How the End of SAVE in 2026 Affects 7.5 Million Borrowers

The federal SAVE student loan repayment plan is permanently ending, forcing 7.5 million enrolled borrowers to select a new repayment strategy or face default placements in standard, high-cost plans. Starting on July 1, 2026, the Department of Education will trigger a 90-day window for borrowers to transition to an alternative, such as the surviving Income-Based Repayment (IBR) plan or the new Repayment Assistance Plan (RAP). Most borrowers will see significant increases in their monthly payments and must act proactively to avoid being locked into fixed-payment plans that offer no pathway to loan forgiveness.

The Legal Demise of the SAVE Repayment Plan

For more than a year and a half, millions of federal student loan borrowers have lived in a state of sustained financial limbo 1. The Saving on a Valuable Education (SAVE) plan, launched in 2023 by the Biden administration, was originally billed as a transformation of the federal student loan landscape. It was designed to be the most generous income-driven repayment plan in American history, offering terms that structurally changed how lower- and middle-income families managed educational debt 12.

However, the plan's ambition proved to be its undoing. SAVE immediately faced aggressive legal challenges from multiple Republican-led states, primarily Missouri, which argued that the Department of Education had vastly overstepped its statutory authority by enacting loan forgiveness provisions without explicit congressional approval 13. In 2024, federal courts agreed, issuing a series of injunctions that blocked the implementation of SAVE's key benefits and forced the Department of Education to place all enrolled borrowers into an administrative forbearance 24.

During this administrative forbearance, borrowers were not required to make any monthly payments. Crucially, however, the time spent in this frozen status did not count toward Income-Driven Repayment (IDR) forgiveness or Public Service Loan Forgiveness (PSLF) 24. Furthermore, while the forbearance initially paused interest, interest on these loans resumed accumulating in August 2025, leaving borrowers' balances to grow while their progress toward debt cancellation remained entirely stalled 1245.

