How to Choose a New Student Loan Plan After SAVE in 2026

The federal student loan SAVE plan officially ends on July 1, 2026, giving the roughly 7.5 million enrolled borrowers exactly 90 days to select a new repayment strategy or face punitive automatic enrollment. To keep your monthly payments tied to your earnings, you will need to transition to either the newly created Repayment Assistance Plan (RAP) or the legacy Income-Based Repayment (IBR) plan. Your best choice will depend heavily on your adjusted gross income, your family size, and whether you are actively pursuing Public Service Loan Forgiveness.

The Collapse of the SAVE Plan and the Rise of the OBBBA

For decades, federal student loan borrowers navigated a dizzying array of income-driven repayment plans, often referred to by experts as an "acronym soup" of overlapping programs 1. In 2023, the Biden-Harris administration attempted to streamline this system by introducing the Saving on a Valuable Education (SAVE) plan, which was designed to be the most generous income-driven option in the history of the federal loan program 234. However, the plan almost immediately faced severe legal headwinds.

A coalition of Republican-led states filed lawsuits arguing that the executive branch had vastly exceeded its statutory authority by creating the SAVE plan without explicit congressional approval 256. By the summer of 2024, the 8th Circuit Court of Appeals issued an injunction that blocked the Department of Education from implementing the plan's forgiveness provisions and lower payment calculations 26. This legal gridlock forced more than seven million borrowers into an indefinite administrative forbearance 256. During this limbo period, no payments were due, but borrowers suffered a major setback: the months spent in forbearance did not count toward Public Service Loan Forgiveness (PSLF) or standard income-driven repayment forgiveness 257. To compound the financial strain, the Trump administration ordered that interest begin accruing on these frozen balances again in August 2025 58.

The final blow to the SAVE plan arrived in late 2025 and early 2026. In December 2025, the Department of Education announced a proposed settlement with the state of Missouri to definitively dismantle the program 5910. On March 10, 2026, a federal appeals court entered the final judgment, officially vacating the rules that created the SAVE plan and ordering the Department of Education to transition all enrolled borrowers into alternative, legal repayment frameworks 9111213.

The Legislative Overhaul: The One Big Beautiful Bill Act

While the courts were dismantling SAVE, Congress was fundamentally rewriting the higher education financing system. On July 4, 2025, President Trump signed the One Big Beautiful Bill Act (OBBBA) into law 38914. The OBBBA is a sweeping piece of budget reconciliation legislation that alters everything from corporate tax codes to federal borrowing limits, but its impact on student loans is particularly profound 151718.

The OBBBA statutorily terminates the SAVE plan and several other legacy repayment programs, effectively replacing the old customizable system with a highly streamlined, two-track framework for new borrowers starting July 1, 2026 1915. Under the new law, future borrowers will only have access to a debt-driven track (the Tiered Standard Plan) or an income-driven track (the Repayment Assistance Plan, or RAP) 13. For existing borrowers caught in the middle of this transition, the law dictates a mandatory migration away from the sunsetting plans and into the surviving options.

The Critical 90-Day Transition Window

If you are one of the millions of borrowers currently parked in the SAVE plan's administrative forbearance, your transition timeline is strictly regulated. The Department of Education has confirmed that starting on or around July 1, 2026, federal loan servicers will begin issuing official notices to all SAVE enrollees 3101316.

Once your specific loan servicer sends this notice, a 90-day countdown begins 101116. During this three-month window, you are required to log into your StudentAid.gov account, evaluate your financial situation, and affirmatively select a new legal repayment plan 101316. For the vast majority of borrowers, this means making a definitive choice before the end of September 2026 11.

The Danger of Inaction and Auto-Enrollment

The most dangerous mistake a borrower can make during this transition is simply ignoring the notices. If you fail to actively transition to a new plan before your 90-day deadline expires, the Department of Education will not default you into a comparable income-driven plan. Instead, your servicer will automatically reassign you to either the traditional 10-year Standard Repayment Plan or the newly created Tiered Standard Plan 310111316.

Because these Standard plans calculate your monthly bill based strictly on the total principal balance you owe and the interest rate of your loans - rather than your ability to pay - borrowers who are auto-enrolled frequently experience sudden, prohibitive spikes in their monthly bills 111617. An auto-enrollment could easily result in a payment that is several hundreds of dollars higher than what you previously paid under SAVE. Furthermore, payments made under the Tiered Standard Plan do not count as qualifying payments for Public Service Loan Forgiveness 171822. To maintain an affordable payment and keep your forgiveness timelines intact, proactive enrollment is mandatory.

