Low-end market disruption pathways

Low-end disruption represents a structural market shift where new entrants displace established industry leaders by initially targeting the least demanding and least profitable customer segments. Rather than competing directly on established performance metrics - a contest incumbents almost always win - the disrupter introduces an offering that is simpler, more accessible, or less expensive. Over time, the disrupter improves its product to meet the needs of mainstream consumers, effectively hollowing out the incumbent's market share from the bottom up. Formulated by Clayton M. Christensen in the mid-1990s, the theory of disruptive innovation remains a foundational concept in strategic management, explaining the persistent failure of well-managed, heavily resourced companies to defend against ostensibly inferior technologies 12.

The academic and strategic discourse surrounding this phenomenon is vast, bridging fields such as organizational behavior, innovation economics, and corporate strategy. Understanding the mechanics of low-end disruption requires a deep dive into the theories of resource dependence, the nature of technological trajectories, and the specific case studies across disparate industries that demonstrate the repeated vulnerability of established enterprises.

The Theoretical Framework of Incumbent Vulnerability

The vulnerability of established firms to low-end disruption is rarely a consequence of managerial incompetence or technological stagnation. Instead, the failure mechanisms are deeply embedded in the rational, profit-maximizing behaviors that initially made the incumbent successful. The theory posits that the very management practices that allow a company to dominate a market ultimately become the root cause of its inability to adapt to disruptive threats 3.

Resource Dependence Theory and Value Networks

The theoretical underpinning of the incumbent's inability to respond to low-end disruption is closely tied to Resource Dependence Theory (RDT). Originally proposed by Jeffrey Pfeffer and Gerald R. Salancik in their 1978 publication, "The External Control of Organizations: A Resource Dependence Perspective," RDT views organizations not as autonomous entities, but as open systems heavily constrained by the external actors that provide critical resources for their survival 456. The core premise of RDT is that power and control reside with those who supply vital resources, namely customers and investors 478.

When applied to the context of technological innovation, RDT explains why established firms consistently ignore disruptive threats. A company's resource allocation processes are inherently biased toward the demands of its most profitable customers and the expectations of its shareholders 7910. If a new technology emerges that offers lower gross margins and appeals only to a peripheral, low-end market segment, the incumbent's best customers will typically express no interest in it 7911. Consequently, corporate resource allocation systems - which are intelligently designed to weed out initiatives that lack clear, near-term profitability and customer demand - will systematically starve the disruptive project of necessary funding 7911. The managers inside the incumbent firm are acting entirely rationally; they are listening to their customers and prioritizing high-margin returns. However, this strict adherence to resource dependence creates an exploitable blind spot, preventing the firm from investing in nascent markets that do not currently satisfy the strict financial criteria imposed by their existing value network 31112.

Furthermore, Christensen categorizes the capabilities of an organization into three elements: Resources, Processes, and Values (the RPV framework) 12. While an incumbent may possess vast resources (capital, talent, technology), its processes (how it develops products and assesses market research) and its values (the criteria by which it prioritizes investments) are optimized for its current business model. In the face of a low-end disruption, these processes and values transform from capabilities into disabilities, as they structurally reject low-margin, small-market opportunities 712.

