Which Student Loan Plan Should You Pick in 2026

In 2026, the federal student loan landscape has been completely restructured, requiring most borrowers to actively choose between the new Repayment Assistance Plan (RAP), the surviving Income-Based Repayment (IBR) plan, or the new Tiered Standard Plan. RAP offers low minimum payments and unparalleled protection against growing balances for moderate earners, while IBR provides strict payment caps and a faster forgiveness timeline that heavily favors high-income professionals. Borrowers must urgently evaluate their income trajectory, family size, and original loan dates to avoid being auto-enrolled into expensive fixed-payment plans before the looming transition deadlines.

What Happened to the SAVE Plan in 2026?

Federal student loan repayment has undergone its most dramatic transformation in a generation, primarily driven by the passage of the One Big Beautiful Bill Act (OBBBA), also known as the Working Families Tax Cuts Act, which was signed into law on July 4, 2025 123. This legislation sought to drastically simplify the complex and heavily litigated web of income-driven repayment options, ultimately leading to the demise of the Saving on a Valuable Education (SAVE) plan.

The SAVE plan, which was designed to offer generous interest subsidies and artificially low monthly payments, faced intense legal scrutiny from its inception 45. For over a year, the plan was tangled in a complex web of lawsuits and injunctions across multiple state coalitions 56. The turning point occurred in December 2025, when the Department of Education proposed a settlement to wind down the SAVE plan 78. Although a lower court briefly dismissed the case as moot in February 2026, the Eighth Circuit Court of Appeals intervened on March 9, 2026, overruling the lower court and effectively demanding the termination of the program 78. On March 10, 2026, the SAVE plan was officially vacated and permanently dismantled 1910.

This abrupt legal conclusion left approximately 7.5 million borrowers stranded in administrative forbearance, a status where no interest accrued, but crucially, no progress was made toward loan forgiveness 4611. In response, the Department of Education announced a massive transition protocol. Starting July 1, 2026, federal loan servicers will begin issuing formal notices to all former SAVE borrowers 1411. Upon receiving this notice, borrowers are placed on a strict 90-day clock to select a new, legally compliant repayment plan 1411. Borrowers who fail to proactively choose a plan within this 90-day window will be automatically enrolled into the standard 10-year repayment plan or the newly created Tiered Standard Plan 1911. Because these standard plans do not factor in income, passive borrowers risk being blindsided by shockingly high monthly payments.

How Does the Repayment Assistance Plan (RAP) Work?

Scheduled to launch on July 1, 2026, the Repayment Assistance Plan (RAP) is the cornerstone of the government's new approach to student debt 1212. It serves as the default income-driven plan for all new borrowers and offers a completely novel mathematical formula for calculating monthly obligations, managing interest accrual, and reducing principal balances.

Calculating Payments on a Tiered Scale

Unlike legacy income-driven plans that rely on "discretionary income" - a metric that shields a portion of your earnings based on the federal poverty line - RAP calculates payments as a direct, tiered percentage of your total Adjusted Gross Income (AGI) 111213. This is a fundamental shift in how affordability is determined.

The RAP formula operates on a progressive sliding scale across eleven distinct income brackets. For borrowers with an AGI of $10,000 or less, the plan requires a flat minimum payment of $120 annually, which breaks down to exactly $10 per month 1214. For those earning between $10,001 and $20,000, the payment is set at 1% of their AGI 1214. The percentage then increases by exactly 1% for every additional $10,000 in income. For example, an AGI between $20,001 and $30,000 requires a 2% payment, while an AGI between $30,001 and $40,000 requires 3% 1415. This progression continues until it reaches a maximum threshold of 10% for any borrower with an AGI exceeding $100,000 121416.

To provide relief for families, RAP allows borrowers to deduct exactly $50 per month from their calculated payment for each dependent child 121314. However, this benefit comes with a strict caveat: the dependent must be officially claimed on the borrower's federal tax return 17.

Crucially, RAP implements a mandatory $10 minimum monthly payment for all participants, permanently eliminating the $0 monthly payments that millions of low-income borrowers relied upon under the defunct SAVE and legacy IBR plans 11213. Furthermore, RAP features no maximum payment cap 1820. For high-earning professionals, this means monthly payments will scale infinitely alongside their salary, potentially resulting in obligations that far exceed what they would have owed under a traditional fixed mortgage-style repayment plan.

