How to Avoid Student Loan Regret Before You Enroll

What Is the Most Effective Strategy for Avoiding Student Loan Regret Before Enrolling?

To definitively avoid the enduring burden of student loan regret, prospective borrowers must strictly cap their total anticipated educational debt at or below their projected first-year starting salary, exhaust all federal borrowing options before considering private credit, and empirically model their repayment trajectory against the new 2026 federal repayment structures prior to matriculation. The foundation of smart borrowing rests on treating federal aggregate loan limits not as a prescriptive target, but as a maximum absolute threshold to actively avoid. By translating complex financial aid offers into rigid debt-to-income ratios, borrowers can insulate their future financial stability against labor market volatility and structural shifts in higher education finance.

For millions of graduates, the true cost of higher education is not measured merely in nominal tuition dollars, but in the deferred milestones of adulthood. The modern student loan is often conceptually misunderstood by prospective matriculants. A more practical analogy is to view excessive student debt as a "reverse mortgage" on one's future labor. Instead of leveraging an existing tangible asset for cash, the borrower is trading a fixed, non-negotiable percentage of their future, unearned wages to finance a present experience. When that percentage becomes disproportionately large, the foundational structure of adult financial life begins to fracture. The long-term shadow of unaffordable debt stretches far beyond the monthly billing cycle; it acts as a heavy anchor on economic mobility, dictating career trajectories, delaying homeownership, and stifling household formation. By utilizing extensive data from the Consumer Financial Protection Bureau (CFPB) and the Federal Reserve, this analysis provides an exhaustive, expert-level examination of how to preempt borrower regret through empirical planning, a deep understanding of sweeping legislative overhauls taking effect in 2026, and a firm grasp of consumer protections.

How Does Educational Debt Impact Long-Term Macroeconomic and Personal Milestones?

Before examining the granular mechanics of loan origination and repayment, it is necessary to understand the macroeconomic and psychological toll of overborrowing. The consequences of signing a master promissory note without adequate financial modeling manifest years later in severe systemic distress. Data collected by the CFPB and the Federal Reserve illustrates a stark reality for those who borrow without strict debt-to-income constraints. In a comprehensive 2023-2024 survey conducted as the pandemic-era federal student loan payment pause ended, the CFPB found that 63% of borrowers reported experiencing significant difficulty making their student loan payments, and 37% had missed at least one payment 123.

