How Retail Traders Deploy Machine Learning Trading Bots

Deploying a live algorithmic trading bot requires bridging the massive, treacherous chasm between a sterile, theoretical codebase and a chaotic live market environment actively hostile to automated execution. The transition from code to live deployment is an exercise in managing catastrophic failure states, continuous server maintenance, and severe market friction, rather than merely predicting price movements.

Social media is currently inundated with "AI passive income" hype, where influencers promise that deploying a fifty-line Python script or a pre-packaged machine learning model will autonomously generate wealth while the operator sleeps. The gritty reality of what it actually takes to keep a bot running is entirely different. An automated trading system is not a passive cash machine; it is a highly fragile, high-maintenance software engine that requires continuous babysitting, rigorous debugging, and ongoing capital expenditure 12. To understand this paradigm shift, one must recognize that offline backtesting is akin to flying an aircraft in a perfectly calibrated desktop simulator with zero wind resistance. Conversely, live deployment is like flying that exact same aircraft into a severe, unpredictable storm, where real-world friction - in the form of internet latency, unavoidable slippage, and abruptly severed broker API connections - actively fights the system's survival 345.

The purpose of this report is to exhaustively detail the architectural, operational, and financial realities of deploying retail algorithmic trading systems in modern financial markets, contrasting these constraints with institutional realities.

Why Do Profitable Offline Bots Fail in Live Markets?

The transition from a highly profitable backtest to a live market environment is notoriously fraught with failure. A fundamental misconception pervades the retail algorithmic trading space: the assumption that superior historical backtest results equate to guaranteed live profits. This "backtest illusion" occurs because historical simulations operate in a frictionless vacuum, ignoring the harsh realities of market microstructure, latency, and execution mechanics 45. Retail practitioners routinely spend months constructing complex statistical models, only to go live and discover they were trading their idealized backtest environment rather than the actual market 45.

The Backtest Illusion: Slippage, Spreads, and Partial Fills

In a standard backtesting environment, an algorithm calculates a signal, places a virtual market order, and receives an instantaneous fill at the exact historical print price. In reality, the act of placing an order interacts with, and alters, the market's liquidity. The spread between the bid and ask prices constantly fluctuates, and the available volume at a specific price tier (the depth of book) may not be sufficient to fill the entire order. This results in slippage - the difference between the expected price of a trade and the price at which the trade is actually executed 36.

Furthermore, automated systems frequently encounter partial fills, where only a fraction of the desired order size is executed before the market price moves away. If the strategy logic is not explicitly programmed to handle state management for partially filled orders, the system's internal accounting will desynchronize from the broker's actual portfolio state. This desynchronization can lead to catastrophic compounding errors, as the algorithm may continuously attempt to reconcile its theoretical position with reality by submitting duplicative orders 7. Real-world markets also feature automation-driven spreads and session liquidity shifts that historical data cannot perfectly replicate; for instance, over 70% of forex trading and US equity volume is generated by automated systems, meaning a bot is constantly competing against other algorithms reacting to the exact same microstructural anomalies 6.

The Latency Gap: Retail SIP vs. Institutional Direct Feeds

A primary reason retail bots fail to capture the alpha identified in backtests is the stark discrepancy in data latency and granularity between retail and institutional operators. Retail algorithmic trading heavily relies on the Securities Information Processor (SIP), an aggregated data feed mandated by Congress in 1975 that calculates the National Best Bid and Offer (NBBO) 12. While the SIP consolidates NMS-protected quotes from all markets and is entirely sufficient for top-of-book discretionary trading, it suffers from inherent geographical and processing latency 3. For example, the CTA/UTP SIPs incur unnecessary latency because data must travel between matching engines in locations like Carteret, New Jersey (Nasdaq), and the consolidation hubs in Mahwah, New Jersey (NYSE) 3.

By the time a retail algorithm receives a SIP price update, processes the signal, and sends an order over the public internet, institutional High-Frequency Trading (HFT) firms utilizing direct proprietary exchange feeds and microwave towers have already updated their quotes or consumed the available liquidity 211. Direct proprietary feeds, such as Nasdaq TotalView-ITCH or NYSE Integrated Feed, bypass the SIP entirely 34. These feeds provide ultra-low latency and granular "Level 2" or "Level 3" data, offering a comprehensive order-by-order view of events including depth of book, order imbalances, and security status messages 34.

