Ecosystem disruption and platform displacement of value chains

Theoretical Foundations of Ecosystem Disruption

The theory of ecosystem disruption represents a fundamental departure from classical models of strategic management and competitive displacement. Historically, disruption was conceptualized through the lens of intra-industry competition, where new entrants introduced cheaper, simpler products that gradually moved upmarket to displace established incumbents within a defined linear value chain. Modern disruption, however, breaks industry boundaries and redefines entire ecosystems, shifting the basis of competition from individual firm advantages to the alignment and orchestration of multi-actor networks 1.

Traditional strategic frameworks, such as industrial organization theory and Porter's Five Forces, operate on the assumption of closed value chains and emphasize erecting barriers against competitors, suppliers, and buyers 23. In contrast, platform strategy necessitates eliminating barriers to production and consumption to maximize interaction value, highlighting the limitations of traditional theories in explaining phenomena like platform competition and ecosystem dynamics 32. Ecosystem disruption occurs when a platform orchestrator reconfigures the fundamental value proposition of a market, displacing the traditional linear value chain not merely by producing a superior standalone product, but by fundamentally altering the architecture of supply and demand integration 13.

A critical vulnerability for legacy organizations navigating this shift is the "ego-system trap," a cognitive and strategic bias wherein firms define their ecosystems around their own assets and historical positions rather than the end-user value proposition 1. This blinds incumbents to the necessity of re-aligning partners and co-innovators when crossing into new domains. True ecosystem orchestration requires a transition from hierarchical authority to network diplomacy, demanding that orchestrators manage decentralized innovation, coordinate autonomous complementors, and establish governance mechanisms that align the incentives of self-interested actors toward a shared system-level outcome 145.

Evolutionary Parallels in Strategic Management

The conceptualization of the "ecosystem" in business borrows heavily from evolutionary biology and ecology, originally adapted in the 1990s to describe how successful businesses evolve by adapting to their environments through co-evolution with other organizations 5. In natural ecosystems, the effects of a disturbance are rarely linear. Disturbance theory indicates that interventions can result in positive, negative, or neutral net effects, often pushing a system across non-linear thresholds into entirely new functional regimes 697.

Similarly, in digital ecosystems, technological disruptions do not simply reduce or increase efficiency uniformly across a value chain. They may stimulate certain functions at the expense of others, leading to complex, system-wide retrogression or adaptive progression (aromorphosis) 68. Because of this complexity, accurate modeling of ecosystem disruption requires acknowledging inherent uncertainty. Just as ecologists utilize sensitivity analysis, Bayesian inference, and model calibration to account for predictive uncertainty in environmental forecasting, strategic analysts must express calibrated uncertainty regarding the long-term impacts of platform displacement, recognizing that ecosystems continuously evolve and that dominant gatekeepers remain susceptible to novel disturbances 9.

