How Buy Now, Pay Later Works and How Klarna Makes Money

Buy Now, Pay Later (BNPL) allows consumers to split retail purchases into interest-free installments, while the BNPL provider pays the merchant upfront and assumes all consumer credit risk. Providers like Klarna generate the majority of their revenue not from consumer interest, but by charging retailers premium transaction fees for the increased sales volume and larger cart sizes the service drives. However, as the industry matures, Klarna is aggressively shifting its business model to include interest-bearing loans, high-yield savings accounts, and late fees to achieve long-term profitability amidst mounting regulatory and macroeconomic pressures.

The Evolution of Consumer Credit and BNPL

To understand the mechanics and meteoric rise of modern Buy Now, Pay Later platforms, one must trace the history of installment-based consumer credit. The concept of paying for goods over time is a foundational element of modern retail. In the mid-1800s, the Singer Sewing Machine Company began selling its expensive equipment on installment plans, allowing middle-income families to afford capital-intensive machines that would otherwise be entirely out of reach . By the 1930s, during the Great Depression, retail "layaway" programs emerged. These programs allowed shoppers to reserve an item and make payments over time, but the consumer only took the item home once the balance was paid in full 13.

The contemporary BNPL industry, spearheaded by fintech pioneers like the Swedish-born Klarna, represents a digital evolution of these historic concepts, explicitly optimized for frictionless e-commerce. Prior to the COVID-19 pandemic, BNPL occupied a relatively minor niche in the broader consumer finance ecosystem. However, as global populations were isolated at home with stimulus capital and an accelerated shift toward digital retail, the industry experienced explosive growth. In the United States alone, the number of BNPL loans originated grew more than tenfold, soaring from 16.8 million in 2019 to 180 million by 2021 1. By 2025, the total BNPL origination volume in the U.S. had surged to nearly $160 billion, permanently altering the digital checkout landscape 2.

The core psychological and financial appeal of BNPL is instant gratification combined with delayed financial impact. Unlike traditional layaway, the consumer receives the product immediately. Unlike a traditional revolving credit card, the core BNPL product charges zero interest and operates on a strict, fixed repayment schedule, offering perceived transparency that appeals heavily to younger and credit-averse demographics 15.

Comparing BNPL to Traditional Credit Avenues

To fully grasp where BNPL sits within the broader financial ecosystem, it is critical to compare its functional mechanics against the traditional alternatives available to consumers at checkout.

| Feature | Buy Now, Pay Later (e.g., Klarna) | Traditional Credit Card | Traditional Retail Layaway |

|---|---|---|---|

| Product Acquisition | Immediately at checkout | Immediately at checkout | Only after the final payment is made |

| Interest Charges | Typically 0% for short-term plans | Yes, if the balance is carried past the grace period | No interest |

| Credit Underwriting | Soft pull (generally does not impact credit score) | Hard pull (can temporarily lower credit score) | No credit check required |

| Payment Structure | Fixed schedule (e.g., 4 equal payments) | Flexible (minimum monthly payment required) | Fixed schedule, but highly flexible terms |

| Consumer Protections | Limited; disputes handled primarily via the BNPL app | Strong federal protections (e.g., Fair Credit Billing Act) | Varies heavily by individual store policy |

| Optimal Use Case | Specific, one-time retail purchases | Everyday, recurring expenses and building credit history | Expensive seasonal gifts without debt risk |

The Mechanics of a Klarna Checkout

When a shopper reaches the digital or physical checkout of a partnered retailer - a network that includes massive global brands like Macy's, Nike, Airbnb, Uber, and Expedia - they are presented with Klarna as a localized payment option alongside traditional credit cards and digital wallets 345. Klarna serves approximately 119 million active global consumers and processes over 3.4 million transactions daily across more than 966,000 merchants 346.

