5 Scenarios for the Future of Money

The future of money is diverging into five primary scenarios: the rollout of sovereign retail central bank digital currencies (CBDCs), the construction of a "unified ledger" for wholesale interbank settlement, the mainstream adoption of privately issued fiat-backed stablecoins, a geopolitical fragmentation of cross-border payment networks designed to bypass the US dollar, and a hybrid model where physical cash endures alongside digital alternatives. Over the next decade, these parallel developments will fundamentally restructure global finance, forcing society to navigate intense trade-offs between transaction efficiency, state surveillance, and monetary sovereignty.

The Structural Shift in How the World Pays

The global payment system is undergoing its most profound transformation in generations. Driven by shifting consumer demands, mobile penetration, and rapid technological advancements, digital payments have surged, resulting in a marked decline in the transactional use of physical cash across most advanced and emerging economies 12. To understand the future of digital currency, it is necessary to examine the baseline of how money moves today.

According to the 2023 Global Payments Report by FIS, physical cash now accounts for approximately 16 percent of global point-of-sale transactions 3. However, this global average obscures massive regional divergence. In North America, cash is used for just 12 percent of point-of-sale transactions, and in the Asia Pacific region, the figure sits at 15 percent 3. Conversely, cash remains deeply entrenched in Latin America at 31 percent, and in Africa and the Middle East, it remains the dominant payment method at 43 percent of all point-of-sale volume 3.

Despite the aggressive digitization of finance, physical cash is not on the verge of extinction. While its share of total global transaction value continues to fall by roughly 4 percent annually, overall cash usage has stabilized at approximately 80 percent of its 2019 levels . The demand for ATM cash withdrawals has generally plateaued rather than plummeted, highlighting the lasting role of physical currency as both a store of value and a fallback mechanism 14. For the estimated 1.4 billion unbanked adults worldwide, physical currency remains an irreplaceable lifeline for economic inclusion 65. Furthermore, in an era of increasing cybersecurity threats, digital outages, and geopolitical instability, physical money continues to provide systemic resilience and absolute independence from centralized digital infrastructure 8.

Nevertheless, the momentum is undeniably digital. Central banks recognize that they can no longer rely solely on physical cash to maintain their mandate as the anchor of the monetary system. If central banks fail to modernize sovereign money, they risk ceding the future of finance to private technology firms and decentralized cryptocurrency networks 67. This existential realization has sparked a global arms race to redefine the architecture of money.

What Are the 5 Future Scenarios for Digital Money?

Based on macroeconomic frameworks, pilot program data, and strategic roadmaps published by institutions such as the Bank for International Settlements (BIS), the International Monetary Fund (IMF), and the Official Monetary and Financial Institutions Forum (OMFIF), the evolution of digital currency is currently fracturing into five distinct, though occasionally overlapping, scenarios 28.

Scenario 1: The Sovereign CBDC Takeover

The first major scenario involves the widespread issuance and adoption of Central Bank Digital Currencies (CBDCs). A CBDC is a digital form of a country's official fiat currency that represents a direct liability of the central bank, rather than a liability of a commercial retail bank 91310. As of late 2025, more than 130 countries - representing 98 percent of the global gross domestic product - are actively researching, piloting, or deploying CBDCs 111612.

This scenario operates on two distinct tracks: retail and wholesale. Retail CBDCs are designed for the general public, serving as a digital equivalent to banknotes for everyday transactions like buying groceries or paying rent 1618. If retail CBDCs achieve mass adoption, citizens would hold digital money directly with the central bank or through highly regulated digital wallets 1819. While this provides the safest possible form of digital money - virtually eliminating the risk of a commercial bank run for the end user - it poses a severe structural threat to traditional banking 913. If consumers move their deposits out of commercial banks and into central bank digital wallets, commercial banks would lose their primary source of cheap funding, potentially restricting their ability to issue credit and thereby slowing economic growth 131415.

To mitigate this risk of bank disintermediation, many advanced economies are shifting their focus toward wholesale CBDCs. Wholesale CBDCs are restricted to financial institutions and are designed to streamline interbank settlement and liquidity management 1116. By putting central bank reserves on a programmable digital ledger, wholesale CBDCs promise to replace legacy Real-Time Gross Settlement (RTGS) systems with faster, more transparent, and highly efficient mechanisms 1316.

