How Money Evolved from Barter to Bitcoin and CBDCs

Contrary to popular belief, money did not evolve from a primitive system of barter, but rather from ancient social credit systems and communal ledgers of debt. Over millennia, human societies have shifted from recording obligations on Sumerian clay tablets and massive stone wheels to issuing paper fiat currencies, and finally to modern digital cryptography. Today, the centuries-old model of centralized institutional trust is fracturing as decentralized cryptocurrencies compete directly with a new wave of highly surveilled, government-issued Central Bank Digital Currencies (CBDCs).

Did the Barter Economy Actually Exist?

For centuries, the standard economic narrative regarding the origin of money was beautifully simple and inherently logical. As famously articulated by Enlightenment economists like Adam Smith, early humans supposedly operated in a pure barter economy, trading goods directly - such as exchanging a pig for a bushel of wheat 1. Because barter requires a "double coincidence of wants" - where both parties must simultaneously desire exactly what the other has - it is highly inefficient and creates immense friction in trade 23. Money, the textbook story goes, was inevitably invented as a technological fix to lubricate commerce, evolving linearly from precious metals to paper to digital bits 12.

There is only one problem with this ubiquitous narrative: there is almost no historical or anthropological evidence to support it 115.

The Anthropological Consensus on Debt

According to the late anthropologist David Graeber and Cambridge political economist Caroline Humphrey, a pure barter economy has never been observed in human history 2. In his seminal 2011 book Debt: The First 5,000 Years, Graeber systematically dismantled the barter myth, demonstrating that barter historically occurs almost exclusively between strangers, active enemies, or in modern societies where people are accustomed to money but have suddenly lost access to it - such as in post-Roman Europe, or during periods of hyperinflation 2162.

Instead, early human economies operated on credit, mutual obligation, and reciprocity 18. Within tight-knit communities and indigenous tribes, individuals did not haggle over immediate, spot-trade exchanges. Instead, a hunter might share their catch with a neighbor, creating a tacit social debt - an informal "I-owe-you" - to be repaid later in goods, services, or labor 119. Money, therefore, was not invented to replace barter; it was invented to quantify and formalize these pre-existing debts 1011.

The Nuance in the Academic Debate

While Graeber's anthropological framework shifted the academic consensus, the debate contains subtle nuances. Some economists and financial historians point out that while the neoclassical version of the barter story - featuring hyper-rational actors trading entirely without social context - is a myth, barter itself is not absent from the historical record 34. Occasional, irregular exchange between strangers did occur, but irregular exchanges do not generate the need for a standardized monetary system 14. As Graeber himself noted, when money finally emerged, it was typically driven by the legal affairs of states and temples - specifically the need to calculate fines, taxes, and formalized debts - rather than commercial transactions between neighbors 1415.

The Original Credit Ledgers: Clay, Stone, and Wood

Long before the advent of minted metal coins, ancient civilizations developed highly sophisticated physical accounting systems to track debts. In doing so, they established the foundational principle of all money: it is, at its core, a ledger of trust.

Sumerian Clay Tablets and Temple Economies

In ancient Mesopotamia (circa 3500 BC), the Sumerian civilization created one of the world's first sophisticated financial systems 5. Large temples and palaces functioned as the region's economic hubs, functioning as fortified treasuries that employed thousands of bureaucrats, priests, and technicians 856. These institutions tracked agricultural rents, commercial loans, and inventory using cuneiform script pressed into clay tablets 86.

To standardize these massive economic operations, the temples established fixed units of account. The value of a silver shekel-weight was set equal to a specific "basket" of barley 67. The administrative year was divided into uniform 30-day months, and a 60-based (sexagesimal) system was used to denominate weights and measure monthly interest allocations 6.

The Code of Hammurabi eventually codified these credit systems, setting maximum interest rates - typically 20% for silver loans and 33.3% for grain loans - proving that institutional credit lending predated the invention of minted coinage by millennia 58. Because these agrarian debts compounded rapidly, ancient kings periodically issued "clean slate" proclamations - debt jubilees - to cancel agrarian debts and prevent the total collapse of the peasant economy, ensuring farmers did not take up arms against the government 5678.