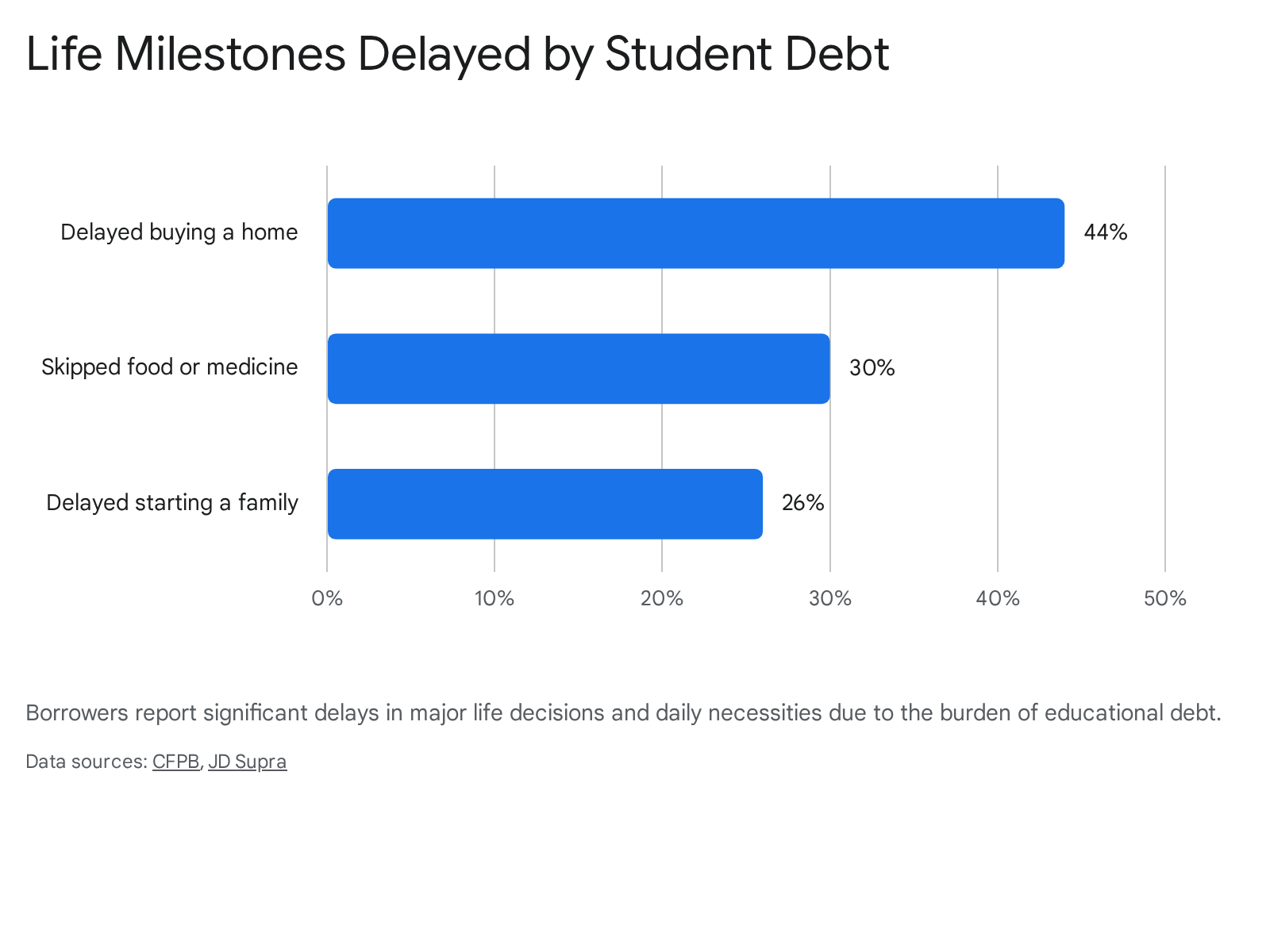

The consequences of these financial strains manifest in severe, quantifiable lifestyle compromises. Among the surveyed borrowers, 44% reported delaying the purchase of a home, and 26% delayed starting or expanding a family as a direct result of their educational debt obligations 23. More alarmingly, 30% of borrowers admitted to going without basic necessities, such as food or medicine, to manage their student loan payments, and 38% carried revolving credit card debt they otherwise would have avoided 23.

The Federal Reserve's 2025 Economic Well-Being of U.S. Households report corroborates these findings, revealing that 20% of borrowers were actively behind on payments or in collections for one or more of their student loans as of late 2024, an increase from 16% in 2023 3. This distress is not distributed equally across the population. It disproportionately affects marginalized and vulnerable cohorts; borrowers who attended private for-profit institutions exhibited a delinquency rate of 35%, compared to 16% for those who attended public institutions 3. Furthermore, Black and Hispanic borrowers, Pell Grant recipients, and individuals who incurred debt but failed to complete a four-year degree report significantly higher rates of repayment hardship 123.

Economists note that student debt hampers broader economic engines beyond the individual household. For every $1,000 in student loan debt assumed, homeownership among recent college graduates declines by 1.8% 5. The entrepreneurial landscape is similarly stifled; business income is 42% lower for the average business owner carrying just $10,000 in student debt compared to their debt-free peers, and those owing more than $30,000 are 11% less likely to start a new business entirely 5. Each time a consumer's student debt-to-income ratio increases by a single percentage point, their broader economic consumption declines by 3.7 percentage points 5.

