Regulatory disruption and conditions for disruptive innovation

Regulatory disruption occurs at the complex intersection where rapid technological advancement challenges existing legal frameworks, forcing policymakers to either adapt legacy rules, construct new governance paradigms, or enforce restrictive measures. The interplay between regulation and innovation is not strictly adversarial. Policy choices can unilaterally create the foundational conditions necessary for new markets to emerge, or they can systematically dismantle the commercial viability of disruptive business models. The role of regulatory disruption encompasses the imposition of compliance burdens, the structuring of market entry, the protection of incumbent industries, and the facilitation of novel ecosystems through targeted institutional mechanisms.

Conceptual Frameworks of Regulatory Disruption

The term regulatory disruption refers to scenarios where a new product, technology, or business practice falls within a government agency's jurisdiction but fundamentally misaligns with the agency's existing regulatory architecture 1. This structural mismatch creates friction between innovators seeking rapid deployment and regulatory bodies mandated to protect the public interest, market stability, and consumer safety.

Agency Threats and Institutional Mismatch

Legal and economic scholars observe that regulatory agencies confronting disruptive innovations face a persistent dilemma. Regulating prematurely risks stifling nascent technology, while regulating too late invites systemic harm and uncontrolled externalities 1. To navigate this uncertainty, regulators frequently rely on "agency threats," which are packaged as guidance documents, warning letters, and policy statements, rather than engaging in traditional, binding rulemaking and adjudication 1. While this posture provides initial flexibility, empirical observations suggest that tentative regulatory postures can calcify into weak defaults, leading to suboptimal long-term regulation. Historical comparisons, such as the United States Food and Drug Administration's initial approach to computerized medical devices versus the Federal Communications Commission's early treatment of the internet, demonstrate that regulatory inertia is often only broken by an external shock or market failure 1.

Conversely, some legal scholars caution against viewing regulatory disruption purely as technological advancement evading government oversight. Critiques of the disruption narrative argue that associating digital innovation with unregulated chaos obscures the complex systems of order that technology creates 2. Furthermore, characterizing administrative systems as inherently brittle discounts the observed resilience of federal agencies, which frequently adapt to digital threats by propagating influence beyond the confines of notice-and-comment rulemaking 2. At a structural level, institutional disruption occurs when the reconfiguration of legal institutions to handle technological problems raises systemic issues regarding authority, competence, and democratic legitimacy 3.

The Precautionary Principle and Permissionless Innovation

The global regulatory landscape is broadly divided by two competing philosophical paradigms regarding technological deployment: the precautionary principle and permissionless innovation.

The precautionary principle dictates that new innovations must be curtailed or explicitly disallowed until their creators can verify the absence of theoretical harm to individuals, environments, or societal norms 456. Prominent in the European Union, this upstream governance prioritizes risk elimination over risk management 67. While praised for ethical foresight, stringent application often results in high compliance barriers. For example, Europe's strict risk classifications under the 2024 Artificial Intelligence Act impose significant costs that predominantly favor large, well-capitalized corporations over resource-constrained startups 7. Critics argue this approach relies on anticipating worst-case hypotheticals, which inherently suppresses best-case innovation scenarios and drives talent and capital toward more permissive jurisdictions 568. The resulting regulatory environment often limits the development of homegrown technology firms, requiring the region to rely on exporting its technocratic mandates globally 6.

In contrast, permissionless innovation posits that experimentation with new technologies and business models should be permitted by default, with regulatory intervention reserved for instances where concrete harm can be demonstrated 4678. Historically embraced by the United States during the commercialization of the internet in the 1990s, this laissez-faire approach minimizes regulatory burdens on startups and relies on market forces and ex post regulatory instruments to address externalities 479. Economic models suggest that ex post liability regimes often outperform ex ante restrictions in scenarios involving high uncertainty about potential harms, particularly for emerging technologies like artificial intelligence 9. However, market forces left entirely unguided may lead to distortions in the direction of technological change, sometimes promoting insufficient diversity in scientific effort across alternative technological paths 9.

The Economics of Regulatory Compliance

A critical vector through which regulation impacts innovation is the imposition of compliance costs, which act as structural barriers to entry and operational scaling. Measuring the precise economic cost of regulation borne directly by producers remains complex, but quantitative analyses provide insight into the financial drag created by compliance mandates.