Structural Distinctions Between Pipelines and Platforms

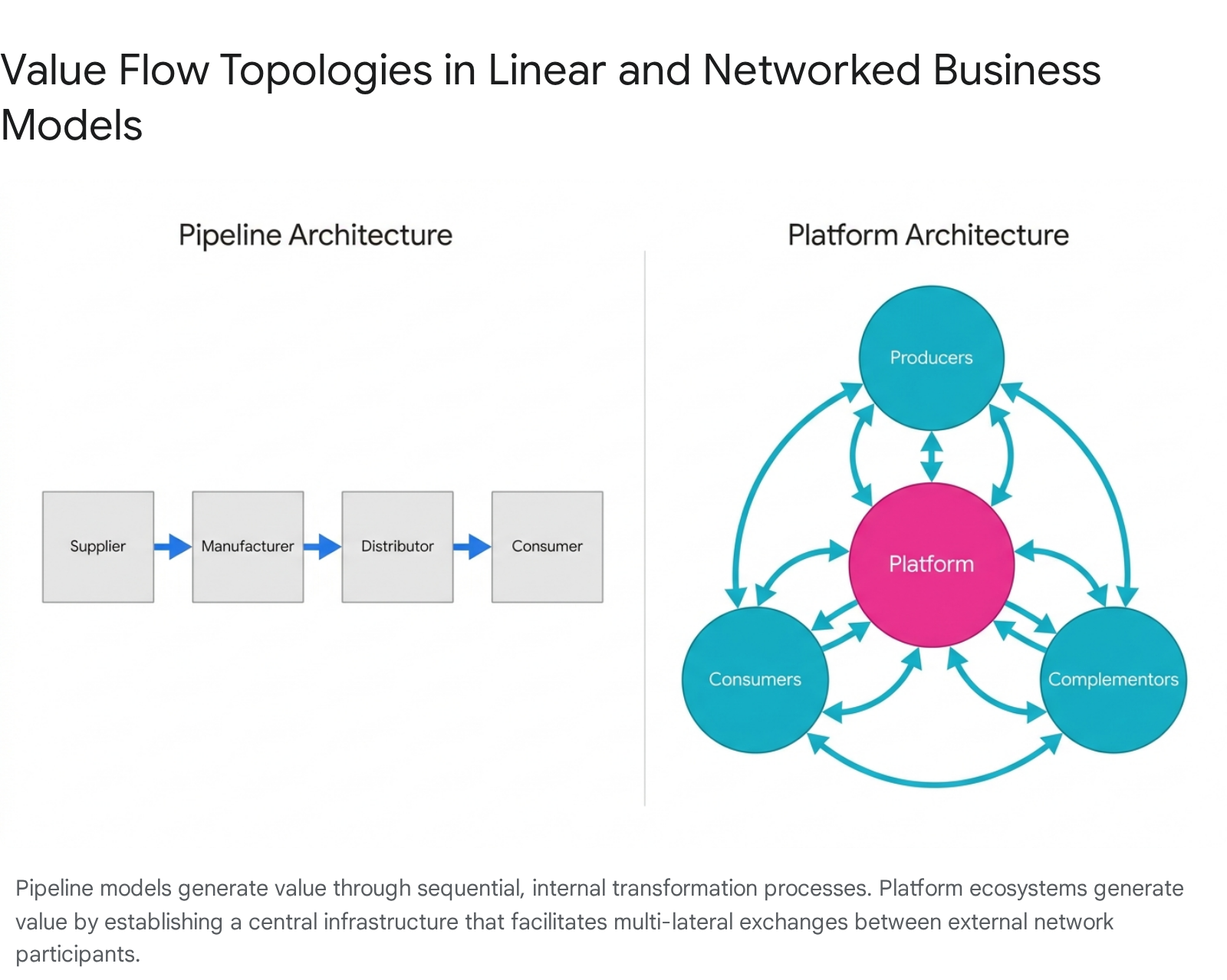

To understand how traditional value chains are displaced, it is necessary to contrast their structural architectures with those of platform ecosystems. Traditional value-chain-oriented businesses operate as "pipelines." They rely on a linear sequence of activities - design, production, distribution, and marketing - where value is added sequentially before a finalized product or service is pushed to the consumer at the end of the line 3101112.

Platform ecosystems, conversely, do not manufacture goods or deliver services directly. Instead, they provide the digital infrastructure and governance rules that facilitate interactions between external producers and consumers 2111314. This architectural shift transitions the firm's role from resource control to resource orchestration 211.

The divergence in these architectures fundamentally alters scalability, marginal costs, and financial performance profiles. Pipeline growth is tied to the expansion of physical capacity and inventory, rendering it capital-intensive and subject to diminishing returns due to the friction of physical asset management 10. Platforms, operating as asset-light facilitators, face near-zero marginal costs for adding new participants to their networks 31015.

