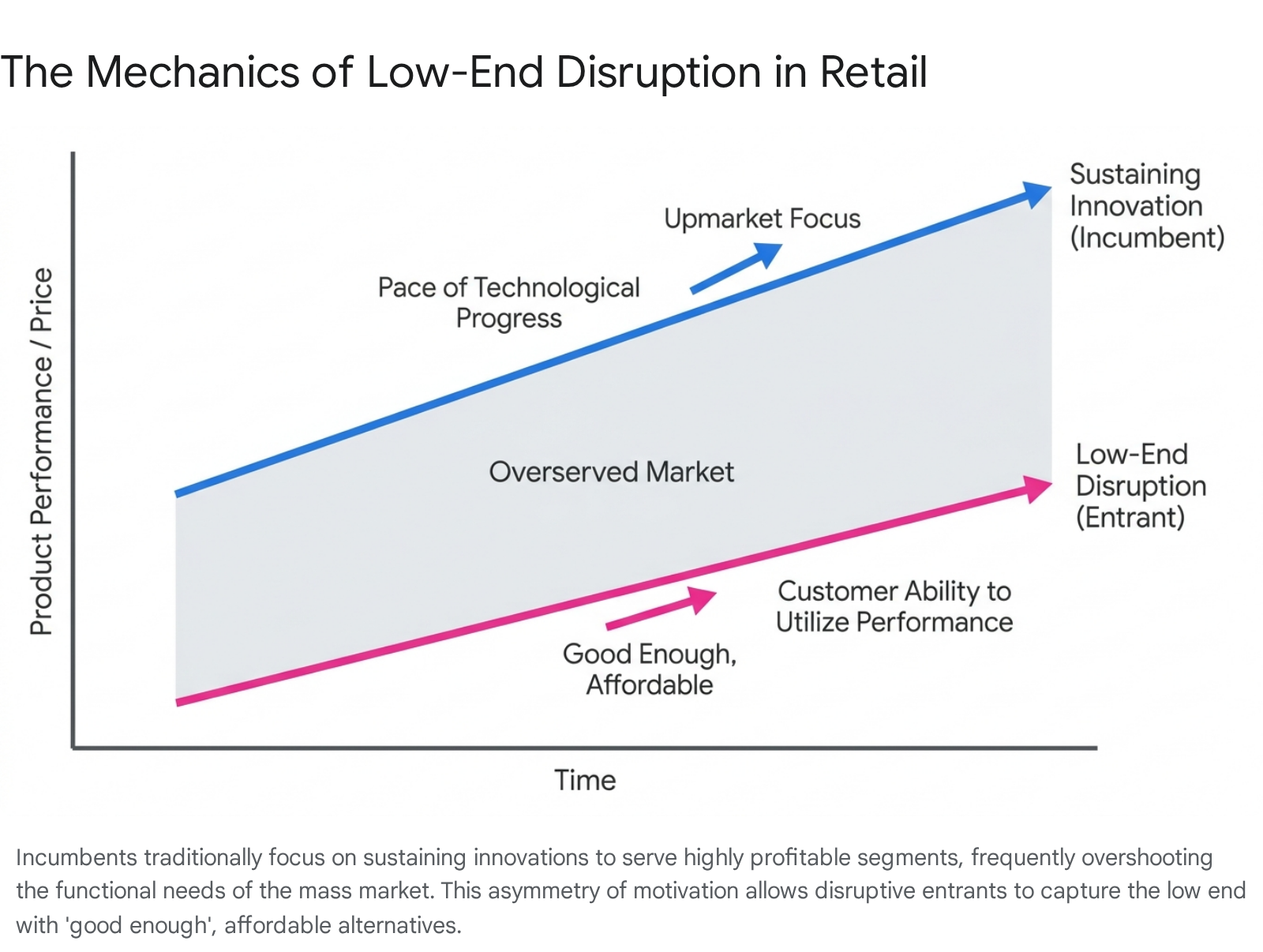

The Mechanics of Low-End Disruption

Christensen defined disruption as a specific process - not a single event - whereby a smaller company with fewer resources successfully challenges established incumbent businesses 56789. Low-end disruption occurs when incumbents focus aggressively on improving their products and services for their most demanding, high-margin customers 578. In doing so, these market leaders introduce product performance and features that exceed the actual needs of the broader market, a phenomenon known as overshooting 710.