Exploring the New Baseline: The Repayment Assistance Plan (RAP)

For borrowers seeking an income-driven option, the centerpiece of the OBBBA legislation is the Repayment Assistance Plan (RAP). Launching on July 1, 2026, RAP is designed to be the government's primary income-driven repayment vehicle moving forward 13910. However, the mathematical mechanics of RAP are a radical departure from the systems borrowers have grown accustomed to over the past decade.

The AGI Percentage Formula

Historically, income-driven plans like SAVE, PAYE, and IBR calculated your monthly bill using a concept called "discretionary income." This meant the government would protect a certain baseline of your earnings (usually 150% to 225% of the federal poverty guideline based on your family size) and only charge you a percentage of the money you earned above that poverty threshold 171920.

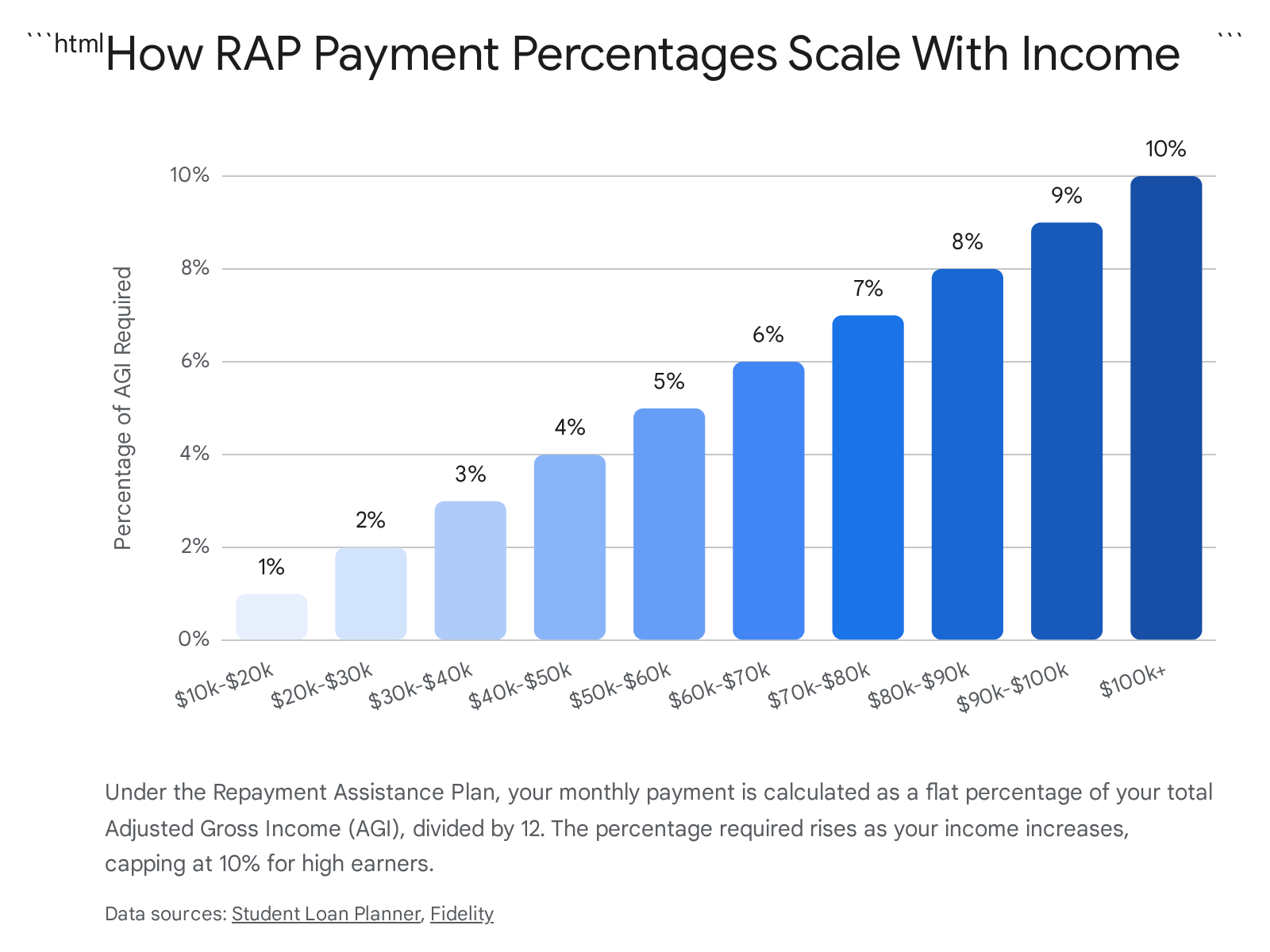

The Repayment Assistance Plan abandons the discretionary income model entirely 1921. Instead, RAP calculates your monthly payment based on a flat percentage of your total Adjusted Gross Income (AGI) 10192122. The program uses a progressive, tiered structure that increases the financial burden as your income grows 192122.

The exact escalating tiers dictate that borrowers earning under $10,000 annually will pay a flat minimum of $10 per month 212223. For borrowers earning between $10,001 and $20,000, the system demands 1% of total AGI 212223. As income rises, the percentage increases linearly: 2% for AGI between $20,001 and $30,000; 3% for AGI between $30,001 and $40,000; 4% for AGI between $40,001 and $50,000; and so forth 2122. This step-up structure continues adding one percentage point for every additional $10,000 in income until it caps at a maximum assessment of 10% of total AGI for anyone earning over $100,000 19212223.

Because RAP calculates against your total AGI rather than a protected discretionary subset, a borrower with a modest income could actually see a higher payment under RAP than they would have under the older legacy plans 21. To mitigate this, RAP includes a family size modifier, but it is relatively rigid: the formula simply subtracts $50 a month from your final calculated bill for every dependent you claim on your federal tax return 1182122.

The Powerful Safeguards: Interest Subsidies and Principal Matches

Despite the strict AGI formula, RAP includes two incredibly powerful structural benefits that make it an attractive option for struggling borrowers.