Operational Divergence and Capital Intensity

This structural advantage is directly reflected in corporate financial metrics. Asset-light models typically achieve a Return on Invested Capital (ROIC) ranging from 25% to 50%, compared to 8% to 15% for their asset-heavy peers 16. Furthermore, platforms enjoy significantly higher free cash flow conversion rates - often converting 80% to 90% of EBITDA into free cash flow, whereas pipeline businesses typically convert between 30% and 50% 16.

| Metric / Characteristic | Linear Pipeline Model | Platform Ecosystem Model |

|---|---|---|

| Value Creation Mechanism | Sequential transformation of inputs into outputs; internal optimization. | Facilitation of multi-sided interactions; external orchestration. |

| Asset Strategy | Asset-heavy; ownership or leasing of physical infrastructure and inventory. | Asset-light; leverages peer-provided assets and external communities. |

| Primary Growth Driver | Economies of scale in production; supply-side efficiencies. | Network effects (direct and indirect); demand-side economies of scale. |

| Marginal Cost of Scaling | High; requires proportional increases in capital expenditure and labor. | Near-zero; digital infrastructure scales interactions with minimal added cost. |

| Key Performance Indicators | Inventory turnover, capacity utilization, gross margin per unit. | Interaction volume, ecosystem engagement, network liquidity, data yield. |

| Return on Invested Capital (ROIC) | Typically 8% to 15%. | Typically 25% to 50%. |

Table data synthesized from structural and financial analyses of business models 231016.

Financial Displacement Metrics and Industry Case Studies

To measure how platforms disrupt and displace traditional value chains, examining the divergence in capital valuation, labor compensation, and revenue efficiency is necessary. The shift from asset-heavy ownership to asset-light orchestration has triggered market reevaluations across multiple legacy industries, including hospitality, automotive manufacturing, and local mobility.

Asset-Light Leverage in the Hospitality Sector

The hospitality industry provides a stark contrast between an asset-heavy pipeline framework and an asset-light ecosystem model. Marriott International operates primarily as a traditional pipeline, requiring substantial physical infrastructure and capital deployment, whereas Airbnb operates a two-sided marketplace connecting property owners with temporary tenants 1314.

While both entities maintain relatively similar market capitalizations - roughly $78.9 billion for Marriott and $79.4 billion for Airbnb as of early 2025 - their underlying efficiency metrics diverge drastically 17. Airbnb records a Return on Equity (ROE) of 30.63% and a net margin of 20.51%, reflecting the high capital efficiency of externalizing property ownership to ecosystem participants 18. Conversely, Marriott exhibits a net margin near 10% alongside significant liquidity constraints characteristic of asset-heavy operations 18. By avoiding the friction of property acquisition and maintenance, the platform model achieves superior free cash flow conversion and reinvestment flexibility 1819.

| Financial Metric (2024 - 2025 Estimates) | Airbnb (Platform) | Marriott International (Pipeline) |

|---|---|---|

| Market Capitalization | ~$79.40 Billion | ~$78.95 Billion |

| Return on Equity (ROE) | 30.63% | -68.97% |

| Net Profit Margin | 20.51% | ~10.0% |

| Dividend Yield | 0.00% (High R&D Reinvestment) | 0.86% (27.6% Payout Ratio) |

Table data synthesized from comparative financial analyses 1718.

Capital Valuation Divergence in Automotive Manufacturing

In the automotive sector, the displacement logic is evident in the divergence between physical manufacturing output and market capitalization. Traditional automakers operate linear pipelines focused on optimizing the production and distribution of physical vehicles. For instance, Ford Motor Co., with 173,000 employees, generates roughly $169.8 billion in revenue, equating to a revenue-per-employee metric of $0.98 million 20. Kia leads the legacy automakers in this specific efficiency metric at $2.13 million per employee 20.

