Plaid Valuation Recovery and Open Banking Infrastructure Economics

The Visa Acquisition Failure and Valuation Trajectory

The trajectory of Plaid's corporate valuation serves as a comprehensive barometer for the structural evolution of the broader open-banking infrastructure sector. In January 2020, Visa announced a definitive agreement to acquire Plaid for a total purchase consideration of $5.3 billion 12. Visa's strategic rationale was deeply tied to its "network of networks" strategy, aiming to neutralize the emerging threat of account-to-account (A2A) and Payment Initiation Services (PIS) that bypassed traditional four-party card rails 23. Plaid's infrastructure, while historically focused on data aggregation, possessed the foundational architecture to facilitate direct consumer-to-business (C2B) payments, posing a long-term disintermediation risk to Visa's core debit and credit card volumes 13.

The acquisition was ultimately abandoned following antitrust litigation initiated by the United States Department of Justice, which successfully argued that Visa's acquisition was a defensive maneuver intended to extinguish a nascent competitive threat to its online debit monopoly. Following the deal's collapse, Plaid capitalized on a period of peak macroeconomic liquidity and fintech acceleration, securing a Series D funding round in 2021 that valued the enterprise at $13.4 billion 4.

By 2026, amid broader capital market contractions, rising interest rates, and a shift in investor focus from top-line expansion to sustainable unit economics, Plaid had successfully stabilized its business model. The company demonstrated substantial valuation recovery, generating approximately $546 million in annual recurring revenue (ARR) with an estimated 40% year-over-year growth rate 44. Crucially, the firm achieved adjusted EBITDA profitability, insulating it from the venture capital retrenchment that severely impacted its fintech peers 4. Industry projections and capital market discussions currently place the company on a trajectory for an initial public offering (IPO) valued between $8 billion and $10 billion 4.

This valuation recovery is not merely a product of market cyclicality but rather the result of a fundamental strategic pivot. Plaid transitioned from a commoditized data-aggregation utility reliant on screen scraping to a diversified financial infrastructure platform providing risk decisioning, identity verification, and multi-rail payment orchestration 456.

| Milestone Date | Strategic Event | Enterprise Valuation / Metric | Market Implication |

|---|---|---|---|

| January 2020 | Visa Acquisition Announcement | $5.3 Billion | Highlighted incumbent payment networks' recognition of open banking as a systemic threat to card interchange revenues 12. |

| October 2020 | UK CMA Investigation | N/A | UK Competition and Markets Authority analyzed Plaid's nascent PIS capabilities as a direct threat to Visa's C2B market share 3. |

| 2021 | Series D Funding Round | $13.4 Billion (Peak) | Reflected peak venture capital enthusiasm for API infrastructure during the pandemic-era fintech boom 4. |

| Mid-2024 | Strategic Pivot to ML Models | N/A | Introduction of foundational AI models shifted focus from raw data pipes to actionable underwriting and fraud intelligence 56. |

| Mid-2026 | Pre-IPO Revenue Stabilization | ~$546M ARR (40% YoY Growth) | Transition to adjusted EBITDA profitability and enterprise customer acquisition re-anchors valuation in the $8B - $10B range 4. |

Core Economic Model and Pricing Architecture

The underlying unit economics of financial data aggregation dictate the strategic imperatives of open-banking providers. Plaid's historical business model relied heavily on facilitating the initial connection between a consumer's bank account and a third-party application, followed by the continuous retrieval of transaction data. By 2026, the company's revenue streams had diversified significantly to reflect its expanded product suite, which now includes identity verification, real-time risk scoring, and payment processing.

Plaid's revenue architecture is fundamentally usage-based, characterized by pricing models highly customized to the specific product configuration utilized by the client application. The infrastructure provider segments its pricing into three primary modalities: one-time fee products, which incur a single charge upon the initial connection of a financial account; subscription products, which assess a recurring monthly fee for the maintenance of a connected account; and per-request products, which levy a flat fee for every successful API call executed by the client 7.