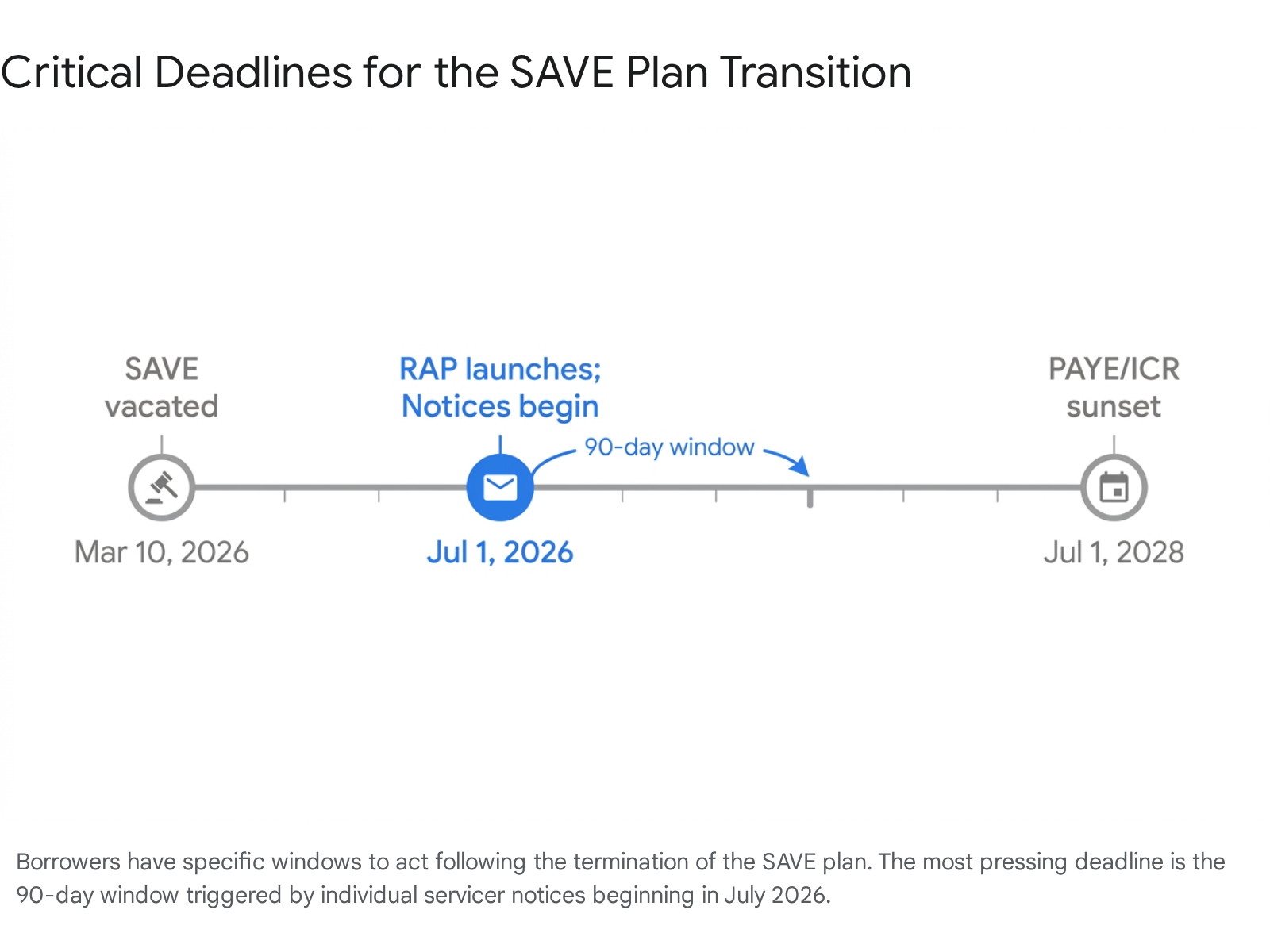

The final blow to the program arrived in the spring of 2026. On March 10, 2026, the U.S. Court of Appeals for the Eighth Circuit issued an order that effectively and permanently terminated the SAVE plan 167. The appellate court reversed a lower court's dismissal and directed the approval of a settlement reached between the newly instated Trump administration and the state of Missouri 147.

Because SAVE was a federal rulemaking standard, the settlement applied nationwide, dismantling the program for borrowers in every state 4. Under the binding terms of the settlement, the Department of Education was required to immediately halt the enrollment of any new borrowers into SAVE, deny all pending applications sitting in the backlog, and forcibly transition the 7.5 million current participants into alternative, legal repayment plans 347.

The 90-Day Transition Window Explained

With the SAVE plan legally vacated, the Department of Education faced the unprecedented logistical hurdle of transitioning 7.5 million borrower accounts without crashing the federal servicing system. To manage this, the government outlined a phased transition process hinging on a critical 90-day window 3.

How the Timeline Works

The transition is not an immediate, overnight event. According to official guidance released by the Department of Education, federal loan servicers - the private companies contracted to manage the collection of federal student loans - will begin issuing formal, individualized notices to borrowers on or around July 1, 2026 4689.

These notices will explicitly instruct borrowers to exit the defunct SAVE plan and select a lawful alternative 39. It is vital to understand that the 90-day clock does not automatically start for every borrower simultaneously on July 1; rather, a borrower has exactly 90 days from the date their specific servicer notice is issued 4.

Because the rollout of these emails and letters will occur in tranches to avoid overwhelming the servicers' web portals, some borrowers may not receive their notice until mid-July or early August. Consequently, the actual deadline to switch plans will fall sometime between late September and November 2026 for the vast majority of the affected population 48.

The Cost of Remaining in Forbearance

While borrowers technically have until the end of their personalized 90-day window to make a move, financial experts and advocacy groups warn that waiting carries a significant opportunity cost. Borrowers are legally permitted to voluntarily apply to switch plans immediately, and for many, doing so is highly advantageous 348.

The primary danger of delaying the transition lies in the mechanics of the ongoing administrative forbearance. Because months spent in this holding pattern yield zero qualifying payment credits toward PSLF or IDR forgiveness, waiting unnecessarily prolongs the time a borrower is tethered to their debt 461210. Every month a borrower waits to transition is another month of capitalization and interest accrual that brings them no closer to the finish line.

For borrowers pursuing PSLF, the situation is particularly pressing. They can either switch to a qualifying plan now to resume earning credits, or they can ride out the forbearance and attempt to use the government's "PSLF buyback" program later 11. The buyback program allows borrowers to retroactively pay for months spent in ineligible forbearance statuses, effectively buying back the lost time 12. However, this requires a lump-sum payment equivalent to what the borrower would have paid on an IDR plan during those months, requiring careful cash-flow management 1112.

Department of Education Processing Backlogs

A secondary risk of waiting until the end of the 90-day window is the likelihood of severe processing delays. The federal student loan system has historically struggled with application backlogs, particularly when rolling out new programs or executing mass transitions 4.

Consumer advocacy groups anticipate a massive surge in IDR applications in the late summer and early fall of 2026 as millions of borrowers simultaneously rush to meet their 90-day deadlines 4. Borrowers who delay their applications may find themselves stuck in processing limbo, during which they remain in forbearance, continuing to accrue interest without making progress toward loan cancellation 11.

