Buy-now-pay-later regulation in the US and EU

Market Transition in Buy-Now-Pay-Later Financing

The global consumer credit ecosystem has experienced a profound structural evolution over the past decade, heavily influenced by the proliferation of Buy-Now-Pay-Later (BNPL) platforms. Originally conceptualized as a frictionless, technology-driven alternative to traditional revolving credit, the BNPL sector expanded rapidly by targeting consumer demand for short-term liquidity at the point of sale. During the economic disruptions of the COVID-19 pandemic, the sector saw unprecedented acceleration. Industry analyses suggest that the equivalent of ten years of e-commerce growth occurred within a ninety-day window, providing a massive macroeconomic tailwind for integrated financing solutions 1. In the United States, nominal BNPL loan origination values from the top six lenders increased by 304.5% between 2019 and 2020, and by an additional 186.5% the following year 2.

Despite this explosive historical growth, the BNPL industry has entered a highly complex and volatile transition phase. The initial era of regulatory arbitrage - in which financial technology (fintech) firms utilized structural exemptions to operate outside traditional banking and consumer credit perimeters - is definitively ending. Jurisdictions globally are moving to close legislative loopholes that previously shielded short-term, low-value, interest-free installment loans from regulatory scrutiny 33. This tightening of the regulatory perimeter coincides with macroeconomic headwinds, shifting consumer credit quality, and changing unit economics for leading market participants.

Firms such as Klarna Group plc, a pioneer of the "pay-in-four" lending model, have been forced to fundamentally alter their business strategies. To maintain revenue growth and consumer engagement, these platforms have pivoted toward regulated retail banking and longer-term, interest-bearing loans 46. This strategic shift has subjected these entities to stringent capital adequacy requirements, complex accounting standards regarding credit loss provisions, and intensified supervisory enforcement across multiple jurisdictions 8. Consequently, Klarna's late 2025 initial public offering (IPO) on the New York Stock Exchange serves as a critical test case for assessing the viability of the BNPL business model within a heavily regulated, high-compliance-cost environment 91011.

This report provides an exhaustive analysis of the evolving BNPL regulatory frameworks in the European Union and the United States. It examines the underlying consumer protection risks driving legislative intervention and evaluates the profound impact of compliance costs and financial reporting standards on Klarna's post-IPO market performance.

Consumer Protection Risks and Behavioral Economics

The fundamental value proposition of BNPL relies on seamless integration into the digital checkout experience. However, the exact mechanisms designed to reduce friction and drive sales conversion have raised substantial concerns among consumer protection advocates, behavioral economists, and prudential regulators regarding their long-term impact on household financial stability.

Debt Stacking and Unsecured Leverage

A primary systemic risk associated with the BNPL model is "debt stacking" - a phenomenon where consumers accumulate multiple concurrent loan obligations across different platforms without respective lenders having visibility into the borrower's aggregate debt exposure. Historically, the majority of BNPL lenders did not furnish loan origination or performance data to nationwide consumer reporting companies. Consequently, traditional underwriting models and external observers remained largely blind to this hidden leverage 513.

Extensive data analysis conducted by the U.S. Consumer Financial Protection Bureau (CFPB), utilizing a probabilistically matched sample of BNPL applications and de-identified credit records, reveals the scale of this issue. In 2022, 21% of U.S. consumers with an established credit record financed at least one purchase using BNPL, an increase from 17.6% in 2021 513. The frequency of borrowing has also escalated; the average number of annual originations per BNPL borrower increased from 8.5 to 9.5 over the same period 13. Most concerning to regulators, approximately 63% of BNPL borrowers originated multiple simultaneous loans during the year, with 33% holding concurrent loans across multiple distinct BNPL providers 513.

The empirical data indicates that BNPL users generally experience higher degrees of financial constraint compared to non-users. Consumers utilizing BNPL hold significantly higher balances on other unsecured credit products, including personal loans, retail loans, student debt, and traditional credit cards 513. On average, BNPL borrowers maintained total unsecured debt balances of $22,163 during borrowing months, with BNPL representing 17% of that total 13. Furthermore, BNPL users maintained credit card utilization rates between 60% and 66% from 2020 to 2023, compared to just 34% for consumers who never used BNPL 5.