Crucially, proprietary feeds contain vital information omitted by the SIP, such as odd-lot quotes. Odd lots currently constitute nearly 50% of unreported U.S. equities market activity, meaning algorithms relying solely on SIP data are operating entirely blind to half of the market's microstructural activity 3. Consequently, latency-sensitive strategies - like statistical arbitrage or high-frequency market making - are essentially impossible for retail operators to execute profitably over SIP feeds 12. HFT strategies demand execution latency under 100 milliseconds, frequently operating in single-digit microseconds or nanoseconds, whereas standard retail internet connections and SIP processing easily introduce 100 to 300 milliseconds of delay 111. While consolidated data is useful for non-latency sensitive portfolio executions and macro algorithmic strategies, the expectation that a retail setup can compete in the microsecond arena is a guaranteed path to failure 12.

Where Do Bots Actually Live?

An algorithmic trading strategy is only as robust as the infrastructure hosting it. While a hobbyist might run a Python script on a local laptop, professional and semi-professional deployment requires dedicated, uninterrupted environments. The hosting landscape is generally divided into three primary categories: the local machine, the Virtual Private Server (VPS), and Cloud-native infrastructure.

Comparing Retail Hosting Environments

| Hosting Environment | Average Monthly Cost | Reliability & Uptime | Latency to Exchanges | Maintenance Effort | Best Use Case |

|---|---|---|---|---|---|

| Local PC / Laptop | $0 (Excluding electricity/ISP) | Low (Vulnerable to ISP drops, power outages, forced OS updates) | High (50ms - 100ms+, depending on home ISP) | High (Requires manual restarts, physical security, network management) | Initial strategy coding, historical backtesting, and paper trading only. |

| Trading-Optimized VPS | $25 - $100+ | High (99.9% uptime, datacenter redundancies, uninterruptible power) | Ultra-Low (<1ms to 5ms if co-located near NY4 or CME Aurora) | Medium (Requires initial OS configuration and patch management) | Latency-sensitive retail trading, automated MetaTrader/NinjaTrader bots, stable GUI execution. |

| Cloud Infrastructure (AWS/Modal) | $30 - $200+ (Variable based on egress/compute) | Very High (Distributed architecture, auto-scaling capabilities) | Variable (Single-digit ms to 20ms depending on AWS Region/Local Zone) | High (Requires DevOps knowledge, containerization, and networking configuration) | Machine learning inference, heavy data pipelines, event-driven microservices. |

Data aggregated from infrastructure cost analysis and latency benchmarking 13141516.

The Shift to Specialized Trading VPS

For retail traders executing standard algorithmic strategies, the specialized Trading VPS has become the industry standard. Providers such as QuantVPS or dedicated Equinix-hosted servers place the execution logic in physical proximity to major exchange matching engines 1415. For equities, this generally means data centers in or near Secaucus, New Jersey (NY4); for futures, it requires Chicago or Aurora-proximate hardware 1315. A specialized trading VPS provides sub-millisecond latency to brokers and protects the algorithm from residential ISP failures or forced local operating system updates 1315. A trading VPS is a professionally managed execution environment that ensures charting platforms, algorithms, and order management systems remain stable during extreme market volatility, making uptime its primary value proposition over sheer speed 15.

The Hidden Costs of Public Cloud Deployment

Conversely, institutional quants and advanced developers often utilize massive public cloud infrastructures like Amazon Web Services (AWS) or Microsoft Azure. While AWS offers unparalleled compute scaling and global redundancy - allowing institutional brokers to scale capacity instantly during volatility - it is rarely cost-effective or manageable for the average retail algorithmic trader 1315.

AWS pricing is notoriously complex. A base instance like an AWS Lightsail or EC2 t3.medium might appear inexpensive at $20 to $30 per month, but the true cost of ownership is hidden in operational add-ons 1416. Continuous data egress charges are particularly punitive for trading workloads; AWS charges approximately $0.09 per GB for data transfer out. A typical algorithmic trader running multiple symbols with high-resolution tick data easily consumes 50 to 100 GB monthly, while active traders using real-time Bloomberg or Reuters feeds can incur $20 to $50 purely in egress charges 1416. Add mandatory snapshot storage ($0.05 per GB), Elastic Load Balancers ($16 monthly), CloudWatch monitoring ($5 to $10 monthly), and the necessity of paid Business Support ($100 monthly) to ensure rapid response during trading hours, and the total AWS cost easily reaches $70 to $150+ monthly 1416. Furthermore, standard public cloud instances are not inherently optimized for the specific routing paths required by financial exchanges, requiring extensive manual DevOps tuning to achieve the sub-millisecond latency offered out-of-the-box by a $50 specialized trading VPS 1415.