This creates a strategic vacuum at the bottom of the market. A disruptive entrant steps into this void by deploying a low-cost business model to offer a product that is technologically straightforward and possesses lower absolute performance than the incumbent's premium offering 81011. Crucially, this product is "good enough" to satisfy the functional requirements of overserved, highly price-sensitive consumers 78101118.

The defining characteristic of low-end disruption is the asymmetry of motivation. Because the lower tiers of the market yield the slimmest profit margins, incumbent leaders are rarely motivated to fight a price war against the new entrant 101812. Instead, the rational management decision is to flee upmarket, abandoning the low-end segment to protect aggregate profitability and adhere to established business models 310181220. Uncontested, the disruptor secures a foothold, captures market share, and gradually improves its product quality. Over time, the disruptor relentlessly moves upmarket until it achieves the performance expected by mainstream customers, eventually displacing the incumbent 3513.

New-Market Disruption and Sustaining Innovations

In addition to low-end disruption, Christensen identified new-market disruption. This occurs when an innovation is so affordable, simple to use, and accessible that it transforms non-consumers into consumers, effectively creating an entirely new market segment 810111314. These disruptive products initially compete against nothing at all, as the target demographic previously lacked the financial resources or technical skills to utilize existing solutions 18. The early personal computer, which brought computing power to individuals who previously lacked access to mainframes, serves as a classic historical example 1814. Similarly, Sony's first transistor radio targeted teenagers who previously had no access to affordable, portable audio devices 14.

In strict contrast, sustaining innovations aim to improve existing products along traditional performance dimensions valued by mainstream and high-end customers 35818. Sustaining innovations entail making a "better mousetrap" 14. They can be incremental, such as faster microprocessors, or radical breakthroughs, but their fundamental economic purpose remains identical: allowing incumbents to sell better products for higher margins to their best customers 351813. Incumbents almost universally win battles of sustaining innovation because their entire organizational structure, resource allocation, and incentive models are optimized for this specific pursuit 1815.

Theoretical Misconceptions and Refinements

Over the past two decades, the term "disruption" has been frequently misapplied, particularly in the technology and startup sectors, to describe any successful, rapidly growing company that shakes up an industry 57916. Christensen and his co-authors, including Michael Raynor and Rory McDonald, explicitly sought to correct these misconceptions in a 2015 update to the theory 5616. They noted that disruption is a specific theory of competitive response, not a general theory of growth or corporate success 69.

A prominent example of this misapplication is Uber. While widely heralded as a disruptive innovator, Christensen argued that Uber did not fit the strict definition of disruption 561116. Uber did not originate by serving the low-end of the market with a sub-standard product, nor did it create a new market of non-consumers 511. Instead, it launched in San Francisco targeting the mainstream taxi market with an arguably superior, more convenient service 511. Uber succeeded through a superior business model and rapid scaling, rather than through the asymmetric retreat of incumbents abandoning the low end 11.

Similarly, innovations that enter at the high end of the market, such as Tesla, simply do not fit the disruption definition 6. Christensen also clarified that the popular mantra "disrupt or be disrupted" can be dangerously misleading 916. Incumbent companies should not overreact to disruption by dismantling still-profitable core businesses; instead, they should continue to strengthen relationships with core customers through sustaining innovations, while simultaneously creating separate divisions to pursue the growth opportunities arising from the disruption 59.

