The Future of the US Dollar as the Reserve Currency

The US dollar is not facing an imminent collapse, but it is undergoing a slow, structural decline in its share of global reserves as a multipolar financial world takes shape. Driven by the fear of geopolitical sanctions and rising US debt, foreign central banks are actively diversifying into gold and building alternative local-currency payment networks. While the dollar's unmatched liquidity will preserve its dominance for years, this gradual erosion threatens to raise US borrowing costs, boost domestic inflation, and squeeze the purchasing power of everyday investors over the coming decades.

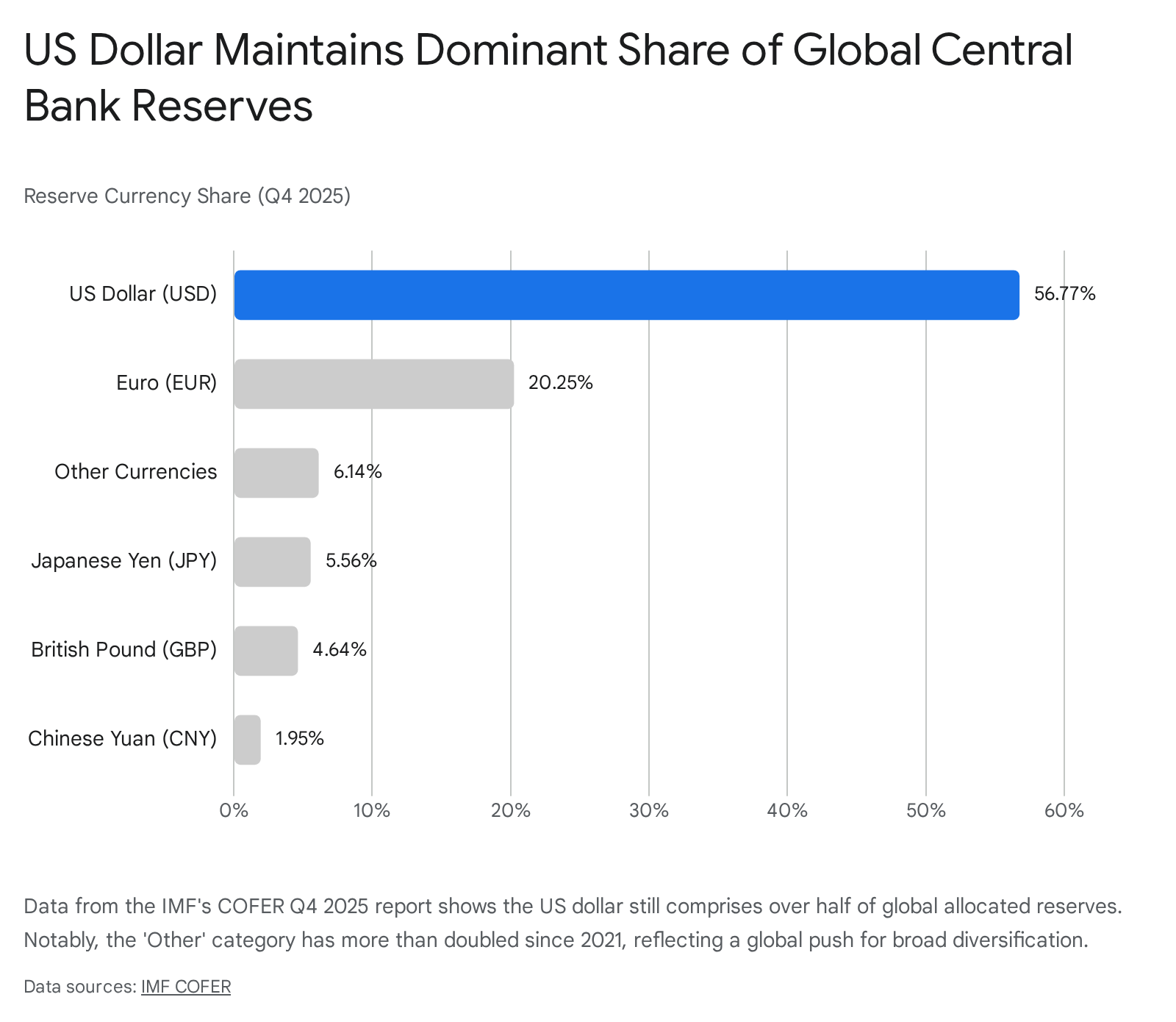

The State of the Dollar Today

Since the Bretton Woods agreement of 1944, the US dollar has operated as the undisputed anchor of global capitalism. It is the lifeblood of international trade, the benchmark for pricing commodities like oil, and the ultimate safe haven during times of global panic 12. Trillions of dollars in global debt are denominated in USD, creating a massive web of cross-border lending and trade finance that relies on American capital markets 3.

