4 Scenarios for the Future of CBDCs by 2035

Direct Answer: The 2035 Trajectory of Central Bank Digital Currencies By 2035, the global financial architecture will have fundamentally bifurcated, abandoning the premise of a single, universal monetary standard. The trajectory indicates that advanced Western economies will heavily prioritize "wholesale" Central Bank Digital Currencies (CBDCs) - focusing on upgrading the backend plumbing of the global interbank system through projects like the Bank for International Settlements' (BIS) Project Agorá - while cautiously delaying direct-to-consumer "retail" variants due to intense political pushback regarding privacy and commercial bank disintermediation. Conversely, emerging markets and geopolitically assertive nations, including China, India, and the United Arab Emirates, will have fully deployed highly programmable, retail-facing digital currencies. These nations will leverage CBDCs to bypass Western-dominated financial rails, execute precision fiscal policy through targeted welfare, and cement absolute domestic monetary sovereignty. Ultimately, physical cash will survive as a mandated fallback, but it will be marginalized by a complex global ecosystem of tokenized fiat, algorithmically governed compliance, and pervasive digital transaction surveillance.

The Everyday Hook: The Coffee Shop Illusion

Consider a standard, everyday transaction: purchasing a morning coffee. A customer taps a smartphone or a plastic card against a merchant's payment terminal, a satisfying chime confirms the interaction, and the barista hands over the coffee. To the consumer, this transaction feels instantaneous, carrying the same finality as handing over a physical five-dollar bill.