Interest Waivers and Principal Matching

To counter the widespread crisis of negative amortization - a scenario where monthly payments are too small to cover accruing interest, causing the total loan balance to balloon over time - RAP introduces two highly robust protective mechanisms.

The first mechanism is a comprehensive interest subsidy. If a borrower's calculated RAP payment is insufficient to cover the newly accrued monthly interest, the Department of Education completely waives the remaining unpaid interest 121719. Consequently, a borrower's loan balance mathematically cannot increase while enrolled in RAP, provided all monthly payments are made on time 17.

The second mechanism is an unprecedented principal matching benefit. The 2026 legislation guarantees that every on-time monthly payment will reduce the borrower's principal balance by a minimum of $50 141719. If a borrower's required payment is low - for example, the $10 minimum - and chip away less than $50 from the principal after covering interest, the government will step in and contribute the difference to ensure a full $50 reduction occurs 121617. This ensures that even the lowest-income borrowers make steady, predictable progress toward debt elimination.

The 30-Year Forgiveness Timeline

The primary strategic drawback of RAP is its extended timeline to debt forgiveness. Under prior plans, undergraduate loans were typically forgiven after 20 years, and graduate loans after 25 years. RAP mandates 360 qualifying monthly payments - equivalent to exactly 30 years - before any remaining balance is forgiven 121417.

This extended timeline significantly alters the lifetime cost calculus for borrowers. A lower monthly payment under RAP may result in paying substantially more total dollars over three decades compared to a higher monthly payment on a shorter 20-year plan 1317. Furthermore, existing borrowers who decide to switch into RAP must be incredibly cautious; entering the plan will subject their remaining balance to the new 30-year threshold, effectively extending the time they remain tied to their debt 1517.

Why IBR Survives as the Legacy Option

Income-Based Repayment (IBR) is the sole legacy income-driven plan to survive the 2026 statutory overhaul 13. It remains permanently available, but only to borrowers whose federal Direct Loans were originally disbursed before July 1, 2026 117. For moderate-to-high earners, preserving access to IBR is arguably the most critical financial strategy in the current landscape.

The Advantage of Discretionary Income

The fundamental advantage of IBR lies in its calculation methodology. Rather than taxing a borrower's total AGI like RAP, IBR bases its payments strictly on "discretionary income." Discretionary income is mathematically defined as the borrower's AGI minus 150% of the federal poverty guideline for their specific family size and geographic location 1720.

Because this 150% buffer actively shields a significant baseline portion of a borrower's income from the calculation, IBR frequently produces lower monthly payments than RAP for individuals earning roughly $80,000 or more 1720. The plan comes in two distinct versions based on when a borrower first took out loans. "New IBR," which applies to borrowers whose oldest loan dates on or after July 1, 2014, sets payments at 10% of discretionary income 1117. "Old IBR," which applies to those with loans predating July 2014, sets payments at 15% of discretionary income 1117.

Crucially, IBR includes a strict statutory payment cap: a borrower's monthly bill will never exceed the amount they would have paid under the standard 10-year repayment plan based on their balance when they entered the program 1720. Even if a borrower's income skyrockets to half a million dollars a year, their IBR payment hits a rigid ceiling, protecting their wealth accumulation. RAP offers no such protection.

Shorter Forgiveness Timelines

In stark contrast to RAP's grueling 30-year requirement, IBR maintains highly favorable forgiveness timelines. Borrowers on the New IBR track achieve full loan forgiveness after 20 years, equivalent to 240 qualifying payments 1417. Those on the Old IBR track reach forgiveness after 25 years, or 300 qualifying payments 1417.

For a borrower who has already accumulated a decade of payment history under a defunct plan like SAVE, transitioning to RAP would mean resetting their finish line to a 30-year mark. Staying in, or switching to, IBR ensures that their existing progress remains mapped to a 20- or 25-year timeline, allowing for significantly faster debt cancellation and a quicker return to total financial independence 1017.

The Negative Amortization Risk

The primary hazard associated with IBR is its lack of a comprehensive interest subsidy. Under IBR, the government only covers unpaid interest on subsidized loans for the first three consecutive years of repayment 17. After that period expires - or immediately for all unsubsidized loans - any interest not fully covered by the borrower's monthly payment is added directly to the total loan balance 17.