Tesla, however, presents a valuation anomaly that is deeply tied to platform strategy. Despite a lower revenue-per-employee ratio of $0.74 million and significantly lower production volumes than legacy automakers, Tesla maintains a market capitalization exceeding $1.18 trillion, making it roughly 24 times more valuable than Ford 2025. This valuation spread indicates that markets price Tesla not strictly as an automotive pipeline, but as an ecosystem orchestrator and AI robotics platform 2521. The expectation is that proprietary data harvested from its vehicles will establish a compounding data moat for autonomous driving and energy networks, creating long-term network effects that traditional metal-bending manufacturers cannot replicate 2522.

Labor Compensation and Capacity Utilization in Mobility

The displacement of traditional taxi services by ride-hailing platforms like Uber highlights how orchestrators restructure labor markets and capacity utilization. Traditional taxi operators rely on fixed-cost compensation models, typically requiring drivers to purchase or lease medallions regardless of the fares collected 2324. In contrast, platform orchestrators utilize proportional compensation schemes, extracting a percentage fee per transaction and drastically reducing the barrier to entry 23.

Analyses of inter-temporal substitution elasticity (ISE) reveal that platform drivers optimize their schedules around peak demand, resulting in higher capacity utilization - the percentage of time a vehicle actually contains a paying passenger 2325. Consequently, the hourly earnings of self-employed platform drivers often exceed those of traditional taxi drivers in comparable markets, though the platform model shifts asset depreciation, insurance, and fuel costs entirely onto the independent contractor 2526. While traditional taxi industry volume is projected to decline to $132.75 billion by 2029, the orchestrator model thrives on removing the friction of fixed lease costs, leveraging dynamic pricing to continually balance supply and demand 2326.

The Architecture and Mechanics of Data Moats

Platform orchestrators displace traditional pipelines through the dynamic utilization and amplification of network effects. When a platform establishes a marketplace or technical architecture, it benefits from demand-side economies of scale. Direct (same-side) network effects increase the platform's value as the user base expands; subsequently, this density triggers indirect (cross-side) network effects, strengthening the platform's attractiveness to third-party developers, advertisers, and sellers 272829.

A critical phenomenon in this displacement is temporal asymmetry in cross-side network effects. The conversion of a platform user base into robust demand for third-party complementary applications is not instantaneous 29. Application developers require time to identify and build functionalities that match diverse user needs. However, once established, this complementary ecosystem creates high switching costs and formidable lock-in effects 2729.