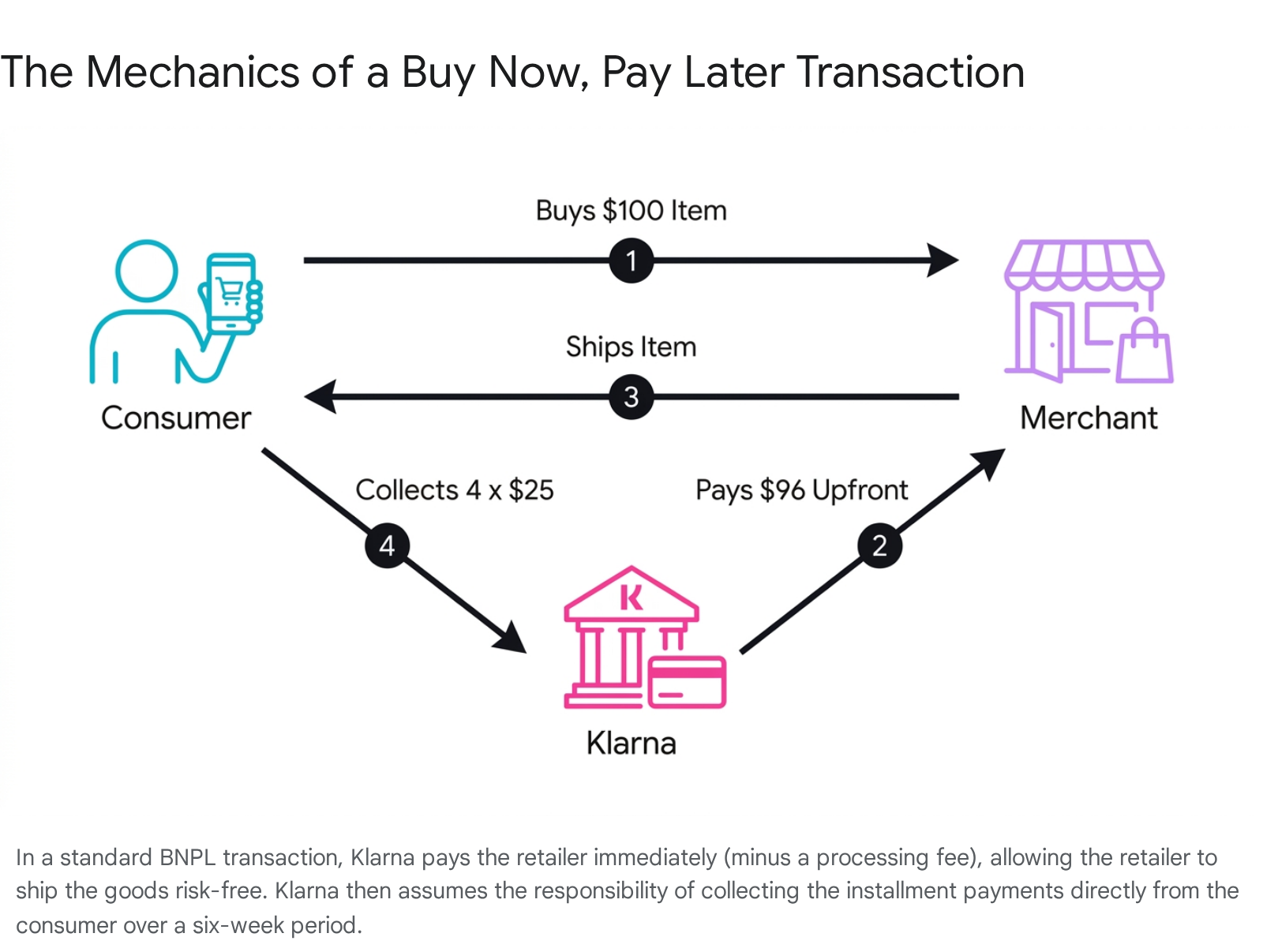

If the user selects Klarna, the transaction flow occurs in a matter of seconds. Klarna performs a frictionless, automated "soft" credit check in the background. This proprietary algorithmic underwriting model analyzes the consumer's purchase history, the cost of the item, the time of day, and basic financial health markers to approve or deny the transaction in real-time 789.

If approved, the transaction mechanics completely isolate the retailer from consumer default. For the merchant, the experience is financially identical to a standard credit card purchase. Klarna pays the merchant the full purchase price upfront, minus a negotiated transaction fee, allowing the merchant to pack and ship the item immediately with guaranteed capital 910. For the consumer, Klarna assumes all responsibility for collections, payment reminders, and repayment tracking 910.

Klarna's Four Primary Payment Products

While Klarna built its reputation on a single primary offering, the company has heavily diversified its payment options into four distinct products to capture a wider array of consumer spending habits and lifecycle needs 5911.

The flagship product is known as "Pay in 4." Under this model, the total cost of the shopping cart is divided into four equal installments. The consumer pays the first 25% upfront at checkout using a linked debit or credit card. The remaining three payments are automatically drafted from that linked account every two weeks over the subsequent six weeks. This option is entirely interest-free, provided the consumer meets the payment schedule 35915.

A second popular option, popularized primarily in European markets, is "Pay in 30 Days." This structure allows a consumer to receive the product, decide if they wish to keep it, and pay the full balance in a single transaction up to 30 days later, again with zero interest. This functionally serves as a risk-free trial period for apparel and consumer goods 359.