The Rai Stones of Yap

Half a world away, the Pacific island of Yap - now part of the Federated States of Micronesia - developed one of the most fascinating physical ledgers in human history 910. For centuries, the Yapese utilized Rai stones: massive, circular limestone discs with holes carved in the center, weighing up to 5 tons and measuring up to 12 feet in diameter 91011.

Because the aragonite and calcite minerals required to make Rai stones were not native to Yap, the stones had to be quarried on the island of Palau and transported over 300 miles across treacherous open ocean in outrigger canoes 101123. The value of an individual Rai stone was not dictated merely by its size, but by its extrinsic history: how difficult it was to quarry, the storms encountered during the journey, and the social status of the people who had owned it 1123.

Because the larger stones were far too heavy to move, physical possession was practically irrelevant 1123. When a stone changed hands to pay for a dowry, settle a political dispute, or purchase land, the entire village simply updated their collective mental ledger to acknowledge the new owner 91011. Even if a stone sank to the bottom of the ocean during transport, it retained its purchasing power as long as the community universally agreed it existed 1023. In the late 19th century, an Irish-American trader named David Dean O'Keefe caused a localized inflation crisis by using modern ships and iron tools to flood the island with newly quarried, less valuable stones 101123. Today, financial historians frequently compare the community-consensus ledger of the Yapese Rai stones to the decentralized, distributed ledgers utilized by modern blockchain networks 10.

Medieval English Tally Sticks

In Medieval Europe, a severe shortage of minted coins led to the widespread use of split tally sticks to document bilateral exchanges and debts 12. Introduced in England by King Henry I around 1100 AD, a tally stick was typically a piece of squared hazelwood or willow, notched to indicate a specific monetary value 121314.

Each notch represented a specific sum: the thickest notches indicated £1,000, while thinner cuts represented shillings and pence 13. The stick was then split lengthwise so that the debtor (who kept the "foil") and the creditor (who kept the "stock") each retained a matching half 1314. Because the organic wood grain of a willow branch is entirely unique, the two halves could not be forged or altered without immediate detection upon comparison 1213.

Tally sticks soon evolved into a form of circulating, interest-free sovereign debt; they were sold at a discount in secondary markets and were legally accepted by the Royal Exchequer for the payment of taxes 121427. The British government utilized this wooden fiat system for centuries. In 1697, the newly formed Bank of England even issued £1 million worth of stock in exchange for £800,000 worth of wooden tallies 12. When the government finally deemed the system obsolete and decided to incinerate centuries' worth of archived tally sticks in a massive furnace in 1834, the fire raged out of control and accidentally burned down the Palace of Westminster 13.

Paper Money and the Alchemy of the State

While commodity money (like silver and gold) carried intrinsic value, the transition to paper money required an immense leap of institutional faith. This paradigm shift occurred in imperial China, pioneering concepts like credit regulation and central banking centuries before the West 28.

The Tang and Song Dynasties: Flying Cash to Jiaozi

By the Tang Dynasty (618 - 907 AD), China was a bustling economic powerhouse, but its official currency - heavy copper and iron coins - was wildly impractical for large, long-distance wholesale transactions 2815. To avoid hauling literal cartloads of metal across the country, merchants began issuing "flying cash," which were essentially promissory notes representing deposited coins 30.

By the 11th century, under the Song Dynasty, merchants in the Sichuan province formalized this system with Jiaozi - widely considered the world's first true paper money 283016. Initially, Jiaozi was a private credit instrument. Merchants operated specialized shops where they charged an exchange fee of 30 wen per 1,000 cash to securely hold a client's coins and issue paper notes printed on bamboo paper with exquisite, hard-to-forge ink stamps 1617.

However, managing large-scale credit systems proved volatile. When over-leveraged private merchants suffered bankruptcies and failed to redeem notes, it triggered localized economic panics 151617. Recognizing the danger, the Song government intervened in 1023, founding the Jiaozi wu (a government office) to nationalize the production of paper money, backing it with state reserves of metal coins 1516.