When surveyed by the CFPB, 42% of federal student loan borrowers reported they had only ever utilized the standard fixed repayment plan, with nearly a third of those borrowers entirely unaware that alternative, income-driven repayment plans existed to lower their monthly obligations 145. The primary mechanism to avoid this regret is hyper-vigilance during the initial financial aid offer evaluation phase, coupled with a deep, systemic understanding of the evolving regulatory landscape governing financial aid and repayment.

How Do the 2024 - 2025 FAFSA Overhauls Alter Financial Need and Borrowing Risk?

The first tactical step in making smart borrowing decisions is understanding the application pipeline that determines borrowing eligibility. The Free Application for Federal Student Aid (FAFSA) recently underwent a historic structural overhaul mandated by the FAFSA Simplification Act, which took full effect for the 2024-2025 academic year 89106. For prospective borrowers, this legislative overhaul fundamentally alters how financial need is calculated by educational institutions, which subsequently dictates the mix of subsidized grants versus unsubsidized loans offered in an aid package.

Historically, the FAFSA utilized the Expected Family Contribution (EFC) metric to estimate a family's ability to pay. This has been entirely replaced by the Student Aid Index (SAI) 89. Unlike the EFC, which bottomed out at a rigid zero, the SAI can drop to a negative value of -1,500 810. This negative allowance provides financial aid administrators with a far more granular view of severe financial need, theoretically allowing institutions to target limited campus-based aid to the most vulnerable students, potentially reducing their reliance on predatory private loans 8. Additionally, the overhaul implemented the FUTURE Act Direct Data Exchange (FA-DDX), which mandates that Federal Tax Information (FTI) be retrieved securely and directly from the Internal Revenue Service (IRS) 89106. This removes the ability for families to manually input or estimate tax data, thereby eliminating a common source of application errors that previously resulted in delayed aid offers or inaccurate loan maximums 8.

However, a critical change that significantly increases the risk of overborrowing for middle-class families is the elimination of the "sibling discount" 10. Under the previous EFC formula, families with multiple children enrolled in college simultaneously saw their expected contribution divided by the number of enrolled students, drastically increasing their eligibility for need-based aid. The new SAI methodology mandated by the Simplification Act explicitly removes the number of family members attending college from the calculation 10. Consequently, families with multiple dependents in higher education simultaneously may see their calculated financial need plummet, resulting in smaller grant offers and substantially larger gaps in the Cost of Attendance (COA) 10.

If a family is unaware of this structural change, they may inadvertently attempt to bridge this newly widened gap by turning to high-interest private student loans or Parent PLUS loans, thereby falling into the exact debt trap that causes long-term regret. Furthermore, the FAFSA changes also removed the exemption of assets for family farms and family-owned small businesses, requiring these assets to be reported and potentially further driving up the SAI for rural and entrepreneurial families 7.

What Are the 2026 Repayment Paradigm Shifts Under the One Big Beautiful Bill Act?

To accurately project affordability and avoid regret, borrowers must look beyond the immediate disbursement of funds and analyze the exact repayment environment they will enter upon graduation. The passage of the One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, completely restructures federal student aid and repayment for all new loans disbursed on or after July 1, 2026 789101611.

Borrowers taking out new loans after this date will find a streamlined, albeit starkly different, set of options. Legacy income-driven plans - such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR) - will be permanently closed to new borrowers 891812. Additionally, the highly publicized Saving on a Valuable Education (SAVE) plan, which was mired in complex litigation, has been formally terminated by the reconciliation bill 89. For new borrowers starting their educational journey in 2026 or later, only two federal repayment plans will exist: the Repayment Assistance Plan (RAP) and the Tiered Standard Plan 781611.

The Repayment Assistance Plan (RAP)

RAP is a newly constructed income-driven repayment plan that radically changes the calculation of borrower affordability 913212223. Instead of relying on complex formulas based strictly on discretionary income metrics tied to federal poverty lines, RAP utilizes a progressive, tiered scale tied directly to a borrower's Adjusted Gross Income (AGI) 212223.