Labor Costs and Economies of Scale

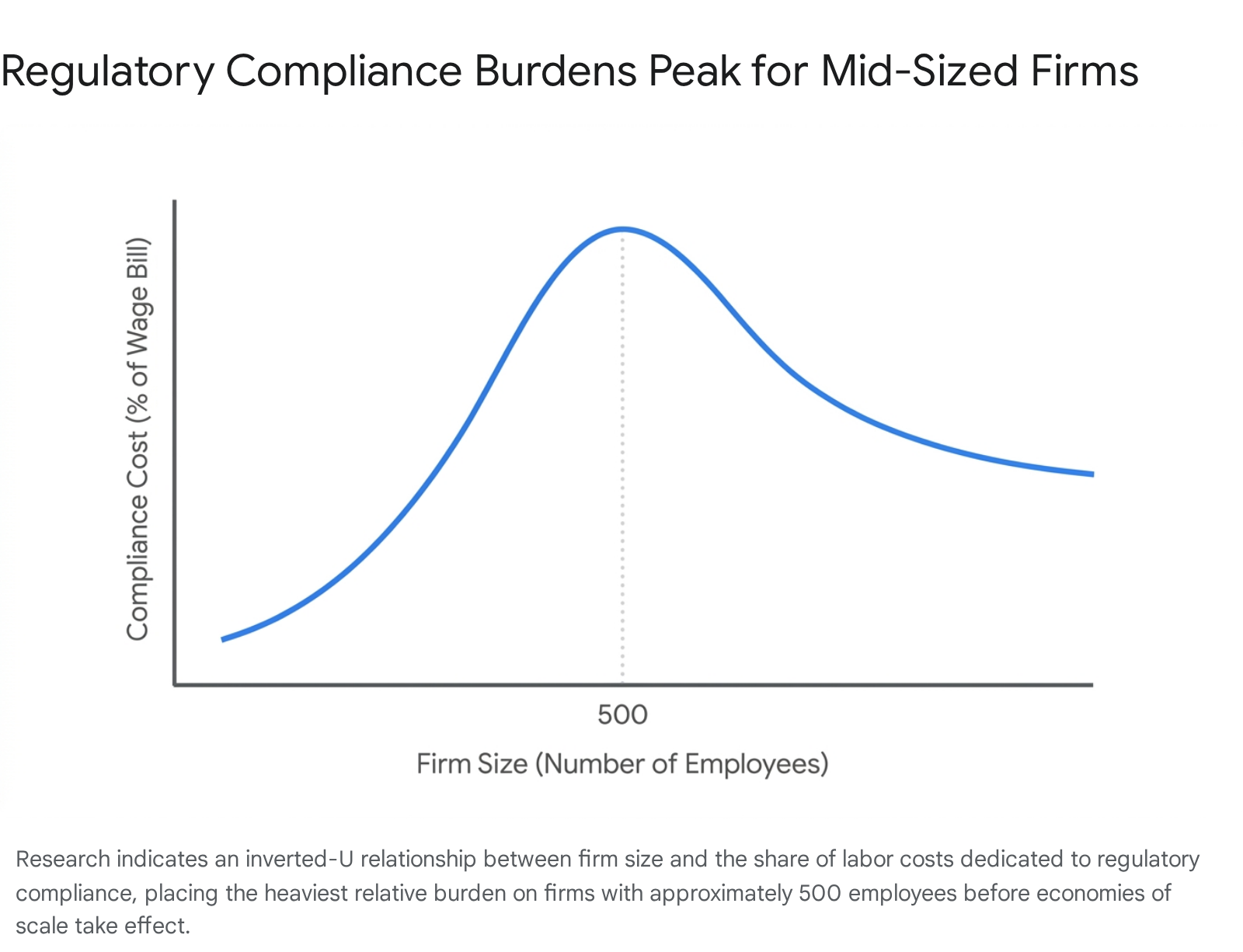

Empirical research combining data on occupational tasks and corporate wage spending indicates that the average United States firm spends between 1.3 percent and 3.3 percent of its total wage bill strictly on regulatory compliance 101112. From 2002 to 2014, these real regulatory compliance costs grew by approximately 1 percent annually 1012. This labor burden varies significantly by sector; for instance, transit and ground transportation dedicate 3.9 percent of labor spending to compliance, while chemical manufacturing dedicates 2.3 percent 11.

Crucially, the burden of regulatory compliance does not scale linearly, creating distinct disadvantages based on firm size. Research reveals an inverted-U relationship between compliance labor costs and firm size 1112. Firms with fewer than 500 employees experience increasing compliance costs as a share of total wages, with the percentage of labor spending sharply increasing as employment grows toward that threshold. However, once a firm surpasses the 500-employee mark, economies of scale take effect, and the percentage of labor spending dedicated to compliance progressively decreases 1011. On average, the compliance burden for midsize firms is roughly 47 percent greater than that of the smallest firms and 18 percent greater than that of the largest enterprises 10.

These compliance structures that feature non-neutral returns to scale distort incentives for producers, induce resource misallocation, and constrain productivity growth 1012. When regulatory costs increase with size up to a certain point, it incentivizes firms to remain small and operate below the efficient scale of production 10. Furthermore, these labor cost estimates do not account for capital expenditure costs, lost profits created by compliance risk, or outsourced compliance costs such as external accounting services, which represent an additional 2.8 percent to 8.7 percent of total compliance costs depending on the sector 1112.

