5 Scenarios for the Future of Crypto and DeFi

Over the next decade, cryptocurrency and decentralized finance will transition from speculative alternatives into foundational layers of global commerce, driven by the mass adoption of stablecoins, real-world asset tokenization, and institutional integration. Depending on regulatory actions and market forces, this evolution will likely fracture into distinct paths: seamless assimilation by traditional banks, a parallel financial system empowering the Global South, a central-bank-controlled unified ledger, a fragmented hybrid model, or - if risks are mismanaged - systemic contagion. The ultimate reality will likely be a hybrid model where regulated digital assets settle on centralized ledgers while permissionless networks serve niche or underserved global populations.

The Paradigm Shift of 2024 - 2026: From Rebellion to Regulation

For years, the narrative surrounding cryptocurrency was defined by profound volatility, speculative retail trading, and a lack of regulatory clarity. The industry's reputation was severely damaged during the "crypto winter" of 2022, catalyzed by the collapse of the algorithmic stablecoin TerraUSD and the subsequent bankruptcies of major intermediaries like Celsius, Three Arrows Capital, and FTX 123. These failures exposed the systemic vulnerabilities of unregulated offshore entities and opaque rehypothecation practices.

However, the period between 2024 and 2026 marked a structural turning point in the digital asset economy. Rather than collapsing under regulatory scrutiny, the sector matured. The global crypto market capitalization breached the $4 trillion threshold in 2025, driven not merely by retail enthusiasm but by the aggressive integration of institutional infrastructure 25. The approval and subsequent success of spot Bitcoin and Ethereum exchange-traded products (ETPs) in the United States acted as a primary catalyst. By the end of 2025, these global exchange-traded products had attracted $87 billion in net inflows, with institutional investors and advisory channels emerging as the fastest-growing allocators 6.

This influx of traditional capital signaled a shift from tech-rebellion to serious financial infrastructure. Bitcoin began to be viewed by some institutional players as a "digital gold" safe-haven asset, while the broader blockchain ecosystem was increasingly evaluated for its underlying utility 7. Furthermore, the macroeconomic environment - characterized by shifting monetary policies, fiscal stimulus, and trade uncertainties - prompted traditional financial institutions to seek alternative avenues for yield and operational efficiency 5.

More importantly, this period saw the implementation of landmark regulatory frameworks that transformed the legal status of digital assets from a gray area into recognized financial instruments, providing the necessary legal certainty for widespread institutional adoption.

The Regulatory Twin Pillars: MiCA and the GENIUS Act

The global regulatory landscape is currently anchored by two divergent but highly influential frameworks: the European Union's Markets in Crypto-Assets (MiCA) regulation and the United States' Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act. The development of these frameworks highlights a transition from disjointed enforcement actions - such as the U.S. Securities and Exchange Commission's peak of 46 crypto-related enforcement actions in 2023 - to comprehensive legislative rulemaking 39104.

The European Union's MiCA Framework

The EU's MiCA regulation, which became fully applicable in December 2024, established the world's first comprehensive, harmonized rulebook for digital assets across all 27 member states 12567. Prior to MiCA, crypto firms operating in Europe faced a fragmented landscape, requiring multiple licenses with varying standards across different jurisdictions 12.

MiCA categorizes digital assets into distinct buckets, with strict rules for e-money tokens (EMTs, backed by a single fiat currency) and asset-referenced tokens (ARTs, backed by a basket of assets) 127. By eliminating jurisdictional fragmentation, MiCA created a passporting regime that allows Crypto-Asset Service Providers (CASPs) to operate seamlessly across Europe under a unified standard of market integrity, consumer protection, and reserve requirements 126. Currently, 102 CASPs are registered under the full framework, with traditional credit institutions representing a growing share of these authorized entities 8. Despite this clarity, some market dynamics remain challenging; U.S.-issued, dollar-backed stablecoins currently constitute 90% of market capitalization and over 70% of trading volume in Europe, prompting debates over economic sovereignty and the treatment of multi-issuance schemes under MiCA 89.