The first is a comprehensive interest subsidy. Under traditional repayment plans, if your income-driven payment was so low that it did not cover the monthly interest generated by your loan, the unpaid interest would accrue, causing your total balance to balloon over time. RAP stops this negative amortization entirely. If your calculated RAP payment is less than your monthly interest accrual, the Department of Education waives the remaining interest 13102122. Therefore, as long as you make your required monthly RAP payment on time, your total student loan balance will never grow 31022.

The second major benefit is a targeted principal reduction feature. Under RAP, if your monthly payment does not inherently reduce your loan's principal value by at least $50, the government will step in and contribute the difference to ensure your principal shrinks by at least that amount each month 112223. This ensures that even the lowest-earning borrowers making the $10 minimum token payment will see their actual debt burden slowly decrease over time 101122.

The Tradeoff: A 30-Year Forgiveness Horizon

The generous interest and principal protections of RAP come at a significant cost in terms of time. In older income-driven plans, any remaining loan balance was traditionally forgiven after 20 years for undergraduate borrowers, or 25 years for graduate borrowers 815.

The Repayment Assistance Plan extends this timeline considerably. Under RAP, general IDR forgiveness is not granted until a borrower has made 360 qualifying monthly payments - a full 30 years in repayment 111522232425. For a borrower who begins repayment in their mid-twenties, they will be approaching retirement age before they see their remaining balances wiped away.

The Enduring Stability of Income-Based Repayment (IBR)

If the mechanics of RAP do not align with your financial situation, you are not entirely out of options. The Income-Based Repayment (IBR) plan serves as the primary "safe haven" for borrowers fleeing the collapse of the SAVE plan 1815. Because IBR was originally created by a separate act of Congress long before the recent executive actions, it was not struck down by the courts and was deliberately preserved by the OBBBA legislation 6715.

The Return of Discretionary Income

For many borrowers, IBR will be preferable to RAP because it retains the traditional "discretionary income" calculation model. Rather than taking a flat percentage of your entire AGI, IBR protects a significant portion of your earnings. The formula takes your AGI and subtracts 150% of the federal poverty guideline for your specific family size and state of residence 1920.