Tax Complexity and Direct Expenditures

In addition to labor costs, tax compliance represents a massive drain on corporate resources. The United States tax code requires an estimated 7.9 billion hours of compliance effort annually, translating to an aggregate cost of $413 billion in labor and $133 billion in out-of-pocket expenses, representing almost 2 percent of the national gross domestic product 13. Business income tax compliance alone accounts for nearly $119 billion of this total, with quarterly tax filings and depreciation schedules costing businesses an additional $70 billion annually 13.

Survey data indicates that corporations dedicate substantial funds to outside tax assistance, averaging $10.2 million per company 13. For these expenditures, 51 percent is allocated to foreign income tax compliance, 37 percent to federal income tax compliance, and the remainder to state and local compliance 13. Corporate sentiment points to international rules, including the Tax Cuts and Jobs Act (TCJA) reforms, the new corporate alternative minimum tax enacted under the Inflation Reduction Act, and the OECD's Pillar Two rules, as primary drivers of increasing complexity 13. These asymmetric and compounding burdens divert venture capital and operational revenue away from product innovation toward legal and administrative overhead.

Regulatory Uncertainty and Capital Formation

While the strictness of regulation presents a known variable that markets can price into their financial models, regulatory uncertainty is far more disruptive to innovation than regulation itself 14. Uncertainty discourages irreversible investment, increases perceived risk, and encourages a wait-and-see approach among capital allocators 14. When future policy conditions are difficult to predict, firms often scale back long-term investment, even if the immediate regulatory burden is not exceptionally high 14. Evidence suggests that uncertainty over rules and enforcement shifts corporate focus from innovating radical new products toward more incremental product improvements 14.