Post-2023 Accessible Tools for Machine Learning Deployment

As algorithmic trading increasingly incorporates machine learning (ML), the infrastructure requirements have shifted from simple execution scripts to heavy inference pipelines requiring GPU compute. Post-2023, the ecosystem has matured to offer sophisticated, retail-friendly deployment tools that abstract away the complexity of managing raw AWS clusters.

For developers utilizing Python-based ML models, serverless platforms like Modal and Replicate have split the deployment landscape into two distinct paradigms 17. Replicate operates as a model marketplace utilizing an open-source container format called Cog; it is highly effective for single-shot API calls to established community models but struggles with cold-start latency 17. Modal, conversely, is a serverless compute platform that allows developers to write Python functions and run them on GPU infrastructure that scales to zero 1718. Modal excels at deploying multi-step pipelines and mitigating the severe cold-start latency issues that plague user-facing applications, making it highly suitable for high-volume, event-driven trading inference 1718.

Furthermore, frameworks like BentoML have revolutionized model packaging 1920. Historically, deploying an ML model involved writing custom, fragile Flask or FastAPI wrappers that struggled with serialization and dependency management 20. BentoML standardizes this process, allowing quantitative developers to package a trained model, its dependencies, and custom pre-processing logic into a deployable artifact (a "Bento") that automatically generates high-performance RESTful or gRPC API endpoints 1920.

For end-to-end quantitative platforms, systems like QuantConnect's LEAN engine provide a powerful hybrid workflow 215. LEAN allows developers to write and backtest C# or Python strategies locally in IDEs like VS Code, utilizing their own data and hardware 216. Once validated, the exact same codebase can be deployed to QuantConnect's managed, co-located cloud infrastructure for live execution 215. This unified pipeline eliminates the historically perilous transition where a backtested model had to be entirely rewritten or translated for a live production environment 21.