For borrowers with massive debt-to-income ratios, such as medical residents or public defenders, an IBR payment might calculate out to $0 or $50 a month, while several hundred dollars in interest accrue simultaneously. Over the course of 20 years, it is common for the total loan balance to double or even triple. While this massively inflated balance is eventually forgiven at the end of the term, it carries severe implications regarding potential federal tax liabilities, which will be discussed later in this report.

RAP vs IBR: Which Income-Driven Plan is Better?

Choosing between RAP and IBR is rarely a matter of preference; it is a rigid mathematical optimization problem based on income level, household size, and career trajectory.

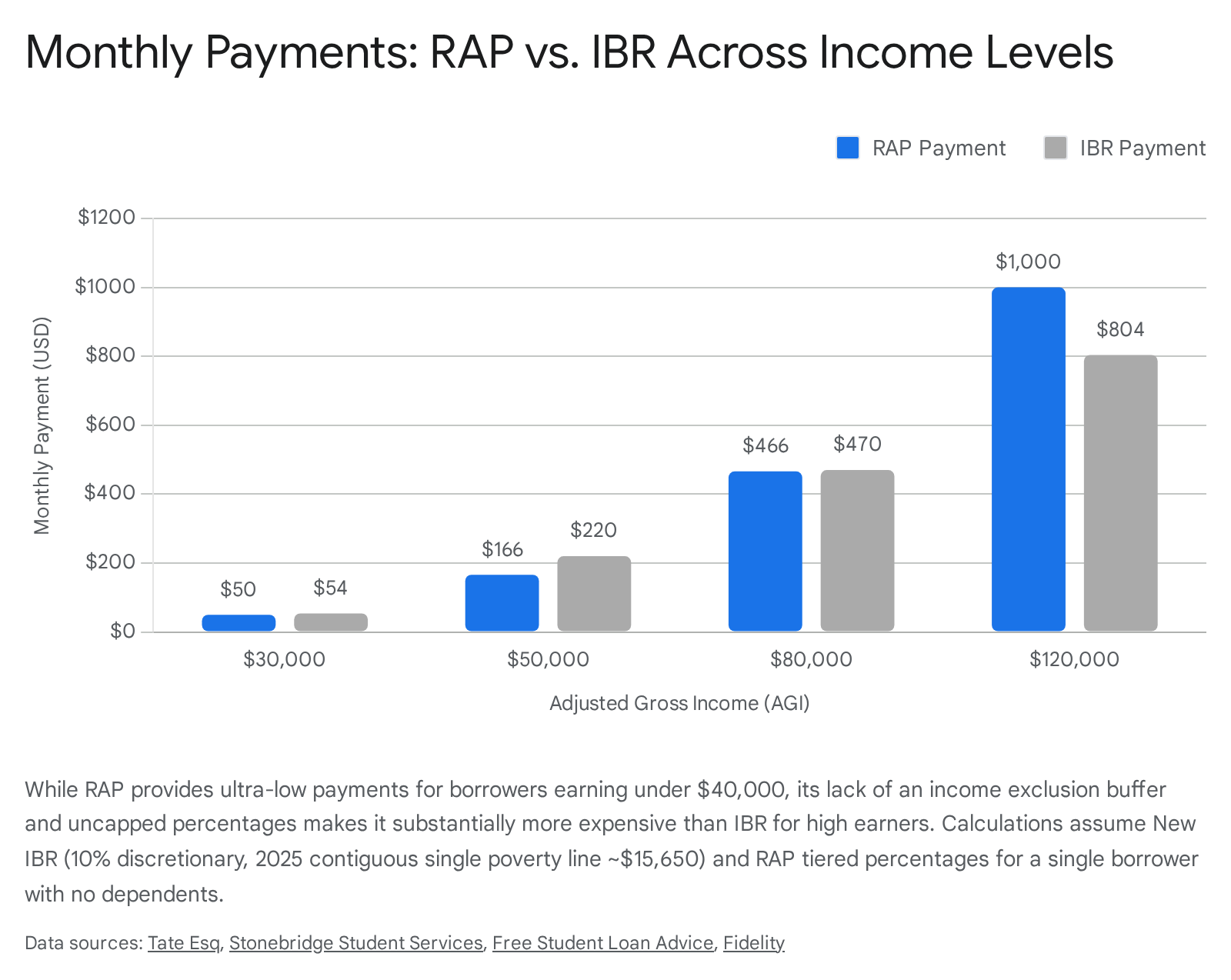

For individuals earning under the $80,000 threshold, RAP frequently emerges as the superior option for immediate cash flow management 17. Because RAP's progressive brackets start at a mere 1% to 3% for lower incomes, the resulting monthly payment is often cheaper than IBR's flat 10% or 15% rate, even after accounting for IBR's poverty guideline buffer 2020. Furthermore, low earners benefit immensely from RAP's absolute assurance that their loan balance will not grow, providing psychological and financial relief from compounding debt 1720.

However, the math aggressively flips in favor of IBR for borrowers with incomes crossing the $90,000 to $100,000 threshold 17. For a mid-career professional earning $120,000, RAP's uncapped 10% rate on total AGI results in substantial monthly obligations. Under IBR, that same high earner benefits from the poverty line deduction and, more importantly, the strict 10-year standard payment cap 172020.

Nuances for Gig Workers and Complex Tax Filers

The choice between plans becomes highly nuanced for freelancers, gig economy workers, and independent contractors whose incomes fluctuate. Variable gig income severely complicates the annual income recertification process 21. Because RAP utilizes straight AGI, independent workers must coordinate carefully with tax professionals to maximize adjustments. Leveraging Qualified Business Income (QBI) deductions and maximizing contributions to health savings accounts or tax-deferred retirement plans become essential strategies to artificially suppress AGI, thereby lowering the RAP payment 1221.