The mathematics governing RAP are highly specific and intended to shield low-income earners while extracting higher payments from affluent graduates. Borrowers earning an AGI of $10,000 or less are required to pay a flat minimum of $10 per month 212223. For incomes above $10,000, the required payment scales upward from 1% to 10% of AGI. The percentage increases by one point for every additional $10,000 in AGI. For example, a borrower with an AGI between $10,001 and $20,000 pays 1% of their AGI annually; an AGI between $50,001 and $60,000 requires 5% of AGI; and any AGI of $100,001 or more maxes out at the 10% threshold 212223. The calculated annual payment is divided by twelve to establish the monthly obligation, which is then further reduced by a flat $50 for each dependent claimed on the borrower's federal tax return 21222314.

Crucially, RAP acts as a shield against runaway negative amortization, a flaw in previous plans that caused balances to balloon even when borrowers made on-time payments. Under RAP, if a borrower's calculated monthly payment is less than the interest that accrues on the loan that month, the federal government entirely waives the unpaid interest 111214. Furthermore, if the required, on-time payment fails to reduce the principal balance by at least $50, the government provides a matching subsidy to ensure the principal decreases by that minimum amount each month, greatly assisting borrowers with small balances 11212314.

However, this structural safety net comes with a severe temporal tradeoff that borrowers must factor into their life plans. While previous income-driven plans offered loan forgiveness after 20 or 25 years, RAP extends the timeline for non-public sector forgiveness to a grueling 30 years (360 qualifying monthly payments) 1112212214. A 30-year student loan effectively runs concurrently with a standard home mortgage, fundamentally altering retirement planning and lifelong wealth accumulation. Borrowers seeking Public Service Loan Forgiveness (PSLF) retain the traditional 10-year (120 payments) timeline under RAP 111222.

The Tiered Standard Plan

For those who opt out of income-driven repayment, or for Parent PLUS borrowers who are statutorily ineligible for RAP, the only alternative is the new Tiered Standard Plan 7111812. The Tiered Standard Plan operates mechanically like a traditional fixed-rate mortgage, requiring fixed monthly payments that guarantee the loan is paid off in full by the end of the term 181321. However, unlike the legacy 10-year Standard Repayment Plan, the Tiered plan forcibly extends the repayment term based on the total outstanding principal balance upon the borrower entering repayment.

| Total Outstanding Student Loan Balance | Required Repayment Term |

|---|---|

| Less than $25,000 | 10 Years |

| $25,000 to $49,999 | 15 Years |

| $50,000 to $99,999 | 20 Years |

| $100,000 or more | 25 Years |

Data Source: U.S. Department of Education, OBBBA Guidelines 1118121321

While extending the term artificially lowers the immediate monthly payment obligation, it geometrically increases the total volume of interest paid over the life of the loan. Borrowers must understand that under the Tiered Standard Plan, a $60,000 debt will actively siphon wealth away from investments for two full decades, offering no timeline for forgiveness 181321.

Sweeping Caps on PLUS Borrowing

The OBBBA also implements strict interventions to prevent predatory borrowing by parents and graduate students. Historically, Parent PLUS and Graduate PLUS loans allowed borrowing up to the full, often inflated, Cost of Attendance - a policy that fueled the $1.7 trillion debt crisis by enabling families to borrow limitlessly 1526.

Starting July 1, 2026, the Graduate PLUS program is abolished entirely for new borrowers 1615161730. Graduate students will be restricted solely to Direct Unsubsidized loans, which are capped at $20,500 annually (or $50,000 for specific medical and law programs), with a strict lifetime aggregate limit across all federal loans established at $257,500 1611151631.

Similarly, Parent PLUS loans will be severely capped. Regardless of the institution's stated sticker price, parents will be legally prohibited from borrowing more than $20,000 per year per child, with an absolute lifetime cap of $65,000 per child across all parents combined 161115261631. By enforcing these strict caps, federal policy is attempting to force families into cheaper educational alternatives, rather than allowing them to indefinitely mortgage their retirements to fund expensive private institutions.

