Artificial Intelligence and the Christensen Disruption Model

The discourse surrounding artificial intelligence (AI), particularly generative AI, is heavily saturated with assertions of its disruptive nature. Industry analyses, corporate declarations, and academic forecasts frequently describe AI as a force capable of upending established markets. However, measuring these claims against formal economic and business frameworks requires a rigorous application of terminology. The Christensen theory of disruptive innovation provides a specific, historically validated mechanism for understanding how market leaders collapse and how new entrants succeed. Evaluating the current state of AI research through this lens reveals a complex landscape: while AI exhibits certain classical patterns of disruption, its immense capital requirements, reliance on incumbent data ecosystems, and its role as a general-purpose technology cause it to systematically break several foundational assumptions of the Christensen model.

Foundations of the Christensen Disruption Model

To assess whether a technology acts as a disruptive force, it is necessary to establish the parameters of the framework popularized by Clayton Christensen in the 1990s. The theory posits that the failure of well-managed companies is rarely due to a lack of technological competence or foresight. Rather, failure occurs because incumbents logically prioritize their most profitable customers, inadvertently creating vulnerabilities at the market's lower tiers 123.

Defining Sustaining Innovations

A sustaining innovation improves existing products or services along dimensions historically valued by mainstream customers. These innovations can be incremental or radical, but their defining characteristic is that they reinforce the current trajectory of competition 3. Incumbent firms almost invariably win the battles of sustaining innovation because they possess the resources, customer relationships, and financial incentives to develop better products for their most demanding clients. When a new technology allows an enterprise software provider to process data faster or enables an automaker to produce a more fuel-efficient engine, it functions as a sustaining innovation 2.

The Mechanics of Low-End Market Footholds

Disruption, by contrast, is not a product or a technology, but a specific competitive trajectory. Disruptive innovations typically enter the market through two distinct pathways. The first is a low-end foothold, where a business model targets customers who are overserved by existing products. These customers do not require, and are unwilling to pay for, continuous high-end improvements. A disruptor provides a "good enough" product at a significantly lower cost. Incumbents, motivated by profit margins, willingly abandon these lower tiers to focus on high-margin segments 12.

Historical case studies illustrate this pattern with clarity. In the steel industry, mini-mills utilizing electric arc furnaces initially produced low-quality rebar, the lowest-margin product in the sector. Integrated steel mills, focused on profitability, ceded the rebar market 2. As mini-mill technology improved, entrants moved upmarket to produce angle iron, structural beams, and eventually high-margin sheet steel, leaving the incumbents with no remaining customer base 24.

The Mechanics of New-Market Footholds

The second pathway is a new-market foothold, which targets non-consumers - individuals or organizations that previously lacked the money or specialized skills to access a product. A classic example is the personal computer, which initially lacked the processing power of a mainframe but enabled entirely new populations to compute 25. Crucially, disruptive innovations initially underperform established products according to historical metrics. However, they are simpler, more convenient, or more accessible 34.

| Disruption Pathway | Target Audience | Value Proposition | Incumbent Response |

|---|---|---|---|

| Low-End Foothold | Overserved customers. | Cheaper, "good enough" functionality. | Willingly cedes market segment to protect high margins. |

| New-Market Foothold | Non-consumers. | Accessibility, simplicity, affordability. | Ignores the entrant, assuming the market is too small or unprofitable. |

| Sustaining Innovation | Existing, high-end customers. | Superior performance along established metrics. | Aggressively defends market share using superior resources. |

Generative Artificial Intelligence as a General-Purpose Technology

Before aligning AI with the Christensen framework, it is necessary to analyze the macroeconomic scale and speed of its adoption. Current research indicates that generative AI functions as a general-purpose technology (GPT), similar to electricity or the personal computer, characterized by broad applicability across diverse industries and a capacity to spur complementary innovations 678.