Usage Tiers and API Call Benchmarks

To accommodate varying scales of operation, Plaid enforces a tiered access model. For early-stage development, the platform provides a completely free Sandbox environment featuring unlimited API calls against simulated financial institutions 9. A Limited Production tier allows developers to conduct up to 200 API calls utilizing live bank data at no cost 79. However, commercial deployment requires transition to full Production access, which is structured across three primary commercial plans: Pay-as-you-go, Growth, and Custom (or Scale) 89.

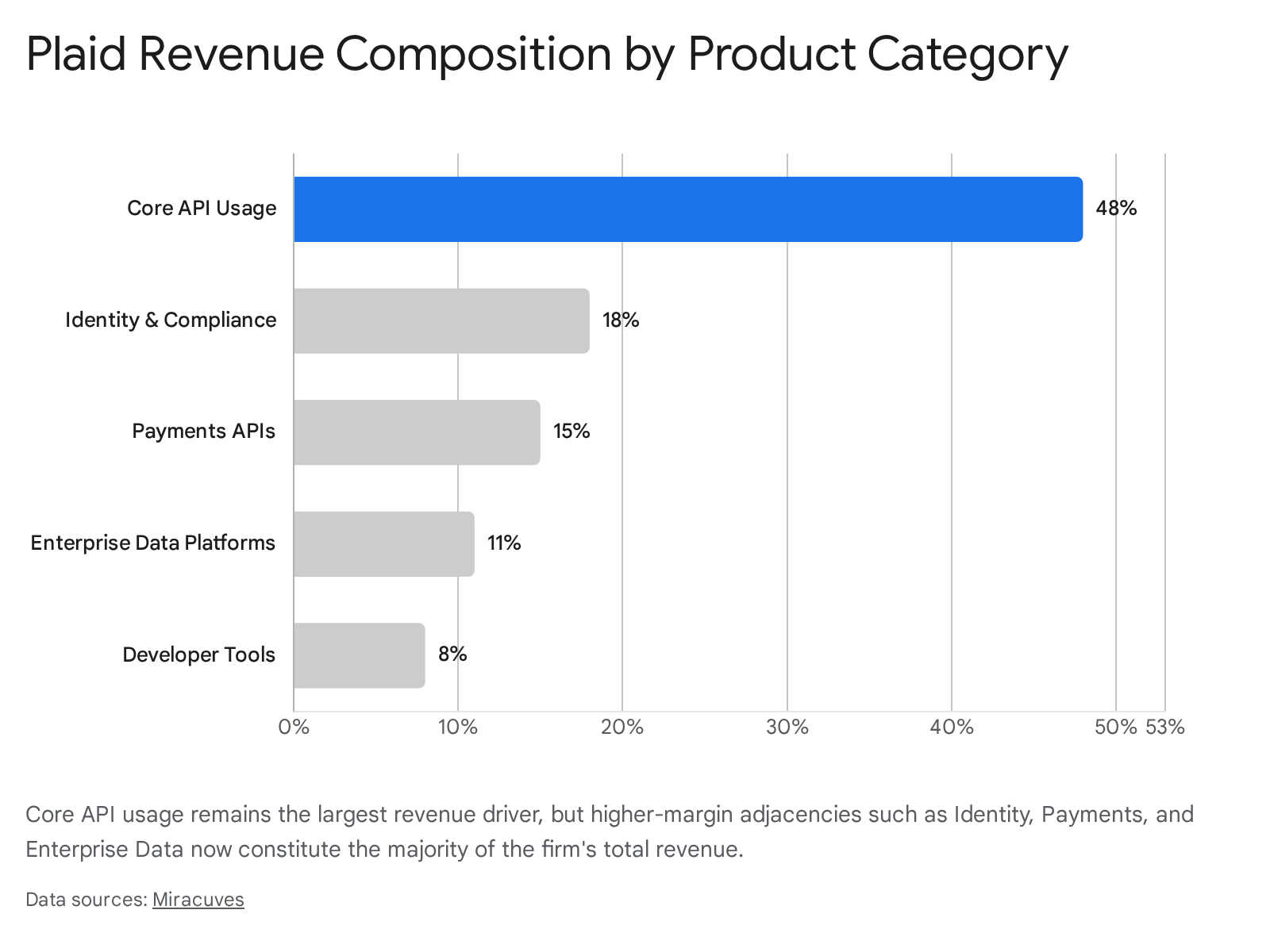

The core data connectivity business, representing an estimated 48% of total revenue, relies heavily on per-API-call and per-user pricing mechanics 12.

