Disruptive innovation of last-mile delivery platforms in logistics

Introduction to the Last-Mile Paradigm Shift

The global logistics and freight industry is undergoing a structural metamorphosis unparalleled since the advent of containerization. At the epicenter of this transformation is the "last mile" - the final, most complex, and cost-intensive leg of the supply chain. While historically viewed merely as the concluding operational step of order fulfillment, the last mile has evolved into the primary battleground for retail dominance, routinely accounting for 41% to 53% of total shipping costs 113. For decades, this sector was dominated by asset-heavy incumbents operating rigid hub-and-spoke models with proprietary fleets. Today, it is being rapidly restructured by digital platform ecosystems that rely on gig-economy labor, algorithmic dispatching, and rapid vertical integration to offer hyper-localized, on-demand fulfillment.

As the digital economy navigates the 2025 - 2026 operational window, the post-pandemic stabilization of consumer demand has forced a profound strategic pivot across the sector. The era of venture-subsidized growth-at-all-costs has receded, replaced by an urgent, systemic focus on unit economics, algorithmic efficiency, and sustainable scaling models. Consumer preferences have correspondingly matured. Longitudinal data, including comprehensive 2024 consumer survey results from McKinsey, indicates a significant behavioral shift: while absolute delivery speed was paramount during the height of the pandemic, by 2024, cost and reliability decisively superseded speed . Delivery speed dropped to the fifth most important factor for consumers, with 90% expressing a willingness to wait two to three days for deliveries if it mitigates shipping fees . Furthermore, cost sensitivity has reached unprecedented levels, with 90% of consumers likely to abandon a shopping cart upon encountering high shipping costs for standard items, and approximately 50% flatly unwilling to pay any shipping premium regardless of speed . However, this extreme cost sensitivity is juxtaposed with a rising demand for environmental accountability; more than 35% of consumers - and over 55% of younger urban demographics - are now willing to pay a premium for certified sustainable shipping options .

This exhaustive research report investigates how last-mile delivery platforms are restructuring the traditional freight and parcel industries. By rigorously applying the academic lens of disruptive innovation theory, this analysis evaluates the ongoing debate regarding whether digital platforms represent true market disruption or merely sustaining technological advancements. The scope extends globally, contrasting the highly evolved architectures of Asian super-apps and Latin American integration models with the distinct economic frictions facing Western platforms. Finally, the report investigates the confluence of emergent technologies - specifically generative artificial intelligence and autonomous delivery vehicles - alongside the intensifying macroeconomic constraints of environmental, social, and governance (ESG) policies and shifting global labor classifications.

The Theoretical Framework: Disruptive vs. Sustaining Innovation in Logistics

To accurately assess the structural impact of digital last-mile platforms on traditional logistics, the analysis must be grounded in rigorous academic frameworks. The prevailing discourse is heavily informed by Clayton Christensen's Theory of Disruptive Innovation, which provides a predictive mechanism for evaluating competitive responses, technology substitution, and market evolution 2.

Defining the Disruption Criteria

Christensen's theory establishes a strict, foundational dichotomy between sustaining innovations and disruptive innovations. Sustaining innovations focus on incremental or breakthrough improvements to existing products and services, meticulously tailored for an incumbent's most demanding, mainstream, and profitable customers 634. In the traditional logistics sector, a sustaining innovation might involve an asset-heavy carrier like FedEx or UPS investing in advanced warehouse management systems, deploying electric delivery vans, or upgrading conveyor belts 3. These technologies demonstrably enhance the efficiency of their existing business models, allowing them to offer faster or slightly more cost-effective services to established enterprise clients. However, they do not fundamentally alter the nature of the service, the core business model, or the target demographic 34.

Disruptive innovation, conversely, originates outside the purview of mainstream incumbent operations, either taking root at the low end of an existing market or within entirely new markets composed of non-consumers 695. According to Christensen's criteria, disruptive products typically enter the market offering inferior performance on traditional metrics - they may be less reliable initially, lack specialized freight handling capabilities, or offer limited geographic coverage - but they introduce entirely new attributes such as extreme affordability, simplicity, or unprecedented localized convenience 345. Over time, these disruptive models leverage rapid iteration cycles to improve their performance on mainstream metrics. Because their initial customer base was largely ignored by incumbents who were focused on higher-margin enterprise clients, disruptors gain a foothold and eventually move upmarket to displace those established leaders 295.

The Academic Debate: Platform Disruption or Systemic Sustenance?

