Klarna IPO Valuation and Financial Analysis

Buy Now Pay Later Market Structural Evolution

The global macroeconomic environment of the post-2022 era forced a profound structural reckoning across the financial technology sector, fundamentally altering the valuation paradigms for consumer finance operators. During the zero-interest-rate policy environment of 2021, deferred payment fintechs were valued almost exclusively on gross merchandise volume growth and market share acquisition, a dynamic that culminated in Klarna's peak private market valuation of $45.6 billion in July 2021 1. However, the subsequent normalization of global monetary policy, characterized by rising funding costs, compressed merchant discount rates, and widespread institutional skepticism regarding unseasoned unsecured consumer credit, precipitated a severe valuation correction. By mid-2022, Klarna's internal valuation had contracted by approximately 85% to $6.7 billion 1.

The company's eventual transition to the public markets represents a critical case study in business model restructuring. Klarna's corporate narrative shifted abruptly from hyper-growth cash burn to rigorous operational leverage, disciplined unit economics, and artificial intelligence-driven cost containment. This strategic pivot resulted in the company recording its first annual net profit since 2019, generating $21 million in net income in 2024 on a gross merchandise volume of $105 billion 11. This momentum accelerated into 2025, with full-year gross merchandise volume reaching $127.9 billion, representing 22% year-over-year growth, alongside total revenues of $3.5 billion 2. By the first quarter of 2026, Klarna achieved an adjusted operating profit of $68 million - up dramatically from $3 million the prior year - alongside a 44% year-over-year revenue increase to $1.0 billion 34.

To fully contextualize the justification and subsequent public market reception of Klarna's initial public offering, it is necessary to deconstruct the granular mechanics of its take-rate economics, analyze the normalization of credit losses across its global portfolios, and evaluate the unprecedented corporate restructuring that fundamentally altered the company's operating leverage.

Initial Public Offering Mechanics and Equity Structure

Klarna formally initiated its transition to the public markets by publicly filing a registration statement on Form F-1 with the United States Securities and Exchange Commission in March 2025, indicating its intent to list ordinary shares on the New York Stock Exchange under the ticker symbol "KLAR" 567. The offering was structured and managed by a premier consortium of financial institutions, with Goldman Sachs, J.P. Morgan, and Morgan Stanley acting as joint book-running managers, supported by a syndicate including Bank of America Securities, Citigroup, Deutsche Bank, Societe Generale, and UBS 68.

The initial public offering comprised a total of 34,311,274 ordinary shares 89. The structure of the offering highlighted the liquidity demands of early investors, as the issuance was heavily weighted toward secondary sales. Klarna offered only 5,555,556 primary ordinary shares, while existing selling shareholders offered 28,755,718 ordinary shares, granting underwriters a 30-day option to purchase up to an additional 5,146,691 shares to cover overallotments 89. Klarna did not receive any proceeds from the shares liquidated by selling shareholders 89. With an initial pricing target between $35 and $37 per share, the offering was designed to raise up to $1.27 billion, establishing an implied debut valuation of approximately $14 billion 89.

Prior to the offering, Klarna implemented a corporate reorganization, redomiciling its parent company from Sweden to the United Kingdom in May 2024 and executing a twelve-for-one share split in early March 2025 10. The equity structure post-IPO features a dual-class voting system designed to consolidate founder control. Alongside the standard ordinary shares, Klarna issued Class B shares as a bonus issue to existing pre-IPO shareholders 7. Each Class B share carries ten votes per share, is strictly non-transferable, and automatically converts into deferred shares without economic or voting rights upon transfer or after a sunset period of twenty years 7.