Navigating the Income-Driven Repayment (IDR) Overhaul

The forced exodus from the SAVE plan arrives at a moment of broader, systemic upheaval in the federal student loan landscape. The One Big Beautiful Bill Act (OBBBA), a sweeping piece of reconciliation legislation signed into law on July 4, 2025, fundamentally rewrote the rules for federal borrowing and repayment 161318.

The primary goal of the OBBBA's repayment provisions was to streamline what policymakers viewed as an overly complex, confusing web of overlapping income-driven options 1415. As a result, legacy plans are being systematically dismantled. Pay As You Earn (PAYE) and Income-Contingent Repayment (ICR) will stop accepting new enrollees on July 1, 2026, and will sunset entirely on July 1, 2028 121616. Borrowers who remain in these plans at the sunset date will be automatically transitioned into surviving alternatives 1216.

For a borrower exiting SAVE in mid-2026, the long-term decision effectively boils down to two distinct income-driven options: the newly created Repayment Assistance Plan (RAP) or the older, surviving Income-Based Repayment (IBR) plan.

The Introduction of the Repayment Assistance Plan (RAP)

Launching on July 1, 2026, the Repayment Assistance Plan (RAP) was created by Congress to serve as the government's flagship income-driven option going forward 16221718. For any federal student loans disbursed on or after July 1, 2026, RAP will be the only income-driven repayment plan available, cementing its role as the future of federal student debt management 16251920.

Borrowers exiting the SAVE plan who wish to enroll in RAP cannot do so immediately; they must wait until the program officially launches on July 1 46828. Advisors suggest that borrowers eager to join RAP may need to temporarily switch to another plan, like IBR, or file for a short-term forbearance to bridge the gap until July 628.

How RAP Calculates Monthly Payments

RAP calculates monthly obligations using a fundamentally different mathematical architecture than any previous IDR plan. Historically, plans like SAVE, PAYE, and IBR calculated payments based on "discretionary income" - defined as a borrower's income minus a sizable percentage of the federal poverty guideline 1218. This poverty deduction created a buffer that allowed low-income earners to qualify for $0 monthly payments.

RAP eliminates the discretionary income formula entirely. Instead, it assesses payments based on fixed percentages of a borrower's total Adjusted Gross Income (AGI) 162122. There is no poverty guideline buffer in RAP 1618.

The payment formula scales progressively across eleven income brackets: * Borrowers earning under $10,000 annually pay a flat minimum of $10 per month (or $120 a year) 202231. RAP firmly eliminates the $0 monthly payment option 820. * For AGI between $10,001 and $20,000, the base payment is 1% of AGI. * For AGI between $20,001 and $30,000, the base payment is 2% of AGI. * The percentage steps up by a full percentage point for every $10,000 increase in income 1822. * The scale caps at 10% of AGI for earners making $100,001 or more annually 2022.

Once the base percentage of AGI is calculated, the Department of Education allows borrowers to deduct $50 per month from their bill for every dependent claimed on their federal tax return 212223. However, this deduction cannot bring the monthly payment below the hard floor of $10 202123.

Crucially for dual-income households, the OBBBA legislation explicitly maintained a vital loophole: married borrowers who file their taxes as "Married Filing Separately" are permitted to exclude their spouse's income from the RAP calculation 18212223. If a couple files jointly, their combined AGI is used to dictate the payment bracket, drastically increasing the monthly obligation for households where only one partner holds significant student loan debt 1821.

RAP's Protection Against Negative Amortization

Despite its more aggressive payment calculations, RAP preserves one highly popular benefit that mirrors the defunct SAVE plan: it provides robust protection against negative amortization 14171920.

Negative amortization occurs when a borrower's calculated monthly payment on an IDR plan is so low that it fails to cover the interest that accrues on the loan that month. Under older plans, this unpaid interest was frequently added to the loan balance, causing the total debt to balloon exponentially even while the borrower made on-time payments 17.

Under RAP, the Department of Education will fully subsidize any unpaid interest for borrowers who meet their monthly payment obligations. This ensures that a borrower making consistent, on-time payments will never see their principal balance grow, regardless of how small their required payment is 317192021. Furthermore, the legislation includes a principal reduction matching feature: if a borrower's calculated monthly payment chips away at less than $50 of the loan principal, the government will apply an additional payment of up to $50 directly toward the principal to ensure the borrower makes tangible repayment progress 82023.

The Lack of a Payment Cap and the 30-Year Horizon

While the interest subsidies are attractive, RAP comes with two significant structural drawbacks that make it risky for high-earning professionals.