Table 1: Financial Profile and Utilization Metrics of U.S. BNPL Borrowers (2022-2023 Data)

| Metric / Characteristic | BNPL Borrowers | Non-BNPL Borrowers | Systemic Implication |

|---|---|---|---|

| Credit Card Utilization Rate | 60% - 66% | 34% | High prior utilization suggests BNPL is accessed when traditional credit is exhausted. 5 |

| Average Unsecured Debt Balance | $22,163 | Significantly Lower | Indicates higher overall financial leverage and vulnerability to economic shocks. 13 |

| Simultaneous Loan Originations | 63% | N/A | High prevalence of "debt stacking" across platforms, creating hidden default risks. 513 |

| Average Annual Originations | 9.5 loans | N/A | Demonstrates reliance on BNPL for continuous consumption rather than isolated large purchases. 13 |

Credit Approval and Subprime Concentration

The data suggests that decreasing availability of traditional credit acts as a primary catalyst for BNPL adoption; credit card utilization rates steadily increase in the twelve months preceding a consumer's first BNPL transaction 5. To maintain high approval rates despite these risk profiles, BNPL providers have increasingly relied on algorithmic counteroffers. Rather than rejecting applicants with subprime credit profiles outright, lenders adjust the terms - such as requiring a down payment larger than the standard 25% or lowering the approved credit limit 513.

This practice sustained an overall credit approval rate of 79% in 2022. Notably, this included a 78% approval rate for applicants categorized within subprime or deep subprime credit tiers 513. Borrowers with deep subprime credit scores (FICO 300-579) accounted for 45% of all BNPL originations, while those with subprime scores (FICO 580-619) accounted for an additional 16% 2. While this broadens financial access, it simultaneously concentrates credit risk among the most financially vulnerable demographic segments, particularly consumers aged 18-24, for whom BNPL debt constitutes 28% of their total unsecured consumer debt 13.