Net Transaction Margins and Take Rate Economics

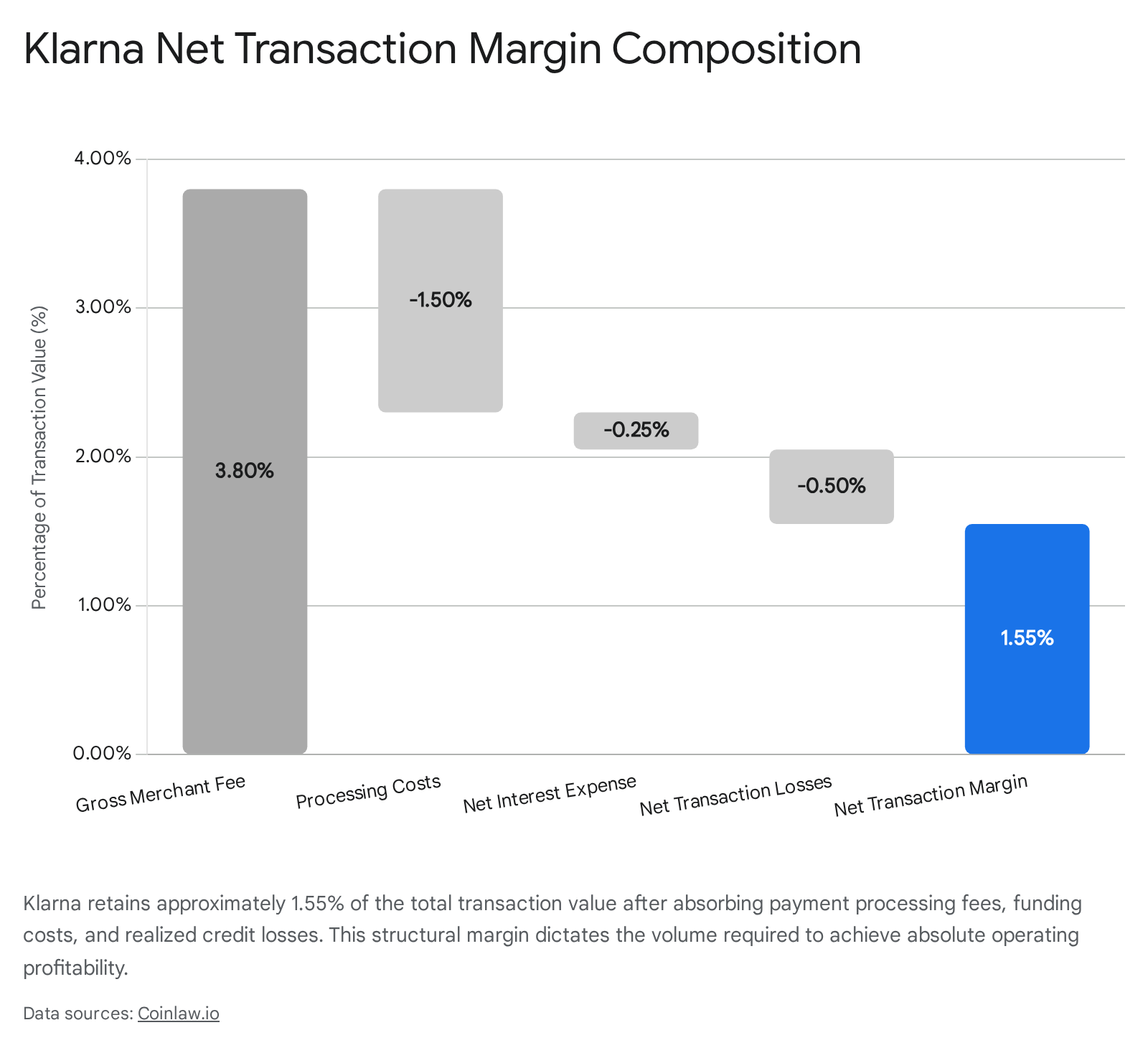

The core economic engine of a deferred payment network lies in its net transaction margin. This metric represents the residual profit remaining after merchant fees are collected and all variable transaction, processing, funding, and credit loss costs are deducted. Unlike traditional credit card issuers that rely heavily on revolving consumer interest and punitive late fees, Klarna's foundational "Pay in 4" and "Pay in 30 days" installment models derive the vast majority of their revenue directly from merchant commissions 113.

Merchants are willing to pay elevated discount rates - typically ranging between 1.99% and 6.00% depending on the region and the specific product - because alternative payment integration structurally drives a 15% to 50% uplift in average order value while completely offloading fraud liability and consumer default risk from the retailer to the payment network 1415.