The First Hyperinflation and the Return to Silver

The convenience of state-issued paper money ultimately proved to be an irresistible temptation for imperial authorities. Facing massive budget deficits to feed the population and fund wars against Mongol invaders, the Song government severed the paper's convertibility to metal reserves and began printing Jiaozi relentlessly 1530. This triggered one of the world's first recorded inflation crises. By 1204, the value of the paper had plummeted so drastically that notes with a face value of 1,000 cash coins were exchanging for as little as 100 physical coins 1617.

When the Mongols eventually conquered China and established the Yuan Dynasty, they doubled down on paper currency. Marco Polo famously marveled that Kublai Khan had discovered the "secret of alchemy" by turning the bark of mulberry trees into universally accepted money 3017. But successive Mongol and Ming dynasties repeated the exact same fiscal mistake, overprinting paper notes to the point of total hyperinflationary collapse 1530.

By the 15th century, the Chinese economy had largely abandoned paper money, shifting back to an imported silver standard 1530. The primary advantage of this "white gold" was explicitly political: it could not be conjured out of thin air by the emperor's command, providing a stable foundation for trade 30. This insatiable demand for silver deeply altered global geopolitics, drawing massive imports from Japan and the newly discovered Americas, and eventually contributing to the collapse of the Ming dynasty when silver inflows were disrupted 30.

The Digital Revolution and the Rise of Cryptocurrency

For centuries following the Chinese paper money experiments, global currencies oscillated between hard commodity standards (like the gold standard) and unbacked fiat money. In 1971, the United States formally decoupled the dollar from gold, transitioning the entire global economy into a pure fiat system where money derives its value entirely from government decree and the public's trust in central banks 310.

In late 2008, amid the catastrophic breakdown of institutional trust during the global financial crisis, an anonymous programmer (or group) operating under the pseudonym Satoshi Nakamoto published the whitepaper for Bitcoin 1819. Bitcoin represented a philosophical, mathematical, and technological rebellion against the sovereign fiat system.

Solving the Double-Spend Problem

Before Bitcoin, all digital money required a trusted, centralized intermediary - such as a commercial bank, a central bank, or a payment processor like Visa - to prevent the "double-spend problem" 319. Because digital files are easily copied, digital money requires an arbiter to deduct the funds from the sender's account and credit the receiver, ensuring the same digital token is not spent twice 19.

Bitcoin circumvented the need for a central arbiter using a decentralized public ledger known as a blockchain 1819. Like the Yapese villagers collectively verifying the ownership of Rai stones, the Bitcoin network relies on decentralized consensus 1018. Thousands of independent computers (nodes) use cryptographic puzzles and immense computational power to verify transactions publicly 319. Furthermore, Bitcoin's code strictly capped its total supply at 21 million coins, creating an algorithmic scarcity explicitly designed to be immune to the inflation that plagued historical fiat currencies 3.

While Bitcoin succeeded wildly as a censorship-resistant "store of value" (often dubbed digital gold), its extreme price volatility and the limited transaction throughput of its base layer have hindered its widespread adoption as a daily medium of exchange for standard goods and services 1936. In response, the cryptocurrency ecosystem evolved, giving rise to programmable platforms like Ethereum (which introduced smart contracts) and, crucially, "stablecoins" 3738. Stablecoins, such as USDC and Tether, are cryptographic tokens pegged 1:1 to sovereign currencies like the US dollar, offering the borderless speed of blockchain technology without the price volatility of Bitcoin 3839.

The Dawn of Central Bank Digital Currencies (CBDCs)

As decentralized cryptocurrencies and privately issued stablecoins surged in popularity and market capitalization, central banks worldwide realized their historical monopoly on the issuance of money was facing an existential threat 1838. Their strategic response is the Central Bank Digital Currency (CBDC).

What Exactly is a CBDC?