However, over the last two decades, the dollar's grip has visibly loosened. According to the International Monetary Fund's Currency Composition of Official Foreign Exchange Reserves (COFER) data for the fourth quarter of 2025, the US dollar accounted for 56.77% of allocated global foreign exchange reserves 45.

While this still dwarfs all other competitors, it represents a significant decline from the roughly 71% share the dollar commanded in the year 2000 15.

If the dollar is slowly losing ground, where is the money going? The data reveals a story not of immediate abandonment, but of calculated diversification.

| Reserve Currency | Q4 2025 Share (%) | Change from Previous Quarter | Long-Term Trend |

|---|---|---|---|

| US Dollar (USD) | 56.77% | Down 0.15 pp | Slow, steady decline from 71% in 2000 5 |

| Euro (EUR) | 20.25% | Down 0.08 pp | Generally stable around 20% over the last decade 5 |

| Japanese Yen (JPY) | 5.56% | Down 0.25 pp | Dropping sharply due to Bank of Japan policy shifts 5 |

| British Pound (GBP) | 4.64% | Down 0.21 pp | Stable, but vastly lower than its historic peak 5 |

| Chinese Yuan (CNY) | 1.95% | Up 0.02 pp | Stalled near 2% due to strict Chinese capital controls 5 |

| "Other" Currencies | 6.14% | Up 0.88 pp | More than doubled since 2021 (AUD, CAD, CHF, etc.) 4 |

Despite this slipping percentage, the dollar remains dominant for three main reasons: the sheer size and robust growth of the US economy, deep institutional trust in American democratic and legal structures, and simple financial inertia 2. Transitioning away from the dollar is incredibly difficult because the global financial system is built entirely on its architecture. Competing nations may boast some of these facets, but the US is uniquely positioned with all three advantages simultaneously 2.

The Catalyst: Sanctions and Geopolitical Shifts

If the dollar is so convenient, why are nations actively trying to replace it? The answer lies in the intersection of macroeconomics and national security.

The turning point for the modern reserve system occurred in 2022. When the United States and its European allies froze approximately $300 billion in Russian central bank reserves following the invasion of Ukraine, it sent a shockwave through the Global South 789. The message was clear: dollar reserves are not just neutral financial assets; they are instruments of US foreign policy. If a sovereign nation runs afoul of Washington, its national savings can be instantly rendered inaccessible.

This weaponization of finance has permanently altered central bank behavior. A May 2025 survey of 84 central bank reserve managers revealed that 88% believe the weaponization of reserves will have permanent consequences for global reserve management 7. Furthermore, 76% now classify US sanctions risk as a "significant" factor in their asset allocation decisions - a massive jump from just 30% before 2022 7.

Recent joint research by the European Central Bank (ECB) and the IMF provides statistical backing to this shift. The data shows a direct correlation between global trade invoicing patterns and geopolitical alignment 6. Countries that are geopolitically distancing themselves from the United States - such as Russia, Belarus, Kyrgyzstan, and Uzbekistan - have seen the share of their exports invoiced in US dollars and euros drop by 10 to 50 percentage points compared to their 2015-2019 averages 6. Central banks are no longer just managing financial risk; they are managing geopolitical survival.

Gold Overtakes US Treasuries

Because fiat currencies rely on the trust of their issuing governments, central banks seeking true financial independence have turned to an ancient alternative: physical gold.

By early April 2026, the global financial architecture crossed a massive, symbolic threshold. For the first time in 30 years, the total market value of gold held in foreign central bank reserves officially surpassed the value of foreign U.S. Treasury holdings 87813. As of that date, global official gold reserves reached an estimated valuation of $4 trillion, edging out the $3.9 trillion held in US sovereign debt 7.