First, RAP explicitly lacks a payment cap 172023. Under old IDR rules, monthly payments were legally capped so they would never rise above what a borrower would have paid on a standard 10-year amortization plan, no matter how high their income grew 51824. Because RAP removes this ceiling, a borrower whose income skyrockets midway through their career could theoretically be required to pay thousands of dollars a month, vastly exceeding the standard 10-year repayment amount 171820.

Second, RAP significantly extends the timeline for debt cancellation. For borrowers who do not work in the public sector (and thus do not qualify for PSLF), RAP requires a grueling 30 years of continuous payments before any remaining balance is forgiven 81725202223. This is five to ten years longer than the 20- or 25-year forgiveness timelines promised by legacy plans, meaning borrowers will spend a considerably larger portion of their working lives tethered to student debt 71725.

The Survival of Income-Based Repayment (IBR)

Because Income-Based Repayment (IBR) possesses its own foundational statutory authority separate from both the OBBBA legislation and the SAVE litigation, it survives permanently for borrowers whose loans were disbursed before July 1, 2026 121616.

For the 7.5 million borrowers forced out of SAVE, IBR represents the most legally stable, time-tested alternative on the market 5. It operates on the traditional "discretionary income" model rather than AGI, and unlike RAP, it maintains a strict ceiling on how high monthly payments can rise 524.

Old IBR versus New IBR

The terms of IBR are bifurcated based on the exact date a borrower took out their very first federal student loan:

- "Old" IBR: If a borrower received their first federal loan prior to July 1, 2014, they are placed in the original iteration of IBR. Under this plan, monthly payments are calculated at 15% of their discretionary income, and they must make payments for 25 years (300 qualifying months) before receiving loan forgiveness 512283124.

- "New" IBR: If a borrower received their first federal loan on or after July 1, 2014, they benefit from a more generous formula. Payments are capped at 10% of discretionary income, and the forgiveness timeline is shortened to 20 years (240 qualifying months) 52831.

The practical impact of these dates hits particularly hard for borrowers who were previously enrolled in SAVE with undergraduate-only loans. Under SAVE, all undergraduate debt was slated for forgiveness after 20 years 24. Now, if their oldest loan predates the July 2014 cutoff, they only qualify for "Old" IBR - meaning they suddenly face 25 years of payments instead of 20. That equates to five extra years of financial burden they did not anticipate 12.

The Importance of the Payment Cap

The defining advantage of IBR over RAP is its payment cap. Under IBR, a borrower's monthly payment will never exceed the amount they would have paid under a standard 10-year repayment plan based on the loan balance at the time they entered IBR 524.

This cap is a vital safety net for professionals with steep earning trajectories - such as medical residents, junior attorneys, or early-career software engineers. Even if their income triples, their student loan bill will hit the 10-year standard ceiling and stop climbing 524. Consequently, financial advisors often steer high-earning professionals toward IBR to minimize long-term cash flow constraints 24.

Risks of Capitalized Interest

While IBR is highly protective of monthly cash flow, it is rigid to exit. If a borrower decides to leave IBR for any reason - whether to switch to RAP, a standard plan, or to consolidate - any unpaid interest that accrued while they were enrolled in IBR capitalizes 5.

Capitalization means the unpaid interest is permanently added to the principal balance of the loan. From that point forward, interest begins accruing on that new, larger principal, causing the debt to compound rapidly. Because of this severe penalty, financial experts warn that IBR is incredibly difficult to use as a temporary stop-gap. Rule of thumb: entering IBR should be viewed as a long-term commitment, not a short-term bridge while waiting for other policies to materialize 5.

Comparing Your Income-Driven Options

Navigating the transition requires understanding how the surviving and newly created plans stack up against the now-defunct SAVE plan.

| Feature | Repayment Assistance Plan (RAP) | Income-Based Repayment (IBR) | The Defunct SAVE Plan |

|---|---|---|---|

| Availability | All Direct Loans (except Parent PLUS). The only IDR available for new loans after July 1, 2026. | Exclusively for loans disbursed before July 1, 2026. | Terminated in March 2026. Closed to all borrowers. |

| Payment Calculation | 1% to 10% of AGI (based on income brackets), minus $50 per claimed dependent. | 10% or 15% of discretionary income, depending on when the oldest loan was disbursed. | 5% to 10% of discretionary income, heavily weighted toward a 225% poverty exemption. |

| Minimum Payment | $10 per month hard floor. No $0 payments allowed. | Can be as low as $0 for low-income borrowers. | Permitted $0 payments for millions of borrowers. |

| Payment Cap | None. Payments scale infinitely with high income. | Strictly capped at the 10-Year Standard Repayment amount. | None, but the low calculation percentages kept payments highly affordable. |

| Interest Subsidy | 100% of unpaid interest is subsidized; completely prevents negative amortization. | Unpaid interest grows and is added to the balance (subsidized only for the first 3 years on subsidized loans). | 100% of unpaid interest was subsidized. |

| Forgiveness Timeline | 30 years (10 years for PSLF). | 20 or 25 years (10 years for PSLF). | 10 to 25 years, depending on original balance and loan type. |