The U.S. GENIUS Act

The U.S. approach crystallized around the passage of the GENIUS Act in July 2025. This legislation provided the first comprehensive federal framework specifically targeting payment stablecoins, aiming to foster innovation while mitigating risks to the broader financial system 181011.

The act mandates that stablecoins must be backed on a 1:1 basis by highly liquid assets - such as cash or short-term U.S. Treasuries - and requires issuers to undergo regular audits and publish monthly reserve disclosures 1810. Critically, the GENIUS Act strictly prohibits stablecoin issuers from paying interest or yield directly to token holders 12. This provision is largely viewed as a protective measure to prevent stablecoins from directly competing with traditional interest-bearing bank deposits, thereby shielding the legacy banking system from rapid disintermediation 111223. Furthermore, the legislation clarifies that stablecoins are neither securities nor commodities, effectively removing them from the primary jurisdictions of the SEC and CFTC, and placing them under bespoke federal and state oversight .

| Feature | EU MiCA Regulation | US GENIUS Act |

|---|---|---|

| Effective Date | December 2024 (fully applicable) | July 2025 (implementation ongoing) |

| Primary Focus | Comprehensive coverage (CASPs, EMTs, ARTs) | Specifically targets USD-backed payment stablecoins |

| Reserve Requirements | Segregated, liquid reserves redeemable at par | 1:1 backing by cash or short-term US Treasuries |

| Yield / Interest | Strict limits to prevent deposit-like behavior | Explicitly prohibits issuers from paying yield to holders |

| Jurisdictional Impact | EU-wide passporting for registered providers | Federal certification overriding state-by-state patchwork |

| Market Dominance | Attempts to limit non-EU currency dominance | Reinforces the global hegemony of the US Dollar |

The Technological Engines: Stablecoins and Tokenization

Before forecasting the specific scenarios that will dictate the future of decentralized finance, it is essential to understand the two core technological engines powering this transition: stablecoins and the tokenization of real-world assets.