Scenario 2: The Tokenized "Unified Ledger"

The most ambitious architectural vision for the future of the traditional financial system is the creation of a "unified ledger," a concept heavily championed by the Bank for International Settlements in its 2025 Annual Economic Report 81617. Rather than treating central bank money, commercial bank deposits, and government bonds as entirely separate digital silos that require slow, expensive clearinghouses to interact, this scenario envisions migrating all of these assets onto a single, programmable platform 817.

This "trilogy" of tokenized central bank reserves, tokenized commercial bank money, and tokenized government bonds would reside on the same interconnected network 817. Tokenization - the digital representation of assets on programmable platforms - integrates messaging, reconciliation, and settlement into a single seamless operation 8. Because the assets live on the same network, transactions can execute with atomic settlement, meaning the transfer of an asset and the payment for that asset occur simultaneously and instantly 817.

Crucially, the unified ledger scenario preserves the existing two-tier banking system. It maintains the "singleness" of money (ensuring one digital euro is always worth exactly one physical euro) and the "elasticity" of money (allowing commercial banks to expand their balance sheets to provide credit to the real economy), while radically upgrading the technological plumbing of global finance 817.

Scenario 3: The Abundant Private Stablecoin Ecosystem

Rather than waiting for state-issued CBDCs, the third scenario sees privately issued stablecoins becoming the default mechanism for global digital commerce 162526. Stablecoins are digital tokens pegged on a one-to-one basis to fiat currencies, most commonly the US dollar or the Euro, and are backed by reserves of cash or high-quality liquid assets like short-term government treasury bills 91625.

Stablecoins have already achieved immense product-market fit, processing trillions of dollars in transaction value annually 1327. In 2024, the transaction value of stablecoins hit $15.6 trillion globally, roughly equivalent to the combined volumes of major credit card networks, with over 110 million monthly transactions 27. In this future scenario, stablecoins act as the primary liquidity layer for the internet, decentralized finance (DeFi), and cross-border remittances 1326.

The viability of this scenario is heavily dependent on regulatory clarity. With the full enforcement of the Markets in Crypto-Assets (MiCA) regulation in the European Union across 2024 and 2025, MiCA-compliant stablecoins have surged 282930. By mandating that issuers hold fully backed, liquid reserves and granting legally enforceable redemption rights at par, MiCA has brought institutional trust to private digital money, fueling a 25 percent growth in the EU's crypto payment market in 2025 alone 283031. In the United States, proposed legislative frameworks aim to harness privately issued, dollar-backed stablecoins to cement the global dominance of the US dollar through private-sector technological innovation 1618.

Scenario 4: The Geopolitical Currency War and De-Dollarization

Money is a tool of geopolitical power. Currently, over 90 percent of international transactions involve the US dollar, and the global financial system is heavily reliant on Western-controlled infrastructure like the SWIFT messaging network 1219. Following the weaponization of the dollar via international sanctions - most notably the freezing of Russian foreign exchange reserves and the exclusion of certain nations from SWIFT - rival economic blocs are actively building alternative digital pathways 121920.

The most prominent example of this scenario is mBridge, a multi-CBDC platform initially spearheaded by the BIS alongside the central banks of China, Thailand, Hong Kong, the UAE, and eventually Saudi Arabia 202122. By utilizing distributed ledger technology, mBridge allows central banks to settle cross-border trades directly using their own digital currencies, completely bypassing traditional correspondent banking intermediaries and the US dollar 2123.

By mid-2025, mBridge had processed tens of billions of dollars in real-value transactions, with the vast majority utilizing China's digital yuan 2425. Following the October 2024 BRICS summit, the BIS formally withdrew from the mBridge project, citing that it had "graduated" from its innovation hub, though geopolitical pressure regarding sanctions evasion was widely noted by analysts 2425. If scaled across the expanded BRICS+ nations, this scenario could lead to a highly fragmented global monetary system, eroding the dollar's "exorbitant privilege" and fundamentally altering global macroeconomic power dynamics 121920.

Scenario 5: Hybrid Cash-Digital Coexistence

The most likely scenario for the near-to-medium term is a messy, pragmatic coexistence. In this reality, no single form of money achieves total dominance. Instead, a "tapestry of currencies" covers the globe 2.