How Can Borrowers Accurately Calculate Their Maximum Sustainable Debt Load?

The most potent defense against borrower regret is the rigorous, mathematical evaluation of debt affordability before signing a master promissory note. Financial planners and the CFPB consistently emphasize a foundational rule of thumb: the total amount of student loan debt at graduation should never exceed the borrower's realistically anticipated annual starting salary 32183419.

This 1:1 total-debt-to-income ratio ensures that the corresponding monthly debt service ratio remains manageable. When total debt equals starting salary, the monthly loan payment on a standard 10-year repayment term generally consumes between 8% and 10% of the borrower's gross monthly income 3218192037. Exceeding this 10% threshold pushes the borrower into extreme financial fragility, making it exceedingly difficult to qualify for a residential mortgage, save for retirement, or absorb unexpected economic shocks, as most mortgage lenders adhere to a strict 36% to 43% cap on total recurring debt-to-income (DTI) ratios across all liabilities 3238.

To operationalize this strategy, a prospective student must research the median entry-level salary for their intended geographic region and specific profession. The resulting figure becomes their absolute borrowing ceiling. The following table models the relationship between projected starting salaries, the recommended 10% maximum gross monthly payment budget, and the corresponding maximum sustainable debt load under a 10-year and 15-year repayment horizon. These calculations assume a projected 6.52% fixed interest rate, which aligns with the forecasted federal undergraduate rates for the 2026-2027 academic year driven by the Treasury auction yields 1730312122.

Maximum Sustainable Borrowing Matrix (Projected 6.52% Interest Rate)

| Projected Starting Annual Salary | Gross Monthly Income | Recommended Max Monthly Payment (10% of Gross) | Max Total Debt at Graduation (10-Year Term) | Max Total Debt at Graduation (15-Year Term) |

|---|---|---|---|---|

| $40,000 | $3,333 | $333 | ~$29,350 | ~$38,200 |

| $50,000 | $4,166 | $416 | ~$36,650 | ~$47,750 |

| $60,000 | $5,000 | $500 | ~$44,000 | ~$57,350 |

| $70,000 | $5,833 | $583 | ~$51,350 | ~$66,900 |

| $80,000 | $6,666 | $666 | ~$58,700 | ~$76,450 |

| $90,000 | $7,500 | $750 | ~$66,000 | ~$86,050 |

| $100,000 | $8,333 | $833 | ~$73,350 | ~$95,600 |

Methodological Note: The "Maximum Total Student Loan Debt" is reverse-calculated using standard amortization formulas for 120-month and 180-month terms at a 6.52% APR. The table demonstrates that to maintain healthy financial ratios, a graduate earning $50,000 cannot safely sustain a debt load larger than $36,650 on a 10-year horizon. 173218202241

A practical analogy for this financial model is residential home construction. Building a house (a career) on a financial foundation where debt service consumes 30% of your take-home pay is akin to building a heavy structure on shifting sand; the entity will collapse under the slightest external pressure, such as a medical emergency or a temporary loss of employment. By capping payments at 10% of gross income, the borrower ensures the foundation is set on bedrock, leaving 90% of gross income to absorb taxes, housing, sustenance, and wealth generation 321819.

To further assist in this modeling, the CFPB developed tools such as the "Financial Aid Comparison Shopper," designed to help families evaluate multiple aid offers side-by-side 4223. This tool allows borrowers to look past the deceptive "sticker price" of an institution and calculate the true "net price," while cross-referencing vital institutional metrics such as the school's graduation rate and federal student loan default rate 422324.

What Are the Most Dangerous Misconceptions About Student Loan Eligibility and Repayment?

A significant driver of post-graduate borrower regret is the persistence of widespread misconceptions regarding financial aid. These myths often lull students into a false sense of security, encouraging them to take on liabilities that run counter to their long-term economic interests.