In a standard transaction, Klarna captures a gross merchant fee of approximately 3.80% 11. However, this gross take rate is subject to immediate, structurally embedded deductions that reduce the top-line yield to a narrower net margin. First, processing costs account for an estimated 1.50% deduction 11. Klarna must absorb the interchange fees and payment gateway costs paid to major card networks like Visa and Mastercard, as well as processors like Stripe, to facilitate the initial consumer transaction 111. Second, net transaction losses deduct an additional 0.50%, representing a provision for unrecoverable consumer defaults and organized fraud 11. Finally, net interest expenses deduct 0.25%, representing the cost of capital required to fund the temporal gap between paying the merchant upfront and collecting installments from the consumer 11.

After all network, capital, and risk deductions are applied, Klarna realizes a net transaction margin of roughly 1.55% per transaction 111.

This figure represents the true fundamental yield of the platform. Because the average duration of Klarna's short-term credit portfolio is approximately 40 days, the company is capable of recycling its balance sheet capital roughly nine times per calendar year 112. This high-velocity capital recycling allows Klarna to generate substantial absolute margin dollars on a relatively asset-light base, which serves as a key differentiator when compared to traditional revolving credit issuers whose capital is tied up in multi-year receivables. In the first quarter of 2026, Klarna's aggregate transaction margin dollars expanded 44% year-over-year to $389 million, demonstrating the scalability of this high-velocity margin model 34.

Strategic Product Mix Shifts and Fair Financing

While Klarna established its global brand presence on the zero-interest "Pay in 4" product, the company has aggressively expanded its suite of financial products into interest-bearing, longer-term point-of-sale installments, branded internally as "Fair Financing." This product allows consumers to finance larger-ticket purchases over terms extending up to 36 months, functioning more as a traditional term loan 1518. The adoption of this product has been rapid; in the fourth quarter of 2025, Fair Financing gross merchandise volume accelerated by 165% year-over-year, taking direct market share from legacy revolving credit cards 1314.

This product mix shift presents a highly complex dynamic for Klarna's overall unit economics. Fair Financing carries structurally higher lifetime take rates than the standard Pay in 4 product because it incorporates direct consumer interest income alongside the merchant fee 12. As of 2024, interest income comprised approximately 24% of Klarna's total revenue, despite Fair Financing representing only 5% of the total gross merchandise volume 13.

However, longer-duration loans require significantly different accounting treatments. Under IFRS 9 accounting standards, Klarna is required to provision for expected credit losses upfront when the loan is originated. Therefore, while Fair Financing drastically improves the long-term lifetime value of a consumer cohort and diversifies revenue streams, its rapid growth can temporarily depress near-term reported transaction margins due to the heavy upfront provisioning requirements 1215. Financial analysts closely monitor this dynamic, as the short-term margin compression masks the underlying long-term profitability embedded in the extended loan durations.

Consumer Credit Risk Normalization

The primary existential threat directed at the alternative payment industry during the 2022 macroeconomic tightening cycle was the prospect of unmanageable credit losses. Market critics hypothesized that proprietary underwriting algorithms, trained almost entirely during a decade of low interest rates, government stimulus, and low unemployment, would structurally fail during an inflationary shock.

Klarna's post-2022 financial results systematically dismantled this bearish thesis. The company's short-duration loan portfolio - where 84% of loans have a duration of three months or less - acts as a structural defense mechanism against macroeconomic degradation 12. Unlike traditional credit cards that issue static, long-term credit limits, Klarna's proprietary machine learning algorithms re-underwrite consumers in real-time at the point of every individual transaction 4. If a consumer misses a single installment payment, their access to the entire global network is instantly suspended, structurally preventing debt stacking.

This dynamic, per-transaction underwriting model allowed Klarna to aggressively curtail risk exposure in deteriorating markets faster than legacy banks. The most profound evidence of this algorithmic normalization occurred in the United States, which serves as Klarna's fastest-growing and largest absolute market, generating roughly $850 million in revenue in 2024 1. In 2021, Klarna's provision for credit losses in the U.S. sat at an unsustainable 3.6% of gross merchandise volume 16. Through rigorous algorithmic refinement and tighter risk parameters, Klarna reduced this U.S. credit loss provision to just 0.63% by the end of 2025, even as U.S. gross merchandise volume expanded by over 213% during the same multi-year period 16.