Furthermore, IBR relies on a much broader definition of "family size" than RAP. Under RAP, borrowers can only claim a $50 deduction for dependents explicitly claimed on their federal tax returns 17. IBR, however, permits borrowers to count any individual - including domestic partners, elderly parents, or extended relatives living in the household - who receives more than half of their financial support from the borrower, regardless of tax filing status 17. For multi-generational households, this expanded definition under IBR can drastically increase the poverty line deduction, resulting in vastly lower monthly payments 17.

Head-to-Head Comparison of Income-Driven Options

The table below summarizes the critical structural differences between the two primary income-driven options available to existing borrowers.

| Feature | Repayment Assistance Plan (RAP) | Income-Based Repayment (IBR) |

|---|---|---|

| Availability | All loans (Default IDR for new loans) | Only loans disbursed before July 1, 2026 |

| Payment Formula | Direct tiered % of AGI (1% to 10%) | 10% or 15% of Discretionary Income |

| Minimum Payment | $10 / month (No $0 payments allowed) | $0 / month (If income falls below threshold) |

| Maximum Payment Cap | None (Payments scale infinitely with high income) | Capped strictly at the 10-year Standard amount |

| Forgiveness Timeline | 30 Years (360 payments) | 20 Years (New IBR) or 25 Years (Old IBR) |

| Interest Subsidy | Full waiver of unpaid monthly interest | Limited (3 years on subsidized loans only) |

| Family Size Definition | Narrow (Only dependents claimed on tax return) | Broad (Anyone receiving >50% financial support) |

Data compiled from Department of Education 2026 policy guidance 1121417.

Does the Tiered Standard Plan Make Sense for You?

For borrowers who prefer absolute predictability over income-driven flexibility, the 2026 legislation replaced the traditional, rigid 10-year Standard plan with the new Tiered Standard Repayment Plan 1922. This plan acts as the default destination for new borrowers who do not actively select an income-driven option, and it operates on an entirely different premise than RAP or IBR.

Fixed Payments Based on Total Balance

The Tiered Standard Plan completely ignores the borrower's income. It does not require annual income recertification, and payments will not increase if a borrower receives a raise or promotion. Instead, the plan offers a fixed monthly payment calculated solely based on the total outstanding principal balance and the interest rate at the exact moment the borrower enters repayment 122.