Venture Capital Allocation in Artificial Intelligence

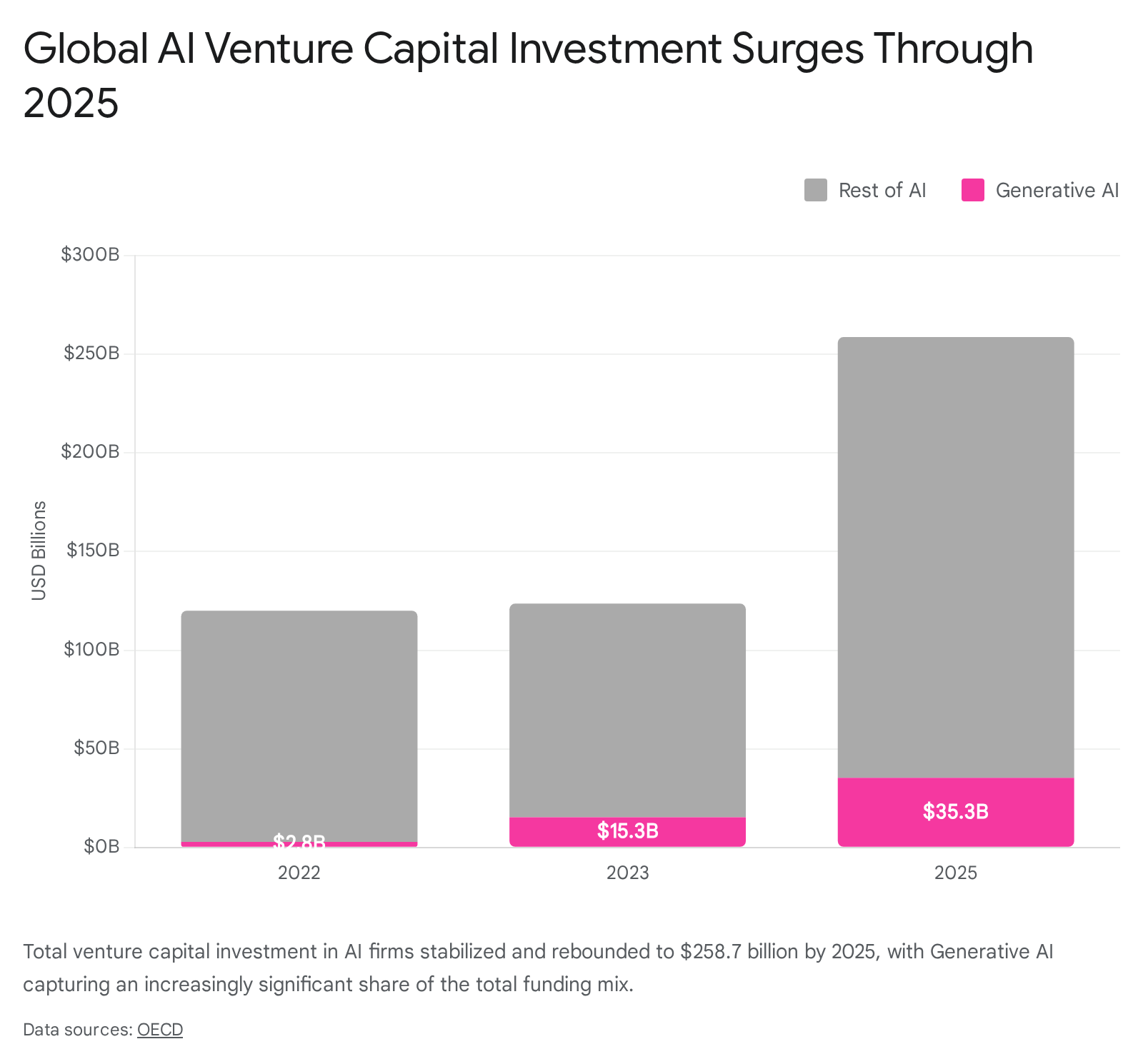

The rapid evolution of artificial intelligence has significantly outpaced global regulatory frameworks, creating an unpredictable environment for venture capital. Governments worldwide are attempting to address issues such as data privacy, algorithmic bias, and security risks, leading to a fragmented landscape of policies and pending legislation 1516. Despite this regulatory ambiguity, artificial intelligence remains the dominant force in global venture funding. In 2025, venture capital investments in AI firms reached $258.7 billion, representing 61 percent of all global venture capital investment, double its 30 percent share in 2022 17. Generative AI specifically surged to $35.3 billion in 2025, accounting for 14 percent of all AI funding 17.

United States firms attract the largest share, capturing 75 percent ($194 billion) of global AI venture capital deal value 17. A significant portion of this capital is heavily concentrated in IT infrastructure and hosting, drawing $109.3 billion in 2025 alone, reflecting a massive rush to build the compute infrastructure critical to scaling advanced systems 17.

Despite this influx of capital, regulatory environments are increasingly fracturing, which complicates long-term scaling strategies for developers. The European Union AI Act, which took effect in August 2024, establishes a stringent framework classifying AI tools into four risk tiers: unacceptable, high, limited, and minimal 1518. Generative AI models deemed high-risk face severe transparency, human oversight, and governance compliance burdens 15. Because retraining large language models for distinct regional compliance is economically and computationally impractical, the EU AI Act serves as a de facto global standard, driving up development costs and disproportionately affecting early-stage startups that lack extensive legal resources 15.

Conversely, the United States remains fragmented, relying on a patchwork of state privacy laws and voluntary federal guidelines 1518. This lack of federal preemption complicates compliance, as developers navigate contradictory rules regarding algorithmic bias, training data copyright, and liability for AI-generated outputs 1516. The threat of regulatory overreach has led to venture capital adopting more disciplined investment approaches, prioritizing companies with solid fundamentals and verifiable compliance strategies 16.

Global Divides and the Emergence of Small Artificial Intelligence

Regulatory capacity and infrastructure readiness dictate how different global populations experience and adopt artificial intelligence. Data indicates a stark divide between high-income and low-income nations. While 24 percent of internet users in high-income countries use applications like ChatGPT, penetration drops to 5.8 percent in upper-middle-income countries, 4.7 percent in lower-middle-income countries, and just 0.7 percent in low-income countries 19. Regression analysis confirms that gross domestic product per capita strongly predicts adoption growth, revealing deepening global inequality in technological access 19.

The World Bank identifies four foundational elements - connectivity, compute, context (data), and competency (skills) - as the bedrock of inclusive AI ecosystems 20. Developing nations face significant deficits in these areas, exacerbated by brain drain where talent outflows are three to four times higher than inflows in countries like Bangladesh, Lebanon, Nigeria, and Ukraine 21.

However, a parallel innovation vector is emerging out of necessity. Low- and middle-income countries are actively adopting "Small AI" solutions 2021. These approaches prioritize affordable, accessible, and highly localized applications designed to run on everyday devices with limited computational overhead, such as mobile phones 2021. Small AI is currently transforming development-relevant sectors like agriculture, education, and health at the community level, allowing emerging economies to leapfrog traditional infrastructural barriers despite a lack of comprehensive national regulatory frameworks for advanced generative models 21. Furthermore, demographic sentiment reveals a reversal of advanced economy trends: generative AI evokes stronger optimism and trust among the youth and populations in emerging economies, whereas advanced economy respondents express greater hesitation and skepticism 22.