Engineering Proprietary Feedback Loops

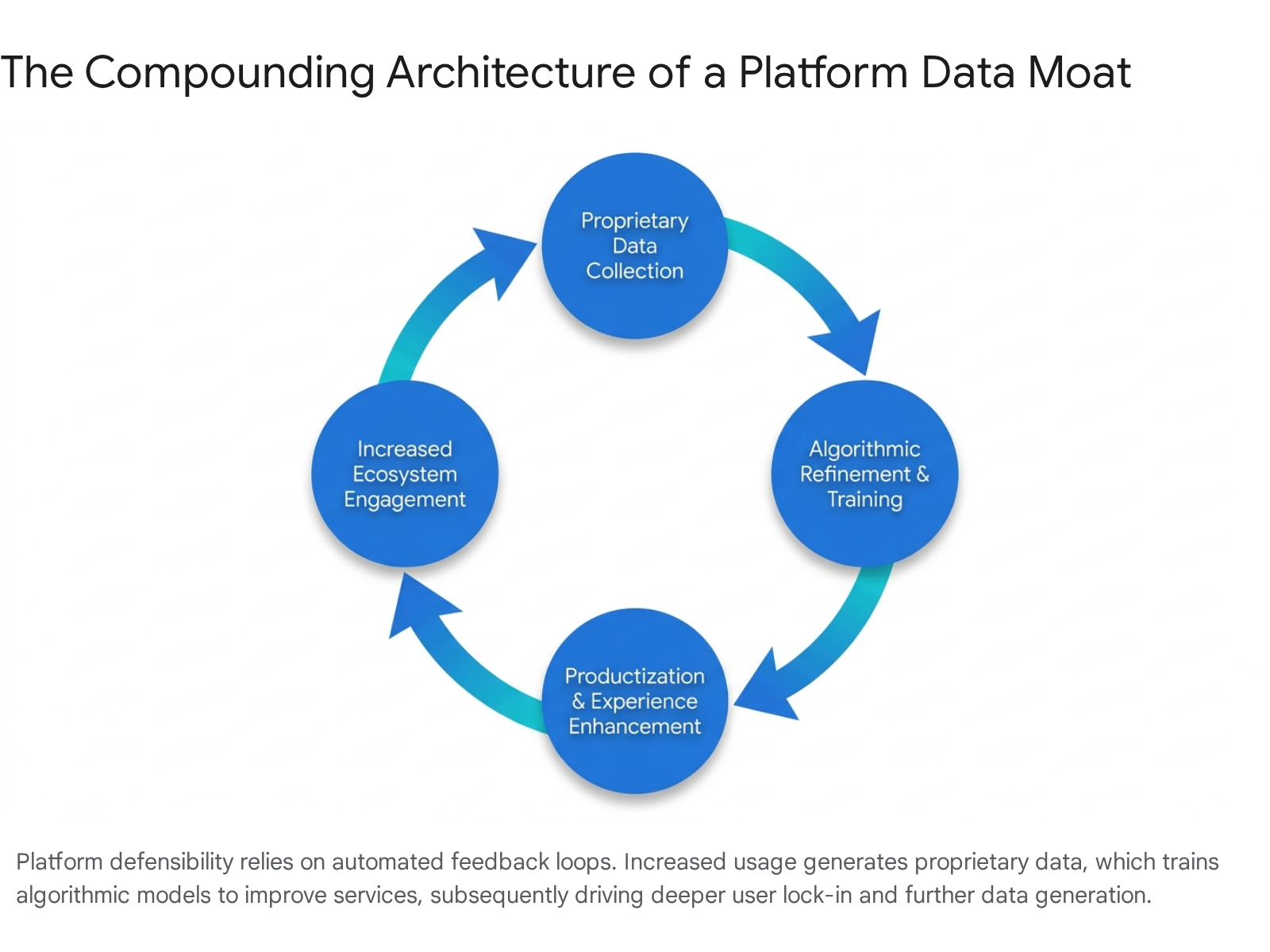

The primary defensive architecture of a modern platform ecosystem is the "data moat." In the contemporary technological landscape, competitive advantage is no longer derived merely from possessing large volumes of static data. Strategic defensibility is engineered through compounding structural layers: data network effects, integration depth, sovereign architecture, and vertical intelligence 3031.

Data moats are engineered through automated, closed-loop feedback systems. When a platform captures proprietary signals - such as search behavior, fulfillment logistics, and transaction histories - at immense scale, machine learning models continuously productize this raw data into optimized workflows, demand forecasting, and personalized recommendations 31.

This architecture creates an exponential value acceleration where the final fraction of algorithmic performance improvement requires exponentially more data and effort, establishing a barrier to entry that new competitors cannot easily breach 31. By turning cognitive and analytical work into scalable infrastructure - such as automated data pipelines and fine-tuned models - platforms serve additional users at a near-zero incremental cost 31. Consequently, traditional software providers offering rule-based point solutions face severe displacement risks from AI-native platform orchestrators that embed automated decision-making across integrated workflows 32.

Platform Disruption in Emerging Markets

The epicenter of rapid platform disruption and ecosystem orchestration is increasingly shifting toward emerging markets. Driven by the structural rewiring of globalization, technological acceleration, and geopolitical fragmentation, emerging economies are transitioning from the world's manufacturing hubs to global innovation centers 333435.