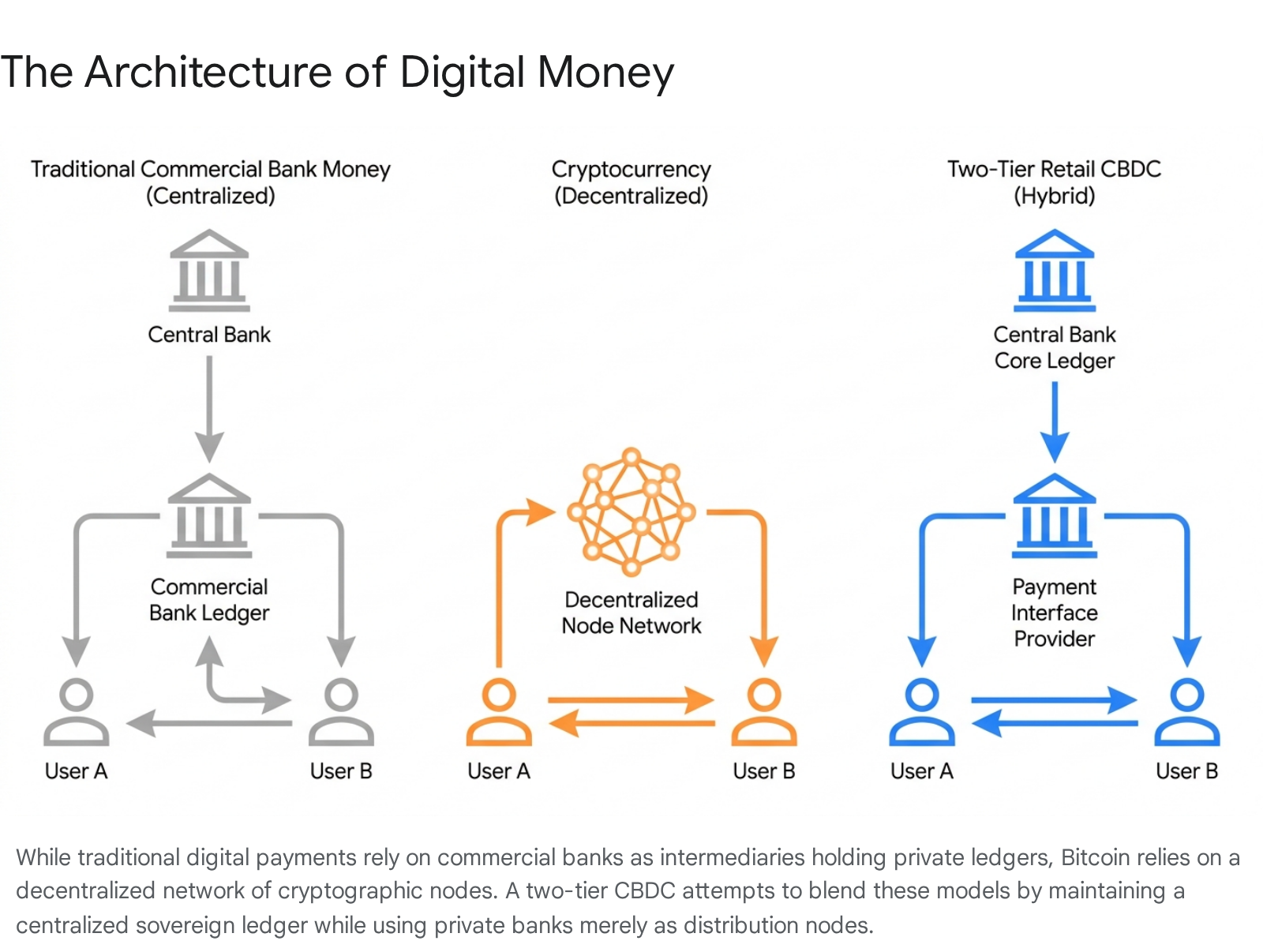

A CBDC is a digital representation of a nation's sovereign fiat currency, issued and backed directly by the central bank 2021. To understand why this represents a radical macroeconomic shift, it is vital to understand how modern digital money actually works.