Digital Asset Classification and Jurisdictional Ambiguity

The digital asset and decentralized finance sectors offer a stark case study in the consequences of jurisdictional overlap and regulatory uncertainty. In the United States, the Securities and Exchange Commission and the Commodity Futures Trading Commission have historically engaged in jurisdictional disputes over crypto-assets 2324. The SEC's reliance on the 1946 Howey Test to classify most cryptocurrencies as investment contracts has resulted in regulation by enforcement, significantly impacting market dynamics 2526. Empirical event studies demonstrate that when the SEC explicitly names a crypto asset as a security, returns plunge by an average of 12 percent over the following week, accompanied by ex-ante trading volume anomalies indicative of pre-announcement informed trading 25.

In early 2026, the SEC and CFTC issued joint interpretive guidance to clarify the taxonomy of digital assets, categorizing them into digital commodities, digital collectibles, digital tools, stablecoins, and digital securities 242728. This guidance confirms that a crypto asset is not inherently a security; rather, the investment contract arises from the transaction and the specific promises made by the issuer to investors 2428. While this interpretation removes a major gray area by placing most assets under CFTC oversight, the guidance does not carry the weight of formal rulemaking 2427. The industry continues to lobby for legislation that would officially shift spot market oversight to the CFTC, seeking structural certainty over interpretive relief 26.

Simultaneously, the European Union implemented the Markets in Crypto-Assets regulation, which became fully applicable to crypto-asset service providers in December 2024, following an earlier rollout for asset-referenced tokens and e-money tokens 232930. While the regulation provides uniform rules and EU-wide passporting rights, it fundamentally assumes the existence of a centralized issuer or legal entity 3031. This requirement creates an existential crisis for true decentralized finance protocols, which are governed by automated smart contracts and decentralized autonomous organizations without an identifiable corporate nexus 31. By requiring a well-defined organizational structure and concrete lines of responsibility, the regulation risks excluding automated structures from the European market entirely, demonstrating how legislation tailored for traditional finance can inadvertently outlaw decentralized innovation 31. The transition phase, which permits existing operators to function while seeking authorization, varies by member state and concludes entirely by July 2026, at which point the full implications for decentralized entities will manifest 23.

Policy Frameworks as Market Creators

Regulation is not solely an inhibitor of technology; affirmative policy mandates can forcefully create entirely new markets, establish interoperable standards, or compel the restructuring of legacy industries.

Open Banking and Financial Data Portability

Open banking policies represent a deliberate regulatory attempt to disrupt the data monopolies historically held by incumbent financial institutions. By mandating that banks share customer transaction data with authorized third-party providers via standardized Application Programming Interfaces, regulators aim to lower switching costs, foster financial technology innovation, and increase competition in retail banking 323334. Research confirms that open banking significantly improves the performance of new financial entrants on both extensive (quantity of users) and intensive (quality of service) margins 32. Furthermore, highly exposed incumbent banks are compelled to adapt, often experiencing declines in traditional loan issuance while shifting their reliance toward fee-based revenue and operational efficiency 32.

The implementation and regulatory philosophy of open banking differ starkly across global jurisdictions.

| Feature | European Union and United Kingdom | United States |

|---|---|---|

| Regulatory Approach | Regulatory-driven mandate. Implemented via the Revised Payment Services Directive and subsequent iterations 3335. | Initially market-driven via industry bodies, currently transitioning to regulatory oversight under the Consumer Financial Protection Bureau 353637. |

| Standardization | Highly standardized application programming interfaces required by law across all member states 35. | Fragmented technical standards; proposed federal rules attempt to establish uniform data sharing protocols 3537. |

| Market Penetration | Structured and secure, but slower initial consumer adoption (e.g., 15.1 million users in the United Kingdom) 3235. | Massive organic adoption (over 114 million connections) driven by consumer demand for specific applications 3536. |

| Incumbent Resistance | Addressed early in the legislative process; banks were statutorily compelled to comply 3335. | High resistance. Major banking institutes sued to block federal rules, resulting in judicial injunctions 373839. |

In the United States, the transition from unsecure "screen scraping" to secure application programming interface data sharing under the Consumer Financial Protection Bureau's Section 1033 rule has sparked fierce litigation 39. Banking trade groups successfully obtained a federal injunction in late 2025, arguing the rule imposes heavy compliance costs, forces institutions to provide data without charging corresponding fees, and fails to adequately address cybersecurity liability when third-party applications suffer data breaches 36373839.

Banking-as-a-Service and Ecosystem Fragility

The evolution of open banking data portability into the functional execution of Banking-as-a-Service introduces profound new systemic risks. This modularization breaks down core banking functions - such as account opening, payments, compliance checks, and lending - and delivers them separately through application programming interfaces 33. This structure allows consumer-facing applications to plug directly into the financial system, offering debit cards and deposit accounts without holding a banking license themselves, relying instead on a sponsor bank 33.

