Platform disruption theory and pipeline business models

Introduction to Platform Economics

The transition from the industrial economy to the digital economy has been fundamentally defined by the displacement of traditional linear business models by multi-sided platforms. Platform disruption theory, extensively developed over the past two decades by scholars such as Geoffrey Parker, Marshall Van Alstyne, and Sangeet Paul Choudary, postulates that platform-based enterprises possess inherent structural advantages that allow them to outcompete traditional firms 1. A platform is defined as an open, participative infrastructure that facilitates value-creating interactions between external producers and consumers, governed by specific rules set by the platform orchestrator 23.

Platform disruption occurs when these multi-sided networks reconfigure value creation, value consumption, and quality control. Unlike traditional organizations that rely on internal resources to manufacture and distribute goods, platform enterprises act as intermediaries that externalize the costs of production and inventory 12. By separating the ownership of physical assets from the generation of value, platforms operate with superior marginal economics. As a platform scales, the marginal cost of serving an additional user or facilitating an additional transaction approaches zero, allowing for unprecedented rates of growth 13.

This macroeconomic shift has forced a fundamental reevaluation of competitive strategy. Strategy in the platform economy moves away from controlling unique internal resources and erecting traditional barriers to entry, pivoting instead toward the orchestration of external resources and the cultivation of vibrant participant communities 24. The traditional focus on maximizing the lifetime value of individual customers is replaced by a focus on maximizing the total value of an expanding ecosystem in a circular, feedback-driven process 4.

Architectural Comparison of Pipelines and Platforms

The distinction between pipeline and platform business models rests on fundamental differences in resource allocation, asset ownership, and scaling mechanisms.