Macroeconomic Adoption Velocity

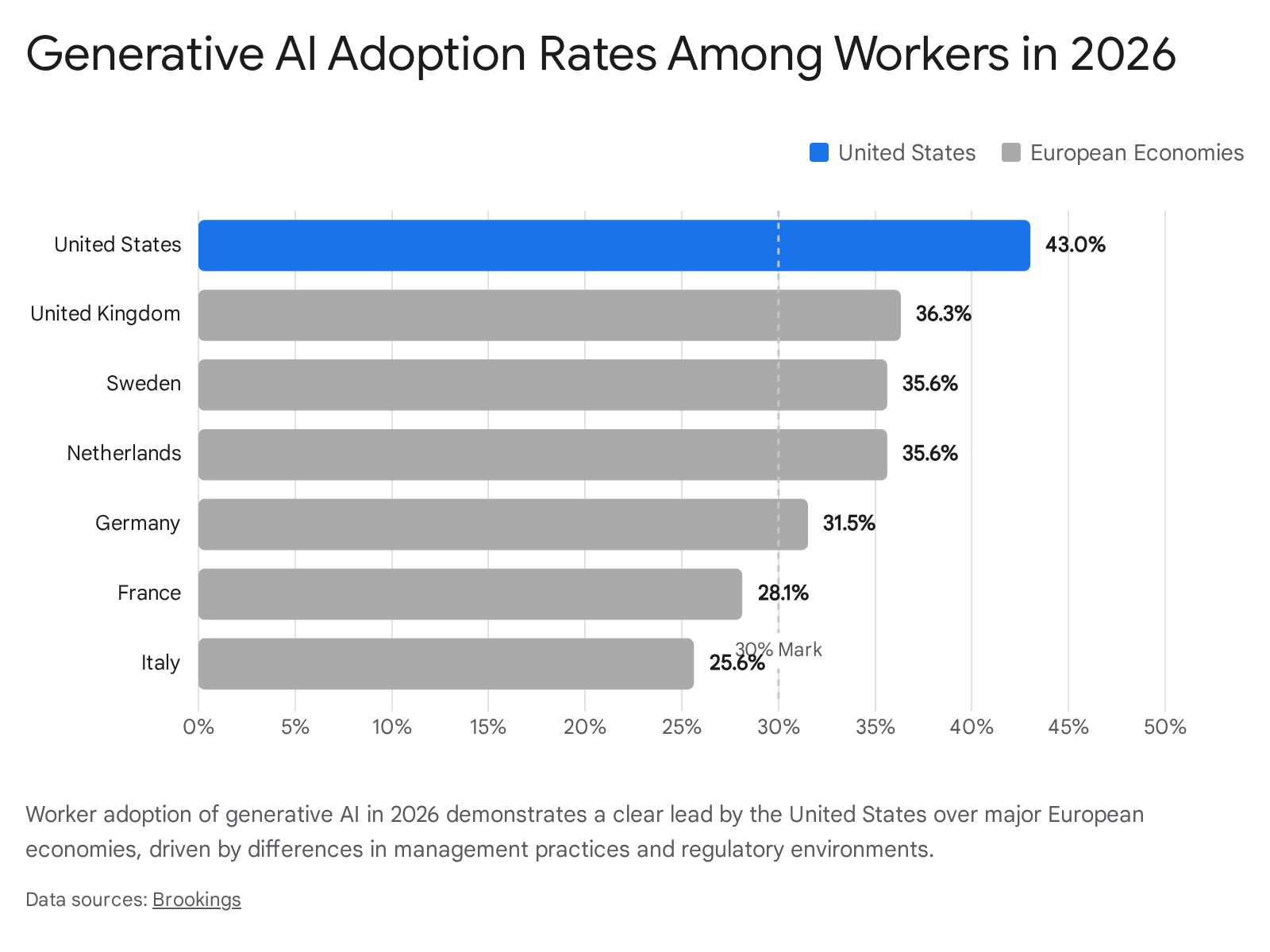

The adoption velocity of generative AI has outpaced prior technological revolutions. Nationally representative surveys conducted in the United States by the National Bureau of Economic Research (NBER) reveal that by August 2024, nearly 40% of the U.S. population aged 18 to 64 used generative AI 910. By 2026, the share of U.S. workers using AI in their jobs reached 43% 11. Relative to the first mass-market product launches of the personal computer and the internet, generative AI has achieved comparable workplace penetration in a fraction of the time. The internet achieved a 20% adoption rate after two years, whereas generative AI reached 39.5% in a similar timeframe 10.

Enterprise Spending and Market Capitalization

The financial commitments backing this adoption are staggering. According to Menlo Ventures, global enterprise spending on generative AI surged from $1.7 billion in 2023 to $37 billion by the end of 2025, capturing 6% of the global Software-as-a-Service (SaaS) market 12. This capital flow represents the fastest-scaling software category in history. The $37 billion expenditure in 2025 segmented into $18 billion dedicated to AI infrastructure (computing resources and model APIs) and $19 billion dedicated to application-layer products, including vertical, horizontal, and departmental AI software 12.