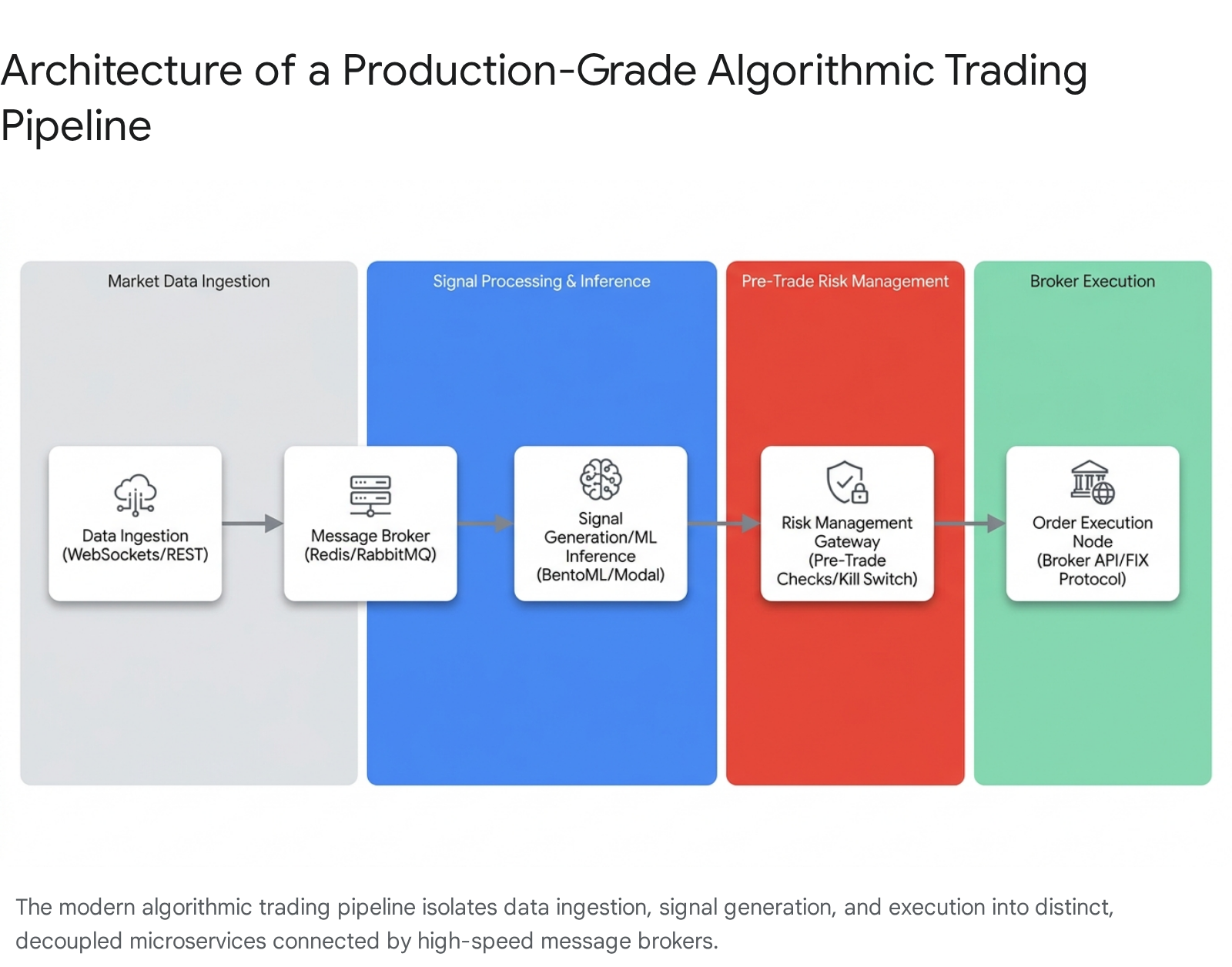

The Live Pipeline: From Signal to Execution

In a live production environment, an algorithmic trading system operates as a continuous, event-driven distributed system rather than a sequential script.

The pipeline must ingest real-time tick data, process machine learning inferences, validate risk constraints, and interface with external broker APIs simultaneously 24. This asynchronous communication is frequently managed by dedicated message brokers, which decouple the services to ensure that a bottleneck in the ML inference engine does not block or drop the incoming real-time market data feed 242526.

Event-Driven Message Brokers: Redis vs. RabbitMQ

The choice of message broker heavily dictates the system's reliability and latency profile. Two dominant technologies serve this purpose: Redis and RabbitMQ 2728.

Redis is an in-memory data structure store that operates primarily in RAM, excelling in ultra-low latency scenarios (sub-millisecond) 27297. It is ideal for transient, real-time prediction queues, caching fast-moving order book data, or acting as a feature store between microservices 2829. Redis can process tens of millions of messages per second; however, it lacks inherent persistence and robust delivery guarantees 287. By default, if the Redis server crashes or loses power, any unread messages residing in memory are permanently lost unless manual snapshotting (RDB) is configured, which inherently slows down data operations 287.

Alternatively, RabbitMQ utilizes the Advanced Message Queuing Protocol (AMQP) to function as a highly reliable, dedicated message broker 25277. RabbitMQ writes messages to disk and utilizes a "smart broker, dumb consumer" model, requiring the consumer application to actively acknowledge receipt of a message before it is deleted from the queue 28731. While this persistent mode introduces higher latency - processing tens of thousands of messages per second compared to Redis's millions - its advanced routing features (fanout, topic, direct exchanges), dead-letter queues, and guaranteed delivery make it the superior choice for routing critical order execution messages 27282931. In trading architecture, dropping an execution command or a trade confirmation packet is unacceptable, making RabbitMQ the standard for the execution leg of the pipeline 2831.

Taming Broker APIs: Rate Limits and Exponential Backoff

Interfacing with retail broker APIs, such as Alpaca, Interactive Brokers (IBKR), or cryptocurrency exchanges, requires highly defensive programming paradigms. A common point of failure for novice algorithmic traders is the mishandling of HTTP 429 (Too Many Requests) and HTTP 504 (Gateway Timeout) errors 83334. Broker APIs utilize token bucket algorithms to enforce rate limits per IP address or authenticated user account, protecting their matching engines from poorly coded, infinite-looping bots 9. For instance, Alpaca limits users to 200 distinct API calls per minute; exceeding this rate immediately returns a 429 error, temporarily blocking the system from placing or modifying orders 33936.

To survive in live markets, the execution code must implement a retry strategy known as Exponential Backoff with Jitter 93710. When a server returns a 429 or 504 error, retrying the request immediately or in a tight loop only exacerbates the throttling and guarantees continued failure 3739. Exponential backoff progressively increases the wait time between retry attempts (e.g., waiting 1 second, then 2, then 4, then 8) to allow the upstream server time to recover or the token bucket to refill 37103940.