Business-to-Business Ecosystem Transformation

In markets across India, the ASEAN region, and Latin America, platform orchestrators are rapidly displacing traditional, highly fragmented B2B supply chains 36. The traditional retail landscape in these regions is dominated by millions of independent grocers - such as the roughly 6.6 million kiranas in India or the warungs in Indonesia - that act as vital community hubs but suffer from severe inefficiencies in procurement, logistics, and inventory management .

Rather than attempting to eradicate these micro-retailers, digital B2B marketplaces, such as Udaan in India or GoTo and Bukalapak in Indonesia, act as ecosystem orchestrators 36. They connect independent stores directly to Fast-Moving Consumer Goods (FMCG) manufacturers, digitizing supply routes, offering integrated digital payments, and utilizing data analytics to optimize inventory. This model of ecosystem orchestration integrates the existing pipeline into a digitized network, capturing value through transaction facilitation and aggregated data visibility rather than direct asset control 37.

Supply Chain Finance and Credit Resolution

The orchestration of commerce naturally extends into financial disruption. Fintech platforms in emerging markets utilize digital footprints, point-of-sale payment data, and e-commerce transaction histories to verify corporate identity and assess credit risk 38. Platforms like Inbonis and Lnndo employ alternative data to provide rapid micro-loans and working capital to Small and Medium-sized Enterprises (SMEs) that are traditionally ignored or underserved by incumbent banks 38.

By orchestrating logistics, commerce, and finance on a single platform, these enterprises establish formidable, localized data moats 3638. These structural tailwinds supporting emerging market platforms are further reinforced by their proximity to AI-critical commodities. Resource-rich emerging markets control significant shares of the rare earth elements, copper, and semiconductor manufacturing capabilities required for advanced data infrastructures, fundamentally shifting supply chains away from linear models toward resilient, regional ecosystem networks 333439.

Defensive Orchestration by Industry Incumbents

Incumbent pipeline organizations, faced with disruptive threats that bleed across industry boundaries, often struggle to mount effective responses. Years of underinvestment in flexible technology, combined with a legacy mindset that prioritizes slow-but-steady growth and dividend payouts over transformative R&D, leave traditional enterprises vulnerable to nimble orchestrators 4041. Furthermore, the initial signals of ecosystem disruption are frequently dismissed by incumbents who falsely believe their niche markets are sheltered from digital platforms 40.

Strategic Integration and Value Convergence

When forced to respond, incumbents generally attempt to graft digital solutions onto existing pipeline frameworks. This approach rarely yields sustainable platform dynamics because it fails to address the two-sided nature of ecosystem value creation, where building tools for both producers and consumers simultaneously is required to solve the "chicken and egg" liquidity problem 3.

However, advanced incumbents are pursuing value convergence strategies. Academic frameworks identify distinct pathways for this convergence, including pipelines evolving into platforms with asset control (e.g., zipcar-style mobility), pipelines transitioning fully to peer-based platforms, or platforms adopting pipeline elements like owned inventory 1013. To defend their market share, incumbents must pivot toward "defensive orchestration," utilizing their existing assets, domain expertise, and brand trust to build proprietary platforms or enter collaborative alliances 4243.

Sovereign Consortiums and Shared Infrastructures

One of the most potent defensive mechanisms against global platform monopolies is the formation of inter-sector and public-private consortiums. In regions highly concerned with digital sovereignty and the monopolistic power of hyper-scalers (e.g., Amazon, Microsoft, Google), industries are collaborating to build shared, decentralized data infrastructures 4445.

The European Union's Gaia-X initiative is a paramount example of macro-level defensive orchestration 444546. Designed to counteract the hegemony of non-European cloud platform gatekeepers, Gaia-X is not a centralized cloud but a federated ecosystem of interconnected nodes governed by shared standards of interoperability, transparency, and data sovereignty 4445. By establishing compliance frameworks like the Distributed Open Marketplace for Europe (DOME) and integrating automated credentialing systems, these consortiums allow traditional enterprises to exchange data securely without surrendering control to a central orchestrator 4647.