Stablecoins as the Internet's Settlement Layer

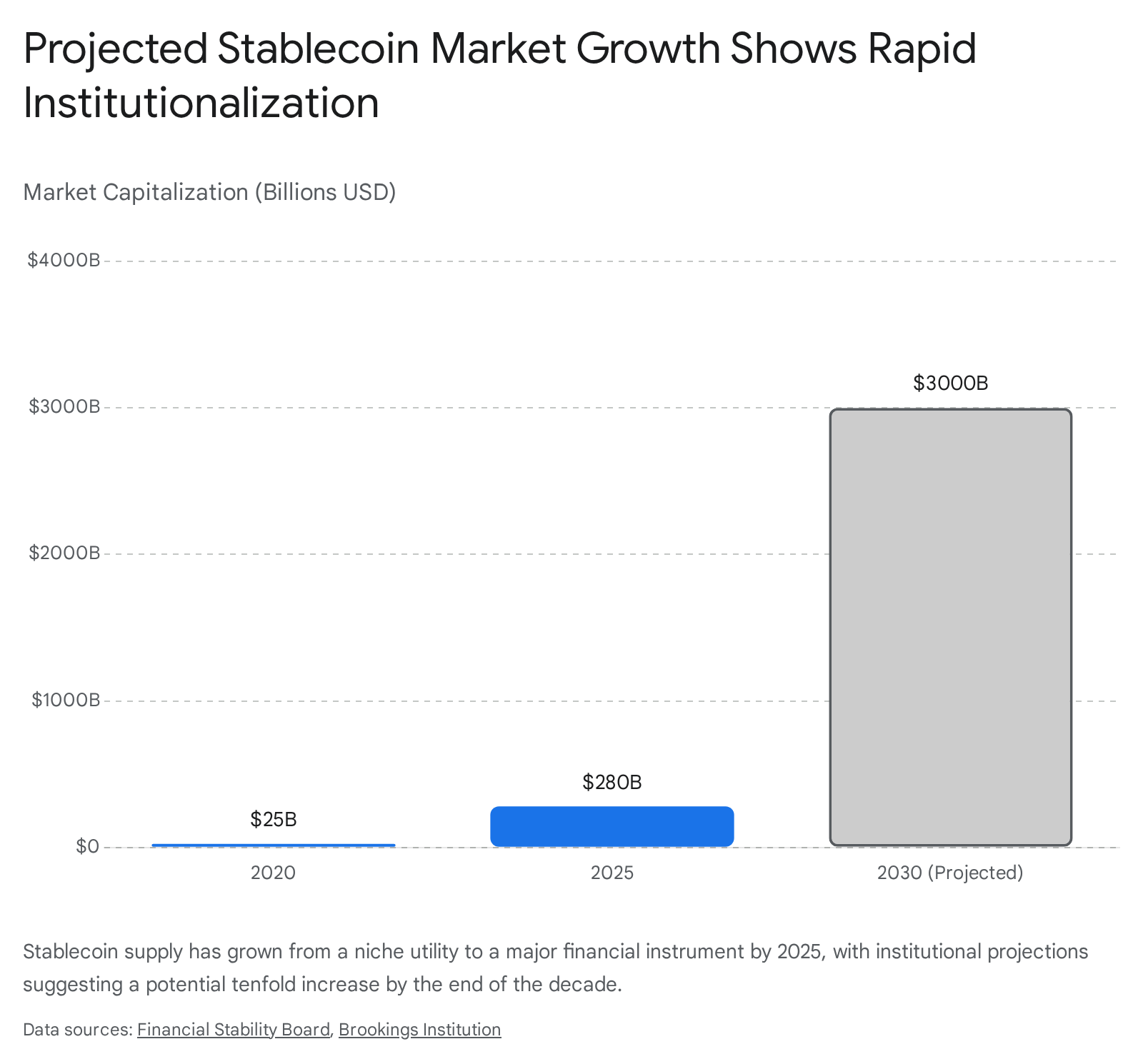

Stablecoins have evolved rapidly from mere fiat on-ramps for crypto speculators into a critical layer of global financial infrastructure. By late 2025, the outstanding supply of USD-pegged stablecoins reached nearly $280 billion, supporting an estimated $33 trillion in total settlement volume over the broader crypto ecosystem 111325.

While the vast majority of this historical volume has been tied to crypto asset trading and decentralized exchange routing, the utility of stablecoins is shifting rapidly toward real-world commercial applications. Corporate finance departments are increasingly utilizing digital dollars for cross-border supplier payments and global payroll. Traditional payment infrastructures suffer from hidden fees, foreign-exchange spreads, and significant delays due to batch cut-offs, bank holidays, and correspondent banking checks 26. Stablecoins solve this by allowing settlements to clear in minutes, operating continuously around the clock, and arriving without exorbitant foreign-exchange mark-ups 26.

Asset Tokenization and Project Guardian

Simultaneously, the traditional financial sector has embraced "tokenization" - the process of issuing digital representations of traditional financial and real-world assets on a distributed ledger. This allows financial claims to become executable objects that are transferable via programming instructions 14.

This movement has been heavily pioneered by public-private initiatives like Project Guardian, an international collaboration led by the Monetary Authority of Singapore (MAS) and featuring participants such as JPMorgan, Deutsche Bank, HSBC, and Apollo 28291531. Through Project Guardian, institutions have successfully tested the tokenization of foreign exchange trades, government bonds, money market funds, and private credit portfolios on both permissioned and public blockchains 28313216.

For example, JPMorgan has actively piloted its own dollar-pegged "deposit token" (JPMD) on secondary networks. Deposit tokens function differently than stablecoins; they are transferable tokens issued on a blockchain but backed directly by a licensed depository institution, offering an alternative backed by deposit insurance similar to traditional bank deposits 34. By utilizing smart contracts, tokenization standardizes subscription and redemption processes, automates portfolio rebalancing, and fractionalizes historically illiquid assets, dramatically lowering the investment threshold for participants 1532.