Misconception 1: Maximum Eligibility Equals Actual Need

Federal student loans come with annual and lifetime aggregate borrowing limits. For example, a dependent undergraduate may borrow up to $31,000 over their academic career, while an independent undergraduate can access up to $57,500 452547. A pervasive psychological trap occurs when students view these maximum limits as a "recommended" borrowing target.

Financial aid award letters often package the maximum allowable loan amount into the initial aid offer, giving the illusion that the educational institution expects the student to accept the full sum to survive the semester. Treating a maximum aggregate loan limit as a target is akin to treating a credit card's absolute maximum limit as a monthly spending goal - it mathematically guarantees long-term financial distress 4525. Borrowers are never required to accept the full amount offered; they possess the unilateral right to request a lesser amount that corresponds strictly to their net tuition shortfall after grants, scholarships, and existing family savings are applied 25. Overborrowing to fund lifestyle expenses - such as off-campus luxury housing, vehicles, or travel - using student loan refund checks is a primary catalyst for post-graduate regret 25.

Misconception 2: Broad Loan Forgiveness is Inevitable

According to legal and financial analysts, one of the most dangerous beliefs held by modern college students is the assumption that broad student loan forgiveness is virtually guaranteed by future federal legislation 48. This misconception encourages reckless borrowing on the assumption that the debt will eventually be wiped clean by political intervention 48.

The reality of forgiveness programs is heavily restricted and highly conditional. While Public Service Loan Forgiveness (PSLF) exists for government and non-profit workers, it strictly requires 120 certified, on-time payments under an eligible income-driven plan 101226. Broad, unconditional forgiveness schemes have repeatedly faced insurmountable legal challenges and Supreme Court reversals. Furthermore, the OBBBA's introduction of the RAP plan explicitly extends the standard private-sector forgiveness timeline to 360 months (30 years), signaling a clear legislative intent by Congress to collect on debts over a much longer horizon, not to cancel them swiftly 122214.

Misconception 3: Interest Rates Alone Dictate Affordability

Borrowers frequently assume that a massive reduction in interest rates equates to a proportional reduction in monthly payments. This is mathematically false. Because student loans consist of amortized principal and interest, halving an interest rate does not halve the required payment 27.

For instance, dropping an interest rate from 10% to 5% on a standard 10-year term merely alters the ratio of principal to interest within the payment structure; the actual monthly cash obligation only drops by roughly 20% to 25%, not 50%, because the underlying principal must still be retired 27. Similarly, borrowers often falsely assume that federal loan consolidation automatically secures a lower interest rate. In reality, a Federal Direct Consolidation Loan simply calculates the weighted average of the original loan interest rates and rounds up to the nearest one-eighth of a percentage point, preserving the overall cost of the debt rather than reducing it 27. Therefore, focusing solely on securing a low interest rate, while ignoring the absolute volume of principal borrowed, is a structurally flawed financial strategy.

Why Do Private Student Loans Pose Uniquely Severe Consumer Protection Risks?

When federal loan limits are exhausted - or when the new 2026 OBBBA caps on Parent PLUS loans create insurmountable funding gaps - families frequently turn to the private student loan market 2630285253. A fundamental lack of understanding regarding the difference between federal and private debt is a premier source of financial regret 54.

Federal loans and private loans are not interchangeable financial products; they operate in entirely different regulatory universes. Federal student loans are issued by the U.S. government, carry fixed interest rates set annually by Congress, and are generally issued without consideration of a student's credit score or income history 2622272852542956. Conversely, private student loans are issued by commercial banks, credit unions, and financial technology firms 262957. They operate identically to personal unsecured loans. Eligibility, interest rates, and loan terms are strictly underwritten based on the creditworthiness of the borrower and, in roughly 94% of undergraduate cases, require a creditworthy co-signer 27522956.

The critical distinction lies not just in origination, but in the vast disparity of consumer protections.