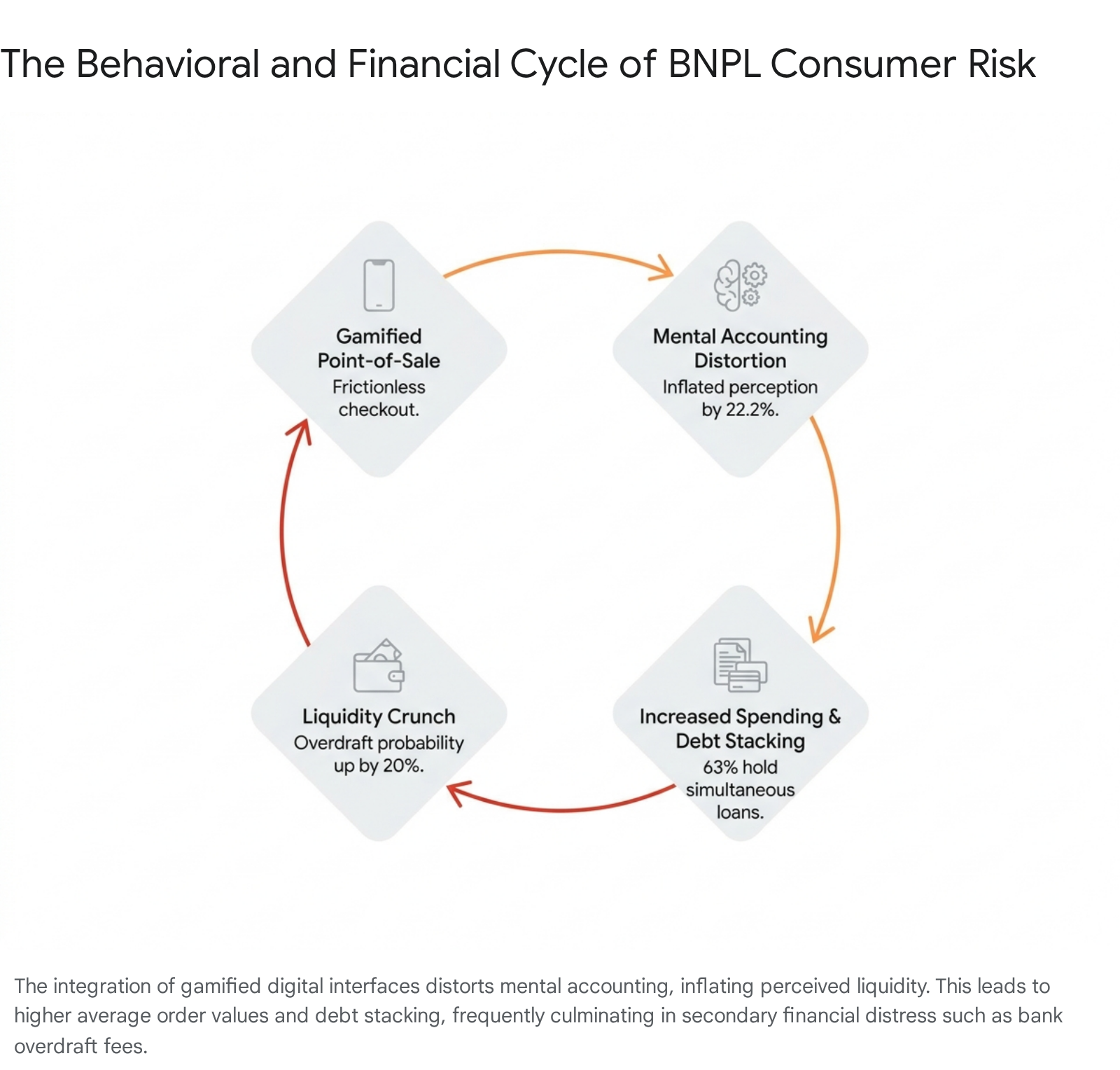

Gamification and Behavioral Economics

The frictionless design of BNPL interfaces is deeply rooted in behavioral economics and gamification, systematically altering consumer spending habits. Empirical research demonstrates that BNPL significantly increases both the likelihood of purchase completion and the average order value (AOV). E-commerce platforms integrate BNPL specifically to combat cart abandonment, with merchants reporting conversion rate increases of 20% to 30% for high-value items when BNPL is offered 16.

An experimental study conducted by the Central Bank of Ireland involving a nationally representative sample quantified these behavioral effects. The research found that participants spent an average of 4.39% more when utilizing BNPL compared to traditional debit cards 7. Crucially, the study identified a "mental accounting" mechanism: the deferral of payment creates an artificially inflated perception of available liquidity. This cognitive distortion led to a 22.2% higher likelihood of consumers purchasing discretionary, non-essential products 7.

The psychological integration of BNPL into daily consumption is often analyzed through the lens of the Technology Acceptance Model (TAM), extended to include Gamification (GM) and Perceived Value (PV). Quantitative studies indicate that gamification - achieved through social media-like interfaces, push notifications, and reward structures - significantly enhances the perceived value and behavioral intention to use BNPL services among younger demographics 168. Sociological analyses further argue that BNPL providers have transformed credit into a lifestyle consumer good. Drawing on theoretical frameworks such as Sianne Ngai's concept of the "gimmick," researchers posit that BNPL services create antinomies for young consumers, positioning debt not as a financial burden but as a gamified, entrepreneurial tool for lifestyle maintenance 189.

However, this behavioral modulation carries tangible secondary financial consequences. The reduction in price elasticity and the shift toward immediate gratification frequently result in subsequent liquidity issues. Research indicates that BNPL usage causes a statistically significant increase in the probability of a consumer incurring overdraft fees (a 20% increase) and low-balance fees (a 17% increase) on their primary bank accounts, suggesting that short-term consumption is financed at the expense of longer-term financial stability 1.

Data Harvesting and Dispute Resolution Deficiencies

Beyond direct financial risks, the BNPL business model relies heavily on data harvesting and monetization. Consumer advocacy groups, including Consumer Reports, have raised alarms regarding the extensive collection of transactional, behavioral, and demographic data. A comprehensive study evaluating BNPL applications against the Fair Digital Finance Framework found significant deficiencies in privacy and data protection 1011.

While most BNPL firms do not explicitly sell raw consumer data, the majority share granular purchasing behavior with third-party networks for targeted advertising, affiliate marketing, and merchant lead generation 1011. This creates a closed-loop ecosystem where consumers are continuously retargeted with bespoke product recommendations financed by the platform's own credit facilities. Furthermore, the study noted that many BNPL applications default to permissive data-sharing settings, fail to commit to real-time fraud monitoring, and utilize mandatory arbitration clauses that strip consumers of the right to pursue class-action litigation in the event of data breaches or deceptive practices 1011.

Regulatory Frameworks in the European Union

In response to the rapid expansion of digital micro-lending and the escalating risks of consumer over-indebtedness, the European Union has undertaken a comprehensive overhaul of its consumer credit legislation. The transition represents a fundamental shift from a "light-touch" regulatory environment to a rigorous, verification-first compliance regime designed to structurally alter how short-term credit is issued.

Implementation of the Second Consumer Credit Directive

The cornerstone of the EU's regulatory response is Directive (EU) 2023/2225, commonly referred to as the Second Consumer Credit Directive (CCD2). Adopted by the European Parliament and Council in October 2023, CCD2 replaces the outdated 2008 directive (CCD1), which was drafted prior to the proliferation of modern fintech solutions and embedded point-of-sale financing 2223. Member states are required to transpose CCD2 into national law by November 20, 2025, with the rules becoming fully applicable and enforceable across the bloc by November 20, 2026 32224.