Based on these regulatory and technological foundations, the future of cryptocurrency and decentralized finance will likely diverge into one of five primary scenarios over the coming decade.

Scenario 1: Institutional Assimilation (The TradFi Takeover)

In this scenario, the revolutionary promises of decentralized finance are systematically co-opted by traditional finance (TradFi). Rather than disintermediating the legacy banks, blockchain technology is seamlessly integrated into the existing banking architecture to serve as an ultra-efficient backend settlement rail.

The Mechanism of Assimilation

Under the protections of frameworks like the GENIUS Act, massive commercial banks become the primary issuers of tokenized deposits and compliant stablecoins 1035. Because current U.S. legislation prohibits non-bank stablecoin issuers from offering yield directly to retail users, all the generated yield from the underlying reserve assets (such as U.S. Treasuries) is captured entirely by the issuers themselves 12.

To compete with tech-native stablecoin providers, traditional banks leverage their massive balance sheets and existing regulatory exemptions to offer tokenized money market funds and blockchain-based deposit accounts that can offer yield 35. The high costs of compliance, mandatory reserve audits, and strict anti-money laundering (AML) surveillance requirements create an insurmountable moat for grassroots DeFi startups, concentrating market power back into the hands of incumbent financial institutions 182617.

The Impact on Consumers

In this future, everyday retail customers gain access to crypto investments seamlessly through their existing banking applications, as seen with early adopters like Belgium's KBC Bank, which plans to allow retail customers to invest in digital assets directly through their standard bank portals 37. For the average consumer, the "blockchain" becomes entirely invisible. It operates merely as an upgraded database that allows for instant weekend wire transfers, real-time cross-border payments, and lower internal friction.

Consequently, the original DeFi ecosystem of permissionless, open-source lending protocols is marginalized into a highly speculative, illiquid niche. The bulk of global liquidity flows through permissioned, institutional blockchains operated by banking consortia, effectively neutralizing the disruptive, anti-establishment ethos upon which cryptocurrency was founded 28151839.

Scenario 2: The Global South Leapfrog

While institutional assimilation dominates the financial centers of the United States and Europe, the second scenario envisions a radically different future for emerging markets. In the "Global South," decentralized finance and permissionless stablecoins bypass traditional banking infrastructure entirely, much like mobile phones leapfrogged landlines in the early 2000s.

Bypassing Failing Infrastructure

In countries plagued by hyperinflation, currency volatility, strict capital controls, and restricted access to U.S. dollars, citizens are turning to peer-to-peer (P2P) crypto networks out of pure economic necessity. According to 2024 data, Sub-Saharan Africa leads the world in DeFi adoption, driven by a desperate need for accessible financial services in a region where only 49% of adults possessed a bank account as of 2021 19.

Similarly, in Latin America - specifically in nations experiencing severe economic instability like Argentina and Venezuela - stablecoin purchases make up more than 50% of exchange buying activity as residents seek safe-haven assets to protect their purchasing power 2541. These populations utilize DeFi platforms to earn interest, take out micro-loans, and hedge against rapidly devaluing local fiat currencies 19.

The Remittance Revolution

The most profound disruption in this scenario occurs within the remittance market. The World Bank estimates the global remittance market is worth roughly $685 billion 20. However, sending remittances globally costs an average of 6.36% to 6.65% of the total transaction amount via traditional channels, severely impacting the low-income families that rely on these funds 2021. In regions like Sub-Saharan Africa, these fees can average as high as 7.4% to 8.78% 2520.

Blockchain-based remittances drop this cost significantly - often below 1% - by eliminating correspondent banking intermediaries and providing near-instant settlement 252044. P2P platforms now handle a growing share of these flows; in Nigeria, for example, P2P platforms account for roughly 80% of crypto transactions amid local banking restrictions 25. In this scenario, informal and decentralized networks effectively create an alternative, sovereign financial infrastructure. Over time, these populations conduct their primary economic activities entirely on-chain, divorcing their local economies from the policy decisions of their domestic central banks 19452247.