Crucially, the addition of "Jitter" is required to prevent systemic cascading failures. Jitter introduces a randomized variable to the calculated delay time 910. Without jitter, if a broker experiences a brief outage and thousands of connected client microservices recover simultaneously, they will all retry their requests at the exact same exponential intervals, creating a "thundering herd" problem that immediately crashes the broker's API gateway again 1041. The implementation of full jitter (randomly selecting a wait time between 0 and the maximum calculated exponential backoff) ensures that traffic spikes are smoothed out over time, greatly increasing the probability of a successful request 10.

Maintaining TCP Socket Persistence

Not all broker integrations rely on standard REST APIs. The Interactive Brokers TWS API, which is heavily utilized by retail quants via asynchronous Python libraries like ib_insync, requires a persistent TCP socket connection communicating directly with a locally running instance of the desktop Trader Workstation or IB Gateway application 11431213. The communication occurs over localhost (typically port 7496 for paper trading or 7497 for live) 111246.

Maintaining this socket is non-trivial. The TCP connection will frequently time out during periods of inactivity, or sever completely during Interactive Brokers' mandatory daily server resets 4312. If the socket disconnects, the trading script will fail silently or crash entirely unless the developer has engineered a dedicated "Watchdog" thread 43. This thread must run asynchronously alongside the main logic, continuously monitoring connection health via periodic heartbeats, dynamically updating the system status, and executing graceful reconnections without duplicating active orders 4312.

How Do You Stop a Bot from Emptying Your Account?

In algorithmic trading, speed is power, but unchecked speed is the fastest route to catastrophic financial ruin 47. The environment is fundamentally unforgiving; a single logic bug, an inverted mathematical sign, a corrupted market data feed, or a software deployment error can result in an algorithm executing thousands of erroneous trades, draining an account balance in mere seconds 4748. History is replete with examples of automated failures, such as Knight Capital losing $400 million in 2012 when a new, untested algorithm bought at the ask and sold at the bid repeatedly 14. Consequently, professional systems rely heavily on mandatory pre-trade risk management frameworks and programmatic circuit breakers.

Pre-Trade Risk Checks

Operating similarly to the compliance guardrails mandated by the SEC (Regulation AT) and MiFID II for institutional firms, pre-trade risk checks act as a specialized gateway 481450. They sit directly between the strategy's signal generation logic and the broker API, evaluating every proposed order against hard-coded constraints before transmission 4814. These localized controls act on a highly granular level and must balance thoroughness with execution speed to avoid introducing latency, often utilizing cached risk limits and parallel processing 5115.

Essential pre-trade checks include 145115: * Volume and Position Limits: Ensuring that a new order does not exceed maximum allowable position sizing for a specific individual security, asset class, or aggregate portfolio exposure. This prevents the bot from aggressively accumulating excessive leverage during a continuous false-signal loop 1451. * Price Collars (Sanity Checks): Rejecting orders that deviate excessively from the current Last Traded Price or the NBBO. This protects the system from executing "fat-finger" market orders or sweeping the book during brief periods of total market illiquidity or flash crashes 1415. * Message Rate Throttling: Monitoring the frequency of order submissions, modifications, and cancellations over a rolling time window. This prevents runaway algorithms from spamming the exchange matching engine and violating broker API rate limits 1415.

The Programmatic Kill Switch

While pre-trade checks prevent individual bad orders from reaching the market, a Kill Switch is a systemic circuit breaker designed to immediately halt all trading activity when aggregate risk thresholds or abnormal behaviors are detected 4714. A professional kill switch must be programmatic, operating in real-time without requiring human intervention to diagnose the problem first, as human reaction times are vastly too slow to prevent high-frequency losses 47.

Designing a reliable kill switch requires precisely defining its scope and testing it rigorously through chaos engineering drills 4753. When activated by a severe anomaly - such as a massive sudden drawdown, a latency spike, or an abnormal cancel-to-trade ratio - the system must execute predefined safety logic 4753. Developers face critical architectural decisions regarding the switch's behavior: should it simply pause new signal generation, explicitly cancel all open resting orders at the exchange, disable routing, or actively flatten (liquidate) existing open positions? 53. Flattening positions automatically can be exceptionally dangerous; if the market is currently experiencing a flash crash or extreme illiquidity, forcing a market order to liquidate an existing position may lock in catastrophic losses 53.