CCD2 specifically targets the legislative loopholes that BNPL providers previously exploited. Under the 2008 regime, credit agreements involving amounts under €200, as well as loans that were interest-free and repayable within three months with only "insignificant charges," were largely exempt from stringent consumer protection oversight 3121327. The BNPL industry systematically built its frictionless checkout models within these structural exemptions 3.

The new directive operates on the principle of "functional symmetry" - asserting that if a product functions as credit, it must be regulated as credit, irrespective of the technological interface or merchant partnership structure 3. CCD2 explicitly brings third-party BNPL arrangements, embedded finance, and small-value digital loans (ranging from €0 up to €100,000) fully within the regulatory perimeter 31228. Consequently, BNPL providers will be subject to strict caps on Annual Percentage Rates (APR) and late fees, mandatory 14-day rights of withdrawal, and rigorous pre-contractual information requirements, including the provision of standardized European Consumer Credit Information (SECCI) forms in a mobile-friendly format 32229.

Open Banking and Article 18 Mandates

The most operationally disruptive element of CCD2 for the BNPL industry is the strict mandate regarding creditworthiness assessments outlined in Article 18. Historically, BNPL providers relied on instantaneous, algorithmic "soft" credit checks based on internal behavioral scoring, basic self-declarations of income, and device telemetry to approve loans in milliseconds without introducing friction at checkout 33031.

Article 18 abolishes this practice. It requires creditors to conduct a thorough, proportionate, and forward-looking assessment of a consumer's ability to meet repayment obligations before granting credit or significantly increasing a credit limit 223014. Crucially, the directive mandates that these assessments must be based on "sufficient, accurate and up-to-date information" regarding the consumer's verified income, expenses, and existing financial liabilities 3283031. Furthermore, CCD2 expressly prohibits the use of health data or non-financial behavioral data scraped from social networks for underwriting purposes 28.

To comply with Article 18 without entirely destroying the user experience, BNPL providers are being forced to integrate with Open Banking infrastructure (facilitated by the Revised Payment Services Directive, PSD2). Open banking Application Programming Interfaces (APIs) allow lenders to instantly query a consumer's primary bank account to analyze real-time cash flows, identifying existing debt obligations and verifying income 32830. While this satisfies the regulatory mandate for objective financial data, it introduces unavoidable latency and technical friction into the checkout process, fundamentally altering the economics of impulse purchasing 331.

Supervisory Enforcement and the Swedish Authority

As the domicile for Klarna and several other major European fintechs, Sweden serves as a critical nexus for BNPL regulation. The Swedish Financial Supervisory Authority (Finansinspektionen, or FI) has proactively increased its scrutiny of the sector ahead of the formal CCD2 implementation, which will be enacted via amendments to the Swedish Consumer Credit Act and the repeal of legacy statutes governing certain consumer credit operations 291516.

The FI's enforcement posture has hardened significantly regarding anti-money laundering (AML) and counter-terrorist financing (CTF) compliance within the payments and BNPL sectors. Following an investigation into Klarna Bank AB's risk assessment processes and customer due diligence measures for the period ending March 2022, the FI identified material deficiencies in how the bank handled clients utilizing invoice products. Consequently, in 2024/2025, the regulator issued Klarna a formal remark and an administrative fine of 500 million SEK (approximately $46 million USD) 353617. While the FI noted that the violations did not warrant the withdrawal of Klarna's banking license, the action underscores the heightened supervisory risk for BNPL platforms operating as licensed credit institutions 3617.

Furthermore, as a fully licensed bank, Klarna is subject to the FI's annual Supervisory Review and Evaluation Process (SREP) under European banking rules. In September 2025, the FI established strict capital requirements for Klarna, mandating a Pillar 2 requirement (P2R) of 1.07% and a risk-weight-based Pillar 2 guidance (P2G) of 5.0% of the total risk exposure amount, heavily reliant on Common Equity Tier 1 (CET1) capital 838. These prudential requirements strictly govern the leverage Klarna can apply, limiting the degree to which it can aggressively expand its loan book without raising highly dilutive equity capital. This operates within a broader Swedish macroeconomic environment where the government is actively attempting to manage household debt-to-income ratios - which reached 210% in 2025 - through strict amortization requirements and adjustments to mortgage caps 3940.