Within the Journal of Business Logistics and broader academic supply chain literature, a nuanced and highly contested debate has emerged regarding the true nature of digital freight and last-mile platforms. Do entities like Uber Eats, DoorDash, and digital freight forwarders represent a genuine disruptive threat to traditional logistics service providers, or are they merely sustaining innovations acting as digital intermediaries?

Research indicates that the assessment depends heavily on the ecosystem network, the initial target market, and the nature of the value contribution 1112. Early iterations of food delivery platforms exhibited classic characteristics of new-market disruption 49. They targeted local restaurants that previously possessed no delivery infrastructure and consumers who previously relied exclusively on dine-in or self-pickup 9. By introducing a "good enough" logistics solution utilizing non-professional crowdsourced drivers, these platforms created a parallel, decentralized logistics network. Traditional parcel carriers largely ignored this emergence because the unit economics of moving a single hot meal point-to-point did not align with their rigid, highly optimized, batched-route hub-and-spoke models 26.

However, as these platforms expand their ambitions from hot food delivery into groceries, general retail e-commerce fulfillment, and eventually traditional parcel delivery, they encroach directly upon the heavily defended territory of logistics incumbents. Theoretical frameworks developed in recent academic literature - such as the Digital Start-up Disruption (DSD) framework - attempt to characterize these digital platforms based on four antecedents: initial target market, ecosystem framing, value creation, and regulatory agenda 12. Applying this framework reveals that while the technological platforms (the algorithmic matching engines) are highly innovative, the underlying physical movement of goods often acts as a sustaining improvement to the broader retail distribution ecosystem rather than a pure disruption of freight 311. When global e-commerce giants build proprietary delivery networks relying on a mix of independent contractors and digital routing, they are deploying a sustaining innovation to support retail dominance. Yet, this exact same network acts as a highly disruptive force against legacy carriers like UPS and FedEx by systematically siphoning away critical baseline parcel volume 3.

The pace and success of this technological substitution are heavily determined by ecosystem interdependencies 3. Platforms that successfully construct complementary networks - integrating point-of-sale systems for merchants, consumer loyalty programs, digital wallets, and high-density courier fleets - dramatically accelerate their upward mobility in the market. This integration allows them to transition from low-end niche disruptors to dominant, unavoidable urban infrastructure providers 378.

Global Archetypes: Restructuring the Logistics Ecosystem

The architectural strategies of last-mile platforms vary significantly across global regions, dictated by variations in population density, labor economics, and consumer digital maturity. By examining the distinct archetypes present in Asia, Latin America, and Western markets, a comprehensive view of how ecosystems are being fundamentally restructured emerges.

The Asian Super-App Ecosystem: Organic vs. Subsidized Expansion

The Asian market presents the most advanced realization of the integrated digital lifestyle ecosystem. Platforms in this region have moved far beyond localized last-mile delivery to act as the foundational digital infrastructure for urban living. A comparative analysis between China's Meituan and Southeast Asia's Grab highlights the divergent strategies required to achieve "SuperApp" status.