In highly sophisticated institutional environments, the ultimate kill switch exists outside the trading software application entirely 54. Sell-side firms route their IP connections through edge network switches equipped with Field Programmable Gate Arrays (FPGAs) 54. The hardware intercepts and decodes the TCP/IP packets, persisting the state of live orders independently 54. If the centralized risk system detects a systemic software failure, the FPGA physically severs the connection to the execution venues or fires pre-programmed, mass-cancel FIX messages at hardware speeds, entirely bypassing the potentially frozen software application 54.

What This Means for You: The Hidden Costs of Deployment

The allure of algorithmic trading, perpetually amplified by internet marketing, often obscures the massive operational burdens required to sustain it. The transition to live execution introduces profound hidden costs - both in financial terms and in human capital - that rapidly separate hobbyists from viable quantitative operations.

The Time Toll: Babysitting the Infrastructure

Developing the trading strategy is only the beginning; deploying it forces the quantitative developer into the role of a full-time Systems Operations (SysOps) engineer. Retail practitioners routinely report spending 30 to 80 hours per week solely maintaining their algorithmic infrastructure 245. Building a robust system from scratch often requires over 500 hours of initial development time, encompassing database logging, user interface design, margin syncing, and broker integration 55.

The operational burden is unrelenting. It involves endlessly monitoring server logs, adapting to unannounced broker API endpoint deprecations, resolving database synchronization errors, and managing data pipeline failures. Developers quickly find that attempting to treat algorithmic trading as a casual "side hustle" is a fallacy; it requires the commitment of running a full-time business 4. As one developer noted, the psychological trap is spending months building an algorithm, only to go live and realize they were "trading the backtest, not the market" 45. Ultimately, a live algorithmic system demands constant supervision to ensure the environment remains stable enough for the mathematical edge to manifest.

The Financial Toll: Professional Data Designations and Egress

The secondary hidden cost of live deployment is the exorbitant pricing structure of institutional-grade market data. When transitioning from paper trading, simulation, or initial backtesting to a live, capitalized entity, traders frequently run afoul of Exchange classifications regarding "Professional" versus "Non-Professional" data subscribers 561658.

An individual retail trader qualifies as a Non-Professional, granting them highly subsidized access to data feeds. They often pay a nominal fee of $3 to $15 per month for direct exchange data 561718. However, the moment a trader utilizes capital from a proprietary trading firm, registers a corporate LLC, registers as a financial advisor, or even acts as a contractor for a financial institution, the exchanges universally classify them as a Professional Subscriber 5616.

This reclassification triggers massive fee escalations. For example, access to the CME Group futures data jumps from roughly $3 per month to $140 per month, per exchange (meaning access to CME, CBOT, NYMEX, and COMEX could total $560 monthly) 5617. Access to the Nasdaq TotalView depth-of-book feed leaps from $15 a month for retail users to over $80 a month for professionals, while non-display usage for automated trading engines incurs fees well into the thousands of dollars 1819.

When trading multiple asset classes across various exchanges, the fixed monthly overhead for professional market data and VPS infrastructure can easily exceed $500 to $1,000 56. This overhead acts as an immediate, heavy drag on the portfolio's expected value, forcing the algorithm to generate substantial minimum returns each month just to break even and offset the operational burn rate 56.

Bottom Line

- Backtests are theoretical; live markets are hostile. A flawless backtest completely ignores the mechanical friction of live trading, including widened bid-ask spreads, order slippage, partial fills, and the severe latency disadvantages of retail SIP data feeds compared to institutional proprietary direct feeds.

- Infrastructure dictates survivability. Live bots cannot reliably run on residential laptops subject to ISP drops and OS updates. They require specialized trading VPS environments co-located near exchange matching engines, or sophisticated cloud deployments utilizing serverless functions (like Modal) and containerization (like BentoML) optimized for managing persistent TCP socket connections.

- Defensive engineering is non-negotiable. A production-grade system must implement programmatic kill switches, granular pre-trade risk collars, and intelligent error-handling protocols - such as exponential backoff with full jitter - to prevent API rate-limit throttling and catastrophic, account-draining runaway execution loops.

- The passive income myth is false. Deploying a bot does not free up time; it merely transitions the operator from a manual trader to a full-time systems administrator, responsible for monitoring logs, absorbing massive professional market data fees, and continuously repairing fragile network pipelines.