On a consolidated global basis, Klarna's credit quality remained highly resilient. Credit loss provisions stood at 0.55% of total gross merchandise volume in the first quarter of 2026, virtually unchanged from the 0.54% recorded in the first quarter of 2025 3417. By successfully maintaining sub-1% absolute credit loss ratios, Klarna proved to institutional investors that its underwriting models could successfully separate credit risk from top-line volume growth. This normalization of credit costs was the primary catalyst enabling the company to pivot from deep operating losses to consistent operational profitability.

Deposit Funding and Liability Management

A critical, often underappreciated variable in Klarna's valuation framework is its sophisticated liability structure. As central bank interest rates rose globally, independent payment operators faced surging costs of wholesale capital. Competitors without banking licenses are forced to rely heavily on forward-flow agreements, warehouse credit facilities, and asset-backed securitization markets to fund their loan portfolios, exposing them directly to volatile capital market pricing 1819.

Klarna, however, holds a full European banking license. Over the past several years, the company has methodically pivoted its funding base away from institutional capital markets and toward retail consumer deposits. By the end of 2025, approximately 90% of Klarna's total funding - amounting to $13 billion - was derived directly from consumer savings deposits across European markets 16. To support further expansion in North America, Klarna launched FDIC-insured high-yield savings accounts in the United States in mid-2026, offering yields above 3% to attract retail liquidity 26.

This structural liability advantage serves two key functions. First, it allows Klarna to secure highly stable capital at a generally lower blended cost than its non-bank competitors, insulating its net transaction margin from wholesale market shocks. Second, it creates a deeply sticky consumer ecosystem. Klarna reported 15.8 million "banking consumers" in the fourth quarter of 2025, representing a highly engaged segment that grew 101% year-over-year 1314. The unit economics of this segment are highly lucrative; these deep-relationship users generate an average of $107 in annual revenue per user, more than three times the $30 generated by an average, transaction-only consumer 1314.

To supplement this deposit base and ensure sufficient capital for its rapidly growing U.S. Fair Financing portfolio, Klarna successfully executed a $2 billion forward flow facility with Santander in early 2026, unlocking $17 billion in U.S. financing capacity 49. The company also finalized an agreement to sell $26 billion worth of seasoned loan receivables to Nelnet Financial Services, optimizing its balance sheet ahead of the public offering 9.

Competitor Unit Economics Comparison

The global alternative payment market is highly competitive and fragmented, with leading platforms utilizing divergent economic and distribution models. Valuing Klarna's $14 billion target requires precise benchmarking of its unit economics against its primary publicly traded competitors: Affirm Holdings Inc. (NASDAQ: AFRM) and PayPal Holdings Inc. (NASDAQ: PYPL).

| Operational Metric | Klarna Group plc | Affirm Holdings Inc. | PayPal Holdings Inc. (Pay in 4) |

|---|---|---|---|

| Primary Consumer Focus | Everyday retail, apparel, broad AOV | High AOV, electronics, home goods | Broad e-commerce, ubiquitous digital checkout |

| Total Platform Consumers | 119 million active consumers 3 | 26.8 million active consumers 19 | 439 million active accounts (all services) 20 |

| Active Merchant Network | 1,075,000 merchants 17 | 515,000 active merchants 19 | 36 million merchants (all services) 20 |

| Gross Take Rate (Revenue / GMV) | ~2.7% (FY 2024 average) 113 | ~8.4% (Projected FY 2026) 1821 | 1.62% overall transaction take rate 29 |

| Net Yield Metric | 1.55% Net Transaction Margin 11 | 4.3% Revenue Less Transaction Costs 19 | Undisclosed specifically for BNPL cohort |

| Credit Loss Rate | 0.55% of GMV (Q1 2026) 3 | 6.0% allowance on held loans 19 | 0.02% total credit loss rate (Q1 2026) 22 |

| Primary Funding Mechanism | Consumer bank deposits 16 | Securitization, warehouse facilities 1819 | Internal corporate cash / blended balance sheet |

| Maximum Financing Duration | Up to 36 months (Fair Financing) 1518 | Up to 60 months 23 | 6 weeks (Pay in 4) / up to 24 months (Pay Monthly) 2425 |