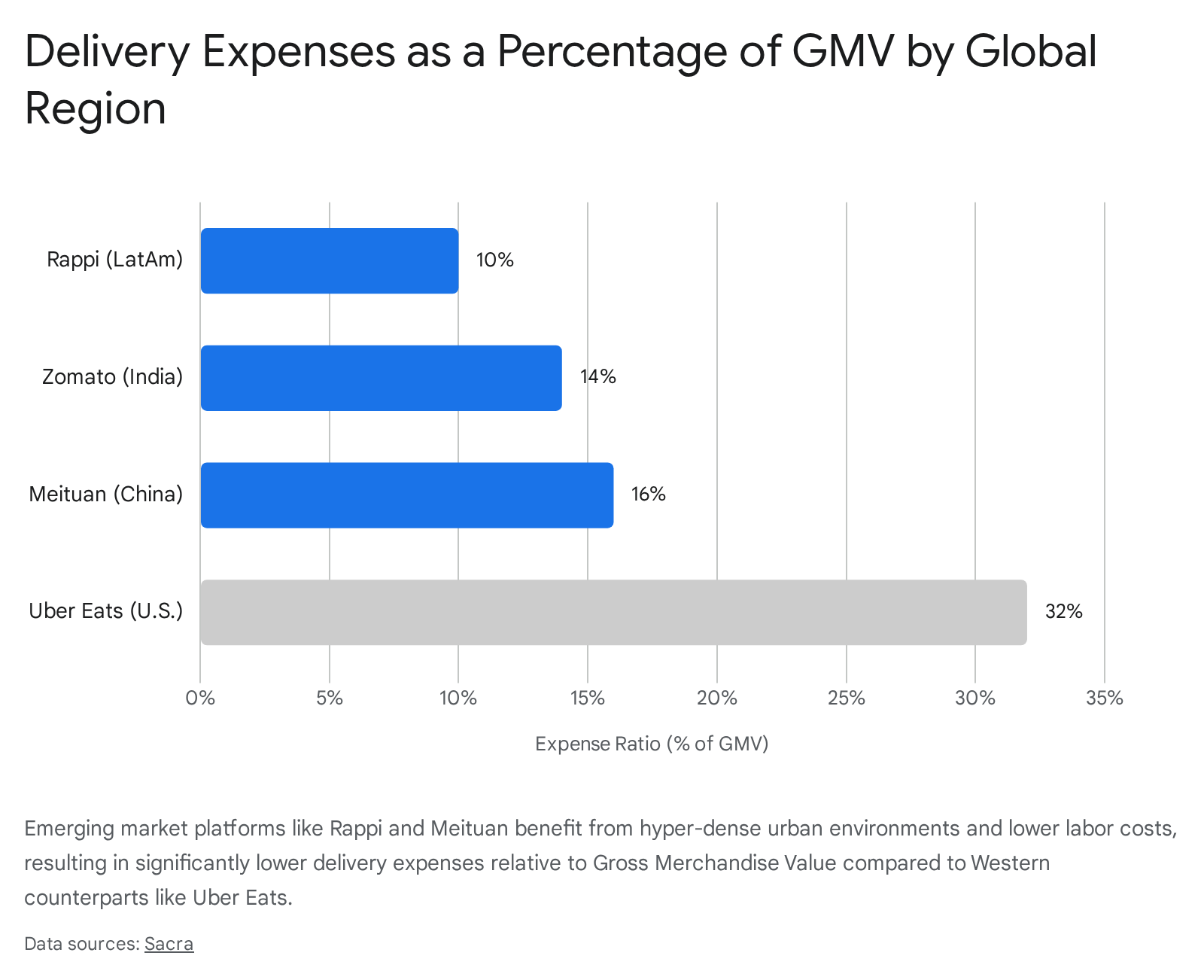

Meituan's success rigorously validates Christensen's theories of moving upmarket to capture profitability. Operating with an estimated 16% delivery expense as a percentage of Gross Merchandise Value (GMV), Meituan manages over 10 million daily orders 6. Food delivery, while accounting for the vast majority of Meituan's total revenue (approximately 57%), operates on exceptionally thin margins, contributing only 34% of its gross profit 6. Recognizing the limitations of this model, Meituan's founder, Wang Xing, explicitly engineered the platform to utilize the high-frequency traffic generated by low-margin food delivery as a highly efficient customer acquisition channel 69. This organic traffic is then cross-sold into lower-frequency but exponentially higher-margin services, such as hotel bookings and travel 69. In the travel segment alone, Meituan generates only 19% of its total revenue but commands a disproportionate 51% of its gross profit, effectively subsidizing the massive logistics network required for food delivery 6.

In stark contrast, Grab, which operates across Southeast Asia, began its ecosystem journey rooted in ride-hailing rather than food delivery. While Grab exhibits many characteristics of a SuperApp, market analysts note a critical strategic distinction: when Grab launches additional logistical services (such as food or parcel delivery), it lacks the organic cross-selling synergy enjoyed by Meituan 9. Consequently, Grab must heavily promote and subsidize new verticals to drive adoption; during its initial foray into deliveries, over 100% of the revenue taken in was reportedly rebated back into the market in the form of incentives to artificially stimulate demand 9. This underscores a vital principle in platform economics: housing multiple services within a single application does not guarantee reduced customer acquisition costs unless the core service naturally satisfies intersecting, high-frequency consumer habits.

Technologically, Meituan operates as an apex orchestrator. Its proprietary dispatch system forms the world's largest minute-level delivery network 18. A detailed study of Meituan's operations reveals a hybrid algorithmic framework that integrates reinforcement learning with hyper-heuristic optimization to manage sequential order assignment 10. Traditional dispatching methods typically focus on short-term cost minimization (finding the immediate shortest path), which fails to account for the long-term implications of assignment decisions on system-wide performance 10. Meituan's approach explicitly models the evolving system state - factoring in demand uncertainty, courier autonomy, and service times - enabling dispatching policies that balance immediate efficiency with future operational readiness 10. Through strategic order postponement and intelligent batching, this system has demonstrated a 12% reduction in overall operational costs 10.

