New-market disruption and non-consumer activation

The dynamics of market evolution have historically been dictated by the continuous refinement of products and services tailored to the most demanding and profitable customers. However, the phenomenon of new-market disruption challenges this traditional trajectory by illustrating how organizations achieve exponential growth not by competing for existing consumers, but by creating entirely new consumption ecosystems. By targeting populations historically excluded from the market due to constraints in wealth, access, time, or skill, disruptive entities forge pathways to profitability that established industry leaders structurally ignore. This report analyzes the theoretical foundations of new-market disruption, the primary barriers to consumption, the strategic mechanisms deployed to overcome these barriers, and the empirical case studies that demonstrate these principles in action. Furthermore, it assesses how generative artificial intelligence and zero-marginal-cost models are currently reshaping the disruptive landscape across global markets.

Theoretical Framework of Disruptive Innovation

The concept of disruptive innovation, introduced by Harvard Business School Professor Clayton Christensen in the 1990s, serves as the foundational framework for understanding how under-resourced entrants can eventually displace established industry incumbents 122. In its earliest iterations, such as the analysis of the disk-drive industry, the theory focused on what was termed "disruptive technology" 3. However, empirical anomalies led to a critical theoretical refinement: Christensen and Michael E. Raynor updated the concept to "disruptive innovation" after recognizing that technologies are rarely intrinsically disruptive; rather, it is the business model that serves as the disruptive vector 345.

Sustaining Innovation and the Technology Mudslide Hypothesis

To isolate the mechanics of disruption, it is necessary to contrast it with sustaining innovation. Sustaining innovations focus on creating better-performing products to sell for higher profits to a company's most demanding customers 678. Organizations already dominant in their industries predominantly rely on sustaining innovations because their internal resource allocation processes and financial incentives - such as gross margin percentages, discounted cash-flow analyses, and return on net assets (RONA) - demand investments in high-profit, high-growth areas 47.

Through sustaining innovations, incumbents consistently improve product performance along an established trajectory. In the "technology mudslide hypothesis," Christensen differentiated this from disruption by noting that sustaining innovation requires constant upward movement just to maintain competitive parity 3. Eventually, this trajectory "overshoots" the performance that mainstream customers can actually utilize or absorb 410. This overshooting creates a structural vulnerability. It opens a vacuum at the lower tiers of the market and completely ignores populations outside the market entirely, setting the stage for disruptive entrants.

Low-End Disruption Versus New-Market Disruption

As disruptive innovation theory matured, researchers bifurcated the phenomenon into two distinct pathways: low-end disruption and new-market disruption, arguing that they represent fundamentally different economic phenomena 4569.

Low-end disruption occurs when a company utilizes a low-cost business model to enter the bottom of an existing market, targeting "overserved" customers who are satisfied with a "good enough" product that performs acceptably at a lower price point 226. In this scenario, the disruptor steals market share directly from incumbents. The incumbent, driven by the pursuit of higher profit margins, willfully concedes this low-margin segment and retreats upmarket rather than engaging in a price war 6712.

Conversely, new-market disruption involves the creation of an entirely new market segment and value network 1310. Rather than targeting overserved customers in the existing value network, new-market disruptors target "non-consumers" - individuals or entities that previously lacked the financial resources, geographic access, or technical skill to participate in the market 4810. Because the new entrant is competing against "non-consumption" (meaning the customer's alternative is nothing at all), the initial product does not need to match the performance of the incumbent's offering; it only needs to be better than nothing 1012.

Performance Trajectories and Metric Evolution

The disruptive trajectory is fundamentally mapped through a "performance over time" conceptual model 14. This performance over time trajectory is the core conceptual backbone of this theory. It effectively plots two intersecting curves on a standard Cartesian coordinate system where the X-axis represents time and the Y-axis represents product performance. Sustaining innovations follow a steep exponential curve that quickly overshoots a shallower, linear band representing mainstream customer demand. Meanwhile, disruptive technologies enter much lower on the Y-axis - below mainstream demand - but improve along their own steep exponential curve. Disruption officially occurs at the intersection point where the disruptive trajectory crosses the threshold of mainstream adequacy 1410.