For larger, big-ticket purchases, Klarna offers "Fair Financing," sometimes referred to as Pay Over Time. This product shifts away from the traditional BNPL model into conventional point-of-sale installment lending. These loans range from 6 to 36 months in duration. Unlike the Pay in 4 model, Fair Financing is an interest-bearing loan, with Annual Percentage Rates (APRs) ranging from promotional 0% rates up to 35.99%, depending heavily on the user's creditworthiness and the specific merchant agreement 91112.

Finally, Klarna offers a "Pay Now" feature. Functioning similarly to a standard debit transaction or a digital wallet like PayPal, this option allows consumers to pay the full amount instantly using their saved credentials. This keeps the transaction within the Klarna ecosystem, allowing users to track deliveries and manage returns through a unified application 1713.

How Klarna Makes Money: The B2B Engine

A frequent source of consumer confusion is how a financial institution can build a multi-billion dollar enterprise while originating millions of short-term loans that charge absolutely zero interest to the borrower. The answer lies in a highly diversified revenue model that relies fundamentally on B2B (business-to-business) transaction fees, which are increasingly supplemented by a growing consumer credit and services operation.

Merchant Discount Rates (MDR) Explained

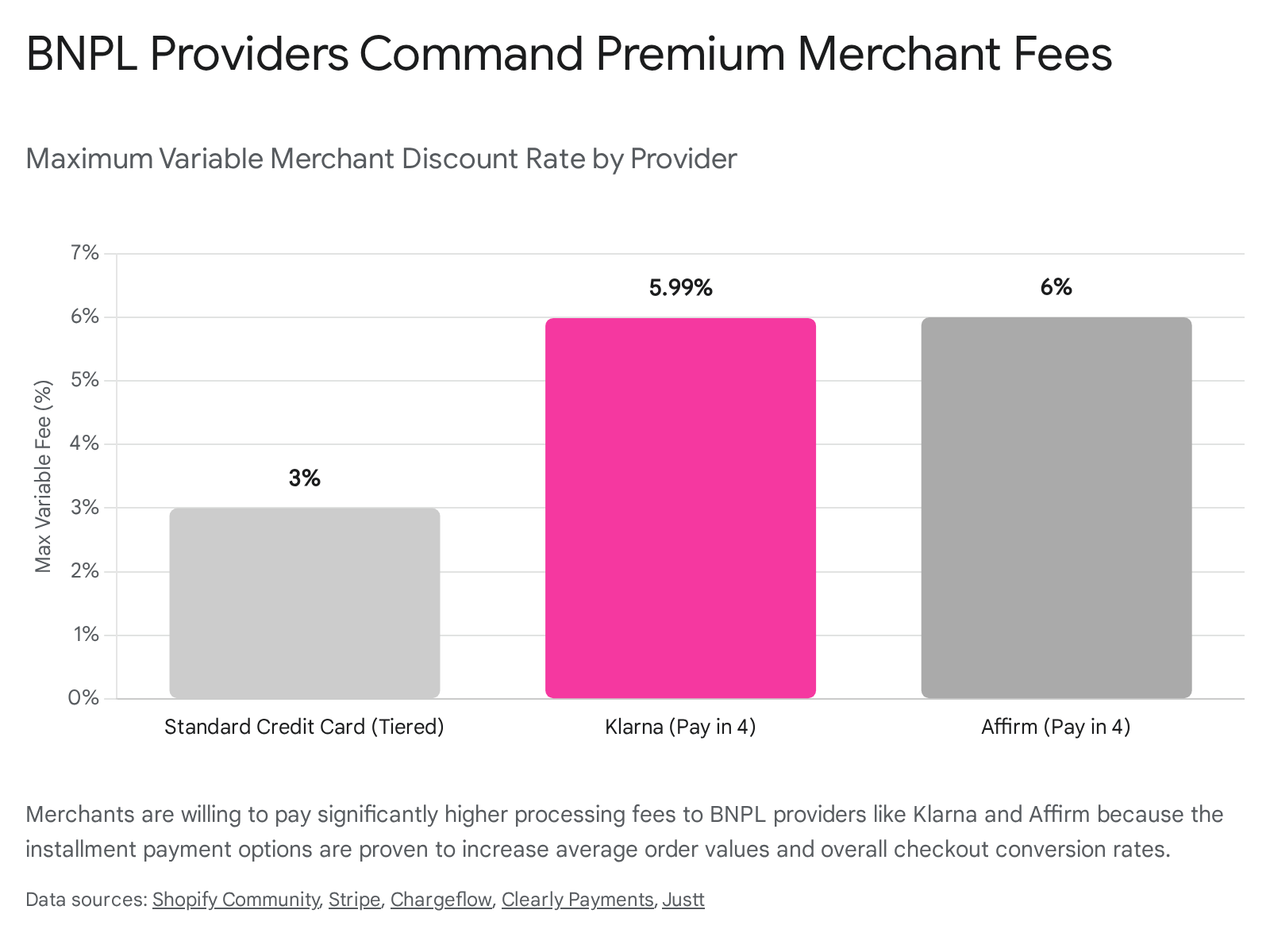

The vast majority of Klarna's revenue - accounting for approximately 57% of its total income - is generated directly from the retailers that embed its service 717. Every time a consumer completes a checkout using Klarna, the retailer surrenders a percentage of the sale. In the payments processing industry, this is formally known as the Merchant Discount Rate (MDR) 1920.