Aggregate Productivity and Labor Impacts

The economic implications of this adoption are measurable across both microeconomic tasks and aggregate productivity. Studies examining the deployment of generative AI in customer support roles demonstrated a 14% increase in agent productivity, measured by issues resolved per hour 13. Notably, unlike prior waves of computerization that disproportionately benefited high-skilled workers, generative AI currently yields the highest productivity gains for less-experienced and lower-skilled workers. The models effectively capture and disseminate the tacit knowledge of top performers, accelerating the learning curve for novices 1314.

At a macroeconomic level, NBER researchers estimate a potential aggregate productivity gain of 1.1% based on 2024 levels of generative AI usage 9. Between 1% and 5% of all U.S. work hours presently involve the direct assistance of generative AI, resulting in mean time savings of roughly 5.4% among active users, or 1.4% across the broader workforce 9. By 2026, aggregate time savings across both users and non-users were recorded at 2.3% of total hours in the United States, compared to 1.4% in Europe 11. Furthermore, organizational readiness heavily dictates the scale of these gains; European companies at an advanced stage of AI adoption reported productivity gains of 62%, compared to merely 40% for firms stuck at the basic adoption stage 15.

Challenges in Economic Measurement

Despite these early indicators, significant measurement gaps remain in tracking the true economic footprint of transformative AI. Current national accounting systems struggle to capture quality improvements and process changes driven by the technology. Output in service sectors - such as healthcare or software engineering - is often measured using cost or revenue data, which obscures enhancements in diagnostic accuracy or the speed of application delivery 7. As AI integrates into the production workflows of other industries, its "forward linkages" are poorly captured by traditional input-output frameworks, suggesting that current statistics may severely underrepresent AI's role in the global economy 7.

Theoretical Alignments with Disruption Dynamics

When evaluated against the strict criteria of Christensen's theory, generative AI exhibits several characteristics of a classic disruptive innovation, particularly in its initial stages of market entry and trajectory of improvement.

Democratization of Complex Tasks

Generative AI aligns with the "new-market foothold" mechanism by enabling non-consumers to perform tasks that previously required expensive specialists. In the realm of software development, early AI code generators produced simplistic and frequently flawed outputs 16. Established software engineering firms largely dismissed these tools as toys unsuitable for production-grade architecture, a textbook response from incumbents serving demanding, high-end clients 16.

However, for individuals lacking coding expertise - or small businesses lacking the capital to hire developers - these inferior outputs were immensely valuable. They represented an alternative to zero capability 2. The technology initially targeted the least demanding applications at the bottom of the market, offering solutions that were cheaper and more accessible, even if demonstrably inferior to human professional standards 16. To successfully push beyond rudimentary automation into true business transformation, organizations must achieve what researchers at the Wharton School term "evolutionary and revolutionary change," embedding AI structurally into risk, engineering, and customer engagement operations rather than merely relying on standalone tools 16.

Rapid Trajectories of Capability Improvement

Following the classical disruption pattern, AI technologies possess a steep trajectory of improvement. Driven by massive scale in compute and data, models quickly advance from handling rudimentary queries to executing complex, multi-step workflows. Features that historically required incumbents substantial time and resources to develop - such as natural language processing interfaces or predictive analytics engines - are increasingly available as commoditized, out-of-the-box application programming interfaces (APIs) 17.

As these models improve, they begin to encroach on the middle tiers of the market, handling tasks of increasing complexity and presenting a viable alternative to established professional services. This relentless upward movement is the defining vector of a disruptive threat, eventually closing the performance gap with incumbent solutions 3417. Kearney notes that use cases cross the "disruptive threshold" when they achieve superhuman scale, leverage predictably unstructured "super data," and facilitate a total redesign of workflows, rather than merely inserting AI into legacy processes 18.

Re-intermediation and Interface Control

Another alignment with disruption theory lies in how AI extracts value. Rather than displacing the incumbent's product directly, AI often disrupts the interface layer. Agentic AI assistants and copilots increasingly become the default method through which consumers search, compare, and execute decisions 20. In this scenario, an incumbent's underlying product may remain high-quality and relevant, but the incumbent loses pricing power and margin because an AI intermediary now controls customer access. This leads to commoditization and margin erosion, not through outright product obsolescence, but through the unbundling of value attribution 20.