This inversion signals a profound shift. Reserve managers are increasingly prioritizing durability, portability, and absolute neutrality over the liquidity and yield offered by US bonds 87. Since 2022, central banks have consistently absorbed over 1,000 metric tonnes of gold annually, effectively putting a hard floor under the precious metal's price and decoupling it from its traditional inverse relationship with interest rates 879. According to the World Gold Council, nearly 18% of all the gold ever mined is now held by central banks 813.

| Global Rank | Country | Official Gold Holdings (Tonnes, Q1 2026) | Gold as % of Total Foreign Reserves | Strategic Context |

|---|---|---|---|---|

| 1 | United States | 8,133.5 | ~69% | Largest holder, but has not been a net buyer in decades 910. |

| 2 | Germany | 3,350.3 | ~69% | Legacy European holdings that remain static 910. |

| 5 | China | 2,313.4 | ~9% | On a massive accumulation streak. Analysts suspect actual holdings are far higher than officially reported 9710. |

| 6 | Russia | 2,304.7 | ~29% | Accelerated buying to sanction-proof the economy post-2022 10. |

| N/A | Uzbekistan | 416.0 | ~87% | Highest concentration ratio among active buyers; a clear bet on monetary independence 910. |

For nations like China, gold is no longer a peripheral asset. The People's Bank of China (PBOC) extended its gold purchasing streak to 16 consecutive months leading into early 2026, bringing its official holdings to over 2,313 metric tonnes 97. By converting dollar-denominated assets into physical bullion housed within their own borders, nations effectively eliminate "counterparty risk" - the risk that the US government might freeze their assets or default on its obligations. This sustained demand has led financial institutions like JPMorgan to forecast that gold prices could push toward $5,000 an ounce by the end of 2026 9.

BRICS Infrastructure vs. The "BRICS Currency"

While gold provides a safe store of value, it cannot easily be used to buy microchips, settle energy contracts, or pay for agricultural imports. To truly bypass the US dollar, nations need alternative payment plumbing. This is where the BRICS coalition (Brazil, Russia, India, China, South Africa, and recent additions like the UAE, Egypt, and Ethiopia) is focusing its efforts 16.

A widespread misconception is that BRICS is preparing to launch a physical, euro-style "BRICS Currency" in the immediate future. In reality, creating a monetary union between economies as disparate as China and India is fraught with insurmountable macroeconomic challenges 1718. Instead, the bloc is aggressively building cross-border payment interoperability - digital plumbing that routes around the Western-dominated SWIFT network 18.

BRICS Pay and Digital Bridges

Central to this effort is BRICS Pay, a cross-border payments concept designed to interconnect the national payment systems of member states 181920. Rather than relying on a centralized dollar clearinghouse, the emerging multipolar financial architecture uses blockchain-based rails to link domestic systems directly. By connecting platforms like Brazil's Pix, India's UPI, and Russia's SPFS, trade can be settled instantly in local currencies 192021. Pilot tests for BRICS Pay involving Brazil, Russia, and China are scheduled for the end of 2026, with financial analysts forecasting full operational capability closer to 2030 1922.

Similarly, the mBridge project - a multi-lateral Central Bank Digital Currency (CBDC) platform initially backed by the Bank for International Settlements - has already processed over $55 billion in transaction volume, roughly 95% of which was settled in digital yuan 2211. The infrastructure for a post-dollar world is rapidly moving from theory to reality.

The BRICS Grain Exchange

To ensure these alternative payment systems have actual goods flowing through them, Russia proposed the BRICS Grain Exchange, which was formally endorsed in the October 2024 Kazan Declaration 2412. The BRICS nations currently account for roughly 44% of global grain production and a massive share of global consumption 2412.

Historically, global agricultural commodities have been priced in US dollars on exchanges in Chicago. By establishing an independent pricing index and a commodity exchange that settles trades in national currencies, the bloc is attempting to remove the dollar from the base layer of human survival: food security 1213.

These initiatives have provoked sharp responses from Washington. By early 2026, President Donald Trump aggressively warned BRICS nations that attempts to replace the US dollar or back a rival currency would be met with 100% tariffs on their exports to the US, a threat that South Africa and Brazil publicly condemned 1617. Despite the rhetoric, under India's 2026 BRICS chairship, the coalition continues to quietly advance its technical payments infrastructure rather than rushing a symbolic currency launch 1824.

The Rise of Competitor Currencies

If the US dollar eventually loses its absolute monopoly, it will likely be replaced not by a single sovereign currency, but by a fragmented basket of regional currencies.

The Chinese Yuan (RMB)

China is the world's premier manufacturing and trading powerhouse, making the renminbi (RMB or Yuan) the most obvious challenger to the dollar. The currency has seen undeniable momentum in commercial use. By February 2025, the RMB surpassed the euro to become the world's second most-used trade finance currency, commanding a record high share of 6.34% 27. Furthermore, China's Cross-Border Interbank Payment System (CIPS) expanded to over 1,680 participants across 180 countries by mid-2025, clearing roughly $100 billion in daily transactions 711.