In a new-market disruption scenario, the entrant's initial product ranks lower on accepted historical performance dimensions (such as processing power, visual fidelity, or physical robustness) 14. However, it introduces a novel mix of secondary attributes - such as being smaller, cheaper, more accessible, or more convenient 14. As the new technology improves at a rate faster than customer demand increases, the disruptive product eventually crosses the adequacy threshold for mainstream use cases 10.

To move upmarket without shedding their cost advantages, successful disruptors rely on an "extendable core." This refers to a business model or underlying technology architecture that enables the entrant to pursue more demanding customers without adding commensurate costs or losing their initial performance advantage 4.

Comparative Dimensions of Innovation Models

The structural differences between these three innovation paradigms dictate organizational strategy, resource allocation, and incumbent response.

| Innovation Category | Target Audience | Economic Profile | Incumbent Response | Trajectory and Market Impact |

|---|---|---|---|---|

| Sustaining Innovation | Existing high-end and mainstream customers ("best customers") 68. | High profit margins; focuses on premium pricing and volume 78. | Vigorous defense and rapid imitation; incumbents thrive and typically win 38. | Incremental or breakthrough improvements along accepted performance metrics 110. |

| Low-End Disruption | Overserved customers at the bottom of the existing market 268. | Low-cost business model; lower profit margins than incumbent products 68. | Incumbents flee upmarket to protect higher margins rather than fight 678. | Captures existing market share; pushes incumbents to abandon the bottom tier 8. |

| New-Market Disruption | Unserved or underserved non-consumers 2810. | Profitability achieved at lower prices per unit; utilizes novel value networks 48. | Ignored by incumbents who view the new segment as non-threatening 8. | Creates a new value network; improves to eventually displace mainstream products 348. |

The Architecture of Non-Consumption

To create a new market, disruptors must convert non-consumers into consumers. Non-consumption is rarely caused by a lack of intrinsic desire for a product; rather, it is enforced by systemic constraints. Research into market-creating organizations reveals a framework of four primary barriers to consumption: wealth, access, time, and skill 11. An analysis of successful market-creating entities indicates that all must overcome at least one of these barriers, while 95% systematically dismantle multiple barriers simultaneously 11. Furthermore, empirical studies show that 100% of these organizations redefined their business activities to create new value networks, 84% integrated internally operations that are conventionally outsourced, and 55% employed breakthrough technologies to achieve their goals 11.

The Wealth Barrier

The most frequently encountered obstacle across both developing and high-income economies is the wealth, or money, barrier 11. Incumbent products are often priced to sustain high gross margins, effectively pricing out the base of the economic pyramid. Disruptors address this barrier not merely by cutting corners, but by fundamentally redefining the business model and cost structure to ensure profitability at vastly lower price points 811. For example, the footwear company Havaianas bypassed the wealth barrier by streamlining sandal design to a flat rubber footbed and a one-piece strap, reducing manufacturing costs to a level affordable for non-consumers 11.

The Access Barrier

The access barrier encompasses geographic, infrastructural, and distributional limitations. Non-consumers may possess the necessary capital but reside in areas ignored by traditional retail or service networks 11. To overcome this, disruptive organizations deploy novel distribution channels. When Havaianas recognized that rural non-consumers could not reach urban retail hubs, they deployed mobile shopfronts via vans to remote towns 11. Similarly, financial service providers leverage existing mobile telecommunication networks rather than building physical bank branches to reach populations isolated from traditional banking infrastructure 11.