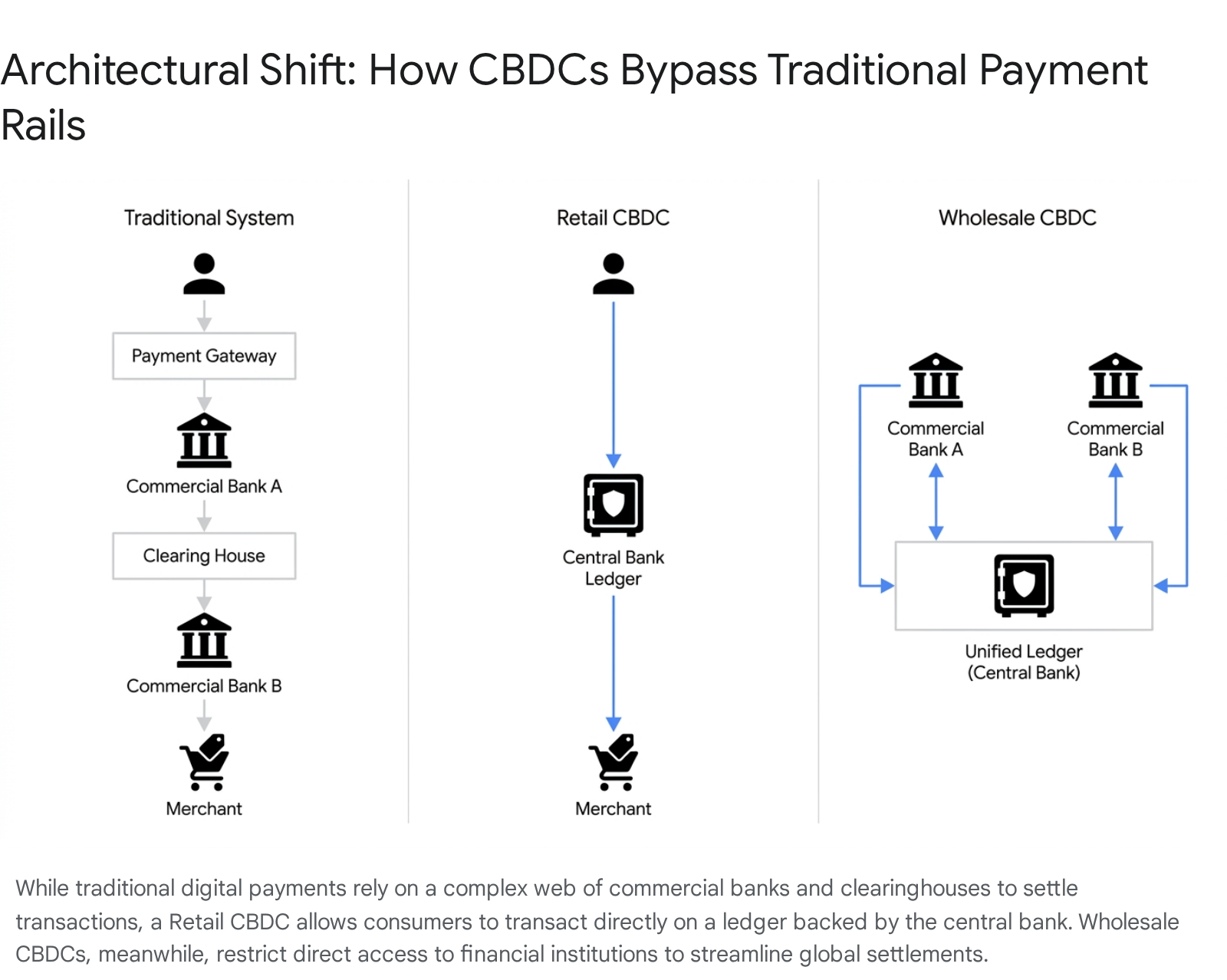

However, beneath the surface of the modern economy, that digital transaction is a chaotic, multi-day relay race. When an application like Venmo, Apple Pay, or a standard Visa card is utilized, actual money does not move instantly. Instead, a sprawling network of payment gateways, acquiring banks, clearinghouses, and commercial bank databases exchange encrypted messages promising to settle the debt later 12. This settlement process routinely takes days to clear and incurs hidden merchant interchange fees ranging from 2% to 3.5% 13. Furthermore, the money sitting in a Venmo balance or a standard checking account is not a direct asset issued by the government; it is fundamentally an unsecured IOU from a private financial institution, bearing commercial counterparty risk 44.

A Central Bank Digital Currency (CBDC) fundamentally rewrites this deeply entrenched architecture. If that same coffee were purchased using a retail CBDC, no commercial bank, credit card network, or private intermediary would need to clear the funds. The digital token would move directly from the consumer's central bank-issued digital wallet to the merchant's central bank wallet in real time 46. It is the digital, programmable equivalent of handing over a physical banknote - a direct, risk-free liability of the sovereign state, executed at the speed of light 56.

FAQ: What Exactly is a CBDC and How Does it Differ from Bitcoin or Venmo?

As central banks worldwide race to digitize their economies, a critical need arises to correct pervasive public misconceptions regarding what CBDCs are - and what they represent for the future of civil liberties and finance.

Misconception 1: CBDCs are just a government-controlled version of Bitcoin. This is fundamentally incorrect, both economically and technologically. Cryptocurrencies like Bitcoin operate on decentralized, permissionless blockchains where no single entity controls the ledger, and the asset's value fluctuates wildly based on market demand and speculative trading 17. A CBDC is the exact opposite. It is entirely centralized, managed, and issued exclusively by a nation's central monetary authority (such as the Federal Reserve, the European Central Bank, or the People's Bank of China). Its value is strictly pegged one-to-one with the national fiat currency; a digital euro will always perfectly equal a physical euro coin 110.

Misconception 2: We already have digital money through commercial banking apps. While it is true that the vast majority of modern money exists as digital entries in banking systems, there is a profound macroeconomic and legal distinction. The digital dollars in a standard commercial checking account are liabilities of that specific bank. If the bank fails, the depositor relies on government deposit insurance to be made whole. A CBDC, conversely, is a direct claim on the central bank itself 45. It carries absolutely zero commercial credit risk or liquidity risk. When a citizen holds a CBDC, they are holding a digital artifact as risk-free as the physical paper currency printed by a sovereign mint 89.