While this creates massive efficiencies and accelerates product deployment, it constructs hidden dependencies within the financial ecosystem. The 2024 bankruptcy of Synapse Financial Technologies, a prominent middleware provider, revealed the structural vulnerability of this arrangement 33. When the intermediary collapsed, the linkage between the underlying sponsor banks and the consumer-facing applications broke, resulting in thousands of end-consumers losing immediate access to their funds 33. This event exposed a critical regulatory gap regarding the supervision of technology providers that sit between regulated banks and end-users, highlighting that while data sharing drives competition, the sharing of core banking functions requires robust prudential oversight 33.

Digital Public Infrastructure in Emerging Markets

While Western nations focus on open banking regulations aimed at opening up legacy private-sector data, emerging economies - led by India - have pioneered Digital Public Infrastructure to digitally leapfrog traditional systems entirely. The "India Stack" relies on government-backed, open application programming interfaces functioning as foundational public goods 37414238.

This infrastructure operates across layered protocols: identity (the Aadhaar biometric system), payments (the Unified Payments Interface), and data empowerment (the Data Empowerment and Protection Architecture) 373844. By providing population-scale digital identity - facilitating over 67 billion verifications - and a real-time payments interface processing 14.05 trillion rupees monthly, the state drastically lowered the cost of customer acquisition for private innovators 42. The cost of executing formal Know-Your-Customer compliance processes fell from approximately $23 to $0.15 42.

Consequently, adult bank account ownership in India surged from 35 percent in 2011 to 77.5 percent by 2021 38. The integration of artificial intelligence with these national digital systems is further modernizing governance, unlocking capabilities in predictive service delivery and dynamic resource allocation 44. The success of this model indicates that state-sponsored digital infrastructure, when designed for interoperability and scale, can catalyze unprecedented private-sector innovation while achieving broad social policy goals like financial inclusion 3741.

Environmental Policy and the Green Technology Sector

Climate policy, emissions standards, and environmental reporting mandates are aggressively reshaping both industrial hardware development and digital financial markets, demonstrating how regulatory targets can manifest as vast commercial opportunities.

Emissions Standards and Industrial Reconfiguration

Government intervention is driving the global transition toward sustainable mobility and energy infrastructure. The United States Inflation Reduction Act utilized direct production subsidies to aggressively engineer a domestic electric vehicle and battery manufacturing supply chain 4539. Economic analysis of the domestic electric vehicle incentive program revealed that it generated $1.87 of societal benefits per dollar spent in 2023 when compared to pre-existing incentive structures 39. This calculation factors in the reduction of carbon dioxide emissions, local air pollution, and the fiscal externalities related to taxation 39.

However, regulatory design significantly impacts market efficiency. Analysis indicates that the optimal one-size-fits-all subsidy would be $6,355, slightly lower than the implemented $7,500 credit 39. Furthermore, shifting from uniform subsidies to vehicle-specific subsidies based on weight and efficiency could yield an additional $2.5 billion in annual net social benefits 39. The impact of regulatory loopholes was also evident; provisions allowing commercial leasing to bypass strict domestic-content requirements caused the share of leased electric vehicles to jump from 15 percent to 30 percent between December 2022 and December 2023 39. Globally, policy support and tougher emissions standards in the United States and the European Union are projected to increase the stock of electric buses sevenfold and electric trucks thirtyfold by 2035, necessitating a massive corresponding expansion in charging infrastructure and electrical grid capacity 47.

Green Financial Technology and Compliance Markets

Concurrently, financial regulations are forcing corporate accountability, giving rise to the "Green Fintech" sector. Policies such as the European Green Deal and the Sustainable Finance Disclosures Regulation force companies to explicitly disclose the environmental impacts of their business operations and investment portfolios 4049. This regulatory pressure has created a structural demand for accurate, verifiable environmental, social, and governance data reporting.

Startups are deploying novel technologies to service this compliance requirement. Innovations include utilizing blockchain ledgers for carbon credit verification and trading, applying artificial intelligence to climate risk analysis, and integrating application programming interfaces to embed climate-focused products directly into financial services 404950. Specific market applications include carbon-neutral payment processing methods that automatically offset emissions through renewable energy projects, and advanced software platforms designed for enterprise carbon emission data management across manufacturing supply chains 4950. The influx of capital into this sector is pronounced; European climate-focused startups raised $1.4 billion compared to $881 million in the United States, illustrating the direct correlation between stringent regional environmental regulation and specialized venture capital deployment 49.

Regulatory Capture and Incumbent Preservation

The theory of regulatory capture posits that regulations are frequently acquired by the incumbent industry and designed to operate primarily for its benefit, utilizing the coercive power of the state to establish rules that extract private rents or block new market entrants 415242. This phenomenon presents a persistent barrier to disruptive innovation, as established entities mobilize immense lobbying resources to shape the regulatory landscape to their advantage.