The Time Barrier

Time friction prevents consumption when the acquisition or utilization of a product demands a disproportionate temporal investment 11. Complex onboarding processes, long transit times, or slow service delivery act as severe deterrents. Disruptors engineer solutions that drastically reduce the time required to consume. In the micro-insurance sector, organizations like MicroEnsure eliminated the time barrier by collapsing a lengthy registration process into the submission of a single data point: a customer's mobile phone number 11.

The Skill Barrier

Incumbent products often require specialized training, literacy, or domain expertise to operate safely and effectively. The skill barrier locks out non-consumers who lack this specialized knowledge 11. Disruptive innovations simplify the user interface or automate complex underlying processes, rendering the product usable by laypeople. When Galanz sought to introduce microwave ovens to the Chinese market, they encountered a population unfamiliar with the appliance. They overcame the skill barrier through extensive newspaper advertisements that functioned as simple, step-by-step instructional guides, empowering first-time users 11.

Strategic Mechanisms for Market Creation

To dismantle the four barriers to consumption, disruptive enterprises rarely rely on brute-force capital expenditure. Instead, they leverage distinct business model innovations and technological mechanisms that rewrite the economics of distribution and acquisition.

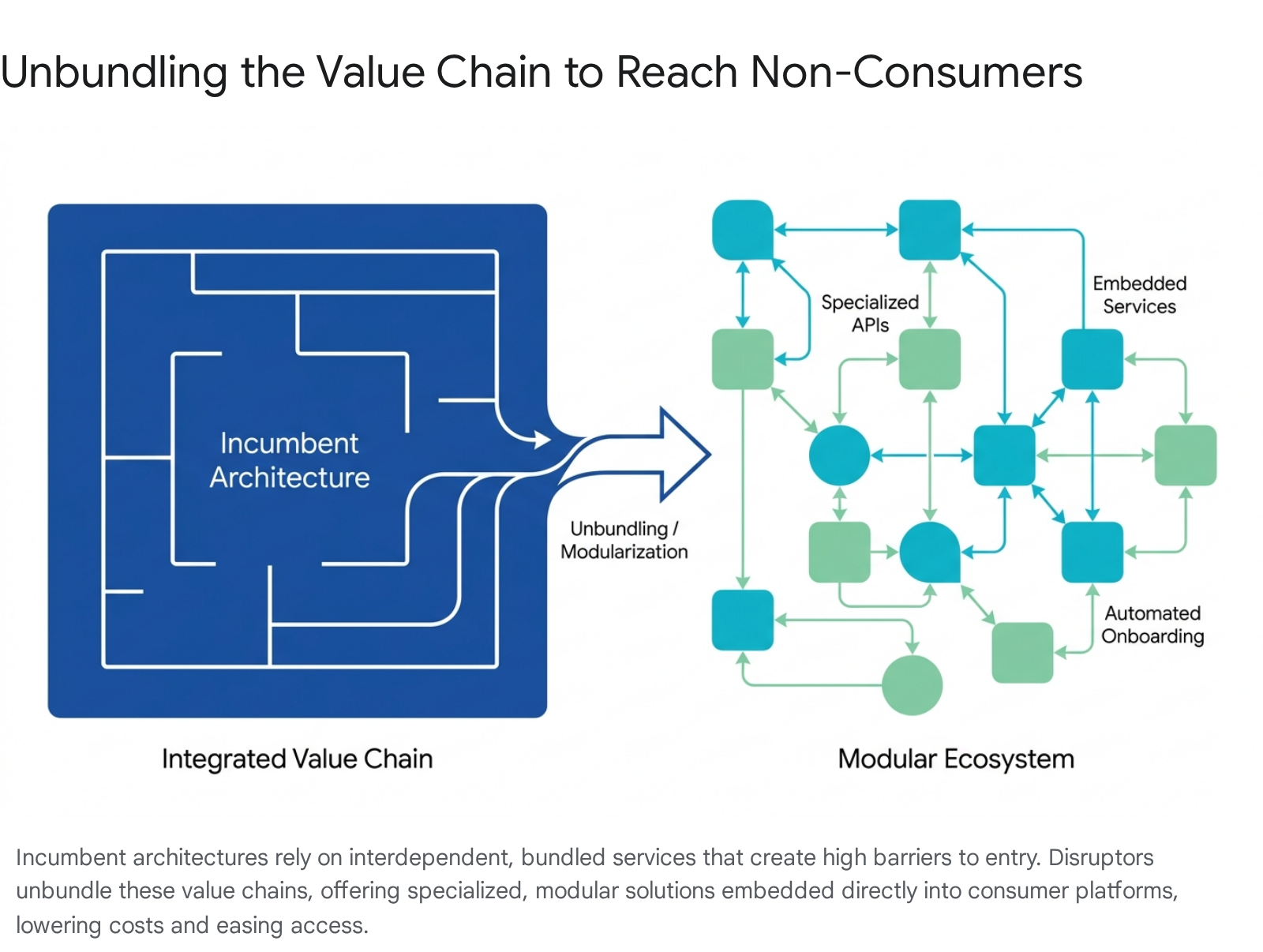

Value Chain Unbundling and Modularization

Unbundling (or modularization) is a strategic mechanism that disaggregates traditional, integrated value chains into specialized, independent components 41213.

Christensen noted that in early markets, firms compete on a primary performance attribute through interdependent, vertically integrated architectures. However, as markets mature, modularization allows new entrants to compete on secondary attributes such as cost, speed, and ease of use 13.

Modularization directly attacks all four consumption barriers. By shifting from monolithic architectures to specialized inputs, providers significantly lower their "cost to serve" and customer acquisition costs, easing the wealth barrier 13. It overcomes the access barrier by allowing financial or retail services to be embedded as APIs directly into the digital environments where customers already operate (e.g., e-commerce platforms or ride-hailing apps) 13. The skill barrier is lowered as modularization enables the integration of automated voice chatbots and AI-driven interfaces that guide weakly literate customers through complex processes 13. Finally, modular value chains reduce the time barrier by facilitating real-time data exchange and faster onboarding 13.