Regulatory Frameworks in the United States

In stark contrast to the European Union's methodical, legislative overhaul via CCD2, the regulatory landscape for BNPL in the United States is characterized by federal volatility, partisan shifts, and aggressive state-level intervention.

Federal Volatility and the CFPB Interpretive Rule

The U.S. federal approach to BNPL has been defined by rapid shifts in executive policy. Under the Biden administration, the Consumer Financial Protection Bureau (CFPB), directed by Rohit Chopra, sought to aggressively rein in the sector using existing statutory frameworks. Because the Truth in Lending Act (TILA) and its implementing Regulation Z generally apply to credit that is subject to a finance charge or payable in more than four installments, the standard "pay-in-four" BNPL model historically operated outside these traditional credit card regulations 4142.

In May 2024, the CFPB attempted to close this gap unilaterally by issuing an Interpretive Rule. The Bureau took the legal position that the "digital user accounts" issued by BNPL providers functioned precisely like conventional credit cards, thereby classifying BNPL lenders as "card issuers" and "creditors" under Subpart B of Regulation Z 43441846. This classification would have imposed massive compliance burdens on the industry, mandating standardized cost-of-credit disclosures, strict billing error dispute resolution mechanisms, mandatory pause of payments during investigations, and formalized refund crediting procedures 41434647.

The industry retaliated immediately. The Financial Technology Association (FTA) - a trade group representing major BNPL providers including Klarna, Affirm, and Block - filed a federal lawsuit against the CFPB in October 2024. The FTA argued that the Bureau had violated the Administrative Procedure Act (APA) by imposing substantive new obligations under the guise of an "interpretive rule" without completing the mandatory notice-and-comment rulemaking process. Furthermore, they argued that forcing short-term, closed-end installment loans into an open-end revolving credit regulatory framework was arbitrary, capricious, and technologically ill-fitting 464849.

The regulatory environment fractured abruptly following the presidential transition. In early 2025, under the direction of the newly installed Acting CFPB Director Russell Vought (appointed by the Trump administration), the Bureau reversed course entirely as part of a broader deregulation mandate that saw the withdrawal of 67 regulatory guidance documents 50. In March 2025, the CFPB and the FTA filed a joint status report in the U.S. District Court for the District of Columbia, wherein the CFPB committed to withdrawing the 2024 Interpretive Rule.

By June 2025, the CFPB formally announced it would not reissue a revised rule. The Bureau conceded that the previous interpretation was "procedurally defective" and applied "ill-fitting open-end credit regulations to BNPL products" which placed a "substantial burden on regulated entities" with "little benefit to consumers" due to the short duration of the loans 484951. This federal retreat effectively returned the U.S. BNPL market to a state of regulatory ambiguity, leaving consumers without standardized TILA dispute-resolution mechanisms or uniform cost disclosures at the federal level 46.

State-Level Intervention in California

The withdrawal of federal oversight has catalyzed individual states to fill the regulatory void, creating a fragmented and complex compliance environment for nationwide BNPL providers. The State of California has emerged as the most aggressive jurisdiction, utilizing the California Department of Financial Protection and Innovation (DFPI) to enforce strict localized standards.

In direct response to the CFPB's rollback, the California legislature advanced Senate Bill 825 (SB 825). Effective January 1, 2026, SB 825 drastically expands the DFPI's enforcement authority under the California Consumer Financial Protection Law (CCFPL). Previously, entities operating under legacy state licenses - such as the California Financing Law, under which many BNPL loans are regulated - enjoyed broad exemptions from the CCFPL's overarching provisions while acting within the scope of their licenses 5253.

SB 825 eliminates these exemptions, granting the DFPI explicit authority to pursue enforcement actions for "unlawful, unfair, deceptive, or abusive acts or practices" (UDAAP) against state-licensed financial institutions, including BNPL platforms and Earned Wage Access providers 531956. This legislation empowers the DFPI to investigate hidden fees, deceptive marketing algorithms, and gamification tactics regardless of a firm's specific lending license, significantly elevating compliance risks, duplicative investigations, and potential litigation costs for operators in the state 5219.

Concurrently, the DFPI implemented new formalized registration, supervision, and data reporting requirements covering income-based advances and various debt settlement services, effective February 15, 2025 205821. These regulations require providers to integrate with the Nationwide Multistate Licensing System & Registry (NMLS), submit detailed financial and operational data, and undergo routine compliance examinations to monitor for abusive practices 205822.