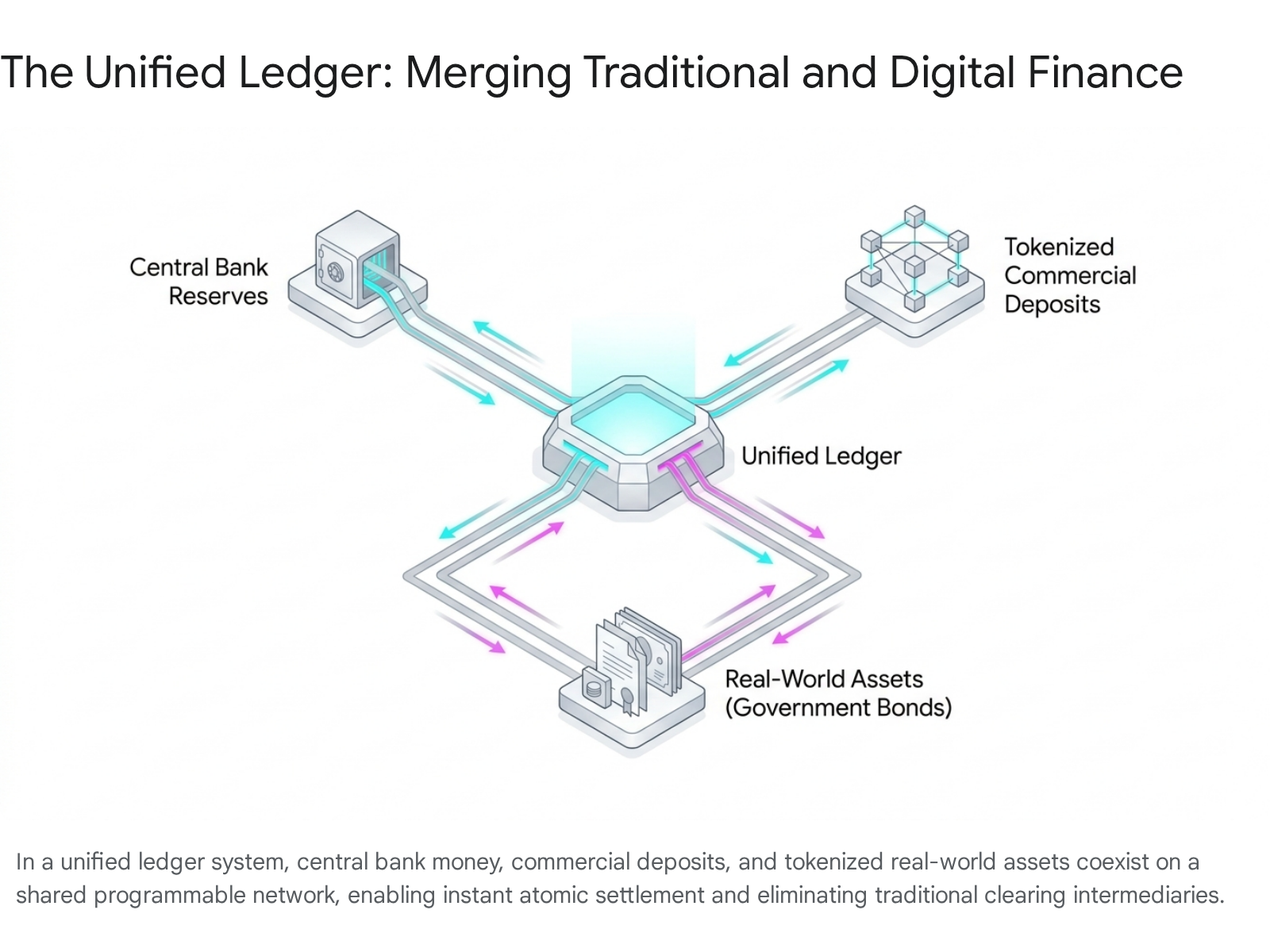

Scenario 3: The Unified Ledger (The Central Bank Vision)

In the third scenario, public authorities and central banks reclaim control of the digital money narrative from private stablecoin issuers by rolling out a next-generation monetary system based on a "unified ledger."