The Evolution of E-commerce Incumbents

To properly contextualize the current wave of retail disruption, it is necessary to establish the historical and current positioning of contemporary retail incumbents. Over the past two decades, companies that were once considered aggressive disruptors have matured, structurally shifting their operations toward sustaining innovations and premium market positioning.

Amazon as a Historical Disruptor

In its formative years, Amazon functioned as a textbook example of an e-commerce disruptor by choice 31215. By bypassing the physical constraints of traditional brick-and-mortar bookstores, Amazon utilized a highly scalable, digital-first business model to offer an unprecedented selection of inventory at lower prices 31215. Traditional retailers, burdened by localized inventory limitations and heavy real estate costs, initially viewed online retail as a low-margin niche and failed to respond effectively 17.

In alignment with Christensen's theory, established players retreated to their core competencies, effectively ignoring the low-end threat until Amazon's logistics network and platform infrastructure had improved sufficiently to capture the mainstream market 1217. Amazon systematically expanded its product categories, moving up the value chain from books to consumer electronics, apparel, and eventually enterprise cloud computing via AWS 3. This evolutionary path contrasts starkly with early online grocery attempts like Webvan, which attempted a massive, capital-intensive infrastructure build-out to disrupt supermarkets but failed due to scale limitations, and Peapod, which pursued a nondisruptive, high-end sustaining strategy by partnering with existing supermarkets 15.

Incumbent Sustaining Innovations and Omnichannel Strategies

Today, Amazon, alongside traditional massive brick-and-mortar giants like Walmart and Target, occupies the role of the established incumbent 181920. The strategic imperatives of these corporations are now firmly rooted in sustaining innovations designed to maximize revenue from their most loyal and demanding customer bases 2921.

Walmart has heavily invested in technology and store modernization, planning to open over 150 new "Store of the Future" concepts in 2025 and remodeling 650 existing locations 293122. These locations feature modern layouts, interactive digital touchpoints, QR codes, and AI-powered inventory management 3122. Furthermore, Walmart is aggressively expanding its omnichannel fulfillment capabilities, leveraging its network of over 4,600 U.S. stores to offer same-day delivery to 95% of U.S. households 292131.

Target has similarly prioritized store modernization, though it has faced recent struggles with comparable sales growth compared to Walmart and Costco, leading to the creation of an "acceleration" office to improve tech deployment and streamline operations 1923. Costco continues to rely on its highly successful membership model, driving recurring revenue through bulk savings and strict product curation, demonstrating sustained strength with 8.1% full-year sales growth in 2025 192024. Amazon's core retail offering is now heavily tethered to its Prime membership ecosystem, which guarantees rapid delivery, streaming media, and exclusive services for a premium annual fee 2035.

These initiatives - ultra-fast delivery, high-touch omnichannel integration (Buy Online, Pick Up In Store, or BOPIS), and AI-driven personalization - are classic sustaining innovations 6182925. They make the shopping experience objectively better, but they inherently increase the structural cost of operations and the baseline price of goods required to sustain those vast logistics networks 1829.

Marketplace Maturation and Fulfillment Economics

As direct retail margins have compressed due to fulfillment costs and macroeconomic headwinds, Western incumbents have pivoted toward high-margin service models. Amazon and Walmart now generate massive operating income from Retail Media Networks (RMNs) and third-party seller fees 26. For example, Walmart's retail media business reached $2.94 billion in 2023 26.

Amazon's commission and fulfillment fees for third-party sellers via Fulfillment by Amazon (FBA) add significant structural costs to the end consumer. FBA requires sellers to ship inventory in bulk to Amazon warehouses, incurring storage fees and peak season surcharges 27. In 2024, fulfillment fees for a standard one-pound unit ranged from $3.22 to $3.77 in the U.S., while oversized units exceeded $9 per order 27. Additionally, sellers face long-term storage penalties and strict labeling requirements 27. While FBA provides unparalleled delivery speed and access to Prime members, it establishes a high cost floor 2728. Amazon's standard commission on third-party marketplace sales typically ranges around 15% of the sale price 29.