Decentralized Distribution Networks

Decentralized distribution networks circumvent the infrastructural deficits inherent in emerging markets. Traditional, centralized distribution allows a firm to exercise high control and skim channel profits, but it requires massive capital investment and assumes the presence of reliable physical infrastructure 17. In environments plagued by fragmented logistics, poor road networks, and unreliable warehousing, centralization becomes a rigid liability 14.

Disruptors deploy decentralized distribution models to empower open access and facilitate peer-to-peer transactions. For instance, distributed ledger technologies and smart contracts eliminate the need for centralized intermediaries, generating distributed trust and reducing transaction costs - a concept rooted in transaction cost economics and the Coase theorem 171516. Organizations like Winding Tree have attempted to apply these decentralized architectures to the travel industry to unseat centralized booking oligopolies 17. By utilizing decentralized platforms, businesses turn previously infeasible models into viable ones, pushing product and service access to the very edges of the geographic network, thereby overcoming the access barrier 1518.

Pay-As-You-Go Financial Models

The Pay-As-You-Go (PAYG) business model represents a paradigm shift in overcoming the wealth barrier for populations at the base of the economic pyramid, who typically earn less than $2.50 a day 1920. Traditional financing and micro-finance models historically failed this demographic due to high upfront costs and a lack of integrated technical support 20.

PAYG models enable "nanofinancing" - the exchange of products and services for micro, daily sums of money that strictly mirror the day-labor earning and spending habits of non-consumers 1921. This model relies heavily on two technological pillars: mobile money integration and machine-to-machine (M2M) connectivity 2022. A consumer pays a small daily fee (often equivalent to or less than what they previously spent on inefficient alternatives like kerosene) via their mobile device. In exchange, an M2M signal unlocks the product, such as a solar home system 2122. If payment ceases, the system is locked remotely 22. By shifting capital expenditure (CapEx) to operational expenditure (OpEx), PAYG has brought clean energy, irrigation, and sanitation to millions of non-consumers, acting as a profound catalyst for new-market disruption 2023.