Physical cash persists due to public demand for absolute privacy, systemic resilience, and financial inclusion 2626. Commercial bank money continues to handle the bulk of domestic credit creation and retail spending 27. Private stablecoins dominate niche but massive markets like Web3 commerce and high-speed cross-border remittances 132628. Meanwhile, wholesale CBDCs quietly upgrade the back-end interbank settlement infrastructure without disrupting the consumer-facing banking experience 131629. In this scenario, policymakers and businesses adapt to arm's-length public-private partnerships, allowing users to seamlessly shift between public and private payment rails based on their specific needs for speed, cost, or anonymity 2.

Comparing the Core Digital Assets

To accurately evaluate these five scenarios, it is critical to distinguish between the three main categories of digital money. While they may all leverage cryptographic ledgers or blockchain technology, their economic foundations, governance structures, and regulatory risk profiles are entirely different.

| Feature | Central Bank Digital Currency (CBDC) | Fiat-Backed Stablecoin | Decentralized Cryptocurrency |

|---|---|---|---|

| Issuer | The national central bank or monetary authority. | Private corporate entities or decentralized protocols. | Decentralized network consensus (no central issuer). |

| Liability & Backing | Direct sovereign liability of the government/central bank. | Backed by reserves (fiat currency, treasury bills) held by the private issuer. | No intrinsic asset backing; value is driven entirely by market supply and demand. |

| Primary Goal | Digitize national fiat, maintain monetary sovereignty, and upgrade domestic settlement rails. | Provide borderless, stable liquidity for trading, decentralized finance, and rapid cross-border payments. | Serve as a decentralized, censorship-resistant store of value or speculative asset. |

| Governance Model | Highly centralized by the state. | Managed by corporate boards or Decentralized Autonomous Organizations (DAOs). | Governed by open-source code, miners, and node operators. |

| Key Examples | e-CNY (China), Digital Euro (EU), Sand Dollar (Bahamas). | USDC (Circle), USDT (Tether), EURS. | Bitcoin (BTC), Ethereum (ETH). |

Table 1: The distinct structural differences defining modern digital assets, synthesized from institutional and market data 913162526283031.

Institutions like the BIS argue that privately issued stablecoins fail to meet the rigorous tests of "sound money" - specifically elasticity - because their issuers cannot expand their balance sheets at will during financial crises, operating instead on a strict cash-in-advance model 1731. However, proponents of stablecoins counter that these digital assets are designed to be high-speed settlement instruments, not macroeconomic stabilization tools, and that rigorous regulatory frameworks like MiCA adequately solve the "singleness" problem by enforcing parity with fiat currencies 31.