This upmarket migration, massive infrastructure investment, and reliance on platform taxation have created the precise conditions Christensen described for low-end disruption. The incumbents have overshot the baseline functional needs of a massive cohort of consumers who simply want inexpensive goods and are willing to sacrifice delivery speed and premium branding to acquire them 730.

The Consumer-to-Manufacturer E-commerce Model

Into the vacuum created by the upmarket trajectory of Amazon and Walmart steps a new generation of cross-border e-commerce platforms originating in Asia, most notably Pinduoduo (PDD Holdings), Temu, and Shein. These platforms execute disruption not merely through lower prices, but through fundamental business model innovation deep within the manufacturing supply chain.

Structural Mechanics of Consumer-to-Manufacturer Frameworks

The foundational engine driving this new wave of retail is the Consumer-to-Manufacturer (C2M) model 423144. Traditional retail supply chains operate on a linear, top-down forecasting model: market demand influences brands, brands dictate production to factories, factories supply wholesalers, wholesalers supply retailers, and retailers hold inventory to sell to consumers 32. This model is inherently inefficient, resulting in long lead times, significant inventory risk, high physical overhead, and multiple layers of margin markups 3233.

The C2M model reverses and flattens this architecture. Platforms like Pinduoduo, Temu, and Shein act as direct data conduits between global consumer behavior and the factory floor 423234. By analyzing real-time search data, social media trends, and localized purchasing habits, platform algorithms dictate production schedules directly to networks of thousands of small and mid-sized manufacturers 323334.

Shein, for example, utilizes predictive analytics to test micro-batches of new apparel designs directly on its application 48. If a design generates high engagement, the algorithm triggers automated production scaling; if it fails, production is halted immediately, minimizing inventory waste 3348. This allows Shein to operate on a 3-to-7 day production cycle, compared to the 3-to-6 months required for traditional retailers, releasing up to 1.5 million items into the U.S. market in a single year 33.

Pinduoduo originally leveraged this C2M model domestically in China, aggregating consumer demand for agricultural and consumer goods, guaranteeing volume to manufacturers in exchange for absolute bottom-tier pricing 31355036. This efficient supply chain guides upstream manufacturers to achieve mass customization and sustainable cost advantages by eliminating distribution and inventory steps 503637. This exact backend infrastructure now powers PDD Holdings' international expansion via Temu 443453.

Fully Managed Logistics Models

To facilitate this disruptive C2M model on a global scale, these platforms have introduced novel logistics structures that deeply contrast with Amazon's FBA system.

Under the "Fully Managed" (or consignment) model, the e-commerce platform assumes total operational control of the retail process 543856. The manufacturer's sole responsibility is to produce the goods and ship them to domestic forward-operating warehouses, primarily located in China's Guangdong province 3238. The platform - such as Temu - handles pricing, marketing, international air-freight logistics, refunds, and last-mile delivery 3856.

Because the platform negotiates the wholesale supply price and controls the final retail markup, it can continuously suppress prices to capture market share 5438. Under this model, Temu's effective commission to the seller is only 2-5% 56. Temu absorbs significant logistical costs to acquire customers; the logistics cost per order under the fully managed model is roughly $9 to $10, consisting of warehousing, international air freight, and last-mile delivery 54. This model effectively abstracts the complexities of cross-border commerce for Chinese manufacturers, allowing them to focus entirely on their core competency of production efficiency 323856.

Semi-Managed Logistics Transitions

As platforms mature and face logistical bottlenecks, changing tariff regulations, or the need to sell bulkier items, they transition toward "Semi-Managed" or direct fulfillment models 323856. Introduced by Temu in March 2024, the semi-managed model shifts inventory responsibility back to the seller 3856.