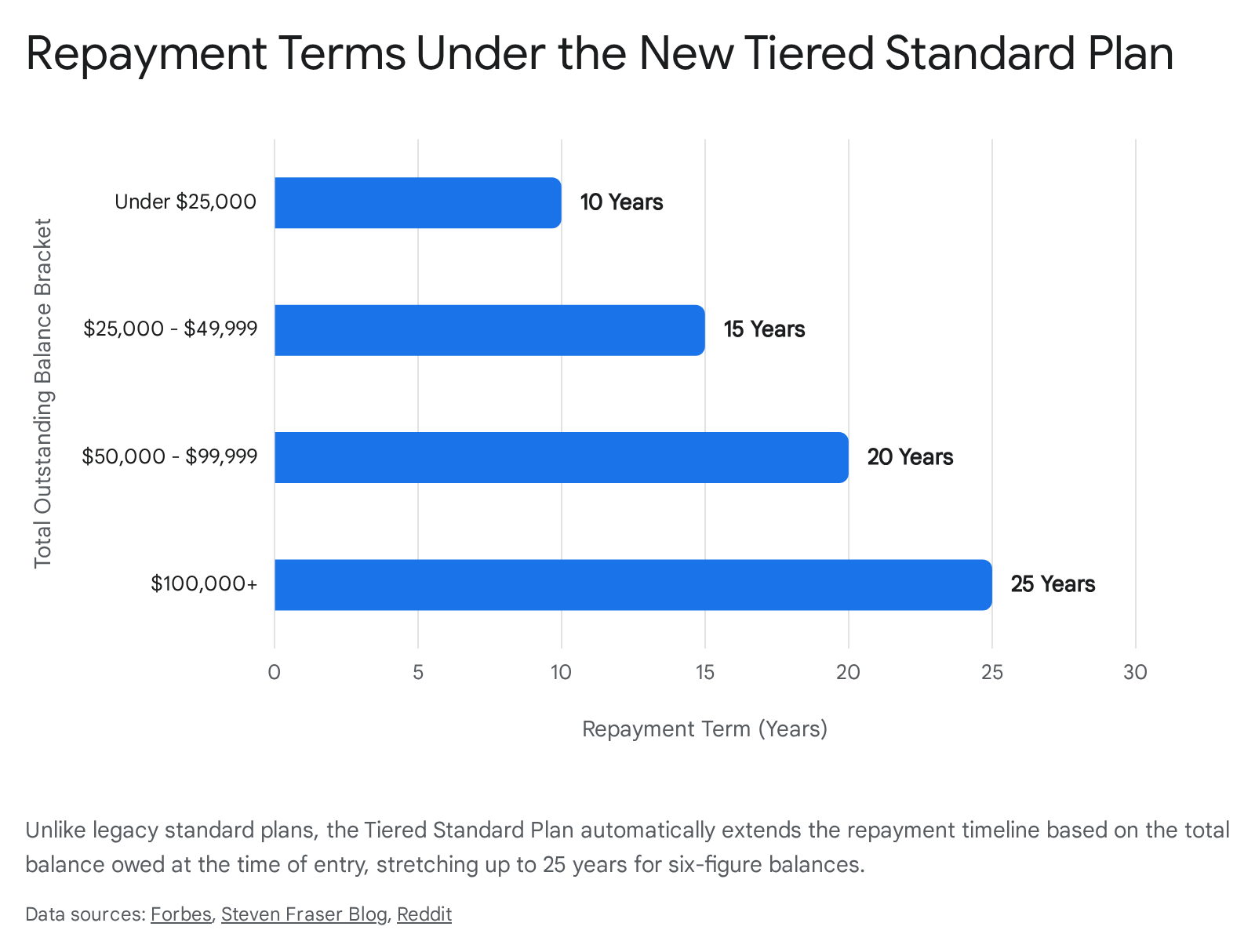

The Default Option: The New Tiered Standard Plan

For borrowers who ignore their loan servicer's notice and let their 90-day transition window expire, the Department of Education will execute an automatic enrollment 369. For loans disbursed prior to July 2026, this usually results in placement into the traditional 10-Year Standard Plan (or a longer consolidation standard plan for merged loans) 6. However, for the future, the OBBBA legislation created a new, mandatory fixed-payment paradigm: the Tiered Standard Plan 16142526.