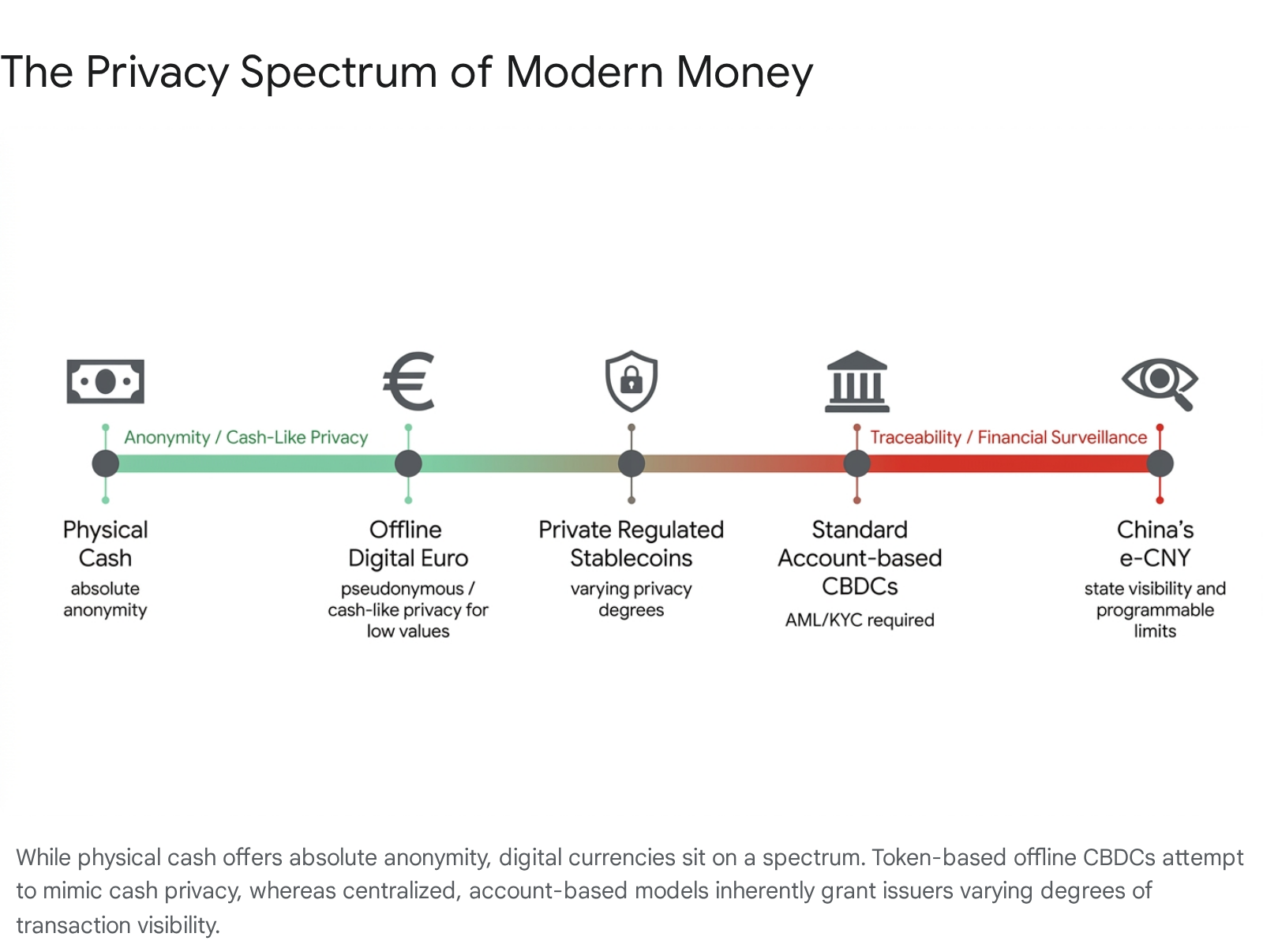

The Privacy vs. Financial Surveillance Dilemma

If there is a single issue that will determine the success or failure of state-backed retail digital currencies in democratic societies, it is the fundamental question of financial privacy 14. When a consumer uses a physical banknote, the transaction is strictly peer-to-peer; it leaves no digital footprint, requires no identity verification, and cannot be frozen, tracked, or censored by a third party 144647.

Most CBDC proposals struggle to replicate this level of anonymity. Because digital transactions must be verified to prevent double-spending, and because governments are bound by stringent Anti-Money Laundering (AML) and Combatting the Financing of Terrorism (CFT) regulations, traditional account-based CBDCs require users to link their verified identities to their digital wallets 144732.

Privacy advocates warn that this architecture could establish an omnipresent financial surveillance state. Critics argue that a centralized ledger gives government agencies "absolute visibility" into every citizen's financial activity by default, effectively bypassing the legal air-gaps and warrant requirements that currently exist between commercial banks and state authorities 4647. In authoritarian contexts, this total visibility can be coupled with social credit systems to arbitrarily freeze funds or restrict dissidents' access to the broader economy 4647.

However, central banks are acutely aware that public adoption hinges entirely on trust. A comprehensive 2024 survey conducted by the BIS, involving over 3,500 participants, empirically demonstrated that robust privacy features increased the public's willingness to use a CBDC by up to 60 percent, particularly for privacy-sensitive transactions 4950.

To solve this dilemma, technological architectures are splitting. Token-based CBDCs behave more like digital cash, relying on cryptography rather than verified accounts, and can potentially be transferred offline without immediate central ledger settlement 1914. Conversely, account-based models rely on identity verification and are inherently geared toward compliance and monitoring 1932.

What Is the Difference Between Programmable Payments and Programmable Money?

One of the most touted - and simultaneously most feared - capabilities of new digital currencies is "programmability." However, technologists and central bankers draw a strict distinction between programmable payments and programmable money 335234.