Traditional credit card processors and payment gateways, such as Visa, Mastercard, or standard Stripe integrations, typically charge merchants an MDR ranging from 1.5% to 3.0% per transaction, plus a small flat fee 2014. By contrast, BNPL providers command a significant premium for their services. For its core Pay in 4 product, Klarna generally charges merchants a fixed fee of $0.30 plus a variable percentage that ranges from 3.29% up to 5.99% of the total transaction volume 51523. This rate fluctuates based on the specific merchant's contract, total sales volume, and the geographic location of the consumer 1516. Competitors in the space command similar or even higher premiums; Affirm, for example, charges an average merchant transaction fee of approximately 6.0% plus $0.30 per purchase 17.

To illustrate the unit economics: If a consumer purchases a $100 item using Klarna's Pay in 4 on a Shopify storefront, the consumer pays exactly $100 over a six-week schedule. Klarna, however, will deduct its fee - for instance, a $0.30 fixed fee plus a 2.9% variable fee, totaling $3.20 - and remit the remaining $96.80 to the retailer 15. If the transaction is cross-border, Klarna may assess additional currency conversion or cross-border processing fees 1516.

Why Retailers Pay Premium Fees

A fundamental question arises: why would retailers willingly surrender a cut of their profit margins up to twice as large as standard credit card processing fees? The answer lies in consumer psychology and the direct impact on top-line revenue.

Extensive industry data proves that offering BNPL services dramatically increases the "Average Order Value" (AOV) and significantly reduces cart abandonment rates 81819. When a $200 purchase is mentally framed to the consumer as "just $50 today," shoppers are statistically much more likely to complete the checkout process and frequently add incremental items to their cart 5. Consequently, merchants do not view Klarna's higher fees merely as an inflated payment processing cost, but rather as a highly efficient marketing and customer acquisition expense. Klarna essentially acts as a conversion engine, and the premium MDR is the price retailers pay for guaranteed incremental sales 820.

The Pivot to Consumer Revenue: Interest and Fees

While merchant fees built the foundation of the company, Klarna has recently executed a massive strategic pivot to diversify its revenue streams. The company has aggressively expanded its consumer-facing financial products, recognizing that merchant fees alone cannot sustain the valuation expectations of public markets.

Fair Financing and Interest Income

The most significant shift in Klarna's revenue profile is the aggressive scaling of its "Fair Financing" product. As of early 2026, interest income - generated almost exclusively from these long-term consumer loans - accounts for approximately 24% of Klarna's total revenue 17.

Fair Financing operates similarly to a traditional personal loan or a high-interest credit card, allowing consumers to finance big-ticket items over extended periods 915. The interest rates on these products are substantial; depending on the consumer's credit profile, these loans carry APRs up to 35.99% 91112. This pivot has been highly lucrative and central to Klarna's path to profitability. In its Q4 2025 financial results, Klarna reported that Fair Financing Gross Merchandise Volume increased by an astonishing 165% year-over-year, indicating rapid adoption of interest-bearing debt by its user base 62122.

However, this transition fundamentally alters the company's risk profile. While Fair Financing yields higher structural margins and take rates than the traditional Pay in 4 product, it requires greater upfront provisioning and exposes Klarna to severe consumer default risks over a much longer duration 2324.

The Logic and Caps Behind Late Fees

Another controversial but critical component of Klarna's consumer revenue comes from late payment penalties. If a consumer misses a scheduled installment payment, Klarna assesses a fee. In the United States, this fee is typically up to $7 per missed payment 725.

The history of these fees is notable. For years, Klarna did not charge late fees in the United Kingdom, viewing it as a customer-friendly differentiator. However, in 2023, the company reintroduced a £5 late fee 253426. Klarna executives stated that internal data revealed a "total absence of late fees actually leads to less favorable outcomes for customers," as consumers were more likely to overextend themselves without a financial deterrent to missing payments 27.

To prevent consumers from falling into compounding debt spirals, Klarna institutes strict caps. Late fees can never exceed 25% of the total order value, and generally, no more than two late fees can be applied to a single retail order 2534. Furthermore, Klarna launched a "Customer Recovery Programme" to proactively contact users with long-overdue balances, offering to waive 50% of the debt if they engage and clear the remaining balance 342627. While Klarna maintains that 99% of its payments are made on time globally, the sheer scale of the network meant that late fees and small consumer charges still generated approximately $254 million in 2024 7.