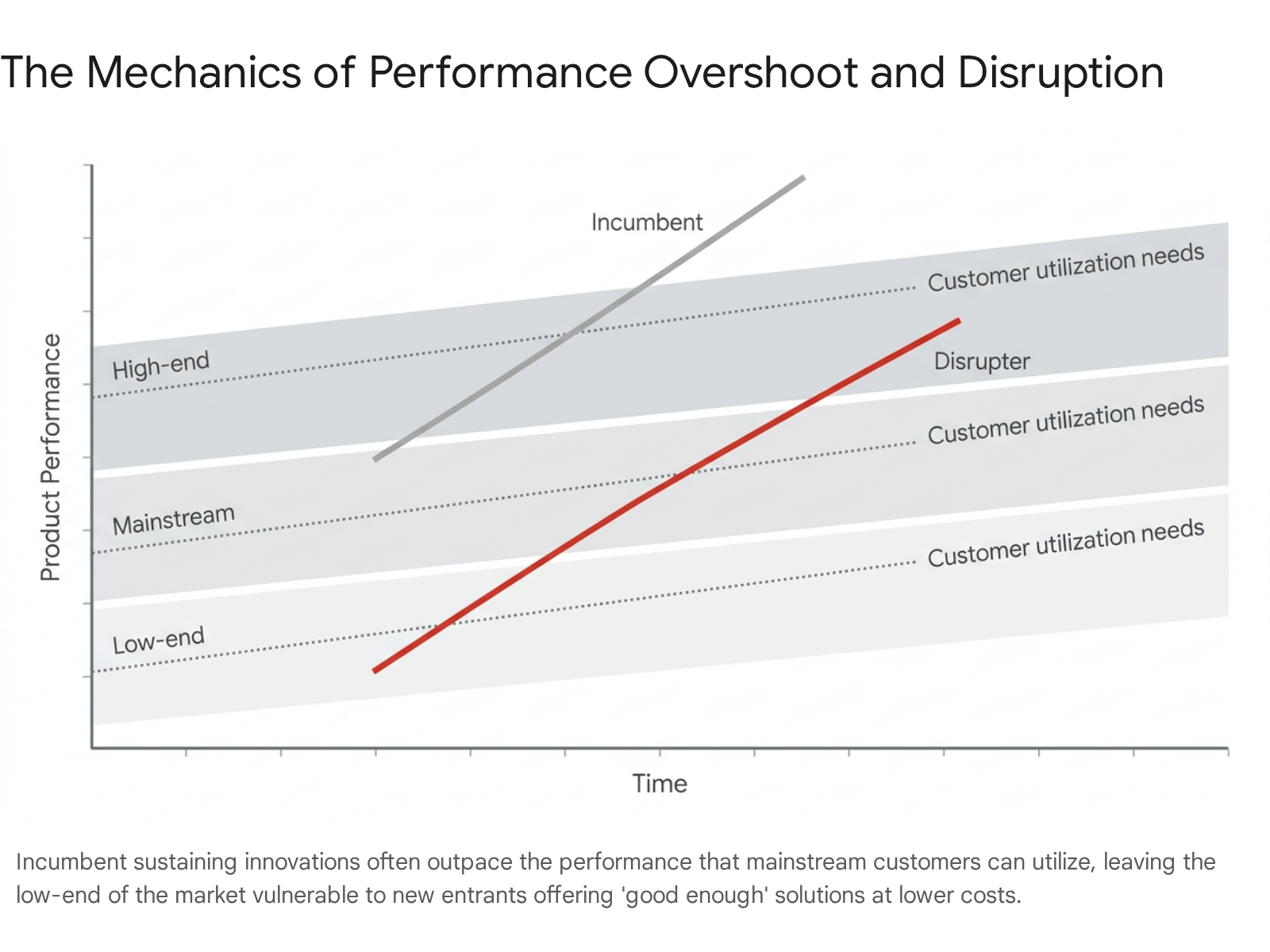

Performance Overshoot and Asymmetric Motivation

The second primary mechanism driving low-end disruption is "performance overshoot." Incumbents consistently engage in sustaining innovation, continually improving their products to satisfy the rigorous demands of high-end customers who are willing to pay premium prices 11314. Over time, however, the trajectory of technological improvement frequently outpaces the ability of mainstream customers to actually utilize or absorb those improvements 1416.

When a product's performance exceeds what the lower and middle tiers of the market require, these segments become structurally "overserved." Overserved customers are fundamentally unwilling to pay premium prices for advanced features they do not need or use 14. This dynamic creates a vacuum at the bottom of the market, providing an opening for a low-end disrupter to enter with a "good enough" product at a significantly lower price point 1316.

When the disrupter claims this lowest tier of the market, the incumbent typically experiences "asymmetric motivation." Because the low-end segment generates the lowest profit margins, the incumbent has little economic incentive to engage in a bitter price war to defend it 11316. Instead, the incumbent willingly concedes the low-end market and reallocates its resources upward toward its most profitable, demanding customers - a phenomenon Christensen describes as a "northeastern pull" on a chart plotting profitability against product complexity 1214.

Initially, this retreat yields a temporary boost in the incumbent's overall profit margins, masking the structural decline taking place 1215. Unopposed at the bottom, the disrupter captures market share, generates revenue, and uses those resources to gradually improve its product quality. The disrupter subsequently moves upmarket to claim the mainstream segment, eventually rendering the incumbent's offerings obsolete when the disruptive technology finally meets the performance demands of the highest tiers 1131416.