Distributed Energy Resources and Utility Monopolies

A modern manifestation of regulatory capture is evident in the ongoing conflict between investor-owned utilities and the distributed solar industry, particularly in California. Historically, the state's Net Energy Metering policy allowed homeowners to sell excess rooftop solar energy back to the electrical grid at retail rates, driving massive adoption and facilitating nearly 2 million rooftop installations 5455. However, monopoly utility companies argued this framework created an $8 billion cost-shift onto non-solar ratepayers who ostensibly bear the fixed costs of grid maintenance and transmission infrastructure 54.

In 2023, the California Public Utilities Commission enacted a new billing structure that slashed the export rates paid to rooftop solar customers by 75 percent 5455. This policy shift destroyed the immediate economic incentive for residential solar installations, triggering an 80 percent collapse in new market volume and resulting in the loss of 17,000 industry jobs within a year 5557. Environmental and consumer advocates sued the regulatory commission, arguing that the rulemaking violated state climate laws and failed to properly evaluate the benefits of distributed solar - such as localized grid resilience and avoided transmission infrastructure costs 545557. Independent analysis refuted the utilities' claims, suggesting that rooftop solar actually provided a $1.5 billion cost savings to the grid in 2024 54. Former regulatory officials publicly characterized the decision as an example of regulatory capture, noting that utilities utilize regulatory frameworks to systematically block decentralized energy generation that threatens their guaranteed rates of return on centralized capital infrastructure projects 5558.

Incumbent Resistance in the Platform Economy

Incumbent industries routinely utilize local regulators to execute blocking strategies against disruptive platform technologies. In the case of ride-sharing platforms disrupting municipal taxi cartels, empirical research identifies two primary regulatory responses: blocking, which involves enforcing existing licensing requirements and outright bans, and incorporating, which involves modifying regulations to align with the new technology's operational realities 43.

Innovators successfully overcome blocking mechanisms by employing "venue shifting" strategies. This involves moving the regulatory battle from hostile, highly captured local commissions to more favorable state legislatures (vertical shifting) or to distinct regulatory bodies (horizontal shifting) 43. By elevating the jurisdiction, disruptive firms bypass captured local entities, demonstrating that regulatory strategy is as critical to market entry as the underlying technological innovation itself.

Institutional Mechanisms for Innovation Facilitation

Recognizing the friction between outdated rules and rapid technological advancement, progressive regulators have developed specific institutional mechanisms to facilitate deployment without compromising systemic safety or consumer protection.

The Regulatory Sandbox Model

Regulatory sandboxes allow firms to test innovative products and services in a live, controlled market environment under the direct supervision of regulatory authorities 444546. By providing a structured framework for experimentation, sandboxes reduce regulatory uncertainty and act as a powerful quality signal to the market. Empirical evidence from the United Kingdom's Financial Conduct Authority sandbox reveals that participating financial technology firms experience a 15 percent higher probability of securing subsequent venture capital funding and demonstrate greater overall survival rates compared to non-participating peers 4748.

Sandbox designs and objectives vary significantly based on national economic priorities and regulatory maturity.

| Jurisdiction | Lead Regulator | Target Focus and Sandbox Design Features |

|---|---|---|

| United Kingdom | Financial Conduct Authority | Focuses on genuine innovation and consumer benefit. Operates year-round, requiring a clear need for supervisory support. Does not offer blanket exemptions but significantly reduces time-to-market. Recently announced a specialized sandbox for artificial intelligence services 6549. |

| Singapore | Monetary Authority of Singapore | Focuses on efficiency and financial inclusion. Utilizes a tiered approach: Sandbox Express provides a 21-day fast-track for low-risk models, Bespoke addresses complex models, and Sandbox Plus offers financial grants up to S$400,000 65. |

| Nigeria | Central Bank of Nigeria | Focuses heavily on payments innovation and economic inclusivity. Operates on annual cohorts with a strict six-month maximum testing duration. Uniquely open to non-bank entities, including telecommunications firms 65. |

| Brazil | National Data Protection Authority | Specialized focus on artificial intelligence and data protection. Currently in design to test generative AI transparency mechanisms, specifically to inform upcoming national legislative debates 50. |

| India | Multi-Agency (Reserve Bank of India, Securities and Exchange Board of India, etc.) | Focuses on broad financial inclusion. Operates via distinct frameworks across multiple regulators. Challenges remain regarding inter-regulatory coordination and stringent data localization mandates 686951. |

While highly effective in mature ecosystems with unified regulatory bodies like the United Kingdom and Singapore, sandboxes in emerging markets often require alignment with broader digital infrastructure and proactive coordination across multiple sectoral regulators to avoid creating fragmented, isolated successes 486851.