In this framework, manufacturers or third-party sellers utilize their own overseas warehouses and handle localized fulfillment directly to the consumer 3856. The platform continues to provide algorithmic traffic and marketing support, charging a higher referral fee of 8% to 15% 56. While this model places the burden of logistics on the seller, it allows the platform to offer significantly faster delivery times (3-to-5 days versus 9-to-12 days for fully managed) and increases the Average Order Value (AOV) from approximately $40 to $65 5438. Even under the semi-managed model, Temu's prices reportedly remain 20-30% below Amazon's 38.

| Operational Metric | Amazon FBA (Incumbent) | Temu Fully Managed (Consignment) | Temu Semi-Managed (Direct) |

|---|---|---|---|

| Pricing Authority | Controlled by 3rd-party seller | Controlled entirely by platform | Set by seller, constrained by platform limits |

| Inventory Location | Domestic U.S./EU warehouses | Origin-country forward warehouses | Seller-owned localized overseas warehouses |

| Primary Fulfillment | Ocean/Air freight $\rightarrow$ 1-2 day local | Direct-to-consumer international air | Localized fulfillment via domestic carriers |

| Platform Commission | ~15% plus high storage/fulfillment fees | Low margin markup (2-5% effective) | 8-15% referral fee 56 |

| Delivery Speed | 1-2 days (Prime) | 9-12 days | 3-5 days |

| Average Order Value | Variable by category | ~$40 | ~$65 5438 |

Social Commerce and Algorithmic Discovery

While C2M platforms disrupt the supply chain, the frontend of the consumer experience is undergoing a parallel disruption through the convergence of social media and e-commerce.

Social commerce represents a fundamental shift in how consumers discover and acquire goods, effectively collapsing the traditional retail funnel 63940. Platforms like TikTok Shop have transformed the digital environment by embedding native purchasing capabilities directly into short-form video content 65960. Rather than a consumer experiencing intent, navigating to a marketplace like Amazon, executing a search, and filtering reviews, social commerce pushes hyper-personalized product recommendations into an entertainment feed 3959.

This "discovery-based" shopping model relies on impulse purchasing driven by gamification, influencer endorsements, and real-time live streams 483961. Because TikTok Shop has integrated the shopping experience directly into its current UI, users can purchase without leaving the app, generating conversion rates significantly higher than traditional social platforms 395960. The algorithm serves as an active merchant, anticipating needs and manufacturing desire rather than passively fulfilling a search query 3248.

A critical component of this frontend disruption is the shift in trust mechanisms. Traditional e-commerce relies heavily on aggregated, anonymous customer reviews and brand reputation to establish trust - a paradigm where Amazon maintains a distinct advantage 354062. However, social commerce utilizes the parasocial relationships between influencers and audiences to bypass traditional brand building 5961. According to TikTok data, 65% of users rely on creator recommendations when making purchasing decisions, substituting the authority of a legacy brand with the perceived authenticity of a content creator 59.

Despite this innovation, social commerce faces distinct headwinds. The integration of aggressive retail monetization into social feeds can degrade the user experience, leading to platform fatigue among users inundated with products 59. Furthermore, establishing the authenticity of products and navigating the high costs of continuous video content creation remain significant barriers for smaller merchants attempting to utilize these channels 60.

Analyzing Modern Platforms Through the Disruption Lens

Evaluating platforms like Temu, Shein, and TikTok Shop against Clayton Christensen's theoretical framework reveals both striking alignments and profound deviations. These platforms clearly utilize low-end strategies, but their massive scale and execution speed challenge the assumption that disruption is inherently a gradual, under-resourced process.

Alignment with Low-End Disruption Characteristics

In many respects, C2M e-commerce perfectly exemplifies Christensen's low-end disruption model.