Distinction From Price Competition and Obsolescence

It is necessary to meticulously distinguish low-end disruption from generic price competition and raw technological obsolescence, as the terms are frequently conflated in popular business discourse.

A low-end disruption strictly requires an asymmetric business model - a structural advantage that allows the entrant to achieve profitability at discount prices that would be mathematically ruinous for the incumbent to match 1317. Generic price competition, conversely, involves offering the same fundamental product architecture and cost structure at a discount, which well-capitalized incumbents can typically weather or match if sufficiently provoked.

Furthermore, disruption is distinct from technological obsolescence. Obsolescence occurs when a radically superior technology entirely replaces an older one, regardless of market tiers, such as the telegraph being abruptly replaced by the telephone or the floppy disk being replaced by the flash drive 181920. Disruptive technologies, in contrast, are often technologically straightforward, relying on off-the-shelf components assembled in a novel architecture that initially performs worse than the incumbent technology on traditional industry metrics 221.

The disruption framework also distinguishes between low-end disruption and high-end disruption. While low-end disruptors enter the market with a low-performing, low-price product and then work over time to improve performance, high-end disruptors enter the market with a high-performing, premium-priced product and then work over time to improve affordability 22. In low-end disruption, consumers are price-choosers who accept whatever performance correlates with that low price; in high-end disruption, consumers are performance-choosers who accept the high price tag 22.

| Concept | Primary Target | Initial Performance | Technological Nature | Incumbent Response |

|---|---|---|---|---|

| Sustaining Innovation | Existing mainstream & high-end customers | Superior to existing products | Incremental or breakthrough improvements | Rapid adoption and deployment |

| Technological Obsolescence | Entire market simultaneously | Vastly superior paradigm | Radical paradigm shift | Total displacement of old architecture |

| New-Market Disruption | Non-consumers (new market creation) | Lower performance on traditional metrics, higher on convenience/access | Simpler, more accessible technology | Ignored as irrelevant to current business |

| Low-End Disruption | Overserved, price-sensitive existing customers | "Good enough" performance at lower cost | Asymmetric business model, often simpler architecture | Concession of the low-end to protect margins |

Academic Critiques and Methodological Debates

Despite its widespread acceptance in corporate strategy and executive education, the theory of disruptive innovation has been subject to rigorous academic scrutiny and intense debate regarding its predictive power, case selection, and methodological rigor 252324.

The Lepore Critique and Circular Reasoning

In the summer of 2014, Harvard historian Jill Lepore published a highly critical article in The New Yorker titled "The Disruption Machine," which argued that the theory relied heavily on retrospective case selection and suffered from inherent circular reasoning 252325. Lepore posited that the theory's diagnostic framework is largely tautological: if an established company fails, the theory concludes it is because it failed to disrupt itself; if a startup fails, it is framed as the natural risk of epidemic failure inherent in disruption; and if an incumbent succeeds, it is simply because it has not yet been disrupted 2525.

Lepore further argued that Christensen's foundational case studies disregarded empirical examples that did not fit the model cleanly. She concluded that the framework lacked predictive validity, functioning primarily as an explanatory theory for why businesses fail after the fact, rather than a prospective tool 252425. The critique struck a nerve in the business community, prompting Christensen to fiercely defend the theory in a Bloomberg interview, where he characterized Lepore's article as a "criminal act of dishonesty." He argued that she ignored subsequent academic sequels and research that refined the initial model, asserting that disruption theory provides actionable frameworks for executives facing emerging threats, such as the mandate to establish independent business units to pursue disruptive technologies 252627.

Empirical Validations and Predictive Limitations

Other academic studies have sought to quantitatively test the predictive power of disruption theory, attempting to move the debate beyond qualitative historical analysis. In a notable 2015 study published in the MIT Sloan Management Review, researchers Andrew King and Baljir Baartartogtokh surveyed 79 recognized industry experts on 77 historical examples of disruption originally claimed by Christensen 2324.