Theoretical Divergences from the Classical Model

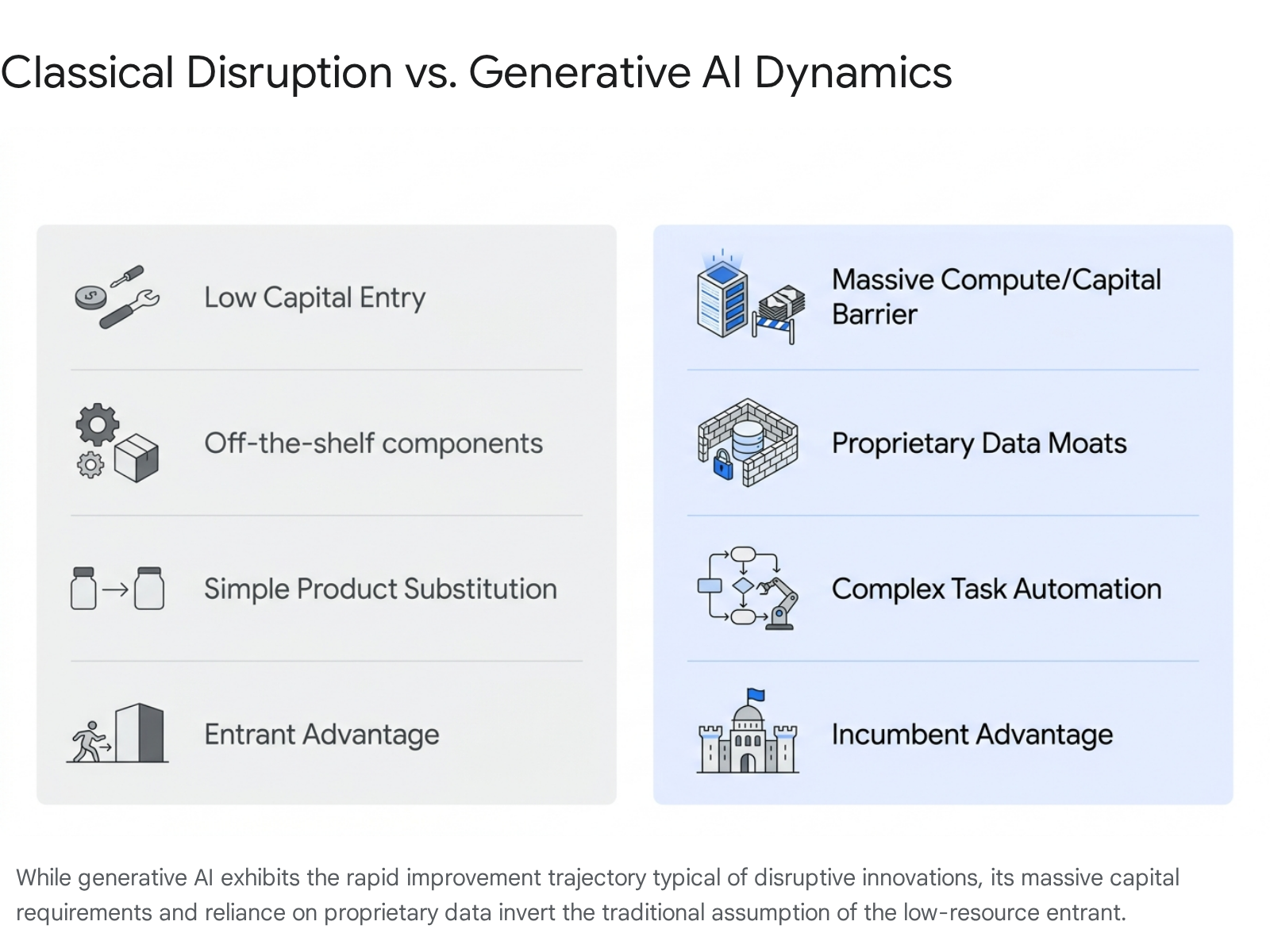

Despite the alignments noted above, generative AI fundamentally diverges from the traditional Christensen model in several critical dimensions. The theory historically assumes that disruptors are resource-constrained entrants leveraging low-cost business models to attack bloated incumbents. The structural economics of modern AI invert this paradigm entirely.