First, these platforms aggressively target the overserved. As Amazon and Walmart optimized for rapid delivery, premium subscriptions, and comprehensive retail media ecosystems, their baseline pricing naturally escalated 2630. A vast segment of the consumer base, particularly in an era of inflation and cost-of-living pressures, is highly price-sensitive and willing to endure 9-to-12-day shipping times if the financial discount is substantial 673038.

Second, they operate on the "good enough" standard. Consumers purchasing from Temu or Shein frequently acknowledge that the product quality may be inferior to premium brands, yet it crosses the threshold of utility 77. For example, a $23 electric foot massager from Temu serves its functional purpose "well enough" compared to a $35 equivalent on Amazon, while Shein's average unit price of $8 dramatically undercuts traditional fast fashion 729.

Third, they initially induced incumbent retreat and paralysis. When the disruptors first entered, incumbents avoided direct price wars. Amazon and Walmart cannot completely abandon their domestic logistics infrastructure to match direct-from-China C2M price points without severely cannibalizing their margins and alienating their high-end customer base 182030.

Ecosystem Disruption and Theoretical Deviations

Where the modern iteration of e-commerce diverges from Christensen's model is in the resource capitalization and speed of the disruptors 20. Traditional theory posits that a disruptive entrant begins with fewer resources and inferior technology, slowly chipping away at the bottom of the market 578.