Reasserting Monetary Sovereignty

Central banks have expressed growing concern that the widespread adoption of private stablecoins and decentralized cryptocurrencies could threaten their monetary sovereignty and complicate the implementation of macroeconomic policy 2349. To counter this, institutions like the Bank for International Settlements (BIS) have proposed a blueprint for a unified ledger.

This architecture brings together three core elements onto the same programmable venue: wholesale central bank digital currencies (wCBDCs), tokenized commercial bank money, and tokenized claims on financial assets such as government bonds 14.

A 2024 BIS survey revealed that wCBDCs are already the most widely used settlement asset in tokenization pilots, outstripping both tokenized deposits and private stablecoins 35.

Atomic Settlement and Programmable Money

The primary advantage of the unified ledger is its ability to enable "atomic settlement." This refers to the synchronous exchange of assets where a transfer occurs only if the corresponding payment or asset transfer is simultaneously completed 14. This mechanism removes the need for separate messaging and reconciliation processes, drastically reduces counterparty credit risk, and ensures the "singleness of money" through final settlement in central bank reserves 14.

By combining programmability with composability, the unified ledger integrates and automates sequences of financial operations. It allows central banks to carry out monetary policy implementation directly on a programmable platform, using smart contracts to calculate and pay interest or manage liquidity facilities instantly 14. In this scenario, private stablecoins are ultimately marginalized, as major institutional players prioritize the absolute settlement finality and trust guaranteed by central bank-backed digital currencies over privately issued alternatives 1449.

Scenario 4: The Fragmented Parallel System

This scenario rejects the "all or nothing" misconception that crypto must either destroy traditional banking or be completely absorbed by it. Instead, the global economy develops a bifurcated, parallel structure where both centralized and decentralized systems coexist, each serving entirely different purposes 50515253.

The Dual-Track Economy

The traditional banking sector heavily adopts tokenization for institutional asset management, relying strictly on permissioned blockchains, digital identity verification, and compliant stablecoins governed by frameworks like the GENIUS Act and MiCA 7121028. These institutional rails provide the safety, recourse, and regulatory compliance required by major corporations, pension funds, and governments.

However, a robust, permissionless DeFi ecosystem continues to thrive in parallel. This decentralized system relies on algorithmic and crypto-over-collateralized stablecoins, decentralized autonomous organizations (DAOs), and automated market makers (AMMs) that operate entirely outside of corporate and state control 12455. Decentralized exchanges (DEXs) allow users to trade assets directly from their self-custodied wallets via smart contracts, avoiding the counterparty risks associated with centralized platforms 125.

Interoperability and Specialized Use Cases

Consumers and businesses treat their financial lives similarly to how they interact with the modern internet. They utilize regulated, institutional rails for conventional financial activities: receiving salaries, securing mortgages, and managing tax-compliant corporate treasuries 2639. Simultaneously, they leverage the parallel permissionless system for specialized activities that traditional finance cannot easily accommodate. This includes borderless peer-to-peer commerce, permissionless micro-lending, and interacting with emerging technologies - such as autonomous AI agents that require decentralized, machine-to-machine payment rails to function without human intervention 4724.

Advanced interoperability protocols and cross-chain bridges serve as the connective tissue between these two worlds, allowing capital to flow cautiously between the highly regulated fiat environment and the experimental Web3 ecosystem 55.

Scenario 5: Systemic Contagion and Regulatory Backlash

The final scenario represents the severe outcome frequently warned about by the Financial Stability Board (FSB) and global central banks. In this future, the rapid and unchecked integration of crypto assets into traditional financial infrastructure creates unrecognized vulnerabilities, culminating in a systemic collapse 2216.

Unrecognized Vulnerabilities and Leverage

While the current scale of tokenization does not pose a material risk to financial stability, aggressive scaling changes the calculus 1626. The composability of DeFi - where different protocols are stacked on top of one another - can introduce profound complexity and opacity 16.