Capital Intensity and Infrastructure Barriers

The most significant departure from the classical model is the capital intensity required to develop foundational AI. Training frontier generative models requires enormous fixed costs, primarily in specialized semiconductor hardware (GPUs) and energy consumption 131419. In 2025 alone, enterprise spending on AI infrastructure - the hardware and cloud computing resources required to train and run models - reached $18 billion globally 12.

This exponentially growing cost curve creates an unprecedented barrier to market entry. In traditional disruption theory, the disruptor utilizes off-the-shelf, cheaper components to build a simpler architecture 45. In the AI landscape, foundation models are built by the world's most capitalized technology conglomerates. Consequently, AI startups are frequently forced into co-opetition agreements with incumbent hyperscalers to secure the necessary computing infrastructure to survive 19. The fundamental engine of the disruption is thus controlled by the incumbents themselves.

Incumbent Advantages in Proprietary Data

Beyond compute constraints, AI reinforces incumbent advantages through the economics of data. NBER research differentiates between training data (necessary to build the models) and input data (necessary to execute specific, context-aware predictions). The non-rival nature of data theoretically allows for broad distribution, but incumbent firms possess vast repositories of proprietary data that they have no incentive to share 20.

This dynamic grants massive market power to established enterprises. While a startup may possess a highly efficient algorithm, an incumbent with decades of structured customer relationship management (CRM) data or enterprise resource planning (ERP) data will generate vastly superior AI outputs. Therefore, rather than rendering incumbents vulnerable, AI often amplifies the value of the assets incumbents already hold 20.

Complex Product Substitution

Classical disruption generally involves a straightforward product substitution: the personal computer replaced the mainframe; the digital camera replaced the film camera 16. Generative AI represents a more complex mechanism. It does not neatly replace a single product; it automates specific cognitive tasks that exist on a continuum within broader workflows 16.

In fields like legal services or software development, high-value activities (strategic architecture) may remain human-led while low-value activities (syntax generation) are fully automated. The disrupted "product" is an interdependent combination of tasks. This complexity makes it difficult for incumbents and entrants alike to draw clear boundaries around vulnerable market segments, forcing organizations to rethink the fundamental definitions of the services they provide rather than simply preparing for product substitution 616.

Incumbent Responses and Sustaining Integrations

Because AI acts as an enabling technology rather than an intrinsically disruptive one, its impact is heavily mediated by business models 2122. To date, the most visible implementations of AI within established enterprises characterize classic sustaining innovation. Incumbents are aggressively utilizing AI to reinforce their existing value propositions, improve operational efficiency, and protect their moats against agile challengers.

Enterprise Software Ecosystems

The enterprise software sector provides the clearest case studies of AI as a sustaining innovation. Global leaders such as SAP and Salesforce have rapidly pivoted their architectures to embed generative AI directly into their existing cloud portfolios 25232425.

Salesforce has deeply integrated its AI suite, Einstein, into its Customer 360 platform, offering predictive, generative, and agentic capabilities 2325. To secure its data cloud dominance and ensure its AI models possess superior enterprise context, Salesforce acquired data-management specialist Informatica for $8 billion 23. The platform's focus has evolved from simple text generation to "Agentforce," allowing autonomous AI agents to reason, plan, and execute multi-step workflows based directly on CRM data through Model Context Protocol interoperability 2526.

Similarly, SAP has positioned its generative AI copilot, Joule, as the central nervous system for its enterprise operations 252324. Rather than treating AI as a standalone novelty, SAP embeds it into supply chain, finance, and human resources workflows 2524. SAP's strategic positioning highlights a fundamental truth about enterprise AI: generative text is statistical and probabilistic, whereas enterprise operations demand deterministic accuracy. A 10% hallucination rate is acceptable in a creative draft but disastrous in a financial regulatory filing 27. By leveraging Retrieval-Augmented Generation for enterprise (RAGe) against its proprietary knowledge graphs, SAP utilizes its massive access to structured enterprise data to ground AI models, effectively locking out startups that lack access to this proprietary contextual data 2327.

Hardware and Industrial Automation

In the hardware and manufacturing sectors, the sustaining deployment of AI is equally pronounced. Samsung Electronics' 2025/2026 strategic roadmap revolves around transitioning its global manufacturing operations into "AI-Driven Factories" by 2030 28. This initiative involves deploying specialized AI agents for quality control, logistics, and digital twin simulations to achieve autonomous production .