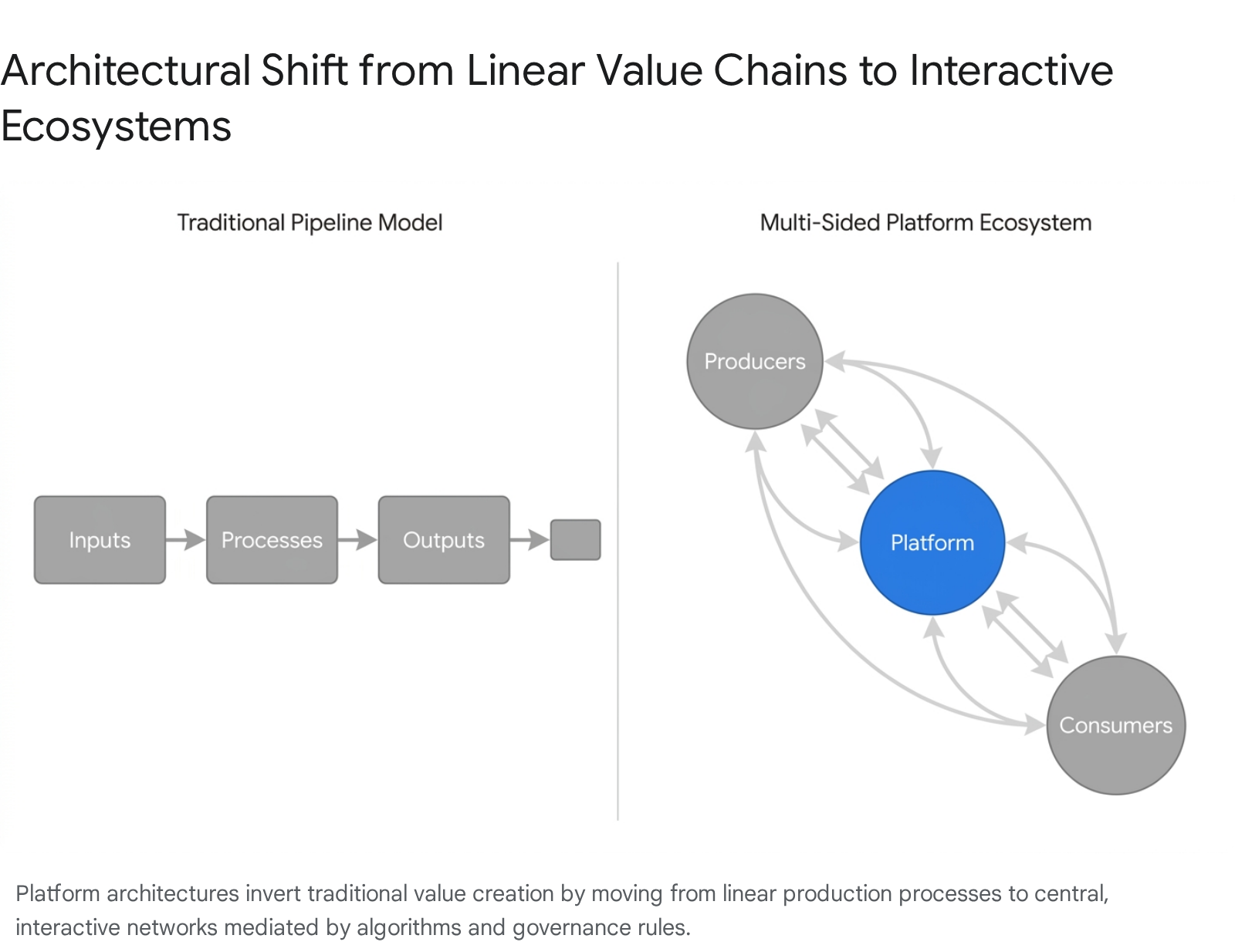

Pipeline businesses create value through a linear series of activities, often conceptualized as the classic value chain. Inputs are sourced at one end of the chain, transformed through proprietary manufacturing or service processes, and delivered as higher-value outputs to consumers at the other end 34. To achieve competitive advantage, pipeline models prioritize internal optimization, economies of scale in manufacturing, and the rigorous protection of intellectual property and physical assets 35.

In contrast, platforms generate value by providing the digital or physical infrastructure that enables independent participants to connect and transact. Because they do not own the core assets being exchanged, platforms are fundamentally asset-light. Their primary assets are the network of participants and the proprietary data generated by their interactions 45.

| Dimension | Traditional Pipeline Model | Multi-Sided Platform Model |

|---|---|---|

| Value Creation Mechanism | Linear transformation of inputs to outputs via internal processes 3. | Facilitation of value-creating interactions between external parties 6. |

| Asset Ownership | High physical/intangible asset ownership; capital intensive 56. | Asset-light; leverages resources owned by external producers 45. |

| Primary Competitive Advantage | Economies of scale, supply chain efficiency, brand equity, intellectual property 35. | Network effects, data-driven matching algorithms, ecosystem orchestration 35. |

| Scaling Constraints | Bound by physical production capacity and capital expenditure limitations 6. | Bound by network liquidity, matching efficiency, and server capacity 56. |

| Core Managerial Focus | Internal optimization, quality control of proprietary outputs, maximizing customer lifetime value 4. | External interaction optimization, ecosystem governance, curating participant quality 46. |

The Convergence of Business Models

The theoretical boundary between pipelines and platforms is increasingly porous, resulting in hybrid models. Academic analyses indicate that a two-directional convergence is occurring across major industries. Traditional pipeline businesses are adopting platform mechanics to expand their market reach without assuming proportional asset burdens, while mature platforms are incorporating pipeline elements - such as owned inventory or first-party services - to ensure quality control and capture higher margins 68.

For example, traditional brick-and-mortar retailers and hospitality chains have launched third-party marketplaces and booking ecosystems, transforming from pure pipelines into hybrid entities. These legacy organizations leverage external networks alongside their proprietary supply chains to emulate the rapid scaling advantages of digital-native platforms 68. This transition requires companies to shift from direct asset ownership toward facilitating transactions between independent providers and consumers, an operational pivot that requires fundamentally different information technology architectures and managerial incentives 6.

Mechanisms of Network Effects

The engine of platform disruption is the network effect - an economic phenomenon where the value or utility a user derives from a product depends directly on the number of other participants utilizing compatible products or services 78. Unlike supply-side economies of scale, which drive down unit costs through mass production and operational efficiency, network effects operate as demand-side economies of scale. They push the demand curve outward as the platform's utility expands autonomously with user growth 311. The adoption of a product by an additional user triggers two distinct effects: a total effect, which increases the value to all existing users, and a marginal effect, which enhances the motivation for non-users to join the ecosystem 8.