Privacy-Enhancing Technologies in Regulated Data Environments

In jurisdictions characterized by strict data protection laws, such as the European Union under the General Data Protection Regulation, technological innovation itself is becoming a critical regulatory compliance tool. Privacy-Enhancing Technologies - including homomorphic encryption, zero-knowledge proofs, and secure multi-party computation - allow entities to extract analytical value from datasets without exposing underlying personally identifiable information 715253.

Driven by the threat of severe regulatory penalties (the European Union issued €2.1 billion in fines in 2024 alone), the market for these technologies is expanding rapidly, projected to reach $12.26 billion by 2030 7154. Surveys indicate that 92 percent of European data organizations use some form of privacy-enhancing technique for compliance 52. The adoption of these tools is accelerating as major hardware manufacturers embed confidential computing capabilities directly into silicon, allowing developers to ensure data privacy at the edge and IoT nodes 71. However, regulatory rigidity remains a bottleneck to full utilization. Even when advanced technologies guarantee mathematical data confidentiality, regulators sometimes continue to demand cumbersome user consent processes, which can neutralize the commercial incentive to innovate privacy-first architectures 52.

Mobile Money Regulation and Financial Inclusion

The development of mobile money across the African continent demonstrates how slight variations in regulatory architecture dictate market outcomes and financial inclusion rates. In East Africa, particularly Kenya, financial regulators permitted a "telecom-led" model, allowing mobile network operators to issue electronic money and manage extensive agent networks without requiring users to open a formal account at a traditional financial institution 7576. This permissionless approach to telecommunications financial services resulted in explosive growth, with platforms processing transaction values equivalent to nearly half of the national gross domestic product 76.

Conversely, the West African Economic and Monetary Union initially mandated a strict "bank-led" model. This framework strictly separated e-money issuers, which had to be prudentially supervised banks, from e-money distributors, limiting mobile network operators to a distribution role 75. This requirement created severe market friction, resulting in highly variable and generally lower mobile money adoption across West Africa compared to the East African telecom-led environments 7577. When jurisdictions revise these guidelines - as Ghana did by permitting mobile network operators to directly offer accounts - the share of adults with mobile money accounts can increase exponentially, demonstrating that an enabling regulatory framework is the primary catalyst for sustainable financial inclusion 55.

State-Directed Industrial Policy and Market Rectification

The ultimate demonstration of regulatory disruption occurs when the state actively intervenes to dismantle thriving commercial sectors in order to realign private capital with national strategic priorities.

Intervention and Capital Reallocation in the Chinese Technology Sector

From late 2020 through 2022, the Chinese government initiated an unprecedented, sweeping regulatory crackdown on its domestic consumer internet, platform economy, and private education sectors 5657. Driven by concerns over systemic financial risk, data security, anti-monopoly practices, and the socio-economic impacts of exorbitant private tutoring costs, regulators executed a series of abrupt interventions 578158. The state halted major public offerings, levied multi-billion dollar fines against dominant e-commerce and social media platforms, and barred the $100 million education technology industry from operating as for-profit entities, sending share prices plummeting by over 80 percent practically overnight 578158.

The immediate financial impact of this rectification campaign was devastating to the targeted sectors. The total market capitalization of Chinese internet companies shrank from a peak of $2.5 trillion in 2020 to $1.4 trillion in 2022, and venture capital investment into the Chinese consumer internet plummeted by 80 percent, falling from $49 billion to just $10 billion 56. Sudden regulatory announcements, such as draft rules aimed at curbing excessive gaming, caused panic sell-offs that wiped out tens of billions in market value in mere hours, severely eroding trust in state-business relations among foreign investors 56.

However, this intervention was not a rejection of technology, but a deliberate, state-directed forced reallocation of capital. While consumer software platforms and the sharing economy were penalized, venture capital investment into Chinese "hard tech" sectors - such as semiconductors, robotics, artificial intelligence, and advanced manufacturing - reached record highs during the same period 8159. The regulatory assault successfully redirected financial and human capital away from what the state viewed as rent-seeking platform monopolies toward core technologies deemed critical for national self-sufficiency and geopolitical competitiveness under the government's techno-nationalist five-year plans 5859.

The Transition to Normalized Supervision

Today, the regulatory environment in China has evolved from abrupt, campaign-style crackdowns to "normalized supervision" 8159. While the era of rapid, unregulated expansion is definitively over, the operating environment for technology giants is now governed by stringent, institutionalized frameworks like the Personal Information Protection Law and the Data Security Law 8159. This new paradigm ensures that technology firms prioritize long-term stability and operate fundamentally as implementers of state policy, aligning their corporate strategies with broader governmental objectives 8159. Companies that efficiently adapt to this new reality and align with state goals demonstrate that robust growth is still possible within highly controlled regulatory paradigms, provided their innovations serve the prescribed national interest 81.