Published baseline pricing and aggregated transaction data from procurement platforms indicate that products like Auth, which enables fundamental account and routing number verification for ACH payments, range from $0.10 to $0.25 per successful call 10. Accessing historical transaction data via the Transactions product typically ranges from $0.30 to $0.60 per call 10. For identity verification products, costs scale between $0.15 and $0.30 per call 10. Enterprise customers processing substantial volumes (e.g., exceeding 10,000 calls per month) transition to the Custom/Scale tier, negotiating aggressive volume discounts in exchange for monthly minimum commitments that range from $1,000 to over $10,000 10.

Bank API Access Fees and Margin Compression

The historical margin advantage of data aggregators relied on free access to consumer data, primarily achieved through legacy credential-based screen scraping techniques. However, as the industry transitions to secure, standard-setting API environments - specifically Open Authorization (OAuth) and protocols developed by the Financial Data Exchange (FDX) - major financial institutions are leveraging their structural position to impose explicit data access fees on aggregators 411.

In 2025, JPMorgan Chase initiated a pricing structure that fundamentally altered the unit economics of the aggregation sector. The bank introduced a fee of approximately $1.50 per authorization token for each data requestor endpoint, coupled with a volume-tiered data request fee ranging from $0.05 to $0.20 per API call 4. Crucially, the pricing model is inherently surgical: if any request involves payment-related activities, all subsequent requests for that specific counterparty default to higher, payment-tier pricing without the ability to selectively cherry-pick lower-cost data endpoints 4.

This dynamic severely compresses the gross margins of pure-play aggregation platforms. When the originating depository financial institution (ODFI) fees are combined with direct bank API access fees and Plaid's own aggregation markup, the total cost of executing a transaction approaches parity with established card network rails like Visa Direct 4. Consequently, the inherent cost advantage of ACH over card rails begins to evaporate. To maintain adjusted EBITDA profitability, Plaid faces a structural dilemma: it must either pass these access costs downstream to fintech developers - who operate under their own stringent margin constraints - or aggressively offset the access fees by cross-selling higher-margin risk, intelligence, and analytics products 4.

The Strategic Pivot: From Raw Connectivity to Artificial Intelligence

Recognizing the commoditization of raw data connectivity and the margin pressure induced by institutional API fees, Plaid systematically repositioned itself as an intelligence and orchestration layer. This strategic pivot required the deployment of proprietary machine-learning models trained on the vast network effects generated by over 150 million connected consumers and nearly one million daily network connections 512.

By moving into credit decisioning and fraud prevention, Plaid targets enterprise clients - such as major auto lenders, tax preparation firms like H&R Block, and mortgage originators like Rocket Mortgage - who require sophisticated decision-making tools that traditional card networks do not natively provide 4.

Foundational Machine Learning Models

In May 2026, Plaid deployed dual foundational AI models to process financial data simultaneously at two distinct levels 6. The first model, focused on Transaction Classification, analyzes individual transactions by their specific metadata attributes to accurately identify the nature of deposits (e.g., distinguishing a salary deposit from a standard peer-to-peer transfer) or the nature of outflows (e.g., categorizing a debit as a loan repayment) 6. The second model performs Sequential Analysis, evaluating the chronological timeline of a user's transactions over extended periods to determine whether a sequence of money movement aligns with routine behavior or flags as anomalous 6. When integrated into Plaid's existing architecture, these models immediately boosted primary categorization accuracy by 13% and delivered 89% precision on income classification 6.

Predictive Underwriting and Credit Decisioning

Traditional credit assessment and fraud detection systems predominantly rely on lagging indicators, such as 30-day delinquency reports issued by traditional credit bureaus, which fail to capture an applicant's real-time financial capacity 512. To capture this market, Plaid developed LendScore, a real-time credit risk score designed specifically for modern underwriting.