Misconception 3: CBDCs will completely and immediately replace physical cash. While CBDCs could technologically substitute for physical cash, global regulatory consensus strongly emphasizes that CBDCs are designed to complement cash, not replace it 9. Policymakers, particularly within the European Central Bank (ECB) and the International Monetary Fund (IMF), recognize the political toxicity of a purely cashless society. Consequently, significant engineering efforts are being directed toward "offline" transaction capabilities via near-field communication (NFC) or Bluetooth, mimicking the physical nature of cash during power outages or network failures 101411.

FAQ: Retail vs. Wholesale: The Two Divergent Paths of Digital Money

The most critical distinction in the global CBDC landscape is the target user. The development of sovereign digital money has split into two parallel, non-exclusive tracks: Wholesale and Retail. By 2035, these two tracks will dictate entirely different aspects of global commerce 212.

The Wholesale Track: Upgrading the Financial Plumbing

Wholesale CBDCs (wCBDC) are restricted strictly to licensed financial institutions. They function as tokenized central bank reserves and are designed exclusively to settle high-value interbank transactions, cross-border transfers, and securities trades 213. The current cross-border payment system, reliant on SWIFT and correspondent banking, is notoriously slow, costly, and fragmented 1814.

Wholesale CBDCs allow for "atomic settlement" - the simultaneous, instant approval and clearing of payments across global jurisdictions, where every leg of a transaction executes at the exact same instant, or not at all 41320. A premier example is the Bank for International Settlements' (BIS) Project Agorá, which reached its prototype phase in mid-2026 2122. Involving seven major central banks (including the Bank of England, Bank of Japan, and the New York Federal Reserve) and over 40 private financial institutions, Agorá merges tokenized commercial bank deposits with wholesale central bank money on a shared, programmable unified ledger 1422. Crucially, it does not aim to replace commercial banks. Instead, it provides them with vastly superior rails, processing anti-money laundering (AML) checks, financial sanctions screening, and fraud detection in parallel to complete international settlements in seconds 142115.

The Retail Track: The Public Faucet

Retail CBDCs (rCBDC) are designed for the general public, functioning as digital cash for everyday consumer transactions. They aim to boost financial inclusion for the unbanked, drastically reduce merchant interchange fees, and provide a sovereign alternative to the monopolistic power of private payment rails (like Visa/Mastercard) and decentralized stablecoins (like USDT or USDC) 2610.

However, as detailed in the IMF's 2025 Virtual Handbook updates, global exploration of wholesale CBDCs is advancing at a much faster, unified pace than retail variants 1617. Retail CBDCs introduce severe, potentially destabilizing political and systemic risks regarding data privacy and commercial bank disintermediation, causing democratic governments to proceed with extreme caution 1718.

| Feature | Retail CBDC (rCBDC) | Wholesale CBDC (wCBDC) |

|---|---|---|

| Primary End Users | General public, consumers, unbanked populations, retail businesses 112. | Central banks, commercial banks, institutional entities, clearinghouses 212. |

| Core Economic Objective | Financial inclusion, digitization of everyday payments, direct government welfare distribution 91327. | Interbank clearing efficiency, cross-border atomic settlement, institutional asset tokenization 1314. |

| Transaction Dynamics | High volume, low individual value (requires infrastructure capable of thousands of TPS) 2. | Low volume, exceptionally high individual value 2. |

| Access & Distribution Model | Digital wallets distributed indirectly via commercial banks or directly via central bank portals 24. | Permissioned unified ledgers and APIs restricted exclusively to licensed financial institutions 2228. |

| Primary Systemic Risks | Bank disintermediation (deposit flight), privacy erosion, state surveillance fears, low organic adoption 419. | Interoperability hurdles, geopolitical misalignment, technological standardization disputes 2020. |

FAQ: The Global Divide: Why the East Sprints While the West Hesitates

A comprehensive analysis of global pilot programs reveals a stark geopolitical divide that will dictate the global financial system of 2035. Emerging markets and Eastern nations are aggressively deploying live CBDCs, utilizing them as potent instruments of statecraft, economic modernization, and domestic control. Conversely, Western democracies are trapped in a cycle of protracted research, paralyzed by civil liberty concerns and lobbying from a deeply entrenched commercial banking sector.