Affiliate Marketing, Advertising, and Interchange Fees

The remainder of Klarna's revenue is synthesized through an array of digital marketing initiatives and banking products. With over 118 million active global users natively browsing the Klarna app, the platform essentially functions as an enclosed search engine for commerce 456. Retailers pay Klarna heavily for sponsored placements, targeted incentives, and affiliate marketing, allowing brands to reach high-intent shoppers directly within the Klarna ecosystem 5817.

Additionally, Klarna has entered the physical card space by issuing Visa debit cards. When a consumer uses a Klarna card at a store that is not officially integrated with Klarna's merchant network, the transaction is processed over the standard Visa network. In these instances, Klarna earns a fraction of a percent of the transaction value - known as an interchange fee - which is paid by the merchant's acquiring bank 52337. Furthermore, for highly engaged power users, Klarna introduced a premium subscription tier, Klarna Plus, priced at $7.99 per month in the U.S., offering exclusive discounts and waived service fees 7.

Klarna's Transformation From Payments Widget to Global Bank

To sustain its valuation and deepen its monetization of individual users, Klarna has fundamentally evolved its corporate identity. It is no longer accurately described as merely a payments widget; it is operating as a fully licensed global digital bank 42328.

The European Deposit Model

In Europe, Klarna secured a full banking license from the Swedish Financial Supervisory Authority in 2017, empowering the company to operate as a bank across the European Union 52839. This license allows Klarna to hold consumer deposits and issue proprietary financial products. By offering competitive interest rates, Klarna successfully attracted billions in consumer capital. As of mid-2026, European consumers have entrusted the company with over $12.3 billion in deposits across eleven markets 294130. In Sweden, these accounts offer interest rates up to 3.58% 2831.

Expanding High-Yield Savings to the United States

Building on its European success, Klarna aggressively pushed its banking model into the United States. In June 2026, the company announced the launch of FDIC-insured Klarna Savings accounts for American consumers. Because Klarna does not hold a direct U.S. banking license, these accounts are provided and held through a strategic partnership with Utah-chartered WebBank 284130.

These accounts launched with highly competitive Annual Percentage Yields (APY) starting at 3.28% for balances up to $50,000, requiring users to maintain active membership to receive the boosted rate 4130. The strategic imperative behind this launch is ecosystem retention. By offering savings accounts, checking balances, and a physical debit card, Klarna seeks to become the primary financial hub for its users, preventing capital from leaving its app 52830.

The economic data validates this strategy. By deepening the relationship beyond a simple checkout transaction, Klarna dramatically increases user lifetime value. As of Q4 2025, Klarna's "banking consumers" - defined as those actively utilizing savings accounts, the Klarna Card, or Fair Financing - grew 101% year-over-year to 15.8 million users. Crucially, these banking consumers generated $107 in annual revenue per user, more than triple the $30 generated by the average checkout-only consumer 62122.

This pivot to high-value banking consumers has been paired with aggressive internal cost-cutting measures driven by artificial intelligence. By heavily integrating generative AI across its operations, Klarna reduced its global headcount by nearly 49% from 2022 to early 2026. Consequently, revenue per employee skyrocketed to approximately $1.4 million, enabling the company to report consecutive quarters of adjusted operating profit 6132021.

Behind the Scenes: Funding a Multi-Billion Dollar Loan Book

Originating billions of dollars in consumer loans requires access to immense pools of capital. How Klarna funds its lending operations differs drastically depending on the geographic region, highlighting the complex financial engineering underpinning the BNPL model.

The Advantage of High Capital Velocity

A BNPL business model is highly working-capital intensive. Klarna must pay the retail merchant on day one, but it does not fully recoup that capital from the consumer until roughly 40 days later 181932. However, this remarkably short duration is actually a profound structural advantage over traditional credit cards or mortgages.

An average loan duration of 40 days means Klarna can recycle the exact same pool of capital roughly nine times within a single fiscal year 1833. This rapid "capital velocity" allows the company to generate massive transaction volumes and associated merchant fees on a relatively light balance sheet, reacting swiftly to shifting macroeconomic conditions 183233. In Europe, where it possesses a banking license, Klarna funds the vast majority of these short-term loans using its $12.3 billion in consumer deposits, providing the company with an incredibly cheap cost of capital 233246.

Securitization and the $6.5 Billion Elliott Agreement

In the United States, which has grown to become Klarna's largest single market (generating over $42 billion in GMV in 2024), the company lacks a direct banking license and cannot utilize consumer deposits to fund its loans 33. Instead, Klarna relies heavily on Wall Street institutional funding through securitizations and "forward flow agreements" 23334634.