You are only billed a percentage on the remaining, unprotected income. There are two distinct versions of IBR, and your assignment depends entirely on when you took out your very first federal student loan: * New IBR: If you were a new borrower on or after July 1, 2014, your payment is capped at 10% of your discretionary income. Any remaining balance on your loan is forgiven after 20 years 81920. * Old IBR: If you borrowed your first loan before July 1, 2014, your payment is set at 15% of your discretionary income. Any remaining balance is forgiven after 25 years 81920.

Crucially, the OBBBA legislation actually made IBR easier to access. In previous years, borrowers could only enroll in IBR if they could prove a "partial financial hardship," meaning their overall debt load was high relative to their income 19153026. The OBBBA permanently eliminated this requirement, throwing the doors open for any borrower with pre-July 2026 loans to use IBR as their primary repayment vehicle 1153026.

The Ultimate Protection: The IBR Payment Cap

The single most important feature of the IBR plan - and the main reason high-earning professionals should consider it over RAP - is its strict payment cap 41920.

Under the Repayment Assistance Plan, there is no upper limit on what you might owe. If your income skyrockets, the RAP formula will continue to demand 10% of your AGI, which could easily result in astronomical monthly payments 41923.

IBR contains a statutory safety valve: your monthly payment will never be higher than what you would have paid under a standard, fixed 10-year repayment plan calculated at the time you entered the IBR program 41920. If you achieve tremendous financial success and your income scales up, your IBR payment will simply hit the 10-year standard ceiling and stop rising, ensuring your federal loan payments remain predictable and manageable regardless of your wealth 41920.

Comparing Your Income-Driven Options

Choosing between the Repayment Assistance Plan and Income-Based Repayment is a complex math problem that hinges on your current income, your future earning potential, and the size of your family.

Side-by-Side Comparison of 2026 Repayment Options

| Feature | Repayment Assistance Plan (RAP) | Income-Based Repayment (IBR) | Tiered Standard Plan |

|---|---|---|---|

| Launch/Availability | July 1, 2026 310 | Available now 720 | July 1, 2026 310 |

| Payment Formula | 1% to 10% of total AGI (Min $10) 2122 | 10% or 15% of discretionary income 1920 | Fixed monthly amount based on balance 317 |

| Upper Payment Cap | None. Payments rise endlessly with income 41923 | Capped at the 10-year Standard amount 41920 | Payments are permanently fixed 31724 |

| Interest Subsidy | Yes. 100% waiver of unpaid interest 132122 | Limited. Subsidized only for the first 3 years 18 | None 17 |

| Forgiveness Timeline | 30 years (360 payments) 11222425 | 20 years (New) or 25 years (Old) 81520 | No forgiveness available 1517 |

| PSLF Eligibility | Yes. Fully qualifies for PSLF 18192733 | Yes. Fully qualifies for PSLF 192034 | No. Does not qualify for PSLF 171822 |

| Family Deduction | $50 off monthly bill per dependent 12122 | Shelters 150% of the federal poverty line 1920 | None 17 |

When assessing these options, financial experts generally advise that RAP makes the most sense for borrowers with highly volatile or consistently low incomes. Because RAP charges a fraction of a percent at the lowest income brackets (e.g., 1% or 2% for those earning under $30,000), a lower-middle-class earner will likely secure a cheaper monthly bill under RAP than under the 10% or 15% discretionary calculation of IBR 192122. Furthermore, for borrowers whose debt is so massive that they will never touch the principal, RAP's total interest waiver prevents the psychological and financial devastation of a continuously ballooning balance 32223.

Conversely, IBR is the superior choice for high-income professionals and borrowers with large families. The 150% poverty line exclusion inherent in IBR provides a massive deduction for large households, shielding a vast swath of their income from the repayment calculation 19. More importantly, high earners - such as doctors or lawyers whose incomes will likely surge mid-career - must rely on IBR to access the 10-year standard payment cap 419. Choosing RAP as a high earner means exposing yourself to an uncapped 10% assessment on a six-figure salary 41923. Furthermore, IBR offers a direct path to total loan forgiveness a full five to ten years faster than RAP 15.

Borrowers must choose carefully, as transitioning between plans later carries risks. The Department of Education has clarified that while prior payments in legacy IDR plans will count toward the 30-year RAP forgiveness timeline, payments made while enrolled in the new RAP plan will not retroactively count toward the 20- or 25-year forgiveness clocks of IBR if you decide to switch back 434.