Historically, forcing large student loan balances into a strict 10-year window resulted in astronomical monthly payments and widespread defaults 19. To rectify this, the Tiered Standard Plan utilizes a sliding scale to automatically adjust the length of the repayment term based on the severity of the debt: * Balances under $25,000: Repaid over a 10-year term 22. * Balances between $25,000 and $49,999: Repaid over a 15-year term 22. * Balances between $50,000 and $99,999: Repaid over a 20-year term 22. * Balances of $100,000 or more: Repaid over a 25-year term 22.

The absolute minimum payment permitted under this plan is $50 per month, or the remaining balance if it falls below $50 22.

The Strategy Behind Fixed Repayment

Because it is not an income-driven plan, the Tiered Standard Plan offers no pathway to standard loan forgiveness 1. The expectation is that the borrower will pay back every cent of principal and interest owed.

However, this plan is mathematically engineered to cost significantly less in total lifetime interest than an income-driven plan. Because payments are designed to steadily and aggressively amortize the principal balance to zero by the end of the specified term, the loan does not languish for decades accumulating interest 1. The Tiered Standard Plan is the optimal choice for high-earning professionals with moderate debt who wish to aggressively pay down their principal, avoid the administrative hassle of annual income recertification, and prevent their high salaries from dictating an exorbitant monthly payment under RAP's uncapped formula.

How Do These Changes Affect Public Service Loan Forgiveness (PSLF)?

The Public Service Loan Forgiveness (PSLF) program, which forgives the remaining loan balance for eligible government and non-profit workers after 120 qualifying monthly payments, remains fully intact under the 2026 legislative framework 1220.

Because both RAP and IBR are legally qualifying repayment plans for PSLF, the strategic objective for public servants is singular: select the plan that yields the lowest legally permissible monthly payment over the 10-year duration 120. In the context of PSLF, every dollar paid to the servicer is a dollar that could have been forgiven tax-free by the government 120.

Navigating PSLF Strategy in 2026

For many early-career public servants, such as teachers or entry-level social workers, RAP will initially present the cheapest option due to its low 1% to 3% percentage tiers at the bottom of the income spectrum 20. However, as public sector salaries naturally rise with promotions and tenure, the calculus inevitably flips.

Consider a government attorney or a physician completing a residency at a non-profit hospital. Once their salary crosses the $100,000 mark, RAP becomes highly punitive, stripping away the poverty line buffer and taxing the upper income heavily without any cap 2020. By contrast, IBR shields a baseline amount of income and caps out completely at the 10-year standard amount 2020. This statutory cap protects the borrower from making excessive, wealth-draining payments in their final, highest-earning years just before reaching the 120-payment forgiveness mark.

Switching Plans Without Losing Payment Counts

A pervasive fear among borrowers is that migrating from an expiring plan, such as SAVE or PAYE, to a new plan like RAP or IBR will reset their PSLF progress clock back to zero. The Department of Education has clarified that this is false.

Qualifying payments "cross-pollinate" between recognized income-driven plans 14. A borrower who made 60 qualifying payments under the defunct SAVE plan, transitioned to PAYE for 24 months, and then switches to RAP in 2026 will retain 84 combined qualifying payments toward their 120-payment PSLF goal 101720. Prior qualifying months carry over seamlessly during plan changes 11. The only administrative action that fundamentally resets IDR or PSLF counts to zero is executing a new Direct Consolidation Loan without a specific historical waiver in place 14.

What Are the Rules for New vs. Existing Borrowers?

The 2026 regulations aggressively stratify the borrower population based on the exact origination date of their debt. The legislation draws a hard, inflexible line in the sand on July 1, 2026, creating two distinct classes of federal student loan borrowers with entirely different rights, options, and limitations.

The July 1, 2026 Cutoff

Borrowers are legally classified as "New Borrowers" if their first federal student loan is disbursed on or after July 1, 2026. This classification also applies to individuals who previously paid off all historical federal loans and decide to take out a new one after this date 123.

New Borrowers are permanently locked out of all legacy repayment options. They cannot access IBR, PAYE, ICR, or the traditional 10-year Standard, Graduated, or Extended plans 12224. Instead, their choices are strictly binary: they must choose between the Repayment Assistance Plan (RAP) or the new Tiered Standard Plan 2225.

"Active Borrowers," defined as those with outstanding loans disbursed prior to July 1, 2026, are grandfathered into legacy access. They may utilize IBR indefinitely 123. Furthermore, they may continue to utilize PAYE and ICR until those plans officially sunset and close permanently on July 1, 2028 111.