Launching July 1, 2026, the Tiered Standard Plan fundamentally replaces the traditional 10-year standard plan as the baseline alternative to income-driven repayment 161536.

How Tiered Standard Calculates Payments

Unlike RAP or IBR, the Tiered Standard Plan is entirely divorced from a borrower's income. There is no annual income recertification required, and changes in employment have zero bearing on the bill 1626. Instead, it offers a fixed monthly payment calculated mathematically to entirely pay off the debt over a set number of years, factoring in only the total principal balance and the interest rate 26.

Unlike the traditional standard plan, which amortized all unconsolidated loans over exactly 10 years, the Tiered Standard Plan stretches the repayment timeline based on the sheer size of the borrower's debt 15312526:

- Balances under $25,000: 10-year repayment term.

- Balances between $25,000 and $49,999: 15-year repayment term.

- Balances between $50,000 and $99,999: 20-year repayment term.

- Balances of $100,000 or more: 25-year repayment term.

The Long-Term Cost of Extended Repayment

While the Tiered Standard Plan's extended terms - such as 25 years for a $100,000 balance - help to mathematically suppress the immediate monthly payment, this relief comes at a massive long-term cost. By stretching the debt over decades rather than 10 years, borrowers will pay exponentially more in compounding interest over the life of the loan 26.

Furthermore, the Tiered Standard Plan offers absolutely no forgiveness at the end of the term, as the payments are specifically designed to zero out the balance 2636. Crucially for public servants, time spent making payments under the Tiered Standard Plan does not qualify for Public Service Loan Forgiveness (PSLF) 36. Public servants defaulted into this plan must actively consolidate or switch back into an IDR plan to resume their trajectory toward cancellation.

Preparing for the "Payment Shock"

The forced transition out of the SAVE plan is widely expected to trigger a significant economic ripple effect, a phenomenon broadly categorized by financial analysts and credit bureaus as "payment shock."

For nearly a year, the 7.5 million borrowers in the SAVE program were shielded by an administrative forbearance. They were legally required to pay $0 per month while the state-led lawsuits played out in the courts 127. When the 90-day transition windows close in the late summer and fall of 2026, these households will abruptly lose that shield. They will be required to absorb a substantial new monthly bill just as other seasonal household expenses - such as back-to-school costs and approaching holiday spending - begin to peak 428.

Data on Expected Payment Increases

Because the SAVE plan featured an exceptionally generous formula with massive poverty exemptions, the required payments on virtually any alternative plan - whether the AGI-based RAP, the 15% discretionary income IBR, or the fixed Tiered Standard - will be substantially higher. Furthermore, when borrowers recertify for their new plans in 2026, their payments will be calculated using their most recent tax returns, meaning those who have received raises over the past two years will see their payments compound upward 828.

Consumer advocacy groups, such as the Student Borrower Protection Center (SBPC), project that the transition will force an immediate, unprecedented payment jump for many Americans. For a typical single borrower with a college degree transitioning off a $0 SAVE payment, the new monthly obligation could hit $431, translating to an annual household budget hit of more than $5,000 27.

Data from major credit reporting agencies corroborates this severity. TransUnion projects that roughly 50% of borrowers experiencing this payment shock will face new monthly obligations exceeding $200 28. Even more alarmingly, nearly one in five borrowers will be required to pay upwards of $500 a month to maintain good standing on their federal debt 28. This shock hits a consumer base that has increasingly turned to credit cards and other debt vehicles to manage inflation since the pandemic, leaving them with thinner margins to absorb a new $500 liability 428.

Demographic and Regional Disparities

The demographic impact of this payment shock will be highly uneven, disproportionately impacting specific regions and age groups. Because SAVE's aggressive income exemptions vastly benefited lower-income families, borrowers in regions with lower median incomes and historically higher student loan default rates enrolled in the plan at massive volume. Consequently, states in the deep South, such as Alabama and Mississippi, will bear the brunt of the immediate budgetary strain as the plan unravels 4. In these areas, absorbing a sudden $300 to $500 monthly bill is significantly harder due to regional wage stagnation.

Generational data further complicates the picture. According to the TransUnion study, older borrowers - specifically the Silent Generation, Baby Boomers, and Gen X - are statistically far more likely to face monthly bills over $500 compared to their younger counterparts 28. Nearly 30% of Boomers and 29% of Gen X borrowers face payments exceeding the $500 threshold, whereas only 5% of Gen Z borrowers face similar burdens 28. This disparity is driven by longer histories of accumulated debt, capitalized interest over decades, and higher current earning brackets that drive up IDR calculations.