Sunsetting Plans: What Happens to PAYE and ICR?

During this transition, you may notice that the Pay As You Earn (PAYE) and Income-Contingent Repayment (ICR) plans still exist in the federal portal. The OBBBA legislation dictates that these plans are formally sunsetting 671524.

If you are already enrolled in PAYE or ICR, or if you apply to enter them immediately, you are permitted to utilize them for a brief grace period. However, both PAYE and ICR will permanently close on July 1, 2028 67824. On that deadline, the Department of Education will systematically force any remaining enrollees to migrate into either IBR or RAP 724. For most borrowers exiting the SAVE plan in 2026, jumping into a repayment plan that is guaranteed to be dismantled in exactly two years is an unnecessary administrative hurdle. It is strategically wiser to evaluate RAP and IBR as your permanent financial homes today.

Non-Income-Driven Alternatives: The Tiered Standard Plan

Not every borrower desires an income-driven repayment strategy. If you earn a substantial salary relative to your debt and simply want a predictable timeline to become completely debt-free without the hassle of submitting your tax returns for annual income recertifications, the OBBBA has provided a new vehicle: the Tiered Standard Plan 31017.

Available beginning July 1, 2026, the Tiered Standard Plan entirely ignores your income and ability to pay 17. Instead, it functions like a traditional mortgage or auto loan, offering fixed monthly payments over a set duration. The length of your repayment term is dictated exclusively by the total outstanding principal balance of your federal loans at the moment you enter the plan 1718.

The Department of Education has established four rigid tiers: * Balances less than $25,000: The loan is amortized over a 10-year repayment term 1718. * Balances of $25,000 to $49,999: The loan is amortized over a 15-year repayment term 1718. * Balances of $50,000 to $99,999: The loan is amortized over a 20-year repayment term 1718. * Balances of $100,000 or more: The loan is amortized over a 25-year repayment term 1718.

The primary benefit of the Tiered Standard Plan is extreme predictability. You lock in a fixed monthly payment and know exactly the month and year you will be debt-free. The downside is strict inflexibility. The plan offers zero loan forgiveness, and if you lose your job or experience a medical emergency, your fixed monthly bill remains due in full 1517.

Public Service Loan Forgiveness (PSLF) in the New Era

For teachers, nurses, government workers, and employees of qualifying non-profit organizations, the chaotic collapse of the SAVE plan has caused immense anxiety. However, the core statutory framework of the Public Service Loan Forgiveness (PSLF) program survived the legal battles and the OBBBA legislation entirely intact 61522. You still need to accumulate 120 qualifying monthly payments while working full-time for an eligible public service employer to achieve complete, tax-free debt cancellation 221928.

Both the new Repayment Assistance Plan (RAP) and the legacy Income-Based Repayment (IBR) plan are fully authorized qualifying repayment programs for PSLF 1819273334.

The mathematical strategy for public servants is straightforward: you must select the plan that generates the absolute lowest legal monthly payment. Because the federal government will wipe out your remaining principal balance entirely after exactly 10 years of service, your sole financial objective is to pay as little out of pocket as possible while the 120-month clock ticks 1934. * If your public sector salary is relatively low, RAP's low-percentage tiers (e.g., 2% to 4% of AGI) will likely calculate the cheapest monthly bill, minimizing your out-of-pocket costs before the 10-year forgiveness trigger 19. * If your income is higher (e.g., a highly paid physician at a non-profit hospital), IBR is essential. IBR's 10-year standard payment cap will shield you from RAP's uncapped 10% AGI assessment, ensuring your payments do not skyrocket in the final years of your public service 19.

A Crucial Warning for PSLF Borrowers: You must be hyper-vigilant during the 90-day transition window in late 2026. If you miss your servicer's deadline and are auto-enrolled into the new Tiered Standard Plan, your progress toward PSLF will immediately halt. The Department of Education has explicitly stated that payments made under the Tiered Standard Plan do not qualify for Public Service Loan Forgiveness 171822. You must proactively execute a transition into RAP or IBR to keep your 120-month tracker moving.

Navigating the PSLF Buyback Changes

Many public servants spent late 2024 and 2025 trapped in the SAVE administrative forbearance, watching helplessly as months of potential PSLF credit slipped away 25. The Department of Education offers a "PSLF Buyback" program that theoretically allows borrowers to retroactively purchase those lost months by making a lump-sum payment 222.