LendScore looks beyond static credit histories to evaluate real-time cash flow, income variability, and network-wide account activity across the Plaid ecosystem. The proprietary model (LS1) is built upon hundreds of individual attributes to predict 12-month default risk. Internal corporate benchmarks indicate that incorporating LendScore alongside traditional credit bureau data delivers a 25% lift in predictive accuracy 51213. Concurrently, the platform deployed the Cash Advance Index, a highly specialized, real-time scoring system (ranging from 1 to 99) designed specifically for short-term liquidity providers. This tool predicts the exact likelihood of a user repaying a cash advance within a 30-day window, resulting in early pilot data showing an 8% reduction in delinquency rates without negatively impacting overall approval rates 6.

Network-Level Fraud Prevention and Orchestration

As authorized push payment (APP) fraud and account takeover attacks escalate, Plaid leveraged its network density to introduce advanced fraud orchestration through its Protect suite, powered by the Trust Index 2 (Ti2) machine learning model 513.

The Ti2 architecture represents a 30% increase in fraud detection efficacy compared to its predecessor 1213. It achieves this by moving beyond single-account analysis to execute live, network-wide graph analysis. This capability detects patterns of shared risk across disparate users, devices, accounts, and applications, effectively surfacing hidden connections indicative of sophisticated fraud rings that remain invisible to applications analyzing their user base in isolation 512. By providing these deep behavioral signals prior to onboarding, Plaid embeds itself directly into the compliance and risk architecture of its enterprise clients, creating a highly sticky revenue stream insulated from the pricing wars of basic data aggregation.

Pay-by-Bank Economics and Guaranteed Settlement

The most significant driver of Plaid's total addressable market expansion - and the primary catalyst for its valuation recovery - is the facilitation of direct account-to-account (A2A) payments, commonly referred to as Pay-by-Bank 1415. As merchants across retail, e-commerce, and bill payment sectors face relentless margin pressure from rising credit card interchange rates, direct bank payments offer an essential cost-reduction strategy 16.