Table 2: Comparative BNPL Regulatory Landscape (2025 - 2026)

| Jurisdiction | Primary Framework | Legal Classification of BNPL | Key Compliance Requirements & Status |

|---|---|---|---|

| European Union | Consumer Credit Directive II (CCD2) | Fully Regulated Consumer Credit | Mandatory Open Banking creditworthiness checks (Art. 18); APR caps; standardized SECCI disclosures. Active Nov 2026. 322 |

| United States (Federal) | Truth in Lending Act (TILA) / Reg Z | Unregulated / Exempt (Closed-end < 4 installments) | None specifically mandated for pay-in-four following the CFPB's rescission of the 2024 Interpretive Rule. 4851 |

| California (State) | CCFPL / SB 825 / Calif. Financing Law | State-Licensed Loans | Subject to stringent UDAAP enforcement; mandatory NMLS data reporting. SB 825 active Jan 2026. 5220 |

| Sweden (National) | Swedish Consumer Credit Act / FI Oversight | Licensed Banking / Credit Operations | Strict AML/CTF compliance; Basel III/SREP capital adequacy buffers; CCD2 integration. Strictly enforced by the FI. 82917 |

Impact on Klarna Unit Economics and Market Valuation

The collision of these tightening regulatory frameworks in Europe, fragmented compliance burdens in the U.S., persistent macroeconomic pressures, and the intrinsic limitations of the zero-interest BNPL business model culminated in Klarna's highly anticipated public market debut. The IPO and subsequent financial disclosures offer a transparent view into the unit economics of a sector undergoing a forced evolution.

Public Market Debut and the Growth Paradox

During the zero-interest-rate macroeconomic environment of 2021, Klarna reached a peak private market valuation of $45.6 billion, fueled by hyper-growth narratives and abundant, cheap wholesale debt 910. However, as global interest rates normalized and credit quality concerns surfaced, the company endured a severe valuation compression, dropping to approximately $6.7 billion in a 2022 private funding round 10.

After executing a rigorous turnaround focused on aggressive headcount reduction - decreasing staff by 49% since 2022 by leveraging artificial intelligence to automate customer service and operations - and slashing sales and marketing expenditures, Klarna filed for an IPO on the New York Stock Exchange in September 2025 under the ticker "KLAR" 491011. The IPO priced at $40.00 per share, raising $1.37 billion and yielding an opening market capitalization of approximately $15 billion 1011.