Similar patterns are emerging in specific industrial verticals. In the automotive industry, projects like Catena-X aim to orchestrate data across the entire supply chain, from original equipment manufacturers (OEMs) to raw material suppliers, creating a resilient network that defends against incursions by tech platforms seeking to dominate in-car operating systems and mobility services 454856. These inter-sector partnerships demonstrate that ecosystem defense is most effectively pursued in a coalition, sharing the massive capital and technical requirements necessary to rival established platform leaders 149.

Regulatory Scrutiny and Market Restraints

The unprecedented scale and monopolistic tendencies of platform ecosystems have triggered aggressive responses from global regulatory bodies, fundamentally altering how orchestrators operate. Because network effects naturally drive markets toward winner-takes-all outcomes, dominant platforms inevitably acquire outsized structural power, allowing them to dictate terms to complementors and consumers 2850. As platforms mature, practices that initially incentivized ecosystem participation - such as subsidized access and open APIs - are frequently replaced by rent-seeking behaviors, increased fees, and the self-preferencing of proprietary services over third-party offerings 50.

Transition from Exclusionary to Exploitative Frameworks

In response, antitrust enforcement in regions like the European Union and the United Kingdom has evolved significantly, shifting focus from traditional exclusionary theories of harm toward exploitative conduct in digital markets 5152. The implementation of ex-ante regulatory frameworks, most notably the EU's Digital Markets Act (DMA) and the UK's Digital Markets, Competition and Consumers Act (DMCC), designates structural "gatekeepers" and imposes strict interoperability and fairness obligations 5153.

In 2024 and 2025, regulatory bodies demonstrated a willingness to intervene directly in platform mechanics. The European Commission launched non-compliance investigations into major tech entities regarding their adherence to DMA obligations and initiated specification proceedings to enforce interoperability standards 53. Similarly, enforcement actions cracked down on labour market cartel practices within gig-economy ecosystems, heavily fining platforms for no-poach and market-allocation arrangements 51.

| Region | Primary Regulatory Frameworks & Focus Areas (2024 - 2025) | Key Enforcement Actions & Trends |

|---|---|---|

| European Union | Digital Markets Act (DMA); Focus on exploitative abuses and interoperability. | Specification proceedings against gatekeepers; €329M fines for labour cartels (Delivery Hero/Glovo) 5153. |

| United Kingdom | Digital Markets, Competition and Consumers Act (DMCC). | Shift toward pro-investment pragmatism; cloud service market investigations 51. |

| United States | DOJ/FTC focus on Big Tech conduct; pragmatic stance on AI transactions. | Landmark monopolization trials regarding search and ad-tech self-preferencing 515254. |

| Mainland China | Provisions on Prohibiting Abuse of Market Dominance. | High fines in pharmaceutical, public utilities, and financial data sectors (Sumscope case) 55. |

Table data synthesized from global antitrust and competition reviews 5152535455.

Global Enforcement Dynamics and Compliance

Regulatory bodies are increasingly treating platform data as an essential, non-substitutable facility. Authorities in jurisdictions ranging from the EU to Mainland China are penalizing orchestrators for data monopolization and the imposition of exclusive dealing conditions 505255. A landmark case in China's financial data sector (the Sumscope case) signals a growing regulatory consensus that proprietary data pools cannot be universally restricted to force complementary market lock-in 55.

Consequently, the strategic calculus for ecosystem orchestrators is changing. Platform leaders must navigate a landscape where aggressive data hoarding and the forced integration of adjacent services may trigger severe regulatory intervention, forcing a recalibration of how data moats are leveraged to sustain competitive advantage 515356. The long-term efficacy of these regulatory frameworks remains subject to ongoing debate and judicial review, but they clearly signal an end to the era of unchecked platform expansion.