The researchers evaluated whether the cases explicitly met the four core premises of the theory: originating in a low-end or new-market foothold, possessing an asymmetric business model, featuring incumbent capability to respond but failure to do so, and eventual incumbent displacement 2324. The findings revealed that only 9 percent of Christensen's 77 cases perfectly matched all four elements of his own theory 2324. For nearly 40 percent of the cases, incumbent firms did not actually possess the capabilities to respond to the new threat, contradicting the premise that they simply chose not to due to resource dependence. In another 40 percent, the incumbents were not ultimately displaced by the entrant at all 24.

These academic reviews suggest that while low-end disruption does occur and describes a very real market phenomenon, the precise conditions required for the theory to apply perfectly are significantly rarer than the popular business lexicon suggests 1124. The widespread colloquial use of "disruption" to describe any successful startup, incremental improvement, or radical innovation has fundamentally diluted the term's precise academic definition 1925.

Case Studies of Low-End Disruption Across Sectors

To understand the practical application of low-end disruption, it is necessary to examine how the asymmetric business model pathway materializes in reality. The mechanisms of low-end disruption can be observed across a diverse range of global industries, from heavy manufacturing to specialized healthcare, regional aviation, and software infrastructure.

Industrial Manufacturing: The Steel Mini-Mill Pathway

One of the foundational and most heavily cited case studies of low-end disruption is the evolution of the North American steel industry, specifically the rise of Nucor and the advent of the electric arc furnace, commonly known as the mini-mill 1531.

In the mid-20th century, the global steel market was dominated by massive, vertically integrated steel mills that used traditional blast furnaces to process raw iron ore 3132. These facilities required enormous capital investments - upwards of $6 billion to construct - and operated with exceptionally high fixed costs 12. Nucor, conversely, pioneered the use of the mini-mill, which bypassed iron ore entirely by melting recycled scrap steel using massive quantities of electricity 15. Mini-mills required a fraction of the capital to build (approximately $400 million) and operated with significantly lower labor requirements, demanding only 0.6 hours of labor per ton compared to 2.3 hours for integrated mills 1215.

Crucially, early mini-mill technology yielded metallurgically inferior steel. It was only suitable for the absolute bottom of the market: concrete reinforcing bars, or rebar 15. The integrated steelmakers, behaving exactly as resource dependence theory predicts, happily ceded the low-margin rebar market to Nucor. They viewed rebar as a commoditized, low-profit business that dragged down their overall corporate profitability. By abandoning the rebar market, the integrated mills saw their profit margins artificially improve, validating their strategic retreat to their investors 1215.

However, Nucor used the reliable revenues generated from the rebar market to aggressively refine its electric arc technology. It systematically moved upmarket into angle iron, then into structural beams, and eventually, utilizing revolutionary thin-slab casting technology, into the highly profitable flat-rolled sheet steel market 3228. The economic advantage was devastating. The production cost for hot-rolled sheets via Nucor's thin-slab casting was estimated at $225 per ton, compared to $261.50 per ton for integrated mills, with construction costs for the new lines sitting at nearly half that of traditional facilities 32. By the time Nucor's metallurgical quality matched the exacting requirements of the high-end sheet steel market, the integrated mills had nowhere left to retreat, resulting in massive market share losses, restructurings, and bankruptcies among legacy providers 3228.