Strategies for Budgeting the Transition

To mitigate the shock, financial advisors strongly recommend borrowers act before their 90-day window expires. The most critical step is ensuring income information is strategically timed. If a borrower's income increased significantly from 2024 to 2025, they may benefit from switching plans before filing their 2025 taxes, allowing them to use their lower 2024 income to secure a more affordable initial payment on IBR or RAP 28. Filing a tax extension can provide the necessary runway to lock in a lower payment for the first year of the transition 28.

For borrowers in severe distress who cannot afford the new RAP or IBR minimums, the options are shrinking. The OBBBA legislation mandates that unemployment and economic hardship deferments will no longer be available for loans issued on or after July 1, 2027, and general forbearance periods are being capped at 9 months within any 2-year window 3136.

The Return of the Tax Bomb in 2026

Compounding the financial anxiety of higher monthly payments is a critical, often-overlooked shift in the federal tax code that takes effect exactly as borrowers are transitioning out of SAVE.

Why Student Loan Forgiveness is Taxable Again

Under the American Rescue Plan Act of 2021, Congress temporarily exempted any student loan debt forgiven by the federal government from federal income taxes 1636. This vital exemption was allowed to expire on December 31, 2025 791636.

As a result, effective January 1, 2026, student loan forgiveness granted through income-driven repayment plans - whether IBR, RAP, or sunsetting legacy plans - is once again considered taxable ordinary income by the IRS 7936.

This creates a terrifying scenario for long-term borrowers commonly referred to as the "tax bomb." If a borrower reaches the end of their 20, 25, or 30-year repayment term and has a $60,000 remaining principal and interest balance discharged, the IRS treats that $60,000 as if the borrower earned it in a paycheck that year. Depending on their resulting tax bracket, this could trigger a sudden, immediate federal tax liability of $10,000 to $20,000 or more, payable by April of the following year 36.

For private-sector workers relying on long-term IDR forgiveness, the return of the tax bomb makes the calculus of choosing a new plan infinitely more complex 1736. Opting for RAP, which extends the forgiveness horizon to 30 years and theoretically allows more interest to accrue, could result in a massive taxable event three decades down the line. Borrowers must now aggressively save for the tax liability parallel to paying down their loans.

PSLF Exemptions

Notably, there is one major exception: Public Service Loan Forgiveness (PSLF). Discharges granted under the PSLF program remain entirely tax-free under a separate, permanent provision of the federal tax code 1636. For teachers, nurses, government employees, and nonprofit workers, reaching 120 qualifying payments will still result in a clean slate with zero IRS blowback 1622. This massive disparity makes PSLF the single most valuable forgiveness pathway remaining in the federal system.

Sweeping Changes Under the One Big Beautiful Bill Act (OBBBA)

While the immediate crisis centers on the 7.5 million borrowers exiting the defunct SAVE plan, the One Big Beautiful Bill Act (OBBBA) institutes permanent, systemic restrictions on future borrowing that will reshape the economics of higher education starting July 1, 2026.

Historically, the federal student lending apparatus allowed graduate students and parents of dependent undergraduates to borrow up to the total "cost of attendance" of a university through the Direct PLUS loan program. Critics have long argued that this uncapped borrowing system created a moral hazard, contributing directly to skyrocketing tuition costs at both the undergraduate and graduate levels 15. The OBBBA sharply curbs this system in an attempt to enforce fiscal discipline on universities 1415.

The Elimination of Graduate PLUS Loans

The most severe cut falls on graduate education. The Grad PLUS loan program is entirely eliminated for all new borrowers starting July 1, 2026 1329303132. Moving forward, graduate students are strictly capped at borrowing $20,500 per year in federal unsubsidized loans, with a lifetime aggregate limit of $100,000 713152932.

For students pursuing designated "professional" degrees - such as medicine, law, and pharmacy - the caps are slightly higher, allowing up to $50,000 annually with a $200,000 aggregate limit 713152943. Regardless of the degree path, the overall absolute lifetime cap for any individual, combining all undergraduate, graduate, and professional study, is firmly set at $257,500 132333. Students attending high-cost master's programs where tuition exceeds $20,500 annually will now be forced to pay out of pocket, seek institutional aid, or turn to private student loans 29.

New Restrictions on Parent PLUS Borrowers

While the Parent PLUS program survives the OBBBA, it is fundamentally restricted. Parents are no longer allowed to borrow up to the full cost of attendance. Instead, they are restricted to borrowing a maximum of $20,000 per year, per dependent student, with a hard lifetime aggregate limit of $65,000 per student 71323303133.