Direct and Indirect Network Effects

Direct, or same-side, network effects occur when the addition of users increases the value for other users within the exact same participant group. Social communication platforms, telecommunications networks, and multiplayer gaming environments are primary examples. In these ecosystems, each new participant exponentially increases the potential connection nodes for all existing participants, driving utility directly without requiring a secondary market side 71213.

Indirect, or cross-side, network effects characterize multi-sided platforms, where the utility for one user group is heavily or entirely dependent on the participation of a distinct, complementary group 81213. On ride-sharing platforms, for instance, an influx of drivers reduces wait times, thereby increasing utility for riders; simultaneously, an influx of riders increases earnings potential, driving utility for drivers. Similarly, the value of computer hardware or operating systems becomes increasingly valuable to consumers as the ecosystem of compatible third-party software developers grows 89. When cross-side network effects achieve sufficient liquidity on both sides, they generate an auto-catalytic flywheel effect. This self-reinforcing loop allows platforms to achieve exponential growth and erect significantly higher barriers to entry compared to linear businesses 1213.

Data, Local, and Compatibility Network Effects

Beyond the foundational direct and indirect dynamics, platform dominance is reinforced by secondary network effects. Data network effects constitute a formidable competitive advantage. As a platform scales, the aggregate interactions generate vast datasets. These data repositories are used to train machine learning algorithms, which subsequently improve search accuracy, matching efficiency, and personalized recommendations. Superior algorithms attract more users, who in turn generate more data, forming an independent cycle of continuous product improvement that is exceptionally difficult for new entrants to replicate 71310.

Local network effects dictate that the value derived by a user is determined not by the aggregate global size of the network, but by the density of the network within their specific geographic location or immediate social circle 139. Ride-sharing and food delivery platforms rely entirely on local network effects; a massive user base in New York provides zero utility to a driver or rider located in London 13. Consequently, these platforms must solve the "chicken-and-egg" cold start problem repeatedly in every new municipality they enter, heavily subsidizing initial participation to achieve localized critical mass 13.

Compatibility and standards network effects emerge when an underlying technology or protocol becomes the industry default, forcing both producers and consumers to conform to the ecosystem's specifications to maintain interoperability 813. This drives path dependence, locking users into established ecosystems even if technologically superior alternatives exist, thereby creating immense switching costs 1311.

Negative Network Effects and Ecosystem Congestion

Despite early theoretical assumptions predicting absolute "winner-take-all" markets driven by positive network effects, contemporary research demonstrates that dominant platforms frequently fail to retain market leadership indefinitely 11. Network size alone does not guarantee increasing returns on user demand. The value of a network is heavily constrained by matching quality and search costs 11. If a platform fails to efficiently match a consumer with the specific producer they desire, the sheer volume of available producers becomes a liability rather than an asset.

As platforms grow unchecked, they risk triggering negative network effects. An overwhelming number of users can lead to network congestion, severely degrading product quality, customer service, and matching accuracy 1210. Furthermore, an influx of low-quality producers can dilute the overall value proposition, necessitating rigorous community curation and algorithmic filtering to maintain the ecosystem's integrity 1212. If the costs of market friction and matching inaccuracy eclipse the benefits of network size, users will bypass the platform, leading to ecosystem collapse 11.

Competitive Strategy and Platform Envelopment

A defining feature of platform disruption is how new entrants unseat entrenched incumbents. In standard industrial organization theory, displacing a dominant incumbent requires a Schumpeterian innovation - a radically superior technology or operational paradigm. However, the unique structure of multi-sided markets introduces an alternative, highly effective pathway: platform envelopment 1314.

Platform envelopment occurs when an orchestrator in one platform market enters an adjacent platform market by leveraging its existing, overlapping user relationships 1314. By combining its core functionality with the target market's functionality in a multi-platform bundle, the enveloper dramatically reduces customer acquisition costs. This strategy elegantly bypasses the severe entry barriers associated with building network effects from scratch 1114.