Frugal Innovation in Emerging Markets: Healthcare

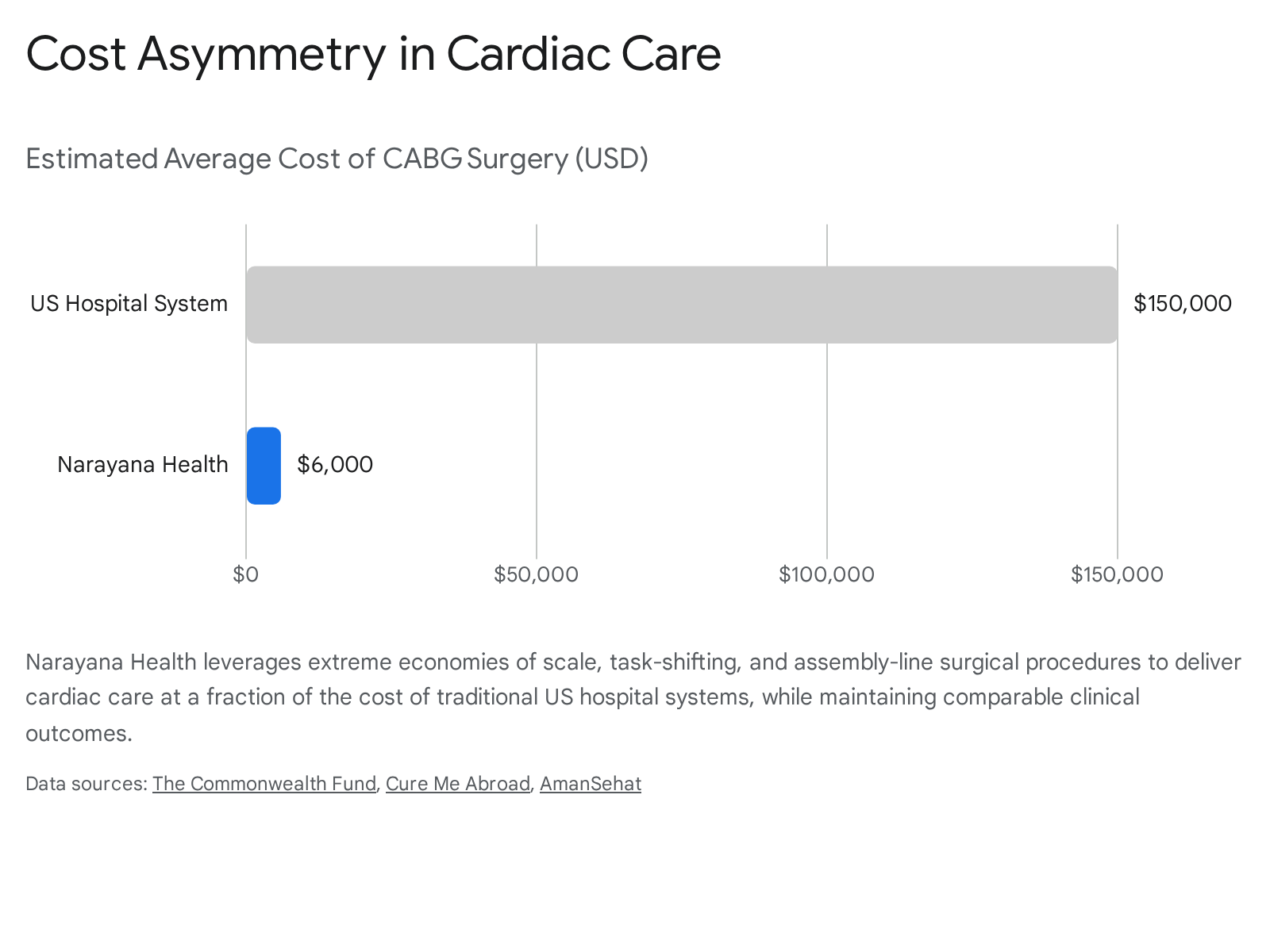

Low-end disruption frequently originates in developing economies through a process known as "frugal innovation." This involves stripping a product or service down to its absolute core functionalities to radically lower costs for underserved populations, avoiding the tendency to over-engineer products with features that low-income consumers cannot afford 293031. This dynamic is prominently evident in the healthcare sector, most notably through the operations of Narayana Health in India.

Cardiac surgery in developed nations operates on a deeply entrenched high-cost, high-margin model. In the United States, the average cost for a coronary artery bypass graft (CABG) ranges from $100,000 to $200,000, and a standard open-heart surgery easily exceeds $100,000 323839. This pricing structure is difficult to dismantle because it is woven into the systemic fabric of the industry, driven by high physician salaries, exorbitant real estate costs, malpractice insurance premiums, and vast administrative overhead required for billing 38.

Dr. Devi Shetty founded Narayana Health to approach cardiac care through a volume-driven, low-cost business model tailored specifically for India's population, where the vast majority of patients pay out-of-pocket and government healthcare spending hovers at roughly 1.5 percent of GDP 3240. The hospital chain implemented an assembly-line concept for surgery and aggressive task-shifting protocols. Highly specialized surgeons perform only the most critical, complex parts of the procedure, leaving pre-operative preparation and post-operative suturing to junior staff and specialized nurses 3240. Under this model, a single surgeon at Narayana might perform 400 to 600 procedures annually, allowing the hospital system to execute up to 150 major surgeries per day 40.