Today, money exists in two primary forms: public money and private money 22. The only "public money" (a direct, risk-free liability of the central bank) available to the general public is physical cash (banknotes and coins) 2122. When a consumer checks their balance in a standard banking app, uses Apple Pay, or sends funds via a Fast Payment System (FPS), they are utilizing "commercial bank money" - a private liability 222324. If that commercial bank suffers a catastrophic failure, those digital deposits are theoretically at risk, shielded only by government deposit insurance frameworks 24.

A CBDC bridges this gap. It provides the general public and institutions with direct, digital access to risk-free central bank money 2223. It is not a cryptocurrency; it does not operate on a decentralized, permissionless ledger, and it carries the exact same credit risk as the physical cash in your wallet 3645.

Retail vs. Wholesale Models

Central banks are currently exploring two distinct formats for this technology: 1. Retail CBDCs (rCBDC): Designed for the general public, acting as a digital replacement or complement to physical cash for everyday transactions 2223. Retail models can be token-based (mimicking the anonymity and peer-to-peer nature of physical cash) or account-based (requiring identity verification by an intermediary) 2526. 2. Wholesale CBDCs (wCBDC): Restricted exclusively for use by commercial banks and major financial institutions for large-scale, interbank settlements 2223. Wholesale CBDCs often utilize distributed ledger technology (DLT) to make cross-border transactions, currency exchanges, and securities trading instantaneous via "atomic settlement" (where the asset and payment are exchanged simultaneously) 2227.

Furthermore, retail CBDCs can be deployed using a one-tier model (where the central bank handles all customer onboarding and disputes directly) or a two-tier/hybrid model 2228. Almost all central banks have rejected the one-tier approach, opting instead for a two-tier system where the central bank manages the core ledger, but private commercial banks and payment providers interface directly with the consumer 222850.

Structuring the Digital Economy: A Comparison

| Feature | Cryptocurrencies (e.g., Bitcoin) | Commercial Bank Money (e.g., Venmo, Chase) | Retail CBDC (Two-Tier Model) |

|---|---|---|---|

| Issuer | Decentralized network protocol | Private commercial banks | Sovereign Central Bank |

| Liability / Risk | No issuer backing; high price volatility | Private liability; subject to bank failure | Sovereign liability; totally risk-free |

| Underlying Tech | Public, permissionless Blockchain | Centralized private databases | Centralized databases or permissioned DLT |

| Privacy | Pseudonymous but publicly traceable | Monitored by private banks and regulators | Dictated by state policy (anonymity varies) |

| Primary Goal | Decentralized financial sovereignty | Everyday commerce, lending, and profit | Monetary sovereignty, efficiency, inclusion |

Table 1: A structural comparison of modern digital payment instruments based on central bank taxonomies 36222326.

Global CBDC Adoption: Pioneers and Pilots

As of mid-2026, 146 countries and currency unions - representing over 98% of global GDP - are actively researching, piloting, or deploying CBDCs 51. Yet, the transition from macroeconomic theory to real-world consumer adoption has proven incredibly difficult.

The Retail First-Movers: The Bahamas, Jamaica, and Nigeria

Currently, only three nations possess officially launched, fully live retail CBDCs: The Bahamas (which launched the Sand Dollar in 2020), Nigeria (the eNaira in 2021), and Jamaica (the JAM-DEX in 2022) 5129.

Despite their status as global pioneers, all three have faced overwhelmingly sluggish retail adoption 2053. In The Bahamas, the Sand Dollar was explicitly designed to boost financial inclusion across its archipelago, offering zero transaction fees and 100% offline payment capabilities 5154. Yet, by 2026, there is only roughly $1.4 million worth of Sand Dollars in circulation - accounting for less than 0.1% of the total Bahamian currency in circulation 5154.

In Nigeria, a nation boasting over 220 million citizens, the eNaira reached roughly 10 million active users by 2024, but absolute transaction values remain muted 5556. The IMF noted that early rollout errors - such as restricting initial access solely to users who already had traditional bank accounts - stunted its growth 53. Furthermore, due to broader economic instability, many tech-savvy Nigerians bypass the eNaira entirely, preferring to transact using private US dollar stablecoins (like USDT) on alternate blockchain networks 56. The IMF warns that retail CBDCs face a classic "chicken-and-egg" problem: consumers will not download a CBDC wallet without widespread merchant acceptance, and merchants refuse to upgrade their point-of-sale systems without evident consumer demand 2053.