However, existing borrowers must exercise extreme caution regarding loan consolidation. If an existing borrower decides to consolidate their legacy loans on or after July 1, 2026, the newly generated Direct Consolidation Loan is legally treated as a "new loan." This action instantly strips the borrower of their grandfathered legacy IBR access, forcing the entire consolidated balance permanently into RAP or the Tiered Standard Plan 21113.

Drastic Cuts to Parent PLUS and Graduate Loans

Beyond repayment plans, the One Big Beautiful Bill Act severely restricts federal lending to parents and graduate students - the two demographics that have historically driven the highest balances and default rates in the federal portfolio.

For graduate students, the Grad PLUS loan program, which previously allowed students to borrow up to the full, unlimited cost of attendance to cover living expenses, is entirely eliminated for new borrowers effective July 1, 2026 32326. Moving forward, graduate students are restricted to strict annual borrowing caps: $20,500 per year for standard graduate degrees (capped at $100,000 lifetime), and $50,000 per year for professional degrees such as medicine or law (capped at $200,000 lifetime) 327.

Parent PLUS borrowers face similarly aggressive contraction. Parents are now legally capped at borrowing a maximum of $20,000 per year per child, with a hard lifetime maximum of $65,000 32829. Crucially, any Parent PLUS loans issued after July 1, 2026, are explicitly barred from utilizing RAP or any other income-driven repayment plan 141628. These new parent loans must be repaid strictly through the rigid Tiered Standard Plan, effectively closing the notorious "Double Consolidation" loophole that previously allowed parents to access IDR flexibility 141628.

For parents holding existing Parent PLUS loans, an urgent deadline approaches. To maintain any access to income-driven repayment and potential forgiveness, parents must fully consolidate their existing PLUS loans into a Direct Consolidation Loan before June 30, 2026 1728. Completing this precise administrative step allows them to access the ICR plan before it officially sunsets, preserving their only available pathway to affordable payments.

Are Forgiven Student Loans Taxable in 2026?

When modeling long-term repayment strategies, borrowers must account for federal tax liabilities, which have fundamentally shifted in 2026.

During the pandemic recovery, the American Rescue Plan Act of 2021 temporarily exempted all student loan forgiveness from federal income tax 2025. However, this critical exemption expired on December 31, 2025, and was not renewed by Congress 2025. Under current 2026 tax law, any balance forgiven under RAP or IBR at the end of their respective 30-, 20-, or 25-year terms is treated by the IRS as ordinary taxable income 25.

For example, if a borrower reaches the end of an IBR term and the government forgives $150,000 in accumulated debt, the IRS will tax that amount as if the borrower earned an additional $150,000 in salary that specific year, creating a massive, immediate "tax bomb."

This reality drastically alters the mathematical comparison between RAP and IBR. RAP's primary virtue - the absolute prevention of negative amortization via its aggressive interest waiver - guarantees that the final forgiven balance will be substantially smaller than an IBR balance that has been allowed to grow unchecked for decades 17. For a private-sector borrower certain to carry debt until terminal forgiveness, RAP's mathematically smaller forgiven balance equates to a proportionally smaller tax bomb, potentially saving the borrower tens of thousands of dollars in IRS liabilities in the final year of the loan 1720.

It is vital to note that this tax liability only applies to standard IDR forgiveness. Balances forgiven under the Public Service Loan Forgiveness (PSLF) program remain statutorily tax-free at the federal level and are completely unaffected by the expiration of the 2021 tax exemptions 2025.

Bottom line

The judicial termination of the SAVE plan and the legislative overhaul of 2026 dictate that federal student loan borrowers must actively secure a new repayment strategy. Income-Based Repayment (IBR) remains the gold standard for high earners and public servants seeking rapid, capped forgiveness, provided their loans were disbursed before July 1, 2026. Conversely, the new Repayment Assistance Plan (RAP) offers unmatched interest protection and ultra-low payments for moderate earners, though it traps borrowers in an exhausting 30-year repayment lifecycle. Borrowers who fail to explicitly model their income and choose between these paths risk defaulting into the inflexible Tiered Standard Plan, inviting immediate and severe financial hardship.