Research outlines various typologies of envelopment attacks, categorized by the relationship between the two markets, which can be complements, weak substitutes, or functionally unrelated 1314. A contemporary example is the cross-category innovation observed in algorithmic platforms. Companies that initially established dominance in short-form video content have utilized their massive, highly engaged user bases and sophisticated algorithmic recommendation technologies to span into adjacent markets, such as e-commerce and local services 15. Envelopers capture market share by foreclosing an incumbent's access to users, effectively weaponizing the very network effects that previously protected the incumbent 14. The integration of microservices and open technical agreements accelerates this process, allowing platforms to test adjacent functionalities without disrupting their core architecture 15.

Supply-Side Vulnerabilities and Multi-Homing

A critical structural vulnerability for multi-sided markets, which severely dampens the efficacy of network effects, is the phenomenon of "multi-homing." Multi-homing is the practice whereby users or producers simultaneously utilize multiple competing platforms 16. For example, a gig economy driver may simultaneously accept ride requests from competing transportation networks, or an e-commerce merchant may list identical inventory on several distinct retail platforms.

Multi-homing fundamentally alters the nature of platform competition. When supply-side actors multi-home, platforms lose the ability to exclusively control their own scale and are unable to extract the full benefits of aggregating supply 16. This dynamic creates an economic paradox. While multi-homing grants external workers and merchants greater freedom and flexibility, it severely disincentivizes the platform from investing heavily in supply-side capacity, training, or capital improvements. Because any investment by the platform might ultimately benefit a competitor that shares the same supply base, platforms are incentivized to reduce wages or operational subsidies 16. The resulting equilibrium is often characterized by a thinned supply pool and deteriorating service quality for the end consumer, indicating that multi-homing can neutralize the competitive advantages typically generated by large-scale platforms 16.

Platform Traps and the Commoditization of Sellers

Recent scholarship has expanded the theoretical boundaries of platform economics by identifying scenarios where platforms actively degrade aggregate welfare. The conventional understanding of network theory assumes that an expanding platform generates positive externalities, making all participants better off 1718. However, economic research by Hagiu and Wright (2026) demonstrates that under specific structural conditions, rational agents can be induced to join a platform even when participation ultimately renders them worse off compared to a counterfactual world where the platform did not exist - a phenomenon termed the "Platform Trap" 1718.

Platform traps manifest primarily through mechanisms of commoditization, discoverability, and dynamic pricing. When an independent business - such as a localized restaurant or a direct-to-consumer retailer - joins a marketplace platform, it frequently brings its existing, loyal customer base into the platform ecosystem. Once these captive consumers are onboarded, the platform's discovery algorithms inevitably expose them to competing businesses within the network. Consequently, the original seller loses direct control over the customer relationship, suffering a form of commoditization where previously loyal buyers begin cross-shopping 19.

Platforms systematically exploit this dynamic through sequential pricing strategies. They frequently offer initial subsidies or zero-commission periods to early adopters, artificially stimulating participation until critical mass is achieved. Once the ecosystem is established and buyer behavior is firmly entrenched within the platform interface, the orchestrator begins a cycle of margin extraction 1718. This extraction takes the form of escalating transaction fees and, increasingly, the necessity for sellers to purchase advertising space simply to maintain visibility among their own former customers 18.

Sellers participate in this ecosystem out of fear that remaining off-platform will lead to immediate market foreclosure. This is driven by off-platform negative externalities: if a seller refuses to join, their competitors on the platform will systematically capture their customer base due to the sheer convenience of the platform's interface 18. Consequently, sellers are locked into an inescapable equilibrium where they face higher operational fees, diminished profit margins, and increased competition, generating a net loss in aggregate seller welfare 1719. This theoretical framework provides a critical counter-narrative to the prevailing assumption that platforms inherently drive market efficiency, revealing the coercive underlying mechanics of digital intermediation.

Structural Drivers of Platform Failure

While platform disruption theory emphasizes the unprecedented growth potential of multi-sided markets, empirical data reveals that platforms fail at an alarming rate 20. The transition from an innovative concept to a sustainable ecosystem requires precise execution across pricing, technical architecture, and market timing.

Strategic and Market Validation Failures

Longitudinal analyses of failed digital platforms identify several primary vectors of collapse. The most prominent causes include severe mispricing on one side of the market - failing to correctly balance subsidies between producers and consumers to overcome the chicken-and-egg problem - and the failure to establish robust trust mechanisms 20. Furthermore, platforms frequently collapse because they prematurely dismiss nascent competition or enter the market too late to achieve critical mass against an entrenched incumbent possessing insurmountable data network effects 20.