On the consumer front, Samsung is executing a "hybrid AI" strategy. By integrating Neural Processing Units (NPUs) directly into its Exynos processors, Samsung allows AI models to run on-device, minimizing latency and addressing cloud privacy concerns while reducing reliance on external AI providers 34. Controlling the entire stack - from semiconductor fabrication to the operating system and the hardware ecosystem - grants Samsung a vertical integration advantage that fragmented entrants cannot easily replicate 34.

Industrial conglomerate Siemens has adopted a similar trajectory. Reporting that 63% of organizations are actively implementing industrial AI, Siemens leverages the technology to orchestrate value chains and optimize energy systems 29. Partnering with Nvidia to bring the "Industrial Metaverse" to life, Siemens data shows that organizations scaling industrial AI are achieving an average of 23% energy savings and 24% reductions in CO2 emissions 2930. In these contexts, AI serves entirely to sustain and elevate premium hardware margins and operational efficiencies.

Regional Divergences in Artificial Intelligence Deployment

The deployment of AI and the resulting market dynamics are not uniform globally. Distinct regulatory, cultural, and economic philosophies have driven stark strategic divergences across North America, Europe, and the Asia-Pacific (APAC) regions 313233.

United States Market Dynamics

The United States operates on an innovation-first philosophy, competing through massive capital deployment, speed to market, and platform scale. Regulation generally follows innovation rather than preceding it 33. Driven by hyperscalers possessing unmatched computing infrastructure, the U.S. model embraces risk and aggressive growth 3334. This environment allows U.S. incumbents to heavily subsidize AI research and rapidly roll out sustaining innovations to their massive user bases. Consequently, worker adoption of AI in the U.S. reached 43% in 2026, significantly outpacing other Western regions 11.

U.S. firms are also scaling agentic systems much more rapidly than international counterparts, seeking full or semi-autonomy in core IT and business workflows 35.

European Market Dynamics and Governance

In stark contrast, the European AI ecosystem is defined by a compliance-driven model prioritizing institutional stability, product safety, and governance 3336. The implementation of the EU AI Act and GDPR has instituted tiered regulations based on risk categories, reshaping how AI can be developed and deployed within the bloc 3133.

While over half of European businesses report using AI (54%), fewer than a quarter (22%) utilize it for complex, transformative workflows, often restricting usage to basic applications like email summarization due to compliance hesitation 15. Longitudinal studies highlight that European firms prioritize ethical stewardship and oversight frameworks over rapid autonomy 35. Furthermore, high energy costs and environmental sustainability mandates present structural headwinds to building massive AI data centers on the continent 33. Despite these headwinds, median financial returns on AI investments are surprisingly similar across regions, yielding approximately $170 million in Europe compared to $175 million in North America, largely due to Europe's deep structural strengths in industrial, automotive, and healthcare applications 3335. Despite EU initiatives like the AI Factories Initiative aimed at closing the innovation gap, Europe remains heavily reliant on U.S. hyperscalers for core AI infrastructure 3436.

Asia-Pacific Agility and SME Adoption

The APAC region, particularly among its tech conglomerates and small-to-medium enterprises (SMEs), demonstrates highly aggressive adoption patterns. In fast-growing Asian markets, speed creates immediate competitive advantages. Consequently, AI strategy in APAC is frequently driven directly by CEOs (33% of respondents vs 18% in North America and 8% in Europe), aligning technology investments tightly with business transformation goals 32.

Southeast Asian SMEs prioritize rapid AI implementation over exhaustive strategic planning, achieving significant efficiency gains while larger Western corporations remain bogged down in committee-led strategy development 37. The Boston Consulting Group projects that AI could contribute up to $120 billion to Southeast Asia's GDP by 2027, driven by a regional "adopt or die" philosophy where 29% of SMEs already use AI and 41% are planning imminent adoption 37.

Chinese Conglomerate Strategies

In China, the landscape is dominated by the BAT conglomerate (Baidu, Alibaba, Tencent). These incumbents act as national champions, leveraging unparalleled domestic data reserves to train their models 3839.

- Baidu: Functions as an early mover, heavily focused on autonomous systems (the Apollo self-driving platform) and robust AI infrastructure (Baige software and proprietary Kunlun chips) 3840.

- Tencent: Operates as a strategic integrator, weaving AI directly into the fabric of its massive consumer applications (WeChat) utilizing its Hunyuan and Yuanbao models 384142.