Affirm operates a model strictly optimized for higher-ticket items, offering structured financing terms that extend up to 60 months with Annual Percentage Rates ranging from 0% to 36% 1523. Because Affirm retains a significant portion of interest-bearing loans on its balance sheet or securitizes them, it captures a substantially higher gross revenue yield as a percentage of gross merchandise volume - projected at 8.4% for fiscal 2026 2126. Consequently, Affirm's Revenue Less Transaction Costs (RLTC) - its equivalent metric to Klarna's net transaction margin - stood at an impressive 4.3% of volume in the third quarter of fiscal 2026, totaling $498.2 million 19. This superior yield profile justifies Affirm's premium valuation multiple, though it comes with elevated absolute credit risk; Affirm's allowance for credit losses stood at 6.0% of loans held for investment, with 30-day delinquencies on monthly installment loans tracking at 2.8% 19.

Conversely, PayPal's payment installment product operates primarily as a defensive conversion tool designed to protect its dominant position in global branded checkout. While PayPal processed over $40 billion in installment payment volume in 2025, representing a 20% year-over-year increase, this still represents barely 2% of the company's massive $1.79 trillion aggregate total payment volume 2024. PayPal's overall transaction take rate has experienced structural, long-term compression, falling to 1.62% in the first quarter of 2026 29. Unlike Klarna or Affirm, PayPal does not rely on deferred payments to drive standalone corporate profitability. Rather, it utilizes zero-interest installments as a loss-leader or margin-neutral feature to prevent merchant and consumer attrition to dedicated external networks.