A forward flow agreement is a financial arrangement wherein an institutional investor agrees to purchase a steady, ongoing stream of loans from an originator at a pre-agreed price. This mechanism is critical for Klarna's expansion. In November 2025, Klarna executed a landmark $6.5 billion forward flow agreement with investment funds managed by Elliott Investment Management, specifically targeting Klarna's U.S. Fair Financing loans 353650.

Under the mechanics of this deal, as Klarna originates new long-term Fair Financing loans to American consumers, it continuously sells those receivables to Elliott's funds on a rolling basis. The facility size is technically $1 billion, but because the underlying assets amortize rapidly, new loans continuously enter the facility, resulting in an expected $6.5 billion in total originations over the two-year term 353650.

This structure is highly advantageous for Klarna. It provides scalable, off-balance-sheet funding, allowing Klarna to instantly achieve asset derecognition and release capital 233435. By offloading the credit risk to institutional investors, Klarna frees up its capital to originate more loans and secures immediate revenue realization, while still maintaining control over the consumer relationship and servicing the loans 343650.

The Consumer Impact: Credit Scores and "Shadow Debt"

While BNPL is heavily marketed as a safer, transparent alternative to predatory revolving credit cards, the reality of its impact on consumer financial health is complex. The friction-free nature of BNPL can easily facilitate overspending, as consumers stack multiple installment loans simultaneously.

If a consumer lacks sufficient funds in their linked checking account when Klarna initiates an automatic bi-weekly withdrawal, the consumer's bank will frequently assess a Non-Sufficient Funds (NSF) or overdraft fee - which can run up to $35 per occurrence 51. Consumer advocates argue this represents a severe hidden cost of the service 51. Furthermore, if a consumer ignores the initial grace period and continues to miss payments, Klarna will suspend their account to prevent further borrowing. If the debt remains unpaid for a prolonged period, the account is transferred to a third-party debt collection agency 3452.

Does BNPL Build or Hurt Your Credit Score?

The relationship between BNPL usage and the major credit reporting agencies (Experian, Equifax, and TransUnion) remains highly fragmented in 2026. Historically, BNPL providers fiercely resisted reporting payment data to credit bureaus. This meant that responsible users could not build positive credit history, but it also resulted in BNPL debt functioning as "shadow debt" - financial obligations entirely invisible to mortgage lenders or auto financiers assessing a borrower's total debt load 53.

As of 2026, the credit reporting rules vary drastically based on the specific BNPL product utilized: * Pay in 4: Most standard, short-term Pay in 4 installment loans are not routinely reported to the three major credit bureaus as active tradelines 3738. Consequently, consistent on-time payments on these micro-loans will generally not build or boost a consumer's FICO score. * Fair Financing: Conversely, if a consumer applies for a longer-term, interest-bearing loan (such as a 24-month Klarna financing plan), this application triggers a hard credit inquiry. These longer-term loans are routinely reported to the credit bureaus and act exactly like traditional personal loans on a credit file 1538. * Defaults and Collections: Regardless of the product used, if a consumer severely defaults and the account is officially sent to a third-party collections agency, that derogatory mark will almost certainly be reported to the bureaus, inflicting severe and lasting damage on the consumer's credit score 345238.

This opaque ecosystem has drawn the ire of federal lawmakers. In May 2026, U.S. Senators Elizabeth Warren, Richard Blumenthal, Tammy Duckworth, and Mazie Hirono launched a probe into the major credit reporting companies, demanding clarity on how BNPL data is being ingested and scored 39. The Senators highlighted that the uneven reporting leaves consumers in a state of limbo and obscures true consumer leverage from the broader financial system 39. In response, FICO has introduced updated scoring models designed to specifically incorporate BNPL payment history, though the widespread adoption of these new models by everyday lenders remains a slow, ongoing process 37.

The Regulatory Reckoning Facing the BNPL Industry

The explosive, largely unregulated growth of the BNPL sector over the past five years has inevitably invited intense scrutiny from global financial watchdogs. Regulators increasingly fear that the seamless nature of digital installments is ushering a new generation of consumers - particularly younger demographics without established credit histories - into unsustainable cycles of debt 3440.

The UK Financial Conduct Authority's 2026 Crackdown

In the United Kingdom, the government has moved aggressively to codify oversight. The Financial Conduct Authority (FCA) announced that beginning precisely on July 15, 2026, all BNPL providers (referred to regulatorily as Deferred Payment Credit, or DPC) will be brought firmly under the formal regulatory perimeter 414243.