- Alibaba: Focuses intensely on cloud infrastructure and a Model-as-a-Service (MaaS) architecture through its Tongyi Qianwen platform, supporting massive transactional volumes 404142.

| Region | Strategic Priority | Adoption Posture | Competitive Drivers |

|---|---|---|---|

| United States | Innovation, Scale, Compute Infrastructure | Aggressive (43% worker adoption). High pursuit of autonomy. | Massive venture capital, dominant hyperscalers, speed to market. |

| Europe | Governance, Ethics, Industrial Precision | Cautious (32% worker adoption). 22% transformative usage. | Regulatory standards (EU AI Act, GDPR), deep industrial AI expertise. |

| Asia-Pacific | Agility, Ecosystem Integration, Survival | Highly Aggressive. CEO-led strategy. Rapid SME adoption. | Massive consumer data pools, existential market pressure, $120B GDP impact. |

Evaluating the Disruptive Threshold

While the current landscape heavily favors incumbents leveraging AI as a sustaining force, the theoretical foundations for future disruption remain present. Generative AI is advancing at breakneck speeds, pushing a growing number of use cases across the threshold of genuine disruption 18.

The Open-Source Challenge

One prominent vulnerability to the incumbent stronghold is the proliferation of high-quality open-source models, which threaten to commoditize the foundation layer of AI. The release of Meta's Llama-2 and subsequent models accelerated open-source adoption within enterprise environments 43.

This vulnerability was starkly exposed in early 2025 with the sudden emergence of the Chinese startup DeepSeek. DeepSeek demonstrated that highly capable, disruptive models could be built with drastically fewer resources (reportedly utilizing a fraction of the GPU clusters heavily capitalized hyperscalers depend on), directly challenging the assumption that vast capital is an absolute prerequisite for frontier model development 42.

However, demonstrating the agility of modern incumbents, Tencent rapidly co-opted this disruption, restructuring its organization to integrate DeepSeek's models into its own flagship assistant, Yuanbao, within days 42. Concurrently, Alibaba responded by pledging an unprecedented $52.9 billion in AI and cloud infrastructure, flooding the zone with capital to protect its infrastructure dominance 42. This rapid, overwhelming response illustrates why classical disruption in the AI era is exceptionally difficult for startups: well-resourced incumbents are intensely alert to the threat and possess the capital to assimilate or outspend emerging technologies.

The Transition to Agentic Autonomy

As AI capabilities transition from generative chat interfaces to agentic systems - AI that autonomously plans, reasons, and orchestrates complex multi-step workflows - the nature of market competition will shift 252735. Disruption may ultimately manifest not as new technology, but as radical new business models built upon these agents.

For example, a new entrant in the educational sector may utilize AI not simply to improve software for existing schools (sustaining), but to construct highly scalable, radically affordable "microschool" models that serve completely new demographics, effectively creating a new value network 21. In the corporate realm, AI disruption will materialize as a pricing squeeze. As AI collapses the differentiation of baseline professional services (e.g., routine legal document review, standard code generation), firms relying on billable hours will face severe margin erosion 1620. Disruption will be fundamentally operational and economic; capacity will scale with compute rather than with human headcount, invalidating the historical assumptions that underpin traditional professional service firms 2027.

Conclusion

Measuring the advent of generative artificial intelligence strictly against the Christensen theory of disruptive innovation yields a nuanced outcome. In terms of its initial market trajectory - beginning as an inferior, simpler tool that appeals to non-consumers and rapidly climbing the value chain - AI operates as a textbook disruptive technology. It democratizes access to complex skills, facilitates the execution of previously insurmountable optimizations, and fundamentally alters the productivity curves of the global workforce.

However, the structural economics of AI severely break the classical model. The prohibitive costs of compute infrastructure and the insurmountable advantage of proprietary enterprise data effectively barricade the market against the low-resource entrant traditionally championed by disruption theory. Consequently, rather than falling victim to the "Innovator's Dilemma," modern technology incumbents are highly alert. Firms like SAP, Salesforce, Samsung, and the global hyperscalers are systematically deploying AI as a sustaining innovation, embedding it deeply into their existing operations to reinforce their competitive moats and expand their service capabilities.

Ultimately, artificial intelligence itself is not inherently disruptive; it is a highly potent, capital-intensive, general-purpose technology. True disruption within the AI era will not stem from the underlying algorithms, but from the novel, radically different business models and value networks that entrepreneurs eventually build on top of them.