Structural Cost Advantages of ACH and RTP

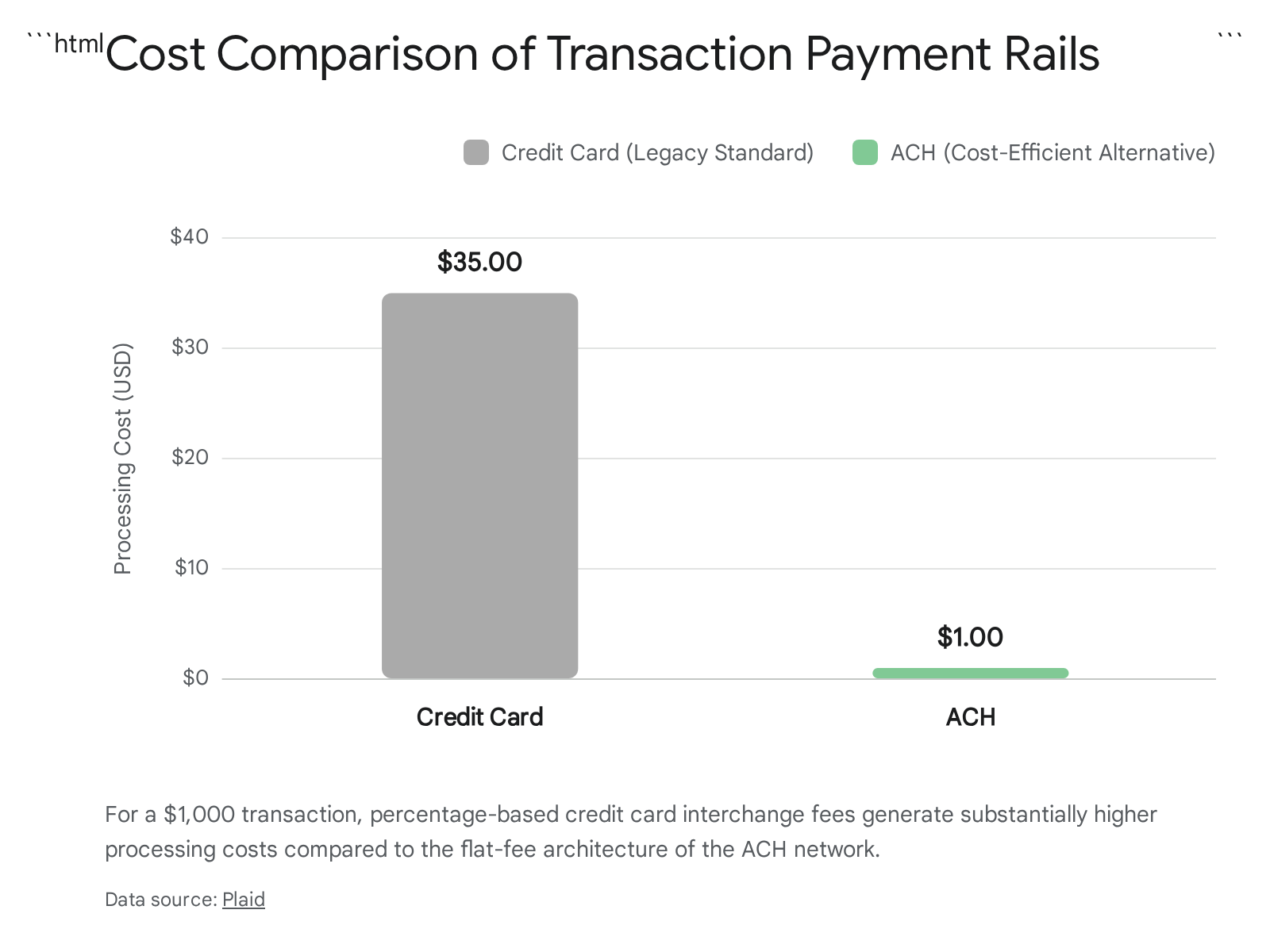

The Automated Clearing House (ACH) network and Real-Time Payments (RTP) rails operate on fundamentally different economic principles than the four-party card networks operated by Visa and Mastercard. Card networks utilize a percentage-based interchange fee structure, which functions theoretically as a transfer payment to internalize externalities and incentivize card issuance and consumer rewards 161718. In recent years, U.S. merchants have observed total credit card processing rates climb to 3.2% to 4.0% per transaction, severely impacting net profitability 16.

Conversely, the ACH system operates on a highly predictable, low flat-fee model 16. According to data from the National Automated Clearing House Association (NACHA), the baseline cost of an ACH transaction ranges from $0.26 to $0.50, though commercial processing fees may range slightly higher 19. Plaid's internal data highlights the stark disparity for enterprise merchants: a $1,000 credit card transaction may cost a merchant up to $35 in fees, whereas processing the identical transaction via ACH typically incurs a flat fee well under $1.50 1620.

By shifting volume from card networks to Pay-by-Bank workflows utilizing Plaid's infrastructure, businesses observe a 20% to 70% reduction in processing costs, with an average overall reduction of 40% across Plaid's merchant base 1621. However, this shift is heavily dependent on overcoming consumer habituation. Internal studies indicate that adoption is largely driven by youth demographics and the UX convenience of OAuth integration, where offering a mere 1% discount at checkout can yield a 2x to 3x lift in Pay-by-Bank selection by the consumer 1522.

Plaid Transfer and Guaranteed Payments

Despite the undeniable cost advantages, traditional ACH suffers from severe asynchronous settlement delays. Standard ACH settles on a T+1 or T+2 timeline, introducing significant friction into modern digital applications that require instant fund availability, and exposing merchants to insufficient funds (NSF) return risk during the delayed settlement window 2023.