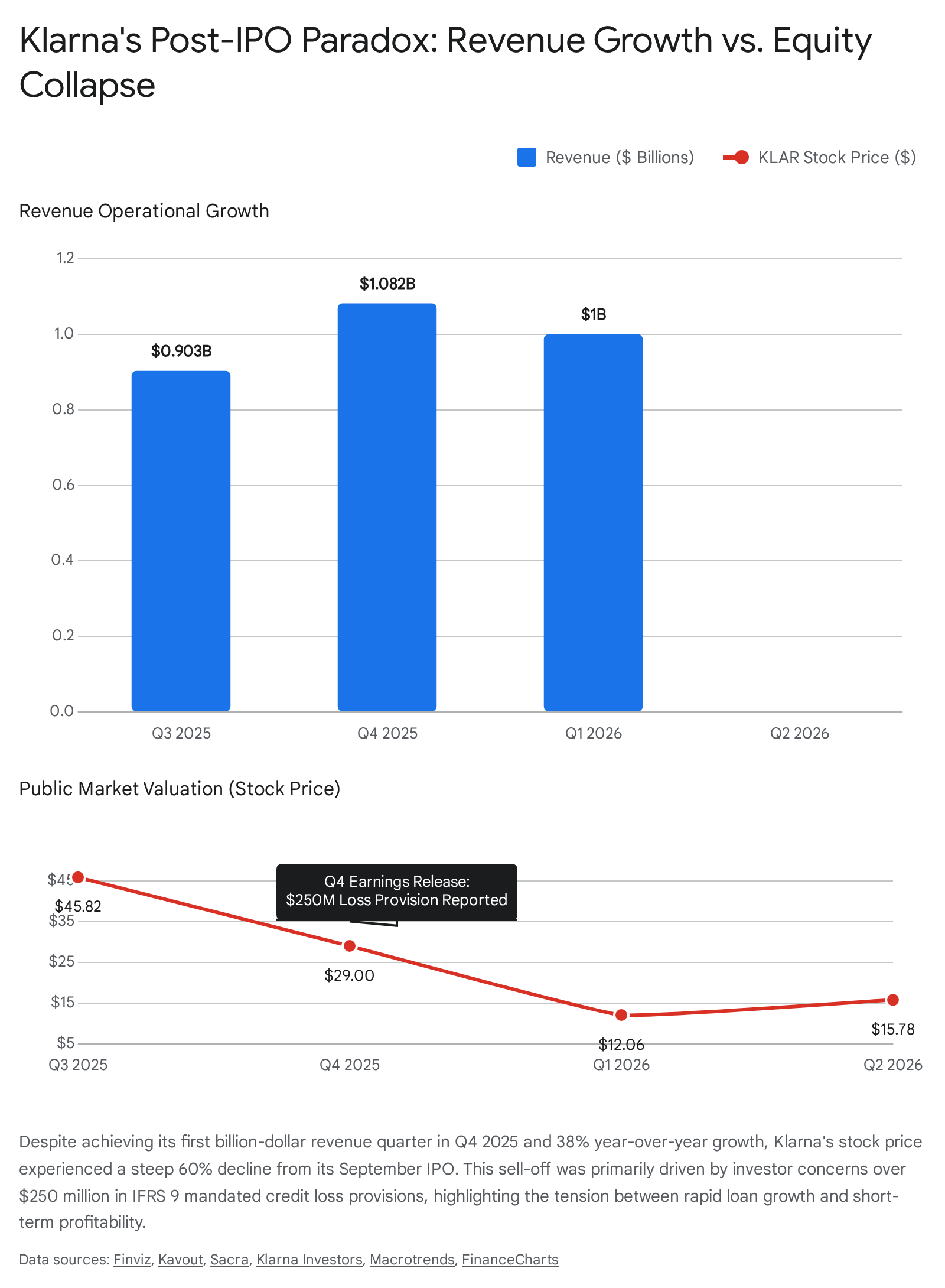

While the listing successfully provided necessary liquidity for early investors and reduced reliance on expensive wholesale debt, the post-IPO market reception was brutal. Despite reporting strong 24% year-over-year revenue growth in FY2024, reaching $2.81 billion, and achieving a nominal net profit of $21 million, the narrative quickly soured 101123. Following the release of its Q4 2025 earnings in February 2026, Klarna's stock price collapsed by nearly 26% in a single day 4. By June 2026, the stock was trading between $15.78 and $17.90, representing a decline of over 60% from its IPO price and destroying significant shareholder value 246364.

IFRS 9 Accounting and Credit Loss Provisions

The precipitous drop in Klarna's equity valuation was not driven by a failure to generate top-line growth. In fact, Q4 2025 represented a milestone for the company: its first-ever billion-dollar revenue quarter ($1.082 billion, up 38% YoY), driven by massive 58% revenue growth in the U.S. market and overall Gross Merchandise Volume (GMV) reaching $38.7 billion 6525. The platform reached 118 million active consumers and 966,000 active merchants 26.

Rather, the stock sell-off was triggered by a sudden swing back to unprofitability, posting a $26 million net loss for Q4 2025 and an aggregate net loss of $273 million for the full year 42365. The core catalyst for these losses was a massive spike in provisions for credit losses, which surged by 59% year-over-year to $250 million in Q4 2025 alone 46.

This dynamic is a direct consequence of Klarna's strategic transition into traditional banking and the mechanical application of International Financial Reporting Standard 9 (IFRS 9). Historically, Klarna relied on short-duration pay-in-four loans (averaging 40 days), which turned over rapidly and required minimal capital lock-up or long-term provisioning 68. However, to drive higher customer lifetime value (LTV) and offset the margin compression caused by rising deposit costs and merchant fee pressures, Klarna aggressively expanded "Fair Financing" - longer-term, interest-bearing consumer installment loans designed to capture market share from traditional credit cards 42568. In Q4 2025, Fair Financing GMV surged by 165% year-over-year 425.

Under IFRS 9's Expected Credit Loss (ECL) model, the moment a longer-term installment loan is originated, the lender must immediately book a "Stage 1" provision for expected credit losses over the next 12 months, taking an upfront hit to the Profit & Loss (P&L) statement. Conversely, the interest revenue generated by that loan is amortized and recognized gradually over the life of the asset 669.

Therefore, Klarna's rapid success in scaling its longer-term lending portfolio inherently generated a severe profitability lag. The massive $250 million loss provision was primarily an accounting requirement driven by volume growth, not a deterioration in underlying credit quality. In fact, Klarna's realized credit losses - the actual write-offs of uncollectible debt - fell to a record low of 0.44% of GMV in Q3 2025, and provisions as a percentage of GMV actually declined slightly quarter-over-quarter from 0.72% to 0.65% 425. Nonetheless, public market investors, spooked by the absolute dollar magnitude of the provisions and cautious about the macroeconomic health of unsecured consumer credit, punished the stock severely. This discrepancy between accounting reality and investor expectations culminated in a securities class-action lawsuit filed against Klarna in early 2026, alleging the company failed to adequately disclose the risks tied to loan losses in its IPO prospectus 665.