The Latin American Integration Model: Rappi

Founded in 2015, the Colombian platform Rappi represents the vanguard of the multi-vertical model in the Western Hemisphere, operating across nine countries and over 100 cities in Latin America 62021. Rappi's operational architecture masterfully synchronizes an independent courier fleet exceeding 200,000 workers (Rappitenderos), a dense retail network, and a highly sophisticated fintech stack 62223.

Rappi's strategic disruption lies in its aggressive, immediate horizontal expansion. Rather than remaining a pure-play food delivery service for years, it rapidly integrated groceries (RappiMarket), pharmacies, e-commerce, travel (RappiTravel), and financial services (RappiPay) 623. This multi-vertical approach creates a powerful retention flywheel: users acquired through high-frequency, low-margin food deliveries are subsequently converted into higher-margin fintech and retail users 23.

Crucially, Rappi operates with a distinct structural and geographic advantage in unit economics. Benefiting from hyper-dense urban environments - Latin America boasts some of the highest route densities globally - and lower relative labor costs compared to Western markets, Rappi maintains one of the most efficient delivery profiles in the world. Rappi's delivery expenses represent only an estimated 10% of its GMV 6. This is substantially lower than even Meituan (16%) and vastly outperforms Western operators 6.

To further cement its logistical dominance and lock in margins, Rappi launched RappiTurbo. This initiative utilizes a vast network of over 400 proprietary micro-fulfillment centers (dark stores) to fulfill ultra-fast orders - often under 10 minutes 23. This micro-logistics infrastructure effectively bypasses traditional upstream warehousing, acting as a disruptive, disintermediating force against both legacy grocers and conventional parcel carriers 23. The underlying technology stack enabling this scale utilizes a microservices architecture to manage surge hours, real-time communication protocols via WebSockets, and custom-built multi-vendor management systems 22.

Western Platforms: The Friction of Unit Economics and Partitioned Pricing

Western platforms, including Uber Eats and DoorDash, face a structurally hostile environment characterized by massive suburban sprawl, high labor costs, and intense regulatory scrutiny 32425. While DoorDash commands roughly 67% of the U.S. meal delivery market, its path to sustainable profitability is heavily reliant on psychological pricing mechanisms rather than pure operational efficiency 11.