This sweeping legislation mandates that firms like Klarna can no longer operate outside traditional lending frameworks. Providers must carry out strict affordability and creditworthiness assessments before offering installment loans to UK shoppers 4344. Furthermore, BNPL operators will be subject to the FCA's overarching "Consumer Duty," requiring them to deliver clear precontract information, transparent terms, and robust support for customers facing financial difficulty 434445. Crucially, UK consumers will gain the explicit right to escalate unresolved disputes with BNPL firms directly to the Financial Ombudsman Service, matching the robust protections afforded to traditional credit card users 43.

To facilitate this transition, the FCA instituted a Temporary Permissions Regime (TPR). BNPL firms that were operating as of July 2025 were required to notify the FCA and pay a £280 registration fee to continue temporarily operating after the July 2026 deadline while their full authorization applications are processed 414244.

The US CFPB's Shifting Mandates

In the United States, the regulatory environment is characterized by significantly more volatility and legal wrangling. In May 2024, the Consumer Financial Protection Bureau (CFPB) issued an aggressive interpretive rule that essentially classified BNPL digital user accounts as "credit cards" under the federal Truth in Lending Act (Regulation Z) 4647. This ruling was designed to force BNPL providers to offer identical legal protections as legacy card issuers, including mandatory dispute investigation procedures, guaranteed refunds for returned products, and the issuance of periodic billing statements detailing all applicable fees 46.

However, in a stunning policy reversal just twelve months later, the CFPB formally withdrew the interpretive rule in May 2025 474849. Following intense lobbying and legal challenges from the Financial Technology Association, the CFPB conceded in a court filing that the rule was "procedurally defective" 47. The Bureau admitted that retrofitting rigid open-end credit card regulations onto BNPL products - which are fundamentally structured as closed-end installment loans - was an ill-fitting approach that placed substantial burdens on the industry while providing little tangible benefit to consumers 47. Consequently, the U.S. BNPL market currently operates in a regulatory gray area, with the CFPB stating it will instead rely on targeted enforcement actions rather than sweeping new interpretive rules 48.

Macroeconomic Headwinds and the 2025 Klarna IPO Crisis

The regulatory uncertainty in the U.S. has been heavily compounded by severe macroeconomic headwinds that have tested the resilience of the entire fintech sector. Klarna officially went public on the New York Stock Exchange in September 2025, pricing its highly anticipated Initial Public Offering (IPO) at $40 a share and achieving a valuation of approximately $15 billion 20376750.

The timing of the public debut proved immensely challenging. The broader technology market was already under heavy pressure from rising inflation data and escalating fears of a global recession. These economic anxieties were severely exacerbated by aggressive trade tariffs instituted on Canada, China, and Mexico following the 2025 U.S. presidential inauguration, creating a highly volatile environment for consumer-facing retail stocks 20.