To resolve this operational bottleneck, Plaid developed Transfer, a comprehensive multi-rail payment orchestration product 24. The Transfer API abstracts the complexity of payment routing, supporting standard ACH, Same-Day ACH, the RTP network, and FedNow through a single endpoint 2324. Merchants utilize the platform's Dashboard and robust webhook ecosystem to monitor granular transfer lifecycles, ingesting real-time event updates as payments transition from pending to posted, and ultimately to settled or returned 2325.

In a highly strategic move to directly challenge card networks, Plaid introduced a Guaranteed Payments service in May 2026, fundamentally overhauling the ACH network's inherent limitations 6. Under this framework, Plaid evaluates ACH transactions instantaneously using its Signal risk model and deep chronological behavior analysis. If Plaid authorizes the transfer, the partner application is empowered to credit the end-user immediately, replicating the instant authorization experience of a credit card 6. Crucially, if the payment subsequently fails during the asynchronous clearing period - due to administrative errors or overdrawn accounts - Plaid assumes full financial liability and absorbs the loss 6. This financial backstop effectively removes the final barrier to ACH adoption for merchants, transforming slow, flat-fee bank rails into a viable substitute for expensive, high-margin card networks.

The U.S. Regulatory Landscape and Section 1033 Litigation

The transition from a highly fragmented, market-led open finance ecosystem to a formalized open banking framework in the United States hinges entirely on the implementation of Section 1033 of the Dodd-Frank Wall Street Reform and Consumer Protection Act 2627. The statute theoretically codifies a consumer's right to access their financial data and authorize third parties to retrieve it 2728.

CFPB Section 1033 Final Rule and Litigation Timeline

In October 2024, after years of dormancy, the Consumer Financial Protection Bureau (CFPB) published the final Personal Financial Data Rights rule, intending to establish a binding framework with a staggered compliance schedule running from 2026 to 2030 2629. The rule ostensibly mandated that banks, credit card issuers, and other financial institutions provide free data transfer to authorized third parties through standardized, secure APIs, simultaneously recognizing the Financial Data Exchange (FDX) as the official standard-setting body 262729.

However, the rule's implementation encountered severe and immediate legal injunctions from the banking sector. On the day of the final rule's publication, the Bank Policy Institute (BPI), the Kentucky Bankers Association (KBA), and Forcht Bank filed suit in the U.S. District Court for the Eastern District of Kentucky 2633. The plaintiffs argued that the CFPB had exceeded its statutory authority, that the rule imposed unrecoverable compliance costs, and that forcing banks to open infrastructure compromised consumer data security and privacy 283330.

The litigation forced a systemic pause on open banking compliance across the United States. Following a change in political administration and leadership at the CFPB, the agency reversed its stance. In May 2025, the CFPB formally requested the court to set the rule aside, acknowledging it as unlawful and signaling an intent to substantially revise it 2628. In July 2025, the court granted a stay of the litigation to permit a new rulemaking process, and in October 2025, it officially halted the staggered compliance deadlines that were slated to begin in April 2026 262830.

| Milestone Date | Regulatory or Legal Event | Market Implications |

|---|---|---|

| October 22, 2024 | CFPB Final Rule Published | Established phased compliance (2026-2030) and mandated free API data access, theoretically protecting aggregator margins 2629. |

| January 8, 2025 | FDX Recognized as Standard-Setter | Formalized the industry's technical transition away from credential-based screen scraping to secure OAuth API standards 1126. |

| May 23, 2025 | CFPB Reverses Course | The CFPB requested the court vacate its own rule, citing a need for substantial revision and signaling a shift in regulatory priorities 2628. |

| July 29, 2025 | Litigation Stayed | Court paused legal proceedings, opening a prolonged regulatory vacuum for infrastructure providers 262930. |

| October 29, 2025 | Compliance Deadlines Halted | Court officially suspended the upcoming April 2026 deadlines, relieving banks of immediate compliance costs 2830. |

By mid-2026, the absence of a binding federal mandate removed the regulatory floor that would have forced banks to provide free API access 42631. Without this protection, massive depository institutions retain the leverage to monetize data access through bilateral commercial agreements, heavily complicating the long-term unit economics of aggregators that originally built their models on frictionless, cost-free data ingestion 431.