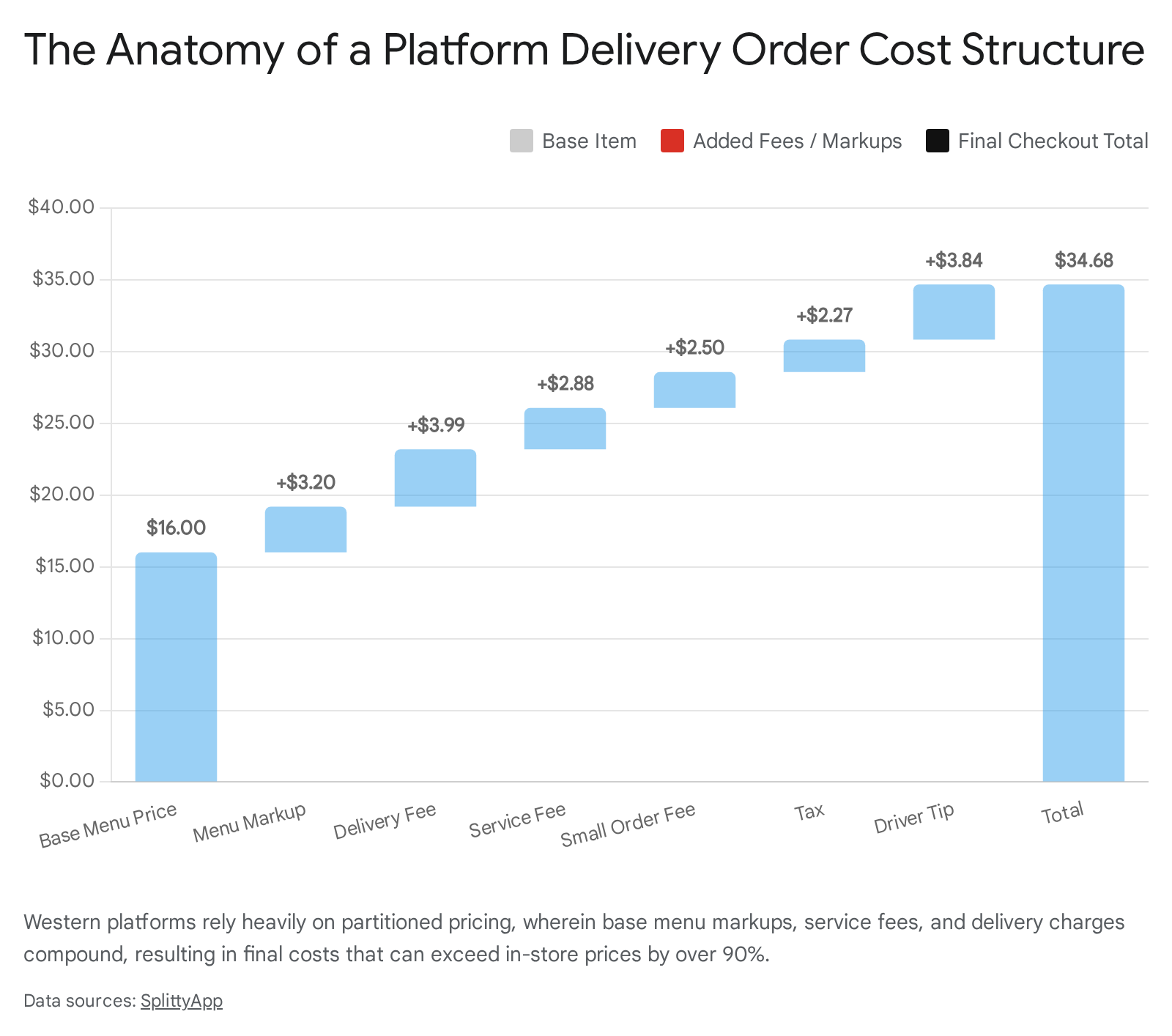

Delivery expenses for Western platforms are exorbitant; Uber Eats operates with delivery expenses estimated at 32% of GMV 6. To overcome these fundamental unit economic challenges, platforms like DoorDash monetize through a highly complex stack of fees, employing a strategy defined by behavioral economists as "partitioned pricing" 2712. This involves breaking a single price into a base price plus multiple mandatory surcharges 12. A consumer using DoorDash faces a cascade of costs: embedded menu markups (often 15-30% higher than in-store prices as restaurants pass on platform commission costs), variable delivery fees based on distance and demand, a percentage-based service fee (approximately 15% of the subtotal), potential small order fees, and finally, the driver tip 271229.

The cumulative effect of this partitioned pricing is staggering. Independent tracking data indicates that a typical order can bear a 40% to 91% markup over standard retail prices 12. For instance, a basic $16 restaurant item can escalate to over $30 at checkout before a tip is even applied 12.

Research published in the Journal of Marketing Research demonstrates that partitioned pricing causes consumers to anchor on the initial base price and systematically underestimate the total cost, thereby artificially increasing demand despite high premiums 12. However, this intense price inflation limits the platform's ability to act as a true, ubiquitous low-end disruptor for all economic demographics. To combat platform churn and stabilize highly variable transaction revenue, Western operators are aggressively pivoting toward recurring subscription models (e.g., DashPass, Uber One) and heavily investing in retail media networks (merchant advertising) to secure high-margin, predictable revenue streams 112712.

Comparative Analysis: Asset-Heavy Carriers vs. Asset-Light Platforms

The divergence between traditional logistics providers and digital platforms is fundamentally rooted in asset ownership, capital allocation, and risk distribution. Traditional models are anchored by massive physical infrastructure deliberately designed for predictable, high-volume, consolidated freight. Platforms, conversely, leverage software, data interoperability, and crowdsourced human capital to manage highly volatile, low-volume, dispersed routing.

| Dimension | Asset-Heavy Traditional Carriers (e.g., UPS, FedEx, DHL) | Asset-Light Logistics Platforms (e.g., DoorDash, UberEats, Meituan) |

|---|---|---|

| Asset Ownership | Extensive proprietary physical infrastructure. Ownership or long-term leasing of aircraft fleets, long-haul trucking assets, highly mechanized sorting hubs, and vast real estate portfolios 303132. | Minimal physical asset ownership. Capitalizes on existing community assets (restaurants, retail storefronts) and relies heavily on couriers providing their own vehicles (bicycles, scooters, personal cars) 303133. |

| Labor Model | Professionalized, highly trained, and often unionized workforces. High fixed labor costs encompassing hourly wages (e.g., UPS drivers averaging ~$20.59/hour in the US), comprehensive healthcare benefits, pensions, and rigorous safety compliance 34. | Gig-economy framework utilizing independent contractors. Highly variable labor costs driven by algorithmic piece-rate pay, dynamic surge pricing, and a heavy reliance on consumer tips. Base pay averages $14-$17/hour without standard employee safety nets 3435. |