Operational Restructuring and Artificial Intelligence Integration

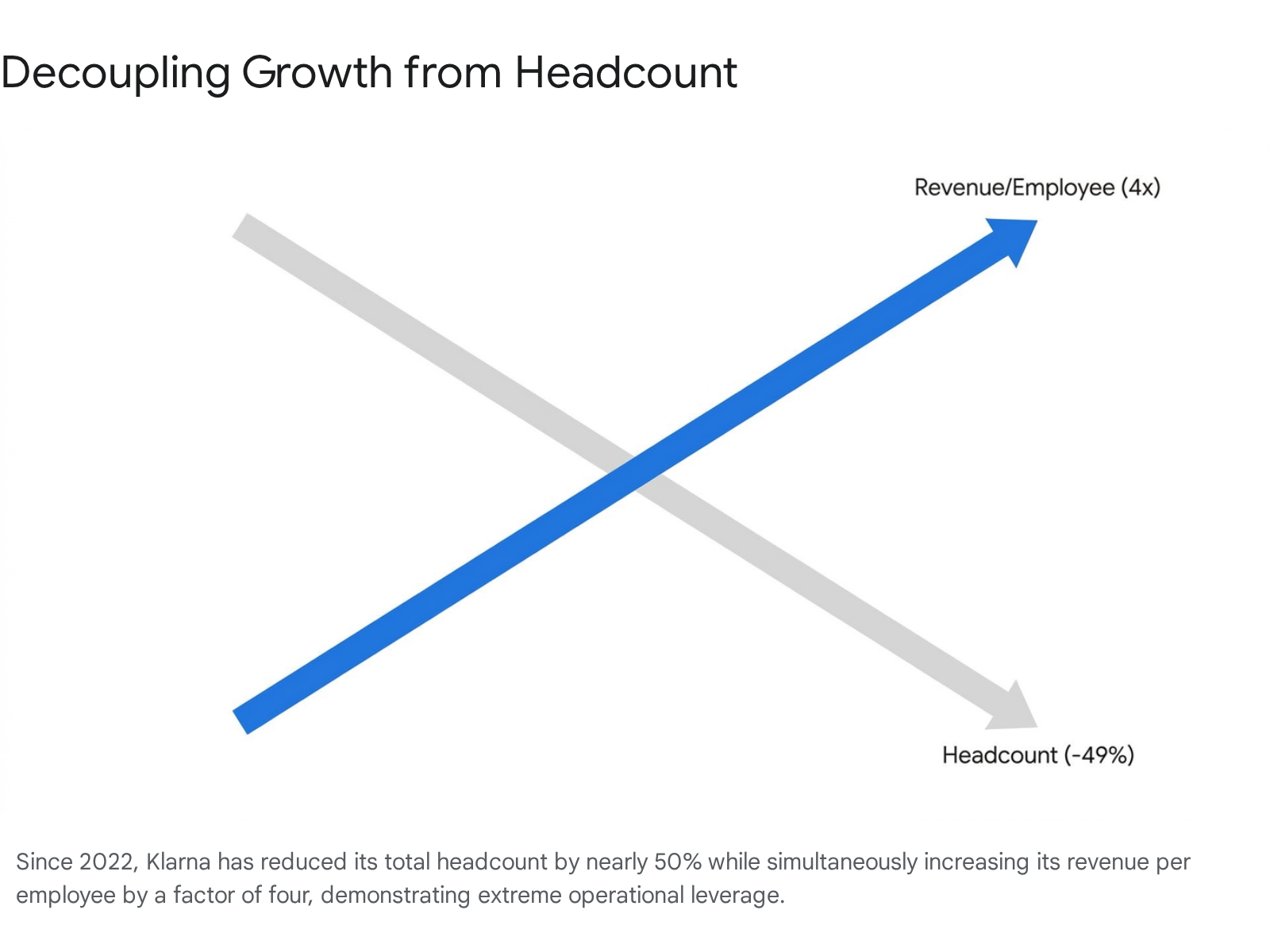

The most compelling narrative supporting Klarna's return to public market viability is its aggressive internal corporate restructuring. Between 2022 and 2026, executive management executed a ruthless transition from headcount-driven scale to technology-driven leverage, utilizing generative artificial intelligence as a core operational component rather than a peripheral tool.

The quantitative results of this efficiency mandate are stark and highly visible in the income statement. Between the fourth quarter of 2022 and the fourth quarter of 2025, Klarna's absolute revenue grew by 104%, yet total operating expenses declined by 8% 1314. To achieve this, the company reduced its global human headcount by 49% 1314. As a direct consequence of integrating proprietary artificial intelligence into customer service workflows, real-time underwriting models, and backend engineering processes, Klarna's revenue per employee metric surged to roughly $1.4 million by the first quarter of 2026 - a fourfold increase from baseline 2022 levels 4.

This extreme operational leverage was the primary driver of the first quarter 2026 financial results. Adjusted operating profit reached $68 million, while GAAP-compliant operating income achieved $17 million, representing a monumental fundamental swing from a $90 million GAAP loss in the exact same quarter the previous year 3417. The company effectively proved to public market analysts that its commerce platform can process and sustain over $127 billion in annual gross merchandise volume without requiring a commensurate, linear expansion of fixed overhead costs.

Equity Lockup Expiration and Secondary Market Dynamics

A crucial technical factor impacting Klarna's post-IPO valuation and stock price performance is the mechanical structure of its equity lock-up expiration. Following the public listing, massive blocks of pre-IPO equity were restricted from trading to prevent immediate market saturation. The primary lock-up expiration event occurred on March 9, 2026, releasing a staggering 335 million ordinary shares - representing nearly 88% of the 378 million total outstanding shares - from strict IPO lock-up agreements .

However, the liquidity reality of this expiration is highly nuanced. The 335 million locked-up shares were divided into distinct legal categories governed by separate sets of securities regulations . Approximately 159 million of these shares (48% of the lock-up pool) were held as depository receipts . Crucially, roughly 97 million of those depository receipt shares were controlled by corporate affiliates - including major institutional investors, executive officers, and board members . These affiliate shares remained subject to stringent ongoing trading volume restrictions under Rule 144 of the U.S. Securities Act, which legally limits the quantity of shares insiders can sell in any given timeframe, regardless of the lock-up expiration .

Furthermore, 82 million shares belonging to pre-IPO investors required the manual submission of a Letter of Transmittal to the transfer agent (Computershare) to initiate the conversion process before they could be actively traded - a bureaucratic process requiring 7 to 10 business days, effectively staggering the supply of new equity entering the open market . Finally, corporate employees had previously been granted an early liquidity window to sell shares up until September 30, 2025, and existing shareholders liquidated 34.4 million shares directly into the IPO, meaning the March 2026 event was not the initial liquidity opportunity for many early stakeholders .