This extreme economy of scale, combined with reengineered supply chains and extensive rural telemedicine networks, allows Narayana Health to perform open-heart surgeries for less than $2,000 on average, and complex CABG procedures for approximately $5,000 to $8,500 323839.

Despite operating at a fractional cost, Narayana Health reports a 30-day mortality rate of around 2 percent and hospital-acquired infection rates that meet or exceed international Joint Commission International (JCI) standards 383933. While this model originated to serve non-consumers in India, it demonstrates the classic disruptive potential to move upmarket geographically, attracting medical tourists from high-cost western regions and threatening incumbent hospital revenues globally 3933. By utilizing a hybrid pricing model where wealthier patients pay for private rooms to subsidize free care for the poorest patients, Narayana Health ensures its low-cost model remains economically viable 33.

Financial Services: The Mobile Money Revolution

A remarkably similar trajectory occurred in the retail banking sector across Sub-Saharan Africa, pioneered by the M-Pesa platform in Kenya. Traditional retail banking relies heavily on physical branch networks and automated teller machines (ATMs). These infrastructure requirements carry high fixed costs, dictating that banks require minimum deposit thresholds to remain profitable 3435. Consequently, prior to 2007, formal banking services were economically inaccessible for the vast majority of the Kenyan population. In the early 2000s, Kenya possessed roughly 1.3 bank branches per 100,000 people, compared to 31 branches per 100,000 in the United States 34. Traditional banks largely ignored the low-income, rural demographic, viewing them accurately as an unprofitable segment under the existing banking architecture 3435.

Safaricom, a mobile network operator, launched M-Pesa in 2007. Crucially, it did not launch as a bank, but as a rudimentary electronic money transfer service operating via simple SMS messages on basic feature phones 3536. It utilized a radically asymmetric business model: instead of building fortified bank branches, M-Pesa leveraged an existing, widespread network of corner stores, petrol stations, and airtime vendors to act as cash-in and cash-out agents 3637. Agents earned a small commission on transactions, creating a highly profitable micro-economy 37. By substituting physical branches with ubiquitous retail agents (growing to over 18,000 locations by 2010), M-Pesa achieved transaction costs low enough to profitably process micro-transactions averaging merely $30 to $40 3637.

Initially serving a fundamental need for urban-to-rural remittances - a classic low-end and new-market foothold catering to people who otherwise had to rely on sending cash via buses - M-Pesa rapidly expanded its capabilities 343638. Over the ensuing decade, the platform evolved into a comprehensive digital financial ecosystem. It began offering virtual savings accounts, merchant payment gateways, and micro-loans, often partnering directly with the very commercial banks it initially bypassed 35. The macro impact was profound: overall financial inclusion in Kenya soared from 26.4 percent in 2006 to over 75 percent in 2016, demonstrating how a low-end disrupter can entirely reshape a national financial architecture 35.

Aviation: The Evolution of Regional Jets

The commercial aviation sector presents a highly nuanced illustration of disruption, demonstrating that yesterday's low-end disrupters frequently become today's incumbents, facing their own competitive threats from new angles.

In the late 1990s and early 2000s, Brazilian aerospace manufacturer Embraer successfully captured significant market share from industry titans Boeing and Airbus by aggressively targeting short-haul, low-demand routes with its ERJ 145 family of regional jets 4748. Boeing and Airbus were focused on sustaining innovations in their highly profitable, larger narrow-body (e.g., 737, A320) and wide-body aircraft 4749. The duopoly largely ceded the 50-to-75 seat market to Embraer and Bombardier, because operating a massive 737 on a low-traffic regional route resulted in too many empty seats, making it economically unviable for airlines 4749. Embraer's smaller regional jets offered a low-cost, "good enough" solution for these thin routes, allowing airlines to utilize fewer crew members and burn less overall fuel, even if the per-seat operating costs were technically higher than those of larger jets flying full 47. The ERJ 145 proved highly reliable, recording zero passenger fatalities in scheduled airline service, cementing its role at the bottom of the commercial aviation market 4850.