Recent data regarding software-as-a-service (SaaS) and digital platform startups in 2025 and 2026 highlights the severity of market timing. Industry analysis indicates that a vast proportion of failures stem from building products in categories suffering from hyper-saturation. Up to 31.5% of new platform ideas are launched into a "too late" zone where market saturation exceeds 70% 26. The leading cause of failure for these ventures - accounting for 42% of platform shutdowns - remains the lack of a verified market need, demonstrating that founders frequently execute advanced technical builds without adequately validating consumer demand 26.

Failure also occurs when ecosystem participants hold fundamentally incompatible views regarding the platform's core asset. In the case of TradeLens, a highly publicized, joint-venture blockchain logistics platform, the initiative collapsed because supply chain actors possessed conflicting conceptions of data. While the platform orchestrators viewed data as a shared resource necessary to facilitate ecosystem efficiency, the participating shipping entities viewed their data as a proprietary competitive asset 21. This narrow, competitive mindset fostered severe distrust and an unwillingness to share sensitive logistical information, ultimately causing the platform to fail despite immense financial backing 21.

Execution and Infrastructure Failures

Internal engineering initiatives to build enterprise platforms also face extreme failure rates, often due to organizational misalignment rather than technical limitations. Internal platforms frequently succumb to the "minimal buy-in trap," where a lack of executive sponsorship results in scattered initiatives, poor developer adoption, and the creation of systems that fail to deliver measurable business outcomes 22.

When execution failures occur at scale, the financial and operational consequences are catastrophic. In the automotive sector, the push to build a unified software platform - such as Volkswagen's Cariad initiative - resulted in strategic overreach. The attempt to simultaneously deliver a complete technology stack, custom silicon abstraction, and advanced autonomous driving capabilities led to sprawling codebases exceeding 20 million lines, resulting in years of delays, massive budget overruns, and severe cybersecurity compliance gaps 23. Similarly, the historic CrowdStrike failure in mid-2024, which triggered cascading boot loops across 8.5 million devices globally, underscored the fragility of centralized digital platforms that lack rigorous edge-case testing and automated rollback mechanisms 3024.

Furthermore, the physical infrastructure required to sustain massive digital platforms is increasingly facing intense regulatory and environmental friction. The expansion of hyperscale data centers, necessary for cloud computing and artificial intelligence, has triggered coordinated environmental litigation 25. Large-scale infrastructure projects - such as the 2,100-acre Digital Gateway project in Virginia or Project Skyway in Minnesota - are facing intense legal challenges regarding energy consumption, water usage, and emissions profiles 25. These infrastructural constraints present a growing physical limitation to the otherwise borderless scalability of digital platforms.

The Impact of Generative Artificial Intelligence

The rapid maturation and integration of generative artificial intelligence (GenAI) in 2025 and 2026 has introduced profound disruptions to established platform dynamics. Traditional platform economics relied heavily on the scarcity, friction, and human labor required for content creation and service delivery. Generative AI fundamentally alters these macroeconomic variables on both sides of the multi-sided market 26.

On the supply side, foundation models significantly lower the marginal cost of production and virtually eliminate historical barriers to entry 26. The ability to instantly generate high-fidelity text, images, code, and video allows external producers to saturate platforms with synthetic content. While this dramatically increases the volume of available digital goods, it raises severe concerns regarding quality dilution and copyright infringement 26. As synthetic content floods digital marketplaces, the signal-to-noise ratio degrades precipitously, forcing platforms to invest heavily in algorithmic curation to maintain user trust and prevent ecosystem collapse 26.

On the demand side, platforms leverage GenAI to amplify user engagement through hyper-personalization, utilizing multimodal systems to dynamically alter choice architectures and recommendation feeds in real-time 2627. However, this introduces new market distortions. The deployment of GenAI as an "algorithmic consumer" - such as conversational recommender systems (CRS) - has been shown to alter human purchasing behaviors. Controlled empirical studies indicate that CRS implementations driven by large language models subtly frame choices in ways that consistently increase consumer expenditure toward premium brands . These systems shift the balance of power from the human consumer to the algorithmic intermediary, positioning AI as a potent choice architect that demands intense regulatory oversight .