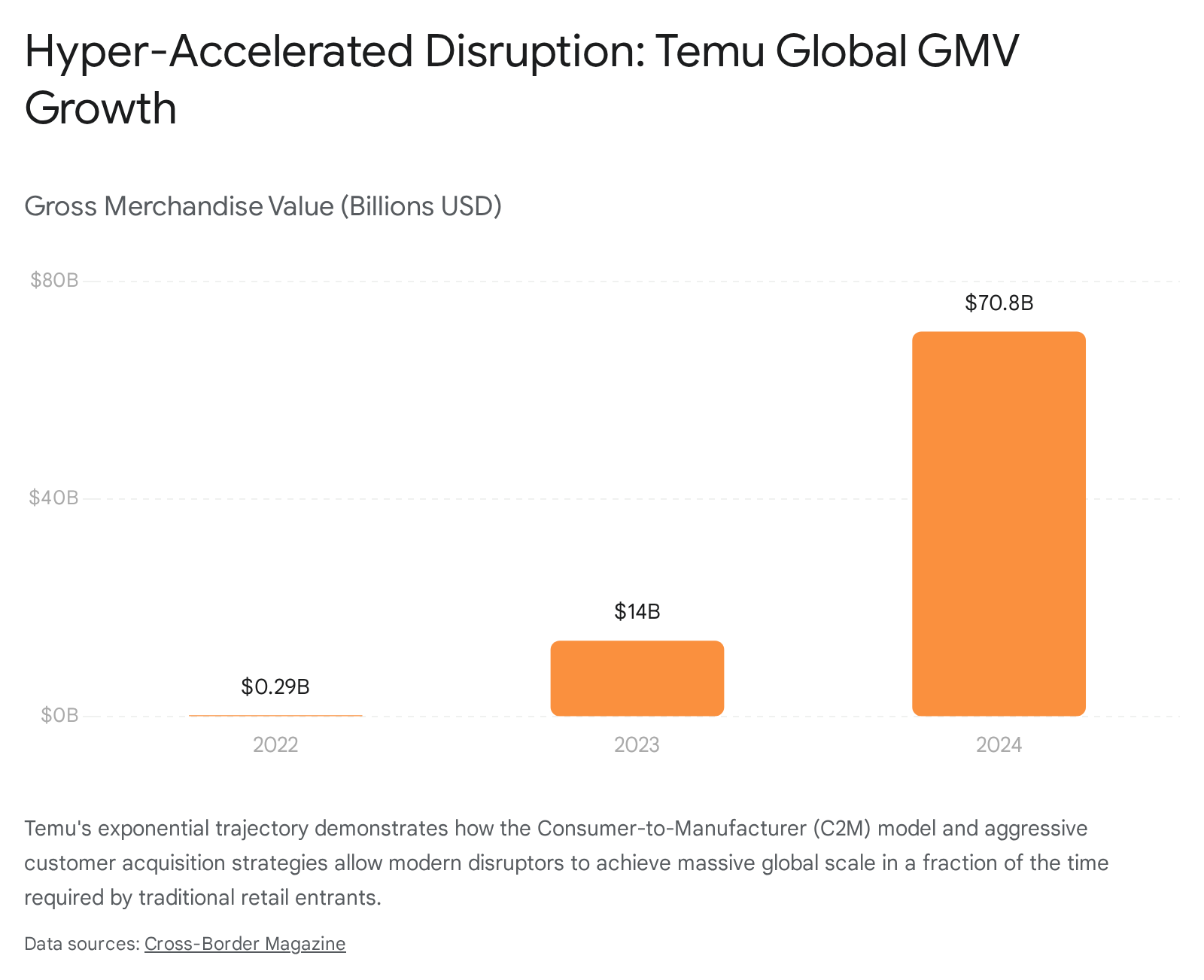

Temu did not begin as an under-resourced startup. Backed by the massive financial and technological infrastructure of PDD Holdings, Temu launched in the United States with overwhelming marketing capital, including multiple $14 million Super Bowl advertising campaigns and billions in digital ad spend 3461. Furthermore, the underlying technology - the AI-driven C2M algorithmic engine - is not technologically inferior to the incumbent's systems; in supply chain synchronization, it is arguably superior 2042.

This dynamic is better described as ecosystem disruption. The threat to Amazon and local retailers does not come from a single inferior product steadily improving, but from an entirely alternative, fully capitalized macroeconomic supply chain imposing itself globally at unprecedented speed 2042. Temu matched Amazon's 25% share of the global cross-border e-commerce market in less than three years - achieving a scale of penetration that took established players decades to build 3963.

Incumbent Strategic Responses

Christensen noted that the ultimate test of disruption is the competitive response 69. Unlike the classic narrative where the incumbent completely ignores the threat until it is too late, leading U.S. retailers have recognized the erosion of their low-end market share and have initiated defensive maneuvers.

Amazon, breaking from its traditional operational mold of sustaining innovations, launched "Amazon Haul" and "Amazon Bazaar" to directly compete with Temu and Shein 2963. These initiatives explicitly mimic the disruptors by offering ultra-low-priced goods (capped at $20) with extended delivery windows 63. However, early data suggests these defensive actions lag behind the disruptors; a 2025 Omnisend survey found 28% of U.S. consumers shop on Temu monthly, compared to 16% for Amazon Haul 63. Simultaneously, Walmart is leveraging its massive domestic store network to enhance its omnichannel superiority, utilizing physical retail proximity - a variable cross-border platforms cannot easily replicate - as a defensive moat against digital-only entrants 2029.

Constraints and Vulnerabilities in the Disruptive Trajectory

While C2M platforms have achieved massive initial success, their trajectory to mainstream market dominance is heavily constrained by structural, regulatory, and perception headwinds. To fulfill Christensen's model of completely displacing incumbents, these disruptors must successfully move upmarket, a transition fraught with significant barriers.

Tariff Policies and Regulatory Interventions

The economic viability of the fully managed, direct-from-China logistics model has relied extensively on exploiting the de minimis customs provision 3064. Under historical U.S. and EU law, packages valued under a specific threshold (e.g., $800 in the U.S.) entered the country duty-free, providing cross-border e-commerce platforms a massive structural advantage over domestic retailers who pay bulk import tariffs 3064.