However, the dynamics of performance and cost efficiency have shifted dramatically. As Embraer sought higher margins by moving upmarket into the 100-150 seat segment with its newer E-Jet E2 family (e.g., the E195-E2), it began competing directly with the lower end of the Airbus and Boeing product lines 513953. Simultaneously, Airbus aggressively targeted this exact overlap by acquiring the Bombardier CSeries program, rebranding it as the A220.

The A220 represents a severe structural threat to Embraer's traditional dominance because it offers vastly superior fuel efficiency. For example, the A220 boasts a fuel-per-seat ratio of approximately 105 MPG, compared to 66.5 MPG for older ERJ 190 models, yielding significantly lower block-hour costs on slightly higher capacity routes 47. Facing this pressure from above, Embraer is now utilizing classic asymmetric tactics against Airbus's massive success. Because Airbus faces immense, multi-year production backlogs for its narrow-body aircraft, Embraer is securing orders from major carriers - such as LATAM - by leveraging rapid aircraft availability and competitive pricing for its E2 jets 5153. Embraer is effectively using the incumbent's massive scale and slow delivery timeline as an exploitable vulnerability to capture narrow-body market share 53.

Software and Data Infrastructure: The SQLite Paradigm

In the realm of enterprise software, the disruption of database architecture provides a stark example of low-end market entry evolving into enterprise dominance. Historically, the database market has been fiercely controlled by massive, centralized client/server architectures, such as Oracle, Microsoft SQL Server, and PostgreSQL 5440. These systems emphasize high concurrency, massive scalability, and strict centralized control, but they inherently require significant administrative overhead, complex configuration, and dedicated server environments 40.

SQLite emerged in the year 2000 as a serverless, embedded database contained entirely within a single, lightweight file (compiled to less than 750 KiB) 545641. In its early iterations, it lacked the robust features demanded by enterprise IT departments: it relied on single-writer concurrency file-level locks, had no built-in network replication capabilities, and was widely dismissed by the professional developer community as a "toy" unsuitable for serious production environments 4142. As its creator noted, SQLite did not intend to compete with enterprise servers; it competed with the standard fopen() command used by developers for basic local file storage 40.

By dominating the absolute bottom of the market - serving as the default local data storage engine for mobile applications, web browsers, televisions, and IoT devices - SQLite quietly became the most widely deployed database engine in the history of software, running on trillions of devices, including Airbus flight systems and Mars rovers 564142.

Over time, sustaining innovations and surrounding ecosystem developments effectively mitigated SQLite's initial enterprise limitations. The introduction of Write-Ahead Logging (WAL) allowed for concurrent reads, and modern edge-replication tools (such as Turso, Cloudflare D1, and Litestream) solved the geographic distribution problem 4142. Today, SQLite is moving aggressively upmarket into the server realm. For a vast class of web applications that are read-heavy and do not require massive write-concurrency, SQLite offers zero-latency local reads, absolutely zero operational overhead, and profound architectural simplicity 4042. It is actively displacing traditional client/server databases in cloud edge computing environments, successfully executing a textbook low-end disruption against entrenched enterprise SQL servers 4142.

Generative AI and the Compression of the Disruption Timeline

The advent of Artificial Intelligence, specifically Large Language Models (LLMs), is fundamentally altering both the pace and the underlying mechanics of low-end disruption in the global software and services sectors 5960.

The Cost Disruption of Open-Source AI

The generative AI market is currently experiencing a rapid low-end disruption cycle, driven aggressively by open-source models challenging proprietary incumbents. OpenAI's GPT-4 established the high-end market standard for complex logical reasoning, multimodal capabilities, and creative text generation, but it did so at a premium enterprise price point (historically scaling around $30 per million input tokens and $60 per million output tokens via API) 614363. Furthermore, utilizing proprietary models requires routing highly sensitive corporate data through external third-party servers 61.

Meta's Llama 3 family of models (specifically the 8B and 70B parameter versions) entered the market as an open-source alternative. While initially lacking the ultimate reasoning ceiling and multimodal complexity of GPT-4, Llama 3 70B achieves an estimated 85 to 95 percent of GPT-4's performance on standard, high-volume business tasks, including document summarization, text classification, and basic question-answering 6164.