International Expansion and the European Regulatory Shift

As the U.S. market faces regulatory stagnation, Plaid's international expansion strategy relies on adapting its technical infrastructure to diverse, highly regulated regimes. The company's formal entry into the United Kingdom was catalyzed by its 2019 acquisition of Quovo - a $200 million deal that secured an Account Information Service Provider (AISP) license from the UK's Financial Conduct Authority (FCA) 3233. Since then, Plaid has established a robust footprint across the European Economic Area (EEA), acquiring Payment Initiation Service (PIS) licenses and localizing underwriting tools, such as expanding Plaid Income to the UK and the Netherlands to serve the 70% of local gig workers who reportedly struggle to access traditional credit products 3383440.

Limitations of PSD2 and the API Quality Gap

The European open-banking ecosystem is the most mature globally, governed primarily by the Second Payment Services Directive (PSD2), which mandated API-based data sharing 1141. However, significant structural deficiencies in PSD2 implementation hampered early API aggregator adoption and forced high operational costs on third-party providers (TPPs). TPPs encountered severe access obstacles due to inconsistent API quality across thousands of member-state banks, excessive downtime, and regulatory exemptions that permitted banks to maintain screen-scraping-resistant fallback interfaces 4135.

A critical friction point involved Strong Customer Authentication (SCA) requirements. Under PSD2 interpretations, banks tightly managed the authentication process, forcing consumers to re-consent to data sharing every 90 days. Furthermore, users initiating payments were often subjected to the "double redirect" issue - requiring multiple authentications across disparate banking apps for a single payment transfer 3536. These UX frictions severely degraded conversion rates, stifling the growth of PIS-enabled A2A payments and creating compliance burdens for aggregators attempting to normalize data across the continent 4135.

The PSD3, PSR, and SEPA Instant Mandates

To rectify these systemic failures and standardize the ecosystem, the European Commission introduced the Third Payment Services Directive (PSD3) and the directly applicable Payment Services Regulation (PSR) 363738. Scheduled for enforcement around 2028, the new regulatory package aims to harmonize conduct-of-business rules without requiring fragmented national transposition 3846. Crucially, it mandates the removal of the 90-day bank-side re-consent burden - shifting management directly to TPPs - and explicitly prohibits friction-inducing practices like double redirects to streamline the user experience 3536.

Concurrently, immediate technical mandates are reshaping European payment architecture. The Instant Payments Regulation requires all PSPs offering SEPA Credit Transfers to ensure the capacity to receive instant payments by January 2025 and to send instant payments by October 2025 46. This mandate is coupled with a strict requirement for continuous name-IBAN verification (payee verification) to mitigate the escalating threat of authorized push payment (APP) fraud 3646.

Furthermore, the PSR framework heavily shifts the liability for fraud and sophisticated spoofing attacks onto Payment Service Providers, converging toward automatic consumer reimbursement models 3638. For infrastructure providers like Plaid, this convergence of mandated instant rails, standardized API access under PSR, and heightened payee verification creates a highly lucrative environment to deploy its machine-learning fraud prevention (Protect) and payment orchestration tools to European institutions desperate to mitigate their expanded liability 3846.

Open Banking Infrastructure Competitive Dynamics

The API aggregation and embedded finance market remains highly fragmented. While Plaid retains dominance in consumer fintech velocity and general developer experience, the ecosystem is characterized by intense competition among specialized providers catering to different geographic niches, compliance requirements, and institutional alignments 4748.

| Infrastructure Provider | Parent Entity | Primary Geographic Focus | Core Differentiators and Product Strengths |

|---|---|---|---|

| Plaid | Independent | US, Canada, UK, EU | Broadest US institution coverage; high consumer fintech market share; advanced ML risk scoring (LendScore, Trust Index); Pay-by-Bank guaranteed settlement 5648. |

| Mastercard Finicity | Mastercard | US | Deep enterprise bank relationships; dominant in mortgage and lending via structured Verification of Income/Assets (VOI/VOA); strict FCRA compliance posture 4748493940. |

| Visa Tink | Visa | Europe | European market dominance with 10,000+ connected banks; highly optimized for PSD2/PSD3 compliance; robust European Pay-by-Bank and PFM integration 41484142. |

| Stripe Financial Connections | Stripe | Global (via Stripe ecosystem) | Seamless integration into Stripe's core payment gateway; predictable per-API pricing; frictionless checkout optimization for existing Stripe merchants 435556. |

| MX | Independent | US | Superior data normalization and enrichment; deep integrations with mid-sized regional banks and credit unions; focused on financial wellness and categorization APIs 474057. |