China's e-CNY: The Largest Digital Currency Experiment

China operates by far the world's most extensive CBDC pilot with its digital yuan (e-CNY) 2051. By late 2025, the e-CNY ecosystem had processed over 3.4 billion transactions worth an estimated 16.7 trillion yuan (roughly $2.3 trillion) across 230 million digital wallets 51.

Unlike Western nations, the People's Bank of China (PBOC) has integrated the e-CNY deeply into the fabric of domestic civic life 30. Citizens use the digital currency for public transportation, school tuition, retirement benefits, and local tax payments 20. To encourage adoption, the government has integrated e-CNY functionality directly into dominant private payment platforms like WeChat Pay and Alipay, and periodically distributes free digital cash via localized stimulus lotteries 2030.

China utilizes a "managed anonymity" model to balance privacy and surveillance. For low-tier transactions, consumers only need a mobile phone number to open an e-CNY wallet, which shields their true identity from the merchant 4528. However, because the state controls the telecommunications network, the PBOC retains the ultimate, centralized ability to track comprehensive money flows, monitor for capital flight, and freeze funds if necessary 452831.

India's Digital Rupee: Targeting the Informal Economy

India has emerged as an aggressive CBDC developer, rapidly expanding its e-Rupee pilots for both retail and wholesale markets 5530. By March 2025, the total value of digital rupees in circulation surged over 334% year-over-year to reach ₹10.16 billion ($122 million), serving roughly 5 million users across 16 participating banks 5155.

The Reserve Bank of India (RBI) views the e-Rupee not just as an efficiency tool, but as a mechanism to deter the nation's massive informal cash economy - often referred to as "black money" - which is used to shield wealth from taxation 45. By utilizing advanced offline payment features, the RBI is attempting to push digital state money into deep rural areas that lack reliable internet connectivity, circumventing the need for private banking infrastructure 5530.

The Western Response: Guarding Monetary Sovereignty

While emerging markets actively deploy CBDCs to boost domestic financial inclusion, major Western economies view the technology primarily through a defensive, geopolitical lens. However, the strategic paths of Europe and the United States have sharply diverged over the past three years.

The Digital Euro: Fending Off Digital Dollarization

The European Central Bank (ECB) is heavily committed to issuing a Digital Euro. Having formally entered a two-year "preparation phase" in late 2023, the ECB has actively drafted rulebooks and finalized vendor contracts to build the platform's technical infrastructure 293233. Assuming EU legislators pass the necessary regulatory framework in 2026, the ECB targets mid-2027 for live pilot testing, with a potential full public issuance by 2029 393435.

For the ECB, the Digital Euro is a tool for preserving European monetary sovereignty. Currently, European retail payments are overwhelmingly dominated by non-EU providers (specifically Visa and Mastercard) 63. Furthermore, ECB President Christine Lagarde has explicitly warned against the "digital dollarization" of European commerce, citing the threat of private, dollar-pegged stablecoins capturing the European digital economy 3964. To counter this, the ECB is advancing major wholesale DLT settlement solutions (Project Pontes) and shared ledger infrastructures (Project Appia) to ensure transactions settle in central bank money rather than private tokens 3935.

To provide compelling use cases for consumers, the ECB's Innovation Platform has heavily tested conditional payments 36. Partnering with industrial giants like Siemens and consultancies like Accenture, the ECB proved that programmable Digital Euros can drastically increase efficiency 66. For example, in B2B manufacturing, a conditional digital euro smart contract can automatically trigger a micro-payment the exact second a machine completes a specific production step, entirely automating working capital flows 3666. However, to protect commercial banks from a catastrophic "run" (where citizens instantly move all their deposits into risk-free Digital Euros during a financial panic), the ECB intends to implement strict holding limits on individual wallets 313335.