Empirical Case Studies in Non-Consumer Activation

The theoretical mechanics of new-market disruption are best illuminated through empirical case studies spanning diverse geographies and industries. These examples highlight how organizations targeted non-consumption through frugal innovation and structural redesign, effectively demonstrating the theories of unbundling, decentralization, and barrier removal.

Mobile Financial Services and M-Pesa

M-Pesa, launched in Kenya in 2007 by the telecommunications firm Safaricom, is a quintessential example of new-market disruption within the financial sector 242531. Prior to M-Pesa's introduction, the vast majority of the Kenyan population constituted non-consumers of formal financial services due to the geographic inaccessibility of bank branches and the high costs associated with maintaining accounts 2425.

Safaricom targeted this non-consumption by transforming the basic mobile phone into a digital wallet. Rather than building costly bank branches, M-Pesa utilized a decentralized distribution network of existing airtime vendors and local shopkeepers who acted as cash-in and cash-out agents 2425. This model required no specialized skills beyond basic mobile phone operation, overcoming the skill and access barriers simultaneously. Furthermore, it facilitated digital bookkeeping, which notably supported women's participation in "chama" (micro-savings) groups 24. Operating as a cornerstone of Africa's "Silicon Savannah," M-Pesa facilitated over 19 billion transactions in Kenya alone during 2022, demonstrating how an early mover can create an entirely new value network that ultimately disrupts traditional banking alliances from the bottom up 2425.

Frugal Innovation in Healthcare: Narayana Health

Frugal innovation - the process of doing more with less to deliver high value at radically lower costs - is a potent driver of new-market disruption 262728. In India, Narayana Health applied these principles to complex medical procedures. Founded by Dr. Devi Shetty in 2000, Narayana Health recognized a massive wealth barrier: millions of Indians required cardiac care, but virtually none could afford the $200,000 equivalent price tag typical of Western open-heart surgeries 29.

By fundamentally redefining the operational business model, Narayana Health achieved extreme economies of scale. Expanding to a chain of 31 hospitals across 19 locations, the organization performs an average of 150 surgeries a day 29. The hospital utilizes activity-based costing models to track the precise cost of every piece of care on a daily basis, allowing them to strip out systemic inefficiencies 29. To overcome geographic access barriers, they rotated staff from their Indian operations to establish Health City in the Cayman Islands 29. Consequently, Narayana reduced the cost of open-heart surgery to approximately $2,000 - without sacrificing clinical outcomes 29. Inspired by Mother Teresa's ethos, this new-market disruption made cardiac care accessible to a population previously excluded from surgical intervention, proving that structural business model redesign can neutralize seemingly insurmountable wealth barriers 29.

Fintech Democratization via Nubank

In Latin America, the banking industry was characterized by severe bureaucratic friction, exorbitant fees, and high interest rates, leaving vast swaths of the population unbanked 303132. Nubank, founded in Brazil in 2013, emerged as a disruptive fintech startup explicitly designed to counter these traditional offerings 3032.

Nubank attacked the wealth and time barriers by offering a no-annual-fee digital credit card managed entirely through an intuitive mobile application, bypassing the labyrinthine bureaucracy of incumbent institutions 3132. Furthermore, Nubank achieved structural cost advantages by eliminating physical branches and relying heavily on data science, technology, and an internally cultivated customer service team known as "Xpeers," who bridged the skill barrier for users transitioning to digital banking 3031. The organization strategically chose to integrate with the Brazilian Central Bank's "Pix" system for real-time, free peer-to-peer transfers rather than building an in-house alternative, showing agility over monolithic control 31. By targeting young, tech-savvy non-consumers, Nubank scaled to serve 85 million customers by 2023 32. Incumbent banks, hindered by their legacy branch costs and dependency on fee revenues, were initially unable to respond to this digitally native entrant 3031.