Despite the challenges of market saturation and algorithmic bias, the macroeconomic impact of AI-driven platforms is overwhelmingly expansive. Economic projections estimate that AI integration could increase global productivity and GDP by 1.5% by 2035, with generative AI technologies fundamentally altering up to 40% of current economic activity 28. This growth is heavily supported by a massive expansion in semiconductor hardware, edge computing, and cloud software services, transitioning AI from experimental novelty to enterprise-grade deployment 2729.

Regional Architectural Divergence in Platform Ecosystems

By 2026, a stark divergence in platform architecture has solidified between Eastern and Western markets, specifically concerning the evolution and adoption of the "Super App." A super app is a comprehensive digital ecosystem, accessible through a unified interface, that integrates a wide range of functionally distinct services - such as financial technology, e-commerce, transportation, food delivery, and messaging 383940.

The Super App Architecture in Eastern Markets

The super app model, pioneered by platforms like WeChat in China and Grab and Gojek in Southeast Asia, resolves the issue of fragmented user experiences by providing a highly centralized infrastructure 3841. Architecturally, these platforms offer a unified identity layer, a seamless integrated payment rail, and a shared data ecosystem for third-party developers building "mini-programs" within the overarching application 3841.

This consolidated architecture radically alters the economics of user retention. It heavily amortizes customer acquisition costs, as users onboarded for a core high-frequency service (e.g., messaging or ride-hailing) are effortlessly cross-sold into adjacent, higher-margin services (e.g., micro-loans, insurance, or e-commerce delivery) 3841. The super app essentially functions as a private operating system, creating an ecosystem where users possess minimal incentive to leave the walled garden, thereby generating massive, cross-service behavioral profiles 3841.

Architectural Divergence in Western Markets

Attempts to directly replicate the monolithic Asian super app model in Western markets (the United States and Europe) have largely stalled. Market analysis indicates that Western consumers display a pronounced aversion to feature bloat, preferring clean, specialized applications over cluttered, multi-purpose interfaces 4230. Furthermore, there is a distinct cultural and historical aversion in the West to knowingly relying on a single corporate entity for the majority of everyday products and services 30.

Crucially, Western regulatory environments actively prohibit the unfettered data sharing across business units required to make a monolithic super app functional. Strict data privacy mandates and intense antitrust scrutiny prevent the seamless consolidation of financial, social, and commercial data that defines the Eastern model 4230.

Consequently, Western platforms have pivoted toward an alternative approach: orchestrating digital ecosystems. Rather than forcing all services into a single user interface, Western platforms rely on deep backend API integrations, modular micro-frontends, and interconnected digital wallets to provide a seamless omnichannel experience across disparate, standalone applications 3842. This "headless" approach allows brands to connect discovery, transactions, and fulfillment across digital and physical environments, providing the continuous, contextual experience of a super app while conforming to Western regulatory and consumer expectations 42.

Antitrust Enforcement and Regulatory Intervention

The immense concentration of economic and biopolitical power within a handful of platform gatekeepers has triggered an aggressive wave of global antitrust enforcement. Regulatory bodies, recognizing the inadequacy of industrial-age antitrust frameworks to manage digital network effects and algorithmic pricing, have initiated multifaceted legal campaigns against dominant technology firms 3132463334.