The Vanguard: China and India Lead the Global Trajectory

China (e-CNY): The People's Bank of China (PBOC) operates the world's largest, most advanced, and most consequential CBDC pilot. As of late 2025, the digital yuan had opened more than 325 million individual wallets and processed an astounding 3.48 billion cumulative transactions worth 16.7 trillion yuan (approximately $2.37 trillion USD) 321. The e-CNY is deeply integrated into daily life, accepted in major transit systems across a dozen cities, utilized for automated tax collections, and embedded within dominant payment platforms like WeChat Pay and Alipay 32223.

More critically, China is executing a structural paradigm shift that will ripple globally. Effective January 1, 2026, the PBOC transitioned the e-CNY from a mere physical cash replacement (M0 money supply) to an interest-bearing "digital deposit money" (M1) model 2124. Under this upgraded framework, commercial banks pay interest on digital yuan wallet balances, treating them as bank deposit liabilities protected by deposit insurance 21. This highly sophisticated hybrid model allows the digital renminbi to perform core monetary functions while mitigating the risk of commercial bank disintermediation 24. Furthermore, China is aggressively pushing its CBDC into the geopolitical arena via Project mBridge - a multi-central bank platform involving the UAE, Hong Kong, Thailand, and Saudi Arabia - aiming to bypass the US dollar-dominated SWIFT system for cross-border commodity settlements 352526.