Logistics Optimization with Rivigo

The Indian logistics and freight sector has historically been plagued by structural deficits: prolonged transit times, driver shortages, poor working conditions, and suboptimal asset utilization 333441. Rivigo initiated a new-market disruption by fundamentally altering the operational paradigm of trucking through its "relay trucking" model 344235.

In a traditional setup, a single driver handles a long-haul route, requiring extended rest periods that idle the asset. Rivigo instituted a system where a driver operates a truck to a designated pit stop, hands the cargo to a rested driver, and takes a return truck back to their home base on the same day 3435. This unbundling of the driver from the specific vehicle ensured non-stop movement of goods, reducing transit times by 50% to 70% compared to industry averages 3442. Additionally, it solved a critical human resource crisis by drastically improving the quality of life for drivers (referred to internally as "pilots") 42.

Coupled with intense technological integration, IoT sensors, and data analytics, Rivigo secured a US patent for its intelligent driver allocation system, which algorithmically balances driving hours, rest, and fuel usage 4235. Backed by significant funding from SAIF Partners and expanding via its Relay-As-A-Service (RaaS) model to an expected 30,000 to 50,000 trucks, Rivigo's model allowed them to scale rapidly, serving an underserved market that demanded transparency and speed but was failed by traditional fragmented logistics 4135.

Summary of Disruption Mechanisms in Case Studies

| Organization | Geography | Industry | Primary Barrier Overcome | Disruptive Mechanism | Market Impact |

|---|---|---|---|---|---|

| M-Pesa | Kenya | Financial Services | Access & Wealth | Decentralized agent network; mobile USSD integration. | 19 billion transactions (2022); broad financial inclusion 2425. |

| Narayana Health | India / Cayman Islands | Healthcare | Wealth | Activity-based costing; high-volume surgical scaling. | Reduced open-heart surgery costs from ~$200k to ~$2k 29. |

| Nubank | Brazil | Financial Services | Wealth & Time | Zero-fee digital model; elimination of physical branches. | Scaled to 85 million customers; bypassed legacy banking bureaucracy 3132. |

| Rivigo | India | Logistics | Time | Relay trucking model; unbundling driver from asset. | Reduced transit times by 50 - 70%; algorithmic fleet optimization 344235. |

Generative Artificial Intelligence as a New-Market Disruptor

The contemporary business landscape is currently navigating a profound technological shift driven by Generative Artificial Intelligence (GenAI). Evaluated strictly through Christensen's framework, GenAI exhibits all the classic markers of a disruptive innovation, specifically threatening the bastions of knowledge work and professional services 10.

GenAI Trajectory and Market Entry

True to disruptive theory, GenAI did not initially enter the market by competing directly with high-end, expert human labor. In its early iterations (circa 2019), GenAI outputs were awkward, error-prone, and largely dismissed by incumbents in law, consulting, and creative agencies as "not professional" 10.

However, GenAI established a powerful foothold as both a low-end and new-market disruptor. It entered at the low end by automating first drafts of code, boilerplate marketing copy, and basic contracts - jobs that incumbents considered too low-margin to fiercely defend 10. More importantly, it enabled new-market disruption by providing non-consumers (e.g., solo entrepreneurs, small businesses, and students) with access to capabilities they could previously never afford 1012. For instance, a small business that cannot afford a full legal team for a non-disclosure agreement finds a GenAI template to be "good enough, fast, and cheap" 10.

Because GenAI is driven by data scale and massive compute capabilities, its rate of improvement (the technology trajectory) is vastly outpacing the slow rise in baseline market demand 10. As the technology climbs this performance trajectory, it crosses the adequacy threshold for mainstream use cases, moving from drafting boilerplate text to writing production-grade code, summarizing complex medical literature, and simulating realistic consumer sentiment through synthetic focus groups 1036. Researchers at the Harvard Business School AI Institute have demonstrated that fine-tuning Large Language Models (LLMs) with historical survey data allows firms to conduct early-stage market research at a fraction of the time and cost of human studies, fundamentally bypassing traditional time and wealth barriers 36.