The United States versus Google

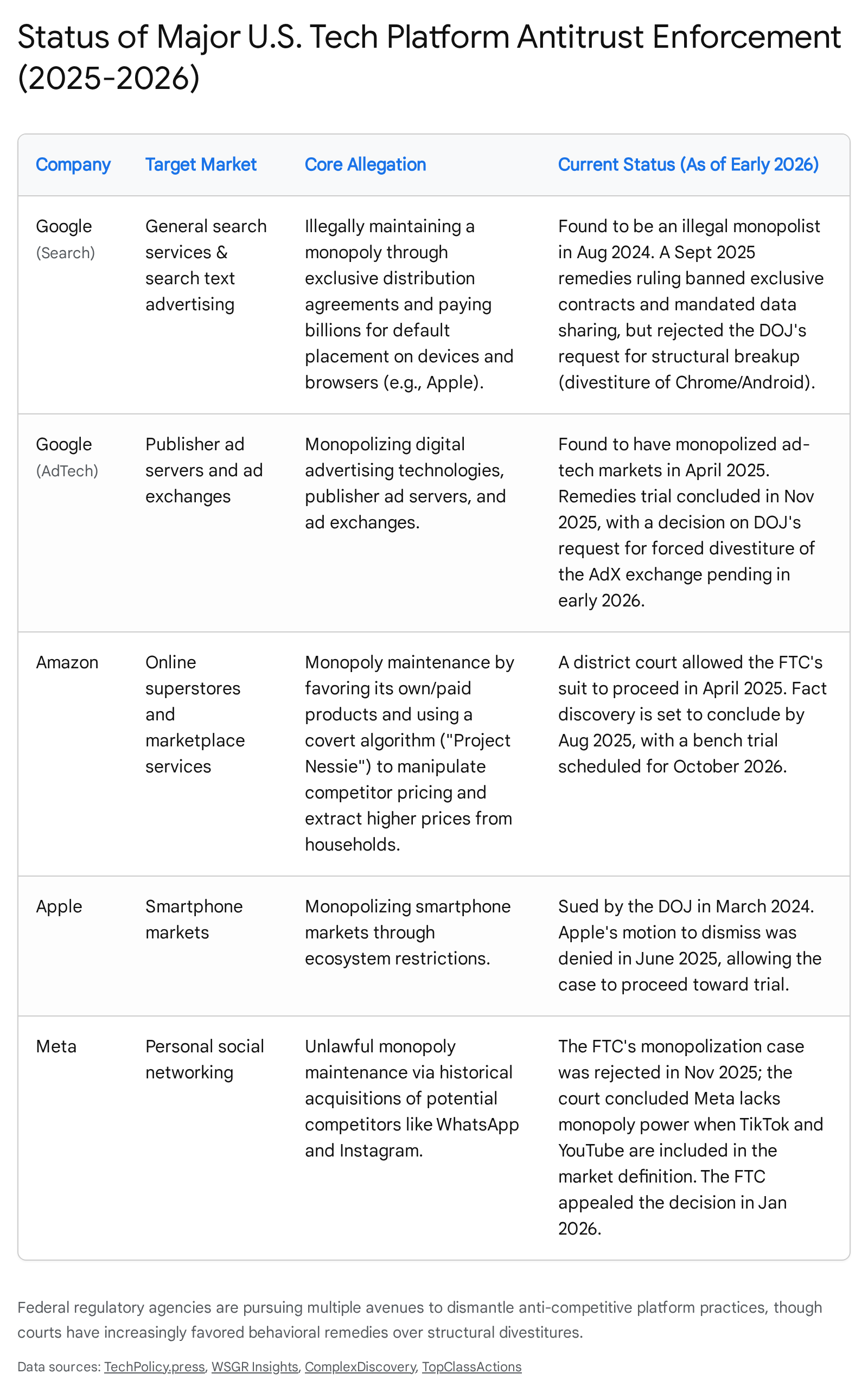

The most consequential development in platform regulation occurred between August 2024 and late 2025 in the landmark United States v. Google LLC case. In August 2024, the U.S. District Court found that Google had illegally maintained monopolies in general search and search text advertising. The court determined that Google weaponized its massive revenue streams - spending upwards of $26.3 billion in 2021 alone - to secure exclusive default placement agreements with device manufacturers and browser developers, including a massive $20 billion arrangement with Apple 355036.

The remedies phase of the trial, concluded in September 2025 by Judge Amit Mehta, marked a significant pivot in antitrust philosophy. The Department of Justice had originally sought extreme structural remedies, including the forced divestiture of the Chrome browser and the Android operating system, alongside severe limitations on artificial intelligence investments 5037. The court firmly rejected these structural breakups. The decision explicitly noted that the rapid emergence and disruptive force of generative AI platforms fundamentally altered the competitive landscape, making the divestiture of Chrome an excessive intervention that could stifle technological innovation 34373839.