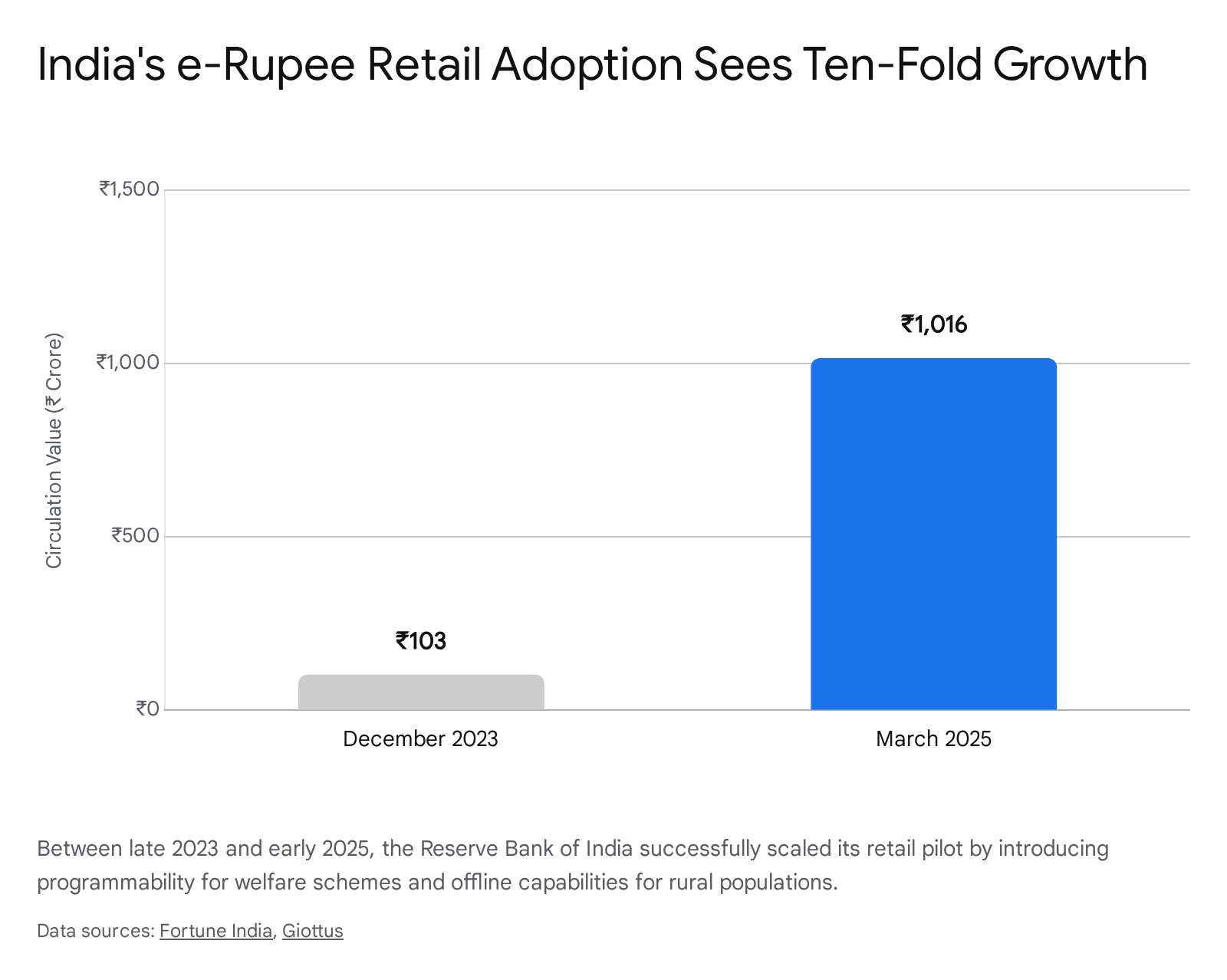

India (e-Rupee): India's trajectory exemplifies rapid, state-directed technological adoption utilizing programmability to solve domestic inefficiencies. Launched in late 2022, the retail e-Rupee expanded ten-fold over a 15-month period, crossing ₹1,016 crore in circulation by March 2025, supported by over 6 million users and 17 commercial banks 273928.

India's strategy hinges heavily on "programmability" for social welfare. Under government initiatives like the Subhadra Yojana, welfare transfers are distributed in e-Rupee tokens that are cryptographically programmed to be spent only at specific merchants or within set timeframes 2729. This ensures public funds are not misallocated or lost to bureaucratic friction. Simultaneously, the Reserve Bank of India (RBI) is actively developing and testing offline functionalities to ensure the CBDC functions in remote, low-connectivity rural regions, treating the technology as a vital tool to bridge the last mile of financial inclusion 392829.

The Struggle for Adoption: Early Adopters Face Apathy

First-mover advantage in technology does not guarantee systemic success, as evidenced by nations that launched CBDCs before fully securing public trust or establishing clear use cases.

Nigeria (eNaira): Launched in October 2021 as Africa's first CBDC, the eNaira has struggled with a chronic lack of organic adoption. Despite early fanfare, IMF reports in 2024 and 2025 confirmed that roughly 98.5% of the 13 million downloaded eNaira wallets remained entirely inactive, with transactions representing a negligible 0.36% of total currency in circulation 424330. Plagued by public skepticism and a preference for cash and decentralized stablecoins (like USDT, which Nigerians actively use as a hedge against crippling domestic inflation), the eNaira has been derisively dubbed "E-vanish" by the public 45. To salvage the project, the Central Bank of Nigeria strategically partnered with blockchain firm Gluwa in 2024 to integrate its Credal blockchain API technology. By allowing unbanked citizens to build on-chain credit scores - completely independent of traditional banks - merely by using the CBDC, Nigeria hopes to incentivize organic adoption through immediate access to micro-loans and fintech services 314748.

The Bahamas (Sand Dollar): Launched in 2020, the world's first retail CBDC was born out of stark geographic and environmental necessity. It is prohibitively expensive to transport physical cash via armored boats across an archipelago highly vulnerable to severe weather events like Hurricane Dorian 732. While adoption currently sits at around 35% of the adult population (with over 160,000 active wallets), the Central Bank of the Bahamas aims to push adoption past 75% by heavily mandating commercial bank integration, proving that even in ideal geographic use-cases, transitioning public payment habits is remarkably slow 3334.