If you are planning to utilize this buyback option, you must brace for sticker shock. In March 2026, the Department of Education quietly revised the algorithmic formula used to calculate PSLF buyback payments for any non-qualifying months occurring on or after July 1, 2024 22. Previously, the buyback amount for those months would have been calculated using the highly subsidized SAVE formula. Under the revised 2026 rules, the government will demand a significantly higher premium, making it vastly more expensive to recapture the time lost to the administrative forbearance 22.

Hidden Traps: Tax Bombs and Future Borrowing Limits

As you finalize your repayment strategy, you must look beyond the monthly premium and consider the long-term macroeconomic traps hidden within the tax code and the broader OBBBA legislation.

The Return of the IDR "Tax Bomb"

During the pandemic era, the American Rescue Plan Act instituted a temporary tax holiday, ensuring that any student loan debt forgiven by the federal government was entirely excluded from federal gross income 151926.

That tax holiday has ended. The exemption officially expired on December 31, 2025 151926. Moving forward, if you reach the 20-, 25-, or 30-year finish line under standard income-driven repayment (IBR or RAP), the IRS will treat the entire forgiven loan balance as taxable ordinary income in the year it is discharged 5131519. This can result in a devastating "tax bomb," where a borrower suddenly owes the IRS tens of thousands of dollars.

You must factor this future tax liability into your financial planning if you intend to carry a balance to the 20- or 30-year mark. (Note: This tax liability does not apply to Public Service Loan Forgiveness. PSLF discharges remain permanently exempt from federal income tax 6221934).

Restrictions on Future Borrowing and Parent PLUS Loans

If you or your family members plan to take out new federal loans to finance further education, the OBBBA fundamentally altered the borrowing landscape.

The legislation entirely eliminates the Graduate PLUS loan program for any new borrowers starting July 1, 2026 14243029. Graduate and professional students will now be strictly capped at borrowing $20,500 per year (with an aggregate lifetime limit of $100,000) for standard master's degrees, forcing many to rely on more expensive private student loans to cover tuition shortfalls 153029.

Parent PLUS loans, utilized by parents to finance their children's undergraduate education, survived but face severe new restrictions. The OBBBA caps Parent PLUS borrowing at $20,000 per year per dependent student 153029. More importantly, any Parent PLUS loan disbursed on or after July 1, 2026, is explicitly banned from accessing the Repayment Assistance Plan (RAP) or any other income-driven option, permanently severing future parent borrowers from the PSLF program 243030.

What Should You Do Right Now?

You do not have to wait passively for your servicer's 90-day notice to arrive on July 1, 2026. Taking immediate action could save you months of lost forgiveness credit.

If your primary goal is to achieve loan forgiveness - either through PSLF or standard IDR timelines - every single month you remain parked in the SAVE administrative forbearance is a month you are permanently losing toward your 120, 240, or 360 required payments 257. Furthermore, interest is actively accruing on your balance 58. You are legally permitted to apply to switch your loans into the Income-Based Repayment (IBR) plan today, which will immediately pull you out of forbearance, restore you to active repayment status, and restart your forgiveness clock 711.

However, if you have run the math and believe the incoming Repayment Assistance Plan (RAP) will offer a significantly lower monthly payment than IBR, you cannot access that program yet. RAP does not officially exist until July 1, 2026 71011. In this specific scenario, you must remain in the SAVE forbearance, absorbing the interest accrual and the lost time, until the RAP application portal opens this summer.

Bottom line

The total legal collapse of the SAVE plan and the subsequent passage of the One Big Beautiful Bill Act will force 7.5 million federal student loan borrowers to make a critical financial decision in the summer of 2026. To avoid the punitive costs of automatic enrollment into a fixed Standard plan, borrowers must proactively transition into either the Repayment Assistance Plan (RAP) or Income-Based Repayment (IBR) within 90 days of receiving their servicer's notice. Lower-income borrowers and those suffering from runaway interest will likely find salvation in RAP's 100% interest subsidies and low starting percentages, while high-earning professionals and large families must rely on IBR's protective payment caps and faster forgiveness timelines. If you are a public servant, it is vital that you carefully choose one of these two income-driven options, as falling into the new Tiered Standard Plan will permanently disqualify your future payments from the PSLF program.