Instead, the court imposed strict behavioral remedies designed to neutralize Google's data network effects. The December 2025 Final Judgment prohibited exclusive default distribution contracts, mandated the sharing of Google's highly guarded web search index and user-interaction data with qualified competitors for a period of five years, and required Google to offer syndication licenses for search results and text advertising feeds 503740. This ruling established a vital legal precedent: courts are increasingly favoring targeted data-sharing mandates and behavioral constraints over corporate fragmentation to restore market contestability 5041. Furthermore, Google faces separate, ongoing antitrust litigation regarding its digital advertising technology, where courts are examining exclusionary design within the ad-tech stack 4642.

Actions Against Amazon, Apple, and Meta

Beyond search, enforcement actions are targeting the mechanisms of platform orchestration across the broader tech industry. The Federal Trade Commission's antitrust lawsuit against Amazon, scheduled for trial in October 2026, attacks the company's dual role as marketplace orchestrator and primary retailer 464344. The complaint alleges Amazon operates an illegal monopoly through exclusionary tactics, notably utilizing a covert algorithmic pricing tool dubbed "Project Nessie" to manipulate market-wide pricing and extract over a billion dollars from American households 43. The FTC further alleges that Amazon aggressively punishes third-party sellers who offer lower prices on competing platforms by suppressing their listings, effectively setting an artificial price floor across the internet 4345. This case tests the limits of platform governance, questioning whether aggregation, fulfillment bundling, and price parity rules fundamentally harm consumer welfare 4546.

Similarly, the Department of Justice filed suit against Apple in 2024 for monopolizing smartphone markets. The core allegation centers on Apple's stringent control over app distribution and application programming interfaces, specifically citing the suppression of multi-functional "super apps," alternative digital wallets, and cloud streaming services, which effectively locks consumers into the iOS ecosystem 313246. Conversely, some antitrust actions have faltered; the FTC's monopolization case against Meta regarding its acquisition of WhatsApp and Instagram was rejected in late 2025 after the court determined that the rapid rise of TikTok and YouTube fundamentally undermined the claim that Meta possessed unassailable monopoly power 4647.

Statutory Reforms and the Digital Markets Act

While U.S. enforcement relies heavily on lengthy litigation, the European Union has implemented a system of preemptive, ex-ante regulation via the Digital Markets Act (DMA). The DMA explicitly designates major platforms as "gatekeepers" and imposes strict, immediate behavioral requirements 3348.

The DMA mandates high-level interoperability standards, enforces the ability for consumers to utilize third-party app sideloading, and heavily restricts platforms from combining personal data across disparate services without explicit consent 334748. The impact has been swift and punitive; in early 2025, the European Commission levied substantial fines against gatekeepers for non-compliance, including a €500 million fine against Apple for anti-steering practices and a €200 million fine against Meta regarding data usage choices 47. Early assessments of the DMA indicate measurable success in opening previously closed ecosystems, compelling structural shifts that are beginning to fragment monolithic platform control in European markets 3348.

Conclusion

Platform disruption theory provides the foundational framework for understanding the transition from industrial, pipeline-driven economies to digital, ecosystem-driven architectures. By leveraging superior marginal economics and the compounding power of cross-side and data network effects, multi-sided platforms have successfully reconfigured global value creation. The transition away from internal asset ownership toward the external orchestration of communities represents one of the most significant macroeconomic shifts of the 21st century.

However, the trajectory of platform dominance is not absolute. Structural vulnerabilities - such as the supply-side erosion caused by multi-homing, the commoditization risks embedded in "platform traps," and the rapid decentralization of production costs driven by generative AI - demonstrate that incumbent platforms face significant existential threats 161726. Furthermore, high rates of platform failure due to market saturation, strategic mispricing, and massive infrastructure constraints highlight the extreme difficulty of maintaining a stable, multi-sided equilibrium 262325.

Concurrently, the macroeconomic environment has shifted from one of permissive expansion to rigorous containment. Global regulatory bodies and antitrust courts are actively dismantling the monopolistic architectures of the past decade. By imposing stringent behavioral remedies, prohibiting exclusive lock-ins, and mandating data interoperability, the emerging legal frameworks of 2025 and 2026 seek to neutralize the anti-competitive extremes of network effects 503940. As a result, the next era of platform evolution will be defined not by unchecked aggregation, but by forced openness, decentralized artificial intelligence integration, and the intense competition to orchestrate increasingly fragmented digital ecosystems.