Programmable Payments

Programmable payments refer to the automated transfer of funds when predefined external conditions are met 335234. This is an advanced evolution of traditional direct debits, powered by smart contracts operating outside the core currency layer. For example, in an industrial setting, a machine on a factory floor could autonomously detect a low parts inventory, negotiate an order, and trigger a payment only when a delivery scanner confirms receipt of the goods 523435. This machine-to-machine automation streamlines supply chains, eliminates settlement friction, and creates massive efficiencies in the emerging "economy of things" 5234.

Programmable Money

Programmable money, on the other hand, involves embedding behavioral restrictions directly into the digital currency itself 335234. This controversial feature allows the issuer to dictate how, when, or where the money can be spent. * Expiration Dates: During an economic downturn, a government could issue fiscal stimulus funds via a CBDC that are explicitly programmed to expire or depreciate after 30 days, forcing citizens to consume immediately rather than saving the funds 153335. * Restricted Goods: Welfare, subsidies, or disaster relief payments could be programmed to only execute at verified grocery stores or educational institutions, technically preventing the digital funds from being spent on alcohol, gambling, or non-essential goods 153335.

While programmable money offers unparalleled precision for macroeconomic policy and fraud reduction, it deeply alarms civil liberties groups 1535. Imposing logic onto the currency itself threatens the fundamental economic concept of "fungibility" - the principle that one dollar is equal to any other dollar, regardless of who holds it or how they intend to use it 35. If a digital dollar can only be spent at certain approved vendors, it ceases to be general-purpose money.

Regional Frontlines in the Digital Currency Race

The transition to digital money is not occurring uniformly. Different global regions are prioritizing different technologies based on their unique economic vulnerabilities, political systems, and strategic ambitions.

China's First-Mover Advantage with the e-CNY

China's digital yuan (e-CNY) is arguably the most advanced major CBDC globally. Having initiated pilot programs in 2019, the e-CNY achieved massive scale by 2025, reaching over 261 million personal digital wallets and recording more than $985 billion in cumulative transaction value 363738.

The People's Bank of China utilizes a two-tier model, issuing the digital currency to commercial banks which then distribute it to consumers 3839. A critical feature of the e-CNY is its integration into smart city infrastructure and its utilization of Near-Field Communication (NFC) technology to allow offline transactions, ensuring usability in remote areas with poor internet connectivity 3638. By design, the e-CNY lacks the privacy constraints expected in Western democracies; it grants the state deep visibility into transaction flows, aiding in macroeconomic tracking and anti-corruption efforts 194737. Internationally, the e-CNY forms the backbone of China's participation in the mBridge project, reflecting a strategic imperative to internationalize the yuan and build settlement rails insulated from Western influence 12233640.

The European Union and the Digital Euro

Europe is moving deliberately on two interconnected fronts: developing a sovereign digital currency while aggressively regulating private alternatives. The European Central Bank (ECB) is currently in a multi-year preparation phase for the Digital Euro 193740. To address intense public anxiety over surveillance, the ECB's design heavily emphasizes "privacy by design," proposing "cash-like privacy" for low-value, offline transactions via secure smart cards or mobile devices, where peer-to-peer transfers settle without the central bank seeing individual user data 19333860. To protect the commercial banking sector, the Digital Euro will likely feature strict holding limits per wallet to prevent a mass exodus of retail deposits 1947.

Simultaneously, the EU has established itself as the preeminent global leader in comprehensive crypto regulation. The Markets in Crypto-Assets (MiCA) framework, which became fully applicable across 2024 and 2025, has strictly standardized the issuance of stablecoins 282961. By requiring crypto-asset service providers (CASPs) to secure licenses, hold 1:1 liquid reserves, and guarantee redemption rights, MiCA transformed the EU crypto landscape from a speculative fringe to a regulated enterprise environment 2830. This regulatory certainty resulted in a 60 percent surge in EU crypto payment adoption and drew traditional financial institutions into the stablecoin ecosystem 306263.

The United States and the Fight Over the Digital Dollar

The United States remains a glaring outlier in the sovereign CBDC race. Amid fierce domestic political pushback over privacy concerns, the Federal Reserve has largely stalled on developing a direct-to-consumer digital dollar 12473738. Legislation such as the CBDC Anti-Surveillance State Act and executive actions aiming to halt retail CBDC development reflect a deep-seated cultural resistance to centralized government financial tracking 124738.