However, the yuan is fundamentally constrained by Beijing's own economic policies. To prevent destabilizing capital flight - a lesson learned during a severe market scare in 2015 - the People's Bank of China maintains strict capital controls and a tightly managed exchange rate 14. Because the RMB is not fully and freely convertible for international investors, global central banks are hesitant to hold it as a primary store of value, keeping its share of global reserves stalled at just 1.95% 511.

Interestingly, while headlines often claim China is "dumping" dollars, macroeconomic data suggests a different reality. Rather than exiting the dollar entirely, China has been migrating its dollar assets off the central bank's official balance sheet and onto the balance sheets of state-owned commercial banks 29. The aggregate dollar position of the Chinese banking system actually surged past $4 trillion by the end of 2025 29. China still relies heavily on the dollar; it is merely rearranging the institutional architecture to protect itself from direct central bank sanctions.

The Euro, Yen, and Rupee

Other competitors face their own structural hurdles that prevent them from unseating the dollar: * The Euro: Consistently holding around 20% of global reserves, the Euro is the only true runner-up to the dollar 45. However, the European Union lacks a unified fiscal policy and a deep, universally integrated sovereign bond market comparable to US Treasuries. * The Japanese Yen: Japan's currency has historically acted as a major reserve and funding vehicle. But as the Bank of Japan was forced to raise interest rates to normalize policy in late 2025, the yen's share of global reserves experienced its sharpest drop since 2009, falling to just 5.1% in Q1 2025 5. * The Indian Rupee (INR): The Reserve Bank of India (RBI) has enacted sweeping regulatory reforms to internationalize the rupee. In 2025, amendments to the Foreign Exchange Management Act allowed foreign banks to open Special Rupee Vostro Accounts to settle trade, and permitted exporters to hold offshore foreign currency accounts 151617. While bilateral Rupee-Ruble trade hit $8.2 billion in 2024 to circumvent SWIFT sanctions, the rupee still accounts for less than 2% of global forex turnover. Global adoption remains an uphill battle 1617.

Economic Theory: Fiat Money as the "Equity" of a Nation

To understand why a currency gains or loses reserve status, it helps to view fiat money through a different economic lens. In their influential academic work Money Capital, economists Patrick Bolton and Haizhou Huang propose a paradigm-shifting framework: fiat money functions as the equity capital of a sovereign nation 18193520.

Just as a corporation issues shares of stock to raise capital for investments, a sovereign nation prints fiat currency 35. The "backing" of this currency is not physical gold in a vault, but the future productivity, output, and taxable capacity of the nation itself 35.

When a central bank prints money to finance highly productive investments - such as building domestic infrastructure, funding technological innovation, or expanding manufacturing capacity - it generates economic output that exceeds the new money created. Under this model, the nation's "equity value" grows without causing severe inflation. Bolton and Huang point to China's massive economic expansion over the last four decades, and the US industrial boom during World War II, as examples of nations printing money to successfully finance positive-net-present-value investments 18.

However, if a corporation issues millions of new shares just to pay its executive bonuses, the existing shareholders suffer massive "dilution" as the stock price plummets. Similarly, if a sovereign nation prints trillions of dollars merely to fund domestic consumption, service existing debt, or cover massive deficits without expanding its real economic output, the existing holders of that currency suffer the equivalent of shareholder dilution: inflation 1821.

This is the core risk facing the US dollar today. If global investors and foreign central banks feel that the United States is continuously diluting the dollar's value to mask domestic fiscal deficits, they will naturally seek to protect their "wealth" by selling their shares (US Treasuries) and buying alternative assets (Gold) 2138.

Historical Precedent: The Fall of the British Pound

For Americans accustomed to dollar hegemony, it is easy to assume the current system is permanent. Yet history shows that reserve currencies are cyclical, and transitions are painfully slow.

At the height of the British Empire in the late 19th and early 20th centuries, the British Pound (GBP) was the undisputed anchor of global finance. It took decades of economic shifts for the US dollar to unseat it. As early as the 1870s, the US surpassed Britain in absolute economic size, but the Pound maintained its global supremacy due to the unparalleled depth of the London money markets and simple institutional inertia 3922.

The transition was catalyzed by World War I, which forced Britain off the gold standard and saddled the empire with immense debt 3941. By the mid-1920s, the US Federal Reserve aggressively developed New York's financial markets, allowing the dollar to overtake the pound in global trade credit, specifically through bankers' acceptances 22.