| Cost Per Delivery | High fixed costs amortized over massive, consolidated route density. Extremely efficient for delivering 10-20 packages per hour in dense zones, but highly inefficient and costly for ad-hoc, single-item, immediate dispatch 2532. | Inherently high unit cost for point-to-point single deliveries, necessitating substantial consumer fees and merchant commissions (often 15-30%) to achieve platform profitability 1229. Highly vulnerable to driver churn and acquisition costs. |

| Technology Stack | Legacy Enterprise Resource Planning (ERP) and Transportation Management Systems (TMS). Technological focus is on massive hub sorting automation, ubiquitous barcode scanning, and static macro-route planning 3637. | Cloud-native microservices architectures. Heavy reliance on real-time telematics, Generative AI for dynamic dispatch and demand forecasting, consumer-facing super-apps, and complex machine-learning algorithms balancing multi-sided markets 2238. |

| Scalability & Risk | Slow, rigid, and highly capital-intensive to scale into new geographies. High financial exposure to asset depreciation, infrastructure maintenance, and stranded fixed overhead during macroeconomic downturns 3132. | Rapid, highly elastic scalability. Geographic expansion requires minimal capital expenditure (primarily digital marketing and localized driver incentives). High exposure to regulatory reclassification risks and intense platform-on-platform competition 303133. |

The broader financial implications of these structural differences are profound. Extensive research across Fortune 500 companies indicates that asset-light companies consistently achieve significantly higher total shareholder returns and market valuations compared to their asset-heavy peers 13. This premium is directly attributed to the asset-light model's ability to transition fixed costs to a variable structure, allowing for extreme operational agility during demand fluctuations 13. As global e-commerce continues its relentless expansion - projected to exceed $6.3 trillion globally and account for over 32% of all retail purchases by 2029 - the capacity to seamlessly scale operations without corresponding massive capital outlays provides digital platforms with a formidable, compounding strategic advantage 1.

The Technological Vanguard: Generative AI and Autonomous Orchestration (2024 - 2026)

To counteract the inherently poor unit economics of point-to-point human delivery, logistics platforms are heavily investing in frontier technologies. The crucial period from 2024 to 2026 has witnessed the definitive transition of Generative AI and autonomous delivery vehicles from theoretical pilot programs to broad commercial deployment 13714.

Generative AI in Routing and Supply Chain Orchestration

Generative AI (GenAI) has rapidly evolved beyond conversational natural language processing to become a core orchestrator of physical supply chains. Unlike traditional combinatorial optimization solvers that rely on static heuristics, GenAI models synthesize vast troves of unstructured data - live traffic feeds, historical weather patterns, social media sentiment, and real-time courier telemetry - to generate dynamic, predictive operational scenarios 364115.

In the highly pressurized last-mile sector, GenAI acts as a critical mitigation tool for complex routing constraints. The implementation of GenAI for estimated times of arrival (ETAs) perfectly illustrates this. In markets like China, intense public outcry and growing regulatory concern over dangerous driving conditions caused by overly aggressive dispatch algorithms forced platforms to adapt. In response, Meituan deployed GenAI-augmented ETA systems that do not merely calculate the absolute shortest path, but dynamically inject game-theoretic safety buffers, explicitly adding minutes of "flexible time" for riders based on real-world constraints, weather variations, and algorithmic negotiation 15. This sophisticated use of AI prioritizes long-term ecosystem stability over short-term speed.

Furthermore, within broader logistics, GenAI facilitates Retrieval-Augmented Generation (RAG) models for optimizing payload capacities. Considering that U.S. freight trucks operate roughly 30% empty on average - representing massive wasted time, fuel, and unnecessary carbon emissions - optimizing capacity is paramount 43. RAG models translate complex multi-objective optimization algorithms into plain-language, prescriptive directives for human coordinators and dispatchers 4143. By continuously running endless "what-if" simulations, these AI systems analyze traffic, vehicle-specific fuel profiles, and driver behavior to generate green-compliant paths, effectively reducing empty miles and cutting carbon emissions by up to 15%, while boosting demand forecasting accuracy by up to 30% 374143.

Autonomous Delivery Networks: Drones and Ground Robots

While GenAI optimizes the software and decision layer, autonomous delivery targets the physical hardware layer, aiming to drastically reduce the industry's heaviest burden: human labor costs.

Amazon Prime Air represents the industry's most aggressive, capitalized push toward aerial autonomy. Following over a decade of iterative testing, public skepticism, and regulatory hurdles, Amazon expanded commercial deployments of its advanced MK30 drone significantly in late 2024 and 2025 141617. The MK30 drone - which is lighter, quieter, and boasts double the range of its predecessor - is capable of flying in light rain and operating beyond visual line of sight (BVLOS) with a 7.5-mile range 141646. To reach this point, Amazon completed over 5,100 test flights totaling more than 900 hours, utilizing AI to address functional hazards such as sensor interference from environmental dust 1416. Despite strategically shutting down early test sites in California and temporarily pausing operations in Italy and the UK to concentrate on scaling U.S. expansion in states like Arizona and Texas, Amazon maintains a publicly stated, highly ambitious mandate to deliver 500 million packages annually via drone by the end of the decade 141718.