Crucially, Llama 3 leverages a profoundly asymmetric cost model. Because the model weights are openly available, enterprises can self-host the model or utilize independent cloud providers to run inference at a fraction of the cost 614363. Processing input tokens through a cloud-hosted Llama 3.1 8B model can be up to 1,000 times cheaper than processing them through the GPT-4 API (dropping from $30.00 to roughly $0.03 per million tokens) 6365. Furthermore, on optimized hardware, smaller open-source models can process tokens significantly faster than their massive proprietary counterparts 61. For enterprise use cases involving high-volume, low-complexity text processing where data privacy is paramount, Llama 3 acts as the ultimate "good enough" product that drastically undercuts the incumbent's pricing model 616364.

| AI Model Architecture | Primary Deployment Strategy | Ecosystem Role | Est. Input Cost (per 1M tokens) | General Performance Profile |

|---|---|---|---|---|

| GPT-4 (OpenAI) | Proprietary API / Subscription | High-end incumbent | ~$30.00 | Industry-leading complex reasoning, coding, and context |

| Llama 3 70B (Meta) | Open-source / Self-hosted / Cloud API | Mid-market alternative | Variable (Self-hosted) | 85-95% of GPT-4 on standard business tasks |

| Llama 3.1 8B (Meta) | Open-source / Cloud API | Low-end disrupter | ~$0.03 | Highly efficient for basic NLP tasks, ultra-low operational cost |

Note: Pricing metrics are highly variable and dependent on specific cloud providers and negotiated enterprise scaling tiers 616465.

Software-as-a-Service (SaaS) and Lowered Barriers

The timeline required for a disruptive technology to capture market share is heavily influenced by the underlying infrastructure of the target industry. Historically, Software-as-a-Service (SaaS) was itself a disruptive force that unseated traditional on-premise software by offering lower upfront costs, easier deployment, and the elimination of physical installation media 4445. However, it took SaaS platforms more than four years to reach a mere 2 percent market share in the global enterprise software market 59.

Generative AI reached that exact same 2 percent threshold in approximately one year, and McKinsey estimates it is primed to capture 10 percent of related software spending by 2028 59. This unprecedented disruption velocity is possible because generative AI dramatically lowers the barriers to entry for software development itself 5946. By automating code generation and allowing for natural language programming, AI structurally reduces the economic surplus that incumbent software companies derive purely from their engineering moats 46.

Incumbent SaaS providers, who rely heavily on per-seat licensing models for their recurring revenue, face immediate threats 6046. A new cohort of nimble upstarts, emboldened by the lower costs of software development, can replicate existing SaaS workflows quickly and inexpensively, attacking incumbents from the bottom of the market with highly automated, niche solutions tailored to specific verticals 5946.

Furthermore, the imminent transition to "Agentic AI" - systems that autonomously execute complex workflows rather than acting as passive tools requiring human input - threatens to fundamentally unbundle the traditional SaaS user interface 6047. In a "headless" software environment where AI agents interact directly with underlying APIs to execute tasks, the primary defensive moat of many SaaS incumbents (their polished user experience and unified dashboard) becomes entirely irrelevant 60. This shift forces a systemic transition from selling software licenses as a tool (SaaS) to selling guaranteed outcomes (Agent-as-a-Service), opening the door for low-end disrupters to bypass traditional enterprise software procurement channels entirely 604748.

Conclusion

The low-end disruption pathway remains a potent, if frequently misunderstood, force in global market dynamics. The persistent vulnerability of established firms is rarely due to a lack of engineering talent or technological capability; rather, it is a direct consequence of their adherence to resource dependence. The rational, institutionalized pursuit of high-margin customers systematically blinds incumbent management teams to emerging threats festering at the bottom of the market.

Whether observing the displacement of massive integrated steel mills by scrap-melting mini-mills, the radical cost compression in frugal emerging-market healthcare models, or the rapid ascendency of open-source AI models against proprietary tech giants, the underlying mechanics are structurally identical. The disrupter leverages an asymmetric business model to achieve profitability at price points the incumbent cannot rationally match, establishes a quiet foothold among overserved or ignored customers, and steadily moves upmarket as its performance technology inevitably improves. As modern cloud infrastructure and generative artificial intelligence systematically lower the barriers to entry across virtually all knowledge sectors, the velocity of low-end disruption is accelerating, requiring incumbents to proactively disrupt their own business models before external entrants hollow out their market share from below.