Western Hesitation: The Digital Euro and North American Reluctance

In stark contrast to Asian acceleration, Western central banks are progressing with deliberate caution, heavily constrained by democratic legislative processes.

The European Central Bank (ECB) entered a two-year formal "preparation phase" for a Digital Euro in late 2023, which concludes in October 2025 1135. If the European Parliament passes the requisite legislation in 2026, the ECB envisions initiating a pilot exercise in 2027, with a potential full issuance delayed until 2029 11. The ECB's hesitation stems from deep political sensitivities regarding state surveillance and the disruption of the commercial banking sector 10. Consequently, the ECB has aggressively marketed the digital euro as a resilient fallback mechanism that will "preserve Europeans' freedom of choice" and strictly "complement, not replace, cash" 101411.

The United States remains fundamentally entrenched in the theoretical research phase, hampered by intense political opposition citing fears of government overreach and the sheer lobbying power of the incumbent financial sector 1235. Canada went a step further; in September 2024, the Bank of Canada officially abandoned its active retail CBDC design program, concluding that Canada's high existing financial inclusion made a CBDC unnecessary, choosing instead to focus entirely on upgrading domestic Real-Time Rail (RTR) gross settlement systems 26.

FAQ: Will a CBDC Kill Commercial Banks and Financial Privacy?

The hesitation in the West is not merely political theater; it is rooted in two legitimate, systemic macroeconomic risks that could destabilize free societies: the disintermediation of the banking sector and the erosion of fundamental civil liberties.

The Disintermediation Dilemma: The Risk of Deposit Flight

The traditional commercial banking model relies entirely on taking in consumer deposits and lending them out (fractional reserve banking) to fuel economic growth via consumer mortgages and corporate business credit. If a central bank introduces a frictionless, state-backed retail CBDC, it creates a "risk-free" alternative to a commercial bank account 436. During times of economic stress - or simply lured by the seamless technology and elimination of fees - households might rapidly transfer their funds out of commercial banks and into their central bank digital wallets 454.

This phenomenon, known as "deposit flight," would starve commercial banks of the liquidity necessary to issue loans, effectively raising the cost of capital for the entire economy and potentially triggering localized banking crises 4854. To mitigate this existential threat, Western models propose heavily tiered systems. They intend to impose strict holding limits on individual CBDC wallets (for instance, capping a digital euro wallet at a maximum of €3,000) and ensure that zero interest is paid on standard retail CBDC holdings 537. This structural friction deliberately forces consumers to keep the bulk of their wealth in traditional, interest-bearing commercial bank accounts, reserving the CBDC strictly for day-to-day transactional utility.

The Privacy Paradox: Zero-Knowledge Proofs (ZKPs)

A retail CBDC, by its fundamental digital nature, creates an immutable, highly traceable footprint. The surveillance concern is acute: if every transaction is recorded on a central ledger, the state gains unprecedented, granular visibility into individual behavior 4. This "Big Brother" perception is the primary hurdle to adoption in democracies, where public trust in institutions is often fragile 419.

To solve this privacy paradox, central banks and the BIS are extensively researching and integrating advanced Privacy-Enhancing Technologies (PETs) 819. The Bank of England, alongside MIT, and the ECB are actively researching Zero-Knowledge Proofs (ZKPs) and Multi-Party Computation (MPC) 5638. A ZKP is a cryptographic breakthrough that allows a user to mathematically prove a statement is true without revealing any underlying data about the statement itself 5638.