However, the regulatory environment surrounding global trade shifted aggressively in 2025. Moves to eliminate or severely restrict the de minimis exemption, alongside the imposition of steep universal tariffs on Chinese goods, mathematically alter the unit economics of these platforms 636441. If cross-border parcels are subjected to standard tariffs and customs processing fees, the 50% to 70% price advantage evaporates 5664. Trade volatility, including temporary tariff spikes to 54%, severely disrupted Temu's fully managed model operations in mid-2025 64. In response, platforms are rapidly accelerating their transition to semi-managed models and local warehousing to insulate themselves from parcel-by-parcel taxation, though this inherently sacrifices a portion of their low-cost margin advantage 323856.

Product Quality Perception and Consumer Trust

The sustainability of the disruptors' growth is highly debated due to ongoing issues with consumer trust and product quality. A 2025 Appinio shopper report revealed that while Temu and Shein maintain high brand awareness, both are seeing stagnation in actual purchasing conversion among aware consumers 35.

Consumer trust remains overwhelmingly weighted toward incumbents. Globally, only 6.4% of surveyed consumers state they trust Temu over Amazon 42. Despite this low trust, 48% shopped at Temu in the past year, indicating that extreme value temporarily supersedes trust during periods of economic strain 42. However, poor quality leads to high return rates. In 2021, the average return rate for online clothing purchases - where fast fashion platforms operate heavily - was 30%, significantly higher than traditional retail averages 33. Furthermore, Amazon maintains a massive advantage in shipping speed and reliable return policies; 66% of surveyed consumers found Amazon's shipping much faster, and 50% preferred its return policies over Temu's 62.

| Platform Metric | Amazon (Incumbent) | Temu / Shein (Disruptors) |

|---|---|---|

| Primary Consumer Driver | Delivery Speed, Reliability 4062 | Extreme Low Price, Gamification 6142 |

| Trust Preference | Overwhelmingly dominant 3542 | Low, but offset by value 42 |

| Return Policy Perception | 50% of consumers prefer 62 | Trailing incumbent, higher absolute return rates 3362 |

| Market Share (Cross-Border) | 25% global share 63 | ~24% global share (Temu) 63 |

Environmental Impact and Labor Controversies

Furthermore, platforms utilizing ultra-fast fashion and C2M models face intense scrutiny regarding environmental sustainability, intellectual property practices, and supply chain labor conditions 33614167. The sheer volume of low-cost, low-quality items generates immense textile waste, often destined for landfills 6167. Reports of poor labor conditions and worker exploitation in supplier factories routinely plague these brands 33614167.

As these companies attempt to move upmarket - a critical requirement of Christensen's disruption model - they will need to overcome the stigma of being "cheap" and "disposable." While recent data indicates gradual improvements in consumer trust regarding product quality for Temu (a 50% increase in trust perception year-over-year in Australia) and Shein, establishing the brand equity required to capture the high-margin, high-expectation consumer segments currently dominated by legacy incumbents will require fundamentally altering their production standards and business ethics 40.

Conclusion

The disruption of retail theory by modern e-commerce platforms highlights a critical evolution in global commerce. Traditional models like the Wheel of Retailing accurately describe the vulnerability of aging formats, but Clayton Christensen's theory of Disruptive Innovation remains the most robust lens for understanding the current market. Amazon, once the ultimate disruptor, has followed the theoretical path precisely, transitioning into an incumbent focused on sustaining innovations, premium memberships, and high-margin retail media networks.

This upmarket migration created a vast opening at the low end of the market, which C2M platforms like Temu, Shein, and TikTok Shop have aggressively exploited. By reversing the supply chain, leveraging fully managed logistics, and substituting traditional brand trust with algorithmic discovery and influencer social commerce, these platforms satisfy the "good enough" criteria for price-sensitive consumers. However, they challenge the traditional disruption model through their unprecedented capitalization and speed, executing an ecosystem-level disruption rather than a gradual, under-resourced ascent. As regulatory environments tighten around de minimis exemptions and consumer demands for quality and sustainability increase, the ultimate success of these platforms will depend on their ability to transition from subsidized, hyper-growth disruptors into stable, upmarket incumbents.