The macroeconomic implications of autonomy at scale are staggering. Financial projections suggest that widespread autonomous drone delivery could disrupt the baseline economics of e-commerce, reducing the cost of last-mile logistics from an average of $3.50-$5.00 via traditional truck or courier to as little as $0.88 per package for items under five pounds, simultaneously slashing delivery times to a reliable 30 minutes 4619. Concurrently, ground-based autonomous robots - such as those deployed by specialized firms like Starship Technologies and Nuro - are steadily capturing market share in structured, controlled environments 1. Operating across select university campuses, suburban enclaves, and low-traffic neighborhoods, these ground units are successfully navigating complex pedestrian infrastructure to fulfill hyperlocal grocery and food orders without the regulatory airspace complexities of drones 1. Meituan is also pioneering physical autonomy, operating over 30 drone routes through China's low-altitude network, completing over 300,000 delivery orders backed by an extensive portfolio of 400 patents related to drone logistics .

The Geopolitical and Regulatory Constraints of 2025-2026

The exponential growth and societal saturation of asset-light platforms have triggered intense legislative and regulatory blowback. Governments worldwide, recognizing that decades-old labor and transport laws are ill-equipped for the digital economy, are moving aggressively to regulate the negative externalities of the platform ecosystem, focusing intensely on labor rights and environmental impact 4920.

The Shifting Sands of Labor Classification

The foundational financial premise of the platform business model - utilizing a massive, on-demand fleet of independent contractors devoid of traditional employee benefits - is facing an existential, multi-jurisdictional legal threat.

In the European Union, the formal adoption of the Platform Work Directive (Directive (EU) 2024/2831) has established a radical, highly consequential new precedent for global labor law 21. The Directive introduces a rebuttable legal presumption of employment. If a digital labor platform exhibits clear indicators of control or direction - such as algorithmically governing how, when, or where work is performed, or dictating task allocation and pricing - the worker is legally presumed to be an employee 21. Crucially, this shifts the burden of proof entirely onto the corporate platform to prove otherwise, rather than requiring the worker to sue for status 21. Furthermore, the Directive enforces unprecedented algorithmic transparency; platforms are legally required to disclose exactly how automated monitoring and decision-making systems are used for task allocation and performance evaluation, while strictly mandating meaningful human oversight to prevent algorithmic discrimination 21.

In the United States, the regulatory landscape regarding worker classification remains highly volatile, fragmented, and subject to intense partisan reversals. Under the Biden administration, the Department of Labor (DOL) finalized a strict rule in 2024 that utilized a comprehensive six-factor "economic realities" test 225323. This rule was deliberately designed to make it significantly more difficult for platforms to classify workers as independent contractors, prioritizing factors such as the degree of corporate control and whether the work being performed was integral to the employer's core business 5323. However, following a change in the executive administration, the DOL announced in May 2025 that it would rescind and entirely cease enforcement of the 2024 rule 222324. The federal standard reverted to a looser interpretation that heavily favors the independent contractor classification relied upon by gig platforms like Uber and DoorDash 222324. Despite this significant federal reprieve, platforms cannot operate uniformly; they still face a complex, fragmented map of state-level regulations. States such as Washington, Massachusetts, and California continue to strictly enforce variants of the highly restrictive "ABC test," which assumes employee status by default unless the platform can prove the worker is free from control and operates an independent business 352224.

Urban ESG Policies and the Rewriting of Kerbside Economics

Beyond labor, Environmental, Social, and Governance (ESG) mandates are physically restricting where, when, and how last-mile delivery can occur 252627. Major global metropolises, grappling with unprecedented congestion and air quality crises, are implementing aggressive urban sustainability regulations that heavily penalize traditional, asset-heavy logistics operations reliant on internal combustion engine (ICE) vehicles 4920.

In London, the relentless expansion of the Ultra Low Emission Zone (ULEZ) across all boroughs in late 2023 applies severe daily financial charges to non-compliant commercial vehicles 35960. This economic penalty is compounded by safety mandates; the Direct Vision Standard (DVS) mandates that from October 2024, Heavy Goods Vehicles (HGVs) over 12 tonnes must meet a minimum 3-star direct visibility rating to operate anywhere within Greater London 360. These overlapping regulations force traditional freight carriers into massive, unplanned fleet renewal expenditures simply to maintain basic route access.