In the context of a digital euro, a consumer could use a ZKP to prove to a merchant and the regulatory network that they have sufficient funds to clear a transaction, and that they are not on a terrorist watchlist, without ever revealing their true identity, their total account balance, or their transaction history to the central bank 5639. Furthermore, recent World Intellectual Property Organization (WIPO) patents connected to the digital euro propose a "Protocol-Level Privacy Enforcement System" combining Virtual Identity (VI) tokens to cryptographically enforce GDPR privacy laws in milliseconds 59. The ECB also proposes a dual-privacy model: "online" transactions would be pseudonymized for AML tracking, but "offline" transactions (using peer-to-peer NFC technology) would offer privacy identical to physical cash, with zero data recorded on the central ledger 3560.

4 Scenarios for the Future of Money by 2035

By analyzing the empirical data from global pilot programs, the BIS's future infrastructure frameworks, and scenario-planning exercises from institutions like the IMF, Deloitte, and Wharton, four distinct trajectories emerge for the state of the global financial system by 2035 4041426443. These scenarios hinge on two critical axes: the degree of Centralization vs. Decentralization and the level of Global Integration vs. Geopolitical Fragmentation.

| Scenario Name | Core Dynamic & Driving Force | Role of Retail CBDCs | Global Infrastructure | Privacy & Civil Liberties |

|---|---|---|---|---|

| 1. United in Prudence (The Unified Ledger) | High Centralization, High Integration. Regulators globally manage a harmonious, slow transition to digital finance. 41 | Tiered, capped retail CBDCs coexist smoothly alongside commercial bank money and regulated stablecoins. 53741 | The BIS "Unified Ledger" succeeds, linking wCBDCs and tokenized assets seamlessly across international borders. 2228 | High privacy via ZKPs. AML/CFT compliance is baked into smart contracts without resulting in gross surveillance. 285659 |

| 2. Highest Freedom (The Tech Takeover) | High Decentralization, Low Regulation. Trust in sovereign governments collapses globally. 40 | Retail CBDCs fail to gain traction against vastly superior, yield-bearing private stablecoins and decentralized finance (DeFi). 40 | Fragmented private blockchains (managed by dominant tech conglomerates) run global liquidity, undermining national monetary sovereignty. 40 | Paradoxical: High state privacy, but a total surrender of financial data to unaccountable "digital oligarchs" (Big Tech). 40 |

| 3. Village Economies (The Splinternet) | High Centralization, High Fragmentation. The world divides into hostile geopolitical blocs, weaponizing trade. 4166 | Highly politicized. Citizens are forced to use localized CBDCs to access basic government services and rations. 64 | SWIFT competes aggressively against Eastern multi-CBDC bridges (like China's Project mBridge) as the US dollar loses dominance. 366 | Extremely low. Money is used overtly as a tool for cross-border sanctions, domestic capital controls, and trade wars. 4164 |

| 4. BINO (Blockchain In Name Only) / Authoritarian | Ultimate Centralization. A highly controlled, tokenized economy managed by artificial intelligence. 4264 | Cash is effectively banned. Retail CBDCs are the mandatory, exclusive lifeblood of daily existence. 4264 | Governments co-opt blockchain tech solely for its surveillance, automation, and efficiency capabilities, ignoring decentralization. 42 | The "Police Officer is an API Call." Programmable money refuses non-compliant transactions instantly based on social scoring. 64 |

FAQ: How Will CBDCs Change Your Daily Life?

Assuming the global economy progresses toward a balanced scenario (such as United in Prudence), the integration of CBDCs will fundamentally alter daily consumer and corporate interactions. The underlying mechanism driving this monumental shift is "programmability" via smart contracts.

Revolutionizing Government Aid and Subsidies: During periods of economic crisis or natural disaster, traditional government aid distribution is severely hindered by administrative bottlenecks, rampant fraud, and the unbanked status of vulnerable populations. A programmable retail CBDC elegantly solves this structural inefficiency. Governments can essentially airdrop funds directly into citizen wallets instantly 2767. Furthermore, these funds can be programmed with sophisticated conditional logic. For example, disaster relief funds could be cryptographically restricted to purchase only food, water, and building supplies, automatically declining at liquor stores or casinos 427. They could also carry an "expiry date" to force immediate spending, thereby stimulating the local economy effectively 29. India has already demonstrated this exact model at a pilot scale for targeted agricultural loans and welfare subsidies via the e-Rupee 2729.