Even then, the pound remained remarkably sticky. At the outbreak of World War II in 1939, the GBP still accounted for 66% of global reserves, compared to the dollar's 31% 42. It was only after Britain was left effectively bankrupt by 1947 that the dollar completely took over the global stage 41.

The lesson for today is twofold: first, reserve currency transitions are slow, agonizing processes that take decades to play out; second, they are ultimately driven by the rising challenger developing superior, deeper financial markets 2242. Today, while China and the BRICS coalition are gaining global trade share, their financial markets remain heavily restricted and vastly shallower than Wall Street. Until a true challenger replicates the depth, liquidity, and legal transparency of the US Treasury market, the dollar's collapse will remain a slow erosion rather than a sudden cliff 3.

The Domestic Impact: Borrowing, Mortgages, and Inflation

For the average citizen, debates about macroeconomic theory and foreign central bank reserves can seem abstract. But the long-term status of the US dollar directly impacts everyday financial realities, from grocery bills to housing affordability.

Being the issuer of the world's reserve currency provides the United States with an "exorbitant privilege." Because foreign central banks and global corporations need dollars to conduct international business, there is a constant, massive demand for US government debt. This artificial demand suppresses yields, allowing the US to borrow money at artificially low rates. Vanguard estimates this privilege saves the US government roughly $80 billion annually in interest payments 12.

If global demand for dollar safe-assets evaporates, that dynamic violently reverses. A recent working paper from the Hoover Institution modeled this exact scenario. Their analysis found that a total loss of demand for dollar reserve assets would result in a steady-state depreciation of the dollar's real value by roughly 7.6%, and would force US long-term interest rates to rise by 0.9% 43.

A permanent 1% increase in the baseline cost of capital would send shockwaves through the domestic economy. As noted by the Consumer Financial Protection Bureau (CFPB), mortgage rates have already fluctuated wildly in the post-pandemic era, severely impacting housing affordability 23. If reserve status is lost, baseline mortgage rates would structurally adjust higher. Auto loans would become more expensive, and consumer credit card rates would climb, putting severe pressure on the American middle class 4323. Furthermore, a depreciating dollar means that imported goods - from electronics to clothing - become significantly more expensive, importing inflation directly to the American consumer 24.

How Portfolios and 401(k)s Will Respond

This macroeconomic shift forces everyday investors and retirement planners to rethink their strategies. If the US dollar loses its reserve status and depreciates sharply, domestic asset prices - such as real estate and the S&P 500 - will likely soar in nominal terms. However, this is largely an illusion driven by a weakening measuring stick 46.

Financial experts point out that if a stock portfolio rises by 5%, but the dollar loses 10% of its purchasing power due to inflation and currency debasement, the investor has actually lost real wealth 2446. Historically, during the stagflation of the 1970s - when the US abandoned the gold standard and the dollar weakened - stock markets appeared to hold their ground nominally, but delivered massive negative returns when adjusted for inflation 46. A depreciating dollar acts as a hidden tax on retirement savings, silently eroding the true purchasing power of a 401(k) 4647.

Because of these risks, financial advisors and major asset managers like BlackRock are actively shifting their long-term strategies 4825. To build financial resilience against de-dollarization, experts recommend several diversification strategies:

- International Equities: Earning dividends in Euros, Yen, or Emerging Market currencies acts as a natural buffer. If the US dollar weakens, the relative value of those foreign earnings actually increases when converted back to USD, turning currency exposure into a return enhancer 4625.

- Physical Gold: As global central banks drive up the price of bullion, many wealth managers advise retail investors to hold a 5% to 15% allocation in physical gold or precious metal IRAs 50512653. Unlike paper assets, gold cannot be diluted by central bank printing and carries no counterparty risk 3853.

- Hard Assets and Commodities: Investments tied to real-world resources - such as energy, agriculture, and real estate - tend to hold their inherent value during periods of currency volatility, providing a bulwark against inflation 4627.

Bottom line

The US dollar is not going to vanish overnight, and its vast liquidity ensures it will remain the cornerstone of global finance for years to come. However, the era of its uncontested global monopoly is quietly drawing to a close. As geopolitical tensions rise and the US national debt expands, major powers across the Global South are systematically insulating themselves by hoarding gold and developing local-currency trade networks. For everyday investors, ignoring this macro shift is a risk; preparing for a multipolar financial future requires diversifying beyond dollar-denominated assets and rethinking the true, inflation-adjusted value of their retirement portfolios.