These technical market mechanics are critical for valuation models. If 335 million shares were to flood the market simultaneously, the resulting supply shock would severely depress Klarna's market capitalization. The staggered, heavily regulated nature of the release mechanisms helped mitigate immediate downward price volatility, though the persistent overhang of insider shares continues to influence institutional buying behavior.

Public Market Capitalization Benchmarking

When Klarna launched its initial public offering on the New York Stock Exchange, it priced its shares to target an ambitious $14 billion valuation 8935. This figure requires careful benchmarking against its peers to understand subsequent market sentiment and price discovery.

In June 2026, Affirm possessed a highly resilient market capitalization oscillating between $21.0 billion and $22.3 billion 36372739. Affirm generated gross merchandise volume of $11.6 billion in the third fiscal quarter of 2026 and guided for roughly $49.5 billion in total volume for the full fiscal year 19. By stark contrast, Klarna processed $127.9 billion in volume in fiscal 2025 2 and reported $33.7 billion in just the first quarter of 2026 alone 3.

Despite Klarna possessing nearly three times the absolute transaction volume of Affirm and a vastly larger global merchant network (1.07 million merchants compared to Affirm's 515,000) 1719, Klarna's initial primary valuation target of $14 billion was significantly lower than Affirm's public market cap.

This apparent discrepancy is rooted deeply in the fundamental differences in unit economics analyzed previously. Because Affirm serves higher order value categories and acts as a long-term balance-sheet lender, its revenue yield on total volume is structurally superior (projected at ~8.4% versus Klarna's ~2.7%). Public market investors consistently assign higher revenue multiples to Affirm's robust interest-income generation and 4.3% revenue-less-transaction-costs yield. Klarna's model - while carrying vastly more raw volume and broader consumer engagement metrics - operates on tighter absolute transaction margins (1.55%) and relies on massive scale to generate absolute cash flow 11.

It is also crucial to note that public market equities are subject to severe post-IPO repricing volatility. Following its public debut, Klarna's market capitalization experienced standard public market multiple compression. Market data from June 2026 indicates Klarna's market capitalization stabilized in the range of $4.9 billion to $6.2 billion, with the stock trading around $15.78 to $16.44 per share 4041424344. This severe contraction from the $14 billion IPO target suggests that while private market sponsors and underwriters modeled an aggressive growth multiple, public institutional investors heavily discounted the stock. This discount is likely attributable to the inherently thin margins of the European payments space, intense competitive saturation from mega-cap technology firms entering the checkout flow, and ongoing regulatory pressures regarding consumer lending disclosures in the European Union and the United Kingdom.

Market Outlook

Klarna's targeted $14 billion IPO valuation was anchored in a mathematically demonstrable operational turnaround rather than the speculative euphoria of previous funding rounds. By definitively proving that it can normalize credit losses in its largest market - compressing U.S. loss provisions from an unsustainable 3.6% down to a highly controlled 0.63% 16 - Klarna neutralized the primary bear thesis surrounding the unsecured consumer lending sector.

Furthermore, the company's aggressive post-2022 restructuring serves as a premier industry benchmark for artificial intelligence-driven operational leverage, allowing the firm to scale past $127 billion in annual volume with half the workforce it required three years prior 214. The strategic utilization of a European banking license to amass $13 billion in sticky retail deposits provides Klarna with a durable, low-cost funding moat that non-bank competitors simply cannot replicate 16.

However, the long-term sustainability of the company's valuation - and the public market's willingness to re-rate the stock upward from its compressed June 2026 levels of approximately $6 billion - depends entirely on Klarna's ability to transition its 119 million global users from low-margin, transient checkout interactions into high-margin, permanent banking relationships. The rapid adoption of the debit-first Klarna Card and the triple-digit growth of its interest-bearing Fair Financing portfolio indicate that this transition is aggressively underway. Ultimately, Klarna has successfully evolved from a highly scrutinized deferred-payment checkout feature into a structurally profitable, highly scaled global retail banking network.