Furthermore, the repayment options for parent borrowers have been severely curtailed. Any Parent PLUS loans disbursed after June 30, 2026, are permanently ineligible for income-driven repayment plans, time-based IDR forgiveness, or Public Service Loan Forgiveness (PSLF) 71618313034. New Parent PLUS borrowers will be forced to repay the debt via the fixed-payment Tiered Standard Plan 3034.

For parents with existing Parent PLUS loans who wish to access income-driven repayment, the window is closing rapidly. They must consolidate their loans into a Direct Consolidation Loan before July 1, 2026, to secure eligibility for the surviving IBR plan 71635.

The Part-Time Proration Rule

In another shift aimed at curbing over-borrowing, the Department of Education will now strictly prorate loan limits for students taking less than a full-time course load. Prior to 2026, students could often access maximum loan limits regardless of their exact credit hour count. Now, if a student enrolls in fewer than 12 units, their federal loan eligibility is mathematically reduced. Consequently, dropping a class mid-semester can result in an immediate downward adjustment of a student's aid package, potentially creating unexpected tuition balances 13233133.

Legacy Status for Current Borrowers

The OBBBA legislation does provide a narrow "legacy status" exemption to protect students currently mid-degree. Borrowers - including parents - who took out loans for a specific academic program prior to July 1, 2026, can continue borrowing under the old, uncapped rules 1323303133.

However, this legacy status is highly fragile. It lasts for a maximum of three academic years or until the student finishes their credential, whichever comes first 132333. Crucially, the student must remain continuously enrolled in the exact same academic program at the exact same institution 2333. Taking a leave of absence, withdrawing for a semester, or transferring to a new university instantly breaks this continuous enrollment requirement, triggering the immediate application of the new, restrictive OBBBA caps 3133.

New Legal Battles Over "Professional" Degree Definitions

While the transition out of the SAVE plan is settled law, the rollout of the new OBBBA borrowing limits has triggered a fresh wave of aggressive, high-stakes litigation. The dispute centers heavily on how the Department of Education is interpreting the statutory definition of a "professional student" under the new law.

Because the OBBBA grants professional students vastly higher borrowing caps ($50,000 annually) compared to standard graduate students ($20,500 annually), the regulatory definition literally dictates whether specialized academic programs can survive financially 152943.

The Department of Education's Final Rule

On May 1, 2026, the Department of Education published a final rule implementing the OBBBA loan limits. In this rule, the Department severely narrowed the definition of a "professional degree." To qualify for the higher $50,000 cap, the Department mandated that a degree program must be generally at the doctoral level, require at least six academic years of postsecondary education, require licensure specifically to begin practice, and fall within specific four-digit CIP (Classification of Instructional Programs) codes 43.

This stringent interpretation explicitly excluded a wide swath of vital healthcare and specialized disciplines. Programs training nurse practitioners, physical therapists, physician assistants, educators, public health professionals, and marriage and family therapists were grouped into the lower $20,500 tier 43.

Lawsuits from States and Healthcare Providers

The backlash from the medical, educational, and political sectors was immediate and furious. Higher education institutions warned that capping physical therapy and advanced nursing students at $20,500 would force program closures and reduce enrollment capacity nationwide 3243.

In late May 2026, a coalition of twenty-five state attorneys general filed suit in federal court in Maryland. The coalition argued that the Department's final rule will decimate the national healthcare workforce by pricing students out of necessary medical training, ultimately harming public health in rural and underserved areas 32.

A parallel lawsuit, driven by major national nursing associations, argues that the Department of Education unlawfully rewrote the OBBBA statute. The plaintiffs contend that Congress only required a professional degree to signify skill beyond a bachelor's degree and require licensure; they argue the Department illegally added the six-year and specific CIP code requirements to artificially suppress lending 43.

These plaintiffs are aggressively seeking emergency injunctive relief to block the rule before the new loan caps officially take effect on July 1, 2026 43. The courts have established a rapid rocket-docket briefing schedule, setting the stage for rulings in early June 2026 that will determine the immediate financial reality for thousands of medical and graduate students entering the fall semester 43.

Bottom line

The termination of the SAVE repayment plan forces 7.5 million federal borrowers to transition to new strategies within a tight 90-day window triggered by their servicers this summer. Borrowers must proactively choose between the surviving Income-Based Repayment (IBR) plan or the new Repayment Assistance Plan (RAP), both of which will likely result in a significant "payment shock" compared to SAVE. Those who fail to act will be automatically defaulted into the inflexible Tiered Standard Plan, permanently losing access to loan forgiveness pathways and trapping themselves in decades of compounding interest.