Compliance Costs and Strategic Pivot

The economics of Klarna's evolution are fundamentally strained by escalating compliance and funding costs. Unlike debt-reliant rivals such as Affirm, Klarna operates as a fully licensed European bank. This provides a structural funding advantage; in 2025, approximately 90% of Klarna's lending was funded by $13 billion in consumer deposits 102370. However, the cost of servicing these deposits has surged dramatically in a higher-rate environment, rising from $63 million in 2022 to $667 million in 2025, severely compressing net interest margins 923.

Furthermore, the transition from a specialized BNPL provider to a comprehensive digital bank demands vast investments in Regulatory Technology (RegTech) and legal infrastructure. The implementation of CCD2 across 27 EU member states necessitates localized compliance architectures. Article 18's requirement for verified open-banking creditworthiness checks forces platforms to internalize high data acquisition costs and build robust, auditable decision engines that can prove to regulators like the Swedish FI that consumer debt capacity was accurately measured 331.

Additionally, the fragmented U.S. landscape, spearheaded by California's SB 825, subjects Klarna to state-by-state licensing battles, disparate UDAAP interpretations, and disjointed reporting mandates 5253. Small-scale BNPL providers will likely struggle to absorb these fixed compliance costs, potentially triggering a wave of distressed M&A activity as larger banks absorb their merchant networks 3. For Klarna, the path to sustained profitability requires leveraging artificial intelligence to ruthlessly slash operational overhead to offset the heavy, inflexible costs of maintaining a regulated banking infrastructure and absorbing mandated credit loss provisions 425.

Table 3: Klarna Group plc Financial & Operational Evolution (2024 - 2025)

| Metric | FY 2024 | FY 2025 | Strategic Implication |

|---|---|---|---|

| Gross Merchandise Volume (GMV) | $105.0 Billion | $127.9 Billion | +22% YoY; Growth driven heavily by US market expansion and 165% growth in Fair Financing. 112526 |

| Total Revenue | $2.81 Billion | $3.50 Billion | +25% YoY; Q4 2025 alone exceeded $1.08 Billion, demonstrating scale. 112526 |

| Net Profit / (Loss) | $21 Million | ($273 Million) | Swing to unprofitability largely driven by IFRS 9 upfront credit loss provisioning on long-term loans. 41023 |

| Realized Credit Losses | 0.48% (Q2 '24) | 0.44% (Q3 '25) | Actual write-offs remain near historic lows, demonstrating AI-driven underwriting discipline despite accounting losses. 11 |

| Consumer Deposit Funding | ~94% of lending | ~90% of lending | Sourced ~$13B in deposits; funding costs surged to $667M (2025), reflecting margin pressure. 102370 |

Conclusion

The Buy-Now-Pay-Later sector has irrevocably crossed a regulatory Rubicon. The foundational era - characterized by unregulated digital micro-loans, frictionless impulse purchasing, and opaque consumer debt stacking - has been terminated by synchronized, albeit divergent, interventions in Europe and the United States.

In the European Union, the impending enforcement of the Second Consumer Credit Directive (CCD2) ensures that BNPL providers will operate under the same stringent affordability and transparency mandates as traditional banking institutions, forcing the integration of Open Banking APIs to satisfy Article 18's creditworthiness checks. Conversely, the United States has descended into a fractured regulatory environment, where the federal retreat by the CFPB has mobilized individual states like California to unilaterally weaponize consumer protection statutes against financial technology firms.

For industry leaders like Klarna, this maturation forces a fundamental renegotiation of their underlying unit economics. The strategic necessity of pivoting toward longer-term, interest-bearing "Fair Financing" to achieve profitability in a high-compliance landscape has subjected them to the harsh realities of traditional banking. As demonstrated by Klarna's tumultuous public market debut, the mechanical application of IFRS 9 accounting standards creates a severe, structural lag between aggressive loan origination and recognized profitability. Ultimately, the survival of BNPL platforms in this new paradigm relies not on regulatory arbitrage or gamified checkout experiences, but on the ability to leverage artificial intelligence to execute flawless underwriting, minimize operational overhead, and transparently communicate the complex realities of banking economics to skeptical public markets.