Frictionless E-Commerce and the Rise of Micro-payments: For the average consumer, checking out at a grocery store or an online retailer will appear visually similar to tapping a phone today. However, the backend settlement will clear in milliseconds rather than days. Because the merchant no longer has to pay a 2% to 3.5% interchange fee to a credit card network, the aggregate cost of goods could theoretically decrease, or merchants could offer steep discounts to incentivize CBDC usage 1310. Furthermore, true "micro-payments" finally become economically viable. Without flat-rate processing fees acting as a floor, a consumer could seamlessly pay $0.05 to read a single news article or stream a few seconds of a video, opening entirely new subscription and digital consumption business models 27.

The Automation of Tax Collection: Programmable money allows for real-time, automated compliance. When a transaction occurs, a smart contract could instantly calculate the exact sales tax or Value Added Tax (VAT) and split the payment - routing the merchant's revenue to their wallet and the tax revenue directly to the government treasury in a single atomic action 1027. This eliminates massive administrative overhead, reduces the burden of corporate compliance, and essentially eradicates certain forms of tax evasion.

The IMF's Blueprint: Strategic Frameworks for Adoption

Recognizing that superior technology does not automatically guarantee user adoption (as starkly illustrated by Nigeria's eNaira struggles), international bodies like the International Monetary Fund have actively intervened to guide central banks. Throughout 2024 and 2025, the IMF released extensive, continuously updated chapters to its CBDC Virtual Handbook, a highly technical resource designed for policymakers in emerging markets and developing economies (EMDEs) 174368.

The IMF introduced the REDI framework (Regulation, Education, Design, and Incentives) to systematically combat adoption apathy 69. The framework stresses that a CBDC cannot merely replicate existing, functional systems; it must solve distinct, localized pain points. For instance, the IMF highlights that in Fragile and Conflict-Affected States (FCS), a CBDC's primary design feature must be payment ecosystem resilience - specifically the ability for the digital currency to function entirely offline during critical infrastructure failures, conflict, or natural disasters 1743.

Furthermore, to combat the looming threat of the "Village Economies" scenario (where the global economy splinters into hostile regional payment blocs), the IMF and the BIS strongly advocate for the "Unified Ledger" approach. This model, championed by BIS innovation projects, proposes a shared programmable platform operated directly by central banks to host both tokenized reserves and commercial assets 222844. By maintaining international standardization and preserving the singleness of money, these institutions hope to prevent the technological splintering of the global financial system while capturing the immense efficiency gains of blockchain architecture 4546.

Bottom Line

The conceptualization and implementation of Central Bank Digital Currencies is not a fleeting, speculative technological trend; it represents the most significant structural overhaul of the global monetary system since the abandonment of the Bretton Woods gold standard.

By 2035, the era of anonymous, purely physical cash dominance will have unequivocally closed. The evidence clearly indicates a bifurcated future. The East, led by China and India, will have demonstrated the immense economic efficiency and domestic control enabled by heavily adopted, programmable retail CBDCs, utilizing them to guide fiscal policy with surgical precision and challenge Western financial hegemony. The West, having observed the systemic risks of deposit flight and grappling with the political toxicity of state surveillance, will lean heavily into wholesale CBDCs to secure the backend of global trade, while deploying heavily anonymized, highly restricted retail digital euros and dollars.

For the everyday consumer purchasing a coffee, this profound transition will be largely invisible, masked behind sleek, familiar user interfaces. Yet, the foundational reality of the economy will have fundamentally shifted: money will no longer be a passive, physical store of value. It will be an active, programmable, and executable software protocol. Ultimately, the success and societal impact of CBDCs will not be judged by the cryptographic sophistication of their ledgers, but by the robustness of the democratic, legal frameworks designed to protect the privacy, liberty, and financial autonomy of the citizens who use them.