Instead, US policy is increasingly leaning on the innovation of the private sector. Through proposed frameworks like the GENIUS Act, US policymakers are recognizing that highly regulated, privately issued dollar-pegged stablecoins (such as USDC and USDT) essentially export US monetary policy and enforce dollar dominance globally 161838. By treating stablecoins as a proxy for the digital dollar, the US aims to maintain global financial hegemony without requiring the government to build, secure, or manage complex consumer-facing retail infrastructure 38.

Emerging Markets and the Stablecoin Boom

While advanced economies debate regulatory policy, the Global South is actively adopting digital currencies out of urgent economic necessity. In regions like Latin America and Sub-Saharan Africa, citizens and businesses are flocking to private stablecoins as an escape hatch from hyperinflation, capital controls, and rapidly devaluing local currencies 274165.

In 2024, Africa recorded stablecoin flows equivalent to 6.7 percent of its total GDP, with the vast majority of transactions being cross-border 42. In Sub-Saharan Africa, stablecoins accounted for an astonishing 43 percent of all crypto transaction volume, with Nigeria alone recording nearly $22 billion in transactions 27. Similarly, in Latin America, stablecoins account for over 60 percent of transaction volume in inflation-hit countries like Argentina 41. For these populations, digital dollars offer immediate cross-border settlement and critical wealth preservation. They bypass traditional correspondent banking networks that often charge exorbitant wire transfer fees, transforming stablecoins from a speculative asset into essential, daily banking infrastructure 5274243.

| Region | Primary Focus | Regulatory / Implementation Status (2025) | Key Driver |

|---|---|---|---|

| China | Retail CBDC (e-CNY) & Cross-border wholesale. | Live at massive scale (261M+ users); driving international mBridge integration. | State control, domestic efficiency, bypassing US dollar dominance. |

| European Union | Digital Euro & Regulated Stablecoins. | Digital Euro in prep phase (launch expected ~2027/2028); MiCA fully active for stablecoins. | Monetary sovereignty, privacy-by-design, consumer protection. |

| United States | Private Stablecoins (Dollar-pegged). | Retail CBDC politically stalled; GENIUS Act guiding stablecoin regulation. | Free-market innovation, maintaining global dollar hegemony. |

| Global South | Private Stablecoins & targeted CBDCs (e-Naira, e-Rupee). | Massive grassroots stablecoin adoption; active CBDC pilots in India and Brazil. | Hedging against local inflation, cutting cross-border remittance fees. |

Table 2: Comparison of regional digital currency strategies and implementation statuses 19273018363738404142.

What Will This Mean for the Everyday Consumer?

Regardless of whether a CBDC, a unified ledger, or a private stablecoin wins out, the transition to programmable digital money will carry profound implications for the end user.

The most immediate benefit will be the radical reduction of transaction fees, particularly for cross-border payments. Currently, the global average cost of sending remittances remains painfully high at around 6.49 percent, acting as a regressive tax on migrant workers sending money home 511. The IMF's scenario analyses project that the implementation of CBDCs or deeply integrated stablecoin networks could reduce cross-border transaction costs by approximately 60 percent 44. The G20 roadmap explicitly targets lowering global average retail payment costs to no more than 1 percent by 2027, and remittance costs to no more than 3 percent by 2030 44.

Furthermore, transaction speed will transition from days to seconds. Digital money bypasses the fragmented correspondent banking networks, allowing for near real-time settlement 4445. For merchants, this means instant liquidity without waiting for credit card processors to clear funds, and for consumers, it means an end to the multi-day delays associated with international wires 545.

Finally, the shift toward digital currencies holds the promise of unprecedented financial inclusion. By decoupling financial access from traditional brick-and-mortar commercial banking, digital wallets allow unbanked populations to access secure savings, peer-to-peer transfers, and micro-credit solely via a basic smartphone connection 102246.

Bottom line

The future of money is definitively digital, but its structural architecture remains fiercely contested among central banks, private technology firms, and competing geopolitical blocs. While sovereign entities push for CBDCs and unified ledgers to maintain monetary control and upgrade aging infrastructure, the private sector is rapidly capturing global market share through stablecoins that solve immediate pain points like high cross-border fees and local currency inflation. For the everyday user, this evolution promises frictionless, instant global payments, but it will simultaneously force society to confront urgent, foundational trade-offs regarding how much financial privacy we are willing to surrender to the state in exchange for digital convenience.