A primary vulnerability is the unchecked build-up of leverage through rehypothecation, where tokenized assets or collateral are lent out multiple times across different protocols 1625. Furthermore, tokenization can create severe liquidity and maturity mismatches if tokens are perceived as instantly liquid, while the real-world reference assets they represent (like private credit or real estate) remain illiquid 16. This mismatch can easily trigger redemption runs 16.

The Contagion Catalyst

The crisis in this scenario is triggered by a "black swan" event, such as the prolonged depegging of a major, systemically important stablecoin like USDT (Tether). Because stablecoins have become the working cash layer of the entire crypto industry, a loss of confidence forces the issuer to rapidly liquidate its massive holdings of U.S. Treasury bills and commercial paper to meet redemption requests 132558. This fire sale disrupts short-term fiat funding markets 58.

Because of the newly established cross-asset correlations, the shock does not stay contained within the crypto ecosystem. The liquidation cascades into traditional equities and credit markets, triggering margin calls that reduce lending to Main Street businesses 2. The fallout leads to devastating losses in state pension funds and retail 401(k) accounts that had recently gained exposure to crypto assets 27. In the aftermath, global regulators enact draconian policies, heavily restricting asset tokenization, outright banning algorithmic stablecoins, and imposing punitive capital requirements on any traditional institution interacting with public blockchains, effectively setting the industry's progress back by a decade 258.

Tracking the Future: Key Indicators

Understanding which of these five scenarios will ultimately dominate requires tracking several macroeconomic, regulatory, and technological indicators over the coming years.

| Scenario | Primary Catalyst | Key Characteristics | Lead Adopters |

|---|---|---|---|

| 1. Institutional Assimilation | GENIUS Act / Spot ETFs | Banks issue tokenized deposits; DeFi is absorbed into regulated backends. | Wall Street, Major Commercial Banks, Institutional Asset Managers. |

| 2. Global South Leapfrog | Inflation / High Remittance Fees | P2P stablecoin networks bypass traditional banking infrastructure entirely. | Retail users in Sub-Saharan Africa, Latin America, Southeast Asia. |

| 3. The Unified Ledger | BIS Frameworks / CBDCs | Integration of central bank reserves and tokenized assets on a single programmable platform. | Central Banks, Monetary Authorities, Wholesale Banking. |

| 4. Fragmented Parallel System | Interoperability Tech | Regulated institutional tokenization coexists with permissionless, open-source DeFi. | Tech-savvy consumers, AI networks, DAOs, Fintech hybrids. |

| 5. Systemic Contagion | Leverage / Cross-Asset Contagion | A major crypto exploit or stablecoin run spills over into traditional fiat markets. | N/A (Represents a systemic failure state impacting all participants). |

Market participants and policymakers should monitor specific warning signs to gauge systemic health. The transparency of major stablecoin issuers is the linchpin of stability; persistent failures to provide verifiable, third-party audits of reserve assets signal elevated contagion risk 1258. Additionally, the sources of DeFi yield must be scrutinized. If yields remain artificially high compared to traditional risk-free rates without a clear mechanism of underlying economic value creation, it may indicate unsustainable leverage rather than genuine financial innovation 6061. Finally, the proliferation of "zombie" projects - cryptocurrencies with dead development repositories, collapsed trading volumes, and abandoned social channels - can indicate a weakening of the broader ecosystem's resilience and a misallocation of capital 62.

Bottom line

The future of cryptocurrency and DeFi is no longer a question of survival, but of structural implementation. The convergence of clear regulatory frameworks like the GENIUS Act and MiCA with institutional tokenization pilots suggests that distributed ledger technology is firmly embedding itself into the global financial architecture. However, whether this integration results in a democratized, highly efficient parallel economy or a centralized system vulnerable to novel contagion risks will depend heavily on how regulators manage the transparency of stablecoin reserves and cross-border liquidity over the next five years.