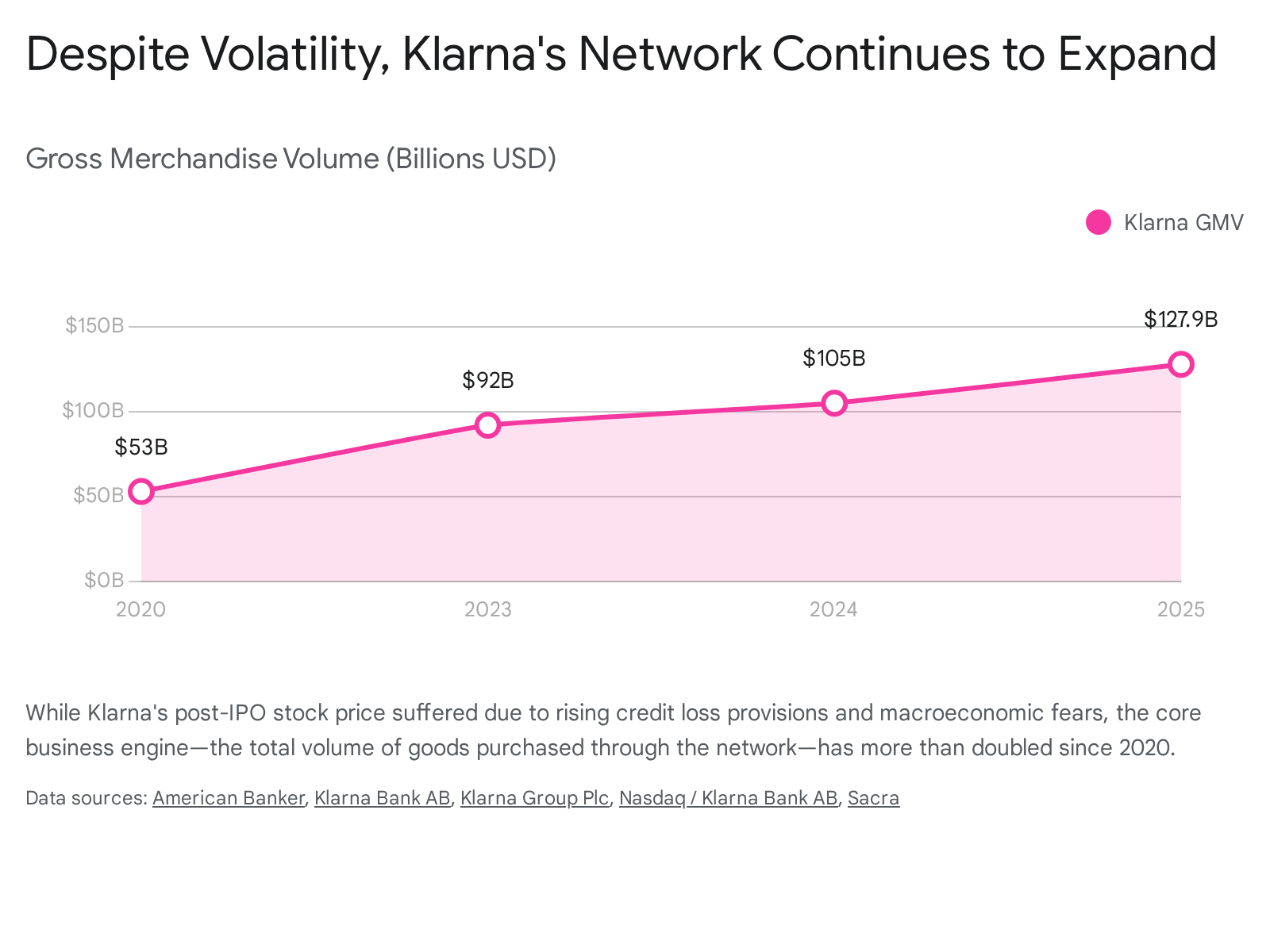

More critically, however, Klarna's own post-IPO financial disclosures profoundly spooked institutional investors. On November 18, 2025, just weeks after completing the offering, Klarna released its third-quarter financial results. The report revealed a staggering 102% year-over-year spike in provisions for credit losses, indicating that a significantly higher percentage of consumers were defaulting on their installment loans than the market had anticipated 5350. This revelation sent the stock into an immediate tailspin. By early 2026, Klarna's shares had plummeted roughly 70% from their $40 IPO price, languishing near $16 per share and erasing billions in market capitalization 4151.

The Nayak v. Klarna Securities Class Action

This dramatic collapse in shareholder value swiftly triggered aggressive legal action. In December 2025, a massive securities class action lawsuit - styled Nayak v. Klarna Group plc - was filed in the U.S. District Court for the Eastern District of New York 5052.

The plaintiffs, representing investors who purchased shares during the IPO, allege that Klarna, its senior executives, and its underwriters explicitly violated Sections 11, 12(a)(2), and 15 of the Securities Act of 1933 6752. The core of the legal complaint argues that Klarna's IPO registration statement and prospectus were materially false and misleading. Specifically, investors claim that management intentionally understated the severe risk that credit loss reserves would surge, despite knowing the precarious risk profile of their underlying loan portfolio 535271.

A highly scrutinized element of the lawsuit focuses on the phenomenon of "fast food financing" 53. Plaintiffs contend that in its relentless pursuit of pre-IPO growth metrics, Klarna aggressively extended credit to financially unsophisticated and vulnerable consumers to finance small, non-durable daily essentials, such as food delivery 5350. The lawsuit alleges that Klarna failed to disclose that its internal risk modeling was fundamentally unprepared for a shifting macroeconomic environment, effectively gamifying debt to inflate revenue figures while concealing the accumulation of toxic "shadow debt" 5352. As of mid-2026, the litigation remains active, with the court establishing a February 20, 2026 deadline for investors to petition as lead plaintiffs 675071.

Despite these intense market pressures and legal battles, the underlying machinery of Klarna's business remains robust. The company reported $127.9 billion in Gross Merchandise Volume and $3.5 billion in total revenue for the full year 2025, ultimately swinging to a modest adjusted operating profit of $65 million, proving that consumer appetite for frictionless digital credit remains voracious despite the systemic risks 4.

Bottom line

Klarna operates a highly sophisticated financial network that leverages the psychological appeal of delayed payment to dramatically boost retail sales conversion rates. While the company historically derived its revenue almost entirely through premium B2B merchant transaction fees, it is now deeply reliant on consumer-facing interest from long-term financing and late fees to sustain its valuation and profitability. While BNPL offers genuine convenience and interest-free terms for highly disciplined shoppers, the rapid expansion of these loans into everyday consumables, paired with rising credit default rates, highlights the profound systemic risks inherent in frictionless digital lending.