The Statutory Safety Net of Federal Protections

A federal student loan operates with an inherent, statutory safety net designed to prevent total financial ruin. If a borrower loses their job, they have a legal right to utilize deferment or forbearance to pause payments without penalty 264852542957. If a borrower suffers a catastrophic health event resulting in total and permanent disability (TPD), or if the borrower dies, federal law mandates the complete discharge and cancellation of the remaining federal loan balance, preventing the debt from haunting grieving families 3031. Furthermore, federal loans offer access to income-driven frameworks like the RAP plan, acting as a crucial insurance policy against labor market volatility 262852535429.

The Hidden Risks and Servicing Abuses of Private Credit

A private student loan is functionally equivalent to driving a vehicle without seatbelts or airbags; it serves the purpose of financing education, but offers zero institutional protection in the event of an economic collision 525354. Private lenders are not legally required to offer income-driven repayment plans, Public Service Loan Forgiveness, or generous forbearance periods 26285253542957.

Historically, the CFPB has identified severe, systemic abuses within the private student loan servicing market. For example, CFPB supervisory reports have highlighted failures where private lenders routinely ignored borrowers' legitimate claims of school misconduct or fraud, deceptively denied eligible disability discharges, and instituted predatory billing practices involving unauthorized withdrawals that violated Regulation E 31606162. In high-profile enforcement actions, the CFPB permanently banned major servicers like Navient from federal servicing due to practices that actively steered struggling borrowers into costly consecutive forbearances rather than affordable income-driven plans, racking up billions in unnecessary capitalized interest 60. The CFPB also took action against the National Collegiate Student Loan Trusts for deploying illegal debt collection tactics, including suing borrowers for debts they could not legally prove were owed and filing false affidavits 60.

Perhaps the most terrifying hidden risk of private student loans involves the co-signer. Because the vast majority of young adults lack the credit history to secure private financing, a parent or grandparent must co-sign, assuming equal and absolute legal liability for the debt 262752. The CFPB has repeatedly issued warnings regarding "auto-default" clauses buried in the fine print of private loan contracts. Under these draconian clauses, if the co-signer dies or declares bankruptcy, the private lender possesses the contractual right to immediately accelerate the loan, demanding the entire principal balance be paid in full instantly, even if the student borrower has a perfect record of on-time monthly payments 30326465. While regulatory pressure has forced many major lenders to abandon the most aggressive auto-default clauses, the risk of credit contagion - where a student's inability to pay ruins a parent's retirement credit - remains a stark reality of the private market 6465.

Furthermore, high-earning borrowers are often tempted by private lenders offering slightly lower interest rates than the projected 2026-2027 federal rates 1731212853. To access these nominally lower rates, borrowers refinance their federal loans into the private market. The CFPB explicitly warns that this action is a one-way street 3254316162. Refinancing federal loans into a private product permanently and irrevocably strips the debt of all federal protections, erasing access to the RAP plan, PSLF, and any future legislative relief 32543161.

Bottom Line

To navigate the high-stakes environment of higher education finance and avoid decades of borrower regret, students and families must completely abandon the assumption that all offered financial aid is inherently safe or necessary. Smart borrowing requires applying strict, empirical mathematical constraints to deeply emotional decisions. By treating the projected first-year starting salary as an absolute cap on total lifetime borrowing, families can ensure that monthly payments remain below the critical 10% threshold of gross income, preserving future wealth accumulation. Furthermore, prospective students must factor in the stark realities of the 2026 legislative landscape - recognizing that the new Repayment Assistance Plan (RAP) requires a staggering 30-year commitment for non-public sector forgiveness, and the Tiered Standard Plan forcibly extends fixed payments for up to 25 years. Finally, the paramount rule of educational finance remains absolute: federal student loans, with their statutory safety nets, income-driven protections, and disability discharge rights, must be entirely exhausted before a borrower ever assumes the unmitigated consumer risks of the private credit market.