Mastercard Finicity and Enterprise Lending

Finicity, acquired by Mastercard in 2020 for $825 million, leverages its parent company's balance sheet, global payment rails, and institutional trust to secure massive enterprise lending contracts 4944. While Plaid commands the consumer fintech space, Finicity dominates complex credit decisioning. Operating as a registered Consumer Reporting Agency under the Fair Credit Reporting Act (FCRA), Finicity provides legally admissible consumer-reporting data, establishing a formidable competitive moat in highly regulated mortgage and auto underwriting workflows 484044. When developers require granular transaction spending analytics for personal finance apps, Plaid is typically preferred; however, when absolute verification of income and assets (VOI/VOA) is required for institutional lending, Finicity is often selected due to its highly structured data outputs 4739.

Stripe Financial Connections and Payment Ecosystems

In the payment facilitation space, Stripe Financial Connections poses a direct threat to Plaid's Pay-by-Bank ambitions 43. For merchants already embedded within the Stripe processing ecosystem, activating Financial Connections streamlines operational overhead, consolidates processing fees, and unifies vendor management within a single dashboard 435559. Stripe utilizes a predictable, flat per-transaction pricing model that is highly attractive for high-volume applications 5559. However, developers report that Stripe's long-tail bank coverage and data categorization depth have historically lagged behind Plaid's specialized infrastructure, occasionally resulting in lower conversion rates during consumer onboarding for less common regional banks 55.

Visa Tink and European Market Dominance

In the European theater, Visa Tink leads the open banking transition. Acquired by Visa in 2021, Tink boasts established API connectivity to over 10,000 European institutions, providing a distinct geographic advantage in navigating the deeply fragmented PSD2 landscape 484142. Tink is structurally positioned as the primary infrastructure layer for European neobanks and personal finance management tools 4841. Plaid's expansion into the continent requires outcompeting these entrenched, network-backed providers by offering a unified transatlantic API for global enterprises scaling in both jurisdictions 3834.

MX and Data Enrichment

MX maintains a strong position in the United States by focusing heavily on data normalization, enrichment, and deep partnerships with mid-sized regional banks and credit unions 474840. While it may lack the sheer breadth of Plaid's institution coverage, MX provides superior transaction categorization and contextual financial wellness tooling natively out of the box, whereas Plaid clients sometimes require custom categorization layers to achieve similar precision 4740.

Conclusion

Plaid's recovery to a projected $8 billion to $10 billion valuation represents a successful navigation of overlapping existential and regulatory threats. The collapse of the Visa acquisition forced the company to chart an independent path during a period of macroeconomic contraction and shifting venture capital paradigms. Simultaneously, the core utility of raw data aggregation faces severe commoditization pressures, driven by the technical standardization of bank APIs via FDX, impending U.S. regulatory ambiguity under a stalled CFPB Section 1033 rule, and the imposition of margin-compressing access fees by dominant financial institutions like JPMorgan Chase.

In response, Plaid has effectively restructured its economic model. By migrating upward in the value chain - deploying sophisticated machine-learning models for credit underwriting, fraud orchestration, and instant payment guarantees - the company has transformed from a passive data conduit into an active risk intermediary. The long-term viability of this valuation trajectory will depend heavily on its ability to drive mainstream merchant adoption of Pay-by-Bank workflows, converting flat-fee ACH infrastructure into high-margin payment orchestration, while successfully defending its enterprise market share against well-capitalized, network-backed incumbents like Visa Tink and Mastercard Finicity.