Zero-Marginal-Cost Economics and the Vulnerability of Solution Shops

The disruptive potency of GenAI is exponentially amplified by its underlying economic structure. Traditional professional service firms - such as major consulting and legal practices - operate as "solution shops." In these models, clients pay high fees for human expertise, which is fundamentally bounded by the constraints of human time and high labor costs 1012. In stark contrast, GenAI operates on a trajectory heading toward a "zero marginal cost" society 373839.

Once a foundational AI model is trained, the cost of generating an additional unit of service - be it a contract review, a coded application, or a marketing strategy - asymptotically approaches zero 373839. If an AI agent can deliver a "good enough" answer for 1% of the cost of a human consultant, the traditional value chain is entirely reconfigured 12. As these AI agents handle search, negotiation, coordination, and enforcement at near-zero marginal cost, the traditional advantages of organizational scale weaken drastically .

This creates severe deflationary pressure in sectors like Software-as-a-Service (SaaS), where enterprise customers are beginning to question high subscription fees when AI models can deliver similar functionality for fractions of the cost 40. Incumbents face a classic innovator's dilemma: serving their current enterprise clients requires sustaining innovations (higher accuracy, premium bespoke service), but fighting the disruption requires embracing a "good enough, cheap, and fast" model that actively cannibalizes their core, high-margin human-capital business 10.

Macroeconomic Implications and the "AI Bubble"

The rapid diffusion of this technology presents broader macroeconomic challenges. Unlike prior technological disruptions that largely impacted routine, manual labor, GenAI threatens non-routine cognitive occupations concentrated at the upper end of the income distribution, potentially leading to unprecedented forms of wage and job polarization 41. The automation of cognitive tasks at zero marginal cost suggests a future where economic growth could decouple from human labor participation 3741.

However, the literature from 2025 and 2026 indicates a growing skepticism regarding immediate enterprise value realization, resulting in discussions of a deflating "AI Bubble" 5142. While generative and agentic AI models are ubiquitous, many organizations struggle to translate individual productivity gains into structural enterprise workflows 5142. Analysts project that the transition from individual tools to true enterprise-level disruption will require significant restructuring of internal data management and business leadership reporting structures 5142. Ultimately, the systemic impact of GenAI will shift competitive advantage away from technical scale toward specialization, proprietary data fine-tuning, and fluid positioning within AI-mediated networks 36.

Conclusions

New-market disruption represents a vital engine for economic democratization and corporate growth. By rigorously analyzing the specific barriers preventing consumption - wealth, access, time, and skill - innovators can architect targeted solutions that transform vast populations of non-consumers into loyal customer bases. Mechanisms such as value chain unbundling, decentralized distribution networks, and pay-as-you-go financial models act as the operational levers that make this transformation possible.

From M-Pesa's revolution of financial inclusion in Kenya and Nubank's digital assault on Brazilian banking bureaucracy, to Narayana Health's frugal healthcare scaling and Rivigo's logistics optimization, the empirical evidence demonstrates that disruption is fundamentally a business model problem, not merely a technological one. Incumbents consistently fail not because they lack resources or technical prowess, but because their rational, profit-maximizing incentive structures blind them to the low-margin, high-volume potential of non-consumption.

Today, as Generative AI and zero-marginal-cost architectures ascend the performance trajectory faster than any prior technology, a new wave of disruption is threatening the bedrock of knowledge work and professional services. Organizations that recognize the markers of new-market disruption - early market inferiority, focus on underserved demographics, and rapidly improving cost-performance ratios - will be positioned to not only survive these transitions but to actively architect the new markets of the digital era.