The UK Digital Pound: Exploring Private-Sector Alternatives

In the United Kingdom, the Bank of England (BoE) and HM Treasury spent years actively exploring a retail CBDC, colloquially dubbed "Britcoin" 3768. However, in May 2026, UK authorities formally signaled they were slowing the project down 38.

Skepticism has mounted regarding the actual utility of a retail CBDC, given the existing efficiency of the UK's domestic Fast Payment Systems 3839. Through its "Digital Pound Lab," the BoE discovered that implementing robust offline payment functionality - a crucial requirement for resilience - was technically daunting due to the persistent risk of offline double-spending and counterfeiting 39. Consequently, the UK is pausing to evaluate whether private-sector innovations - specifically "tokenized commercial bank deposits" - can deliver the benefits of programmability, speed, and cross-border efficiency without requiring the central bank to manage complex retail infrastructure 38.

The United States: Legislative Bans and the Stablecoin Pivot

The United States has executed the most dramatic policy pivot. While the Federal Reserve spent several years researching digital dollar mechanics (such as Project Cedar), the concept of a US CBDC devolved into a highly contentious domestic political issue 214041. Critics strongly argued that a retail digital dollar would grant the federal government unprecedented surveillance powers over citizen spending habits 73.

In early 2026, the US Senate passed the "21st Century ROAD to Housing Act" via a sweeping bipartisan vote of 89-10. Tucked inside this broader legislation was a provision that explicitly bans the Federal Reserve from issuing a retail CBDC until at least the end of 2030 7442. In May 2026, US Treasury Secretary Scott Bessent reaffirmed this stance, stating that the current administration had taken a digital dollar entirely "off the table" due to surveillance and civil liberty fears 7342.

Instead, the US strategy has shifted aggressively toward leveraging the private sector. By establishing regulatory frameworks for private, dollar-pegged stablecoins (via legislation like the CLARITY Act), the US is allowing private cryptographic companies to digitize the dollar on public blockchains 7374. This effectively exports digital USD supremacy globally, expanding dollar hegemony without expanding the Federal Reserve's balance sheet or surveillance apparatus 3873.

The Core Dilemma: Privacy vs. State Surveillance

As the history of money shifts from analog cash to central bank cryptography, policymakers and technologists face an inescapable trade-off: balancing consumer privacy against regulatory oversight 2831.

Physical cash is inherently anonymous. If CBDCs are designed with "high data intensity" - recording the identities of both transacting parties on a centralized state ledger - they offer incredibly powerful tools for governance 28. They can drastically reduce money laundering, ensure tax compliance, and enable highly targeted welfare and stimulus payments 3645. However, this exact same architecture enables potentially dystopian levels of financial surveillance 31. In such a system, a government could theoretically track every purchase, freeze the wallets of political dissidents, or program expiration dates on money to force consumer spending 3173.

Conversely, "low data intensity" designs (like token-based CBDCs that mimic the untraceable anonymity of physical cash) protect civil liberties but open the door to unchecked illicit finance and capital flight, directly conflicting with international Anti-Money Laundering (AML) standards like the FATF travel rule 2831. Central banks are actively exploring Privacy-Enhancing Technologies (PETs) and zero-knowledge proofs to thread this needle 3143. For global central banks, navigating this "privacy vs. surveillance" dilemma will be the defining technological and ethical challenge of the coming decade 3177.

Bottom line

The history of money is fundamentally the history of how human societies record debt, quantify obligation, and establish trust. From the clay tablets of ancient Mesopotamia and the wooden tally sticks of medieval Europe to the cryptographic blockchains of Bitcoin, the technological medium has evolved, but the necessity of a reliable ledger remains absolute. As we look toward the 2030s, it remains deeply uncertain whether state-backed retail CBDCs will overcome public skepticism and privacy fears to achieve mass adoption, or if a combination of private stablecoins and wholesale interbank digital currencies will ultimately dominate. What is certain, however, is that the digitization of sovereign currency is fundamentally rewriting the relationship between the state, the central bank, and the financial privacy of the individual.