Similarly, Paris has enacted the Zone à Faible Émission (ZFE), a comprehensive policy that systematically phases out older, polluting vehicles via the Crit'Air categorization system, with strict total bans expanding continuously through 2028 2061. Across the Atlantic, New York City implemented its highly anticipated Manhattan Central Business District congestion pricing toll in January 2025, while simultaneously piloting "Smart Curbs" programs and deploying microhubs specifically designed to consolidate freight and reduce commercial vehicle idling 362.

In response to these draconian (yet necessary) urban policies, platforms are brilliantly leveraging their asset-light flexibility. Because they do not own the physical delivery fleets, they face no stranded asset risk. Instead, they quickly alter their algorithms to incentivize their gig workers to transition to electric bicycles, cargo trikes, and other micro-mobility solutions 60626364. By utilizing these alternative modalities, platforms effectively bypass the congestion tolls and zero-emission zone penalties that financially cripple legacy truck operators, turning restrictive ESG legislation into a competitive moat against traditional carriers.

Incumbent Counter-Strategies: The Legacy Carriers Strike Back

Faced with the existential dual threats of platform disruption from below and stringent ESG regulations from above, traditional logistics providers (such as UPS, FedEx, DHL, and national postal authorities) are not remaining passive. Recognizing that their massive, inflexible infrastructure cannot compete purely on agility in the ad-hoc, point-to-point on-demand space, incumbents are pivoting to hybrid operating models and leveraging their massive scale to force efficiency.

First, incumbents are investing heavily in automated parcel locker networks and establishing vast localized pick-up/drop-off (PUDO) networks within existing retail locations 1163. By consolidating dozens of individual residential last-mile deliveries into a single, secure, centralized location, carriers dramatically reduce the overarching cost-per-delivery 11. Crucially, this model entirely eliminates the massive inefficiency and financial drain of failed delivery attempts (which traditionally cost carriers between $6 and $12 per incident to rectify) and perfectly aligns with consumer desires for secure, flexible package retrieval 1.

Second, legacy carriers are actively deploying their own advanced AI and computer vision solutions to modernize their aging physical processes. For example, in mid-2024, FedEx launched VisionInAssisted Package Retrieval technology 65. This system utilizes advanced computer vision and machine learning to help drivers instantly locate specific packages within dark, crowded step-vans, shaving vital seconds off the search time at every single stop - a marginal gain that translates into massive network-wide cost savings 65.

Finally, and perhaps most tellingly, traditional asset-heavy logistics firms are increasingly embracing the core tenets of the asset-light playbook that initially disrupted them. Many are strategically divesting their heavy commercial real estate portfolios through sale-leaseback agreements 32. Furthermore, they are aggressively outsourcing localized warehouse operations to agile third-party logistics (3PL) providers 3233. This strategic unbundling allows legacy carriers to transition rigid fixed costs into flexible variable expenses, ensuring they remain financially resilient and competitive in an era defined by volatile e-commerce demand and rapid technological substitution 3233.

Conclusion

The academic theory of disruptive innovation provides an extraordinarily precise lens through which to view the ongoing, permanent restructuring of the global logistics industry. While digital platforms initially emerged as classic low-end disruptors - providing "good enough" delivery services to previously underserved local merchants using non-professional labor - they have rapidly and aggressively ascended the value chain to threaten the core business of established freight and parcel carriers.

Today, international super-apps like Meituan and Rappi demonstrate the absolute apex of platform evolution, masterfully using high-frequency, low-margin logistics as a loss-leading acquisition mechanism to capture immense, defensible value in fintech, advertising, and high-margin retail. Conversely, Western platforms, hindered by substantially higher labor costs, suburban sprawl, and fragmented pricing power, are fighting a grueling war for profitability through complex partitioned pricing models, recurring subscriptions, and GenAI-driven algorithmic efficiency gains.

As the logistics industry advances through 2026 and beyond, the stark dichotomy between asset-heavy traditional carriers and asset-light digital platforms is beginning to blur into a complex synthesis. Incumbents are systematically shedding heavy assets, building locker networks, and deploying AI to mimic platform agility. Simultaneously, platforms are quietly acquiring physical microhubs and investing billions in heavy autonomous hardware like BVLOS drones to ultimately escape the volatile, increasingly regulated costs of gig labor. Ultimately, the future of the last-mile ecosystem will not be dictated by a single, pure operating model, but by the hybrid entities capable of orchestrating the most resilient, digitally integrated, and legally compliant supply chain architectures on a global scale.